Outlook for Mining in Alaska. Global Markets Alaskan Issues Resource Potential.

21

Outlook for Mining in Alaska

-

Upload

dina-osborne -

Category

Documents

-

view

215 -

download

0

Transcript of Outlook for Mining in Alaska. Global Markets Alaskan Issues Resource Potential.

Outlook for Miningin Alaska

Global Markets

Alaskan Issues

Resource Potential

• Capital Markets Are Very Tight• Junior Capital Market is Dismal• Management Focused on Return on Capital• 40% of Top Mining Companies Have Disappeared in the

Past 5 Years

Global Consolidation & Change

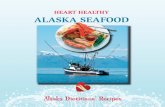

Average Annual Copper Prices(Cents per Pound)

0

50

100

150

200

250

300

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

2001$ $ of the year

Annual Average Zinc Prices

(Cents per pound)

0

20

40

60

80

100

120

140

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

2001 $ $ of Year

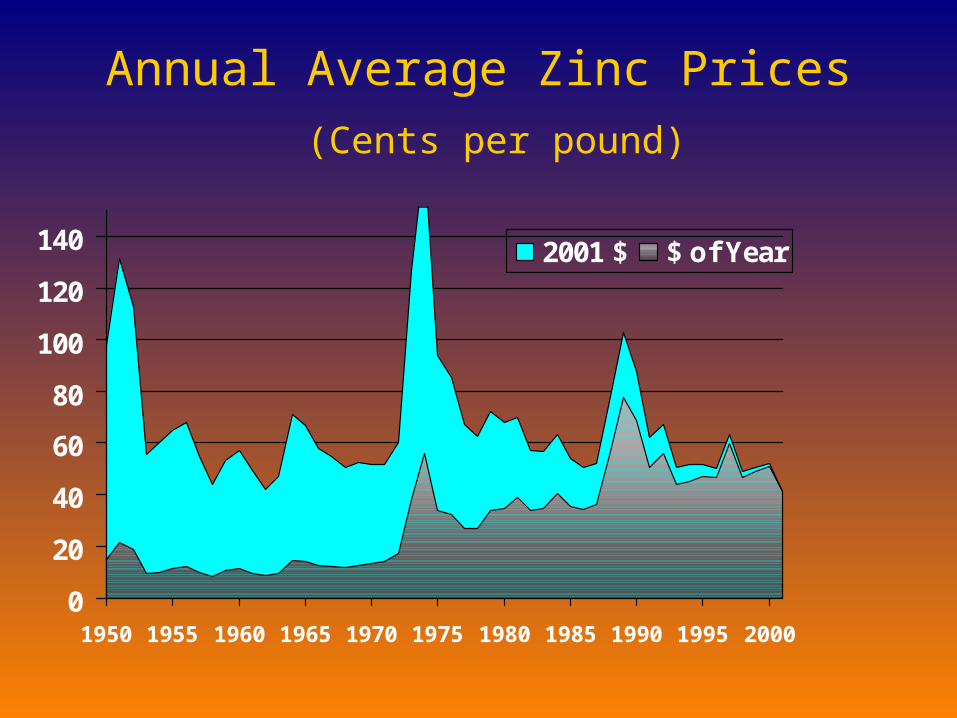

Average Annual Gold Prices (Dollars per troy ounce)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

2001$ $ of the year

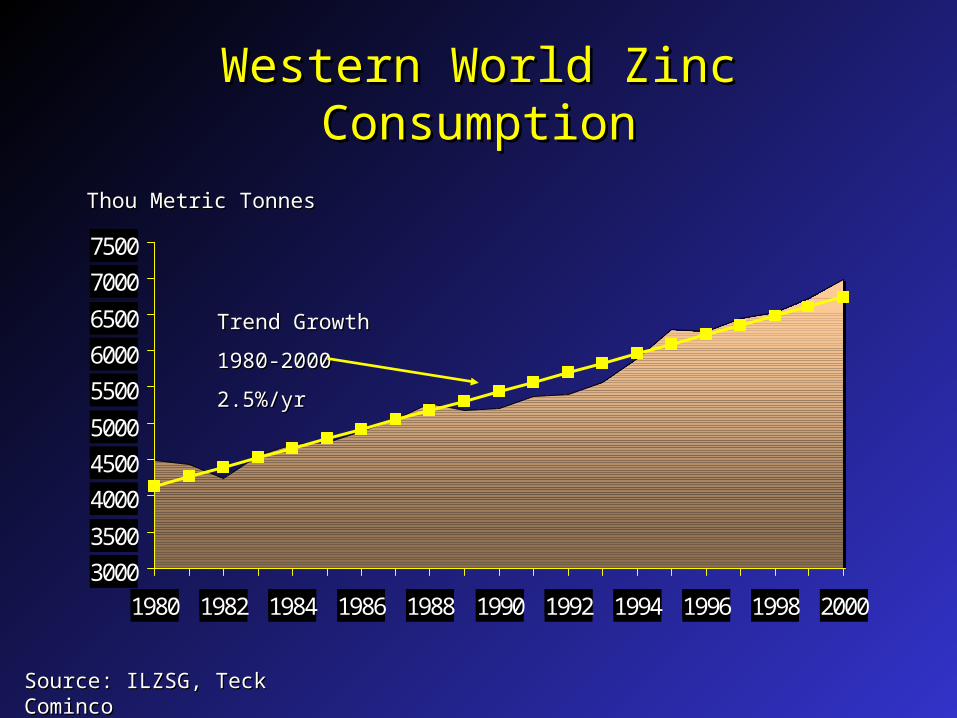

Western World Zinc ConsumptionWestern World Zinc Consumption

3000

3500

4000

4500

5000

5500

6000

6500

7000

7500

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

Trend GrowthTrend Growth

1980-20001980-2000

2.5%/yr2.5%/yr

Thou Metric TonnesThou Metric Tonnes

Source: ILZSG, Teck ComincoSource: ILZSG, Teck Cominco

ZINC REFINING CAPACITYZINC REFINING CAPACITY

2%

6%5%

4%

13% 8%33%

11%7%

2%

9%

Source: Teck ComincoSource: Teck Cominco

Total World Capacity 9,300,000mtTotal World Capacity 9,300,000mt

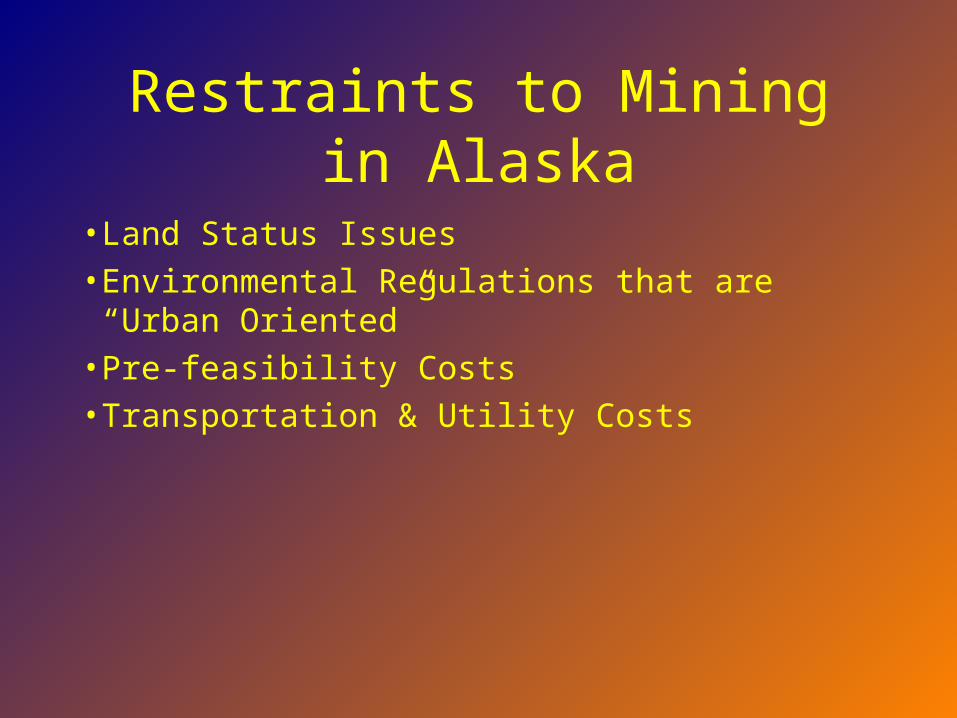

• Land Status Issues

• Environmental Regulations that are “Urban Oriented”

• Pre-feasibility Costs

• Transportation & Utility Costs

Restraints to Mining in Alaska

• Native Lands

• State Lands, Mining Laws & Taxation

• Effective DEC Committed to Finding Solutions

• AIDEA & Positive State Attitude

Dealing With Restraints

• Healy (Usibelli) Coal

• Green’s Creek Silver/Zinc/+

• Red Dog Zinc/Lead

• Fort Knox Gold

Alaskan Mine Producers

• Beluga Coal• Red Dog District Zinc/Lead• Pogo Gold• Donlin Creek Gold• Pebble Copper• Ambler District Copper/+

Known Big Deposits

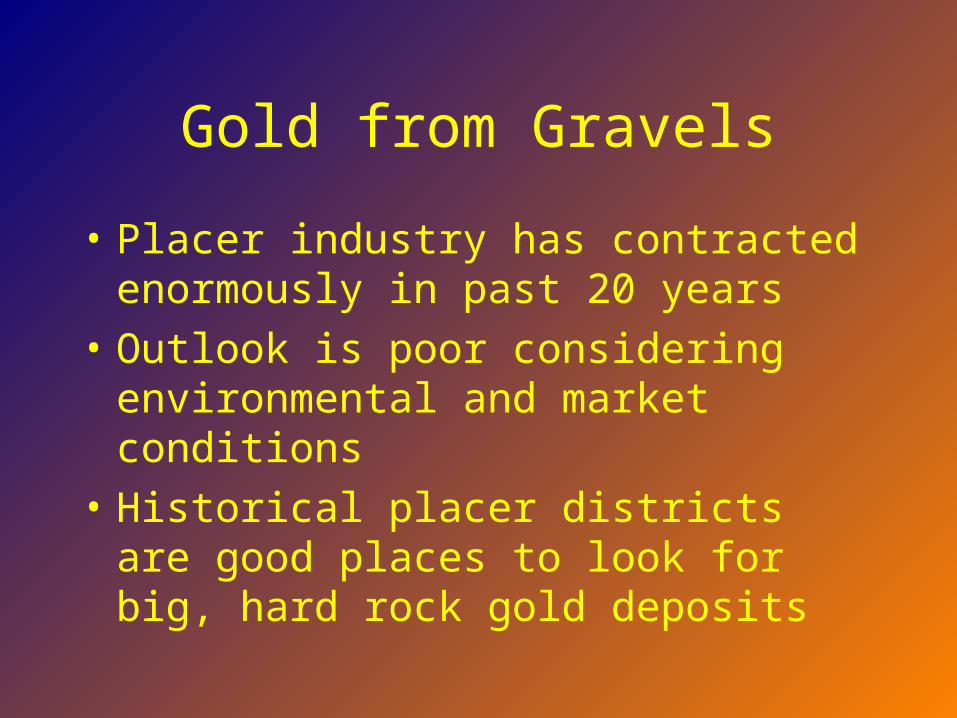

Gold from Gravels

• Placer industry has contracted enormously in past 20 years

• Outlook is poor considering environmental and market conditions

• Historical placer districts are good places to look for big, hard rock gold deposits

Do Not Forget Gravelis Mined Too

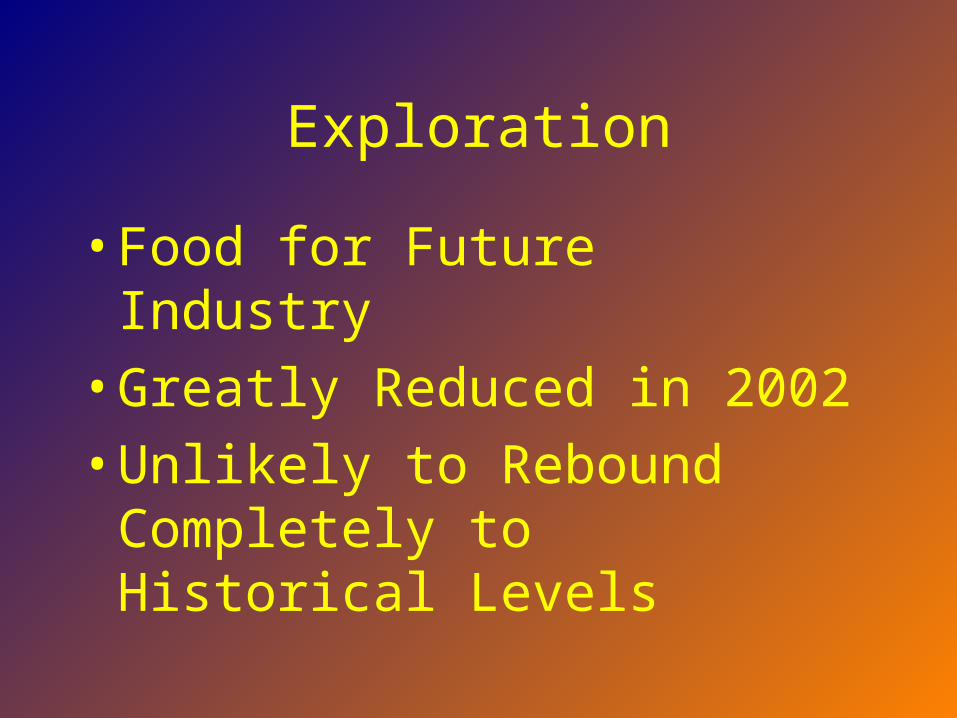

Exploration

• Food for Future Industry

• Greatly Reduced in 2002

• Unlikely to Rebound Completely to Historical Levels

Long Term

• New Big Discoveries

• New Commodities: Platinum, Palladium, Gemstones, Tin, Others

• New Technology Especially Related To Local Power Generation and Producing Metals from Concentrate

Conclusions

• Excellent Producing Mines Insure Industry for 30 or More Years

• Very Little New Activity in 2002

• Long Term Metal Trends Are Not Favorable

• Unlikely to Rebound Completely to Historical Levels

Thanks To...

Paul Glavinovich (Anchorage) Steve Borell (AMA) Neil Seldon (Vancouver) Charlotte MacCay (TeckCominco) Andy Roebuck (TeckCominco) Jason Brune (RDC) & Others

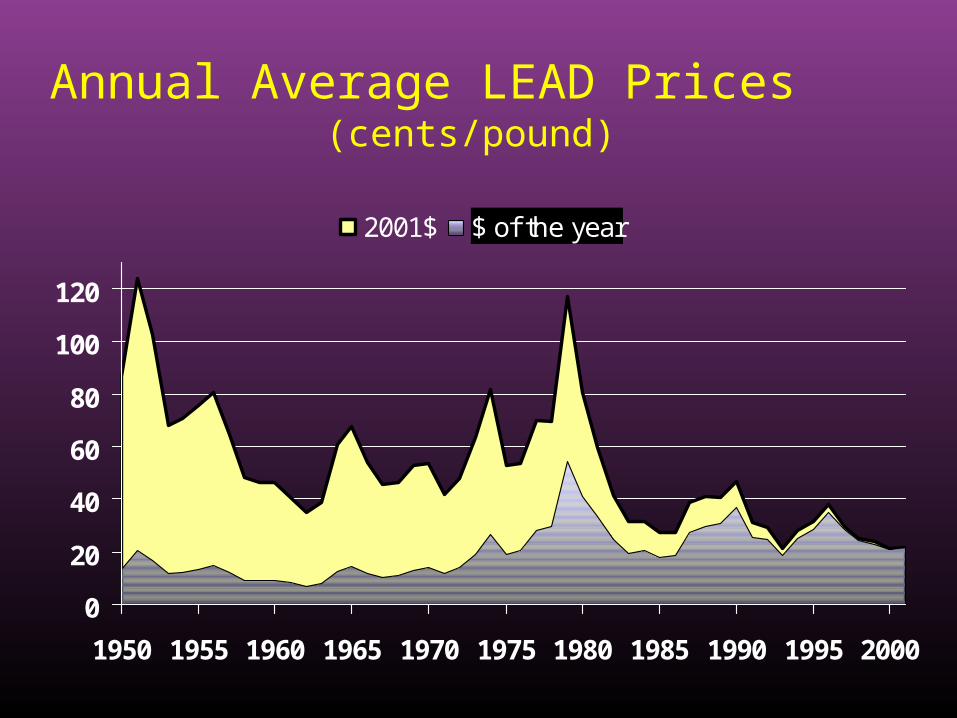

Annual Average LEAD Prices (cents/pound)

0

20

40

60

80

100

120

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

2001$ $ of the year

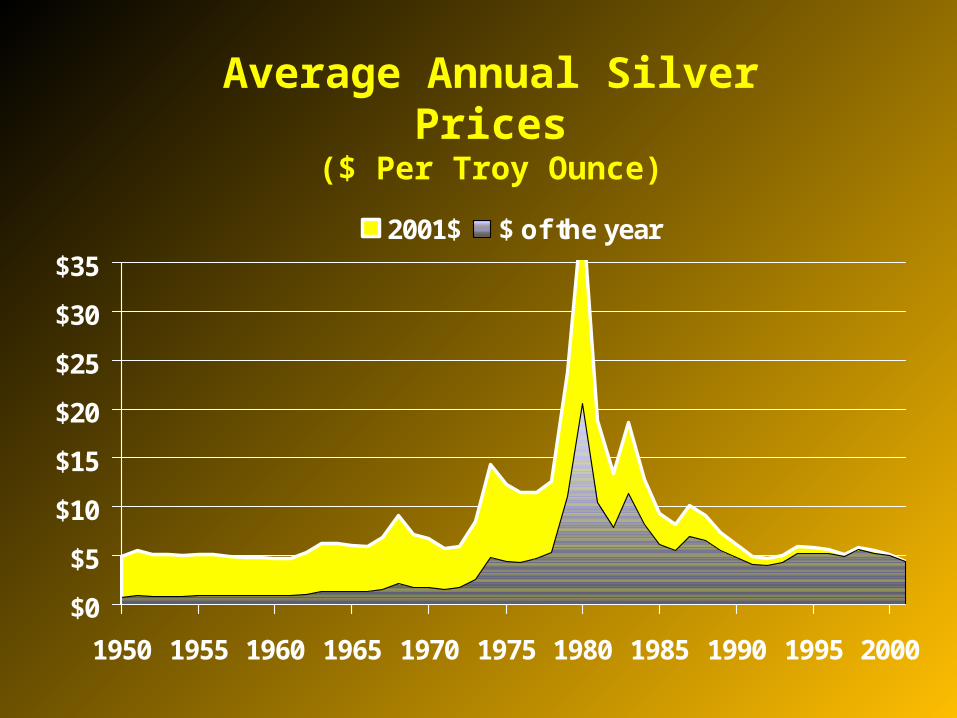

Average Annual Silver Prices($ Per Troy Ounce)

$0

$5

$10

$15

$20

$25

$30

$35

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000

2001$ $ of the year