Over-indebtedness & responsible lending in the UK ... · Over-indebtedness & responsible lending in...

45

© 2005, Experian-Scorex Proprietary and Confidential #1 Over-indebtedness & responsible lending in the UK Dr Paul Russell Director - Analytical Solutions www.experian-scorex.com [email protected]

Transcript of Over-indebtedness & responsible lending in the UK ... · Over-indebtedness & responsible lending in...

© 2005, Experian-Scorex Proprietary and Confidential #1

Over-indebtedness & responsible lending in the UK

Dr Paul RussellDirector - Analytical Solutions

www.experian-scorex.com [email protected]

© 2005, Experian-Scorex Proprietary and Confidential #2

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #3

Recent cases

© 2005, Experian-Scorex Proprietary and Confidential #4

October 2004

• £100k debts reported

• 16 credit cards

• 20 credit lines

• Nearly every account at max utilisation

• Weekly income £340

• No serious arrears

© 2005, Experian-Scorex Proprietary and Confidential #5

• 800 out of 60,000 had debts > £100,000

• 2,500 owed 66x monthly income

• 200 had > 15 credit cards

• One had 48!

CCCS report February 2005

CCCS – Consumer Credit Counselling Service

© 2005, Experian-Scorex Proprietary and Confidential #6

This House……is horrified to find that existing credit checking is not working;

...believes that there has to be full information sharing between all financial institutions, clear credit to income ratios set for maximum credit limits, agreed triggers for industry-funded independent debt counselling and that such systems must operate across all lenders;

...calls on a self-regulated system to be agreed before the House rises in the summer and to be seen to be working before the next Queen's speech; and resolves that, in the absence of such a system, Parliament must regulate the industry within the next year.

Early Day Motion 934 (30 March 2004))

Westminster concerns

© 2005, Experian-Scorex Proprietary and Confidential #7

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #8

UK indebtedness

• Personal debt now exceeds £1Tr

• Consumer credit is low relative to annual incomes

• Personal debt is dominated by secured lending

Source: Bank of England, Experian Business Strategies

© 2005, Experian-Scorex Proprietary and Confidential #9

0.00%

1.4% 1.5%

2.3%

3.3%

1.5% 1.4%

1.8%

1.3%

2.1%

0.43%

0.26% 0.23%0.10% 0.09% 0.08% 0.07% 0.06% 0.04% 0.03% 0.01% 0.02%

2.7%

1.0%

1.3%1.2%

1.4%

1.8%

2.0%

3.0%

2.2%

1.8%1.8%

1.7%

1.1%

1.5% 1.2%

0.27% 0.29% 0.25% 0.32% 0.29%0.33%

0.38%0.29% 0.34%0.37% 0.29%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

The UK retail credit marketBank of England Write-Off Rates (%)

Over the last 10 years, average write-off levels across the UK have increased on average by 5.3% p.a., with a marked decline in mortgage write-off levels. However, credit card write-off levels have surged over the last 5 years, reaching 3.3% by end 2004.

Source: Bank of England, Experian

Mortgages

Personal Loans

Credit Cards

TotalCAGR= 5.3%

© 2005, Experian-Scorex Proprietary and Confidential #10

18.8%

11.1% 11.4% 11.8%12.8% 12.9% 13.0%

14.1%15.4%

16.5%17.5%

18.3% 18.4%

17.9%

9.4% 9.3% 8.9%7.6% 7.2%

8.6% 8.2% 8.0% 7.9% 7.2% 7.3% 7.5%8.8%

11.6%13.1%

11.0%

27.6% 27.9% 27.7%

18.7%18.6%

20.4% 21.0% 20.9% 20.9% 21.2%22.7%

23.9%

26.3%

28.9%

31.5%29.9%

0%

5%

10%

15%

20%

25%

30%

35%

Mar

-96

Sep-

96

Mar

-97

Sep-

97

Mar

-98

Sep-

98

Mar

-99

Sep-

99

Mar

-00

Sep-

00

Mar

-01

Sep-

01

Mar

-02

Sep-

02

Mar

-03

Sep-

03

Mar

-04

Sep-

04

Mar

-05

Sep-

05

Mar

-06

Sep-

06

Mar

-07

Sep-

07

The UK retail credit marketDebt Servicing Payment* as a Percentage of Income - Total

Households now spend around 25% of their income to service debt (up from 20% 10 years ago), and this is predicted to rise to 28-32% over the next few years.

* Debt servicing payment is the sum of capital and interest payments for mortgages, credit cards and other unsecured lending.Source: Bank of England, Experian Business Strategies

Total

Capital

Interest

Actual Projected

Downside ScenarioOptimistic Scenario

© 2005, Experian-Scorex Proprietary and Confidential #11

0.38%

0.43%

0.29%

0.29%

0.25%

0.32%

0.29%

0.33%

0.34%

0.47%

0.50%

0.54%

0.20%

0.25%

0.30%

0.35%

0.40%

0.45%

0.50%

0.55%

0.60%

15% 17% 19% 21% 23% 25% 27% 29%

19961997199819992000200120022003200420052006 Optimistic2006 DownsideLinear (Trendline)

The UK retail credit marketWrite-Off Rate by Debt Servicing (12 Month Lag)

Write-off levels have traditionally been closely related to debt servicing to income ratios, and further increases in the ratio could see write-off levels reach 0.50% in the next few years (from 0.43% today).

Note: The graphs shows write-off % in a given year and debt servicing ratio in the previous year.Source: Bank of England, Experian

Using the trend line, a prediction of write-off can be estimated for 2005 and for both scenarios in 2006

© 2005, Experian-Scorex Proprietary and Confidential #12

UK indebtedness: survey data

Source : Bank of England and NMG Research. Figures up to 2002 are calculated using the BHPS, 2003 and 2004 figures are from the NMG Research surveys.

• Significant differences between owners and renters

• Renters are more likely to have problems but their share of total debt is small

• The vast majority of debt is attributable to homeowners but veryfew have current problems

• 40% of total household debt is owed by those spending over 25% of gross income servicing debts

• The share of debt owed by those with current debt problems is lower than a decade ago

• Generally, UK credit industry is very healthy

• Isolated cases of irresponsible borrowing exist

• Detection of those cases can be improved

© 2005, Experian-Scorex Proprietary and Confidential #13

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #14

Industry initiatives

• Department for Trade and Industry (DTI) Task Force on Indebtedness

• Financial Services Authority Financial Capability Initiative

• APACS agreement to share all available data

• Industry/DTI/Department for Constitutional Affairs – historical consent

• Steering Committee on Reciprocity working group – new data sources

Student loansUtilities

© 2005, Experian-Scorex Proprietary and Confidential #15

Supporting industry initiatives – The Debt Test

• Simple questions about personal financial circumstances

• Answers ‘scored’ to determine likelihood of indebtedness problems

• Score drives ‘risk messages’:Suggestions on how to improve the situationSources of help – Citizen’s Advice etc

• Supports ‘What-if’ scenarios

• Initial launch on BBC website

© 2005, Experian-Scorex Proprietary and Confidential #16

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #17

Measuring consumer indebtedness

Full data sharing will help

UK credit industry has committed to share full data on most products by 2006

Approximately 40 credit accounts that cannot be shared due to lack of consent

Need to properly quantify individual indebtedness

A more refined view of credit bureau data has led to better understanding of individual commitments

Developed the Consumer Indebtedness Index (CII) as a predictive measure of risk based upon a more detailed view of indebtedness

True affordability requires some knowledge of income

Developed Estimated Disposable Income models to assist in the assessment of individual affordability.

Developed an Affordability Index (AI) as a predictive measure of risk based upon a good understanding of individual affordability

© 2005, Experian-Scorex Proprietary and Confidential #18

Research - existing credit card customers

G:B Odds

• Highly-committed customers

identified via current Delphi block 10.4:1

now identified 2.6:1

• Customers with current payment problems 2.4:1

© 2005, Experian-Scorex Proprietary and Confidential #19

Segmentation

Total Population

No Trace of Address

Valid Address

Very Low Balances

All other balances

Very High Balances

Recent Derogs (Payment problems L3Y)

Uns Balance <= £2,000

Uns Balance > £2,000

Uns Balance <= £2,000

Uns Balance > £2,000

No Recent Derogs & No Derogs

Low Balance

High Balance

Low Balance

High Balance

© 2005, Experian-Scorex Proprietary and Confidential #20

Consumer Indebtedness Index (CII)

• Number of active accounts in use

• Number of revolving accounts in use

• Limit utilisation across revolving accounts

• Type of neighbourhood1.921-30

10.661-70

16.371-80

30.481-90

57.791-100

4.341-50

6.551-60

0.71-10

1.311-20

3.431-40

Bad Rate (%)Index

Key Predictors Strong Prediction

© 2005, Experian-Scorex Proprietary and Confidential #21

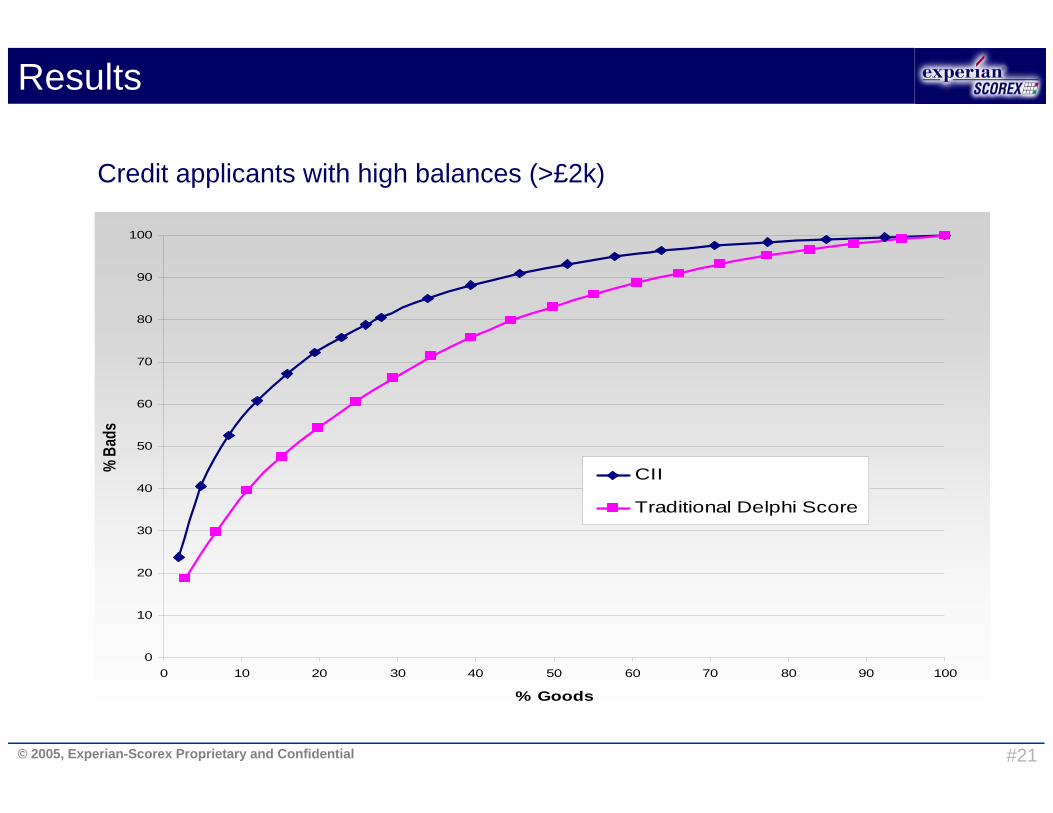

Results

Credit applicants with high balances (>£2k)

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100

% Goods

% Ba

ds

CII

Traditional Delphi Score

© 2005, Experian-Scorex Proprietary and Confidential #22

Consumer Credit Counselling Service (CCCS)

• Consumers approaching CCCS in 1 month analysed (~3,000)

• Credit bureau data (including CII) attached retrospectively at 3 monthly intervals over previous year

• AnalysisCompare CII profile of indebted cases with general populationCould lenders have made better decisions?

© 2005, Experian-Scorex Proprietary and Confidential #23

CII Comparison

SP Cumulative % Population

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0 2 4 6 8 10 13 15 17 19 21 24 27 31 33 38 40 42 46 48 52 56 62 64 68 70 78 86 91 93 95 97 99

CII Value

Perc

enta

ge

CCCS Cumulative % CIB Cumulative %

~26%

~95%

© 2005, Experian-Scorex Proprietary and Confidential #24

Affordability-based methodology

• Standard Good/Bad DefinitionBad - current delinquency 3+

current delinquency = 2 and overlimitIndet - current delinquency = 2

current delinquency = 1 and worst delinq L24> 1overlimit

Good - current delinquency = 0current delinquency = 1 and worst delinq L24 = 1

• Affordability-based Good/Bad DefinitionBad - currently classified as 'bad' or CII at outcome = 50+Indet - currently classified as 'indet' or CII at outcome = 30 - 49Good - all other accounts

© 2005, Experian-Scorex Proprietary and Confidential #25

Affordability-based methodology

• Applicants very highly indebted at outcome (CII 50+)

247

378

659

# Accepts

-62.5%9.7Affordability-based methodology

-42.6%14.8Standard methodology

_25.9Current scorecard

ChangeAccept Rate

© 2005, Experian-Scorex Proprietary and Confidential #26

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #27

Estimated Disposable Income

Estimated Disposable

Income

Net Monthly Income

Monthly Expenditure

MonthlyCredit

Commitments

Taken from application form

Derived from credit bureau data

Models based on application form information

© 2005, Experian-Scorex Proprietary and Confidential #28

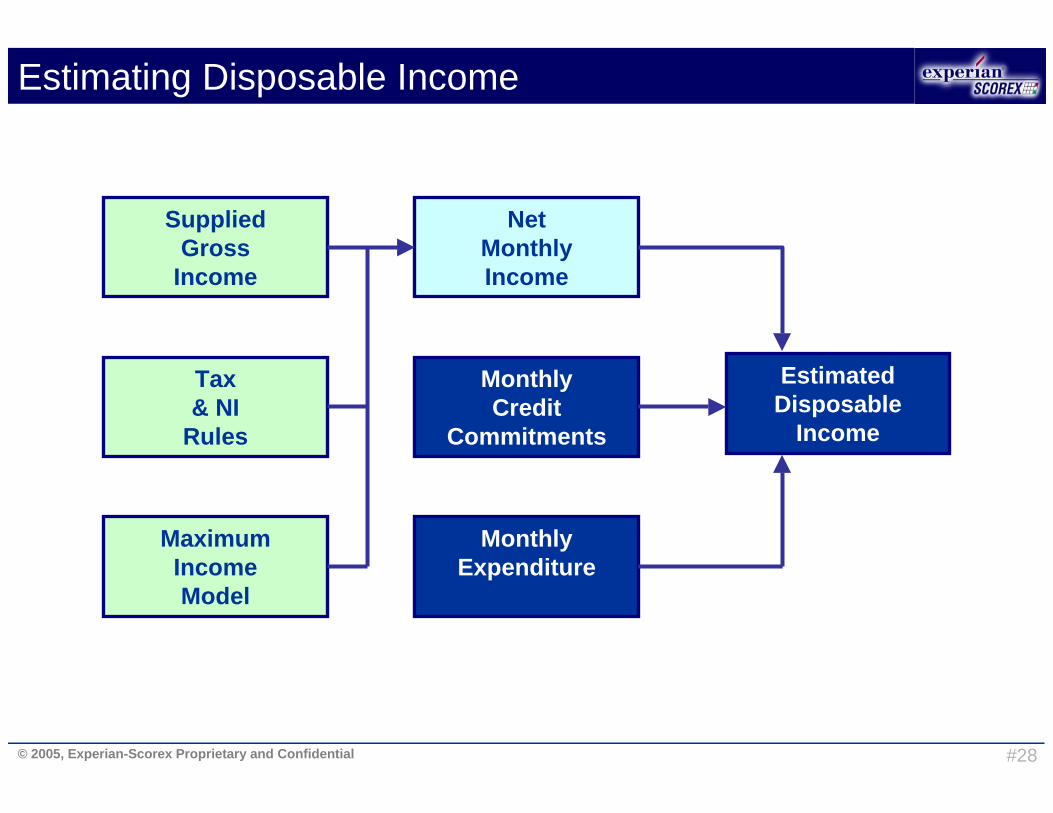

Estimating Disposable Income

Estimated Disposable

Income

Net Monthly Income

Monthly Expenditure

MonthlyCredit

Commitments

Supplied Gross

Income

Tax& NI

Rules

MaximumIncomeModel

© 2005, Experian-Scorex Proprietary and Confidential #29

Estimating Disposable Income

Estimated Disposable

Income

Net Monthly Income

Monthly Expenditure

MonthlyCredit

Commitments

Personal Loan (CAIS) monthly

repayment

Proportion of Credit Card

(CAIS) balance

OtherAccounts

New Account(including

consolidation)

© 2005, Experian-Scorex Proprietary and Confidential #30

Estimating Disposable Income

Estimated Disposable

Income

Net Monthly Income

Monthly Expenditure

MonthlyCredit

Commitments

Mortgage CAISor estimated

Mortgage/Rent

Estimated essential

expenditure

© 2005, Experian-Scorex Proprietary and Confidential #31

Expenditure Survey Data

• Random sample of 12,096 Households with responses from 6,809 Households

• Response rate of 62%• Weekly expenditure amounts• Diary entries for 2 weeks

AdultsChildren

• Household and personal level values converted into totals for "Financial Units"

© 2005, Experian-Scorex Proprietary and Confidential #32

Expenditure Models

Models

Financial Units

Sub-pops

Mortgage

Rent

Expenditure

Grown-up

Children

-

Owners Pensioners

Renters

Owners Singles

Renters

Owners Working Families

Renters

Owners Low Income

Households Renters

Key PredictorsAgeIncomeUK regionCouncil Tax bandTime at address# ChildrenSingle parent

© 2005, Experian-Scorex Proprietary and Confidential #33

Affordability Index

• Builds on CII using income and other personal data

• AI is score-based using:• Estimated disposable income

• Consumer Indebtedness Index

• Residential/Marital Status

• Net Monthly Income (NMI)

• Monthly Credit Commitments as a % NMI

• Monthly Mortgage Payment as a % NMI

• Applicant’s Age

• AI is tuned to ‘potential accepts’ – not the through-the-door population

1

100

0 Unclassified

Very Low Affordability

Very High Affordability

.

.

.

.

.

.

© 2005, Experian-Scorex Proprietary and Confidential #34

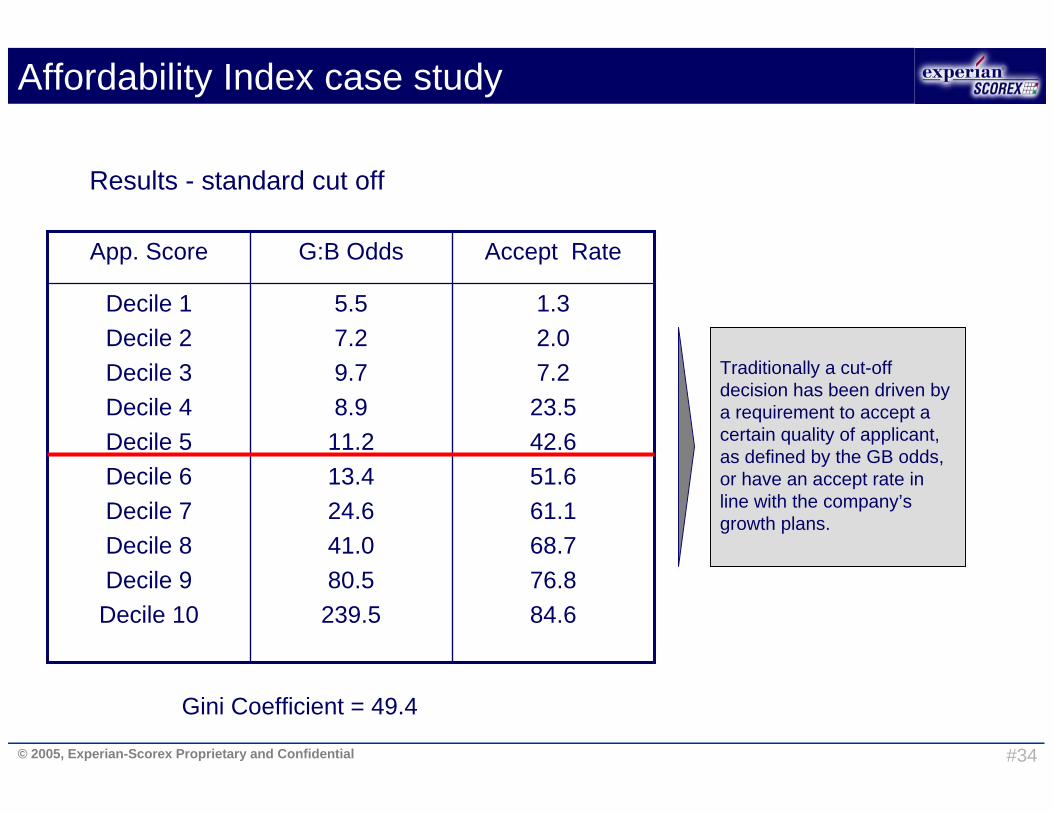

Results - standard cut off

1.32.07.223.542.651.661.168.776.884.6

5.57.29.78.911.213.424.641.080.5

239.5

Decile 1Decile 2Decile 3Decile 4Decile 5Decile 6Decile 7Decile 8Decile 9

Decile 10

Accept RateG:B OddsApp. Score

Gini Coefficient = 49.4

Affordability Index case study

Traditionally a cut-off decision has been driven by a requirement to accept a certain quality of applicant, as defined by the GB odds, or have an accept rate in line with the company’s growth plans.

© 2005, Experian-Scorex Proprietary and Confidential #35

Results - Affordability Index

10.024.633.555.579.9

5.510.718.540.4112.1

Lo – 6869 – 7677 – 8990 – 94

95+

Accept RateG:B OddsAI

Gini Coefficient = 46.7

Affordability Index case study

The Affordability Index is a highly predictive characteristic in its own right.

© 2005, Experian-Scorex Proprietary and Confidential #36

Results – G:B Odds misalignment

AIApp. Score

26.1112.140.418.510.75.5Total

5.57.29.78.9

11.213.424.641.080.5239.

5

-4.4-

30.726.590.883.368.4

138.5252.2

1.55.86.6

21.119.921.332.954.499.4617.4

6.910.79.08.1

11.611.823.541.148.093.1

8.04.59.97.28.48.8

12.415.924.4

-

3.24.49.94.94.35.55.08.0--

Decile 1Decile 2Decile 3Decile 4Decile 5Decile 6Decile 7Decile 8Decile 9

Decile 10

Total95+90 – 9477 – 8969 – 76Lo – 68

Affordability Index case study

Using the Affordability Index, it can be shown that at the given cut-off there are large differences in the quality of the population.

© 2005, Experian-Scorex Proprietary and Confidential #37

Affordability Index case study

Results - potential improvements

Through the use of the Affordability Index, we can significantly reduce the bad rate or increase the accept rate.

3.0

3.2

3.4

3.6

3.8

4.0

40 42 44 46 48 50

Accept rate

Bad

Rat

e

CurrentSame Bad rate -

Improved accept rate by 7%

Same Accept rate -reduced bad rate by 11%

© 2005, Experian-Scorex Proprietary and Confidential #38

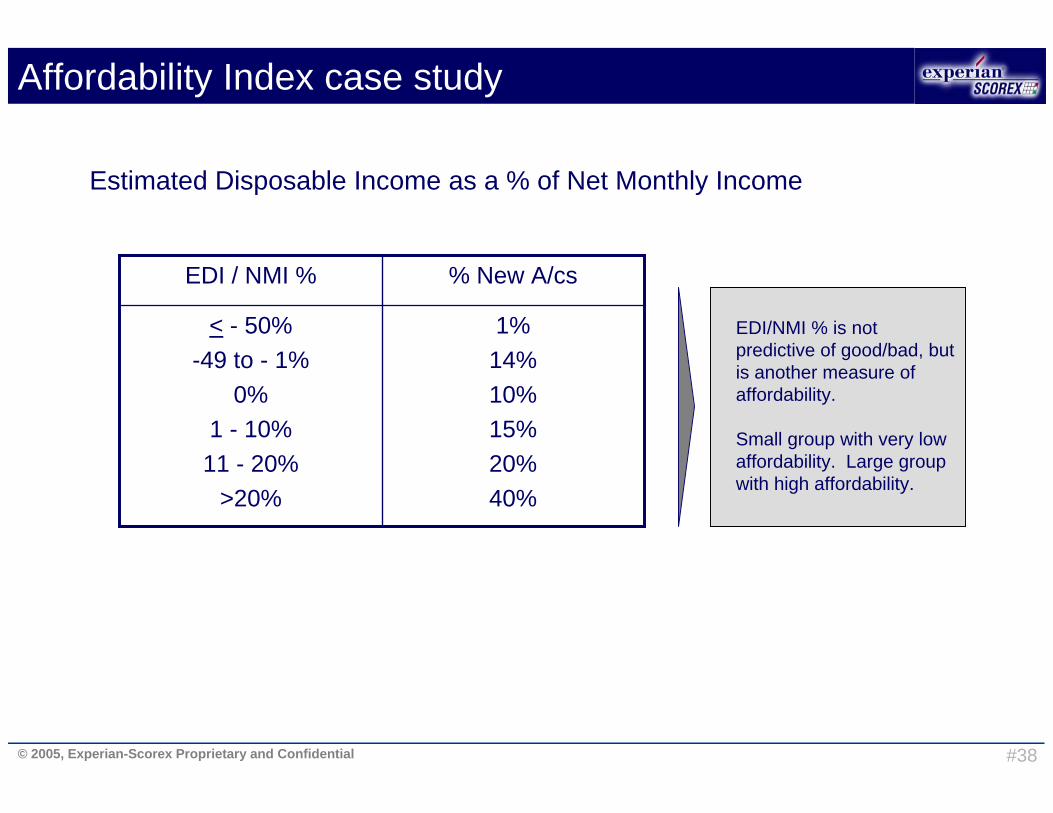

Estimated Disposable Income as a % of Net Monthly Income

1%14%10%15%20%40%

< - 50%-49 to - 1%

0%1 - 10%11 - 20%

>20%

% New A/csEDI / NMI %

Affordability Index case study

EDI/NMI % is not predictive of good/bad, but is another measure of affordability.

Small group with very low affordability. Large group with high affordability.

© 2005, Experian-Scorex Proprietary and Confidential #39

New credit application process

Delphi for New BusinessModule

CVM ModuleRisk Models

Application Input

Decline - Risk

Potential Accepts

Credit Decision

© 2005, Experian-Scorex Proprietary and Confidential #40

New credit application process

Delphi for New BusinessModule

DetectModule

CVM ModuleRisk Models

Application Input

Decline - Risk

Decline - Fraud

Potential Accepts

Accepts

FraudDecision

© 2005, Experian-Scorex Proprietary and Confidential #41

Delphi for New BusinessModule

CVM ModuleReward Models

DetectModule

CVM ModuleRisk Models

Application Input

Take most appropriate up-sell/ cross sell action

Decline - Risk

Decline - Fraud

Potential Accepts

Accepts

Up-Sell / Cross-SellDecision

New credit application process

© 2005, Experian-Scorex Proprietary and Confidential #42

Using the AI with the credit risk score

High Credit Score

(Low Risk)

Low Credit Score

(High Risk)

Risk Score Cut-Off

SCORE ACCEPTS

SCORE REJECTS

AFFORDABILITY INDEX

Previous Accepts now declined for low

affordability

Previous Refers with high AI's can be auto accepted

CREDIT SCORE

© 2005, Experian-Scorex Proprietary and Confidential #43

Agenda

• The headlines

• UK credit market and indebtedness

• Industry initiatives

• Measuring consumer indebtedness

• Affordability and customer value management

• Conclusions

© 2005, Experian-Scorex Proprietary and Confidential #44

Conclusions

• Sharper focus on indebtedness

• Increased pressure to demonstrate responsible lending

• Credit bureau data provides a more complete picture

• More than just data sharing

• Analytics will be vital in making sense of the data

© 2005, Experian-Scorex Proprietary and Confidential #45

Over-indebtedness & responsible lending in the UK

Dr Paul RussellDirector - Analytical Solutions

www.experian-scorex.com [email protected]