Outlook 2017: Will the Bull be Extended or Extinguished?€¦ · Every Republican President Since...

35

Outlook 2017: Will the Bull be Extended or Extinguished? December 15, 2016 Kenneth Leon Global Director of Industry and Equity Research (Moderator) Sam Stovall, CFP® Chief Investment Strategist Scott Kessler Deputy Global Director and Industry Analyst Todd Rosenbluth Senior Director of ETF and Mutual Fund Research Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Transcript of Outlook 2017: Will the Bull be Extended or Extinguished?€¦ · Every Republican President Since...

Outlook 2017: Will the Bull be Extended or Extinguished?

December 15, 2016

Kenneth Leon Global Director of Industry and Equity Research (Moderator) Sam Stovall, CFP® Chief Investment Strategist Scott Kessler Deputy Global Director and Industry Analyst Todd Rosenbluth Senior Director of ETF and Mutual Fund Research

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Today’s Speakers

1

Kenneth Leon Global Director of Industry and

Equity Research (Moderator)

Sam Stovall, CFP® Chief Investment Strategist

Scott Kessler Deputy Global Director and

Industry Analyst

Todd Rosenbluth Senior Director of ETF and

Mutual Fund Research

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

CFRA Overview

2

Founded in 1994, CFRA is a leading provider of independent investment research using a differentiated proprietary methodology to help our global subscribers improve their investment and business decision-making

On October 1, 2016, CFRA acquired S&P Global’s Equity and Fund Research business. The combined firm now has 65 global investment professionals. The Equity and Fund research business has qualitative/STARS research coverage on over 1,500 global companies and quantitative research that covers over 20,000 global companies.

CFRA is a privately-held and employee-owned firm with operations in New York, London, Kuala Lumpur, Charlottesville, Denver, and Washington D.C.

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Outlook 2017

Investment Outlook 2017

3

Sam Stovall, CFP® Chief Investment Strategist CFRA

Twitter: @StovallCFRA

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

A Summary of Assumptions for 2017

4 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Recommending a 65% equities/35% fixed income allocation

S&P 500 12-month target of 2335

Improving but not exploding GDP growth

Inflation to end the year at 2.3% area; U.S. dollar up 3.5%

FOMC to raise rates in December; “2017 is the new 2016”

Double-digit EPS growth; strong revenue increase

“Reversion to the Mean” could be the mantra for foreign stocks

S&P 500 GAAP P/E Ratios at Bull Market Tops Since WWII

5 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

10.013.8

23.8

18.1 19.1 18.7

9.6

23.4

17.4

31.7

19.9

25.4

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

1948 1956 1961 1966 1968 1973 1980 1987 1990 2000 2007 2016

Average:19.2X

Source: CFRA, S&P Dow Jones Indices. Past performance is no guarantee of future results. Data: as of 12/9/16.

Average S&P 500 First-Year Price Returns

6 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

13.7%

-2.7%-5.0%

0.0%

5.0%

10.0%

15.0%

Democrat Controlled WhiteHouse

Republican Controlled WhiteHouse

The S&P 500's Average Price Returns and Frequencies of Price Advances by Political Party During Presidential Election Years Since WWII

Source: CFRA, S&P Dow Jones Indices. Past performance is no guarantee of future results. Data: 12/31/44-12/31/15.

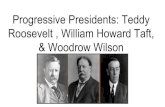

Presidents and Recessions Since 1902

7 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Every Republican President Since Teddy Roosevelt Experienced a Recession Within the First Two Years in Office

President RecessionsRoosevelt (1901-08) 1902-04, 1907-08Taft (1909-12) 1910-12, 1913-14Wilson (1913-20) 1918-19, 1920-21Harding/Cooldige (1921-24) 1923-24Cooldige (1925-28) 1926-27Hoover (1929-32) 1929-33Roosevelt (1933-40) 1937-38, 1945Truman (1945-52) 1948-49Eisenhower (1953-60) 1953-54, 1957-58, 1960-61Kennedy/Johnson (1961-64) NoneJohnson (1965-68) NoneNixon/Ford (1969-1976) 1969-70, 1973-75Carter (1977-80) 1980Reagan (1981-88) 1981-82Bush-41 (1989-92) 1990-91Clinton (1993-2000) NoneBush-43 (2001-08) 2001, 2007-09Obama (2009-16) None

Source: CFRA, NBER. Past performance is no guarantee of future results. Data: 12/31/1901-12/9/16.

Progression of S&P 500 Operating EPS Estimates

8 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%1-

Jan

1-Fe

b1-

Mar

1-A

pr

1-M

ay

1-Ju

n

1-Ju

l

1-A

ug

1-Se

p

1-O

ct

1-N

ov

1-D

ec

1-Ja

n

1-Fe

b

1-M

ar

1-A

pr

1-M

ay

1-Ju

n

1-Ju

l

1-A

ug

1-Se

p

1-O

ct

1-N

ov

1-D

ec

Prior Year Current YearPrior Year Current YearPrior Year Current YearPrior Year Current Year

----FY 2016

FY 2015----

----FY 2017

Source: CFRA, S&P Capital IQ. Past performance is no guarantee of future results. Data: 12/31/1901-12/9/16.

MSCI-EAFE Rolling 10-Year Compound Growth Rate (excluding dividends)

9 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

-5%

0%

5%

10%

15%

20%

25%

Dec

-79

Dec

-83

Dec

-87

Dec

-91

Dec

-95

Dec

-99

Dec

-03

Dec

-07

Dec

-11

Dec

-15

Now: -2.2%Feb. 2009: -3.1%

Oct. 2007: +7.2%

Apr. 1987: +21.3%

Median: +5.1%

Mar. 2013: +6.8%

Sept. 2000: +7.9%

Source: CFRA, MSCI. Past performance is no guarantee of future results. Data: 12/31/69-12/9/16.

International Markets: Greater Risk/Lower Valuations

10 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Div.

Global Market Index 2016E 2017E 2016E 2017E Yield

S&P 500 SPX (0.0) 11.8 19.2 17.1 2.0%

S&P MidCap 400 MID 2.7 12.0 22.6 20.2 1.5%

S&P SmallCap 600 SML 5.3 19.1 25.3 21.3 1.1%

Developed Int'l. MXEA 30.0 10.9 16.0 14.4 3.3%

Emerging Markets MXEF 23.0 14.6 13.8 12.0 2.5%

Frontier Markets MXFM (18.8) 17.3 12.3 10.5 4.2%

Int'l Small Caps. MXEASC 74.4 15.4 17.4 15.0 2.5%

EPS % Chg. P/E Ratios

Source: CFRA, S&P Capital IQ, Bloomberg. Data as of 12/9/16.

Outlook 2017

Sectors and Stocks: 2017 Winners and Losers Post-Election

11

Scott Kessler Deputy Director and Industry Analyst CFRA

Twitter: @KesslerCFRA

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Sector Disruptors Series of Thematic Research

12 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

We think Sector Disruptors has become differentiated source of sector and stock research since inception in December 2014

S&P Capital IQ Equity Research’s experienced fundamental research team authors these reports multiples times a year

Major market theme addressed across all economic sectors with emphasis on potential company/stock impacts

– Prior reports focused on infrastructure, investor activism, buybacks and dividends, and the U.S. presidential election, as well as annual outlooks

For 2016, we anticipated: energy company dividend cuts, high drug prices as key issue, adoption of mobile phone leasing

Source: CFRA

Sector Disruptors: 2017 Winners and Losers Post-Election

13 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Our latest Sector Disruptors report, published last week, focuses on how last month’s elections will influence companies/stocks

New sector themes for 2017 include:

– Efforts to “repeal and replace” the Affordable Care Act in Health Care

– Infrastructure spending aiding Materials demand

– Easing Financials regulations

– More military spending bolstering defense contractors

– Potential repatriation of foreign earnings by big Technology companies

Source: CFRA

President-Elect Trump’s Priority – Domestic Growth

14 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

We think President-elect Donald Trump will look to stimulate U.S. economic growth through:

– Domestic spending

– Lower taxes

– Less regulation

We see relative positives and negatives

– Positives for firms with U.S. focus, higher tax rates, more regulated units

– Negatives for firms with more international emphasis (consider impact of strong U.S. dollar), lower tax rates (but note repatriation), less regulated

Source: CFRA

Post-Election Index/Sector/Sub-Industry Performance

15 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

We have already noted considerable price movements

Source: CFRA, S&P Dow Jones Indices. Past performance is no guarantee of future results.

Sector Focus – Industrials and Technology

16 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

These sectors account for nearly a third of the market cap of the S&P 500 (recently 31%)

We see significant impacts in these sectors related to:

– Greater domestic spending

• We see tens of billions more in annual defense spending

– Tax changes

• Although Technology companies often have relatively low tax rates, given considerable international revenues/profits, they also have considerable overseas cash that could/would be repatriated with related tax reduction

Source: CFRA, market cap calculation as of December 1, 2016.

Industrials Sector

17 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

We see the Industrials Sector benefiting from more domestic spending, in particular defense spending:

– We see sequestration (automatic spending cuts imposed by Budget Control Act of 2011) pertaining to the military as largely over

– Trump has called for increasing “military preparedness,” including more soldiers, ships and jets, and strengthening nuclear and missile defenses

– We think annual spending increase of $55-$100 billion is possible

• ~$580 billion budgeted spending for FY 16 (Sep.)

Source: CFRA, Department of Defense Fiscal Year 2017 President’s Budget Proposal.

Positive on Aerospace & Defense Sub-Industry

18

The day after Election Day in the U.S., we raised our Fundamental Outlook on the Aerospace & Defense sub-industry to Positive from Neutral

Related Strong Buy/Buy recommendations include:

– General Dynamics (GD $174, Buy)

– Lockheed Martin (LMT $259, Strong Buy)

– Orbital ATK (OA $87, Strong Buy)

– Raytheon (RTN $146, Buy)

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Source: CFRA, prices and recommendations as of December 8, 2016.

Technology Sector

19 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

We see the Technology sector benefiting from a reduction to 10% from 35% in tax rate on foreign earnings

– Candidate Donald Trump proposed cutting repatriation tax

– Ten largest IT companies in the S&P 500 by market cap recently had:

• $709 billion in cash/investments

• $523 billion in overseas cash/investments (74% of the total)

– We see Technology sector companies using such capital for domestic investment, buyback and dividend actions, M&A

Source: CFRA as of November 30, 2016.

Large-cap Technology Names in Light of Overseas Cash

20 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Many Technology companies have considerable non-U.S. cash

We look to firms with significant percentage of overseas cash and investments (70% or more), accounting for notable part of market-cap (over 20%)

Related Strong Buy/Buy recommendations include:

– Apple (AAPL $112, Strong Buy)

– Intel (Intel $36, Buy)

Source: Source: CFRA as of November 30, 2016, prices and recommendations as of December 8, 2016.

Outlook 2017

Sector-Focused Strategies: What’s Inside Matters

21

Todd Rosenbluth Senior Director of ETF and Mutual Funds CFRA

Twitter: @ToddCFRA

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Popularity of Passive Funds

22

In 12-month period ending October 2016, US Equity:

– Passive funds added $191 billion of new assets

– Active funds shed $249 billion of their assets

In 12-month period ending October 2016, Sector:

– Passive funds added $15 billion of new assets

– Active funds shed $26 billion of their assets

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Source: Source: Morningstar Direct Asset Flows.

Large Disparity Among Fund Costs

23 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

0.00% 0.50% 1.00% 1.50%

Large Cap Core

Small Cap Core

Industrials

Avg. Mutual FundCheapest ETF

Source: Source: MarketScope Advisor, as of December 7, 2016.

Industrial ETFs: What’s Inside Counts

24

Industrials Select Sector SPDR (XLI)

– Climbed 20% in 2016

– Top 10 holdings comprised 47% of assets

– Net expense ratio: 0.14%

Fidelity MSCI Industrials (FIDU)

– Climbed 21% in 2016

– Top 10 holdings comprised 42% of assets

– Net expense ratio: 0.08%

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Data: as of December 8, 2016.

Industrial ETFs: What’s Inside Counts

25

PowerShares Aerospace & Defense (PPA)

– Climbed 22% in 2016

– Top 10 holdings comprised 57% of assets

– Net expense ratio: 0.64%

SPDR S&P Aerospace & Defense (XAR)

– Climbed 25% in 2016

– Top 10 holdings comprised 46% of assets

– Net expense ratio: 0.35%

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Data: as of December 6, 2016.

Technology ETFs: What’s Inside Counts

26

Technology Select Sector SPDR (XLK)

– Climbed 12% in 2016

– Key industries: Software (15% of assets), IT Services (16%), diversified Telecom Services (10%), etc.

– Net expense ratio: 0.14%

Vanguard Information Technology (VGT)

– Climbed 21% in 2016

– Key industries: Software (21% of assets), IT Services (18%), semiconductor & semiconductor equipment (15%)

– Net expense ratio: 0.10%

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Data: as of December 6, 2016.

ETFs Tied to Repatriation

27

First Trust NASDAQ Technology Dividend Index (TDIV)

– Climbed 17% in 2016

– Key industries: Semiconductors & semiconductor equipment (29% of assets), Diversified Telecom Services (15%), and Software (15%)

– Net expense ratio: 0.50%

PowerShares Buyback Achievers (PKW)

– Climbed 12% in 2016

– Key industries: Industrials (24% of assets), Financials (16%), Information Technology (16%)

– Net expense ratio: 0.63%

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Data: as of December 6, 2016.

Our Q&A session will begin

momentarily.

28 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Q&A

29

Kenneth Leon Global Director of Industry and

Equity Research (Moderator)

Sam Stovall, CFP® Chief Investment Strategist @StovallCFRA on Twitter

Scott Kessler Deputy Global Director and

Industry Analyst @KesslerCFRA on Twitter

Todd Rosenbluth Senior Director of ETF and

Mutual Fund Research @ToddCFRA on Twitter

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Thank You for Attending

30 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Your opinion is very important to us. Please fill out the survey!

For in-depth information on these topics and more, contact us: Email for a Free Trial: [email protected] Learn: For more information about CFRA, visit: www.cfraresearch.com Call: 800-523-4534 Important Replay/Document Resource Center Information: Please note – the replay of this webcast and supplemental resource center documents will be made available in 3-4 business days. You will be notified of its availability via email.

Speaker Biographies

31

Kenneth Leon Global Director of Industry and Equity Research at CFRA Research Ken is Global Director of Research and an Industry Analyst at CFRA. He is responsible for global analytical research and client servicing. As a subject matter expert, his industry research coverage includes Real Estate Investment Trusts (REITs), Investment Banking, Private Equity and Market Exchange companies. Ken is a thought leader and he provides with the analytical team ongoing in-depth research and communications to key customer segments. Notable innovations are related to Differentiated Idea Generation (D.I.G.) reports and our Sector Disruptors issues. Additionally, he previously was a lead developer of the firm’s ETF analytical research product and served as a member of the ETF Investment Portfolio Committee. Ken holds both a Bachelor of Science degree and an MBA from New York University. He was also licensed in the State of New Jersey as a Certified Public Accountant.

Sam Stovall, CFP®

Chief Investment Strategist at CFRA Research Sam Stovall is Chief Investment Strategist of U.S. Equity Strategy at CFRA. He serves as analyst, publisher and communicator of S&P’s outlooks for the economy, market, and sectors. Sam is the Chairman of the S&P Investment Policy Committee, where he focuses on market history and valuations, as well as industry momentum strategies. He is the author of The Standard & Poor’s Guide to Sector Investing and The Seven Rules of Wall Street. In addition, Sam writes a weekly investment piece, featured on S&P Global Market Intelligence’s MarketScope Advisor platform and his work is also found in the flagship weekly newsletter The Outlook. He holds an MBA in Finance from New York University and a B.A. in History/Education from Muhlenberg College, in Allentown, PA. He is a CFP® certificant and is a Trustee of the Securities Industry Institute®, the executive development program held annually at The Wharton School of The University of Pennsylvania.

Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

32 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

Speaker Biographies (cont.)

Scott Kessler Deputy Global Director and Industry Analyst at CFRA Research Scott Kessler is Deputy Global Director and Industry Analyst at CFRA, Equity Research. In addition to managing a team of industry analysts, Scott establishes and executes on longer-term strategies and directs day-to-day operations to produce and distribute high-quality and timely research content. He also conducts fundamental analysis and valuation assessments within the Internet, Software and Fintech areas. Additionally, Scott oversees and coordinates team media and compliance efforts. Scott holds a bachelor’s degree from Brandeis University and a law degree from Washington University in St. Louis.

Todd Rosenbluth Senior Director of ETF and Mutual Fund Research at CFRA Research Todd Rosenbluth is the Director of ETF and Mutual Fund Research at CFRA where he leads the firm’s holdings-based research efforts within the Equity Research and Fund group. Todd publishes regular thought leadership content on equity and fixed income products, maintains the quantitative fund models and supports client needs. He also serves as a member of Portfolio Strategy Committee and the Investment Policy Committee. Todd holds a B.G.S in Finance from the University of Michigan and an MBA in Finance from New York University.

Disclosures

33 Permission to reprint or distribute any content from this presentation requires the prior written approval of CFRA. Not for distribution to the public. Copyright © 2016 by CFRA. All rights reserved.

S&P GLOBAL™ and S&P CAPITAL IQ™ are used under license. The owner of these trademarks is S&P Global Inc. or its affiliate, which are not affiliated with CFRA Research or the author of this content. This content has been prepared by Accounting Research & Analytics, LLC and/or one of its affiliates. It is published and distributed by Accounting Research & Analytics, LLC d/b/a CFRA with the following exceptions: In the European Union/European Economic Area, by CFRA UK Limited (company number 08456139 registered in England & Wales with its registered office address at 131 Edgware Road, London, W2 2AP, United Kingdom), which is an Appointed Representative of Hutchinson Lilley Investments LLP, which is regulated by the UK Financial Conduct Authority (No. 582181); in Malaysia, by Standard & Poor’s Malaysia Sdn Bhd, which is regulated by the Securities Commission Malaysia (License No. CMSL/A0181/2007). The content of this report and the opinions expressed herein are those of CFRA based upon publicly-available information that CFRA believes to be reliable and the opinions are subject to change without notice. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, to the full extent permitted by law, regarding the accuracy, completeness, or usefulness of this information and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of CFRA. The Content shall not be used for any unlawful or unauthorized purposes. CFRA and any third-party providers, as well as their directors, officers, shareholders, employees or agents do not guarantee the accuracy, completeness, timeliness or availability of the Content. Past performance is not necessarily indicative of future results. This document may contain forward-looking statements or forecasts; such forecasts are not a reliable indicator of future performance. This report is not intended to, and does not, constitute an offer or solicitation to buy and sell securities or engage in any investment activity. This report is for informational purposes only. Recommendations in this report are not made with respect to any particular investor or type of investor. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors and this material is not intended for any specific investor and does not take into account an investor's particular investment objectives, financial situations or needs. Investors should seek independent financial advice regarding the suitability and/or appropriateness of making an investment or implementing the investment strategies discussed in this document and should understand that statements regarding future prospects may not be realized. Investors should note that income from such investments, if any, may fluctuate and that the value of such investments may rise or fall. Accordingly, investors may receive back less than they originally invested. Investors should seek advice concerning any impact this investment may have on their personal tax position from their own tax advisor. Please note the publication date of this document. It may contain specific information that is no longer current and should not be used to make an investment decision. Unless otherwise indicated, there is no intention to update this document. CFRA’s financial data provider is S&P Global Market Intelligence. THIS DOCUMENT CONTAINS COPYRIGHTED AND TRADE SECRET MATERIAL DISTRIBUTED UNDER LICENSE FROM S&P GLOBAL MARKET INTELLIGENCE. FOR RECIPIENT’S INTERNAL USE ONLY. The Global Industry Classification Standard (GICS) was developed by and/or is the exclusive property of MSCI, Inc. and Capital IQ, Inc. (“Capital IQ”). GICS is a service mark of MSCI and Capital IQ and has been licensed for use by CFRA. Redistribution or reproduction is prohibited without written permission. Copyright © 2016 CFRA. All rights reserved. CFRA, the CFRA inverted pyramid logo, and STARS are registered trademarks of CFRA.

S&P GLOBAL™ and S&P CAPITAL IQ™ are used under license. The owner of these trademarks is S&P Global Inc. or its affiliate, which are not affiliated with CFRA Research or the author of this content. The content of this report and the opinions expressed within are those of CFRA. This analysis has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this analysis, CFRA AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, regarding the accuracy, completeness or usefulness of this information. and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. In particular, the research provided is not intended to constitute an offer, solicitation or advice to buy or sell securities. CFRA, CFRA Accounting Lens, CFRA Legal Edge, CFRA Score, and all other CFRA product names are the trademarks, registered trademarks, or service marks of CFRA or its affiliates in the United States and other jurisdictions. CFRA Score may be protected by U.S. Patent No. 7,974,894 and/or other patents. If you have any comments or questions, please contact [email protected].