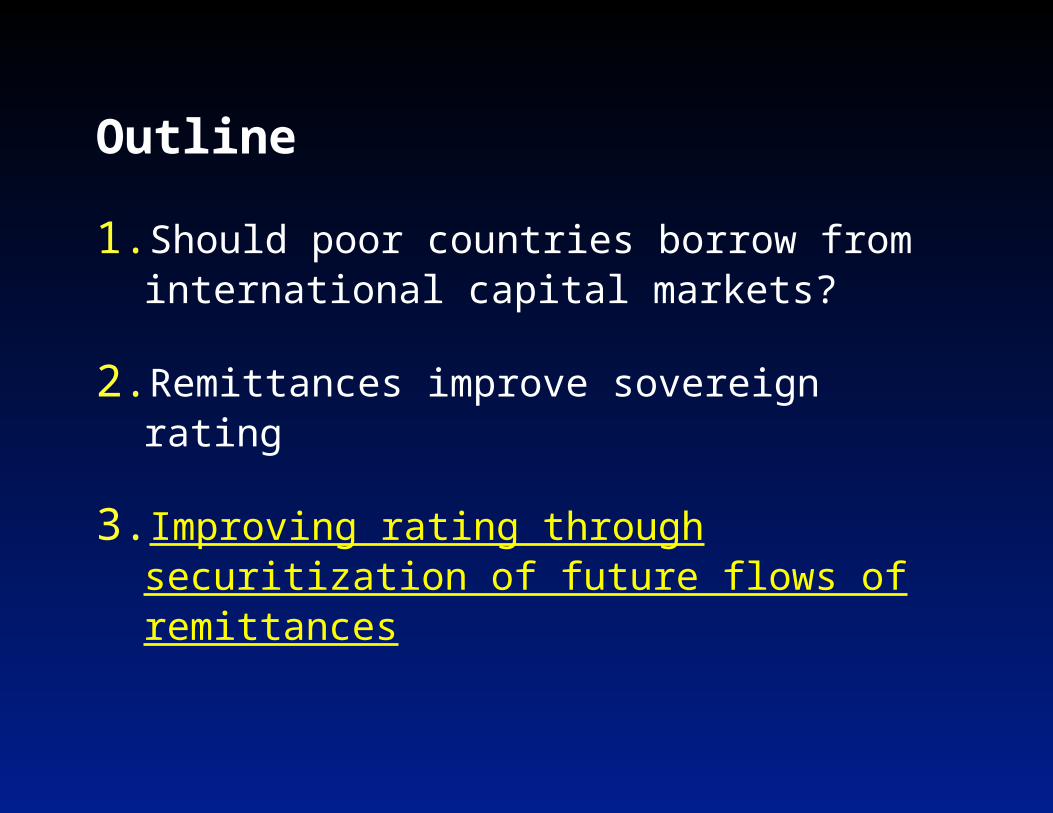

Outline

36

Leveraging Remittances for International Capital Market Access in Poor Countries Dilip Ratha (with Prabal De and Sanket Mohapatra) Migration Thematic Group World Bank October 19, 2006

-

Upload

martena-clayton -

Category

Documents

-

view

17 -

download

0

description

Leveraging Remittances for International Capital Market Access in Poor Countries Dilip Ratha (with Prabal De and Sanket Mohapatra) M igration Thematic Group World Bank October 19, 2006. Outline. Should poor countries borrow from international capital markets? - PowerPoint PPT Presentation

Transcript of Outline

Leveraging Remittances for International Capital Market Access in Poor Countries

Dilip Ratha(with Prabal De and Sanket Mohapatra)

Migration Thematic GroupWorld BankOctober 19, 2006

Outline

1. Should poor countries borrow from international capital markets?

2. Remittances improve sovereign rating

3. Improving rating through securitization of future flows of remittances

Outline

1. Should poor countries borrow from international capital markets?

2. Remittances improve sovereign rating

3. Improving rating through securitization of future flows of remittances

Should poor countries borrow from international capital markets?

Sanskrit saying by sage Charbak:"Yavat jivet sukham jivetRunam krutva ghrutam pivet"

"Live luxuriously as long as you liveBorrow if need be, but enjoy your ghee"

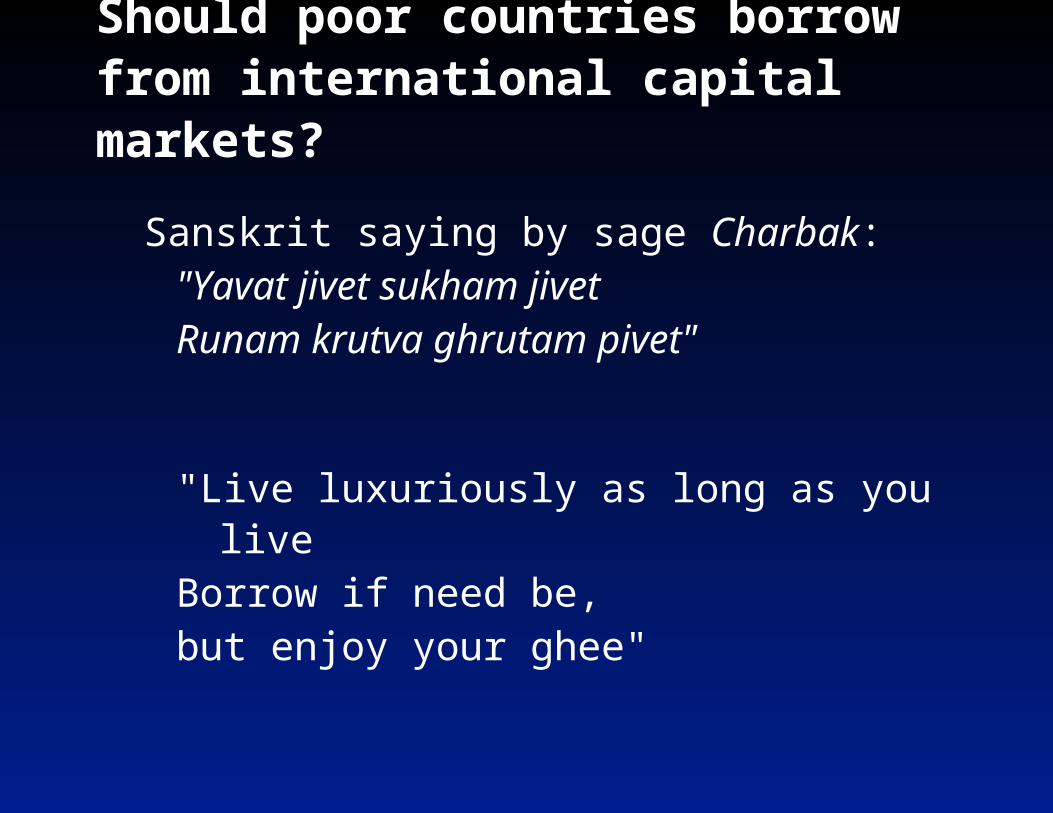

Borrowing cost rises exponentially as credit rating deteriorates

0

100

200

300

400

500

600

700

800

900

A+ A A-

BB

B+

BB

B

BB

B-

BB

+

BB

BB

-

B+ B B-

CC

C+

Investment grade

Below inv. grade

Interest spread, basis points

2005

2003

Launch spreads and S&P ratings for sovereign issues of size $100 million and 7 years tenor. Source: Bondware, S&P, and authors’ calculations

Borrowing cost rises exponentially as credit rating deteriorates

0

100

200

300

400

500

600

700

800

900

A+ A A-

BB

B+

BB

B

BB

B-

BB

+

BB

BB

-

B+ B B-

CC

C+

Investment grade

Below inv. grade

Interest spread, basis points

2005

2003

Launch spreads and S&P ratings for sovereign issues of size $100 million and 7 years tenor. Source: Bondware

Absence of sovereign rating constrains private sector access to international capital

Au

stri

aC

anad

aD

enm

ark

Fin

lan

dF

ran

ceG

erm

any

Irel

and

Lu

xem

bo

ur

Net

her

lan

ds

No

rway

Sin

gap

ore

Sp

ain

Sw

eden

Sw

itze

rlan

dU

KA

ust

ralia

Nzl

and

Jap

anIc

elan

dB

elg

ium

Ber

mu

da

Ital

yP

ort

ug

alS

love

nia

Tai

wan

Ho

ng

Ko

ng

Ku

wai

tIs

rael

Bah

rain

Moodys S&P Fitch

Sovereign ratings in high-income countries

AAA

AA

A+

A-

AA+

AA-

A

BBB+

Cze

ch R

epH

un

gar

yC

hin

aP

ola

nd

Ko

rea

Sau

di

Mal

aysi

aC

hile

So

uth

Afr

ica

Th

aila

nd

Ru

ssia

El S

alva

do

rB

ulg

aria

Kaz

akh

stan

Ro

man

iaE

gyp

tIn

dia

Co

sta

Ric

aC

olo

mb

iaP

eru

Ph

ilip

pin

esB

razi

lT

urk

eyU

krai

ne

PN

GIn

do

nes

iaV

enez

uel

aL

eban

on

Uru

gu

ayD

om

Rep

Bo

livia

Arg

enti

na

Ecu

ado

r

Moodys S&P Fitch

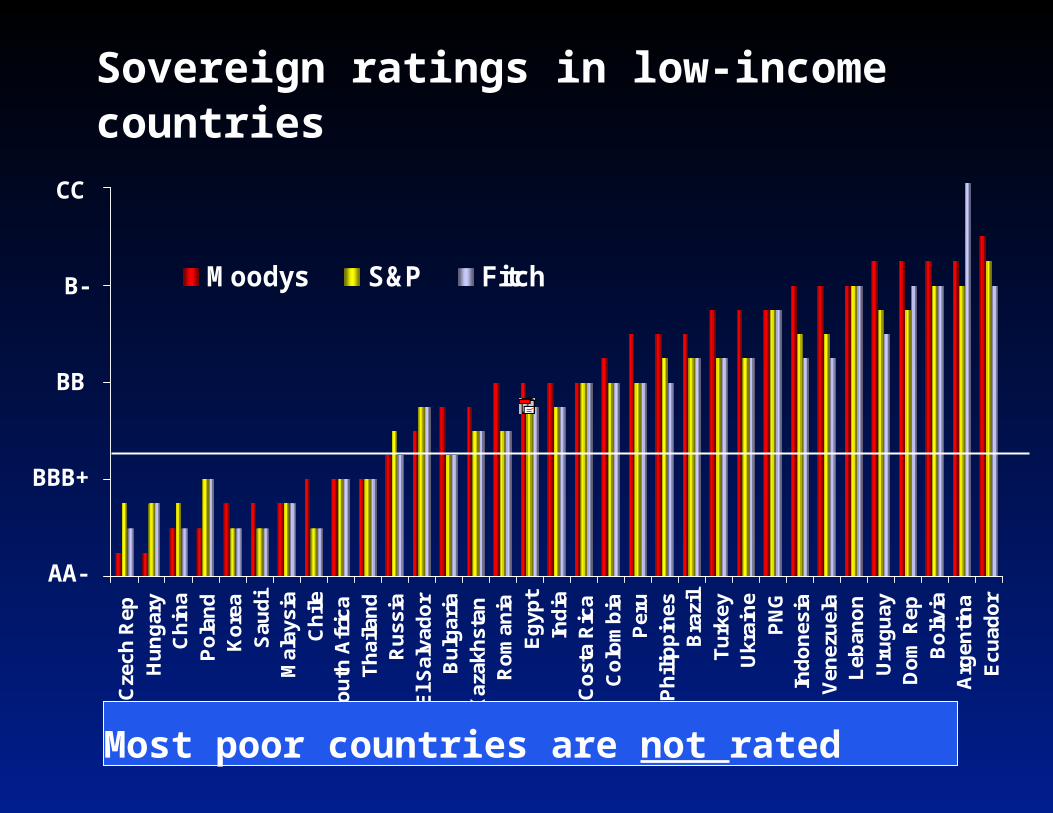

Sovereign ratings in low-income countries

AA-

BBB+

BB

B-

CC

Cze

ch R

epH

un

gar

yC

hin

aP

ola

nd

Ko

rea

Sau

di

Mal

aysi

aC

hile

So

uth

Afr

ica

Th

aila

nd

Ru

ssia

El S

alva

do

rB

ulg

aria

Kaz

akh

stan

Ro

man

iaE

gyp

tIn

dia

Co

sta

Ric

aC

olo

mb

iaP

eru

Ph

ilip

pin

esB

razi

lT

urk

eyU

krai

ne

PN

GIn

do

nes

iaV

enez

uel

aL

eban

on

Uru

gu

ayD

om

Rep

Bo

livia

Arg

enti

na

Ecu

ado

r

Moodys S&P Fitch

Sovereign ratings in low-income countries

AA-

BBB+

BB

B-

CC

Most poor countries are not rated

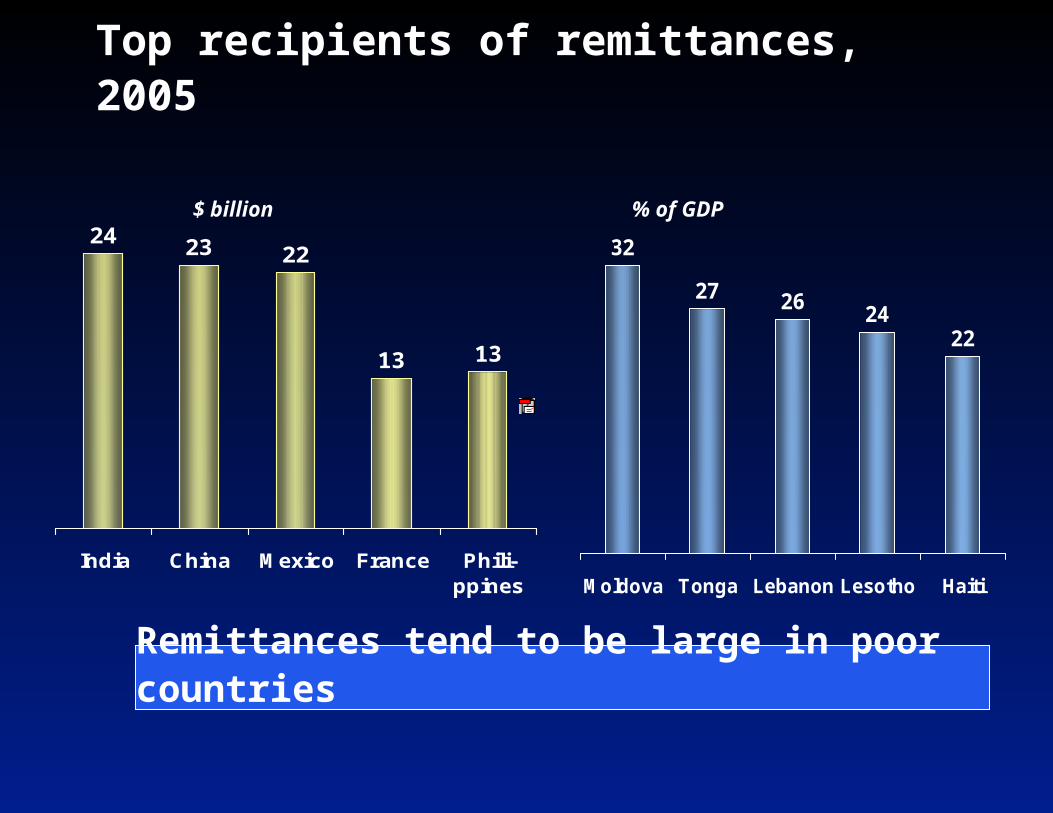

24 23 22

13 13

India China Mexico France Phili-ppines

Top recipients of remittances, 2005

32

27 2624

22

Moldova Tonga Lebanon Lesotho Haiti

$ billion % of GDP

Remittances tend to be large in poor countries

Remittances tend to rise following crisis, natural disaster, or conflict

Remittances as % of private consumption

0.5

1.2

1.7

1.4

2.0 2.0

1.0

2.0

1.8

Indonesia Mexico Thailand

year before

year of crisis

year after

Outline

1. Should poor countries borrow from international capital markets?

2. Remittances improve sovereign rating

3. Improving rating through securitization of future flows of remittances

Remittances improve a countries’ ability to service external debt

0

100

200

300

400

500

600

700

800

Excluding remittancesIncluding remittances

Present value of external debt as % of exports of goods, services, and remittances

Predicting ratings

1.Fit a regression model to explain ratings

2.Predict shadow ratings

3.Calculate effect of remittances on shadow ratings

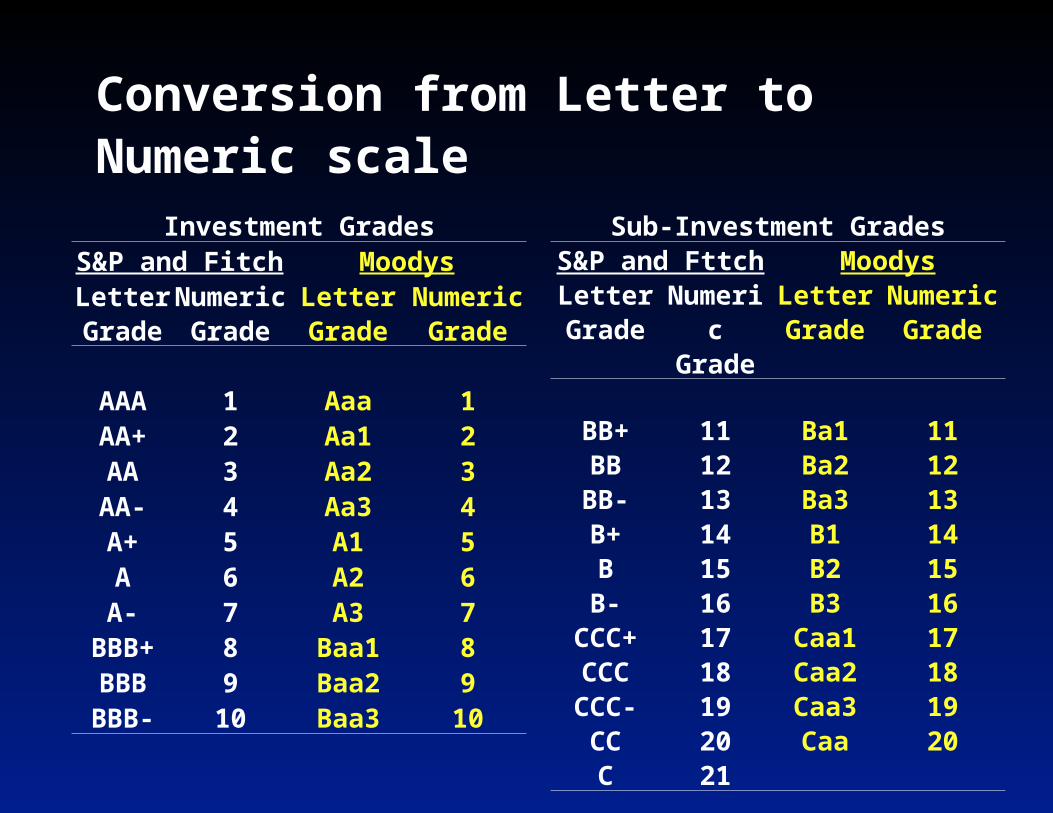

Conversion from Letter to Numeric scale

Sub-Investment GradesS&P and Fttch MoodysLetter Grade

Numeric Grade

Letter Grade

Numeric Grade

BB+ 11 Ba1 11BB 12 Ba2 12BB- 13 Ba3 13B+ 14 B1 14B 15 B2 15B- 16 B3 16

CCC+ 17 Caa1 17CCC 18 Caa2 18CCC- 19 Caa3 19CC 20 Caa 20C 21

Investment GradesS&P and Fitch MoodysLetter Grade

Numeric Grade

Letter Grade

Numeric Grade

AAA 1 Aaa 1AA+ 2 Aa1 2AA 3 Aa2 3AA- 4 Aa3 4A+ 5 A1 5A 6 A2 6A- 7 A3 7

BBB+ 8 Baa1 8BBB 9 Baa2 9BBB- 10 Baa3 10

Regression Results (work-in-progress)

Rating as a function of– macro variables– rule of law– debt and international reserves– volatility

R2 is high

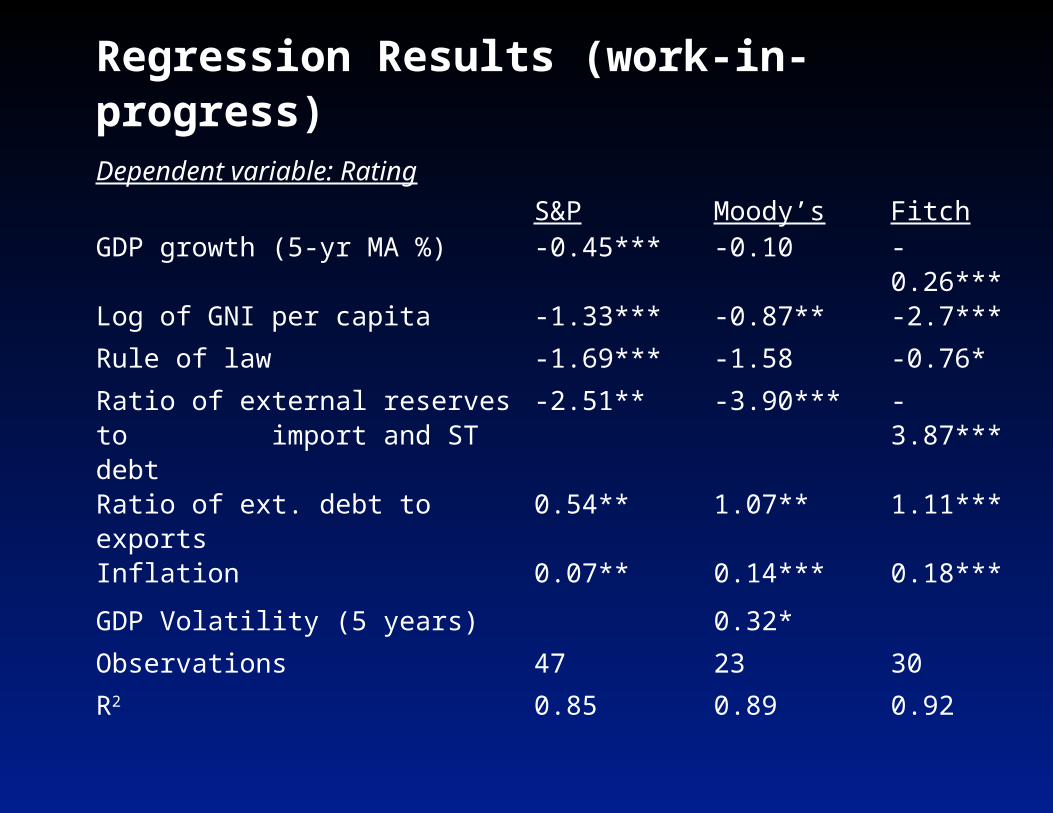

Regression Results (work-in-progress)Dependent variable: Rating

S&P Moody’s FitchGDP growth (5-yr MA %) -0.45*** -0.10 -0.26***

Log of GNI per capita -1.33*** -0.87** -2.7***

Rule of law -1.69*** -1.58 -0.76*

Ratio of external reserves to import and ST debt

-2.51** -3.90*** -3.87***

Ratio of ext. debt to exports 0.54** 1.07** 1.11***

Inflation 0.07** 0.14*** 0.18***

GDP Volatility (5 years) 0.32*

Observations 47 23 30

R2 0.85 0.89 0.92

* significant at 10%; ** significant at 5%; *** significant at 1%

Regression Results – using dated control variables (work-in-progress)

Dependent variable: Rating

S&P FitchGDP growth (3-yr MA %) -0.44*** -0.30***

Log of GNI per capita -1.38*** -0.97***

Rule of law -2.65*** -2.29**

Ratio of external reserves to imports and ST debt

-2.57*** -2.19**

Ratio of ext. debt to exports 0.76*** 1.09***

GDP Volatility (5 years) 0.24** 0.38***

Observations 43 53

R2 0.85 0.81

•significant at 10%; ** significant at 5%; *** significant at 1%

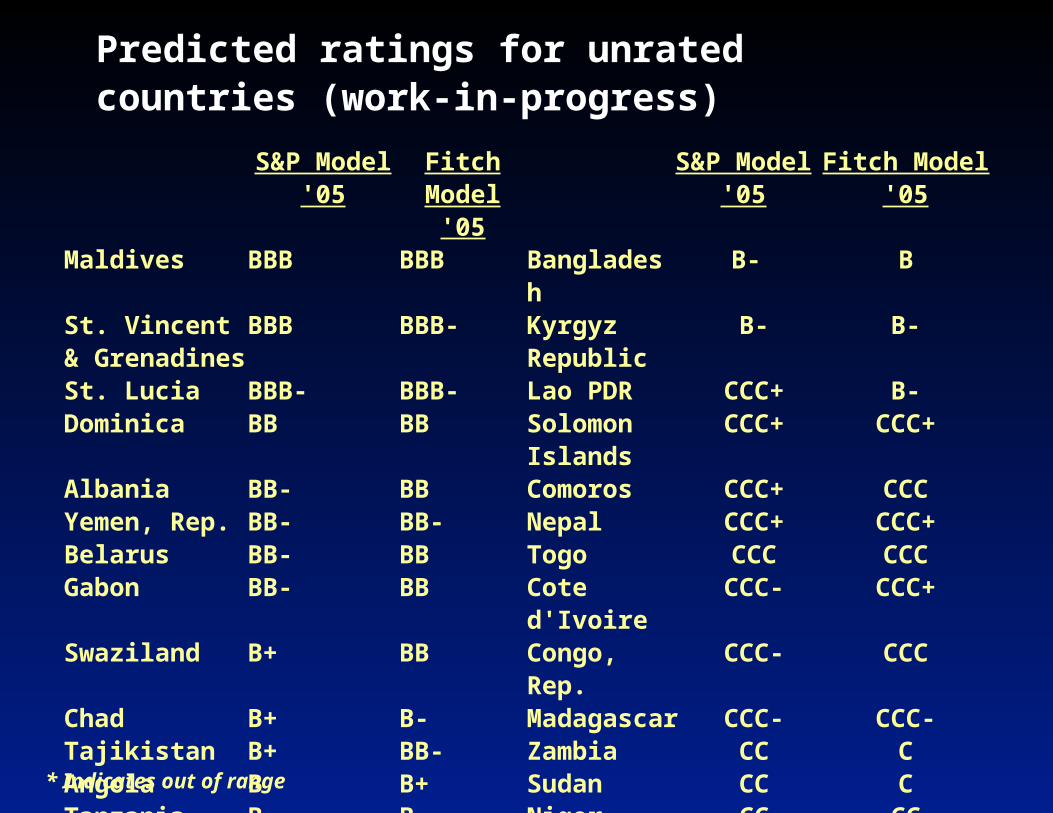

Predicted ratings for unrated countries (work-in-progress)

S&P Model '05

Fitch Model '05

S&P Model '05

Fitch Model '05

Maldives BBB BBB Bangladesh B- BSt. Vincent & Grenadines

BBB BBB- Kyrgyz Republic

B- B-

St. Lucia BBB- BBB- Lao PDR CCC+ B-Dominica BB BB Solomon

IslandsCCC+ CCC+

Albania BB- BB Comoros CCC+ CCCYemen, Rep. BB- BB- Nepal CCC+ CCC+Belarus BB- BB Togo CCC CCCGabon BB- BB Cote d'Ivoire CCC- CCC+Swaziland B+ BB Congo, Rep. CCC- CCCChad B+ B- Madagascar CCC- CCC-Tajikistan B+ BB- Zambia CC CAngola B B+ Sudan CC CTanzania B B Niger CC CCCambodia B B+ Sierra Leone CC O*Guyana B- B Ethiopia C C

* Indicates out of range

Shadow-rated vs. rated countries (work-in-

progress) (Shadow ratings underlined and italicized)

Country S&P rating Moody's ratingFitch rating

Country S&P rating

Moody's rating

Fitch rating

Botswana A Aa3 India BB+ Baa2 BBB-Barbados BBB+ Baa2 Macedonia BB+ BB+Oman A- A2 Morocco BB+ Ba1Poland BBB+ A2 BBB+ Cape Verde BB+ B+South Africa

BBB+ Baa1 BBB+ Sri Lanka BB-

Thailand BBB+ Baa1 BBB+ Brazil BB Ba2 BBArmenia Baa3 Bb- Colombia BB Ba2 BBBulgaria BBB Baa3 BBB Costa Rica BB Ba1 BBCroatia BBB Baa3 BBB- Jordan BB Baa3Mexico BBB Baa1 BBB Panama BB Ba1 BB+

Maldives BBB Peru BB Ba3 BB+

Russia BBB+ Baa2 BBB+ Gabon BB-Tunisia BBB A3 BBB Guatemala BB Ba2 BB+Mauritius Baa1 Philippines BB- B1 BBKazakhstan

BBB- Baa2 BBB Serb.& Mont. BB- BB-

Romania BBB- Ba1 BBB Turkey BB- Ba3 BB-Seychelles B Ukraine BB- B1 BB-

Albania BB- Venezuela BB- B2 BB-

Egypt BB+ Ba1 BB+ Georgia B+El SalvadorBB+ Baa3 BB+ Cambodia BThese model-based ratings should be treated as indicative; they are clearly not a substitute for the broader and deeper

analysis, and qualitative judgment, employed by experienced rating analysts.

Shadow-rated vs. rated countries (work-in-progress) (Shadow ratings underlined and italicized)

Country S&P ratingMoody's rating

Fitch rating

Country S&P rating

Moody's rating

Fitch rating

Senegal B+ Mongolia B B1 B+

Belarus BB- Mozambique B B

Swaziland B+ PNG B Ba2 B

Moldova Caa1 B- Bangladesh B-Congo, Rep.CCC- Argentina B+ B3 B

Tanzania B Bolivia B- B3 B-

Benin B B Cameroon B- BGhana B+ B+ Lebanon B- B3 B-Indonesia BB- B1 BB- Paraguay B- B3Pakistan B+ B2 Suriname B- Ba2 B

Guyana B- Nigeria BB- BB-

Yemen BB- Nicaragua B- B3

Kyrgyz Rep B- Uganda CCC+ B

Honduras Ba3 Kenya B+Burkina Faso B Ecuador CCC+ Caa1 B-Dom. Rep B B3 B Togo CCCJamaica B B1 Cote d'Ivoire CCC-Madagascar B Niger CCMali B B- Ethiopia C

These model-based ratings should be treated as indicative; they are clearly not a substitute for the broader and deeper

analysis, and qualitative judgment, employed by experienced rating analysts.

Shadow-rated vs. rated countries (work-in-

progress) (Shadow ratings underlined and italicized)

Country S&P ratingMoody's rating

Fitch rating

Country S&P rating

Moody's rating

Fitch rating

Senegal B+ Mongolia B B1 B+

Belarus BB- Mozambique B B

Swaziland B+ PNG B Ba2 B

Moldova Caa1 B- Bangladesh B-Congo, Rep.CCC- Argentina B+ B3 B

Tanzania B Bolivia B- B3 B-

Benin B B Cameroon B- BGhana B+ B+ Lebanon B- B3 B-Indonesia BB- B1 BB- Paraguay B- B3Pakistan B+ B2 Suriname B- Ba2 B

Guyana B- Nigeria BB- BB-

Yemen BB- Nicaragua B- B3

Kyrgyz Rep B- Uganda CCC+ B

Honduras Ba3 Kenya B+Burkina Faso B Ecuador CCC+ Caa1 B-Dom. Rep B B3 B Togo CCCJamaica B B1 Cote d'Ivoire CCC-Madagascar B Niger CCMali B B- Ethiopia C

These model-based ratings should be treated as indicative; they are clearly not a substitute for the broader and deeper

analysis, and qualitative judgment, employed by experienced rating analysts.

Many unrated countries likely have better market access than currently believed

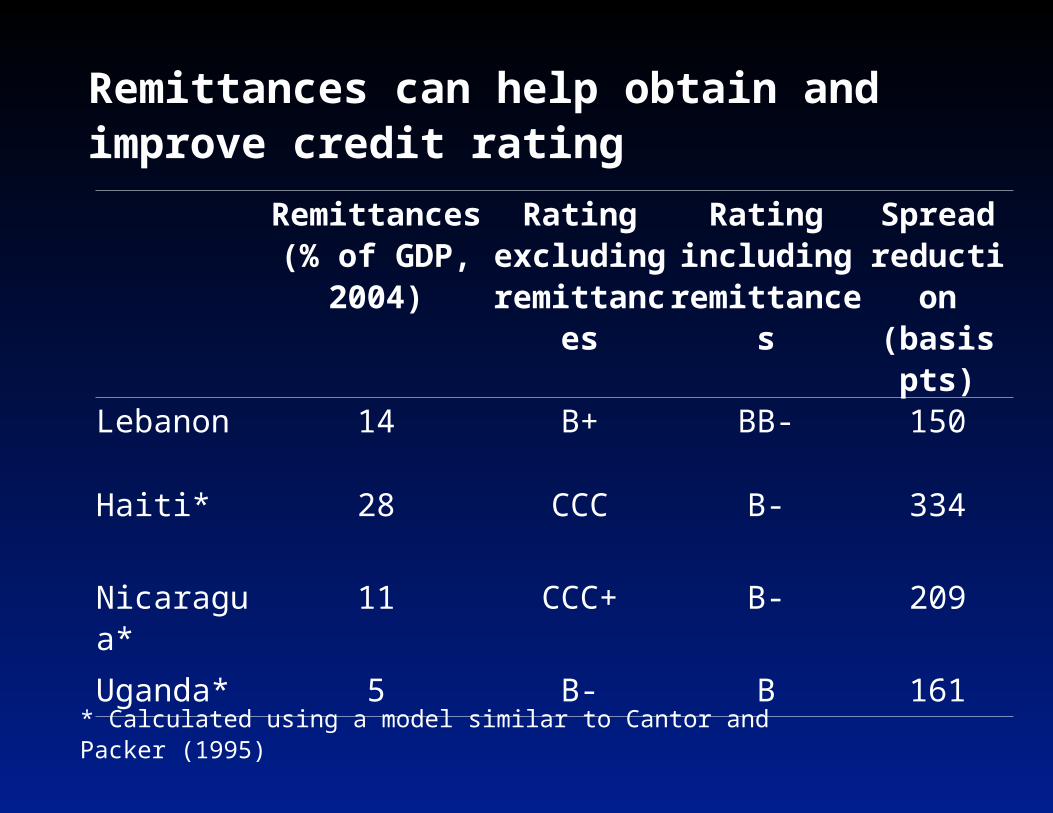

Remittances can help obtain and improve credit rating

Remittances (% of GDP,

2004)

Rating excluding

remittances

Rating including

remittances

Spread reduction

(basis pts)

Lebanon 14 B+ BB- 150

Haiti* 28 CCC B- 334

Nicaragua* 11 CCC+ B- 209

Uganda* 5 B- B 161

* Calculated using a model similar to Cantor and Packer (1995)

Including remittances may improve potential ratings for Bangladesh by two notches

Rating model

Shadow rating w/o remittances

Shadow rating with remittances

Moodys B3 (16) B1 (14)

S&P B- (16) B+ (14)

Fitch B (15) BB- (13)

Countries in similar rating category as Bangladesh

Argentina, Dominican Republic, Indonesia, Pakistan, Paraguay, Uruguay, Venezuela

Benin, Bolivia, Burkina Faso, Ghana, Jamaica, Mali, Surinam

Outline

1. Should poor countries borrow from international capital markets?

2. Remittances improve sovereign rating

3. Improving rating through securitization of future flows of remittances

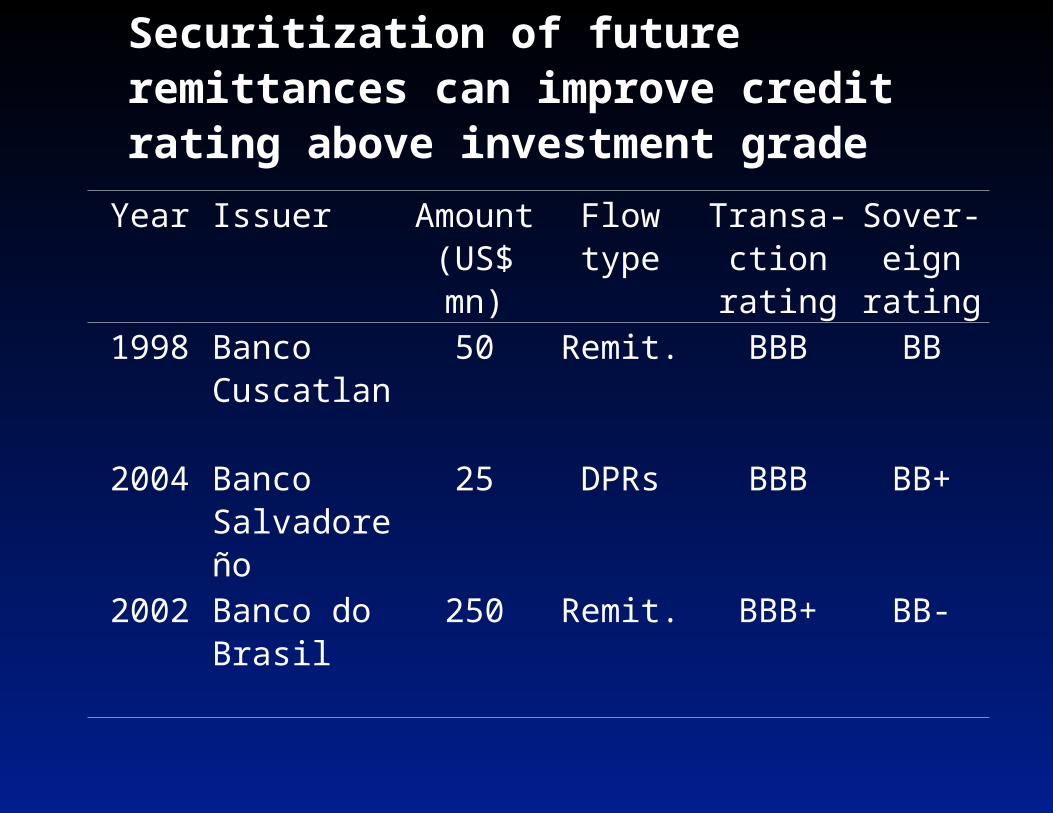

Securitization of future remittances can improve credit rating above investment grade

Year Issuer Amount(US$ mn)

Flow type Transa-ction rating

Sover-eign

rating1998 Banco

Cuscatlan50 Remit. BBB BB

2004 Banco Salvadoreño

25 DPRs BBB BB+

2002 Banco do Brasil

250 Remit. BBB+ BB-

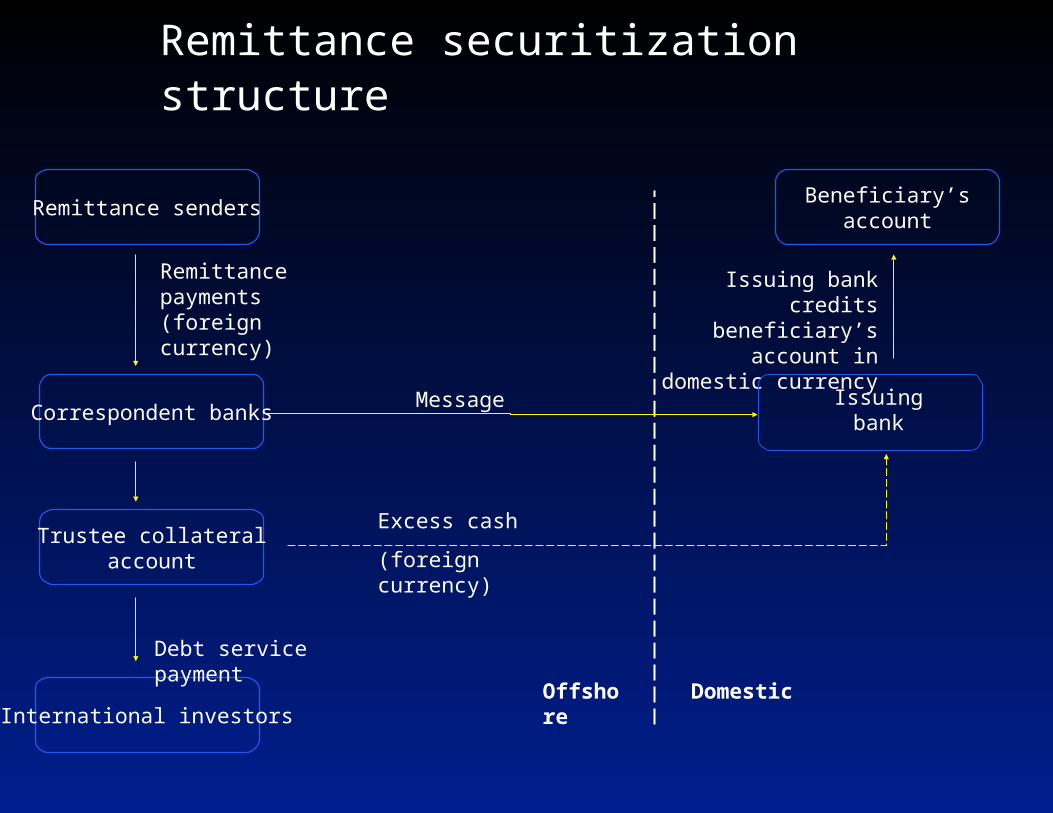

Remittance payments (foreign currency)

Remittance senders

Remittance securitization structure

Correspondent banks

Issuing bank credits beneficiary’s account in

domestic currency

Beneficiary’saccount

DomesticOffshore

Issuing bank

International investors

Remittance payments (foreign currency)

Remittance senders

Excess cash

(foreign currency)

Debt service payment

Remittance securitization structure

Trustee collateralaccount

Correspondent banks

Issuing bank credits beneficiary’s account in

domestic currency

Beneficiary’saccount

Message

DomesticOffshore

Issuing bank

Securitization of remittances has increased in recent years -

65206

350115

540

1,175 1,170

1,600 1,690

2,837

1,055

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004to

July

$ million

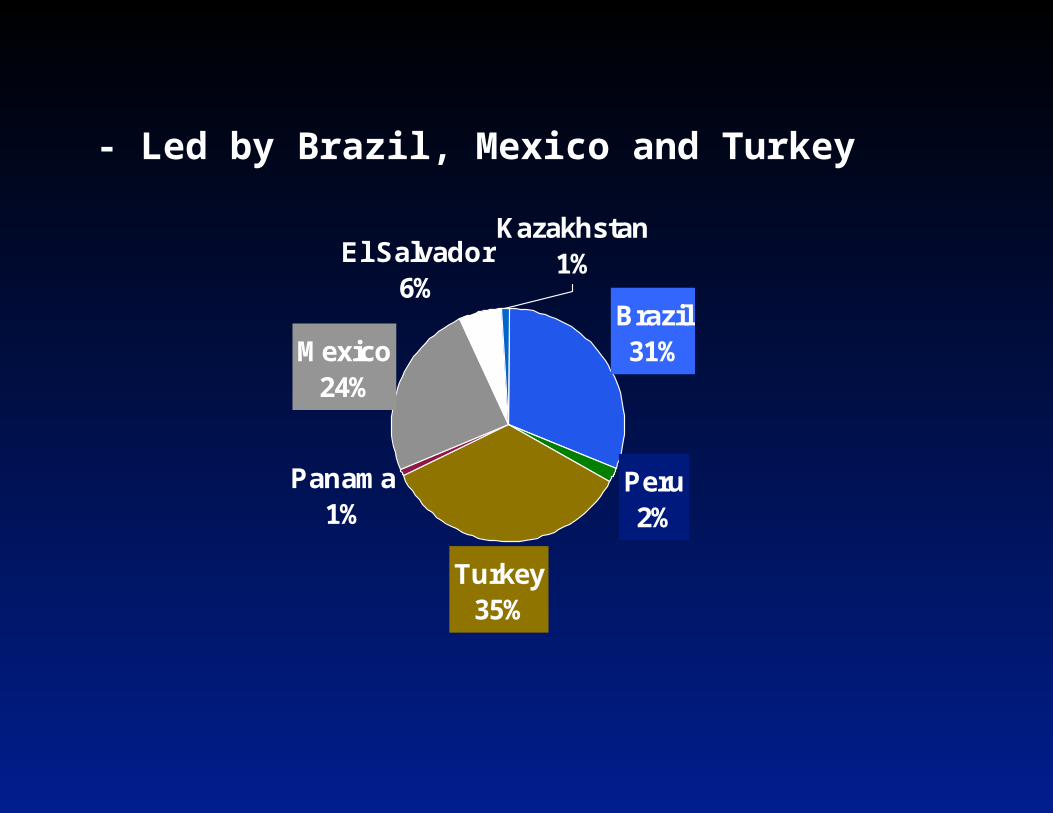

- Led by Brazil, Mexico and Turkey

Panama1%

El Salvador6%

Kazakhstan1%

Mexico24%

Turkey35%

Peru2%

Brazil31%

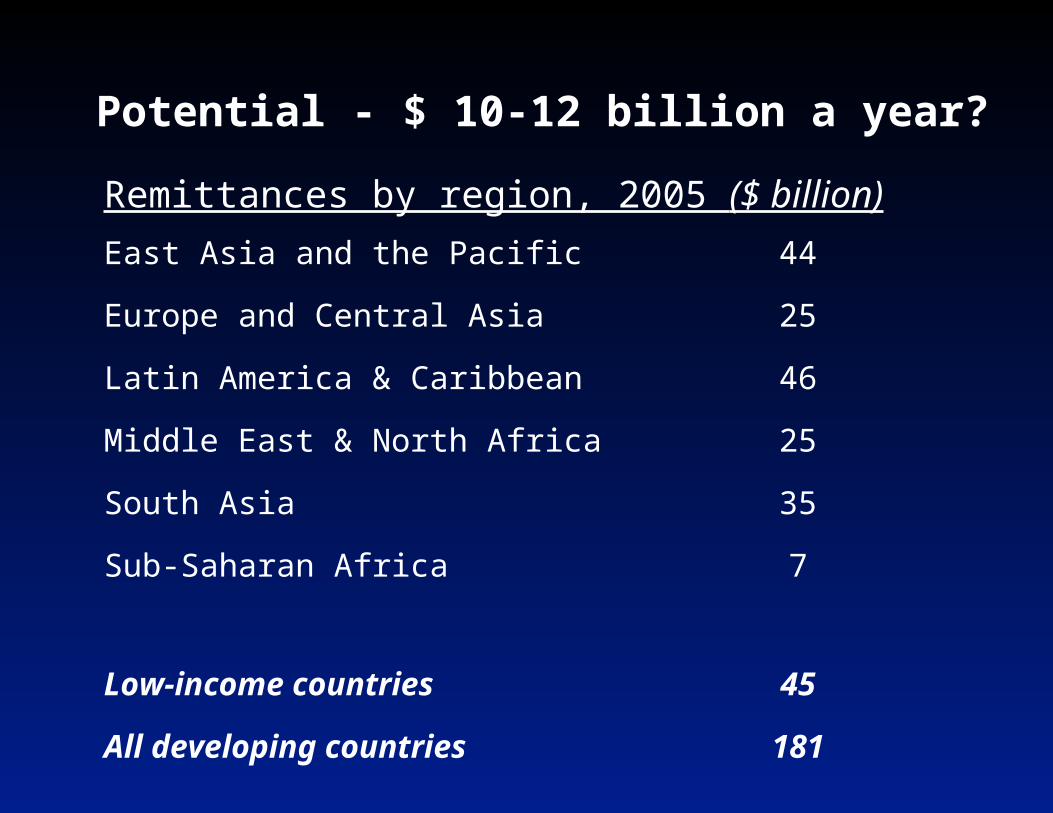

Potential - $ 10-12 billion a year?

Remittances by region, 2005 ($ billion)

East Asia and the Pacific 44

Europe and Central Asia 25

Latin America & Caribbean 46

Middle East & North Africa 25

South Asia 35

Sub-Saharan Africa 7

Low-income countries 45

All developing countries 181

Constraints

Paucity of highly rated entities

Long lead times

High fixed costs (legal and others)

Non-transparent legal structure

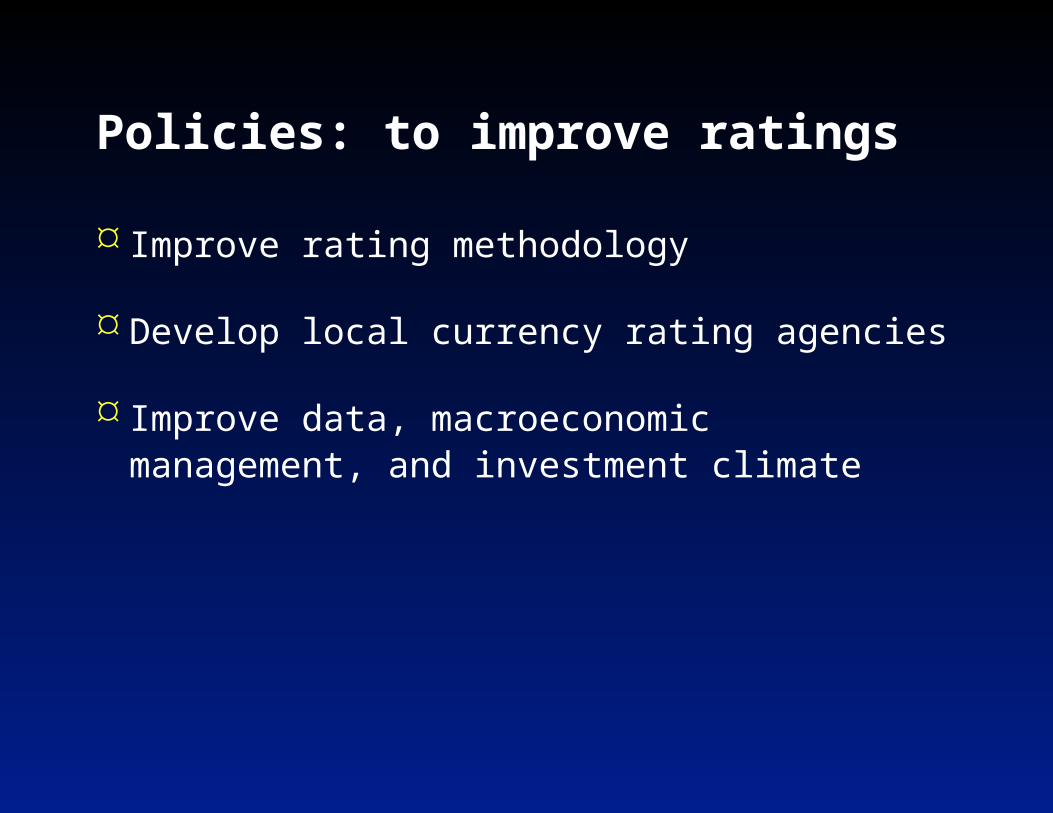

Policies: to improve ratings

Improve rating methodology

Develop local currency rating agencies

Improve data, macroeconomic management, and investment climate

Policies: to facilitate securitization

Master Trust arrangements, and receivable pooling, may alleviate the constraint of high fixed costs

Beware of negative pledge in the case of public sector borrowers

IFIs can help– Provide seed money– Improve legal framework– Assume counter-party risk as in Unibanco– Educate policy makers– Improve remittance data

Summary

Poor countries need to access to international capital markets

Absence of sovereign rating constrains their (especially sub-sovereign and private entities) access to international capital markets

Remittances, properly accounted, can contribute to establish/improve sovereign rating

Future remittance flows can further improve the rating of external financing transactions

Master Trust arrangements, and receivable pooling, may alleviate the constraint of high fixed costs

![[ Outline ]](https://static.fdocuments.in/doc/165x107/56815a74550346895dc7db61/-outline--56b49f971d862.jpg)