Our only alpha choice? FX Markets Summer 2015. Regulatory driving change in market expectations Dodd...

32

Our only alpha choice? FX Markets Summer 2015

-

Upload

winfred-owen -

Category

Documents

-

view

214 -

download

0

Transcript of Our only alpha choice? FX Markets Summer 2015. Regulatory driving change in market expectations Dodd...

Our only alpha choice?

FX Markets Summer 2015

• Regulatory driving change in market expectations

• Dodd Frank, EMIR, Volker, Basel III

• Collateral demand vs net Exposure

• Collateralization of OTCs effects on global rates

• Fed funds rate- “they will probably raise rates in the second half…”

• Lack of ‘reasonability’ in markets

• China, Greece, South America, Singapore….

Level Setting

• Can we make decent risk adjusted returns in this environment?

• Examples: “picking up pennies on the rail road tracks” – US Treasury market– Global stock prices– Lack of (adherence to) alternative investments– China– CDS index, IRS Swap

FX Opportunities

Regulation

Sovereign debt, & bail in

provision

High valuations in equity prices

Funding need

(collateral)

• The forces in the market has left us with little investment choices

• FX markets – only trade with correct risk reward ratio…

• Collateral demands (into 2030) will stymie global markets

• Questions for audience: Are market structure & regulatory changes for the best?

Perfect storm for spot FX as an investment vehicle

1. Extreme, historic, levels

2. Trend is cleaner than other asset classes

3. Gov’t supported markets are untradeable

4. FX reacts to global macro economic data

5. More predictable, achievable trades / returns

6. Leverage in FX markets constant

7. Market players catching on: Exchanges1. Deutsche Boerse AG $793 million purchase of

currency market 360T2. Bats Global Markets Inc., $365 million on

Hotspot FX.

The case for FX

• Foreign-exchange trading declines amid speculation the Federal Reserve will raise interest rates only gradually.

• Daily trading in the U.K., the largest currency market, fell 8 percent to average $2.5 trillion, down from October’s record of $2.7 trillion

• In the U.S., volumes dropped about 20 percent from last October to $881 billion

• pace of policy tightening will be dependent on an improvement in the economy

FX market eyeing rate hike

Turnover in average daily trading in Japan’s capital declined 2.8 percent to $362.7 billion in April compared with October 2014, according to the Tokyo Foreign Exchange Market Committee. In Singapore, volumes dropped 21 percent. The Australian Foreign Exchange Committee said its nation’s volume dipped 4 percent to $135.9 billion.

• Trading in the Chinese yuan versus the dollar bucked the general trend. Trading in this exchange rate in London rose by 25 percent to a record $43 billion a day in April, according to the BOE committee, making it the ninth-biggest currency pair.

• Turnover in London in the yen versus the dollar fell 25 percent, the BOE said. Trading in the pair also declined 1.4 percent in Tokyo, even as such trades accounted for more than half of all transactions.

Japan Turnover

Euro-yen trading in Tokyo climbed 24 percent. Transactions for the Australian dollar versus the greenback accounted for 44 percent of total average daily volumes in the South Pacific nation.

• The British pound strengthened 3.6 percent against the dollar in April and is the best-performing major currency in the past six months, according to Bloomberg Correlation-Weighted Currency Indexes. Sterling has benefited as the BOE is widely seen as the next major central bank to tighten policy after the Fed. The Aussie appreciated 3.9 percent in April, while the yen strengthened 0.6 percent.

• Foreign-exchange trading in the U.S. and U.K. climbed to records in October, reports in January from the nations’ central banks showed, as American monetary policy diverged from that in Europe and Japan. The data showed average daily currency turnover in North America jumped 36 percent to $1.1 trillion, compared with April 2014, while U.K. volumes expanded 13 percent to a record.

• Electronic trading in Japan dropped 19 percent to $161.9 billion a day, or just 45 percent of transactions, after accounting for more than half in October.

Euro-Yen

Currencies of a number of major emerging economies decline sharply against the dollar

The Thai baht, the Korean won, the Malaysian ringgit vs. the dollar

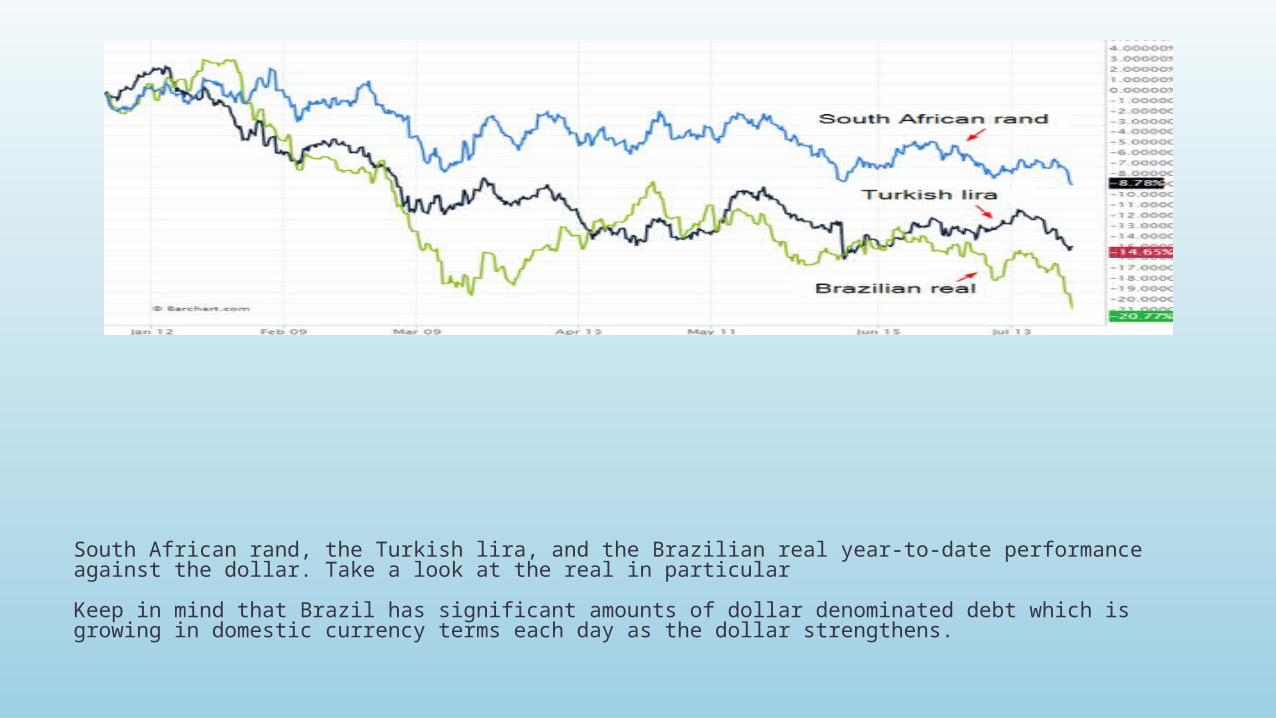

South African rand, the Turkish lira, and the Brazilian real year-to-date performance against the dollar. Take a look at the real in particular

Keep in mind that Brazil has significant amounts of dollar denominated debt which is growing in domestic currency terms each day as the dollar strengthens.

JPMorgan Emerging Markets Currency Index hit a 13-year low

China’s busting IPO market is issue # 1…Will institutional investors ever come back?

China's markets are now completely dependent on government stimulus of all types. There is no question the government will be able to push this market higher

The trade-weighted US dollar index is now the strongest in over a decade

G-10 weakness…

• renewed dollar will make it increasingly difficult for US exporters to compete internationally

• particularly in selling into emerging economies

• US manufacturers will have to focus on domestic markets.

• commodity deflation is becoming quite broad in the US - from coffee to copper.

• Will a potential boost from lower commodity/energy prices offset the weakness in the manufacturing sector?

$USD Strength

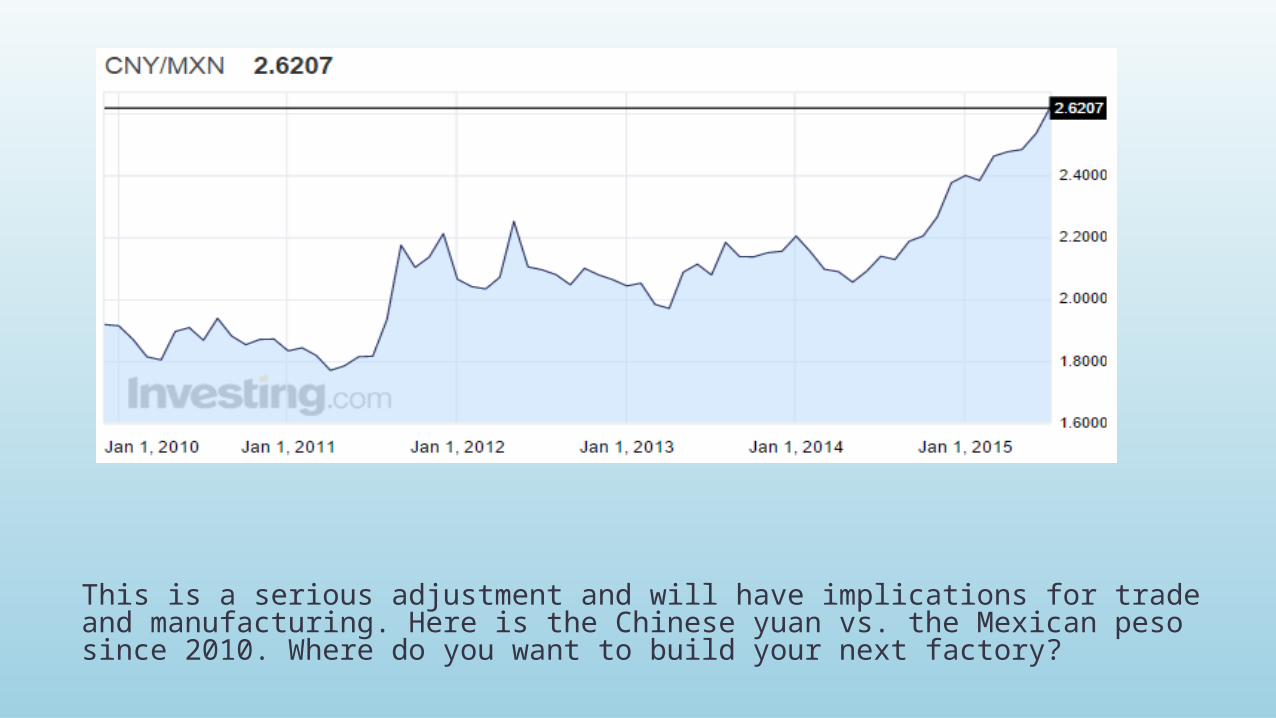

This is a serious adjustment and will have implications for trade and manufacturing. Here is the Chinese yuan vs. the Mexican peso since 2010. Where do you want to build your next factory?

The Turkish lira is down 24% vs the dollar, with the uncertainties around security spooking investors

Indonesian rupiah and the Malaysian ringgit are back to the late 90s currency crisis lows (charts show USD at the highs relative to these currencies)

The Russian ruble gave up another 2%, approaching 60 to the dollar, as it trades in lockstep with crude oil.

BrentWTI

Brent futures are now trading below $53/bbl and the NYMEX crude (WTI) is now below $47/bbl. We are going to see all sorts of knock-on effects of this correction.

US diesel prices are now the lowest since late 2009

Canadian stock market is now under pressure

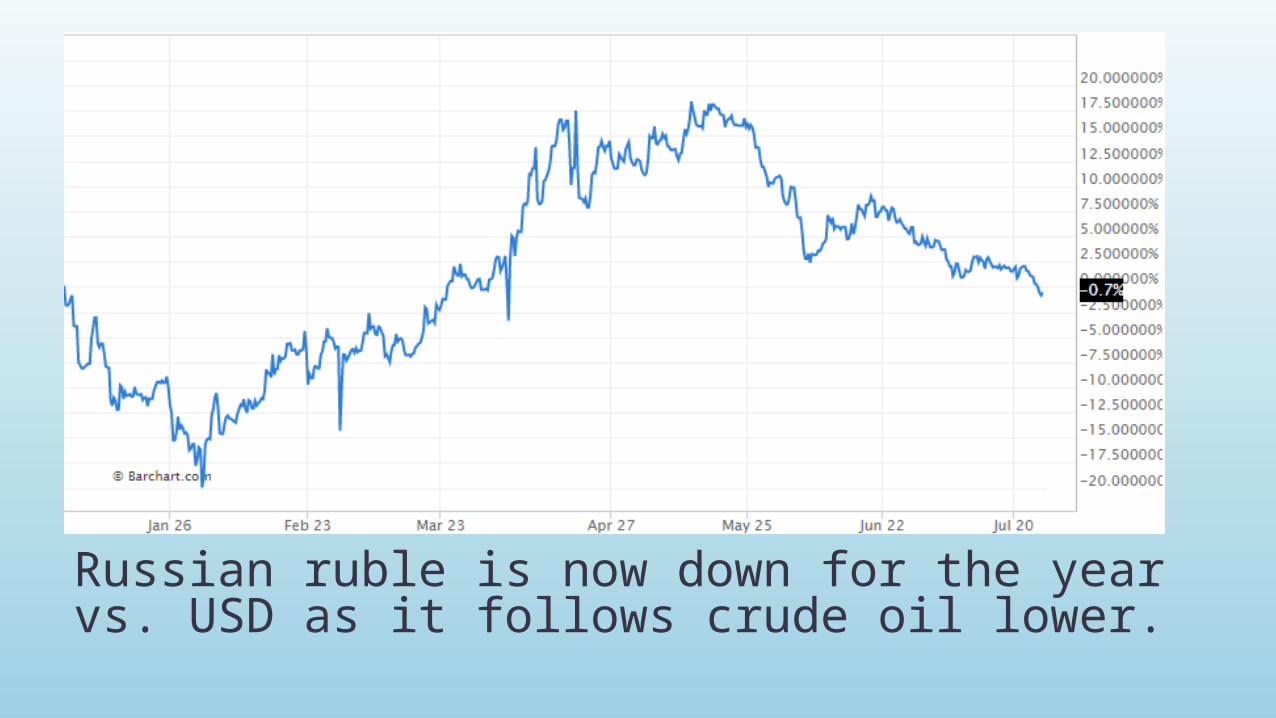

Russian ruble is now down for the year vs. USD as it follows crude oil lower.

The Venezuelan bolívar is collapsing in the "unofficial" market; it now takes almost 700 bolívares to buy 1 US dollar. This is not going to end well.

Global demand for commodities has fallen, take a look at income growth in emerging markets.

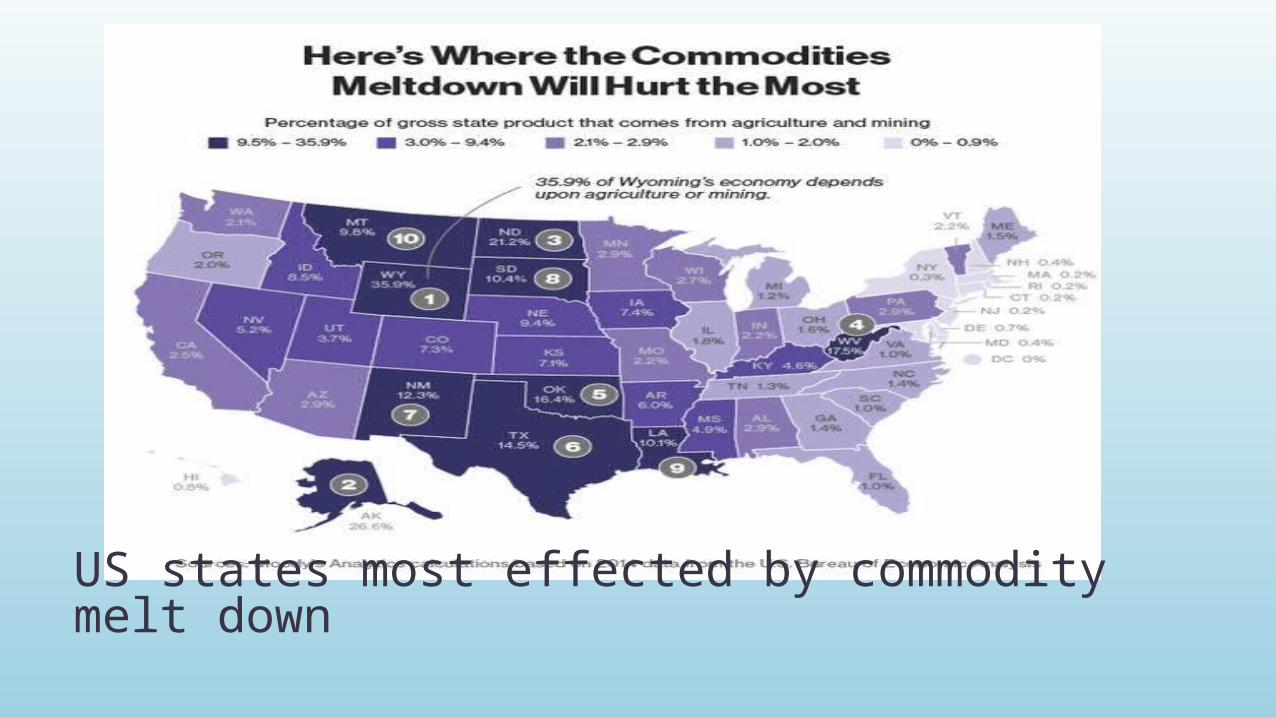

US states most effected by commodity melt down

All this pummeling that commodities markets are taking is not going unnoticed in the inflation markets, as inflation expectations (from TIPS breakevens) are turning lower again.

The FOMC should be asking themselves: is this really the right environment to begin raising rates?

• OTC partners

• Research

• Whitepapers (custom)

• TL articles (white-labeled)

• Benchmarking

• Events

• Advisory

Contact Information