Outlook for the U.S. Livestock and Poultry Sectors in 2011 Presented By Shayle D. Shagam World...

47

Outlook for the U.S. Livestock and Poultry Sectors in 2011 Presented By Shayle D. Shagam World Agricultural Outlook Board, USDA USDA Outlook Forum Washington, D.C. February 25, 2011

-

Upload

maryann-oconnor -

Category

Documents

-

view

218 -

download

1

Transcript of Outlook for the U.S. Livestock and Poultry Sectors in 2011 Presented By Shayle D. Shagam World...

Outlook for the U.S. Livestock and Poultry

Sectors in 2011

Presented By

Shayle D. Shagam

World Agricultural Outlook Board, USDA

USDA Outlook Forum

Washington, D.C.

February 25, 2011

Situation Facing Livestock and Poultry Producers in 2011

• Higher feed prices– Corn: $5.05-$5.75/bu in 2010/11

$3.55 in 2009/2010 – Soybean meal: $340-380/ton in 2010/11

$311 in 2009/2010

• Shrinking returns

Higher Feed Bites into Gains from Livestock and Poultry Prices

0

10

20

30

40

50

60

2001 2003 2005 2007 2009 2011*

Rat

io

Cattle/Corn Hog/Corn Broiler/Feed* Forecast

Highlights for Livestock & Poultry in 2011

• Offsetting meat production– Beef, lamb, and turkey lower– Pork and broilers higher

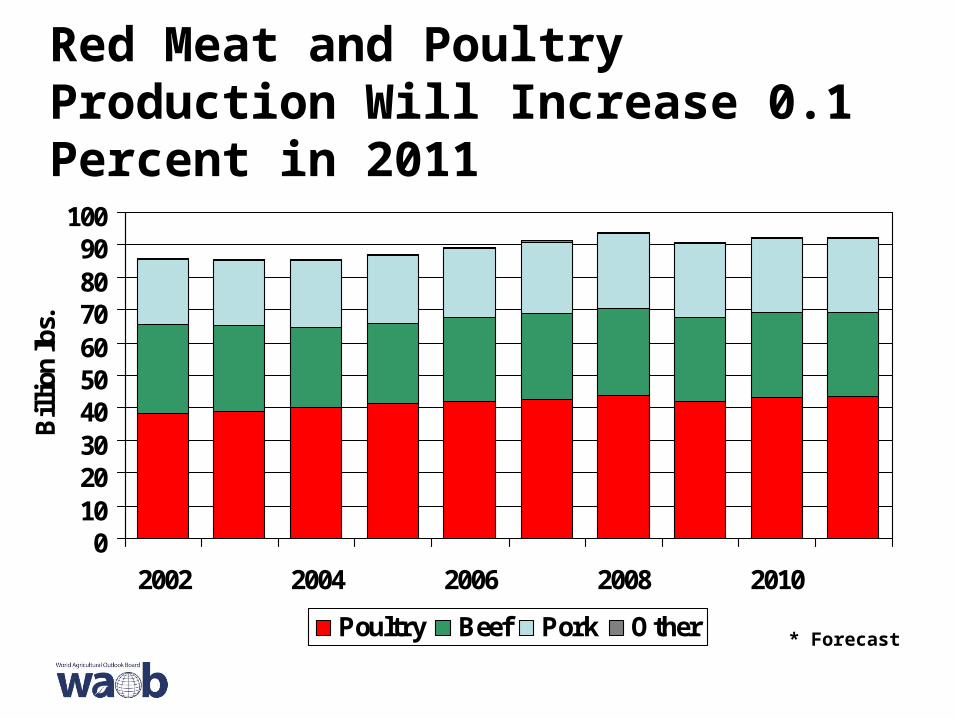

Red Meat and Poultry Production Will Increase 0.1 Percent in 2011

0102030405060708090

100

2002 2004 2006 2008 2010

Bil

lion

lbs.

Poultry Beef Pork Other * Forecast

Highlights for Livestock & Poultry in 2011

• Offsetting meat production

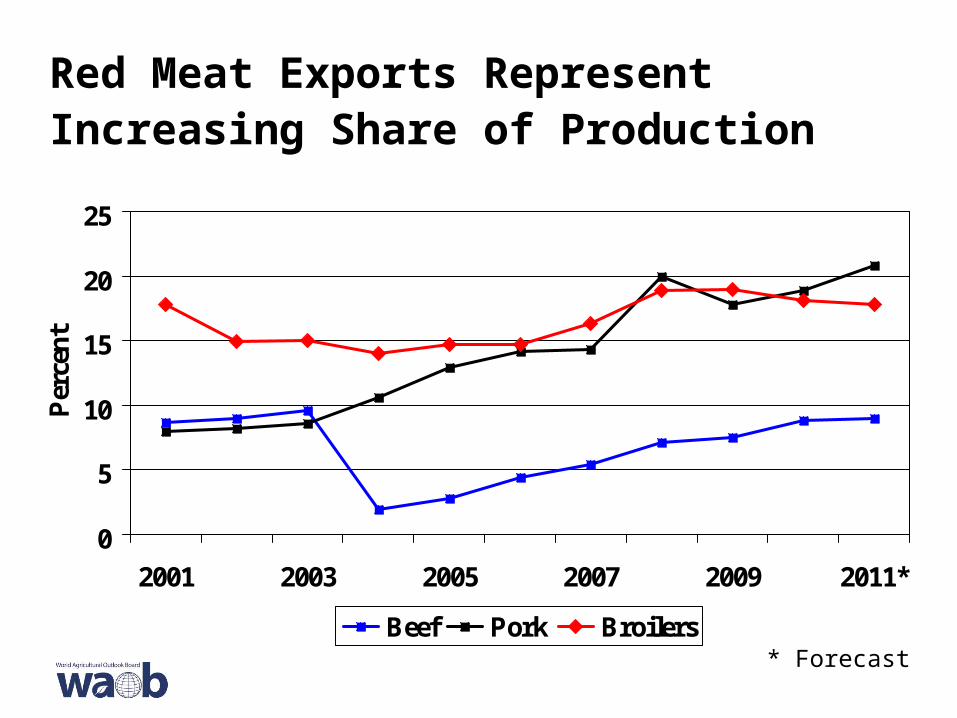

• Stronger red meat exports but weaker broiler exports

Support for Exports

• Rising incomes fuel increased demand for meat protein. – World GDP, less U.S., at about 3-4 percent in

2011

• Weaker U.S. dollar will support meat exports.

• Trade issues remain irritants– Pork issues resolved– BSE restrictions remain– Poultry issues

Red Meat Exports Represent Increasing Share of Production

0

5

10

15

20

25

2001 2003 2005 2007 2009 2011*

Per

cen

t

Beef Pork Broilers* Forecast

Highlights for Livestock & Poultry in 2011

• Offsetting meat production

• Stronger red meat exports but weaker broiler exports

• Domestic supply impacts mixed– Larger broiler meat net supplies– Smaller beef, pork, and turkey net supplies

• Gradual economic improvement– U.S. GDP growth about 3 percent– Unemployment gradually declining

Total Per Capita Retail Basis Meat Disappearance in 2011 at 207 Pounds

40

50

60

70

80

90

Pou

nds

per

capi

ta

Beef Pork Broilers* Forecast

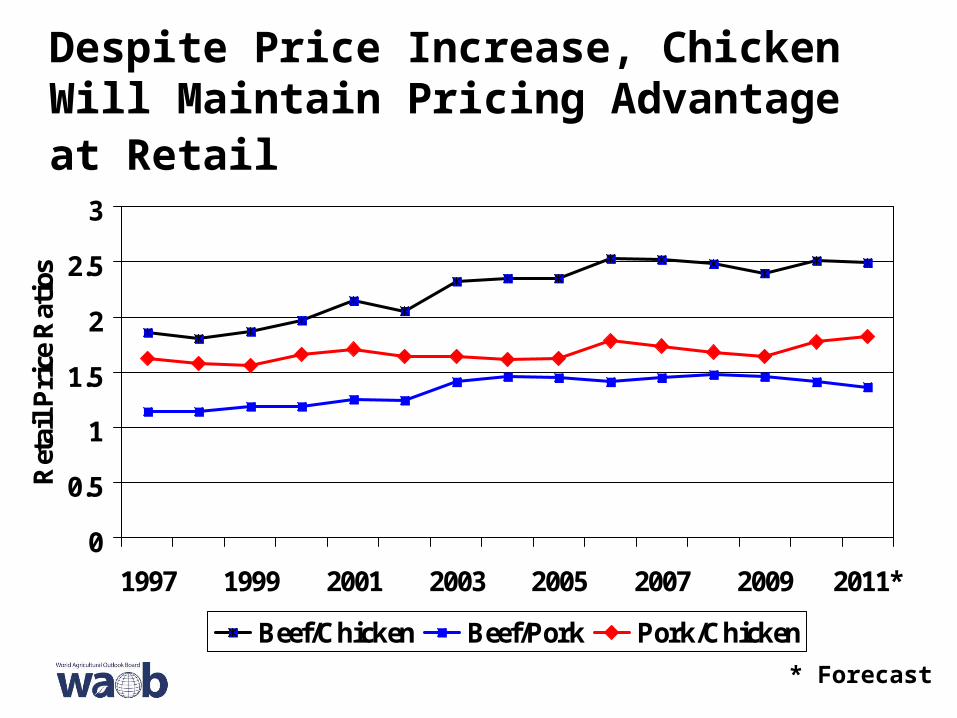

Despite Price Increase, Chicken Will Maintain Pricing Advantage at Retail

0

0.5

1

1.5

2

2.5

3

1997 1999 2001 2003 2005 2007 2009 2011*

Ret

ail P

rice

Rat

ios

Beef/Chicken Beef/Pork Pork/Chicken

* Forecast

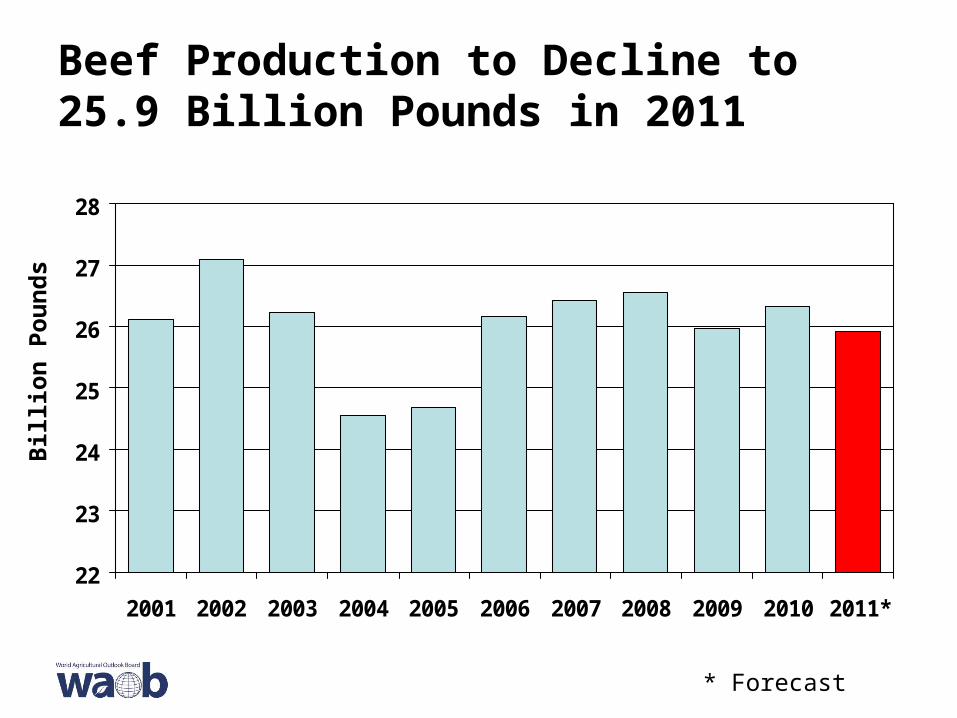

Beef Production to Decline to 25.9 Billion Pounds in 2011

22

23

24

25

26

27

28

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Bil

lio

n P

ou

nd

s

* Forecast

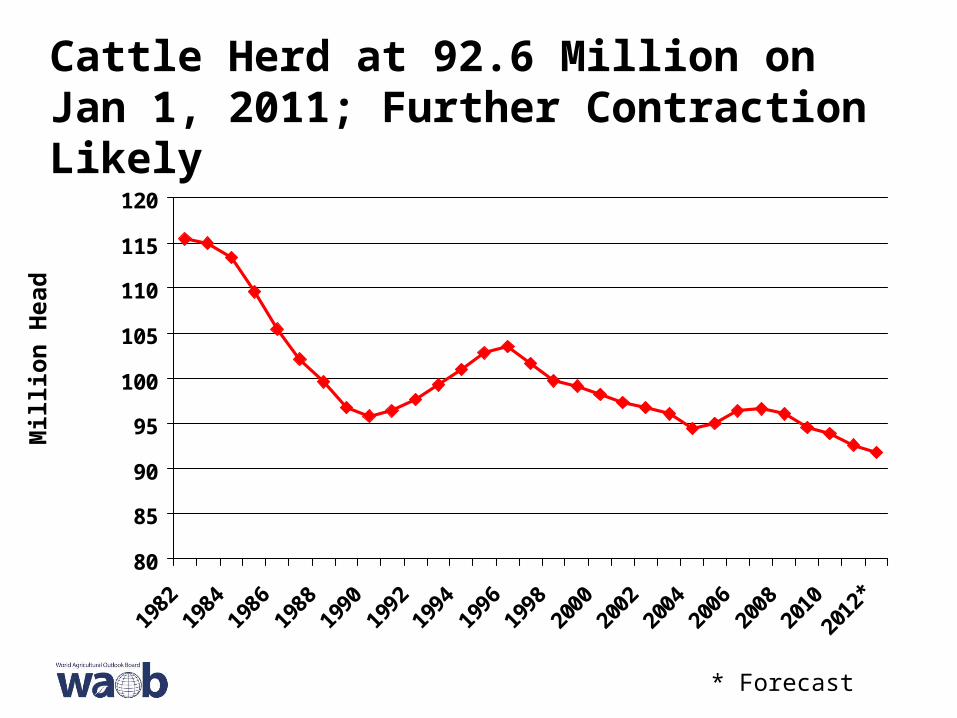

Cattle Herd at 92.6 Million on Jan 1, 2011; Further Contraction Likely

80

85

90

95

100

105

110

115

120

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

*

Mil

lio

n H

ead

* Forecast

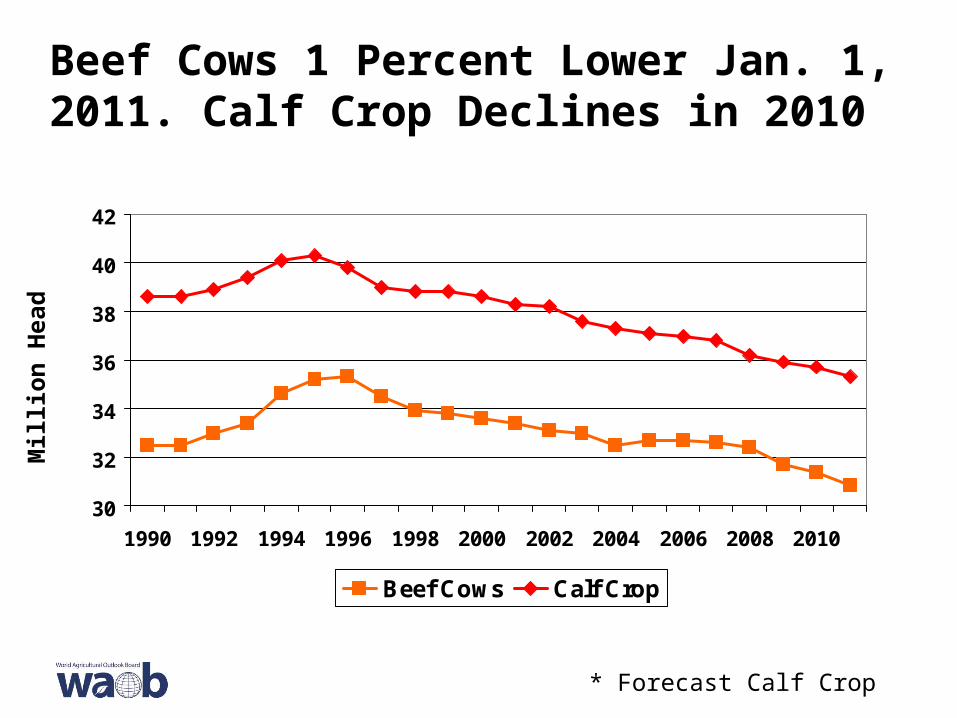

Beef Cows 1 Percent Lower Jan. 1, 2011. Calf Crop Declines in 2010

30

32

34

36

38

40

42

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Beef Cows Calf Crop

Mil

lio

n H

ead

* Forecast Calf Crop

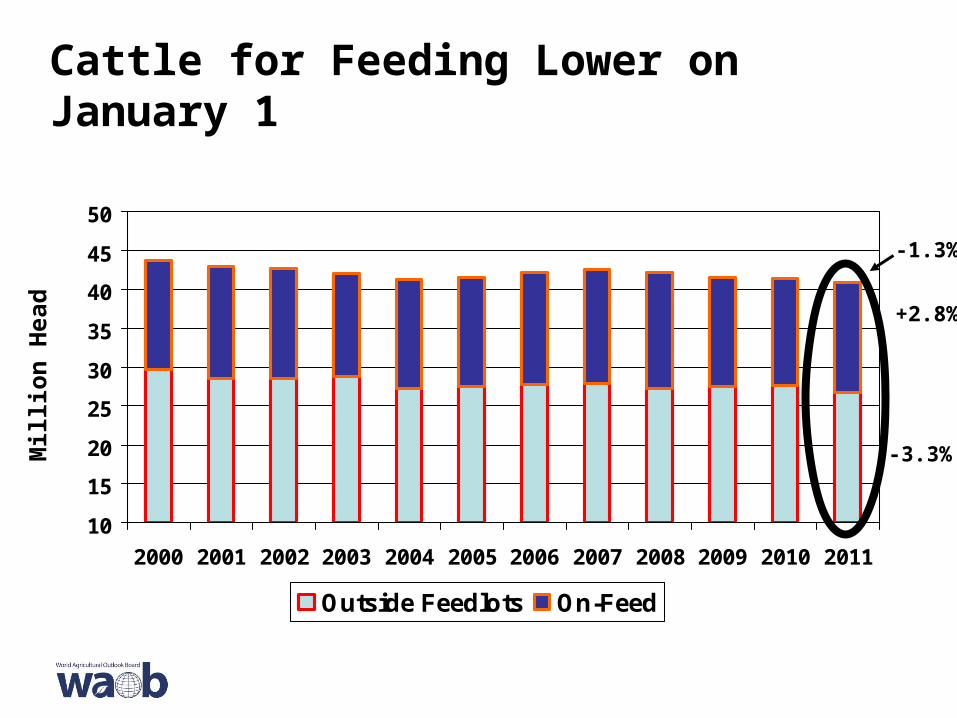

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Outside Feedlots On-Feed

Cattle for Feeding Lower on January 1M

illi

on

Hea

d

-3.3%

+2.8%

-1.3%

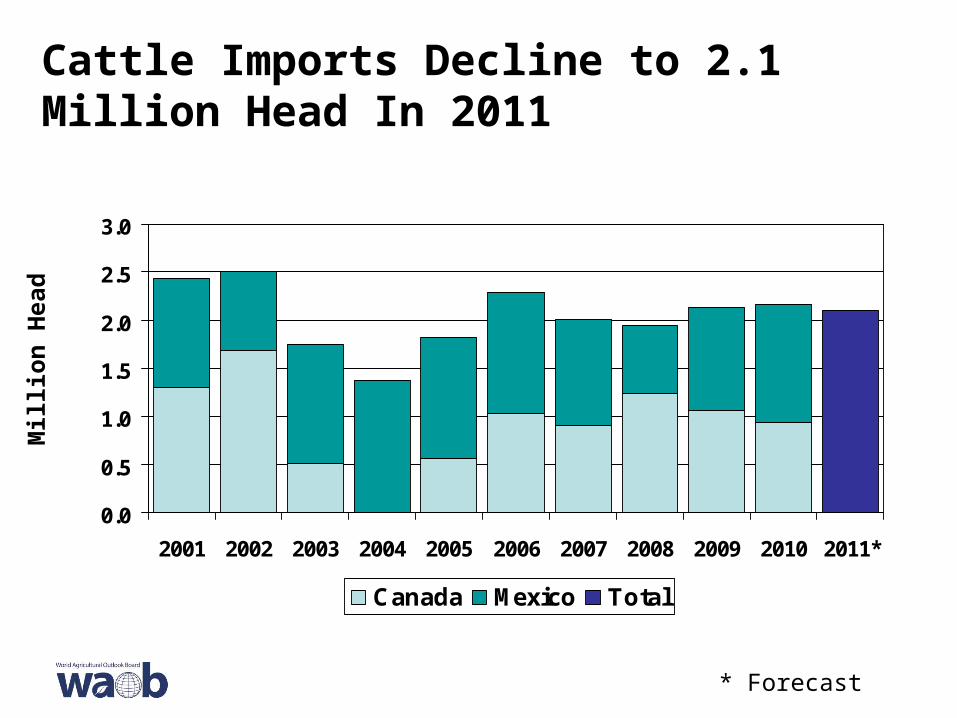

Cattle Imports Decline to 2.1 Million Head In 2011

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Canada Mexico Total

* Forecast

Mil

lio

n H

ead

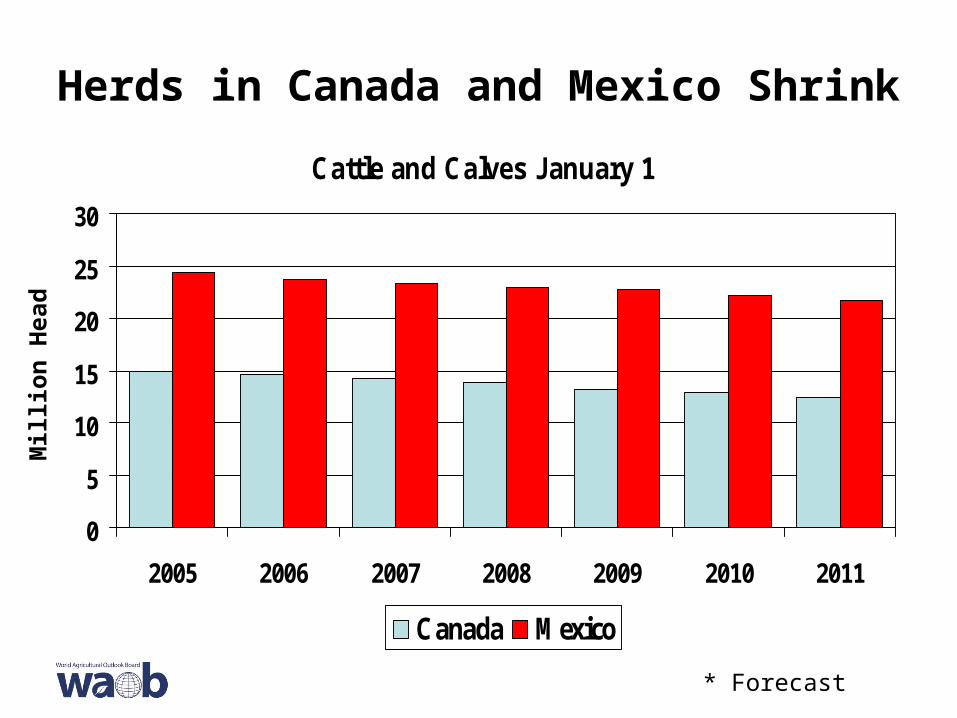

Herds in Canada and Mexico Shrink

Cattle and Calves January 1

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011

Canada Mexico

Mil

lio

n H

ead

* Forecast

Average Cattle Carcass Weights Recover to Near Record in 2011

720

730

740

750

760

770

780

790

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

* Forecast

Po

un

ds

Beef Exports Increase 2 Percent to 2.4 Billion Pounds

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Exports

* Forecast

Bil

lio

n P

ou

nd

s

2011 Exports Remain Below 2003

0.0

0.5

1.0

1.5

2.0

2.5

2005 2006 2007 2008 2009 2010 2011*

Bil

lio

n p

ou

nd

s

Mexico Canada Japan South Korea Vietnam Other

* Forecast

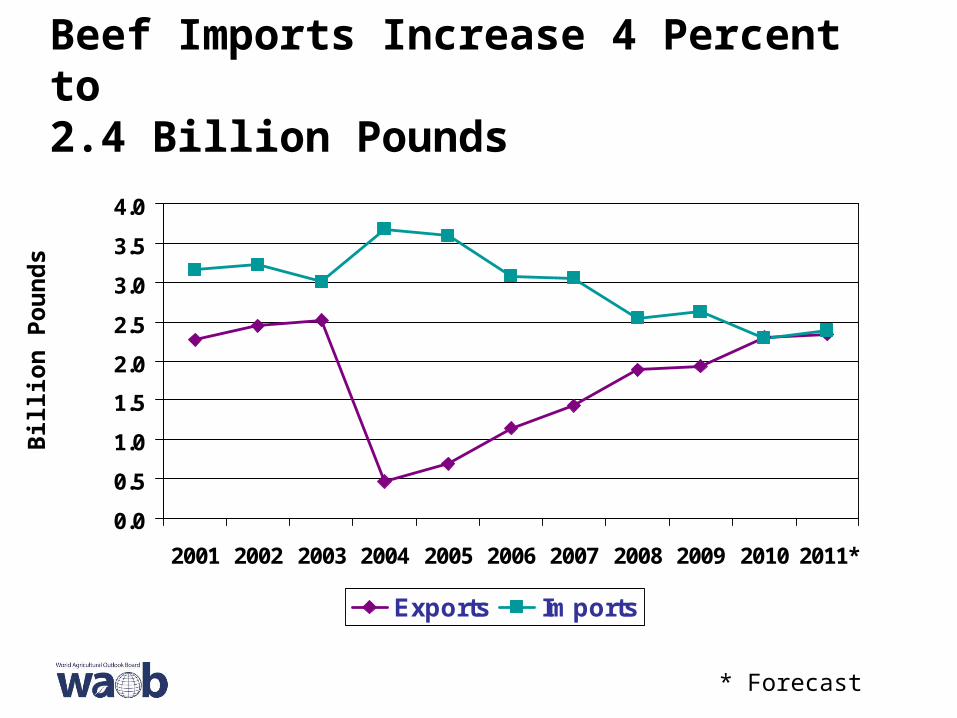

Beef Imports Increase 4 Percent to 2.4 Billion Pounds

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Exports Imports

* Forecast

Bil

lio

n P

ou

nd

s

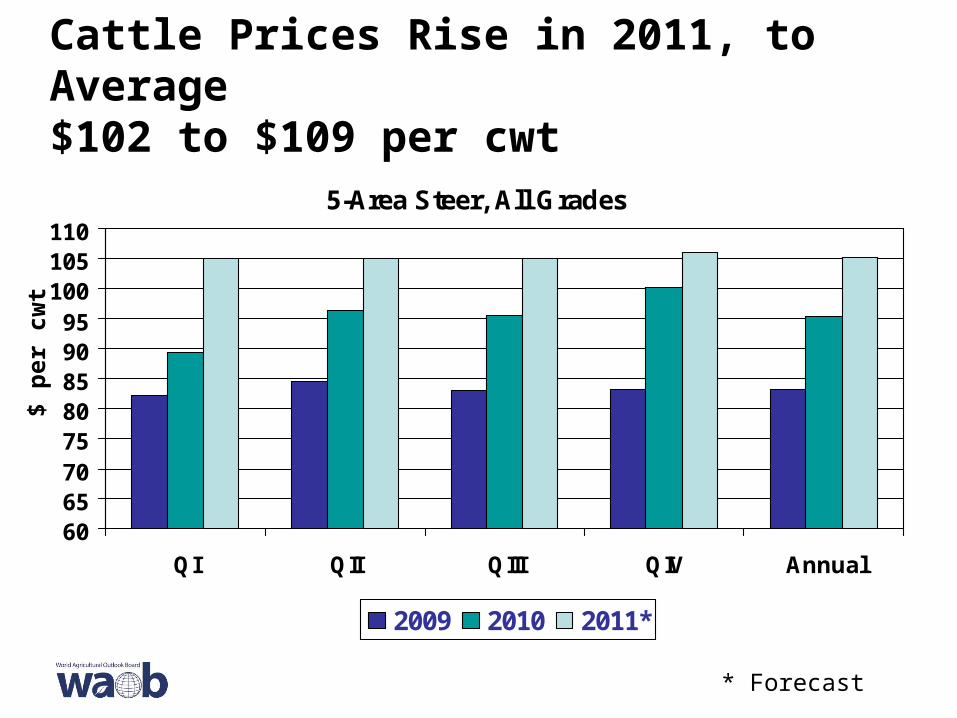

Cattle Prices Rise in 2011, to Average$102 to $109 per cwt

5-Area Steer, All Grades

6065707580859095

100105110

QI QII QIII QIV Annual

2009 2010 2011*

* Forecast

$ p

er c

wt

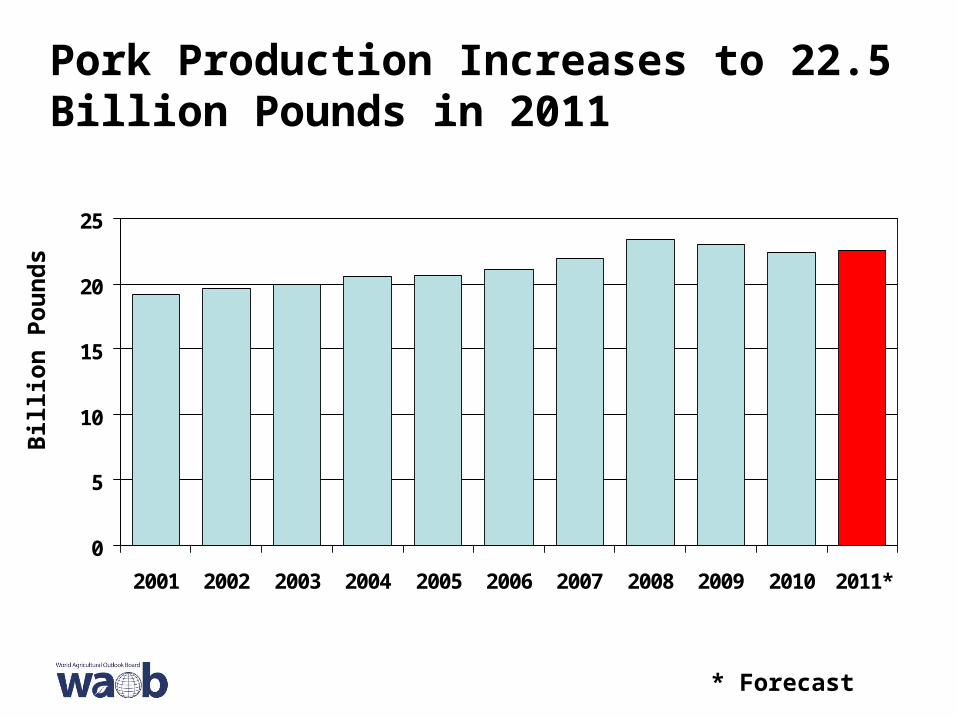

Pork Production Increases to 22.5 Billion Pounds in 2011

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

* Forecast

Bil

lio

n P

ou

nd

s

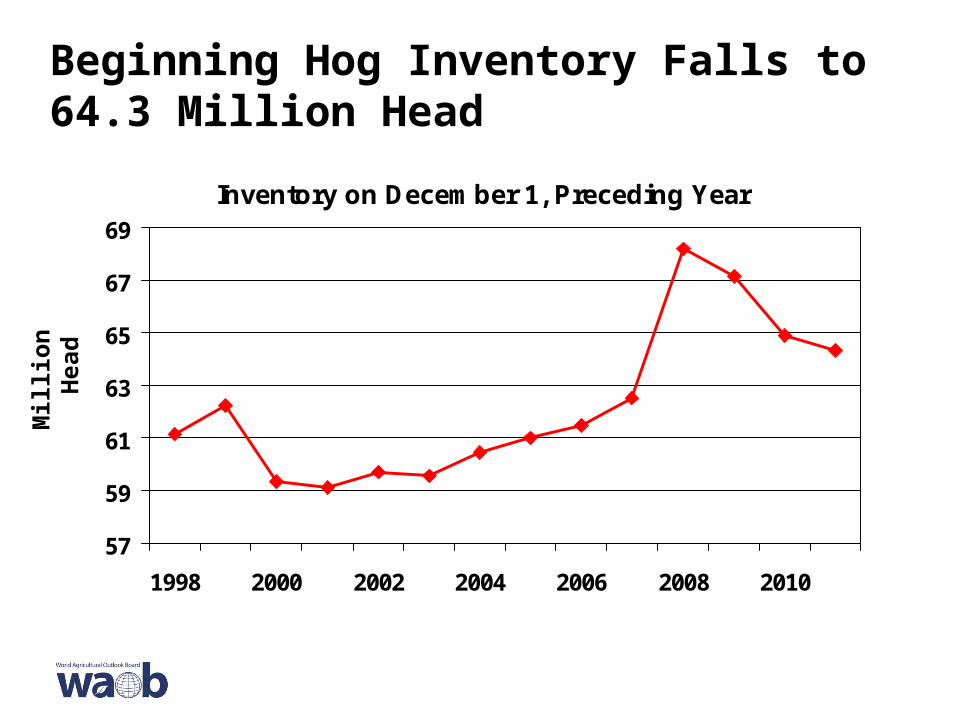

Beginning Hog Inventory Falls to 64.3 Million Head

Inventory on December 1, Preceding Year

57

59

61

63

65

67

69

1998 2000 2002 2004 2006 2008 2010

Mil

lio

n H

ead

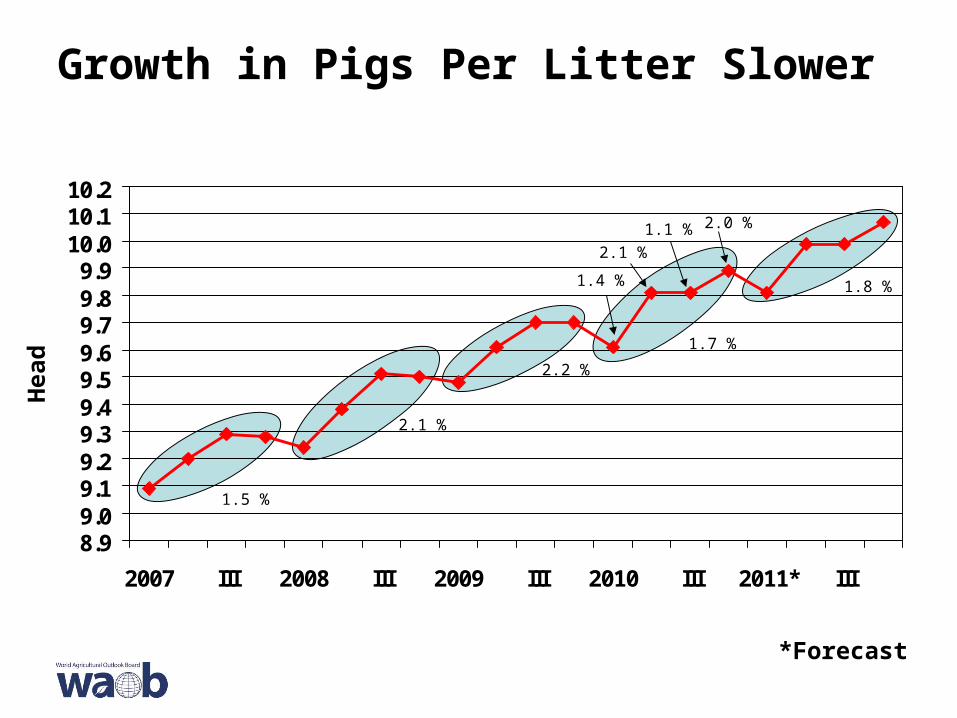

Sows Farrowing Expected to Stabilize in Late 2011

2.5

2.6

2.7

2.8

2.9

3.0

3.1

QI QII QIII QIV

2009 2010 2011*

* Quarters 1-2 NASS Reported , Quarters 3-4 Forecast

Mil

lio

n H

ead

-0.6%-2.3% -0.6%

+0.1%

8.99.09.19.29.39.49.59.69.79.89.9

10.010.110.2

2007 III 2008 III 2009 III 2010 III 2011* III

Growth in Pigs Per Litter Slower

*Forecast

Hea

d

2.2 %

1.7 %

1.5 %

2.1 %

1.8 %

2.1 %

1.1 % 2.0 %

1.4 %

Hog Imports at 5.8 Million Head in 2011

0

2

4

6

8

10

12

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Feeders Other Total

* Forecast

Mil

lio

n H

ead

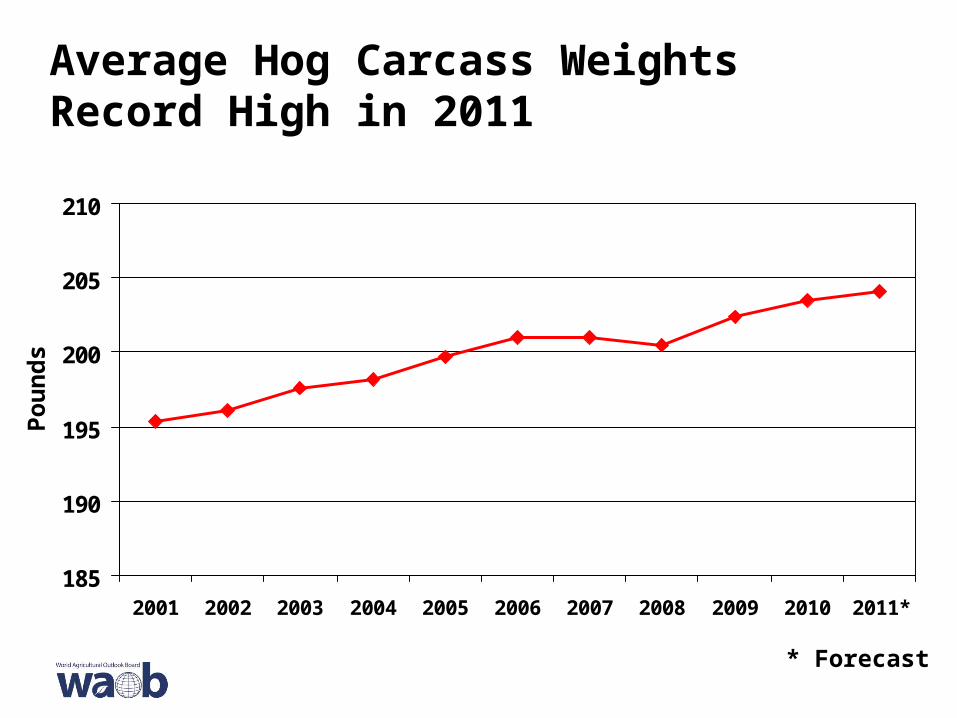

Average Hog Carcass Weights Record High in 2011

185

190

195

200

205

210

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

* Forecast

Po

un

ds

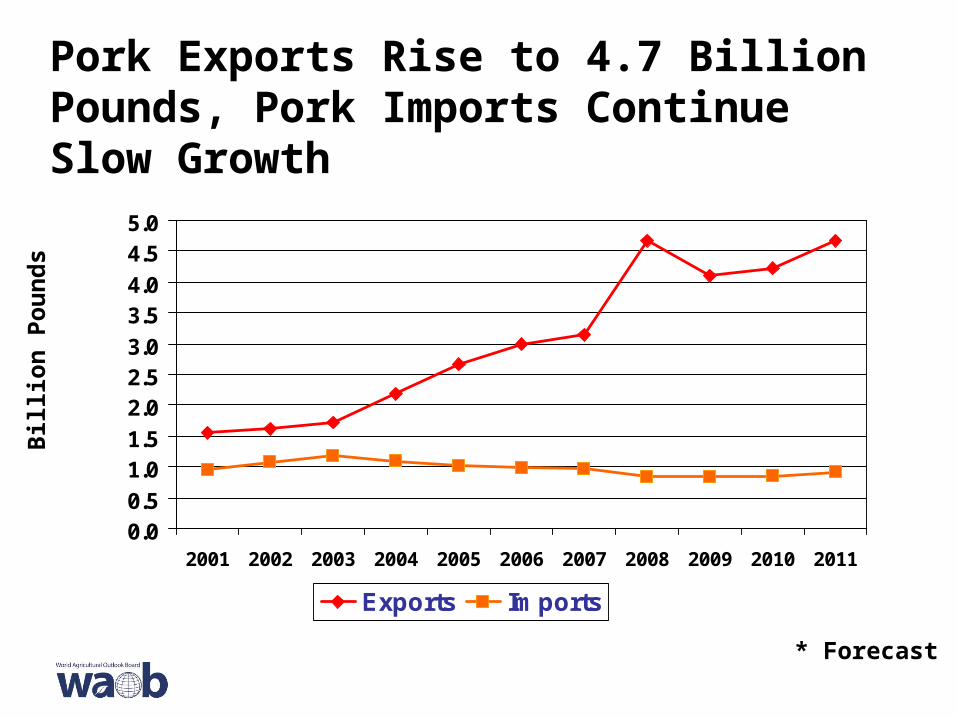

Pork Exports Rise to 4.7 Billion Pounds, Pork Imports Continue Slow Growth

0.00.5

1.01.5

2.02.53.0

3.54.0

4.55.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Exports Imports

* Forecast

Bil

lio

n P

ou

nd

s

2011 Pork Exports Record High

00.5

11.5

22.5

33.5

44.5

5

2005 2006 2007 2008 2009 2010 2011*

Bil

lio

n l

bs.

Japan Mexico Canada South Korea China/H.K. Other

* Forecast

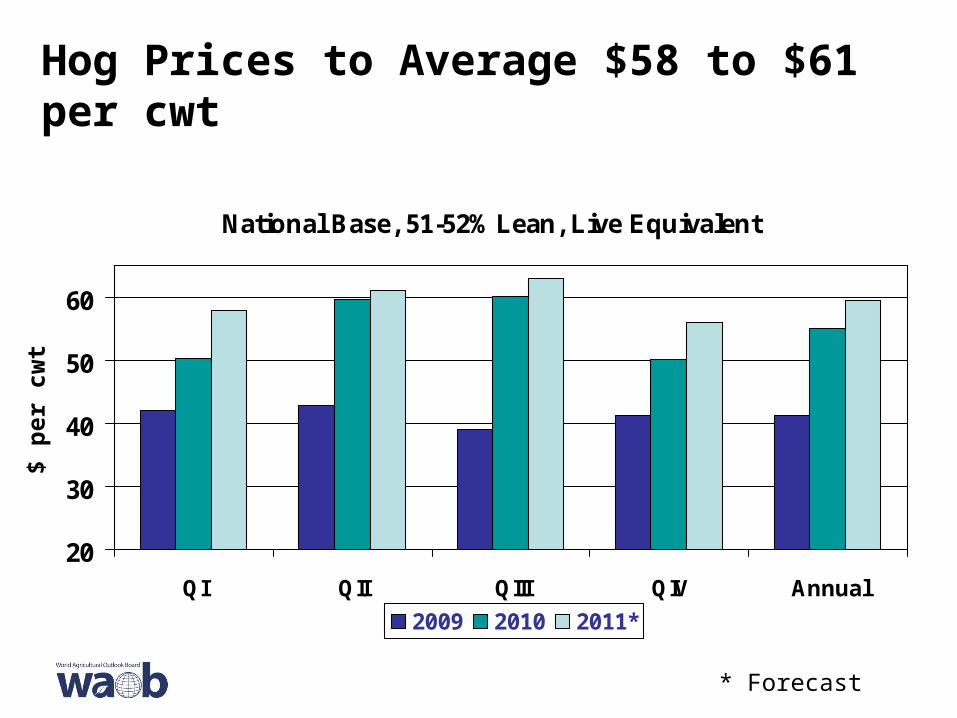

Hog Prices to Average $58 to $61 per cwt

National Base, 51-52% Lean, Live Equivalent

20

30

40

50

60

QI QII QIII QIV Annual

2009 2010 2011*

* Forecast

$ p

er c

wt

Broiler Meat Production Record High in 2011

15

20

25

30

35

40

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

*

Bil

lio

n l

bs.

* Forecast

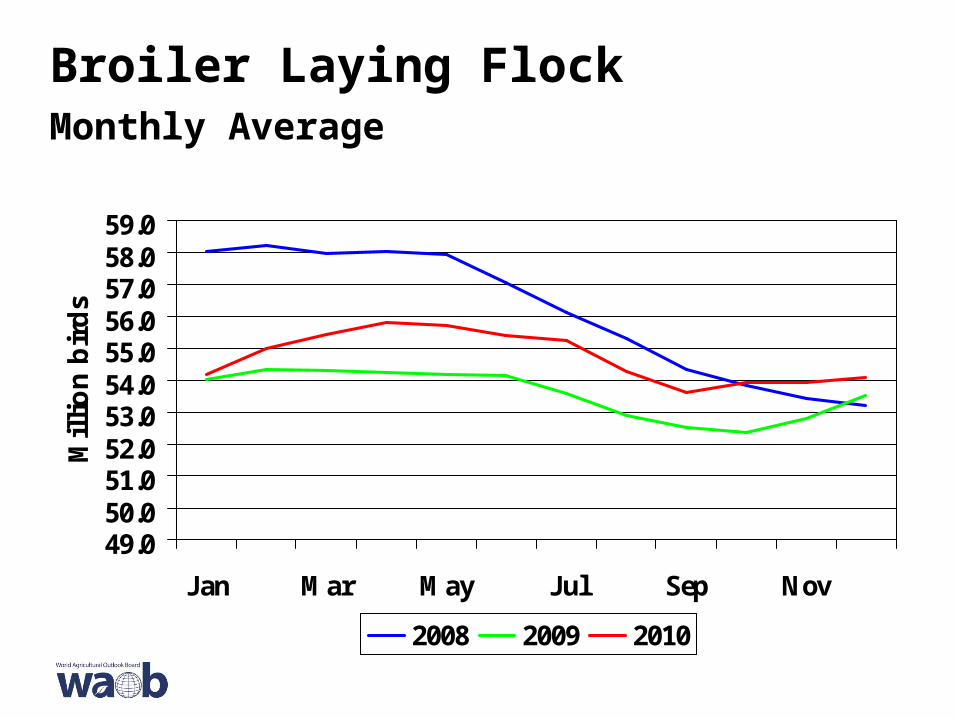

Broiler Laying FlockMonthly Average

49.050.051.052.053.054.055.056.057.058.059.0

Jan Mar May Jul Sep Nov

Mil

lio

n b

ird

s

2008 2009 2010

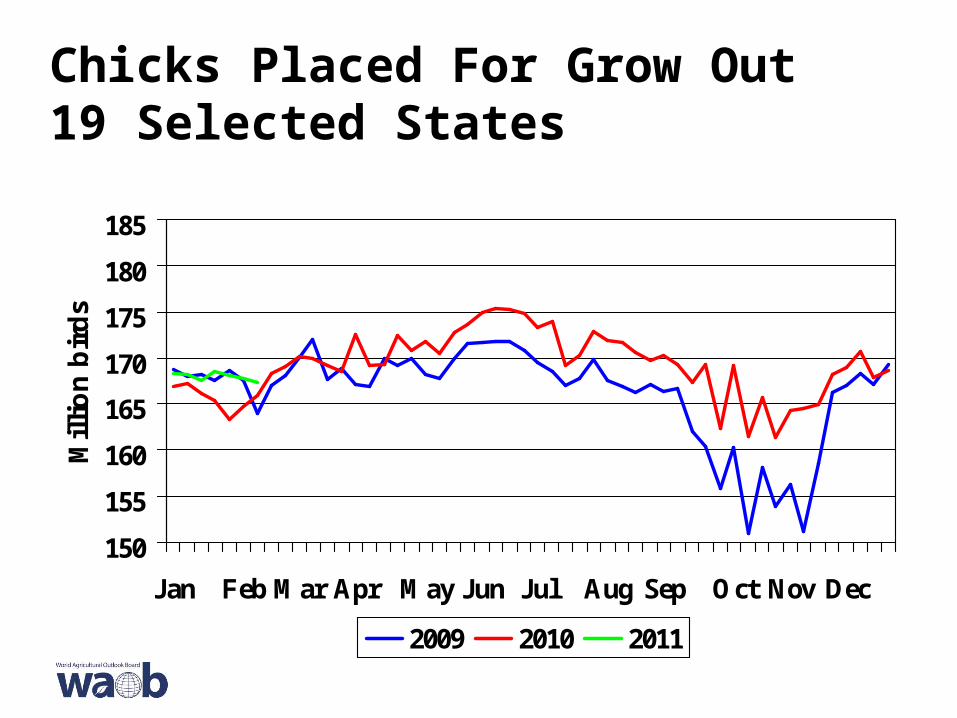

Chicks Placed For Grow Out19 Selected States

150

155

160

165

170

175

180

185

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mil

lio

n b

ird

s

2009 2010 2011

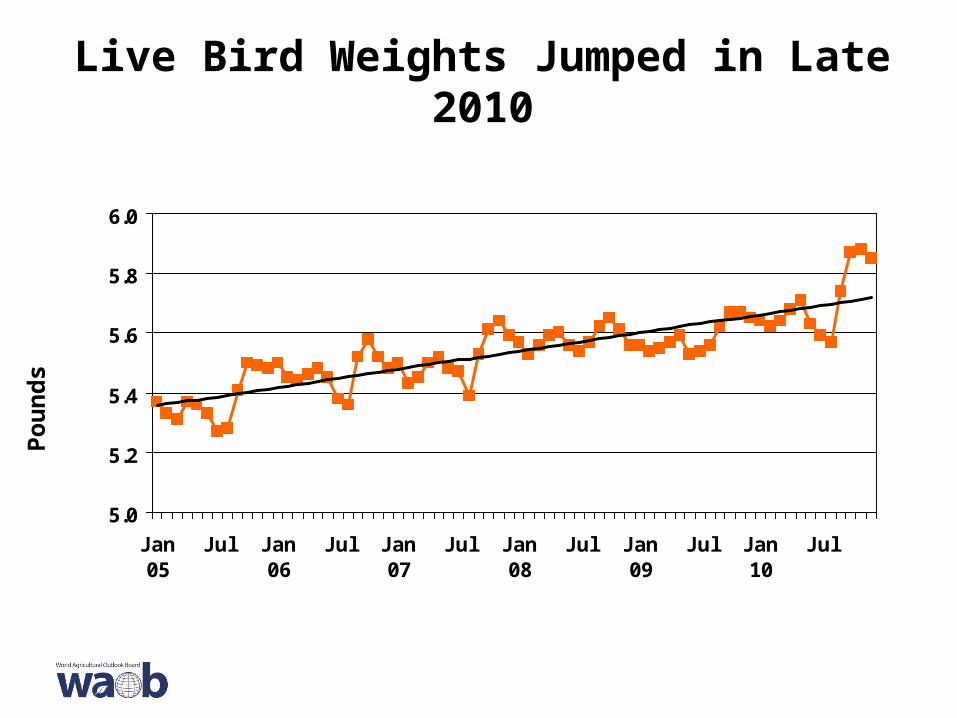

Live Bird Weights Jumped in Late 2010

5.0

5.2

5.4

5.6

5.8

6.0

Jan05

Jul Jan06

Jul Jan07

Jul Jan08

Jul Jan09

Jul Jan10

Jul

Po

un

ds

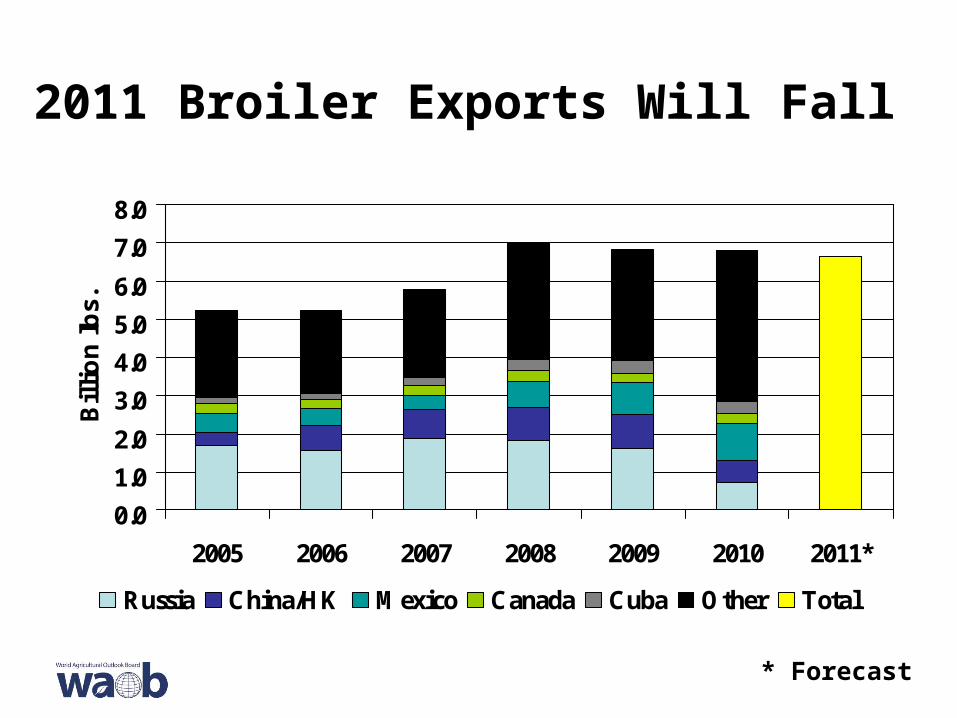

2011 Broiler Exports Will Fall

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

2005 2006 2007 2008 2009 2010 2011*

Bil

lio

n l

bs.

Russia China/HK Mexico Canada Cuba Other Total

* Forecast

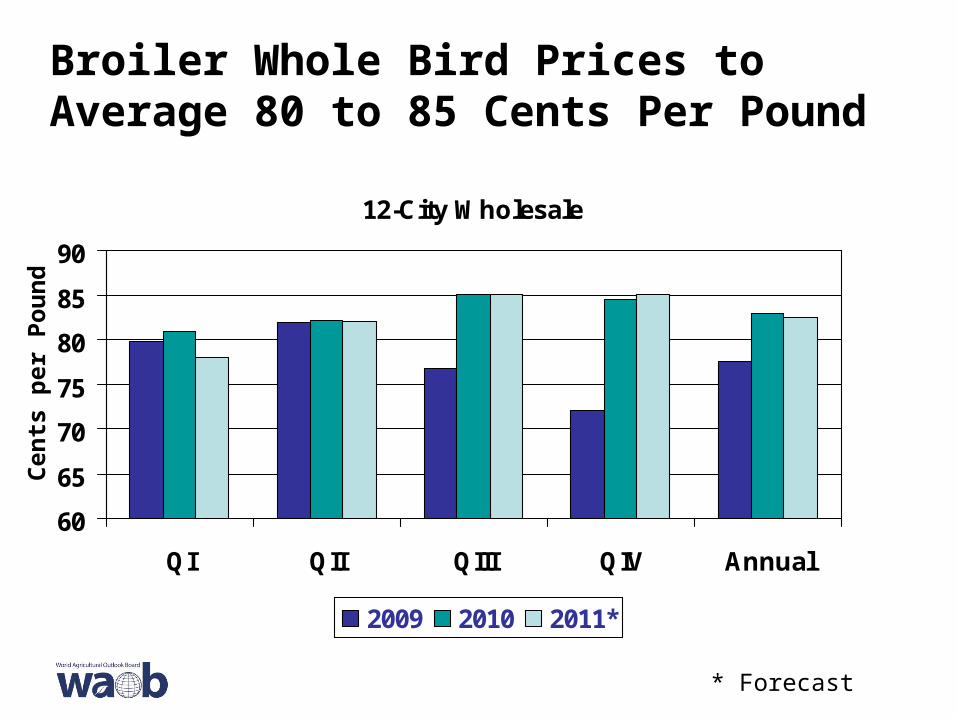

Broiler Whole Bird Prices to Average 80 to 85 Cents Per Pound

12-City Wholesale

60

65

70

75

80

85

90

QI QII QIII QIV Annual

2009 2010 2011*

* Forecast

Cen

ts p

er P

ou

nd

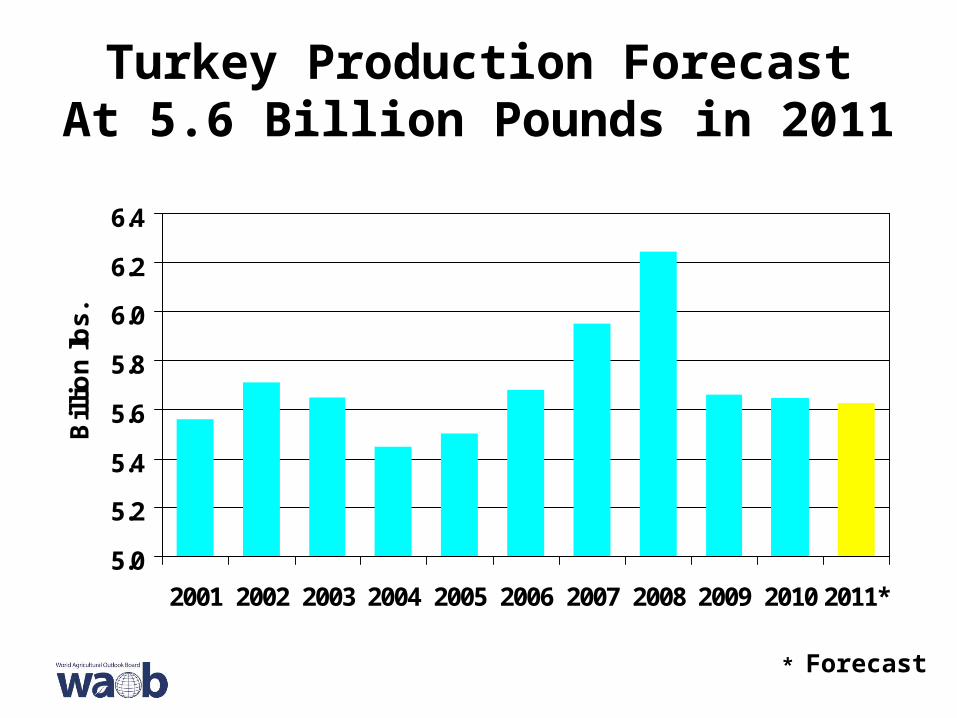

Turkey Production ForecastAt 5.6 Billion Pounds in 2011

5.0

5.2

5.4

5.6

5.8

6.0

6.2

6.4

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Bil

lio

n l

bs.

* Forecast

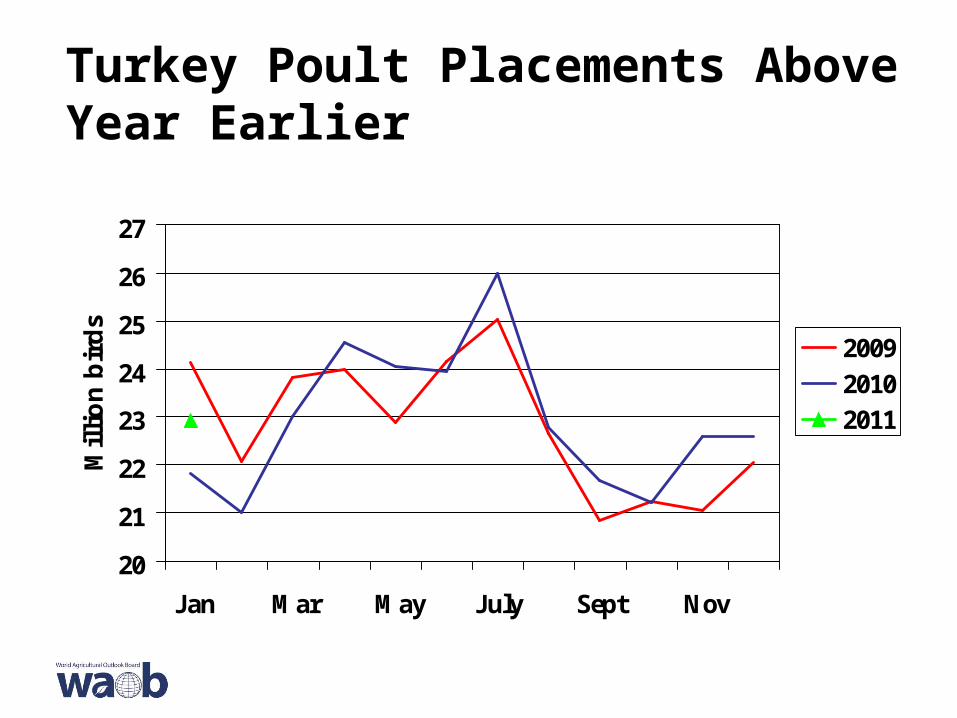

Turkey Poult Placements AboveYear Earlier

20

21

22

23

24

25

26

27

Jan Mar May July Sept Nov

Mil

lio

n b

ird

s

2009

2010

2011

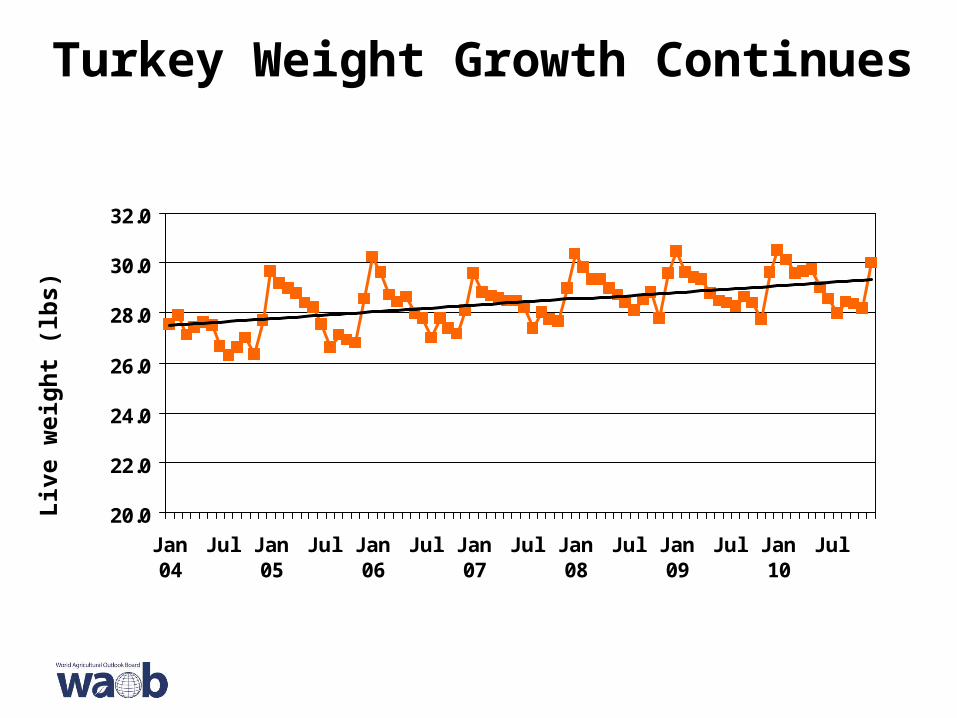

Turkey Weight Growth Continues

20.0

22.0

24.0

26.0

28.0

30.0

32.0

Jan04

Jul Jan05

Jul Jan06

Jul Jan07

Jul Jan08

Jul Jan09

Jul Jan10

Jul

Liv

e w

eig

ht

(lb

s)

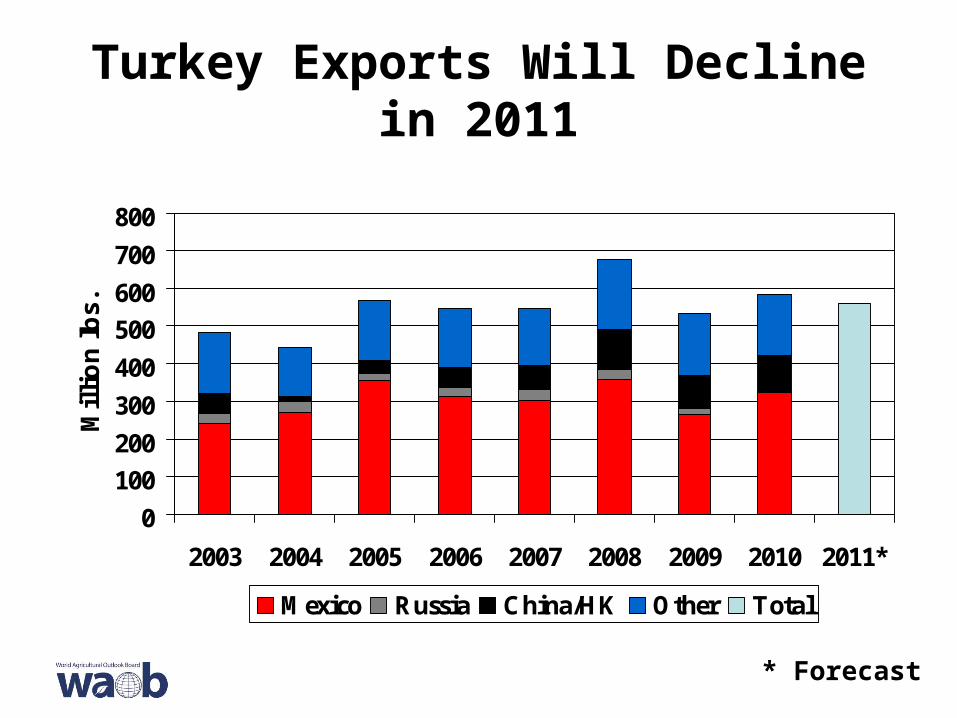

Turkey Exports Will Decline in 2011

0

100

200

300

400

500

600

700

800

2003 2004 2005 2006 2007 2008 2009 2010 2011*

Mil

lio

n l

bs.

Mexico Russia China/HK Other Total

* Forecast

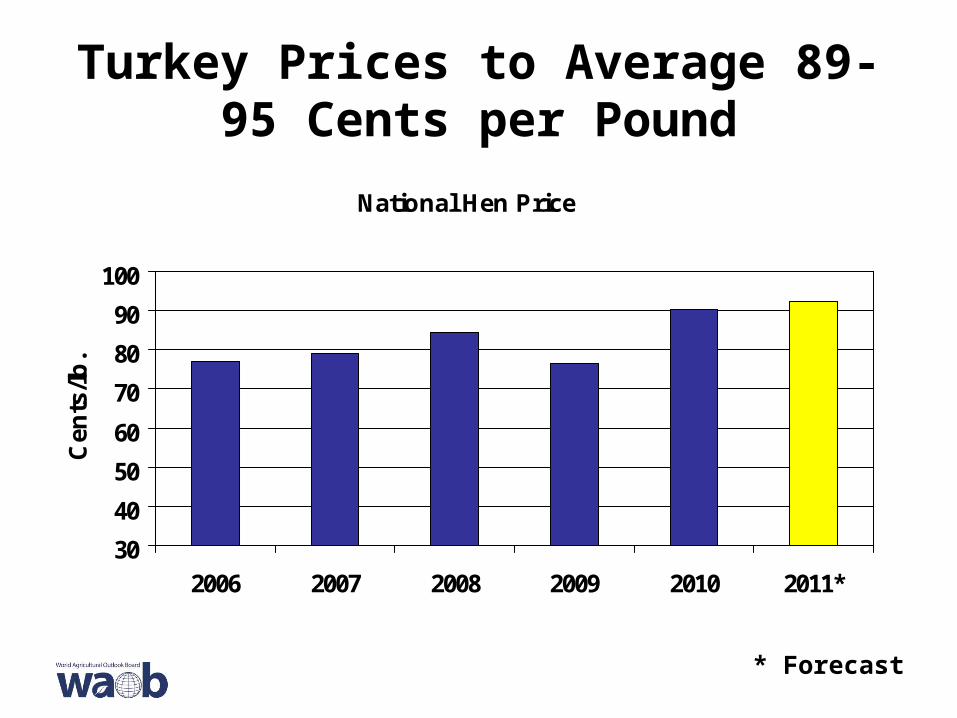

Turkey Prices to Average 89-95 Cents per Pound

National Hen Price

30

40

50

60

70

80

90

100

2006 2007 2008 2009 2010 2011*

Cen

ts/l

b.

* Forecast

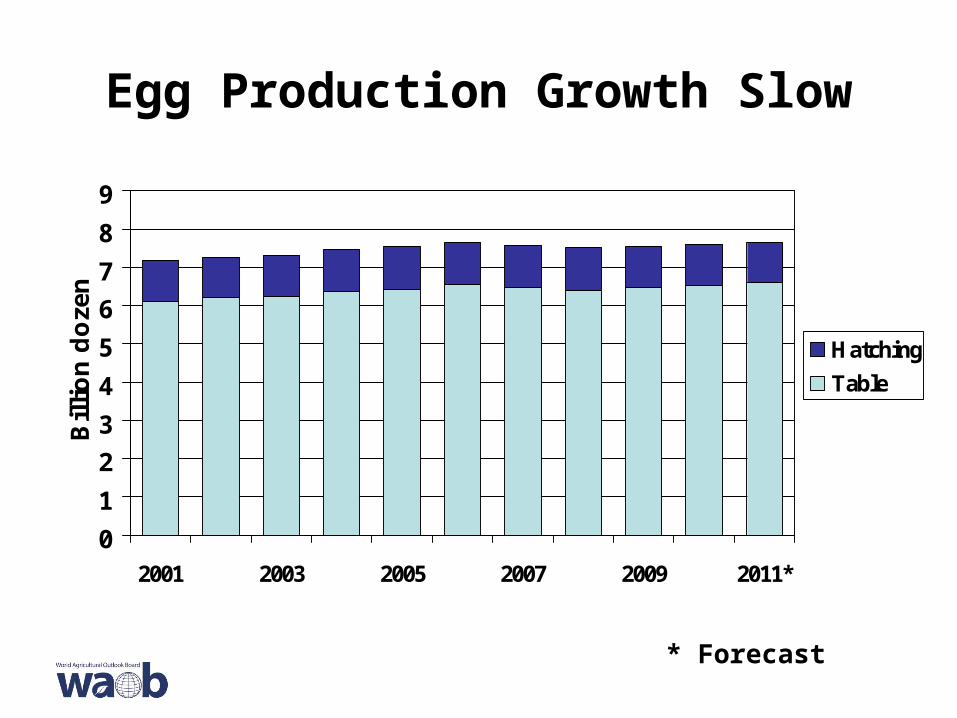

Egg Production Growth Slow

0

1

2

3

4

5

6

7

8

9

2001 2003 2005 2007 2009 2011*

Bil

lio

n d

oze

n

Hatching

Table

* Forecast

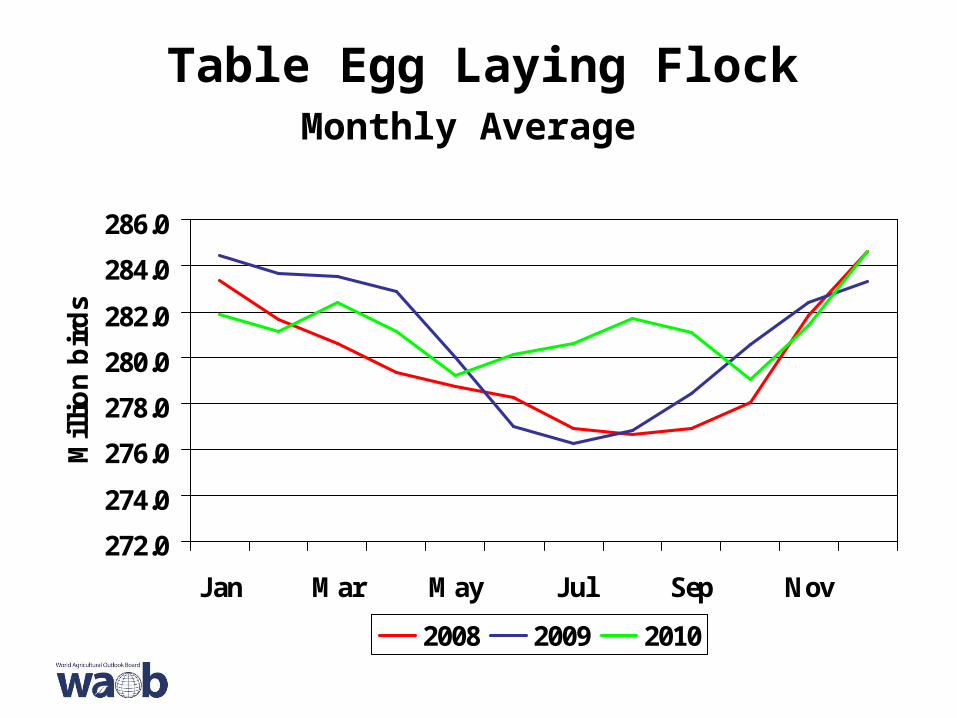

Table Egg Laying FlockMonthly Average

272.0

274.0

276.0

278.0

280.0

282.0

284.0

286.0

Jan Mar May Jul Sep Nov

Mil

lio

n b

ird

s

2008 2009 2010

Egg Prices Will Decline

N.Y. Wholesale Price - Large Eggs

30405060708090

100110120130140

2003 2004 2005 2006 2007 2008 2009 2010 2011*

Cen

ts/l

b.

* Forecast

Additional information about the 2011 outlook is available at the following websites:

• World Agricultural Outlook Board (WAOB)World Agricultural Supply and Demand Estimates– www.usda.gov/oce/commodity/wasde/index.htm

• Economic Research Service (ERS)Livestock, Dairy, and Poultry Situation and Outlook– www.ers.usda.gov/publications/ldp/

• Foreign Agricultural Service (FAS)Livestock and Poultry: World Markets and Trade– www.fas.usda.gov/dlp/livestock_poultry.asp