Outlook_Money_Augest_2011

76

Transcript of Outlook_Money_Augest_2011

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 1/76

SHOU'LD ¥OU DIG FOIR MINING ST'OCKS? 9

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 2/76

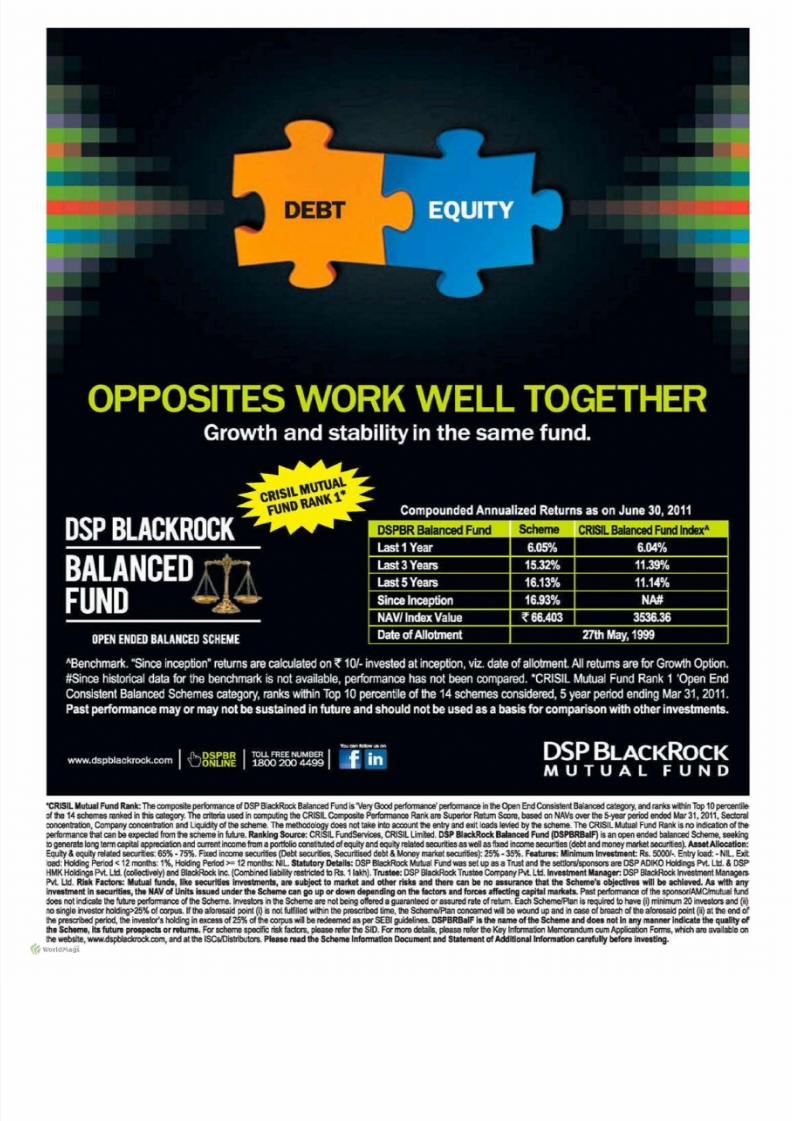

D E B T

'C R lS IL M u lu a l F u nc llW l k : Th e c o m p o S i 1 B p e d a m a l l c e ! o f l D S P B l a c k R o c k B a la n c e d fu n d i i s ' V e r y G o o d p e r f o r m a n o e ' p e t f o r m a n o e i n ! h e, O p e n E n d C l ll ls is le n t E J a 1 a n o e d c a t e g o r y , M d r a n k s w i t h i n T o p 1 0 ' p e r c e n l i l e

o f ! h e l 1 4 ~ r . m ~ e d in t h i s c a le g ll lY , T h e C I i 1 e r i I , u se d in C O O l p u l l n g ! l l e C R _ lS fL C om p os i!e P e do nn an oe R a nk a re S I l p e r i o r l R e n s I l l S c o r e , b a s e d O ~ N A V s M r lila 5 - y e a l i p e r o o e r ! C I e d M a r 3 1 , r o u , S e d : o r a I

0 0 f 1 C 8 I I 1 r a t i o n , C o m p a n y C I l I 1 O e o ' 1 t a l l o a n d U q ) l ld iI y o f I t !e , s C h e m e , T he m e t l' lc ld o !o g y d oe s n o l t ak e 1 1 1 0a c c o u n t , Ih e e n t r y a n d sJt l o a d s I e I I i e d by'ihe s c h e m e . ihel o ru s l L M u tu a l f ;W 1 d R a n k is n o i lH l ic a ti o n o ll ll e ,

p e I 'f tI /I Il a tl c e lt la t c a n I le ~ f r om 1 he s m em e in fu I! l r e. R a nk in g Sau t e e : C R IS IL F U l1 d Se IV iC e S , C R iS IL L im l ! e d . O S , B l a c l ! R o c k B a I a t I c e d I fu n e ! ( D S P E lR B a IF ) i s a i l l C p e i l , e n d e d l b a l a n C e d S c h e m e , s e e k i n g

1 0 g e r e r a l a Iorgtem c a p i t a l ~ p l 1 ! C i a l i !l l 'l l in d Q l r r e n t i n I: :o m e , f r om a p o r tk ll io c o n s li lu l ed o f e q u it y a n d l e q u it y r e l a t e d s e O J r it ie s a s w e l l a s f i x e d I nc c m e s e cu r i1 ie s . (d e bI a n d m o n e y nwke I s e c u m e s ) . ,but A l l o c a t i o n :

E q u it y ,& e q u il ¥ r e l a t e d s ec u rr ne s ,: 6 5 % - 75 % . , f i x e d i no o m e s e c ur it ie s , ( D e b l5 e C lJ li 1J e s1 S e c u r i ! i s e d d e b ! & I M O n e y m a r k e t s ec u r ff i e s) : 2 5 % - 3 5 % . F aa tu ra s. Mlnlmwn I rms tmlnt : R s . 5 0 0 0 1 - . Enlryload: - N I L , . E x i t

b a d : J -t ld i n s P e r I o d < 1 2 m a n l N : I ~ H o I c l l n g I P e l i o d > = c 1 2 m o o l h s : N I L S l J t u t o , r y D t t I I I $ : I l S P I B I ; , l r ; k R Q C k M u tu a l F u n d ' I Q S s e t u p , S S < l T r u S t a n d t .e ~ ~ a r e D S f l l I D l K O H o l d i n g s I'vllll:l, ,& D S P

H M K H o ld i 9 1 M L ld l ( 1 X I I l e c E v e I y ) a n d B la c k R od t I l t C . ( C c r r b i n e d r ~ I 8 S I r ic Ie <I I DR s .

llakh). lNaIee: D S P Blac i lRodt l i ru s te e C o m p a n y P-. l U ti . t n ve st m t n ll l h na g . . : D S P B l a c k R o c k t nW s t m e n t M a n I9 l£ S ,

M L Id , R _ la kF IC '! o rs : IMu lua l fund I , O k e ACU11 t I . . I l rrmtmenl l , all l ub j o c t to m a rk e t a _ nd lo t h e r lila a nd d IG it " " b e 110' IAlI I ' I I ICI tN t tile ~ um t 1 1 o b je c1 lm w il l 1 10ad l lmd.A i w i t h a n yI n 'IH tm tn ti !n u cu ri tl n , d ie IMAVof Un it s l uued l undarth.11 SoOI,.1I I Ian go up or down d e pe n dI ng o n lflii f lc lO II Iln d fD l'C lll fil df lll l , ap lt ll rnad! i t l . Past p e r f o I m a n c s o f th e sponsor lAMC/mutuaJ l u n d

d o e s n o l M c a l i ll l le l u l l w p e t I ' o r l l l l l l ' l O O o I th e S I : Il e I o o , L n v e s I D r s l iM h e S d 1 e m e a re n O l i b e i n g dered a J u a r a n l e e l l o r ,a s s u re d r a te o f lr ll ll lm . E a c h S c I l e m e I 1 ' 1 a n is req_1o ha W (i ) I " n in u n 2 0 i n v e st o rs an d 0 0n o s i n s l e , m e s l l l r h o lc I in g > 2 s % c fo : rp u s . t f l l 1 e a f O r es a id p o in ' e il is n o t f u l f d ~ 1 v i i 1 h i n ! h e p r e s c r i b e d l t i m e , th e S c I l e m e J P l a n c c n c e m e d w i! be w o u n d u p a n d l in c a se o fl b re a d : 1lo 1 lh e a fo le s a id p o i n t Q Q a 1 ! h e en d o f!h e p t e S a i J J e d p e O O d , l h e i lM S l l lr ' h O I d l n g in e x c e s s o f : 2 5 % 0 I 1 ! 1 8 c o r p u s w i! be l ! \ !deemed a s p E l f S E B I I P o Ik ! e li n e & I IS P B R B a I I' l i t h e IIIm8 o U I l e S d 1 am & a n d d D H n o t I n I iny m a n n e r t l l d i c a f a Ifill q u l l l t y ,o f

thlSCl' IImf,1ts Mu.. p ! ' O i I I p e c I I oll1iluml. F a ' s c h e m e s , ll !I C ff ic lr is k fa d o rs , I p le a s e r e fe r ! h e ' S I D . F a ' I Il O I8 d e l a i l s , l p l e i s a re(e( II'e K e y i 1 f o r m a : l i O O M e m o n In du m c um A p p l i c a t i o n F O I I l l S . wtich a r e a v a : l l I b : e o n

Ih e w e b s i t e , W M ' I .d s p t la d u ' o c l lo o r n , an d a t 1 1 1 8 S C s It l i s lr i b u tl n . P lu M r u d th " S c h e m a l r n fo m la tl o n D o cu m e n t a n d S tm m e n t o f A d d lt l o n a l i n f o m ll l l o n c m f u ll y I b I f D n t I hm t lng ,< ~worldl'\ag~

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 3/76

11 '0AUGUST 2,011V OLUM E 1 0

ISSUE 1 1 6

COVERSTORYSOUMIK~AR

RU UPWARDLY MOBILE?

18From a mere style statement to an utter neoessity,the mobile phone has come a long way. Now, you

can u se your cell phone to not only make utility billpayments or transfer funds, but also to trade in thestockmarket, buy mutual funds, and so on. But like

everything else involving technology, there are in-herent pitfalls and fraud risks..In this cover story, welook at what you can do with your mobile. Plus,the

precautions you need to take to ensure thatsomeone doesn't pull a fast one on you. And, ofcourse, you can continue making those calls and

sendinq texts as you always have.

eHU~INDER SINGH

IN:SURANCE

INTERVIEW:JAYANTDUA

34With Ulips losing

steam, questionsare being raised

a bo u t th e ir f ea sib il ity.

J ava rrt D ua , C E O,

B ir la Su n L ife In su ra nc e

Company, dispels

s u c h worries.

Co ve r De sign & Im aging '; M AN O'J lT DA TTA

H EA D O FF :I: CE IIB ·1 0, S J. E n cla ~e . N ew D elh i 1 10 0 29 ; T el: (0 11 ) 4 68 67 20 0. 2 61 00 72 2; F ax : ( 01 1 ) 26 19 1'1 20 O TH ER O F: FIC ES B an ga lo re : (0 80 )2 55 82 80 ~

F ax : (0 80 ) 2 55 32 81 0; K oik ats : (0 33 ) '1 .0 03 50 12 . F ax: ( 03 3)2 28 23 59 3; C he nn ai: ( 04 4) 28582251/52, F a x: 2 85 82 25 0; H yc le ra b ad : ( 04 0) 2 33 71 1 44 , F a x: (OdO) 23375676 ;

M u mb al: ( 02 2) 6 7.3 82 22 2. F ax :: (0 22 ) 6 73 82 23 3. P rin te d a nd p ub lis he d b y V in ay ak A gg arw al o n b eh alf o f O utlo ok P ub lis hin g [In dia ) Pvt L td . E d it or : U cl ay a n R a y.

P I'in te ei a t rn fo me dia 1 8 L td , !'J ot N o.3 , Se cto r 7 , Off S ia n P an ve l R oa d, N eru l N avi M um ba i-4 007 0B . a nd p ub lis he d fro m A B-1 0 Sa fe la ~u ng E nc la ve , N ew De lh i 1 1002 9

For Subscnp ti on queri es , p lease 9 li i3JI : YOllrbelplloe@QlltIQpkmoney(pm

Pub l i shed to r th e fo rtn ig ht o f J u l l ' 2 7-A ug us t 1 0.2 01 1. O utlo ok M on ey d oe s n ot a cc ep t re sp on sib ility lo r a ny in ve stm en t d ec is io n ta ke n by re ad ers on th e b as is o f

in fo rm atio n p ro vid ed h ere in . Th e o bje ctive is to k ee p re ad ers b ette r in fo rm ed a nd h elp th em d ec id e fo r fh em se lve s,

< ~worldl'\ag~ wwwoutlookmonevccm • 1:01AUGUST 2011 • OUTLOO:K MO:NEY t

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 4/76

C o n t e n t s

A. P IM BHAKAR RAO

JOBS &CAREERS

24 THE RIGHTSHOT

In the t irs t of the quarterly surveys

by H R consultancy rna Iol randstad,

shared e x c lu s iv e ly w i t h Ou tl oo k Mon e y.

we present a view of the compensation

trends in the pharmaceutical industry.

'ENTERPRISE

28 GETTING STARTED

The second instalment in our series

with tax, auditing and oonsultancy

f in n D e l o it te on self-employment. looks

at the approvals for starting a firm.

30 GREENTECHNOLOGY

Wi t h the wo r l d grappling with g l oba l

warming. a technology that does good,

pg 440LM50

On the back of the yellow metal's

strongestraUy in 32 years, gold funds

register good returns despite a strug-gllng Nifty and Senscx, Fund 'Watch:

Birla Sun Life Monthly Income ..

while earning profits, is a smart option.

IINIVESTING

38MININ BLUES

Mining companies are facing the heat

as a group o f ministers r e c o mm e n d s

that they share their profits with thedisplaced local population.

4' AVANT GARDEThe slowing of the world economy

means that Indian consumers wil l

continue to attract euro, dollars and

yen, says Mohit Satyanand.

42 DOESSIZE MATTER?

r e s common perception that more

a sse ts a fu nd m a n age s, th e h igh er

returns it gives ..But is it always true?

REAL ESTATE

o LESSONS FRO OIDA

Thousands of people are .in the danger

of losing their lifetime savings f o l l ow -

ing the land dispute in Greater l -orda

The lessons to [earn from the episode.

PLANNIING&4 GLOBAL I DIANA look at the major routes by which

NRls can invest in Indian enterprises

and the related restrictions,

WEALTH A AGE ENT

vl/hy you need. to change your ap-

proach to wealth management over

time t o . make your money grow.

8PORTFOLIO MAKEOVER

In the second Instalment of our new

series, we give a makeover to the

mutual fund, stock and insurance

portfolio. o f Pnne-based sales profes-

sional Sandeep Rawal,

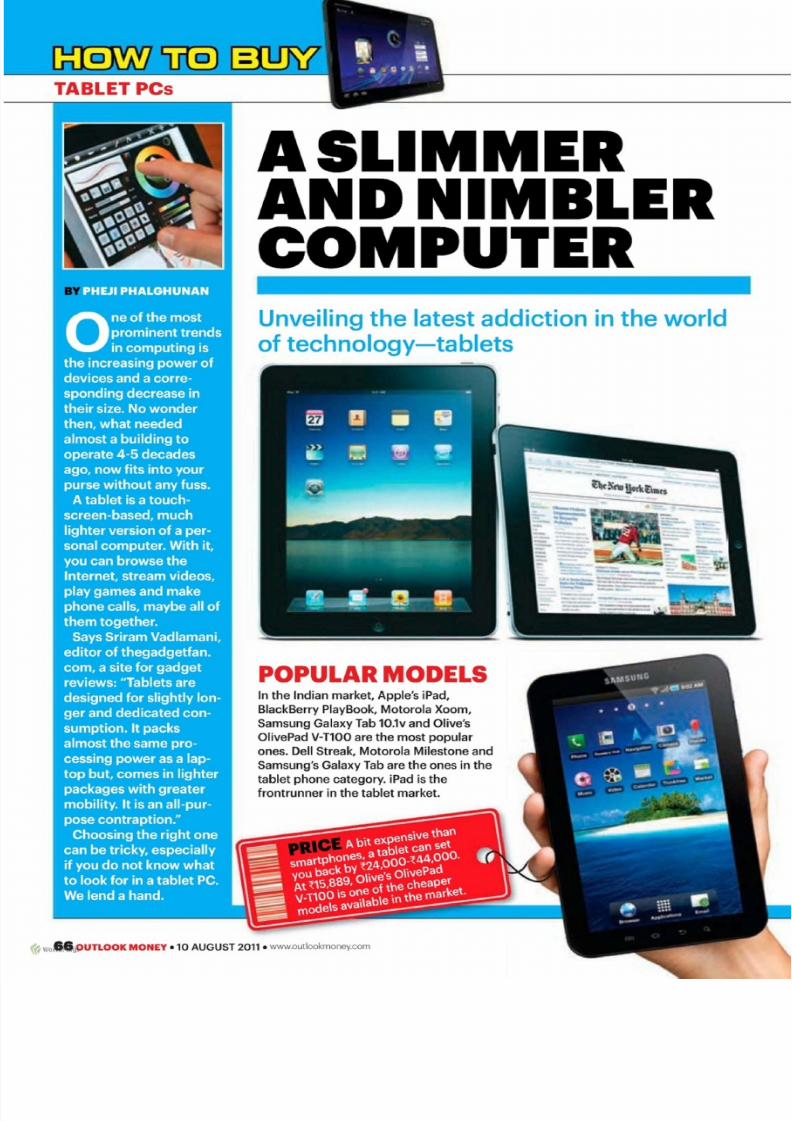

HOW TO BUY A TABLET

Tablets are the latest addtctton m the

w o rld o f technology. The what, w h y

and how of this new sensation.

13Macro Money:

Global uncertainty

18Queries.

33The Decoder: Future

Generali's Birna Advantage

40 Stock Pi:ck: Bosch

48 F&O: Gold futures

47 Fixed Income:

FDvs

M IS

48 Alert Investor:

Third-party insurance

IREGIULARS

Editor's Note

• Letters

• Newsroll.: Cashless

claim impasse over; Al-

ternate banking! channels

gain prominence; EPFO's

new fund manag:ers; Com-

modity Watch; Street Talk

"".... _,.....Ul'LOOK MONEY. 1.0 AUGUST 2011 • wwwoutlookrnonevcorn,~" womMirgs

2 My Plan: Ujjwal Gaurav

60 Interiors: Baby's room82TailLight: Renault's

newSUV

84 Leisure 360:

Michael Lewis' The Big

Short: A True Story

&8 For What It's Worth

.8 Fortniight Figures

72 Sunny's MOllley:

Mobile Migraine

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 5/76

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 6/76

INDIA'S NO 1PERSONAL FINANCE MAGA.ZINE O'N THE WEB

CHECKOUT

- - - -~.- - -----.. .- - . .

Subscribe toOutlook Money's

weekly

newsletter at

to stay updated

about the latest con-tents of forthcomingissues of Outlook

Money and Outlook

Money Digital, andsubscription offers

Lb~: : :~===: : : : : :~==d=-~~~=Jnd other hot deals.

INIDIA!'SI F I IRSTPERSO'NAL

FINANCEeWEEKLY

LATEST ISSUE 22 JULY 2011To stay on top of your finances visit

http://digital.outlookmoney.,eom and clickon 'subscrlbe' for a free subscription

LASIWEEKON 10 IGITA IL

Gold for All Seasons A ne w s tu d y m ad e p u b lic la s t w e e k

s ugge sts g re ate r a llo c atio n to go ld in a ll in fla tio n s ce na rio s

Boost Y ou r C :r ed it Score You r c re d it s co re w ill d ete rm in e

fu tu re b orrow in g s . He nc e fo rth , p ro te ct y ou r s co re

.AIMixed Bag for I T ' Giants In fo s ys c on tin u e s to s tru gg Ie ;

les d ec lin es too , b ut s till l p os ts a bove -a ve ra ge ga in s

Go for Your Worth Sa la ry n ego tia tio n is on e o f th e tr ic kie st

m om en ts in a n in te rvie w . Know h ow to s c o re th e re

Useand Forget V irtu a l c a rd s can h elp y ou m ake s e cu re d

online p aym en ts ..R ea d to know h ow

< ~wo~iI'lOOK MONEY.10 AUGUS12Q11 • wwwoutlcokmoneycom

l : E l f a c ebook

What: you saidTushar kulkarni: IIl ike the ne w initia-

tive . Th e ne w fo rm o f p rin t e d it io n is

v e ry r e fr e s h in g .

16J1u l y

Biswajit Saha: This is the best finan-

c ia l m a ga zin e a va ila b le .

16. !July

Biranchi Narayan, Panda: T ha nk s fo rb rin gin g ou t a lo ve ly e - w e e lk ly Outlook

Moneyed i l t i o n

12 Ju l y

Al11it KUl11arBurman: A n ew m ile -

s tone fo r Out look Mone y a nd it g e t's

m o re liq uid ity . C on gra ts !

1 2 J u ly

Winston Daniel: It h as b ee n a f a n -

ta stic jo urn ey fro m Intelligent I nves to r

to OLM-Digi ta. l . A ll om b e s t w is h e s fo r

th e e W e ek ly .

12Ju l y

JloinOutlook Moneyo:nFacebookLog in to F ac eb ook 8 i n d v is it h tt p :/ /

www . o u t l o o kmone y . c om / l F a c e b o o k /

p age . O r. s ea rc h 'O utloo k M o ne y'

in th e s e a rc h b a r. Tra c k u s to ge t a

s ne ak -p ee k in to u pc om in g is su es .

H ··9ave a query.J oin o ur individual g rou p s: c lic k onth e D ISCU SSIO N ta b, s ta rt a N lE W

TOP IC and p os t y ou r qu e ry a t

h t tp : / /www. facebook .com/o lm ind ia

Followu on TwitterLog in to y ou r Tw itte r a c c ou n t, c lic k

o n F IN ID P E OP LE a nd s ea rc h fo r

O utloo lk mon ey to vis it o u r p ro file on

Tw itte r. A lte rn ative ly , y ou c an ty pe

h t t p : / / tw iUe r . com/Ou t l oo kMoney in

y o u r b r ows e r ' s a d d r e s s ba r . Fo l low

u s to ge t d ailly n e ws u p da te s, lin ks toa rtic le s on ou r w eb site a n d u p da te s

o n o ur e ve nts a nd a ctiv itie s .

~ ht tp : / / twi t ter .com/Out lookMoney; h t t p : / /www: fa cebook . com/o lm ind ia

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 7/76

An investment yourwife will approve of!

S u n d a r amYou h ave ,always be lie ve d in th e po te n tia l o f e qlil ily in ve stm en ts.

B ufyo u h o ven lt be e n ab le to 'c o n vin c e yo u r w ife , w Il ,o a lw ays fa it f l la t

go l 'd w as ,a b e f le r in ve stm en t. , N ow yo u f la ve a n o ptio n th at wi l l ' k e ep

y o u b o tl-! h a pp yl

E qu ity P lu s *S u nd O liO m E qu ity P ,lu s. The f un d in ve st s p rim C l l1 il yin equity cm d up to

35% in d om estic Go ld ET Fs (a .m an ge '[m ded Fu n d s) , Im ak in g it a n

ir re sist ib le e qu it y f u nd w i tl li'l l g a 'l !d e n sh e e n I

Iinvestiing in E,quily and Gold ElFsA ll OplJlI-ell(J BqW!y 1 lCh6mtJ

• 'Plus- used In the s c!h em e n am e ' I. only Interms,ofDset allocation and riot In lenni ofnrtumlyleld. Su n d a rGm l ii qu i ty P l u s , ihe e qlJ ity p lu s g old fu n d

w hich e n su r e s th a t yo u r w ife

a n d yo u a re in l perfect

h an no nyl C alil lyo ur

in ve stm ;en t ad viso r o r d ia l

1800-4.25-11000" n o w .

S T A R T O N E T O D A Y ' !

'C a ll To l l F re e : 1 800~425 ·1 000S M S : S F U N D t o 5 6 7 6 7 A J I S e r v i 'c e P r o vid e rs , 0 4 4 - :2 8 5 7 8 7 0 0

E m a J l : s e n i ic e @ s u n d a r a m m u l u a ll .c o m w w w . s u n d a r a m m u t u a l. cc Q m

Scheme i n fl lrma li oo dOOJme l1 1(S ID ) an d apPIicati l ln f o rm s , ar e a v a il ab le a ll ho o ff ic e s, o fSundBr am .A s se tM an ag emoo~ ; it s d is ll ib u lo rs a n d a l.WI 'iW. sun da rammur ua l. 'a lm . F 'u n d I fa d l: N .I IM ' : Sund a ram .: Equ it yI Pi usf P l u , ' used In,Ule l ICheme , name l . o n l , l n Ief!M ofauet l l iocat lon an d nDtln ' termtofretumtx~ldl ; Typ e : A ll o p en -e n d 8q) Ji t' lS dl ame ; t ll l' 8S tme tl tO l! J S'C6 I! e :T os e ak c: a ,p it al r ac ia '~ o n ~ in ve s ti ng in GClI!ian d e q U i l y o f l l l a t e d I ns tr yme nt s f ts l! !d I n India B l1 d I n gqk l- ETF . A s s ai AlIOCI I ion: IEq)l i tyand l ! O : I u i I v r e 1 il 1Sd_ l os l rume l1 t s : ~5% - BS'l Io .Ga ld l _E if ( D p 1 ] S S ' t K : Miari tet): 1 5% - 35%. IlnCllllleand !M oney markei n s l l 1 J m e n t s , O%·2()%.D e d V 9 I i Y & E x o o s ! m l : 0%-50%. a v e , ! Sea ,S . S ec u ri ti , _ . "a s I n v e s t m e n , t s : ( 1%,35%. T 8 I ' I I I $ o f Offe r . N A V . 0 - l ions; G l ' O W t I l, D M d e i 1 d (P 'ul & R e , l lI lI eS tm e n l) . _ m lJImtment ~ , O O O a n dmulUp lesof~1 lhe reaf te r lrncaseofF f r s tl l' lV8Slmen lan tHoradd it lonSlpurchaseo l~an l j mul ti p le so l~1 Ihe lV l lf te r . SIP Iso~ ona mont ll lyand l I u a m r b a s i s . i he m ' Iml Jl Tlm oon tI s~ fo r MOIl th lyO",t Ionanf 750 f or Qua rt er lY Opl lon. Avai lable i llVe s lmen l d a t e s for m o n t h l y an d quarterly'ODIion fo r S IP a re 1 .,7, 1 4,2 0 a nd 25 , I f a n I nv es !m e lr t d ay u nd er S IP Is n ot a b u sime s s d a ~ . t h e i nv es lme nl w il l be~ oolhe n e x

b u si ne s s d a y. &ItLoad: I % i fr ed ee m ad w ith in 1 . 2 m o n t l !s f inm da te, o f, a ll oimeni . NAV pub li c a6oni s ai e ir e d empOOn w i ll b e8 li a il abj 'e onbus i nO I ls d ays . S C hI m e-S pe cI lk R lI 'k FlcIora: TI le p ri co o f g o ld is I n f t ' u e n c e d byseve ra l g , 1o I ia1an d l oc a l v ar ta b Ie s ~Th l! SS ll nd u d e 9 o b a l d em a nd s up p~ ! r e n d s , p u rc h as e sl sa le s by c o nl ra l b a n k s , d~ In bltnglng n e w m i n e s " on l in e mac ro -e i: « lom lc v ar i~OI l. g II 01 lO ll tl ca l f aC t o r s, s e a s o n aD t y J nd e m a n d; c I1 a r, -a s h 'l , d U W a M 1 a r t I I s , c u r r e n c y an d nqu l~.1 i h e s e v a ria b le s m a y h avt! a n Im ~ Oil lI1 e p lic es o f \ W i d an d lX l~u enUy 0II1 11 eN AV o f ih e S c h e m e , 10 Ih e e xI eI ll in ve st me nti s m a de ill gok l : - Ei l iF . E.TI r1 v e s fm e n t s ~ b e s ub ' e d . 1 : o r i s'ksof'1he under l yimg S c h e i ' n e i n c l u d i n g tracki I1g e l l O r ; Tile , e q U i t y ~o60 will be ,sub jed III marke risk price risk and 1 1 O I l . . c l i v e r s i f i c a t i o n , to , name a t a w . Ch~ in G overnment poncy in981*81 a n d c h a n g e s inbl l b e n e f i t s a p p l i c a b l e t o mUtua l f und s ~y i mJ l3 d t ho l f e t umsI I I rnves tOrS.Derivative exposut8R is1cM od alis~rmarke l f iqu l d i t yis 'kand b a s i s r iS~ .~B S S e c u r i t i e s InWls tmf lnt R i s k : C o u I 1 t r yrisk, cur re l )CY r i s k " ; , geo.poIiIk;al r isk , ~ega Ir e s1r i tt io n s and ~a l iiO li l c h a . . . ' - . raphy otl1er 1 f I a n Ind ia . GentraJ Ri l l! Fae t o !l : A u mutua l l unl s a_nd IS ICU .r lt fe s , Inveslln8l\ l1 aI I8 8Ub~ to ma.r l !e l r isks, an dt he rv c an IM i 11 0l J u a r an1 e9hat t l l e fu nd'II ob l9c t lvu w i l l D e ac h ~ . _ iii.S ch em e m ay go up o r d o w n depe ll d lng I ll !On H I. ,f ac: tO l' l, and f or c as i I f rec t Inglhesecur i1 lasm alke l lP l eaq I91d I t I I ,SIDII efo re illlYe stln ll~ P as tP llrfo rm an ce o fllle M u fiia J F un dll'n ve stm en l M a p on sc rd oe s n o t i nd ic a lB tI iI e fU lum p e rf urman c e o ll hl s S c hema . U nl !h o ld e ls in th e Sd leme a re n ot b e in g o ff il re d a n y Qua ra n il le d /a s su re dre turns . Su. IKI IJ 'I1 ! I IEI IUJ ty PlUS Is only th e nama $I f I t h e Sci1eme,md d o e S notJlI I l I lX mann er I nd rc at e e lt !ie ~ the l I u a l l t J ! a rth a Sc he ma ItIf ll li lm p i :OSp e c II 'o r r e tu r ns . JlI:aIutDry Dalal ls: M u tu ali F u nd :SUIIiAOmMtdFlmd ( T r u st l s p o nu r . S I Il ' I c Ia r am f inancelLlC!I. (lLia!l~i ty i limited 1 I I ~ l l l a k 1 i ) . I ' l I V t S t m . n t M I M g e c S i l n d a r a m A S s e l Ma~eme ntCOmpan yU d. T l' UJ lt II : s u nd a ramTr us te eCo rn p a! \~ 1 L1 lL

IFidelJis-SM-432B

SUND'ARAM'MUTUAL

UNEARTHING OPPORTUNITU:S

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 8/76

I Editor's NOlte I

(Udayan Ray)e d i t o r@ou t l o o kmon ey ; c om

h IIp:l/lwil t er ,c om /u d ay a n r ay

TrueMobile-ity

M y e ar lie st m em o ry a bo ut m o bile ph on e s is a c a r to on th at a ppe a re d in a

I ,e a d in g A m e r ic a n m aga zin e . I t sh o w ed a m an in a n o ve r c o a t a n d a h a t u sin g a

m o bile ph on e in th e m id dle o f m a ny o th er s im ila rly-a tt ir e d m e n, u sin g th eir

ph on es. T h e m a n sa ys, "G oo d thing th a t th is c am e a lo n g . o w Ia n w alk f o r

b lo ck s to ge th er w ith ou t a nybo dy th in kin g th at Im m a d, spe ak in g to m yse lf :"

M o b ile p ho n es h ave sin ce e sta blish e d aflrm p la ce in o ur l ive s. But, m o re im p or-

ta n t. th ey a r e c le ar ly se t to m a k e st il l d ee pe r in ro ad s I n to o ur l ive s. I nc lu de d in ,

th e n um e ro us a re as a r e o ur f in an ce s, T o d ay, m a n y pe op le a re d isc ove rin g th e

c on ve nie nc e o f f in an cia l tr a nsa ct io ns o ve r m o bile s. Expe ct t il ls to b e w id e ly pe r-

va sive in th e fu tu re wi t h pe op le m a k in g c ash t ra nsf e rs a nd c ash le ss pa ym e n ts,

b uy i ng and s ellin g f in a nc ia l in ve stm e n ts" u sin g m o b ile s to k e e p th e m s el ve su pd ate d o n f in an cia l in fo rm a tio n , th e sta tu s of th e ir in ve stm e n ts a nd o th er mat-

te rs. A n im p o rta nt c ata lyst ill th e sp re a d o f m o b ile m o ne y w o uld b e th e go ve rn -

m e n t's c u r re n t f in an cia l I r r c l u s ion pro gra m m e" w h e re o rga nise d f in an cia l se r-

vic es a re b e in g sp re ad a c ro ss th e c ou nt ry th ro ugh m o bile ph on es , a n e n d e a v o u r

th at w ill b e a ssiste d by th e a ssign in g o f a u niqu e td en tif l c atio n n um be r to e ve ry

In d ia n . N o n e o f u s c a n a f f o rd to rem a in o blivio us to th e c h an ge s th at m o bile

m o n e y is i n t r o d u c i n g to o u r live s, T h a t is w h y in th is issu e 's c ove r sto ry w e lo ok

a t th e type s o f f in an cia l tr a n sa c tio ns th at a re po ssib le o ve r th e m o bile ph on e a n d

h o w to d o it sa fe ly to m ak e th e m ost o u t o f th e d e vic e t ha t, till r ec en tly , w a s u se d

fo r j ust c om m u nic atin g (a n d m a ybe so m etim e s a s a f la sh ligh t a t a d ar k p la c e) ,

S t ay i ng in th e d ig ita l d om a in . d o c he ck o ut o ur re vam pe d w e bsite w w w .o ut-

l o o km o n e y . c om . A t th e m om en t . n o t o n ly c a n YOIl r e a d th e m aga zin e l ive o n o ursite . yo u c an a lso vis it it to re ad o ur la te st o ff e rin g. O u tlo ok M o ne y D ig ital (h t tp : / /

d lg ita l.o u tlo o km o n eyc o m ), I nd ia 's f ir st p erso n al f in an ce e -w c e ld y, thatprovides

yo u w ith e xc lu sive o n lin e pe rso na l f in an ce c on te nt f r e e e ve ry S atu rd ay m o rn -

in g. I n O utlo ok M o ne n D ig iw l yo u w il l f in d e xpe rts f ro m e ba y.

P ric e w ate rh o use C oo pe rs a nd rna fo i r an dsta d sh ar in g th eir vie w s a nd a nsw e r-

in g yo u r q ue st io n s in a ra n ge o f a re a s. W r ite in to u s to g ive yo ur fe e d ba c k a n d

su gge st io ns. T o s ta y u pd ate d, su bsc rib e to o ur w e ek ly n ew sle tte r by w r itm g in a t

e le tte r@ ou tlo ok m on ey;o om . T h e y sa y "m o ne y ta lk s' . W ith a ll th is a n d m o re w e

w ill h elp yo u m a ke it t a lk e ve n m o re , -

Our new

offerings(c lo c kw is e f rom

r ight)

a be t t e r- lo o k lnq

w e bs ite : th e

la te st issu e o f

O utlo o k M o n e y

Digi ta l a nd th is

issu e o f Ou t l ook

Mon ey , w ith th e

cover story all

h ow th e m ob ile

p h o n e can re-

s h a p e y ou r

f i n a n c e s

-- . . . . . . .-. . . . ~~..-.. . . . . . . - . . . . .-- - -- - --------

1 I 1 ' 1 I I I - _ - : - : . - --=--.r . . : . a • ~"'III'r-.. •

""....tOUJLOOKMONEY .10 AUGUST 2011 • www.outlookmonevccrn, ~" w or Ta 'M a gT

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 9/76

Availlable at: __ andl other NoktalOutJets I NEIKIA~lt I I :: I To1mow mOl'e a'bout ,our N:olda, Iregister' at ~~~~~~~~. ~.[J

Always InSis~all Originall NDkia l l i ld ia 'Warranty t,o sa f i eguard , against buying u s e d , I refurblshe,d Dr t ampe r e d phon es . t lokfa IMia Warranty I s a p ,p li ca b le , o n ly f ior ph o n e sim p o rt ed /m a n uf ac tu re d b y N o : l t ia , Ind ia I P v t . L t d . # F or os siS lo nce o n N akla' p ro ducts an d s er vice s, , al l N o k ia Ca re . A r i d SI O (a rie wh en ' d Iallin g fr om a G:5Hconnect ion .

< ~worldl'\ag~ 5252.2(H1

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 10/76

I Lett'ers I

Pu hpendra Parikh email

The five stocks handpicked by O u tlo o k M o n e y are very

impressive not only by the virtue of their debt-free status, but

also from the po:int o f their ability to grow businesses at morethan, at least, double the GDP in the last five years.

These stocks may not give stupendous returns, but their

robust businesses and fundamentals together with their

reasonable valuations warrant their inclusion in a discerning

investor's portfolio.

1 am sure that an investor with a moderate risk

appetite should include these stocks in their portfolio, because

of the market shares of these companies command in their

respective territories.

Stocks MatterAnkur Pathare, email

I wan t to c on gra tu la te th e

O utlo o K M o n ey te am fo r its

1 3 th Ann iv e rs a r y !

I h ave b e e n a n avid re ad er

fo r a long tim e now . I w ork

w ith a p riva te a ir line , and

re cogn is e th e Ta ct t h a t f rom

tim e to tim e w e ne e d to

re inve nt ou r p rod uc ts an d

fa cillita te ou r c us to me rs . Ilike th e ne w Ilook o f y ou r

magaz i ne .

How eve r, I fe el th at y ou

ne ed to c ove r th e Ind ian

s toc km ark et w ith m ore

d e ta ils a s it h a s b e e n th e

b igge s t g row th s to ry in th e

la s t f.e w years. Th ough y ou

p rovid e e xp erts ' vie ws an d

s ugg es t a p artic ula r s to ck

in th e S to ck P ick sec t ion ,

I p ers on ailly fe el th at m orec ove ra ge is r eq uir ed .

Second HomeBhargava M . R . , email,

In th e a rtio le a bou t

inve s ting on a s e c ond h om e

(The B e st fo r Your N ex t, 15

June) , I f ee l th a t one ne ed s

to cons id e r th e im pa o t o f

c h ange s p rop ose d in th e

Dire ct la x Co de (DTC) w h ile

m a kin g s uc h in ve stm e nts .

In th e d ra ft o f th e DTC,

INew Additions

Ram Goyell , em.ai lI would like to point out

that JCICI Pru Focus

Bluechtpis missing from

OLM 50.Also, I wou l d

suggest an overhaul o f

category-wise allocation

with separate columns

for large-cap and mid-

cap funds, You can also

start to cover one age-

group in every issue and

suggest a mutual fundand insurance portfolio

for that particular age-

group. For instance, fo r

age limit between 30-

35: these four funds +term plan of a certain

company + PublicProvident Fund.

The magazine is looking

good, but you should

allocate more pages to

queries from readers and

portfoliomakeover.

13 July 2011

c ap ita l ga ins ob ta ine d on

s uch inve stm en ts , w he n on e

dec i d e s to se l l o n e ' s se condh om e, b ec om e s ta xa ble

a s p er th e e xis tin g inc om e

ta x s la b ..A ls o, th e p re se nt

e xemp t i o n a va ila b le fo r

re in ve stm e nt o f s uc h g ain s

on a n ew re sid en tia l p ro pe rty

is w ith draw n. I w ond e r if

c ons id e ring th e s e it w ou ld b e

a d vis ab le to go fo r a s e c ondh om e a s 'in ve stm e nt', if on e's

h old in g tim e fra me is lim ite d

to 3-5 y ea rs .. M a yb e, y ou

c an w rite a n a rtic le h ellp in g

re ad ers figw e ou t th e im pa c t

th at th e D TC w iill h ave .

EOl lOR- : IN-CHIEF

V in od lV I eh taIPRESIO:ENT

M ah es hw el Pe ri

EDl laR

Udayan R ay

IDEPUTY E ID I ITO I IS

A b h iji t M i tr a, C li ff ord A lva re s

SENIOIIIEDITORS

P an ka j A n up Tappa, Sunil Dhawan

C'ONSUl liNG IEOI' l'ORS

M o hit S aty a n an d.

S wa mi S ata n S ha rm a

S EN IO R A SS IS TA NT E DIT O: RS

R a ie sh K um ar . T us ha r S riva sta va

SPEC' IA L CORRESPONDE INTS ·

Anagh Pa l , Kundan K isho re ,

Teena J am K au sh a l

I P R INC IPA l CO :~ R ESPON I) E NTS

K avy a l3 ala ji, K um ar G a uta m

SEN 1011CORRESPONOENliS

A sh w in i K um ar S ha rm a.

N ave en Ku ma r. P he ii Pha lphunan

COPYDESK

A bh ig ya n C ha nd ,

S i d d h a r t h a Sarma .(Deputy Copy Ed i to rs ) .

J o y i ta Cha tt e rj e e (SI. Sub·edi tor )

A 'RT

M a n oji t D at ta (Art Edi tor) ,M iro on B ora (A SS OC ia te A r t

Director ) .

S a ii C .S . ( Pr in c ip a l D e s ig n e r) ,Bhoomesh Dutt S ha rm a {S r.

D e si gn e r), V a ru n V a sh is h th a (C h ie f

o f Graph ic s )

PHOTOGRAPHY

Bhup i n de r S in gh , S ou mik K ar (C hie f

P h oto gra p he rs ), R .A . C h an d ro o

( Pr in c ip a l P h oto gr ap h er) . N ilo tp a lB aru ah , P I!y am D ha r, Vishal Koul (Sr.Photographe r s ) ,

TECHlfEAM

A nw ar A hm ed Kh an . H as an Ka zrn l,Mena v M i sh ra . R a m an A w as th i.

S ur aj W ad h w a

BUSIN iESS OFFICE

PRESIDENT

I nd ra nil R o y

ADVERTISEMENT

V I ICE I PR ESI IDENT Jo hn son D'silva

NORfH Ka il as h L oh a n i ( R e gi on a l

Manager ) , Vini ta Ramtek e ,

Abhishek Berry

WEST Mano j Nair (AG 'M) . Ra ke s h

N ig am . S uc hitra V aid ya ,D e ve s h S he tty

EAST M ou sh um i Ba ne rje e G h os h(GIV i )

SOUTH I a r o o n K um ar (R e g M g I),

P ra ve en K um ar, S un il R a juG E NI ER A L M A NA G ER Ka b ir K h at ta r(Corp)

CIRCULATION

V , ICE I PR ESI IDENT N ir aj R a w ll e y

N AT IO N'A L H EA DS · H me ns hu Pande y( BU Sin es s D eve lo pm e nt) , A le x

J o se p h ( R eta il )

GENIERAL MANAGER Arakia Raj,

B . S . Joha rASSISTANH~EIN ERAL MANAG ER

'Mukesh LakhanpalIO NA lS.A LE S M AN AG E RS An indya

Ba ne rje e (We st), G R am esh (So uth )

DEP II TY MANAGE .R Sh e kh a r S u va rn a

PRODUCTION & SYSTEM

SENIOR MANAGERS De s h ra j J a s w al ,S an ja y N a ra n g, Shekha r Pan dey

IDE' PUTYMAN AGER Trilok SinghR awa t

ADMINISTRAilON

SENIOILIMANAGER Ralendra KUFUP

< ~wolRNTLOOK M:ONIEY .10 AUGUST 2011, . ' www.ou t lookmoney . com

Propert.y Pri,cesArockia Rajasekha.r, email

I am a re gu la r re ad er

o f O utlo o k M o n ey. I am a

r es id e nt o f C oim b a to re ,

You ne ve r se em to cove r

C oim ba to re in : you r lis t o f

p ro pe rty p ric es in : For tn igh t

F ig ure s. I w on de r if peop l e

a re a wa re th at p rop erty

p r i ces ar e a ls o s k y r oc k e ti ng

in th is p art o f th e c oun try ,

~~~~~-~~~~~~-~~~~-~~: L e t t e r s m u s t b e a d d r e S S e d t o : :

: T h e E d i to r. Ou tl oo k Mone y , 8 th f lo o r, N A F E D :IBuilding, A sh ld m , N e w De lh i 110014

: l e t1e rs@ou l lookmoney ,co f fi

I P le a s e m e l/ t i o l1 y ou r f u ll n a m e 8 1 1 d

: r e s i d e nt i a l a d d r e s s .

~ - - - - - ~ - - - - - - - - - - - - - . - - .

~ h lt p :/ /l .w i tl er .c D m /O u ll oQ k MD n e y; h l lp : /I w ww . la c e b oo k. co m /o !m · nd i a

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 11/76

ACT liONThe International: Monetary Fund hastold Europe to take collective actionto contain the eurozone crisis andprevent a spil l lover from the affectedeconomies damaging the region.

e

GOCASHLESSATHO'SPITAILS AGAINIDeadlock over cashlessclaims over, hospitals andinsurers reach settlement

c ha in s th at k ep t th em se lve s o ut o f th e

pr efe rr ed pr ovid er n etw o rk ( P P N ) se em to

have a c c ep te d th e a r ra n ge m en t T h e

manag emen t s o f these g roup s have

ag re ed to th e sta n da rd tre atm e nt r a te s

n ego t i a t e d by th e p u bl ic se c to r h e a l t h

in su r an c e p ro vid e rs.

The,beginning of the feud. A r te r c la im -in g th a t h o sp ita ls w e r e o ve rb il l in g po lic y-

h old ers . a nd fa ce d w ith e sc ala t in g a n d

u nsu sta in ab le c la im ra tio s in th e ir p ro d-

uc t s . health in su ra n ce c o m pa n ie s

la un ch ed a pre fe rr e d pro vid e r n e tw o rk

(PP ) o n 1 July 2010, f ixin g th e ra te s o f

tr e atm e nt a n d p ro ce du re s fo r hospitals .

T H IE

st al em a t e o v er c a sh le ss

- tr e atm e nt c la im s f in al lyc am e to a n e n d L ast fo rtn igh t w ith fo ur

sta te -o w n ed h ea lth in su ra nc e lirm s -

N e w In d ia A ssu ra nc e. O rie n ta l

In su ra nc e, U nite d In dia In su ra n ce a n d

N a tio n al I nsu ra n ce -s-a nd a ll b ig h o sp i-

ta l s , ex c ep t A po llo H o sp ita ls . a gr ee in g o n

a n ew se t o f ta rif fs . M o s t pr iva te h ospita l

WOW!The Insurance IRegulatory and Devel-opment Authority has suggested thathealth insurance benefiits also inclludeout-patient department (OPD)servlicesin hospitals as well as childbirth.

M a ny h ospita ls h ad d ro ppe d o ut 01 th e

cashl e s s t r e a tm e n t list w h ile f e w a gre edt o j o in it. O ve r tim e , h ow e ve r, m o re h o spi-

t al s a g re e d a n d jo in ed th e P P N n e two r k .

T h o s e that didn't, e s pe c ia ll y t h e p riv a te

h o s pit al c h a in s . a rgu e d th a t h ig he r t re a t -

m e n t costs=high se rv ic e sta nd a rd s. h ig h

cos t o f m e dic al. e qu lpm en t a nd n ew a n d .

la te st p ro ce du re s-r e su lte d in h igh er

c o sts. O n ly th o se h o sp ita ls th a t agre e d to

t h e in s u re r s' t e rms w e re k e p t o n th e P P •T ho se w ho a gre e d to P P N w ere to fo l-

lo w th e pa c k age ra te s a s pre pa re d by th e

fo u r in su re rs in c on su lta tio n W ith th ird -p ar ty a d m in ist ra to r s ( T P A s) -t he in te r-

m e d ia ry b etw e en th e po lic yh o ld er a nd

th e insurer=for s p e c if ie d p r o c e d u r e s .

T ho ugh th e pa tie nt c o uld still g o to h o sp i-

ta ls o utsid e th e n etw o rk fo r tr e atm e nt. h e

w o u ld n o lo nge r be a b le to ava il th e c a sh -

le ss f a cil it} , T h is m e an t th at h e w o u ld

n ee d to m ak e h is ownarrangements to

f u n d th e tr e a tm e nt a n d, l a t e r , a pply to th e

in su ra nc e c om p an y fo r r e im b u rse m e nt

W h al t it m e a ns. A s a health insu rance

po l i c y h o l d e r , th e c ash le ss m o de o f pa y-m e nt m a y stil l b e th e e asie r w ay. H o w eve r.

th e c o st o f tr e a tm en t w o u ld d e pe n d o n

the g r a d i ng o r e ac h h o sp ita l. so m e th in g

th at h as a lr e a d y h appe n ed , E n su re tw o

th in gs b ef ore h o spita lisa tio n : c he ck if

h o spita l is u nd e r P P a n d th e g ra d e to

w h ic h it b elo n gs.

S a ys Y a sh ls h D a ht ya , C E O , . Po l t cy l l a z a a n

c o m , an in su ran ce c o m pa r iso n po rta l:

"I t 's a g oo d m o ve . Itsh o w s th a t in su re rs

a n d T P As c a n negot ia t e b ette r d ea ls to

o ffe r t h e c usto m e r su pe rio r m e d ic al tr e at-

m e n t a t th e h ospita l o f h is choice ."

SUNIL DHAWAN

< ~worldl'\ag~ http://digltal.outlookmoney,com.lI0 .AUGUST 2011 • OUTLOOK MONEY 9

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 12/76

I NewslRoll l1

HOPEThe finance ministry is optimistic aboutmeeting its disinvestment target of~40,000 crore for 2011-12,.although only

~t1I44,55 crore has been mopped upthrough this route so far this fisoal.

PL,EASE!Banks have asked the Reserve Banikof India to take a pause and not hikeinterest rates in its monetary policy

review next week as bank oredit hasallready seen some moderation.

A PAIRADIOM SHIIFTAl te rna te banking

ch ann els a re fast

g ain in g g round inIndia

ACROSS In d ia . c usto m e rs n ow visit

ba nk bra nc h es le ss o fte n th an e ar lie r .

I n s t e a d . they h a ve ra m p ed up th e u se o f

th e Internet a nd m o bile dev tces , a c c o r d -

ing to A sia Su rv ey o f P erso nal J : t l l 1 a l l c i a l

Servkes by c on su lta nc y M c K in se y &

C om pa ny. W h a t m a ke s the f in d in g in t e r-

es t i ng is th at b a n k b ra n ch u sage h a s

d ro ppe d a cro ss A sia . in clu d in g In d ia . f o r

th e f ir s t t im e sin ce l \k K in se y sta rte d c on -d u ctin g th e su rve y 13 y ea rs a go . .

Alternate channels gaining traction.

T h e su rve y w a s ba se d o n in te rvie w s w ith

n e a r l y 20,000 A sia n c on su m e rs a cro ss

13 m a rk ets, o f w h ic h th e la rg e st su rve y

p oo l w a s In d ia . with 5,000 r e spond en t s .

T he su rvey reve als th at w h ile In dia h as

se e n a 15 pe r c e n t d ec l in e in b r a n c hu sag e . th e u sa ge o f th e In te rn et a n d

mob i l e b an kin g h as m o re th an tr ip le d . In

I nd ia , a bo u t 7 pe r c en t o f a l l b an kin g

c on su m ers n ow u se In te rn et ba n k in g, a

s ev en -f o ld l ea p f ro m 1 pe r c en t in 2007.

Say s R e nn y T h om a s, pa rtn er in

M cK in se y's I n d ia o f fic e : " T h is r ep re se n ts

a fu n d am en ta l sh ir t in c o nsum er be h av-

io u r a nd h as S ign if ic an t im p lic atio n s fo r

ba nk s a s th ey c on sid er th eir c ha nn el

str a te gy a nd h ow th ey sh ou ld a l lo ca te

in v e st m e n t r e so u r c e s. "O th e r f in d in gs in c lu de d th at c on su m e rs

h ave be co m e m o re c a u tio ns w h e n it

c o m e s to b or ro w in g.

by VARUN VASHISHTHA

EPFO 'S NEWLIST OUTOrganisation announcesn ew fun d m an agers, all

but on e hold term

S t a t e Ban k o f I nd ia (S B l). H S B C Asse t

Man a g em e n t a n d R e lia n ce C a pita l A sse t

M a nage m en t h ave be e n re ta in ed a s I u n d

man a g e r s by t he Em p lo y ee s' P r o vid e n t

F u n d O r ga n is at io n (EPPO) . IC IC r

S e cu rit ie s P r im a r y D ea le rsb ip h a s be e n

a ppo in te d a s a n ew fu nd m an age r in th e

g ro u p. I CI cr P ru d en tia l A sse t

M a nage m en t, o ne o f th e fu nd m a n ag e rs

fo r th e pre vio us th re e-ye ar te rm (M a rc hlOOS to M a rc h 2011). h as b ee n d ro ppe d .

O th e r b id d er s th at h ad qu alif ie d th e

te ch nic al ro un d w e re B ir la S un Life MlI lC.

UTI A sse t M a n a ge m e n t. S e cu rit ie s

T ra din g C orpo ra tio n o f In d ia , K o ta k

M a h in d ra A sse t Ianagement a n d

F ra n klin T e m p le to n A sse t M a n a ge m e n t.

Says S . C h a tt er je e , c e n tr al p ro vid e n t

f u nd c o mm iss io n e r: ' :A s o f n o w . w e h ave

c l o s e to 'N ,OO,OOO e ro r e o f c o rpu s , o u t o f

w h i ch a b ou tn .5 0 .0 00 croreis w ith th e

R e s e r v e B an k: o f In dia an d r em a i n i n g~2,5(J.OOO c r o r e w Lll b e ma n a g e d by t h e

f o u r fund m a n age rs." O u t o f th is , 8m will

ma n a g e 3 . 5 pe r c en t 01 th e c orpu s ..fo l -

lo w e d b y IC Ic r at 2 5 pe r c en t. R e lia n ce

a n d H SB C w ill m an a ge 2 0 pe r c e n t e a c h .

W h e n asked w h y IC IC I Prudentlalwas

d ro pp ed f ro m th e list d e sp ite g en e ra tin g

th e h ig he st yie ld among th e four f u n d i

m a n ag ers o ve r th e ir la st th re e-ye ar te rm .

C h a tt er je e s aid : "It w as an o pe n b id din g

a nd IC IC I P ru de n tia l A sse t M a n ag em e n t

m u st h ave qu ote d h igh er r a te s fo r I ts se r-

vic es. a n d th at m u st be th e r e aso n."

ASH.IN. KUIMAR S'H'AR.MA

""....nOUTLOOK MONIEY .10 AUGUST 2011 • http://outloakmoneycom\ I~worrd ' i ! l ' a! i l '

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 13/76

RESCUEA group of ministers is diiscussingaproposal for an additional ,{1,800 croreof equity infusion in Air-India i'nthe

current year, apart from the ~t200crore already announced this year.

Commodity

GOOlDA positive recruitment trend was seenin smaller towns and rnlnl-metros dur-ilng April-June 20111due to increased

hilring in engineedng and manufactur-ilng:sectors, says a recent study.

G old touches n ew high ,silver rem ain s stron g on

dollar w e a k n e s s

PREC'IO 'U S ME .T A LS

Du rin g th e w ee k e n d ing 15 J u ly , gold

touched a h igh or $1.594.9'0 p er o u nc e

and continued to r ise on th e bac k o f th e

eu rozone d e b t c ri sis . U s safe-haven buy -

in g w a s a lso su p po rte d by th e f a ilu re o f

U S p o l it ic ia n s to r e ac h a n a gre em e nt o nra isin g th e d eb t c eil in g fo r th e c ou n try .

G old c on tin ue d it s a sc en t d ur in g th e w e ek

b e g in n in g 18 Ju ly to to u c h a n e w h igh o f

$1,607 pe r o un ce , O n th e M C X, th e ye l-

lo w m e ta l r e a c h ed a h ig h of~ 2 3 .2 91 pe r

1 09 . H o w e v er , by th e m id d le o f th e w e e k ,

it lo st s te am a n d fe ll by o ve r 1 pe r c en t a s

in ve sto rs m o ve d to w a rd s r isk ie r a sse ts o n

RE PORT C AIRD

.Gold I!/g)

Pr i ce 2,28•. 50

1-yr return (% ) 33..33

• S illve r ((/g)

Pr i ce 54.5,7

1-yr return (% ) t28.08'

• C ru d e ,Oill { $ l b b l l )

P r i c e 88.621-yrreturn (% ) 23.28,

th e bac k o f a p o ss ib le s o lu -tio n to th e e uro zo n e c risis,

S ilve r h as r e m a in ed stro n g

fo r th e la st tw o w e e ks fo l-

lo w in g w e a k ne ss in th e d o l -

l ar . A f te r g a in in g 6 pe r c en t

in th e p r ev i ous w e e k . it

a dd ed a no th e r 3 p er c en t

ga in d ur in g th e w e ek

beg i nn i ng 18 J u l y . I t

to u c h e d a h igh o f ~60 . 2 53

pe r k g o n th e M CX

S e p te m b e r c o n tr ac t.S a ys [l ga r P a n d it , a ss is ta n t v ic e -p re si-

d en t. c om m o d ite s a nd c ur r e n cie s,

S h are kh an : "T h e o ve ra ll o u tlo o k is b ull -

ish fo r g old . b u t c on so lid at io n is r e qu ir e d . .

M o n ey c an m o ve l im n go ld in to e qu itie s

a n d o th e r r isk y a sse ts fo r th e sh o r t te L'L T I.

A n d silve r p ric es a re n 't su pp or te d b y fu n -

d am e n ta ls a s th e g lo ba l p ic tu re is f r a gile ,"

IIMPACT OF GLOBAL FACTORS

T h e e u r o z o n e d e b t c r i s i s a n d w e a k n e s s

in t h e d o l l a r c o n tin u e d t o s u p p o r t g o lda n d s il v e r p r i c e s , w i t h t h e y e i l l o w m e t a l

e v e n m a n a g in g t o r e a c h a n e w h ig h .

C r u d e o il l w a s a g a in v o la t i le

B AS E M E .T AL SE xc e pt a lu m i n um . a ll o t h e r

b ase m e ta ls r e co rd e d ga in s

d ur in g th e w e ek e nd in g 15

J U l y , t h a n k s to th e d e pr ec ia -

tio n in th e ru pe e a n d th e

success fu l s t r ess tes t o n

E uro pe an b an k s. H o w e ve r,

itw as a m ixe d tr e n d in th e

w e e k b e gin n in g 18 J u ly d u e

to a w e ak e r d o ll a r, p osit ive

U S h o u sin g da t a a n d th e

e u ro z on e c r is is . S a ysPa n d i t "C o pp er is lo o kin g g oo d a nd is

ta kin g o ut r e sis ta nc e a t H40. I t c o u ld

r ise f ur th e r, A te st o f p sy ch o lo gic a l r esis-

ta nc e a t N 4 9 is a po ssib il ity; h ow e ve r,

f r o m th ere th e m e ta l c a n m o ve lo w er . I n

c ase o f l e ad a nd zin c, th e r a lly is o ce r-

d o ne . W e su gg est b oo k in g p ro fits in le ad

w h en it to uc he s n2S..50."

ENERGY

Du rin g th e w e ek e nd in g 15 Ju ly . c ru de o il

h ad ga in ed o ve r 1 pe r c en t w ith p r ic esto uc h in g a h ig h o f $9 9 .2 1 pe r ba r r e l

(bb l) o n th at d ate . T n th e w e ek be gin nin g

1 8 Ju ly, c ru de o il f lu ctu ate d bu t h ad

ga in ed o ve r 1 pe r c en t by th e m id dle o f

th e w ee k . O n th e M CX . it to uc h ed a h ig h

or N ,4 24 Ibb l o n 2 0 Ju ly . P an dit says:

"C ru d e o il h a s be en stu ck in th e $94 -

99 .5 0 ra n ge . W i ld sw in gs in c ru de o il

w o uld c o n tin ue . O n th e In d ia n b o urse s, it

c ou ld r ise to N,S60 if it ta k es o u t r esis-

ta nc e a ro u nd H,430. H o w e ve r, w e w o u ld

su gg est se ll in g in to ra ll ie s a s a m u c h

l o w e r p ric e is p o ss ib le e v en t u al ly "

KAVYA B.A.LAJI I

< ~worldl'\ag~ http://dig,taLoutlookmoney.com .10 AUGUS'J 2011 • OUTILOOK. MONEY 1 1 1

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 14/76

I NewslRolll1

TOUGHAcknowledging persistent high inflationand signs of an industrial slowdown, thegovernment has pared its gross domes-

tic product growth forecast for 2011-12to 8 .6 per cent from 9 ' per cent earlier.

ABOUTTIMI!The government has started working ona new perception index to counter theimpact of the Doing Bus i ne s s Report o f

the IFe, which ranks India belowPakistan, Samoa and Mongolia.

SEBITHE REGULATO : R

Securities andExchange Board oflndia has allowedstock exchanges tosh itt. securities ofcompanies listed inAnnexure A havingestablished connectiv-it y with depositories

to normal rollingsettlement subjectto conditions

Onthe

5 , 8 0 0

- N i ! t y

5 } O O

. 5 . 6 0 0

5 5 0 0

1 0 6

1 0 4

1 0 2

1 0 0

9 8

9 6

su r 2 0 J u l ' 1 1 1

Sensex felll by cliose to 2per cent on gllobal uncer-tainty. BSIEReality indexwas the biglgest gainer

Street

RESCUE ACTGovt to step up

assistance toe le c tr ic ity b o a rd s

W ith m o s t sta te e le ctr ic ity

b oa rd s stru gg lin g w ith h igh

d is tr ib u tio n l os se s. p o w e r

min l s te rs o r var ious s ta tes

m e t in ew De lh i th is fo r t-

n igh t T h e sta te s a gr ee d to

r e vis e t ar if fs a n n u a ll y i f th e

c o st o f p ur ch a se 01 e lec t r i c i tygo es u p, w h ic h a c c ou nts fo r

70-80 pe r c e n t o f th e c o st o f

s up pl y. T h e st at e g o ve rn m e n t s

wil l c l e a r a ll p e n d i n g subs idie s

to th e bo ard s a n d wi l l e n s u r e

a dva nc e pa ym e n ts o f su bsi-

d ie s a s p er th e E le c tr ic ity A c t.

T h ese m e asu re s a r e be in g

lo ok ed a t a s a m a jo r po sit ive

fo r the sta te b oa rd s a nd thetw o b ig sta te -o w n e d le n de rs.

P o w e r F in an c e C o rp or atio n

(PFC) a n d th e Rural

B l e ct n fic a n o n C o r po r a ti o n

(REC) . A s a re su lt , bo th sto ck s

witnessed h ig h b u yin g In t e r -

es t . PFC and R EC r o s e 9.6 and

7..3 pe r c e n t , r e sp e c ti ve ly, o n

1 4 J ul y, H o w e ve r. b oth th e se

c ou n te rs h ad se en su bsta ntia l

c u ts in th e last le w m on th s o n

concerns about the a b il it y o fs ta te b o a r d s t o r ep ay deb t .

R E C f e ll f ro m {2 67 inMa r c h

t his y ea r t .o a lo w of n80 in

J u n e . PFC too wi t n e s s ed a

s im i l ar d e c l in e . A s w e go to

p re ss , P P C a nd R EC w e re tra d -

in g ~208.50a n d ~216.40.

RAJESHI KUMAR

R.K.

HI IGHIONACTI IONI

S K S M ic ro f in a n cem a k es so lid ga in sd e s p it e v o la t il it y

SKS iV 11 c ro it na n c e , th e o n ly

m i c r o f i n a n c e company l is ted

in I nd ia , w i tn e sse d h ig h

d ra m a a nd sign if ic an t pr ic e

volatility t h is f o rt ni gh t . Af t e r

it w a s d ec id ed that th e

R e s e r v e Bank o r In d ia wi l l beth e r e gu la to r o f th e c o m pan y.

th e be a te n -d ow n c ou nte r saw

a slg ntf lc an t su rg e in a ctivity.

It mov e d up by 20 pe r c en t

o n tw o c on se cu tive d ays

(7 a n d 8 J Uly ) to h it th e c ir -

c u it . L a te r, the e x c h a n g e s

revi sed the c ir cu it l im i ts , b u t

th e sto c k m ove d u p c lo se to

]0pe r c e n t e a c h in th e n e xt

tw o d ays.

H o w eve r, w h at go es upmust c o m e d o wn . so th e

st o ck c o rr e ct ed 10pe r c en t

o n bo th 13 and 1 4 J uly.

N o n e t h e l e s s , :i t is s til l u p

60 ' pe r c en t sin ce the begin -

n i ng of J u ly . E a rl ie r . d u e to

unc e r t a i n ty on t he r eg u la -

t i on front and o t he r is su e s,

it h ad d ro ppe d f ro m n.400

in S e pte m b er 2 c n o to a lo w

on'270 in MaJ I 2011. A s

w e go to pre ss , it i s t r ad i n g

at~548.45.

R.K.

LOTS IN I A NAM EN ew s o f sta k e sa leby Jhunjhunwaladrags Lupin s t o c k

S ha re s o f d ru gm a ke r Lupin

su dd en ly f e l l a bo ut 4 pe r c en t

o n 20 July a n d a fu rth er 3.16

pe r cent o n 21 J u ly on the

n ew s th at R a k esh [h un ih un -

w a la , th e billionaire i nves to r .

h as so ld pa r t o f h is h old in g

in th e c om pa ny dur ing th e

J u ne q u ar te r. In fact .

[hunjhunwala, along wi t h

h ts w i f e . now hold a s t a k e o f

1.73 pe r cent in th e c om p an y

c o m pa re d to 3.22 pe r c en t at

th e e n d o f M a rc h 2m 1.

Meanwh l l e , f o re ig n in s tit u -

tio n al in ve sto rs [F Ils) h a ve

r ais ed t he ir stake in th e c om -

pan y to 2 3.5 7 pe rc e n t a t

th e Ju ne -e n d qu ar te r c om -

pa re d to 18.60 pe r cent in

J u n e 2010 ..

"".... .~ OUTLOOKMONEY .10 AUGUS12011 • http://outlookmoney.com, ~ " w o r r d l' ra g s

= hllp:/!twitl er.com/Outlooklvlcney, htt p:/fwwwJacebook.com/olmindia

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 15/76

a r e w a rn in g U S of str ip pin g its tr ip le A

ra tin gs re pe ate d ly. A d ef au lt a n d lo w erc re dit r a tin g fo r U 8 m igh t pu sh th e m a r-

k e t in to a f in a l ta ilsp in . T h e q ue stio n is,

if US d eb t is n o t sa fe , th en w h a t i s ?A n d

h ow d oe s o ne va lu e $]4 .3 t r il l io n d e b t

o u tsta nd in g? B u t, h e pe fu lly C o ng re s-

sm e n w iU r eso lve th eir d if f er en ce s a nd

r a ise th e lim it b e fo re 2 A ugu st, th ou gh

it m ay o nly h appen if th e Obam a adm ln -

istr a tio n a g re es to a d ee p c ut in b u dg e t

d ef lc tts, A c u t in go ve rnm en t spe n d in g a t

th is sta ge , h o w e ve r, m ig ht a ff e c t th e

f r ag ile r ec ove ry o f th e e c o n om y wh i c hh as a d if f e re nt se t o f im p lic at io ns, su ch

a s so fte r e co n o m ic a ct ivit~ 7 ,fo r a n

e xt en d e d p er io d . A w e a k e r US e c o n o m y

wi l l a f fe c t e xp o rt s f r om th e

r e st o f th e w o r ld , : i:n c lu d in g

In dia . W i th so m a n y ir s a n d

• Debt crisis is b uts, u nc er ta in ty a nd in te re stra te s a nd its im p lic atio n s c o n-

tin ue o n th e d om e st ic f ro nt .

In fla tio n ba se d o n th e

w h o le sa le p r ic e in de x w a s 9 .4

pe r c e n t fo r th e m on th o fJu ne , w h ic h is st il l w a y a bo ve

th e c om fo rt le ve l o f o ur

c e ntr al b an k , a n d e c o n om i s t s

a re e xpe ct in g a n oth er 2 5 ba sis

po in t ra te h ik e by th e R e se rve

B an k o f In d ia o n 261u ly .

O n th e p ositive s id e . in fla tio n m ig ht b e

pe a k in g a n d th ere w ill so on be a pa u se

o n ra t e h i k e ,

Your money. T h e u nc er ta in ty c on tin -

u es, a t l e ast in a sse ts l ik e e q uitie s. G o ld ,

m e an w h ile . in th e in te rn atio na l m a rk e tto uc h ed a n a ll -tim e h igh o f $1 .600 pe r

o un c e th is f o rtn igh t o n th e b a c k o f

u n ce rta in ty. H o w e v e r. Out look : M o t l e y

h as a lw ays a dvise d yo u n ot to pu t su b-

s ta n tia l am o un ts o f m o ne y in go ld an d

k e ep it ju st a s a d ive rsif ie r (se e Hedging

al e H e d q e , . 2 7 Ju ly ) . I n e q n tt le s, itwo u l d

be a dvisa ble to re m ain in ve ste d a nd c on -

t in ue yo ur S [P s. bu t k ee p so m e in ve st-

a b le c ash in h an d to ta k e a d va n ta ge

o f a n y d ee p c or re ct io n in o ur m a rk ets

b e ca use o f th e w o rse nin g g lo ba l c eo -

SHAK-Y,GROUND

.aftectiing larg:-

er countries in

Europe·

• US is inch-

in g towards asovereign

default

I MacroMo,ney I

BY RAJESH KUMAR

FINGERSCROSSEDBad news on severalfronts continues. Whatmust you do with your

money?

ve ry qu i ck ly fo r th e w o r se . W e saw th at

in th e a f te rm a th o f th e c o lla pse o f

L eh m an B ro th ers in S e p t em b e r 2008 ..

If th is w a s n o t e n o ugh to c r e a te u n c e r -

ta in ty in th e g lo ba l f in an cia l sys t em , w eh av e US . th e la rg e st e co no m y o n th e

p l an e t . inching to w a rd s a so ve re ig n

d e fa ult . T h e c o un tr y wi l l r e ac h th e le ga l

l im i t o f b o rr o w in g . se t by th e

US C o n gr es s. o n 2 A u gu st. If

th e lim i t is n ot r e vise d o n tim e

a n d if th ere is e ve n a m in o r

d e fa u lt . t h e r ep er cu ssio n

w o u ld b e visib le a ll o ve r: th e

w o r ld . C re d it r at in g a ge n cie s

in c o m i n g q u ar te r ly n umb e r s

by c o r p o r a t e In d ia fo r th e June

quarter h ave d on e ve ry l it tl e , s o

f a r , in te rm s o f lif t in g th e

m o ra le a t th e sto ck m ark et Eve n th ou gh

th ere h as n o t b e e n a n y n e ga t ive n ew s o n

th e e arn in gs f ro nt . th e m a rk et is m o r e

w o rr ie d a bo ut th e g lo ba l a n dlo ca l m a c-

ro ec on om ic sl tu at io n . W h i le n ew s f ro m

th e re st o f th e w o rld : iso nly a dd in g toth e u nc er ta in ty, o n th e d om e stic f ro n t,

in fla tio n a nd in te re st ra te s c o nt in ue

to h ur t th e e arn in gs e xpe cta tio ns

o f c o rp ora te In d ia .

O n th e in te rn at io na l f ro nt, th e

e xpe cta tio ns a re sw in gin g be tw e en tw o

e xtre m es in E uro pe a nd U S . In E uro pe .

th e d eb t c risis h as sta rte d sh ow in g its

im p ac t o n la rg e r e co no m ie s l ik e I ta ly

a nd S pa in . w ith d if f e re nc e o n yie ld s r is-

in g sig nif ic an tly a bo ve G e rm a n b on d s,

c on sid ere d to b e th e sa fe st in t he r eg io n .T h e p r o ble m is if th er e is a se rio us f ln an -

c ia l m a rk e t a tta ck o n I ta lia n so ve re ign

d e bt , it w i l l b ec o m e re al ly d if fic u l t f o r th e

m o n e ta ry u n io n to c a lm n e rve s, a s it

m igh t tu r n o u t to b e a c a se o f 'to o b ig to

sa ve '. I ta ly is th e th ird -la rg est issu er o f

d eb t in th e w o rld a n d its to ta l d eb t s to ck

is in e xc ess o f $2 .5 tr il l io n . H o w e ve r, th e

s av in g g ra c e , so la r, is th a t f un d am e n ta ls

o f th e l ta l la n e co no m y a re fa r su pe rio r

to th ose o f o th er sm a lle r e co no m ie s,

su c h a s G re e c e a n d P or tu ga l . B u t th e

p ro ble m is , w h e n c on fid en ce is lo w in

th e f in an cia l m a rk e ts, th in gs c h an ge

V I \R UN V A S HI SmHA

• lnflation inlndla is sti ll

high

n o m ic e n vir on m e n t, 0

Irajeshkumar@outlookindia ..com

III h t l p :! ! tw i tl e r .c om !Ou t !o o kMon ey ; h l l p :/ ! www . la c eboo k . com /o !m ·n d i a

http://drgilal.outlookmoney.com.10AUGUST20.11 • OUTLOOK M'ONEY 13< ~worldl'\ag~

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 16/76worldMags

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 17/76worldMags

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 18/76

I Queries I LIFE INSUR.ANCE GENIEIRA.LINSURANCE MUTUAL FUNID'STA

on taking up employment outside India, or (b) for

c ar ryin g o n a bu sin ess o r vo ca tio n o utsid e In dia ,

o r (c ) fo r any o th e r p ur po se .

T h er e f o re . if a pe rso n stays fo r 182days o r more in the preceding finan-

c ia l y ea r an d g oe s o u t o f In dia in th e

current flnanctal ye ar fo r taking up

e m plo ym e nt o r c ar ryin g on a n y

business o r fo r any other pu rp os e

which w o n ld in d ic ate his in t en t ion

to stay outside India f o r an uncertain

p e rio d , h e will n o t b e t re a te d a s a

r esid e nt in J nd l a f or th e c ur re nt

f in an cia l ye ar. S o, in yo nr c ase , a s

yo u h ave le ft In dia f o r th e pu rpo se

o f jo b yo u wil l b e c on sid ere d n on -re sid en t in Jn dta f or th e c ur re nt

f in a nc ia l y ea r. 0

ATULasked

What penaltyis charged forprematurewithdrawals offixed deposits?

ApnaPaisa's Harsh

Roongta replies:

Normally,a bank

charges a penalty

of 1 per cent below

the interest rate applicable on the date of deposit for the

period the fixed deposit was with the bank. For instance.

i f you had started a fixed deposit on 1 June 2011 for five

years, at a rate of 9.50 per cent per annum for 5 years.and 4.50 per cent per annum for a period between 30-90days, you will get an interest of 4.50 per cent per annum

minus the penalty amount of 1per cent per annum(which is 3.50 per cent per annum) incase you withdrawthe deposit on 20 July 2011 (which is 50days from date

of deposit). The original contracted rate of 9.50 per cent

per anllllin has no bearing in this matter. LJ

l.u·]:tI;j I i I,]3 : ' I , ]0:.RUDRA JALA'L, email

II left India for the purpose of job in Dubai.

Meanwhile, I alpp~liedfor a dealership in

India for which one needs to be a resident of

llndia. IIam stilillunder the income tax law in

llndia. Willill be considered a resident under

Foreign Exchange Mana.gement Act (FEMA),

as I do not have any lntentton to settle per-

manently in Dubai?

PwC experts reply Accordingto S e c tio n

2 (B ) ( \ 1 ) of FEMA . a r es ld en t o f India is a person

re sid in g in In dia fo r m o re th an 182 d ay s. d u r i n g

th e c ou rse o f th e p re ce din g f in an cia l ye ar , bu t d oe sn o t in c lu d e a pe r so n w ho h a s go n e o u t o f In d ia , o r

w h o sta ys outside India. in e i t h e r case-(a) for or

"".... tA OUTLOOK IMONEY .10 AUGUST 2.011.' www.outlookmoney.com, ~ " w o r ,. <M a g s

ltj~:1 4 i " " U F l i J j l"J:T3lJCHETANI CHAVAN. email

Ihave taken a home loan of ~uakhalldpurchased a flat in Navi Mumbai for ~21Ialkh.

Iam earniing~6,.OO'Oper month through

rent. Should IIpay the tax for this? How can I

recover it?

OLM Rep~liesA s pe r th e 1n c o m e T ax Act O TAct). yo u n ee d to fi le tax re tu rn in c a se yo ur to ta l

income w a s le ss th an n.60 la k h in th e financial

ye a r 2010-11, w h ic h is n ow ralsedto n . 80 I akh

£01" the f i n an c i a l year 2011-12.

I n yo ur c a se , a s yo u h ave m en tio ne d th at yo u

have a r e n t a l income o f ~6,OOO pe r m o nth , yo ur

total in co m e u nd er "in co m e fro m h ou se p ro pe r ty"

du r i ng the year comes to ~72 ,DOD, which is less

th an th e in c o m e e xem pte d f r o m tax. Th e r e f o r e ,

yo u need not f i le an income tax return ..Moreover.

yo u a r e a llo w ed to m a ke sta nd ard d ed uc tio n o r a

maximum o f 30per cent from th e rent re ce ivedw h i c h willi fu rth er re du ce yo ur in co m e. Itis a sta t-

u t o ry deduction which is n o t d e pe n d e n t o n th e

a ctu al expe nd itu re in cu rr e d o n re pa irs, o r c olle c-

t ion by th e o w ne r : Y o u can also claim deduction for

th e pr in cipa l r e pa ym e nt a nd in te re st pa ym e nt d ur-

ing the year on home lo an u nd er Section 80C and

S ec tio n 2 4 o f th e IT A ct. re spe ctive ly;

H o w e c e r , if yo u h ave a ny additional income f r om

sa la ry , p ro f essio n , b u sin e ss, c a pit al g ain s, 01 " o t h e r

sources, during th e yea r and you r total i n c om e

e xc ee ds th e e xe m pte d in co m e limit. yo u n ee d to m e

areturn.

Wh i l eftllngthe

return. c h e c k the type of

in co m e ta x re tu rn fo rm a pp lic a ble fo r you a s pe r

your d i f f e r e n t sources of income.

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 19/76

ATIONI BANK.ING REAL ESTA'TE RE,TIIREIME,NTSTOCKS NRI

I I ~ 1 ~ 4 1 1 : HI J ;?,' :(3jPRIITAMIGUPTA. email

II want to take a loan 31gainst m y life lnsur-

ance policy from Life Insurance Corporationof India (Ue) for the construction of my

house. I have an endowment policy which

is two year.s old. As per pollicy conditions. I

willi be eligible for the loan only after three

pollicy years. The third premium is not due

as yet. If I palYthe next premium in advance,

willi Ibecome eligible for the loan?

OLM Replies T h e lo an a ga in st a l ife in su ra nc e

p o lic y is granted o n th e ba sis o f th e su rr e nd er

va lu e o f t ile po lic y. T h e stipu la tio n o f th re e ye ars

f o r g ra n t o f lo an is a lso c on sid ere d a s y o ur p o lic y

w i .U acqui re t he s ur re n d e r va lu e o nly a fte r th ec om p le tio n o f th e sa id p er io d ..I t wil l n o t m ak e a n y

d if fe re n ce e ve n i f yo u pay o n e ye a r 's p rem ium in

a dva nc e. F ur th e r , e ve n a fte r th re e ye ars , yo ur e lig i-

b il ity f or lo a n w ill be m ea gre a s th e su rre n de r

va lu e o f yo ur po lic y in th e in it ia l ye ar s wil l be lo w .

H o w eve r, a s an a lte rn at ive o ptio n, yo u c an e xplo re

h o usin g f in an ce c om p an ie s. B e in g a po lic yh o ld e r

o f U C. yo u rn a} ' g et so m e pre fe re nc e if }'OU

a ppro ac h L IC H o u sin g P in an ce C orpo ra tio n ..0

MOTI RAO, email

My uncle holds a life insurance policy witha crltlcal illness rider. Recently he was diag-

nosed positive f,or cancer, When can his fam-

ily expect to get a payment under the rider?

OLM Replies T h e payment u n d e r a 'critical ill-

n ess rid er ' a t ta ch ed w ith a lif e in su ra nc e po lic y is

normally made 30 days a f t e r the named critical ill-

n ess is d ia gn o se d . T h e c on d itio n is th at th e in su re d

m u s t survive the pe r i o d of 30 days.alter t he d ise a se

is d ia gn o se d . A d vise yo ur u n cle to f ile h is c la im

immed i a t e l y , if h e h a s n ot d o n e so . A s pe r ge n e ra l

Lo g o n to

www.ou t lookmoney .

c om

a nd p os t y ou r qu erie s

a t th e E x pe rt A d vic e

b ox or ma i l a t

l e t te r s@ ou t lookmooe ' )! ,

c om

conditions of the p o l ic y . t h e payment is m a d e

im m e d ja te ly o n c om p le tio n o f 30 d ays f ro m th e

date of detection o f disease. a

R.KRISHNAN, emaill

I am 4 1 1 . I am pl1anning to take a life ins'Ulr-

anee pollicy. Im confused as to how much I

should insure for. Various quarters sugg:est

various thumb rules to figure out the correct

sum insured. Can you suggest an approprt-

ate amount of insurance?

OLM I Rep'lies In su ra nc e is m e an t to pro vid e

f in an cia l se cu rity to th e d epe nd an ts in th e e ve nt o f

d ea th o f th e in su re d . T h er ef or e, t ile bes t w ay to

de t e rm in e th e am ou n t o f in su ran c e is to im ag in e

t h e [in a n cia l needs o f your d epe nd an ts in yo ura bse n ce . T h e su m in su re d sh ou ld be an a m o u n t

w h ic h if in ve ste d sa fe ly wi l l ge ne ra te a n in co m e

w h ic h w ill be su ff ic ie n t to m e e t th e p r o j e c t e d

expenditure of your dependants. You mu s t aliso

consider th e fluctuating interest rates. F ro m th is

sum, you m ay reduce th e accumulated savings.

Af t e r a sc e rta in in g th e n e e d f o r in su ran c e . a im to

secure th at m u ch cover. Dep e n d i n g on th e premi-

u m pa yin g c apa city, yo u c an a cqu ir e po lic ie s e i the r

in o ne go , o r sm a ll tranches, 0

I: Jhttp://twlttermm/OutlookMoney; http://wwwfacebookcom/olmindi3

Yo ur c h ild 'is ,doing h e r b e st. Are you?

3 U 'n i qu eBene f it 5:

. ' L if e & i He 'a l th b ene f i t

. , P r em ium wa iv e r

. ' M a t u n ii ty b e n e f it

WDIFe

Life

< ~world"'ag~ http://d'gltal.outlookmoney.com .·10 AUGUST 2011 • OUTLOOK MONEY 17

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 20/76

I m ag in g : M A NO JI T D A TT A

""....tlOUTLOO:KMONEY .10 AUGUST 2011 • www.outlookmoney.com, ~ " wo rr <Mag s

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 21/76

1;·#4,1.1 Jobs & Careers 1 Enterprise I' Banking I Taxation I Insurance 'Investing 1 RealEstate' Financial PlannIng' Flipside I

BY PANKAJ ,ANUIPTOP,PO AND SUNIL DHIAWAN

Mobile phones are taking time andgeography out of your finances. Areyou networked into the revolution?

he humble mobile phone is no longer an

instrument just to make phone calls or

send messages to your near and dear

ones. In fact, with financial institutions

adopting t e c h n o l o g y j n a big way, the

mobile phone is an effective tool fo r

w e e l t h creation. The benefits of th emobile as a means for dissemination of

products and! services create a win-win situation both lor

the customers and financial institutions providing such ser-

vices. For institutions, it helps to reach out to a large set of

consumers at a lower cost. and for tndlvtduals it helps to

receive the latest information and carry out transactions at

their convenience. However, like aU other products and ser-

vic es , y ou w iU need to complete a few f o rmah t i e s before you

can avai.l these services on your mobile. Here we tell you

about all the wonders opened up through your mobile, and

what you need to do 00 avail those products and services.

BANKING

T o carry out mobile transactions and receive alerts on your

transactions on the mobile you . are only required to get your

mobilenumber

registered. Also, most credit card issuing

banks offer instant SMS a le rts on every transaction that you

make through your credit card ..

The Benefits. For one. you can bank anytime. anywhere.

Second, it is safe and secure, especially incases where the

ba nk o ff e rs se rvic es lik e fu nd tr a nsfe rs, Fo r example, :if yo u

lose your P I N , and enter the wrong P IN three times, then

the application wi l l lock i tself You will need to

get in touch with the customer care centre of

the b a n k to get itu n lo c k ed . 'T h is security

measure wilt however; work inyour favour

if you happen to lose your mobile. provided

you have signed out after completing your

last mobile transaction.

What's On Offer. There are a host of services

Y o u

can benkanywhere, and

it is as safe and

secure asNetbanking

< ~worldl'\ag~ http://drgital.outlookmQney.com.10 AUGUS'J 2011 • OUliLOOK MONEY t9

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 22/76

Cover Story----------

that banks offer under their mobile banking services. For the

m o re c o m m on o n e s, se e W e al th in Y ou r H a nd se t. Apart f r om

these. there are other things as wen that you can do through

m o bile b a n kin g. T h e sem c lu de fu nd s t r a n sf e r (within a n d

outside the bank). Interbank Mobile Payment Services

(IM I P S ), de m a t e n qu iry se rvic e . b il l payment (utility bi l ls ,credit cards, insurance premiums), donations. subscriptions,

m o bile to p-u p , a n d m -c o m m e rc e (to p-u p o f Tata Sky,B i gT \ 1 ,

Sunfnrect, DishTV counections and receiving recharge PINs

f o r D ig it a lTV o r V l de o co n d2h).

Mow To Get Started. In order to avail the services of mobile

banking, you w i ll n e ed to register your mobile ph on e w ith

the b a n k . Also. the registration process wi l l differ according

to th e se rv ic e s o ff er ed by the bank. In case th e b an k only

o ff e rs se rvic es lik e S M S a le rts . f ixe d d epo sit e nqu iry a nd so

011, through m o b il e b an k in g, then the registration process is

fairly s imp l e (see Ge tU n €J Mo b ile B cmkil' lf J) .

How e v e r ; if th e ba nk o ff e rs se rvic es like f u nd s tr a nsf e r a ndin te r-b an k m o b il e bill paym e nt se rvic es. th en yo u wi l l n e e d

to d o w nlo ad an app lic a tio n o n yo u r m o bil e ph o ne . Fo r

example, i f yo u want to avail mobile banldng services of

ICICI B a n k , you w1.11n e e d 1 :0 dow nlo ad the iM o bU e a p pl ic a -

tion, If yo u want to avail mob i l e banking services o f State

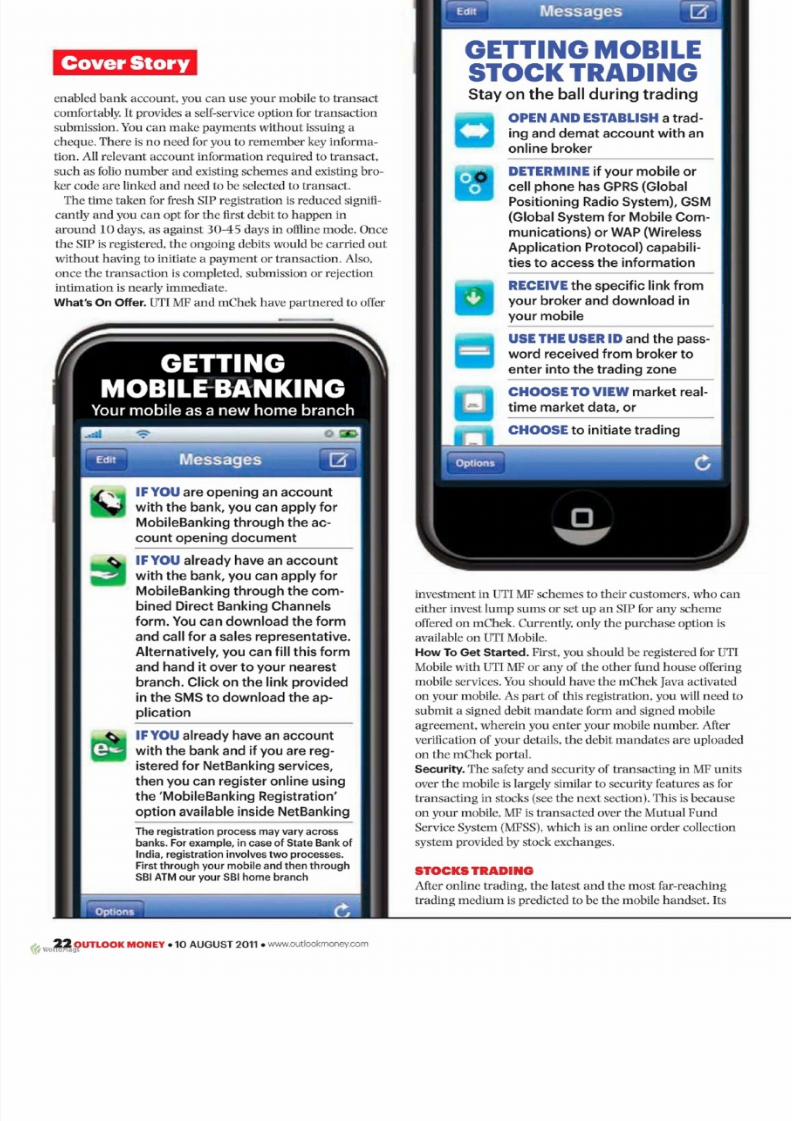

STOCKS Buy and sell stocks, track

orders, vliew market data,

MUTUAL I i=UND-SLumpsum or SIP

buyingl,.Redemption and switch-

ing facillities are in the offing

Transact View balance funds, pay

bills, place a stop payment on a

cheque, request a chequebook,

view an account statement and

present bills

Ulpdate Transaction alerts, check

last three transactions on your

prjrnarv account for MobileBank-

ing, cheque status inquiry, fixed

deposit inquiry, a Help menu

forms available on the website

(UTI MFBindBirla MF)and sub-

mit at their office

PROCESSAND ECSdebit man-

date verification is performed,

On receipt ofcontirmation ofs u ce e s e tu l m a n d ate re g iis tlr'a -

tion hom the investor's bank,

the services are activated, The

regist!ration process takes up to

25 days

F OR A LL S UC 'C ES S!F UL REGM

IISTRA:TIONS 8 1 link is sent to

download and install the appli-

cation on the phone

Bank of India, there are two processes-first through your

phone and then at an SSTATM or your SBr home branch.

The Rules. W h ile th e r e a r e a host of services t h a t you can

avail under mobile banking, there are certain restrictions

w ith r e ga rd to fu nd tr a n sf e r s. A s per R B I g uid e lin es. b an k s

are now permitted to offer mobile banking service to their

c usto m e rs su bje ct to a daily c a p of ~50.000 pe r c u sto m e r fo r

both f u n d s transfer and transactions involving purchase of

g oo d s o r se rvic e s. T r an sa ct io n s up to {S .OOO c a n b e facllltat-

ed by banks. without end-to-end encryption.

Security. In case you only receive instant SMS alerts from

your bank for the transactions that you do, then it will be in

your interest to delete them once you have read them. In

other cases. where the bank allows services funds transfer

through an application, am o ng th e f ir s t things that you n e e d

to do is sign out after you have completed your transaction.

MUTUAL FUNDS

Mobile MF transacttons m e re ly n ee d registra-

tion for an ECS or standing instructions factl-

ity. Currently. you may invest a lump sum

or start an SIP. but in future you m ay be

able to redeem, switch funds, and access

AVs on the phone. TJTI MF and Blrla MF

offer N I P services all mobile.

The Benefits. If you arc holding an ECS-

Mobile

mutual fund

transactions

need registration

for an ECSfacillity

"".... ..,nOUTLOOK IMONEY .10 AUGUST 20111. wwwoutlookmonevcom, ~ " w o r m ~ g s

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 23/76

Dre'am big with

S81 Student Loan!

< ~World~l.gs

0" Maximum loon of Rs.l0 lacs for

studies in Indio

I i1 Malxi'mum loon 'of Rs.20 lacs for

studies: abroad

ltr No processing fee

o Simple interest during morotorium/

repayment holiday

01 % int,erest rate concession for

serv ic ing in te r e s f d lu ! rin g

morotorium/repcyment hoHdoy

IZ I Repayment up to 7 years

o Repayment srcrts 1 y eQ l r ofter

com pletion of course Of 6 months after

getting job, whichever is earlier

o No security for loan upto RsA lees and

only parent! guardian as co-borrower

o No margin for loans upto RsA lacs

o Loans above RsA lacs, 5% margin for

studies in Indio & 15% for studies

abroad

I i 1 Online registration o,f lioon

StadeL"all

24x7 Helpline: 18004253800 (Tollfiree from BSNUMTNL landllines/mobil'e nos.) orVlslt www.sbi ..ee.ln o:r

Email: contactcentre@slbtcoJn

5/9/2018 Outlook_Money_Augest_2011 - slidepdf.com

http://slidepdf.com/reader/full/outlookmoneyaugest2011 24/76

Cover Story- - -----

enabled bank account, yon can use your mobile to transact

comfortably; Itprovides a self-service option for transaction

submission. You can make payments without issuing a

c h equ e. T he re is n o need f o r yo u to rem em be r k e y in fo rm a -

tion. A ll relevant account information required to transact.

su ch a s fo lio n um be r and e xistin g sc he m es a n d e xistin g b ro -ker code are linked and need to be selected to transact.

T he tim e ta k en fo r f r e sh S IP re gistr a tio n is r e d uc ed sig n lf i-

cantly and you can opt for the first debit to happen in

a ro u n d 10 d ays, a s a ga in st 30 -4 5 d ays in om in e m od e . O n c e

the S]F is registered, the ongoing debits would be carried out

w ith o u t h avin g to in it ia te a paym e n t o r tra n sa c t io n . A lso .

once the transaction is completed. su bm issio n o r r e je ctio n

i n t ima t i o n is n ea r ly im m e d ia te ..

W h at 's O n O ffe r . U T I M F and mC h e k have pa r tn er e d to o ff e r

IF YOU are opening an account

with the bank, you can apply for

MobileBanking through the ac-count opening document

IF YOU already have an account

with the bank, you can apply for

MobileBanking through the corn-

bmed Direct Banking Channels

form. You can download the form

and call for a sales representative,

Alternatively, you can fill this form

and hand it over to your nearest

branch. Click on the link provided

in the 8M8 to download the ap-p!li:cation

IF YOU already have an account

with the bank and i f you are reg-

lstered for NetBanking services,

then you can register online using

the 'MolbileBanking R'egistration'

option available inside NetBanking

The registration process may vary acrossbanks. For example, in case of State Bank ofIndia. registration involves two processes.Firstthrough your mobile and then through

S!BIATMour your SBI home branch

"".... "" OUiI'LOO'K MONEY .10 AUGUS12011 • www.outlookmoneycorn\I~wolTll~gr