Outlook 2013—Rebalancing on a Tightrope - Porcimex Outlook 2013 Rebalancing.pdf · Q1’12...

33

Outlook 2013—Rebalancing on a Tightrope Agri Commodity Markets Research

Transcript of Outlook 2013—Rebalancing on a Tightrope - Porcimex Outlook 2013 Rebalancing.pdf · Q1’12...

Outlook 2013—Rebalancing on a Tightrope

Agri Commodity Markets Research

Rabobank International

Agri Commodities Market Research

Food & Agribusiness Research and Advisory

Authors:

Luke [email protected]

Keith Flury [email protected]

Erin FitzPatrick [email protected]

Nick Higgins [email protected]

Agri Commodity Markets Research

Disclaimer: This document is issued by Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. incorporated in the Netherlands, trading asRabobank International (“RI”). The information and opinions contained in this document have been compiled or arrived at from sourcesbelieved to be reliable, but no representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. This document is for information purposes only and is not, and should not be construed as, an offer or a commitment by RI or any of itsaffiliates to enter into a transaction, nor is it professional advice. This information is general in nature only and does not take into account an individual’s personal circumstances. All opinions expressed in this document are subject to change without notice. Neither RI, nor otherlegal entities in the group to which it belongs, accept any liability whatsoever for any loss howsoever arising from any use of this documentor its contents or otherwise arising in connection therewith. This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of RI. All copyrights, including those within the meaning of the DutchCopyright Act, are reserved. Dutch law shall apply. By accepting this document you agree to be bound by the foregoing restrictions. © Rabobank International Utrecht Branch, Croeselaan 18, 3521 CB, Utrecht, the Netherlands +31 30 216 0000

Outlook 2013—Rebalancing on a Tightrope

Contents | i

ContentsPage

Section 1

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Our price for ecasting performance last season . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Section 2

Agri Commodity Outlooks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Wheat . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Corn . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Soybeans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Soy oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Soymeal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Palm oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Sugar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Coffee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Cocoa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Cotton . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

| iii

Dear Valued Client,

We are proud to provide you with our Agri Commodity Markets Research Outlook 2013—Rebalancing on a Tightrope .

As the year comes to a close, the supply of many agri commodities is at historically low levels.Capacity constraints, adverse weather and strong global demand have caused some prices toreach record highs in 2012, creating uncertainty around how markets will respond in 2013. High price levels and increased volatility highlight the increased need for market knowledge,foresight and strategic planning.

Our outlook for 2013 suggests that the volatility in agri commodity prices looks set to continue into the foreseeable future. Whatever your role is in the Food & Agri supply chain, be it primary producer, processor or retailer, you face challenging times. And we are here to face them with you.

We hope you find our research and price forecasts useful as you prepare your plans andstrategies throughout the year. This report is a key example of the work we provide to helpsupport our clients through a dedicated team of specialised Food & Agri analysts around the world.

Wishing you great wisdom and insights in these challenging times.

With kind regards,

Sipko SchatMember of Executive Board, Rabobank

29 November 2012

Section 1 Introduction | 1

Agricultural markets are faced with thechallenge of rebuilding global stocks nextseason given precariously balancedfundamentals. In order to achieve a build in stock levels in 2013, we expect prices—particularly in grain and oilseed markets—willneed to move higher in Q1 to slow demandfrom its current pace. Higher prices duringthis period should also encourage increasedglobal production, resulting in a rebalancingof fundamentals and a weaker price outlookfor 2H 2013. The soft commodity marketsoffer more of a mixed bag in 2013, with arelatively neutral to bearish outlook for prices.Using the S&P Agri Index as a proxy for ourcommodity forecasts, we expect a decline inagricultural prices of around 10% between Q1 and Q4 2013. However, it is the lack of

buffer stocks which leaves the marketexposed to another season of extremeuncertainty and high volatility.

Consistent with recent years, the outlook forthe agri commodity complex is clouded byglobal macro uncertainty, although we do not expect a material slowdown in demandfor agricultural commodities. Rabobankforecasts world GDP to increase 3.75% in2013. Confidence levels continue to beadversely affected by the eurozone crisis andthe drag it is having on the labour market,trade and, ultimately, growth in marketsaround the world. Compounding the globaluncertainty is the outlook in the US, with thefiscal cliff and impact of Hurricane Sandythreatening to destabilise what is already a sluggish recovery.

1 Introduction

Figure 1.1: Rabobank’s 2013 agri commodity price forecasts

Q1’12 Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

Wheat (CBOT) USc/bu 643 641 871 870 910 775 735 700

Wheat (Matif) EUR/tonne 210 212 259 270 290 245 217 204

Corn USc/bu 641 618 783 740 790 700 625 600

Soybeans USc/bu 1,272 1,426 1,677 1,450 1,475 1,400 1,350 1,300

Soy oil USc/lb 53 52 54 48 49 50 50 49

Soymeal USD/ton 339 413 514 450 450 425 375 350

Palm oil MYR/tonne 3,245 3,225 2,884 2,360 2,800 3,000 2,800 2,700

Sugar USc/lb 24.6 21.2 21 19.5 19 19 18.5 18.5

Coffee USc/lb 205 170 172 155 160 170 175 170

Cocoa USD/tonne 2,308 2,222 2,438 2,450 2,500 2,450 2,550 2,550

Cotton USc/lb 93 81 73 72 70 70 75 80

Source: Rabobank, Bloomberg, 2012

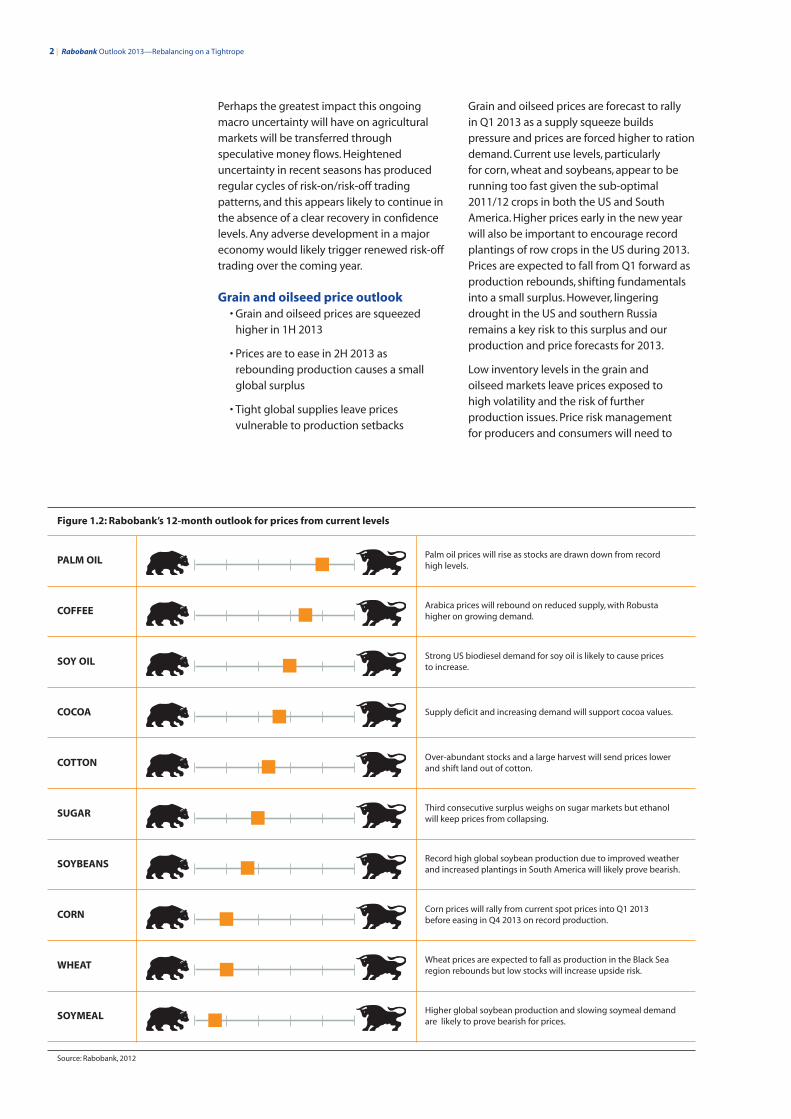

Perhaps the greatest impact this ongoingmacro uncertainty will have on agriculturalmarkets will be transferred throughspeculative money flows. Heighteneduncertainty in recent seasons has producedregular cycles of risk-on/risk-off tradingpatterns, and this appears likely to continue inthe absence of a clear recovery in confidencelevels. Any adverse development in a majoreconomy would likely trigger renewed risk-offtrading over the coming year.

Grain and oilseed price outlook• Grain and oilseed prices are squeezedhigher in 1H 2013

• Prices are to ease in 2H 2013 asrebounding production causes a smallglobal surplus

• Tight global supplies leave pricesvulnerable to production setbacks

Grain and oilseed prices are forecast to rally in Q1 2013 as a supply squeeze buildspressure and prices are forced higher to rationdemand. Current use levels, particularly for corn, wheat and soybeans, appear to berunning too fast given the sub-optimal2011/12 crops in both the US and SouthAmerica. Higher prices early in the new yearwill also be important to encourage recordplantings of row crops in the US during 2013.Prices are expected to fall from Q1 forward asproduction rebounds, shifting fundamentalsinto a small surplus. However, lingeringdrought in the US and southern Russiaremains a key risk to this surplus and ourproduction and price forecasts for 2013.

Low inventory levels in the grain and oilseed markets leave prices exposed to high volatility and the risk of furtherproduction issues. Price risk management for producers and consumers will need to

2 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Figure 1.2: Rabobank’s 12-month outlook for prices from current levels

PALM OILPalm oil prices will rise as stocks are drawn down from record high levels.

COFFEEArabica prices will rebound on reduced supply, with Robusta higher on growing demand.

SOY OILStrong US biodiesel demand for soy oil is likely to cause prices to increase.

COCOA Supply deficit and increasing demand will support cocoa values.

COTTONOver-abundant stocks and a large harvest will send prices lower and shift land out of cotton.

SUGARThird consecutive surplus weighs on sugar markets but ethanol will keep prices from collapsing.

SOYBEANSRecord high global soybean production due to improved weatherand increased plantings in South America will likely prove bearish.

CORNCorn prices will rally from current spot prices into Q1 2013 before easing in Q4 2013 on record production.

WHEAT Wheat prices are expected to fall as production in the Black Searegion rebounds but low stocks will increase upside risk.

SO YMEALHigher global soybean production and slowing soymeal demandare likely to prove bearish for prices.

Source: Rabobank, 2012

Section 1 Introduction | 3

be prudent as prices will be highly sensitive to weather developments, governmentintervention and macro uncertainty.

While we expect a decline in grain and oilseedprices, our price forecasts do not suggest acollapse in prices in 2H 2013. Despite a record196 million tonne production increase incorn, wheat and soybean production,Rabobank forecasts that the combined globalstocks-to-use of these commodities will riseby just 1.9 points to 19.9%. Therefore, weexpect 2013/14 stocks-to-use to remainbelow 2011/12 levels, highlighting the factthat the rebalancing of fundamentals willrequire multi-season surpluses in order torebuild global inventories.

Soft commodity price outlook

• The outlook is neutral to slightly bearishin most markets

• Fundamentals are balanced or in slightsurplus

• Range-bound trading will continue in 2013

The outlook for prices in the soft commoditymarkets —sugar, cocoa and cotton—is neutralto slightly bearish in 2013. Fundamentals inthese commodities are more balanced, and insome cases (e.g. sugar and cotton), surpluses

have been built over recent seasons. Despitethe support of a weaker US dollar, a numberof soft commodity prices are forecast to fall to multi-year lows in 2013.

Current prices are mostly in line with our fairvalue expectations, and forward curves arereflective of our forecasts for the year ahead.The balanced fundamental outlook suggestsmore range-bound trading—as seen in 2H 2012—should continue. A trigger, such as a weather event, major policy shift orgeopolitical event, would be needed to see a substantial readjustment of ourforecasts in 2013.

The soft commodity markets have realisedincreased supply due to high prices in 2010and 2011, with the record coffee, cotton andsugar crops in 2011/12. The increased supplyresulted in strong downward corrections ascoffee, cotton and sugar were the three worstperformers of liquid agricultural commoditiesin 2012. Therefore, the softs have alreadymoved through the cycle we expect for thegrain and oilseed sectors in 2013. The softsmarkets have now fallen near levels we deem as fair value, and we expect unwindingof investor short positions and commercialbuying to keep markets flat or supported in 2013.

inde

x

EUR/

USD

Figure 1.3: The S&P Agri Index is expected to decline next year—despite being supported by a falling US dollar

Source: Bloomberg, Rabobank, 2012

140

232

324

416

508

600

2001

2003

2005

2007

2009

2011

2013

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

S&P Agri Index EUR/USD (RHS)

Figure 1.4: Stocks of wheat and corn held by major exporting nations are expected to increase significantly in 2013/14—helping prices to ease

mil

lio

n t

on

nes

per

cen

t ch

ang

e

Percent change (RHS)

Source: USDA, Rabobank, 2012

Ending stocks

13/1

4f

11/1

2f

09/1

0

07/0

8

05/0

6

03/0

4

01/0

2

99/0

0

97/9

8

95/9

6

93/9

4

91/9

2

60

70

80

90

100

110

120

130

140

150

160

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

4 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Our price for ecasting performance last season

The past 12 months have been a mixed bag in terms of price forecasting accuracy.

In our Outlook 2012—Down, But Not Out (released December 2011), we outlined expected key themes for the year ahead.

1. Economic slowdown2. Speculators and the US dollar 3. Policy risks4. Capacity constraints

From a fundamental viewpoint we expected prices to decline in 2012 but remain above historical averages. The keythemes we highlighted did in fact play a large role in shaping 2012 price direction. The US dollar has continued to trendlower, speculators’ bullish bets on grains and oilseeds reached new highs, and policy changes continued to reshapemarkets. However, the key price driver in 2012 was adverse weather and the resultant inability for global grains andoilseeds production to meet global demand, which pushed some prices to new record highs. This was largely driven bythe worst US drought in more than 50 years, which caused our price forecasts for grains and oilseeds to be too low on anabsolute basis in 2012.

Our most bullish pick for 2012 was soymeal, while our most bearish expectation was for coffee. Our directional view heldup well: soymeal prices rose 39% and coffee prices fell 37%. Compared to actual price moves, our wheat, soybean andsoymeal price forecasts were on average 15%-25% too low. However, our forecasts for cotton, sugar and cocoa werewithin 5% of the actual annual prices.

Figure 1.6: Rabobank 2012 forecasts (December 2011) vs. actual prices

Rabobank Dec 2012 forecasts Actual

Q1’2012 Q2’2012 Q3’2012 Q4’2012 Q1’2012 Q2’2012 Q3’2012 QTD Q4’2012

Wheat USc/bu 595 630 615 595 643 641 871 870

Corn USc/bu 610 645 630 610 641 618 783 748

Soybeans USc/bu 1,178 1,226 1,260 1,251 1,272 1,426 1,677 1,529

Soy oil USc/lb 48.7 50.2 49.1 47.5 52.9 52.3 54.0 50.2

Soymeal USD/ton 310 290 330 335 339 413 514 470

Palm oil MYR/tonne 2,800 2,900 3,000 3,100 3,245 3,225 2,884 2,334

Sugar USc/lb 23.5 23.0 22.0 22.0 24.6 21.2 21.0 20.1

Coffee USc/lb 220 200 180 170 205 170 172 161

Cocoa USD/tonne 2,350 2,450 2,350 2,300 2,308 2,222 2,438 2,407

Cotton USc/lb 85 85 80 80 93 81 73 72

Source: Bloomberg, Rabobank, 2012

Figure 1.5: 2012 forecast results show we underestimated bullish grain and oilseed moves

aver

age

fore

cast

as

% o

f act

ual

Source: Bloomberg, Rabobank, 2012

-30

-25

-20

-15

-10

-5

0

5

10

Co

tto

n

Co

coa

Co

ffee

Sug

ar

Palm

Soym

eal

Soy

oil

Soyb

ean

s

Co

rn

Wh

eat

Section 2 Agri Commodity Outlooks | 5

2 Agri Commodity Outlooks

6 | Rabobank Outlook 2013—Rebalancing on a Tightrope

CBOT Wheat prices are forecast to rise to USD 9.10/bushel in Q1 2013 and then fall 23% to USD 7.00/bushel by Q4 2013. StrongerUS corn prices in Q1 2013 are likely to supportworld wheat prices in the same period,reflecting the 4.6% QOQ uplift in our CBOT Wheat price forecast. But the NorthernHemisphere wheat harvest is expected tobring about a strong fall in prices from Q1 to Q2, provided production in the US, the EU and Black Sea region is within 5% of trend.

Wheat prices are forecast to maintain apremium to corn in order to limit wheat feeduse in the US. We expect CBOT Wheat prices to maintain a spread of USD 0.75/bushel toUSD 1.30/bushel over CBOT Corn pricesthroughout 2013. We believe the spread will decline to USD 0.75/bushel in Q2 due to harvest pressure from the winter wheatcrop. Conversely, the spread is likely to rise to USD 1.10/bushel in Q3 as wheat harvestpressure wanes and the corn harvest begins.With total US feed demand nearly double thesize of the domestic wheat crop, profitablewheat feeding could create significantincremental demand—with a drastic impact on already tight stocks.

Matif Wheat contracts are expected toaverage EUR 239/tonne during 2013, falling to EUR 225/tonne in Q4. The EU productiondecline of 6 million tonnes YOY to 131 milliontonnes in 2012/13 has not yet been matchedby sufficient reductions in demand. We stillexpect a 1% YOY increase in EU poultrynumbers in 2013, and the issuance of wheatexport licenses remains 3% above year-agolevels. As a result, 2012/13 stocks-to-use for

EU wheat is expected to be a record low 5.6%, a 3.8 point decline YOY. This is theprimary driver of increased spreads to CBOTWheat prices and will push demand awayfrom the EU to North America and Australia in early 2013.

We forecast Matif Wheat premiums to CBOT Wheat to be EUR 12/tonne in Q1 andEUR 10/tonne in Q2. However, with the EU2013/14 wheat harvest forecast to be at a five-year high of 144.8 million tonnes, thisspread could decline to EUR 3/tonne in Q3 2013 and back to parity by Q4 2013.

Major wheat exporting regions are forecast tosee the lowest ending stocks-to-use on recordof 11.3% in 2012/13, with the drawdown inbuffer stocks likely to increase price volatilityin 2013/14. Any supply shock in 2013 wouldthus have a large effect on wheat prices.However, downside volatility is enhanced by managed money net long positions of48,431 contracts, well above the historicalaverage of 10,374. Our forecast stocks-to-usein major exporting countries, up 3.9 points to 15.2% in 2013/14, highlights the risk ofspeculator liquidation as fundamentals turnbearish. Current implied volatility levels forDecember 2013 options remain 5 pointsunder the 10-year seasonal average of 32%—too low given the fundamental risks.

US wheat production is expected to rise 3.9% YOY to 2,357 million bushels in2013/14—the highest level since 2008/09.Winter wheat plantings in the US areexpected to reach 43.4 million acres—thelargest area since 2008 as wheat is substitutedfor cotton in the Southern Plains, particularlyin Texas. However, only 39% of the 2013/14

WHEAT

12-month outlook from spot

500

550

600

650

700

750

800

850

900

950

1,000

201320122011

USc

/bu

Historical Base case Low/high case Spot

unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

CBOT Wheat USc/bu 641 871 870 910 775 735 700Matif Wheat EUR/tonne 212 260 270 290 245 217 204

Low caseLa Niña allowsAustralian productionto rise to a recordhigh 30 milliontonnes in 2013/14

Above-trend cornyields in the US seecorn prices fall belowUSD 5.00/bushel—diminishing supportfor wheat prices

North Americanwheat productionrises but isuncompetitive on the export market

Base caseImproved conditionssee European andBlack Sea productionrebound to normallevels

Wheat feeding is scarce in the US as wheat’s premium to corn is maintained above USD 0.70/bushel

Black Sea exportablesurplus is tempered bythe need to rebuilddomestic stock levels

High caseDrought in the Black Sea regionlingers, pushing2013/14 productionbelow trend

El Niño-relateddrought causesAustralian wheatproduction to fallbelow 20 milliontonnes in 2013/14

High CBOT Cornprices lead a CBOTWheat rally

Source: Bloomberg, Rabobank, 2012

Section 2 Agri Commodity Outlooks | 7

winter wheat crop is in good or excellentcondition, the lowest on record for this pointin the year, reducing yield expectations to 46 bushels/acre—down 1.2 bushels/acre YOY.Subsequently, we expect US winter wheatproduction to reach 1,668 million bushels, up 23 million bushels YOY. Larger spreads to CBOT Corn and other competitors in thebattle for acreage are forecast to support USspring and durum wheat area, up 1.3 millionacres YOY to 15.8 million acres in 2012/13,with trend yields seeing production rise 62 million bushels YOY to 686 million bushels.

Wheat production in the Black Sea region is forecast to increase 23.9 million tonnes to 88.1 million tonnes in 2013/14, althoughproduction risk remains high. The expansionof Russian wheat production will be a keybearish influence in the grains complex, withharvested area expected to rise 3 millionhectares to 25 million hectares—the largestsince 2009/10. Ukrainian and Kazakhstaniplanted wheat area are also forecast to rise bya combined 1.3 million hectares, the majorityof which is in Ukraine. The breakdown offorecast increases in wheat production in the Black Sea region is as follows:

• 53.2 million tonnes in Russia (+15.2 million tonnes YOY)

• 15.5 million tonnes in Kazakhstan (+4.5 million tonnes YOY)

• 19.4 million tonnes in Ukraine (+4.3 million tonnes YOY)

There is more upside to these estimates thanusual as our yield estimates were tempered inparts of southern Russia by poor soil moistureand slow emergence in winter wheat areas.

However, exportable surpluses will becurtailed for the third time in five years due to the need to rebuild inventories afterstocks-to-use was almost halved to 11.3% in 2012/13—a supportive factor for wheatprices in early 2013.

Global wheat feeding is expected to increase2.6 million tonnes to 135.7 million tonnes in2013/14. Improved corn availability shouldsee wheat spreads return to near historicalaverages and discourage feeding. We believethat loosened restrictions on the types of cornthat can be imported should increase cornexports to Europe. This should mean highercorn feed rates and lower wheat use, althoughthe full impact will only be felt after severalyears. As a result, we believe EU wheat use will remain flat in 2013/14, while corn use forfeed is expected to rise 3.5 million tonnes.

Global wheat stocks-to-use is set to rise 0.8% to 24.6% in 2013/14. This is acomparatively small increase in view of the large increase in planted area. Wemaintain our forecast stocks-to-use of 23.8% in 2012/13, 1.8 points below currentUSDA estimates. Production increases in2013/14 should help avert the ninth globalwheat deficit in 14 years, with high pricesrelative to other crops helping to expandacreage of crops planted in early-to-mid 2013.

Figure 2.1: Global wheat ending stocks and stocks-to-use are forecast to rise in 2013/14

mill

ion

to

nn

es

sto

cks/

use

Ending stocks Stocks/use

Source: USDA, Rabobank, 2012

-50

-40

-30

-20

-10

0

1020

30

40

50

10

15

20

25

30

35

40

13/1

4f12

/13f

11/1

2f10

/11

09/1

008

/09

07/0

806

/07

05/0

604

/05

03/0

402

/03

01/0

200

/01

99/0

098

/99

97/9

896

/97

95/9

694

/95

93/9

492

/93

91/9

2

Figure 2.2: Wheat production in major exporting countries is expected to rebound in 2013/14 but significant production risks remain

Source: USDA, Rabobank, 2012

-80

-60

-40

-20

0

20

40

60

80

100

04/0

5

05/0

6

06/0

7

07/0

8

08/0

9

08/0

9

10/1

1

11/1

2

12/1

3f

13/1

4f

mill

ion

to

nn

es

US Argentina Australia Canada EU Black Sea

8 | Rabobank Outlook 2013—Rebalancing on a Tightrope

We expect CBOT Corn prices to fall 24% fromQ1 2013 to average USD 6/bushel in Q4 2013during the US 2013/14 harvest. Despite thebearish outlook, the beginning of 2013 isexpected to see prices rise from current levelsto encourage further demand rationing in theUS. Our Q1 2013 forecast of USD 7.90/bushelis USD 0.70/bushel higher than implied byfutures prices, with a rally expected to followthe USDA Grain Stocks report in January 2013.We believe this report will confirm furtherreductions in 2012/13 production and tighterstock levels versus current USDA estimates.The transition from Q2 to Q3 will likely be themost volatile period of 2013 as the US corncomplex transitions from a strong deficit to a moderate surplus.

US corn production of 14,100 million bushelsis the key factor in determining the CBOT Corn price decline in 2013/14—rebounding35% from the drought-induced lows of2012/13. We project that a record 97.6 millionacres will be planted in the US, furtherdisplacing soybeans as CBOT Corn prices areforecast to outperform CBOT Soybeans aheadof US planting decisions in Q1 2013. Our state-by-state model suggests that the majority ofthe 0.7 million acre increase in planted areawill be in the Northern Plains, displacingsoybeans and wheat, and in the Delta,displacing cotton. Acreage increases are notexpected in the Midwest, with disappointingcorn-on-corn yields and strong wheat pricesdriving farmers to diversify via increasedwheat and soybean plantings.

US stocks-to-use scenarios for 2013/14support a wide range between our high-endCBOT Corn price forecast of USD 7.50/busheland our low-end scenario of USD 4.50/bushel

for Q4 2013. Our base case scenario showsstocks-to-use rising to 13.6% although weacknowledge significant risks to our return-to-trend yield forecast. We adopt a trend yield forecast of 157 bushels/acre for US corn in 2013/14, with a range between 169 bushels/acre and 145 bushels/acreencompassing two-thirds of likely outcomes.

Evidence from recent years suggests that thefirst decade of the new millennium producedbenign yield variability and that yieldvolatility should be wider in future years,including 2013/14. Adjusting for demandelasticity, our yield scenarios imply stocks-to-use between 6.0% and 16.4% in 2013/14—supportive of the wide spread in our pricescenarios. There is already heightened risk toyields in 2013/14 as 38% of the contiguous US remained in severe drought as at 6 November—14 points above year-agolevels. Despite these risks, market indicatorssuggest above-average levels of confidence in price outcomes, with the implied volatilityof December 2013 CBOT Corn contracts 4 points under the historical average of 28% for November—which our analysissuggests is too low.

Record corn production in South America in 2012/13 is expected to contribute to priceweakness. We forecast corn production inBrazil and Argentina to reach 97.3 milliontonnes, although high yield volatilitymagnifies production risk relative to the US.Focus on South American production duringQ1 2013 should help deferred corn futuresshift lower than implied futures, with marketfocus shifting to the US in Q2. Compared to2011/12, when drought significantly impactedyields in Argentina, these production

CORN

12-month outlook from spot

400

450

500

550

600

650

700

750

800

850

201320122011

USc

/bu

Historical Base case Low/high case Spot

unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

CBOT Corn USc/bu 618 783 740 790 700 625 600

Low caseUS corn yields reach a record 169 bushels/acre

Renewable FuelStandard is modified to substantiallyreduce US ethanolproduction

Above-trend South Americanproduction limits US corn exportprogramme

Base caseTrend-line yields in the US seeproduction rise 35% YOY to 14,100 millionbushels

US ethanol demandrebounds to 5,050 million bushels

US feed and residualuse rises to 4,800 million bushels

High casePoor conditions result in US corn yields of 145 bushels/acre

Delayed plantingtempers safrinha corn yields in Brazil

Crude oil prices aboveUSD 120/barrel liftethanol productionabove 4,500 millionbushels

Source: Bloomberg, Rabobank, 2012

Section 2 Agri Commodity Outlooks | 9

forecasts represent an increase of 3.5 milliontonnes for the region. We forecast productionof 24 million tonnes in Argentina for2012/13—4 million tonnes below currentUSDA estimates. Brazilian production isexpected to be roughly flat YOY at 73.3 milliontonnes as yields are tempered from abovetrend levels in 2011/12. Despite recordproduction, the movement of more Brazilianland to double-cropping (planting corn aftersoybeans) increases production risks.

We expect Chinese import demand to reach 5 million tonnes in 2013/14, 3 million tonnesabove USDA estimates for 2012/13 and asupportive factor for prices. CBOT Corn pricedeclines in mid-2013, due to US and SouthAmerican harvests, are expected to be tempered by ‘buy the dip’ procurement from China, with domestic production unable to meet growing demand. Ongoingindustrialisation of the animal proteinindustry is expected to support feed demandgrowth in China. Despite slowing economicgrowth, we believe Chinese expansion isrobust enough to support increases of 7%YOY in 2012/13. This would increase totalChinese feed demand to 141 million tonnes in 2012/13. Upside price risk from increasedChinese imports is significant as Chinese feeduse is by far the largest source of demand inthe global corn sector, and is 36% larger thantotal US corn feed use. Any significant declinein Chinese corn production in 2013/14 wouldhave a substantial bullish effect on CBOT Cornprices as imports would rise. As US pricesdecline, we expect Chinese prices to remainsupported by government policies,encouraging imports. This means profitableimport margins are likely in 2H 2013,supporting an estimate higher than USDA forecasts.

Corn stocks in the US are likely to be minimalby 31 August 2013 as we believe the USDAcontinues to overstate US production, withfeed demand running at an unsustainablepace. Demand for US corn has slowed,particularly from the ethanol sector and forexport, but the pace of feed use is too high in view of current supply constraints. Total2012/13 US corn production was 1 billionbushels below the previous year’s total use,highlighting the need for immediate demandrationing, with only 988 million bushels ofstocks entering 2012/13. Our calculationssuggest that US domestic consumption,absent significant imports, must decline 11% YOY in 2012/13—well above currentindicators of a 5% to 6% reduction YOY. The need to further ration feed and ethanoluse to meet our targets, or encourageadditional imports, is key to our forecast for a CBOT Corn rally in Q1 2013.

We expect global corn stocks-to-use toimprove 3.5 points YOY to 15.9% in 2013/14,which is still substantially below the 10-yearaverage of 17.2%. Strengthening globalconsumption of corn—up 59 million tonnesYOY to 911 million tonnes in 2013/14—isforecast to prevent stocks-to-use levels fromrecovering to long run average levels. Weexpect the largest ever YOY increase in world corn demand in 2013/14, 43 milliontonnes above the previous record use in2011/12. The majority of this increase willcome from consumption growth in the USand China, 34 million and 13 million tonnesYOY, respectively.

Figure 2.3: World and US corn stocks-to-use are forecast to rebound in 2013/14

per

cen

t

World US

Source: USDA, Rabobank, 2012

0

5

10

15

20

25

30

13/1

4f

12/1

3f

11/1

2f

10/1

1

09/1

0

08/0

9

07/0

8

06/0

7

05/0

6

04/0

5

03/0

4

02/0

3

01/0

2

Figure 2.4: Corn production in major exporting countries is expected to see record growth YOY in 2013/14

Source: USDA, Rabobank, 2012

-60

-40

-20

0

20

40

60

80

100

01/0

2

03/0

4

02/0

3

05/0

6

04/0

5

07/0

8

06/0

7

09/1

0

08/0

9

11/1

2

10/1

1

13/1

4f

12/1

3f

mill

ion

to

nn

es

US Brazil Argentina South Africa Ukraine

Soybean prices are expected to remainsupported in Q1 2013 on tight export suppliesbefore declining as production rebounds laterin the year, with prices for the year averagingbelow 2012 levels. In our view, the currentglobal supply shortage of soybeans, a result ofdrought in both North and South America lastseason, has not been fully accounted for inprices. Although we expect record large SouthAmerican production will come online in 2H 2012/13 and result in lower prices in 2013,we believe prices will rebound from currentlevels until this crop is available in March. The CBOT Soybean futures curve remains inbackwardation, which indicates the marketcontinues to price in higher supplies in 2013,although at values below our forecasts. Webelieve speculative liquidation has pressuredprices in Q4 2012 below fair values and thismay persist in the short term. Managed moneyhas reduced its net long position in CBOTSoybeans by 50% from the record high253,889 contracts reached in May 2012.However, its position remains 45% above the five-year average. This is in contrast tofundamentals which suggest global soybeansupplies will remain tight in 2013 asproduction in the Americas is expected torebound 38.8 million tonnes YOY in 2012/13,while global stocks-to-use will persist below23% for a second consecutive year.

It will likely take multiple seasons to replenishglobal soybean supplies to adequate levels asweather and capacity constraints continue tohinder production. We forecast global stocks-to-use for soybeans at 22.1% in 2012/13—0.9 points below USDA’s November forecast.This is despite our forecast for an increase inworld production of 29 million tonnes (largely

on South America’s crop) reaching 266 milliontonnes—a record high. Corn is forecast tocontinue winning the battle for acreage in the US, which will result in only a modestexpansion in Northern Hemisphere soybeanoutput. We expect China’s demand will remainstrong, rising to nearly 30% of global soybeanconsumption, up from only 15% 10 years ago.Seemingly inelastic demand from China willincreasingly price other major importingcountries out of the market and will also resultin a historically high floor price for internationalsoybean values. Even with trend yieldassumptions, the global soybean balance sheet is likely to remain tight in 2012/13,leaving little room for error. Our forecasts arebased on normalised weather in the newseason, and if additional supply shocks areexperienced, we see considerable upside riskto our price forecasts.

We expect South America’s soybean output to recover 30% from year-ago levels to reachrecord levels in 2012/13 and be a bearish factorfor prices. However, we believe Brazil’s outputwill fall below USDA’s November forecast of 81 million tonnes as our estimates show moremodest area and yield expansions. We forecastBrazil’s harvested area in 2012/13 to reach 26.9 million hectares, which would be thelargest YOY increase in eight years, after recordhigh prices have encouraged farmers to plantmore. This is 642,000 hectares below USDA’sexpectations, and there is a risk that even ourestimate is too high. Argentina’s harvested areais also expected to increase, reaching a recordlarge 20 million hectares in 2012/13. Yields arealso expected to recover from last season’sdrought induced decline.

SOYBEANS

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

USc/bu 1,426 1,677 1,450 1,475 1,400 1,350 1,300

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

201320122011

USc

/bu

Historical Base case Low/high case Spot

Low caseImproved SouthAmerican weatherallows production in Brazil to exceed 81 million tonnes

China’s importdemand growth slowsto less than 4% YOY

Strengthening USdollar and crude oilbelow USD 100/barrelslow global demandgrowth

Base caseGlobal soybeandemand growthremains below the five-year average at 2% YOY

Record SouthAmericanproduction

China’s importdemand grows 6% YOY

High casePoor weather causesBrazil’s 2012/13 cropto drop below 78million tonnes

China’s importdemand grows morethan 8% YOY

Crude oil is above USD 120/barrel and global demandgrowth is higherthan expected

Source: Bloomberg, Rabobank, 2012

10 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Section 2 Agri Commodity Outlooks | 11

If trendline yields are achieved, Brazil’s yield will be 11% higher YOY at 2.97 tonnes/hectare, and Argentina’s will be up 30% YOY at 2.8 tonnes/hectare. As a result, we forecastBrazil’s harvest to increase 13.3 million tonnesYOY to 79.8 million tonnes and Argentina’sharvest to be 16 million tonnes higher YOY at 55 million tonnes.

Price volatility is expected to remain high asthe world’s dependence on South Americansupply increases. Relative to export suppliesfrom the US, South American supply is lessreliable given the inherent yield variability,increased political risk and greater logisticalchallenges. We believe that Q4 2012 pricelevels currently underestimate production risksand that the price response to any downwardproduction estimates will be large. Adverseweather has delayed plantings and may causeyields to drop below trend. Furthermore, largeexport volumes will be needed to offset thedrawdown in US stocks in early 2013, whichwill likely be bullish for prices. The delayedplantings and frequent logistical issues in bothcountries are likely to add to price and volatilityupside in Q1 2013.

US soybean area planted is likely to declineslightly YOY in 2013/14, and we expect theprice ratio to corn to remain below 2.3 in early2013 in order to incentivise higher corn area.US soybean stocks-to-use are forecast todecline 0.8 points YOY to 4.6% as productionfalls to a five-year low of 2.98 billion bushels in2012/13. Strong domestic crush, as a result ofhigh soymeal demand, and a large exportprogramme are likely to push ending stocks tothe lowest level since 2008/09 at 189 millionbushels. Despite this, we expect cornproduction in South America to show a smallerYOY increase than soybeans, which we expectwill cause CBOT Corn prices to outperformCBOT Soybean prices ahead of US plantings—

keeping the soybean-to-corn price ratio below2.3. As a result, we forecast a decline in USsoybean planted area of 400,000 acres to 76.8 million acres but expect that lessabandonment will result in a 200,000 acreincrease in harvested area to 75.9 million acres.A trend yield of 42.2 bushels/acre would result in US soybean production increasing 219 million bushels YOY to 3.2 billion bushels.

China’s soybean import demand will be a keybullish factor for CBOT Soybean prices in 2013.We forecast China’s soybean imports to rise 6% YOY to 62.5 million tonnes for 2012/13 anda further 7% in 2013/14 to 67 million tonnes.We believe China’s structural shift towardsincreased soybean imports will persist.Evidence of this can be seen through thecontinued growth of crush capacity near keycoastal areas and government-set prices forsoybeans, which have tended to be low inrelation to set prices for corn or rice. Weforecast China’s domestic soybean crop for2012/13 to be 9% below USDA’s Novemberforecast, with a further 3% drop likely in2013/14. At the same time, we believe theeconomics of crush margins will continue toplay a diminished role in predicting importpace. The Chinese government hasdemonstrated a strong desire to contain foodinflation and this is likely to persist into 2013,particularly given the recent leadershipchange. The support for crush margins throughthe release of strategic reserves to only somecrushers along with state support payments,have been supportive for crush volumes. Webelieve this strong demand combined with thedrawdown in strategic reserves will likely drivehigher imports in 2013, with prices being lessof a determinant. China remained a strongsoybean buyer despite CBOT Soybean pricesaveraging well over USD 15/bushel inSeptember and October 2012.

Figure 2.5: China’s soybean imports continue to increase despite CBOT Soybean price increase of USc 400/bushel

mill

ion

to

nn

es

Source: Bloomberg, Rabobank, 2012

-800

-400

0

400

800

1,200

-2

-1

0

1

2

3

08/0

9

09/1

0

10/1

1

11/1

2

12/1

3

CB

OT

Soyb

ean

pri

ce c

han

ge

(USc

/bu

shel

)

YOY change soybean imports YOY price change (RHS)

Figure 2.6: Global soybean stocks-to-use forecast will remain low despite increased stocks in major exporting countries

YO

Y p

rod

uct

ion

ch

ang

e (m

illio

n t

on

nes

)

per

cen

t

Source: USDA, Rabobank, 2012

19

21

23

25

27

29

-20

-15

-10

-5

0

5

10

15

01/0

2

03/0

4

05/0

6

07/0

8

09/1

0

11/1

2f

13/1

4f

US Argentina Brazil Global stocks-to-use (RHS)

12 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Soy oil prices are forecast to remain range-bound at the beginning of 2013 on high USsupplies, before increasing in mid-2013 assupplies are drawn down. CBOT Soy oil priceslargely underperformed the grains and oilseedscomplex in 2012 as strong crush marginsencouraged US soy oil production and globalpalm oil availability was high. We expect thisdynamic will continue in early 2013, particularlygiven the supply shortage of soymeal, whichcontinues to drive crush margins and thuscrush volumes in the US. However, as USsoybean supplies are drawn down after Q1 2013 and global soybean demand shifts toSouth America, we expect this will prove bullishfor CBOT Soy oil prices. We forecast the US willbe in deficit for vegetable oils in 2H 2012/13 as soybean crush volumes slow and the biofuel mandate increases.

US biodiesel demand is likely to prove a key bullish factor for CBOT Soy oil prices in

mid-2013. The US mandate for biodiesel in2012 is 1 billion gallons and will increase to 1.28 billion gallons in 2013. According to the US Energy Information Administration,2.89 million pounds of soy oil was used toproduce biodiesel in the first nine months of 2012. Total production of biodiesel for 2012is likely to exceed 1.1 billion gallons with theexcess production used to meet the totaladvanced biofuel mandate. On a marketingyear basis, the current pace of output wouldimply US soy oil demand for biodieselproduction would be flat YOY in 2012/13.However, there is upside to this estimategiven spillover demand from the totaladvance biofuel mandate, which is unlikely to be met entirely with Brazil ethanol imports.We expect this will create additional soy oildemand at the same time as US soy oil outputslows and will prove bullish for CBOT Soy oilprices in mid-2013.

SOY OIL

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

USc/lb 52.3 54.0 48.0 49.0 50.0 50.0 49.0

40

42

44

46

48

50

52

54

56

58

60

201320122011

USc

/lb

Historical Base case Low/high case Spot

Low case Record large ethanolimports from Brazilfulfil the US advancedbiofuel mandate

Crude oil prices dropbelow USD 100/barrel

The EU furthercurtails biofuelmandates

Base caseUS soy oil biodieselproductioncontinues toincrease

US stocks tighten in 2H 2012/13 as soy oil supplies are drawn down

Brazil’s ethanolblend mandate isincreased, limitingexports to the US

High caseStrong US biodieseldemand is spurredby reduced Brazilethanol exports andrising energy prices

Other vegetable oilproduction is lowerthan expected

Argentina’sproduction fallsbelow expectations

Source: Bloomberg, Rabobank, 2012

Figure 2.7: Global soy oil stocks-to-use is forecast at a 44-year low in 2012/13, supporting prices

per

cen

t

USc

/lb

Stocks-to-use Price (RHS)

Source: USDA, Bloomberg, Rabobank, 2012

10

20

30

40

50

60

70

7

8

9

10

11

12

13

14

15

16

17

77/7

8

79/8

0

81/8

2

83/8

4

85/8

6

87/8

8

89/9

0

91/9

2

93/9

4

95/9

6

97/9

8

99/0

0

01/0

2

03/0

4

05/0

6

07/0

8

09/1

0

11/1

2f

13/1

4f

Figure 2.8: A deficit is forecast for US soy oil as demand remains high and production falls

bill

ion

lb

Production Domestic consumption

Source: USDA, Rabobank, 2012

15

16

17

18

19

20

21

13

/14

f

12

/13

f

11

/12

f

10

/11

09

/10

08

/09

07

/08

06

/07

05

/06

04

/05

03

/04

02

/03

01

/02

00

/01

Section 2 Agri Commodity Outlooks | 13

CBOT Soymeal prices are likely to drop bynearly USD 75/ton from current levels by the end of 2013 as demand slows. Key to ourbearish CBOT Soymeal price forecast is ourexpectation for demand growth to slow in 2013 and a rebound in soybean production toincrease supplies. Hog and poultry producershave seen their margins squeezed in 2012,which will likely result in a contraction in animalnumbers and a slowdown in global feeddemand for soymeal. Our forecast is based onCBOT Soymeal prices remaining elevated untilat least the end of Q1 2013. We forecast globalsoymeal demand growth will be less than 2% in 2012/13 reaching 178.9 million tonnes. In our forecasts, China remains a clear outliercompared to price responsive countries. Weexpect Chinese demand to remain strong as crush increases 7% YOY in 2012/13, driven by continued soybean import growth.

As soymeal demand slows, we expect CBOTSoymeal prices to underperform relative toCBOT Soybeans and CBOT Soy oil in 2013. Weexpect crush margins to contract in 2013 andoil share to rebound. Given CBOT Soymeal’srelative outperformance to CBOT Soy oil in 2012 we expect to see a pronounced drop inconsumption past Q1 2013, whereas US soy oil demand is likely to be more robust due tothe increased biofuel mandate. We expectfundamentals to diverge as soymeal demandgrowth slows and US soy oil demand continuesto grow, which will push oil share higher in2013. Furthermore, China’s strong soybeanimport demand is likely to limit CBOT Soybeanprice downside, which will result in contractingcrush margins. We believe this will cause asignificant divergence for prices in 2013 andwill result in bearish CBOT Soymeal price movesbut bullish CBOT Soy oil price moves.

SOYMEAL

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

USD/ton 413 514 450 450 425 375 350

0

100

200

300

400

500

600

201320122011

USD

/to

n

Historical Base case Low/high case Spot

Low case Global feed demandfalls more than 2%

Higher planted areaand improvedweather increasesoybean productionabove expectations inthe Americas

Negative macrofactors promptspeculativeselling/shorting

Base caseGlobal feed demand increasesless than 1%

Prices remain above USD 415/tonthrough Q1 2013

South Americansoybean productionis up 32.4 milliontonnes

High caseGlobal soybeanproduction fallsbelow our base caseestimates

Rising hog andpoultry pricessustain demandgrowth above 2%

China’s soybeanimport demandexceeds 64 milliontonnes

Source: Bloomberg, Rabobank, 2012

Figure 2.10: US soymeal production is forecast to remain high in 1H 2012/13 before slowing in 2H 2012/13

mil

lio

n t

on

s

09/10

Source: Bloomberg, NOPA, Rabobank, 2012

10/11 11/12 12/13

2.0

2.5

3.0

3.5

4.0

Au

g

Jul

Jun

May

Ap

r

Mar

Feb

Jan

Dec

NovOct

Sep

Figure 2.9: Global soymeal demand growth is forecast to slow for 2012/13 as a result of record high prices

mill

ion

to

nn

es

USD

/to

n

YOY change global soymeal feed demand Price (RHS)

Source: USDA, Bloomberg, Rabobank, 2012

0

100

200

300

400

500

600

-6

-4

-2

0

2

4

6

8

10

71/7

2

76/7

7

81/8

2

86/8

7

91/9

2

96/9

7

01/0

2

06/0

7

11/1

2f

14 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Palm oil prices are forecast to rise in Q1 2013as stocks are drawn down from record highlevels before falling later in the year as palmoil and soybean output rebound. Significantlyhigher seasonal output coupled with waningdemand caused Malaysia’s palm oil stocks toreach a record large 2.51 million tonnes inOctober. Falling energy prices added to thebearish sentiment and caused prices to fall toa two-year low of less than MYR 2,100/tonne.We expect stock levels to decline in early 2013as production slows seasonally and palm oil’sprice discount relative to alternativevegetable oils encourages end user buying.However, we do not expect prices to reachnew highs as a rebound in domestic oilseedproduction in India and slowing demand forEU biodiesel limit demand growth.

Global palm oil production is likely tocontinue reaching new highs, limiting price upside. We forecast global palm oilproduction to increase 6% YOY in 2012/13 to 53.6 million tonnes—0.25 million tonnesmore than USDA’s forecast. The bulk of thisgrowth will emanate from Indonesia, wherewe forecast production to be up 1.8 milliontonnes to 27.2 million tonnes. Malaysia’soutput is also forecast to recover afterdropping in 2011/12. We expect Malaysia’soutput to rise 450 thousand tonnes to 18.7 million tonnes. Global production willcontinue to be concentrated in these twocountries at 86% of total world palm oilproduction. We base our productionexpectations on current weather forecasts,which do not see an El Niño weather patterndeveloping in 2013. If this changes and ElNiño does develop, this will be a key

downside risk to our output projections andlikely a bullish factor for prices.

An uncertain outlook for future EU biodieseldemand will limit palm oil export potential.This has been driven by the increased amountof double-counting allowances, quotasystems and a recent anti-dumping probe.Although biodiesel quotas continue toincrease in Europe, this does not necessarilytranslate into higher physical demand forbiodiesel. The European Commission recentlyannounced an investigation into whetherbiodiesel exports from Argentina andIndonesia have been sold at prices belowcost. This anti-dumping probe will be decidedin 2013 and could result in anti-dumpingduties for half a year. Additionally, the EUrecently proposed to cap the share of energyfrom food crop based biofuels at 5%—downfrom their original 10% target by 2020. Thiswould essentially limit future biodieseldemand in Europe and is a key bearish risk toMDEX Palm oil prices. Where double-countingis allowed, physical demand is essentiallyhalved. We therefore use a base case scenariothat EU biodiesel consumption and importswill decline in 2013, which will reducedemand for Indonesia’s biodiesel exports.However, higher EU non-biodiesel industrialdemand will continue to be supportive ofhigher palm oil imports in 2012/13.

Demand in India is forecast to continue itssteady growth and be a supportive factor for palm oil prices in 2013. The combineddomestic production of rapeseed andsoybeans is forecast to rebound 0.8 milliontonnes YOY in 2012/13 to 18.3 milliontonnes—due primarily to a record large

PALM OIL

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

Palm oil MYR/tonne 3,225 2,884 2,360 2,800 3,000 2,800 2,700

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

201320122011

MY

R/t

on

ne

Historical Base case Low/high case Spot

Low caseGlobal biodieseldemand declinesfurther

Palm oil productionincreases more than7% globally

Crude oil price falls below USD 100/barrel

Base caseGlobal oilseedproduction increases5% in 2012/13 and2% in 2013/14

Global palm oiloutput grows 5%-6%

Palm oilconsumptionincreases 4%-6%

High caseGlobal oilseedproduction remainsflat YOY

Global palm oilproduction increases3% or less

Crude oil price is above USD 120/barrel

Source: Bloomberg, Rabobank, 2012

Section 2 Agri Commodity Outlooks | 15

soybean crop. With increased domestic crushavailability, we expect India’s oil output to benearly 120 thousand tonnes higher YOY in2012/13. However, we expect this to beslightly lower than demand growth, whichhas averaged 10% during the past five years. As a result, we believe India’s reliance on palmoil imports to meet growing food demandwill continue to increase, reaching a record-large consumption level of more than 55% in 2012/13. We forecast palm oil imports willgrow 2% YOY in 2012/13 to 8 million tonnes.This will be a key supportive factor for MDEXPalm oil prices.

China’s palm oil import demand mayapproach record levels in 2012/13, whichcould prove bullish for prices. Decliningdomestic oilseed availability in China is likelyto continue to drive import demand for palmoil in 2012/13. We forecast China’s soybeanimports to increase 3.3 million tonnes YOYbut reduced Canadian rapeseed productionwill lower rapeseed imports 622,000 tonnesYOY in 2012/13. This will limit China’s onshorecrush growth. China’s demand growth forvegetable oils over the past five years hasaveraged 7%. Although we forecast this tomoderate in 2012/13 and substitution is not1:1, the reduced growth rate of domesticallycrushed oilseeds is likely to prompt higherpalm oil imports. Our forecast for China toimport 6.2 million tonnes of palm oil in2012/13 is above the record high reached in2008/09 but below USDA’s 6.4 million tonneNovember 2012 forecast. A key risk to ourforecast is our domestic crush projections inChina, which could be lower than expected if South American soybean production fallsshort, or higher than expected if China’soilseed production increases.

Palm oil price downside will likely be limitedas its value has dropped to near historicallows relative to other oils. While production of other oilseeds has been hampered due toadverse weather last season, palm oil outputcontinues to reach new highs. This has causedprices to diverge as palm oil’s underlyingfundamentals appear relatively bearish. In 2H 2012, MDEX Palm oil’s price discount toCBOT Soy oil increased to the highest levelsince the global financial crisis at more thanUSD 400/tonne. Values dropped below that of Brent Crude oil in late September 2012 and have continued to diverge, widening toas much as a USD 90/tonne discount to crude.We believe MDEX Palm oil prices have littledownside relative to other oils and do notexpect valuations to further diverge in 2013.

Palm oil supplies are likely to be drawn downin Q1 2013, which will drive prices higher. The bearish sentiment which has persisted in MDEX Palm oil prices is likely to wane asproduction slows seasonally in early 2013.Although we expect stocks to remainhistorically high for the remainder of 2012, we believe MDEX Palm oil’s attractive pricelevels relative to other oils and the tighteningsupply of soybeans will spur end userdemand and draw down stocks in early 2013.Palm oil production in Malaysia tends to behigher in the second half of the calendar yearand then drop 18% lower in January-March.However, in recent years, this cyclicality hasintensified with a production decline of morethan 20% from Q4 to Q1 in three out of thepast four years. Given the record highproduction levels which have occurred so farin Q4 2012, we expect to see a pronounceddrop in production in Q1. This will likely occur simultaneously with the anticipatedtightening of soybean supplies, which we expect to further drive prices higher.

Figure 2.11: MDEX Palm oil price relative to other oils has dropped to the lowest level since 2008

Source: Bloomberg, Rabobank, 2012

200

400

600

800

1,000

1,200

1,400

1,600

2007

2008

2009

2010

2011

2012

US

D/t

on

ne

Crude oil Soy oil Palm oil

Figure 2.12: Palm oil stocks in major exporting countries are forecast to decline in 2012/13 but remain historically high

mill

ion

to

nn

es

per

cen

t

Malaysia Stocks-to-use (RHS)Indonesia

Source: USDA, Rabobank, 2012

0

1

2

3

4

5

4

6

8

10

12

13/1

4f12

/13f

11/1

210

/11

09/1

008

/09

07/0

806

/07

05/0

604

/05

03/0

402

/03

01/0

200

/01

99/0

098

/99

97/9

896

/97

95/9

694

/95

93/9

492

/93

91/9

2

16 | Rabobank Outlook 2013—Rebalancing on a Tightrope

Sugar prices (ICE #11 contract) are forecast to ease 5% over the next 12 months as world sugar supply reaches a net surplus of5.9 million tonnes. While the magnitude ofthis net surplus remains a key variable to ourprice forecast, current projections suggeststocks-to-use returning to the 10-year averageand the lowest annual average prices since2009. We view market expectations of a largerBrazilian sugarcane crop in 2013 and theincreased inventories from the current seasonas tempering bullish market sentiment in2013. Risks of supply side disruption remain aconstant and with the large speculator grossshort position anticipated to remain in 2013,the market is highly exposed to short coveringrallies. However, if our base case crop scenariosare realised, there will be a sufficient supply ofsugar in the market, with much of it yet to besold. Risk of downside bias is elevated, but thealready bearish positioning of the funds andthe ethanol dynamic in Brazil as well asproduction risk premiums are expected to limit sustained price movement below USc 18/pound.

Brazil, the largest producer and exporter ofsugar, is the focal point for the internationalmarket. Crop expectations along with policymoves will dictate speculator positioning andthe available supply of exportable sugar. The2013 raw sugar supply from Brazil will be afunction of crop sizes as well as the share of sugarcane processed for ethanol. Weexpect the allocation of sugarcane to ethanolto increase in the new season. However, the increase in sugarcane will also allow an increase in raw sugar production. Earlyprojections for the sugarcane crop in the

Centre/South region in 2013/14 is for anincrease on the 2012/13 crop estimate of 520 million tonnes.

Given the weather still to come, it is difficult to project Brazil’s 2013/14 sugarcane crop with confidence, but early market expectationsare for an improvement from the currentseason with forecasts ranging between 530 million tonnes and 580 million tonnes forthe Centre/South. The age of the sugarcaneplantation will remain above optimal in 2013,but replanting has continued to lower it fortwo consecutive seasons thus supportingagricultural yield potential in 2013. The rangeof outcomes is wide for the Centre/South crop given potential crop sizes and allocationbetween ethanol and sugar. However, 35 million tonnes of raw sugar, or 2 million to 3 million tonnes above the current cropforecast, are certainly possible. We anticipatethat market expectations for a largersugarcane harvest and the potential for anincrease in raw sugar supply from Brazil in2013 will keep speculator positioning bearishand users looking to buy sugar at prices belowUSc 20/pound.

Brazilian ethanol policy impacts the share ofsugarcane available for raw sugar production.Therefore, anticipation that the governmentwill implement moderate measures tosupport mills is expected to be a positivefactor for sugar prices in 2013. Policy-makershave signalled a likely increase in theanhydrous blending rate back to 25% from20%, but so far, the government has shown nosign of shifting the ethanol demand curve byincreasing gasoline prices or reducing taxes in2013. The hydrous ethanol parity, which

SUGAR

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

Sugar USc/lb 21.2 21.0 19.5 19.0 19.0 18.5 18.5

0

5

10

15

20

25

30

35

201320122011

USc

/lb

Historical Base case Low/high case Spot

Low caseEven at lower prices,import demand isdiminished as stocklevels are seen ascomfortable

The macroeconomicenvironmentdeteriorates, promptingindex funds to liquidatesugar positions

Sugarcane output inBrazil reaches the highend of expectations and ethanol profitabilityremains low

Base caseProduction in Brazil meets earlyexpectations, resultingin an increase in rawsugar supply

Prices for spring wheatshift lower in 2013,resulting in less shiftout of beet in theNorthern Hemisphere

Indian productionrealises currentexpectations and does not shift lower

High caseIndian sugar productiondoes not meetexpectations and importsreduce the forecast globalsurplus and tightenending stocks

The Brazilian governmentincreases the gasolineprice or implements otherpolicy measures that raiseethanol demand,potentially reducingsugar supply

Consumption isunderestimated and newseason demand pushesprices higher

Source: Bloomberg, Rabobank, 2012

Section 2 Agri Commodity Outlooks | 17

averaged just below USc 18/pound in 2012YTD, will remain a key supportive factor forinternational sugar prices as mills can beexpected to concentrate on ethanolproduction if sugar prices fall below the paritylevel. International raw sugar prices never fellbelow the parity in 2012, which would havecaused mills to focus on maximising sugarproduction, with the share of sugar forecast to be 48% to 49% by the end of the 2012/13season, a multi-year high. In 2013, thesugarcane share devoted to sugar is forecastto fall due to increased ethanol demand andlower sugar prices. Despite this forecast, thetotal raw sugar output is expected to behigher YOY due to a larger sugarcane crop.

Brazil’s sugar industry has been underfinancial pressure due to increasingproduction costs, negative weather impactsand lower availability of sugarcane. Thefinancial situation of many Brazilian millssuggests that they need raw sugar pricesabove USc 20/pound to operate profitably,although this depends greatly on ethanolprices. Production costs in the new seasoncan be expected to fall due to an increase in sugarcane supplies, but this will only have a moderate impact. With greater support from ethanol sales and higher sugarcaneavailability, the mills’ profitability may bebetter in 2013, but reticence to sell sugarbelow USc 20/pound is likely to be strong,which is a positive factor for prices.

Indian sugar production is lower on a reducedmonsoon, and a risk premium will likelyremain in the market until harvest. However,international price impacts are anticipated tobe moderate. The 2012/13 crop is forecast tobe 2.5 million tonnes to 3 million tonnes downYOY, but sufficient for domestic demand.Estimated ending stocks of 4 million tonnes to4.5 million tonnes in 2012/13 are a buffer for

supply disruptions and the outlook suggestsfarmer payment arrears may not increase in2013. For 2013/14, we do not expect a majorchange to acreage, suggesting that if weatheris supportive, production will again coverdomestic consumption. In our view, Indiansupply risks still exist in the sugar market, butsupply dynamics suggest the balance sheetwill not shift into deficit.

The large Russian beet crops of the currentand past seasons may not be equalled in2013/14 as high grain prices and fallingdomestic beet prices result in land shifting out of beet production. Ending stocks builtover the past two seasons are anticipated totemper price reaction if planting expectationsare reduced in 2013. This dynamic could alsoreduce land under beet in the EU and Ukraine.The scale of this shift is likely to be modestrelative to total supply of sugar, but we expectit to be one of the supportive factors keepinginternational values near our forecasts.

Sugar imports to China doubled in 2011/12from the previous season and have had apositive impact on international prices in2012, but this is not expected to continue in 2013. A large domestic sugar crop, up 12% YOY to 12.9 million tonnes for 2012/13,implies Chinese import needs will besignificantly reduced in 2013. If China and other structural importers in Asia,including Indonesia, buy more sugar on the international market to further increaseinventories, we anticipate interest only wheninternational prices are low, likely below USc 20/pound. If international values movehigher, we anticipate the short-term demand profile will shrink quickly. With better domestic and international supply,importers can become disciplined buyers,which is expected to support our lateral price forecasts.

Figure 2.13: The hydrous ethanol sugar equivalent has been a resistance factor for sugar prices

Source: Bloomberg, Rabobank, 2012

USc

/lb

Spread Raw sugar #11 Hydrous ethanol equivalent

-5

0

5

10

15

20

25

30

35

Oct

-12

Au

g-1

2

Jun

-12

Ap

r-12

Feb

-12

Dec

-11

Oct

-11

Au

g-1

1

Jun

-11

Ap

r-11

Feb

-11

Dec

-10

Oct

-10

Au

g-1

0

Jun

-10

Ap

r-10

Feb

-10

Figure 2.14: Global sugar ending stocks are forecast to grow for the third consecutive season

mill

ion

to

nn

es

per

cen

t

Surplus/deficit Stocks/use (RHS)

Source: Rabobank, 2012

-15

-10

-5

0

5

10

30

32

34

36

38

40

42

44

46

48

50

12/1

3f

11/1

2f

10/1

1f

09/1

0

08/0

9

07/0

8

06/0

7

05/0

6

04/0

5

03/0

4

02/0

3

01/0

2

2000

/01

18 | Rabobank Outlook 2013—Rebalancing on a Tightrope

COFFEE

12-month outlook from spot unit Q2’12 Q3’12 Q4’12f Q1’13f Q2’13f Q3’13f Q4’13f

ICE USc/lb 170 172 155 160 170 175 170

Liffe USD/tonne 2,066 2,095 2,000 2,050 2,075 2,100 2,075

0

50

100

150

200

250

300

350

201320122011

USc

/lb

Historical Base case Low/high case Spot

Low caseBrazilian farmerspanic-sell stored coffee

An emerging marketsslump reducesRobusta demand

Demand for Arabicacontinues to slump asrecession constrainsconsumption

Base caseA second largeVietnamese croptempers speculatordemand for Robusta

Brazilian 2013 off-season Arabica cropshifts global balanceinto a deficit

Roaster buyingincreases in Q1-Q2 2013

High caseDemand for washedArabica increases onimproved economicgrowth

Frost or other bullishnews prompts majorspeculator shortcovering in Arabica

Vietnamese cropestimates are reduced

Source: Bloomberg, Rabobank, 2012

Coffee prices are expected to increase in 2013 finding support from increasing globaldemand and tightening stock levels. Arabicaprices are down over 52% from the 2011 high.However, in our view, a potential deficit seasonin 2013/14 and an already large shortspeculator position will temper furtherdownside. Robusta market prices arecontingent on the Vietnamese crop, and as the current outlook is positive, we do notanticipate major rallies but expect moderatelyhigher prices in 2013. The price differencebetween coffee varieties has settled to a levelwhere we anticipate stability in the comingyear. The range-bound outlook for the spreadbetween Arabica and Robusta prices in 2013 is a function of our forecast for less volatileprice action in the Arabica market. Coffeeconsumption has not decreased but demandhas largely moved away from washed Arabicato Brazilian natural Arabica or Robusta, whichhas shifted differentials closer. This dynamic is a focal point in our forecasts for mostly lateralbut positive movement in 2013.

Arabica fundamentals are forecast to be insurplus for 2012/13, which will be a bearishaspect weighing on prices in late 2012 andearly 2013 due to investor shorting and hand-to-mouth roaster buying. We anticipatemarket prices will hit a bottom in 2012, with a positive outlook in 2013 based on newseason fundamentals and increased buying.Our 2012/13 fundamental forecast for Arabicais for a 4.1 million bag surplus, while earlyprojections for 2013/14 suggest a likelydeficit. The Arabica price outlook in 2013 is positive due to this potential deficit,anticipated roaster buying and Brazilianfarmers holding supply off the market.

Farmers in Brazil still have a significantamount of 2012 Arabica harvest to sell on the market, but given their well-capitalisedposition and government subsidies forstorage, we anticipate the supply from Brazilwill arrive only if prices are attractive—likelyabove USc 160/pound in NY. The speculatorgross short position, which is near historichighs, is expected to be pared back in 2013 as the deficit season looms. The gross shortposition is equivalent to 14 million bags ofcoffee, and a reduction in 2013 will likelysupport futures prices. With the Arabicamarket in surplus, roasters have beendisciplined buyers in 2012, likely based on the assumption the oversupply will result in a further reduction in prices. Our outlook for2013 calls for end users to increase buying to build stocks, which will support a retracingin the market.

Market expectations for the 2013 BrazilianArabica crop will drive roaster buying andspeculator positioning in the coming year.While early development is positive, it will bean off-season crop, potentially shifting theArabica fundamental balance into deficit. The scale of the season-to-season productionshift has fallen in the past decade due toagronomic practices. We anticipate thedifference between on and off-season cropswill continue to shrink in the coming years,but given the scale of Brazilian productionrelative to global Arabica output, forecast at46% in 2012/13, the off-season harvest will still likely bring about a global deficit in thecoming seasons. Also impacting the supply ofArabica in 2013 will be lower incentives fromprices. Multi-year production highs of Arabicain Central America, Asia and Africa in 2012/13

Section 2 Agri Commodity Outlooks | 19

were in part a reaction to the highest nominalseason average NY price ever. In 2013, weanticipate lower NY values and lower washeddifferentials will reduce incentives to useinputs and thus moderate yield potential inthe short term. With reduced yields and an off-season Brazilian harvest, we see a highprobability of an expected Arabica deficitsupporting NY prices in 2013.

In our view, the shifting demand profile in thecoffee market will keep washed Arabica pricesand differentials under pressure and supportBrazilian Naturals and Robusta markets in2013. Coffee demand growth in 2013 is likelyto be concentrated in emerging and non-traditional markets as it has been for the pastcouple of seasons. Given the price consciousconsumers in these growing markets, roastersare expected to focus on lower priced beans,therefore maximising Robusta use. The2010/11 price rally in NY had been supportingwashed Arabica production. This coupledwith demand moving towards BrazilianNaturals is projected to result in anoversupply of washed Arabica. In the shortterm, oversupply is illustrated by the NYexchange inventories growing 52% in 2H 2012 as origins sell to the board due tomodest physical buying interest. The post-boom Arabica market leaves Brazilian supplyin demand while higher cost washed supplyexceeds demand. In 2013, the market willhave to pay Brazilian farmers higher prices to draw out supply while producers ofwashed Arabica will find the marketoversupplied. In our view, this has resulted in differentials moving closer together, asituation which is likely to remain in 2013.

The Robusta market has been balanced withstrong demand growth and large Vietnameseharvests, and in 2013 we see this dynamic

continuing. We expect the market to besupported by increased consumption,especially at origin and in Asia. In our view, the substitution of Arabica for Robusta in 2010 and 2011, which we estimate atbetween 3 million and 5 million bags globally,was a dynamic not expected to occur again. If the Robusta/Arabica price spread remainsnear current levels, we do not expectconsumption to shift back to Arabica, and wedo not expect further substitution. Robustademand is forecast to increase 3.8% in2012/13, down from 11% the previous year,and will likely grow at a similar pace in thefollowing season if prices are near ourforecasts. Robusta market fundamentals are forecast to be in a modest deficit of204,000 bags in 2012/13. The continuedgrowth in demand is expected to becountered by a large Vietnamese crop of 27 million bags in the new season.

The speculator gross long position in theRobusta market has been pared backsignificantly since its peak in July 2012 as thesupply outlook improved. If Vietnamese andIndonesian crops meet expectations, weanticipate investors will keep reducing longpositions. A sharp reversal in the fundpositioning is probable if bullish supply newsarrives, and consequently our sense for pricespike risks in Robusta are elevated. With ourbase case Robusta supply scenario for2012/13, we do not anticipate investorsincreasing the net long levels, but we expect commercial buying and the need to encourage Robusta production to besupportive factors, resulting in increasingprices in 2013. Early season harvest pressurecoupled with fund liquidation is forecast togive way to commercial buying supportingfutures prices.

Figure 2.15: Arabica differentials have shifted closer together as demand has moved from washed to naturals

USc

/lb

USc

/lb

NY Colombian NY BraziliansNY other milds NY front month (RHS)

Source ICO, Bloomberg, Rabobank, 2012

-20

0

20

40

60

80

100

50

100

150

200

250

300

Oct

-12

Jul-

12

Ap

r-12

Jan

-12

Oct

-11

Jul-

11

Ap

r-11

Jan

-11

Oct

-10

Jul-

10

Ap

r-10

Jan

-10

Oct

-09

Jul-

09

Ap

r-09

Jan

-09

Figure 2.16: Robusta is forecast to move to deficit in 2012/13 while Arabica will be in surplus

mil

lio

n b

ags

Arabica surplus/deficit

Source: Rabobank, 2012

Robusta surplus/deficit

-15

-10

-5

0

5

10

15

12/1

3f

11/1

2f

10/1

1

09/1

0

08/0

9

07/0

8

06/0

7

05/0

6

04/0

5

03/0

4

02/0

3

01/0

2

20 | Rabobank Outlook 2013—Rebalancing on a Tightrope