ORPORATIONS - cans.ubclss.comcans.ubclss.com/application/media/cans/Davis_Law_230... · Cox &...

198

1 CORPORATIONS Course Summary Course Code 230B Section 002 Instructor Ron Davis Term 2011W Fall Author Vic Schappert School University of British Columbia Faculty of Law Textbook Yalden et al, Business Organizations: Principles, Policies and Practice (Toronto: Emond Montgomery, 2008) CONTENTS CONTENTS ..................................................................................................................................................................... 1 1. Business Organization .......................................................................................................................................... 5 Framework of Analysis .................................................................................................................................... 5 Glossary of Terms ........................................................................................................................................... 5 Sole Proprietorships........................................................................................................................................ 6 Partnerships.................................................................................................................................................... 6 General Partnerships ............................................................................................................................... 6 Limited Partnerships.............................................................................................................................. 12 Limited Liability Partnerships ................................................................................................................. 14 A Relationship of Trust and Confidence ................................................................................................. 14 Partnerships Example Problem .............................................................................................................. 14 2. Introduction to Corporations ............................................................................................................................. 15 Three Theories of Corporations ..................................................................................................................... 16 Nexus of Contracts ................................................................................................................................ 16 Mediating Hierarchy .............................................................................................................................. 16 Public Institution ................................................................................................................................... 16 Incorporation and Its Consequences ............................................................................................................. 17 The Corporation as a “Separate Legal Person” ....................................................................................... 17 Limited Liability ..................................................................................................................................... 17 The Process of Incorporation ........................................................................................................................ 19 Articles of Incorporation ........................................................................................................................ 19 When Does a Corporation Begin to Exist? .............................................................................................. 19 Piercing the “Veil” ......................................................................................................................................... 20 Rough Taxonomy of Reasons ................................................................................................................. 20 When the Veil Won’t Be Pierced ............................................................................................................ 21 Insurable Interests Cases ....................................................................................................................... 21 Fraud and Reasons of Justice ................................................................................................................. 22 Tax Liability ........................................................................................................................................... 22 Enterprise Liability................................................................................................................................. 22 Tort Liability .......................................................................................................................................... 23 Final Notes on Veil Piercing ................................................................................................................... 23 Pre-Incorporation Contracts .......................................................................................................................... 24 Common Law of Pre-Incorporation Contracts ........................................................................................ 24 CBCA Statutory Regime ......................................................................................................................... 25

Transcript of ORPORATIONS - cans.ubclss.comcans.ubclss.com/application/media/cans/Davis_Law_230... · Cox &...

1

CORPORATIONS Course Summary

Course Code 230B Section 002 Instructor Ron Davis Term 2011W Fall Author Vic Schappert School University of British Columbia Faculty of Law Textbook Yalden et al, Business Organizations: Principles, Policies and Practice (Toronto: Emond Montgomery, 2008)

CONTENTS CONTENTS ..................................................................................................................................................................... 1

1. Business Organization .......................................................................................................................................... 5

Framework of Analysis .................................................................................................................................... 5

Glossary of Terms ........................................................................................................................................... 5

Sole Proprietorships ........................................................................................................................................ 6

Partnerships.................................................................................................................................................... 6

General Partnerships ............................................................................................................................... 6

Limited Partnerships.............................................................................................................................. 12

Limited Liability Partnerships ................................................................................................................. 14

A Relationship of Trust and Confidence ................................................................................................. 14

Partnerships Example Problem .............................................................................................................. 14

2. Introduction to Corporations ............................................................................................................................. 15

Three Theories of Corporations ..................................................................................................................... 16

Nexus of Contracts ................................................................................................................................ 16

Mediating Hierarchy .............................................................................................................................. 16

Public Institution ................................................................................................................................... 16

Incorporation and Its Consequences ............................................................................................................. 17

The Corporation as a “Separate Legal Person” ....................................................................................... 17

Limited Liability ..................................................................................................................................... 17

The Process of Incorporation ........................................................................................................................ 19

Articles of Incorporation ........................................................................................................................ 19

When Does a Corporation Begin to Exist? .............................................................................................. 19

Piercing the “Veil” ......................................................................................................................................... 20

Rough Taxonomy of Reasons ................................................................................................................. 20

When the Veil Won’t Be Pierced ............................................................................................................ 21

Insurable Interests Cases ....................................................................................................................... 21

Fraud and Reasons of Justice ................................................................................................................. 22

Tax Liability ........................................................................................................................................... 22

Enterprise Liability ................................................................................................................................. 22

Tort Liability .......................................................................................................................................... 23

Final Notes on Veil Piercing ................................................................................................................... 23

Pre-Incorporation Contracts .......................................................................................................................... 24

Common Law of Pre-Incorporation Contracts ........................................................................................ 24

CBCA Statutory Regime ......................................................................................................................... 25

2

BCBCA Statutory Regime ....................................................................................................................... 26

Summary of Statutory Regimes ............................................................................................................. 27

Agency .......................................................................................................................................................... 27

Actual Authority .................................................................................................................................... 28

Defective Appointments ........................................................................................................................ 28

Indoor Management Rule (a.k.a. Ostensible Authority) ......................................................................... 28

Management Hierarchy: CBCA ............................................................................................................... 29

Ultra Vires: Boundaries on the Corporation’s Capacity to Act ........................................................................ 29

Ultra Vires Doesn’t Really Exist Anymore ............................................................................................... 29

Modern Restrictions on Management Authority .................................................................................... 29

Constitutional Considerations ....................................................................................................................... 30

Federal vs Provincial Incorporation ........................................................................................................ 30

Charter Rights........................................................................................................................................ 31

3. Equity Investments ............................................................................................................................................ 33

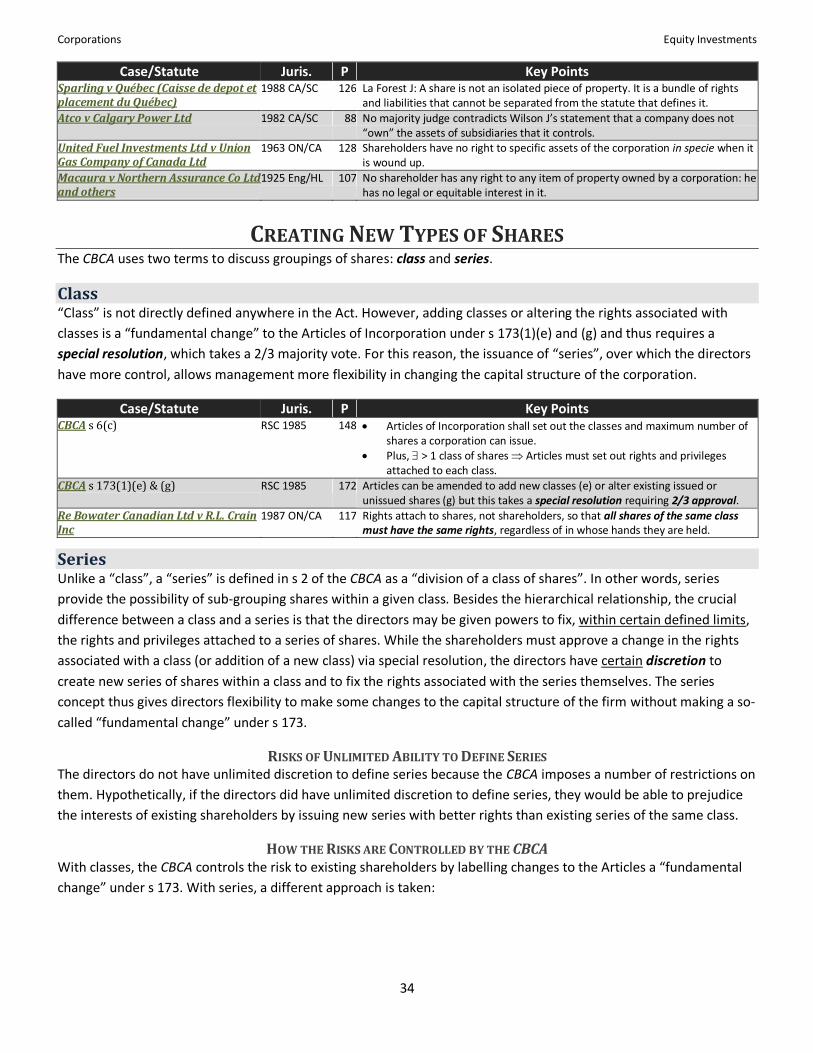

Bundles of Rights & Obligations, Not Ownership ........................................................................................... 33

Creating New Types of Shares ....................................................................................................................... 34

Class ...................................................................................................................................................... 34

Series .................................................................................................................................................... 34

Issuing Shares ............................................................................................................................................... 35

Par Value Shares are Prohibited............................................................................................................. 35

Consideration for Shares ....................................................................................................................... 35

Authorized Share Capital ....................................................................................................................... 37

Rights Attached to Shares ............................................................................................................................. 37

Minimum Rights .................................................................................................................................... 37

Distribution of Assets on Dissolution of the Corporation ........................................................................ 38

Dividends .............................................................................................................................................. 38

Rights Attach to Shares, Not Shareholders ............................................................................................. 39

Debt Stands Before Equity ..................................................................................................................... 39

Pre-Emptive Rights ................................................................................................................................ 39

Preferred Stock and Common Stock .............................................................................................................. 40

Common Stock ...................................................................................................................................... 40

Preferred Stock ..................................................................................................................................... 40

Risks to Shareholder ..................................................................................................................................... 40

4. Directors’ Powers and Duties ............................................................................................................................. 42

Powers .......................................................................................................................................................... 42

To Appoint Corporate Officers and Delegate Certain Functions ............................................................. 42

To Organize and Conduct Shareholder Meetings ................................................................................... 42

To Change Corporation’s Capital Structure ............................................................................................ 42

Duties ........................................................................................................................................................... 42

Duty of Care .......................................................................................................................................... 43

Duty of Loyalty (The Statutory Fiduciary Duty) ....................................................................................... 45

Duty to Comply ..................................................................................................................................... 49

Statutory Liabilities ....................................................................................................................................... 50

3

Defences to Statutory Liabilities ............................................................................................................ 50

Director Indemnification and Insurance ........................................................................................................ 50

CBCA Indemnification Structure ............................................................................................................ 51

Requirement of Good Faith ................................................................................................................... 51

Indemnification as of Right .................................................................................................................... 52

CYA ....................................................................................................................................................... 52

BJR and Defenses to Illegal Payment of Indemnities .............................................................................. 52

Director and Officer Insurance ............................................................................................................... 52

Selecting (and Removing) Directors ............................................................................................................... 52

Qualifications of Directors ..................................................................................................................... 53

Removal of Directors ............................................................................................................................. 53

Summary of CBCA Provisions ................................................................................................................. 53

5. Shareholders and Governance ........................................................................................................................... 54

Shareholders’ Meetings ................................................................................................................................ 54

Ordinary and Special Resolutions........................................................................................................... 54

Business Conducted At Meetings ........................................................................................................... 54

Special Meetings of the Shareholders .................................................................................................... 55

Voting Rights Attached to Shares ........................................................................................................... 56

Voice in Management ................................................................................................................................... 56

Fundamental Changes ........................................................................................................................... 57

Agreements among Shareholders .......................................................................................................... 58

Unanimous Shareholder Agreements .................................................................................................... 58

Nominating a Different Slate of Directors .............................................................................................. 58

Other Shareholder Proposals ................................................................................................................. 59

Proxy Voting and Governance of Widely-Held Corporations .......................................................................... 59

Intermediaries and Beneficial Owners ................................................................................................... 60

Proxies and Proxyholders ...................................................................................................................... 60

Proxy Solicitation ................................................................................................................................... 61

NI 54–101 .............................................................................................................................................. 62

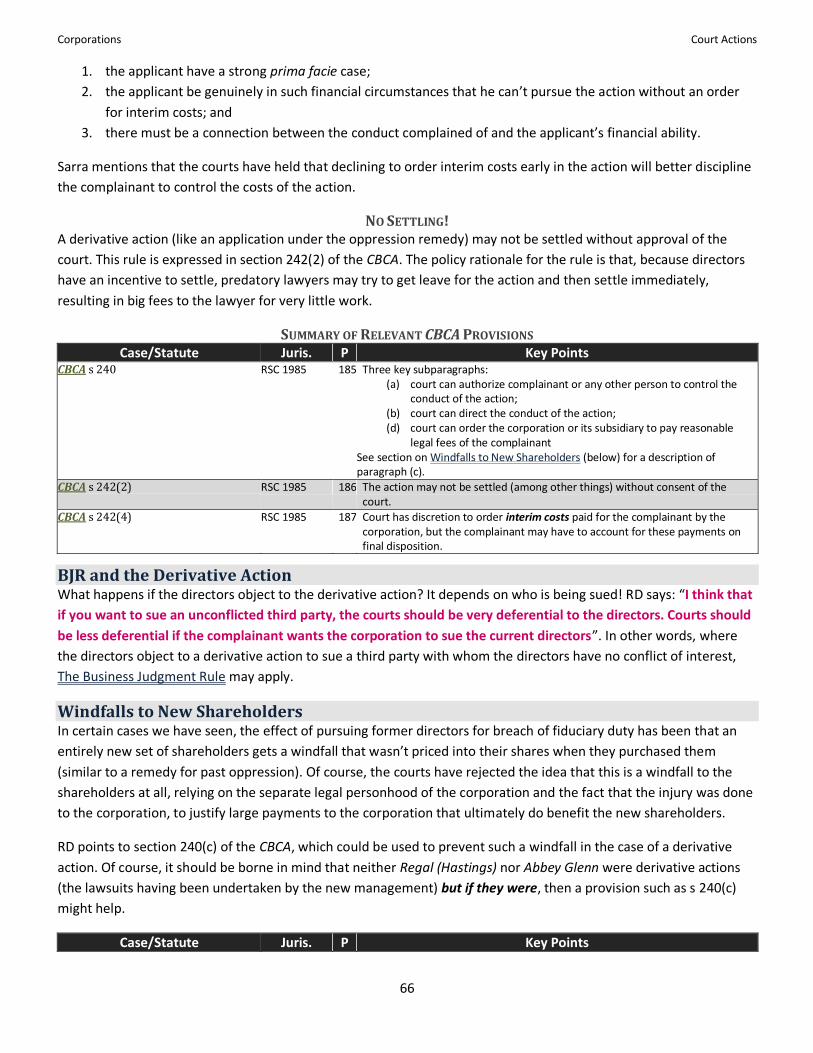

6. Court Actions ..................................................................................................................................................... 63

General Concepts.......................................................................................................................................... 63

Complainants ........................................................................................................................................ 63

Compliance Order Remedy .................................................................................................................... 64

Investigation Remedy ............................................................................................................................ 64

Derivative Action: Enforcing Managers’ Duties .............................................................................................. 64

Requirement of Leave/Test for Leave .................................................................................................... 64

Court Control of the Action ................................................................................................................... 65

BJR and the Derivative Action ................................................................................................................ 66

Windfalls to New Shareholders .............................................................................................................. 66

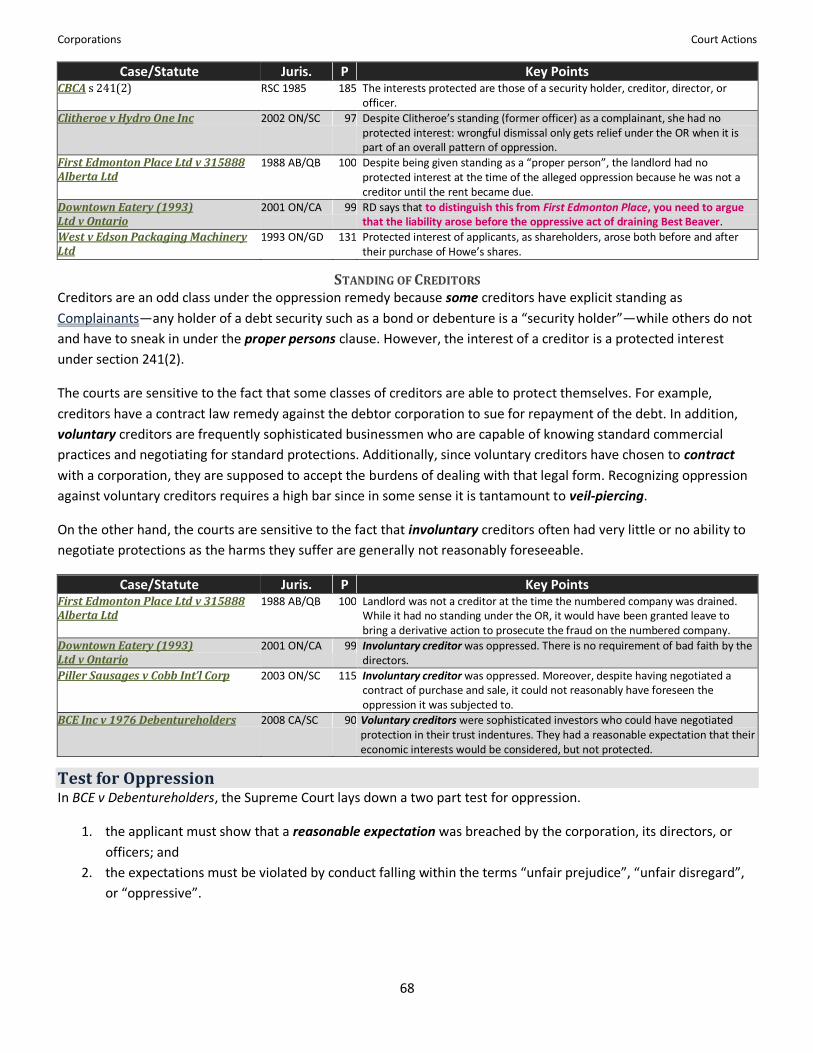

Oppression Remedy: Limiting the Power of Directors .................................................................................... 67

Standing and Interests Protected ........................................................................................................... 67

Test for Oppression ............................................................................................................................... 68

Court Control of the Action ................................................................................................................... 70

4

Tying the Order Sought to Protected Interests ....................................................................................... 70

Limits to the Scope of the Remedy ........................................................................................................ 71

Comparing Oppression and Derivative Action ............................................................................................... 72

When is Oppression Remedy Allowed? .................................................................................................. 72

Advantages and Disadvantages ............................................................................................................. 72

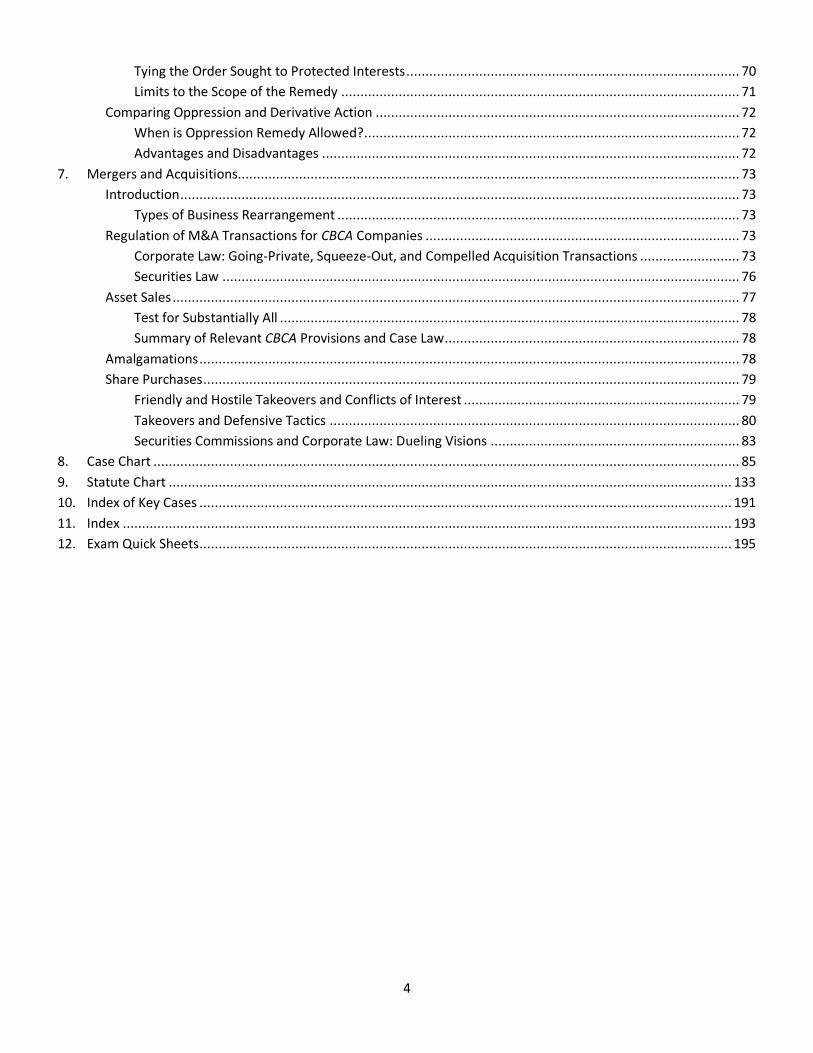

7. Mergers and Acquisitions................................................................................................................................... 73

Introduction .................................................................................................................................................. 73

Types of Business Rearrangement ......................................................................................................... 73

Regulation of M&A Transactions for CBCA Companies .................................................................................. 73

Corporate Law: Going-Private, Squeeze-Out, and Compelled Acquisition Transactions .......................... 73

Securities Law ....................................................................................................................................... 76

Asset Sales .................................................................................................................................................... 77

Test for Substantially All ........................................................................................................................ 78

Summary of Relevant CBCA Provisions and Case Law ............................................................................. 78

Amalgamations ............................................................................................................................................. 78

Share Purchases ............................................................................................................................................ 79

Friendly and Hostile Takeovers and Conflicts of Interest ........................................................................ 79

Takeovers and Defensive Tactics ........................................................................................................... 80

Securities Commissions and Corporate Law: Dueling Visions ................................................................. 83

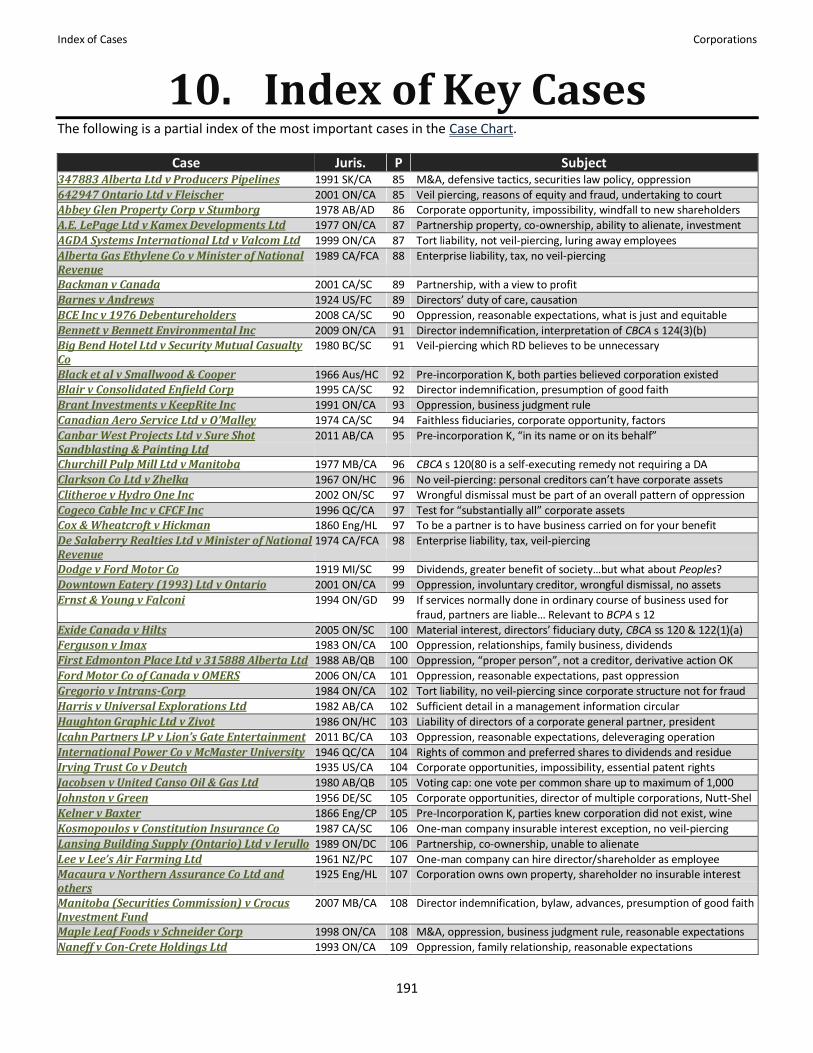

8. Case Chart ......................................................................................................................................................... 85

9. Statute Chart ................................................................................................................................................... 133

10. Index of Key Cases ........................................................................................................................................... 191

11. Index ............................................................................................................................................................... 193

12. Exam Quick Sheets ........................................................................................................................................... 195

Business Organization Corporations

5

1. Business Organization

Concept Cases/Statutes Framwork of Analysis Glossary of Terms Sole Proprietorships Partnerships

o General Partnerships Is there a partnership? Cox & Wheatcroft v Hickman, Pooley v Driver,

Backman v Canada, A.E. LePage Ltd v Kamex Developments Ltd, Lansing Building Supply (Ontario) Ltd v Ierullo

What is the effect of partnership? Ernst & Young v Falconi, Re Thorne and NB Worker’s Compensation Board

How is a partnership governed? Partnership Act Table of Statutory Provisions Partnership Act

o Limited Partnerships Remainder of the Act Applies Partnership Act At Least 2 Partners Partnership Act s 50 Limited Liability Partnership Act ss 57, 64

Corporate General Partners Haughton Graphic Ltd v Zivot, Nordile Holdings Ltd v Breckenridge

Separation of Ownership and Control Table of Statutory Provisions Partnership Act

FRAMEWORK OF ANALYSIS When analyzing a business organization problem, ask yourself:

1. What is the form of the legal relationship among those involved in the business?

2. How does the law treat a business organization in which those involved have this kind of relationship, with

respect to:

duties and obligations between themselves;

how business decisions are made and by whom;

the need to advise the rest of the world about the type of relationship;

the ability of individuals in the relationship to make binding commitments on behalf of the business

or the other individuals involved; and

the potential that the activities of one individual in the business will make all or some of the other

individuals personally liable for any damage resulting from those activities?

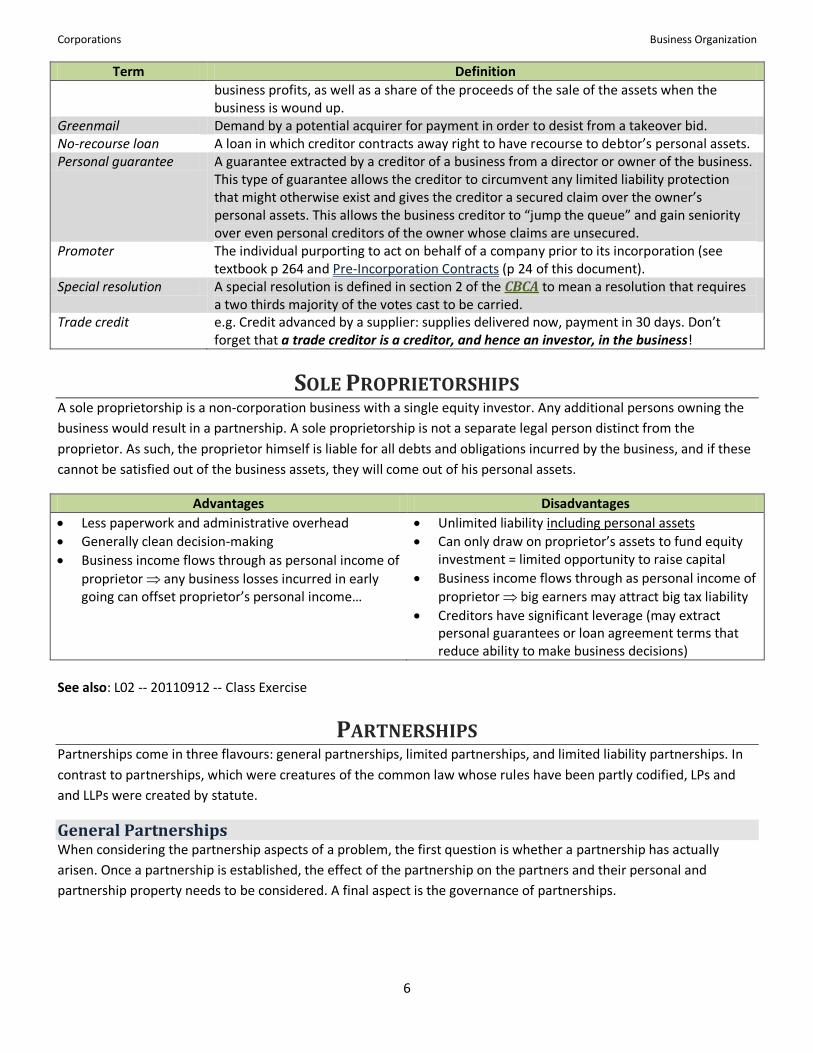

GLOSSARY OF TERMS

Term Definition Continuation The process of changing the corporate law regime that governs a corporation (e.g. moving

from BCBCA to CBCA governance). Distributing Corporation

Essentially, a public company (a “reporting issuer” under securities regulation).

Equity The right to receive a residual amount. Normally represents a claim to a share of the

Corporations Business Organization

6

Term Definition business profits, as well as a share of the proceeds of the sale of the assets when the business is wound up.

Greenmail Demand by a potential acquirer for payment in order to desist from a takeover bid. No-recourse loan A loan in which creditor contracts away right to have recourse to debtor’s personal assets. Personal guarantee A guarantee extracted by a creditor of a business from a director or owner of the business.

This type of guarantee allows the creditor to circumvent any limited liability protection that might otherwise exist and gives the creditor a secured claim over the owner’s personal assets. This allows the business creditor to “jump the queue” and gain seniority over even personal creditors of the owner whose claims are unsecured.

Promoter The individual purporting to act on behalf of a company prior to its incorporation (see textbook p 264 and Pre-Incorporation Contracts (p 24 of this document).

Special resolution A special resolution is defined in section 2 of the CBCA to mean a resolution that requires a two thirds majority of the votes cast to be carried.

Trade credit e.g. Credit advanced by a supplier: supplies delivered now, payment in 30 days. Don’t forget that a trade creditor is a creditor, and hence an investor, in the business!

SOLE PROPRIETORSHIPS A sole proprietorship is a non-corporation business with a single equity investor. Any additional persons owning the

business would result in a partnership. A sole proprietorship is not a separate legal person distinct from the

proprietor. As such, the proprietor himself is liable for all debts and obligations incurred by the business, and if these

cannot be satisfied out of the business assets, they will come out of his personal assets.

Advantages Disadvantages Less paperwork and administrative overhead Generally clean decision-making Business income flows through as personal income of

proprietor any business losses incurred in early going can offset proprietor’s personal income…

Unlimited liability including personal assets Can only draw on proprietor’s assets to fund equity

investment = limited opportunity to raise capital Business income flows through as personal income of

proprietor big earners may attract big tax liability Creditors have significant leverage (may extract

personal guarantees or loan agreement terms that reduce ability to make business decisions)

See also: L02 -- 20110912 -- Class Exercise

PARTNERSHIPS Partnerships come in three flavours: general partnerships, limited partnerships, and limited liability partnerships. In

contrast to partnerships, which were creatures of the common law whose rules have been partly codified, LPs and

and LLPs were created by statute.

General Partnerships When considering the partnership aspects of a problem, the first question is whether a partnership has actually

arisen. Once a partnership is established, the effect of the partnership on the partners and their personal and

partnership property needs to be considered. A final aspect is the governance of partnerships.

Business Organization Corporations

7

Two of the most crucial aspects of partnership are unlimited liability and the fact that a partnership may arise by

operation of law. This means that a partner may be liable under one or more provisions of the BCPA despite believing

himself not to be in a partnership. The courts may also refuse to recognize a partnership.

IS THERE A PARTNERSHIP? The test for partnership is found in s 2 of the Partnership Act. It is an objective test:

1. The relation which subsists between persons

2. Carrying on a business

3. In common

4. With a view to profit

Two people are needed for a partnership. This is obvious! One person by himself is a sole proprietor.

Any legal person can be a partner in a partnership. This means partnerships can arise between any mix of natural

persons and corporations.

Case/Statute Juris. P Key Points Lansing Building Supply (Ontario) Ltd v Ierullo

1989 ON/DC 106 Intention of the parties does not matter. Despite emphasizing in the “co-ownership agreement” that they are not partners and there is no partnership, the court found a partnership.

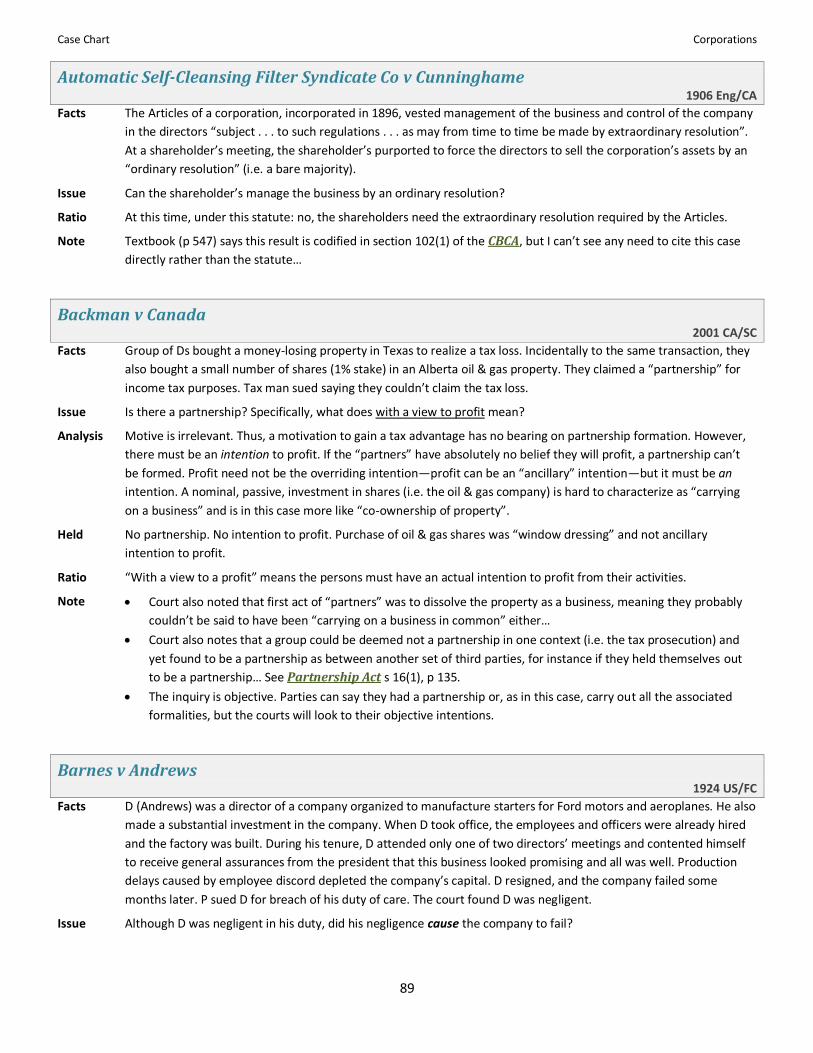

Backman v Canada 2001 CA/SC 89 Objective test: intention of the parties does not matter. Despite calling itself a partnership and carrying out all the formalities, a “partnership” set up purely to realize a tax loss was found not to be a partnership.

CREDITORS A “true” creditor is not a partner, but partnerships may arise between “creditors” and “debtors” if, for example, the

“debt” is actually a disguised equity interest.

Case/Statute Juris. P Key Points Cox & Wheatcroft v Hickman 1860 Eng/HL 97 To be a partner is to have a business carried on for your benefit.

While receipt of profit is evidence of a partnership, the presumption is rebuttable.

Creditors found not to be partners. Pooley v Driver 1876 Eng/CH 116 Debt investment looked suspiciously like an equity investment.

“Creditors” found to be partners. This would not fall under BCPA s 4(c)(i) because the debt is never

liquidated!

CARRYING ON A BUSINESS IN COMMON The courts look for various indicators that the putative partners are carrying on a business, and consider whether

they intended to carry it on in common. As usual, the test is objective.

Case/Statute Juris. P Key Points A.E. LePage Ltd v Kamex Developments Ltd

1977 ON/CA 87 No partnership found. Key facts: owners of the building maintained completely separate interests

which they could alienate. This is inconsistent with partnership property, which is jointly held.

Court also implied mere buying of an apartment building for resale does not constitute “carrying on a business”.

Corporations Business Organization

8

Case/Statute Juris. P Key Points Lansing Building Supply (Ontario) Ltd v Ierullo

1989 ON/DC 106 Partnership found. Distinguished from Kamex because onerous restrictions on each co-owner’s

share were more consistent with jointly owned partnership property. Also, real estate development found to be “carrying on a business” in

contrast with merely investing in an apartment building. Volzke Construction v Westlock Foods 1986 AB/CA 130 This case is on pp 80–3 of the text. We did not cover it in class, but it is worth re-

reading once to see a relationship that was found to be a partnership by the courts.

WITH A VIEW TO PROFIT The putative partners must intend to profit, even if they do not in fact actually manage to. However, their motivation is irrelevant. For instance, if they intend to profit from a relationship and enter into it because they are motivated to

realize a tax advantage, this motivation is irrelevant. But if they don’t intend to profit, they aren’t a partnership.

Case/Statute Juris. P Key Points Backman v Canada 2001 CA/SC 89 The supposed partners wanted to realize a tax loss and had no intention of

profiting from the transaction. It isn’t necessary for the overriding intention to be for profit-making. It is

sufficient that there is an ancillary profit-making purpose. However, the oil & gas property failed to meet the ancillary profit-making

purpose, partly because SCC found that aspect of the partnership failed even to meet the “business in common” requirement—it was a nominal investment and at best co-ownership of property.

WHAT IS THE EFFECT OF PARTNERSHIP? Partnership at law affects the partners in various ways. General partnership has its single most important effect on

the liability of the partners for debts, contracts, and torts. This liability follows from the law of agency and status of

the partners as agents for each other. There are additional considerations, such as how partners and partnerships are

treated for income tax purposes; whether partnerships can employ a partner; and procedural aids made available to

people who want to sue partnerships.

AGENCY Under s 7 of the BCPA, “every partner is an agent of the firm and of every other partner for the purpose of the

business of the partnership”. This means that any contract entered into by one partner ostensibly on behalf of the

firm is binding on all the other partners. I’m not sure this is as relevant to tort liability as it is to contract, but in any

case, liability is discussed directly below.

LIMITS OF AGENCY Clearly the concept of agency must have some limits. Both s 7(1), s 7(2), and s 10 of the Partnership Act help define

these limits (see p 134).

s 7(1) uses the words “for the purpose of the business of the partnership” to delimit the scope of agency. s 7(2) further clarifies. Acts of partners “for carrying on business in the usual away bind the firm”. But if both

subparagraphs (a) and (b) are satisfied, namely:

(a) the partner has no authority to act in the matter; and

(b) the third party knows about the lack of authority, or does not believe the partner to be a partner

then the act does not bind the firm.

s 10 allows partners to agree among themselves that a certain partner will not have authority to bind the

firm in a certain matter. If a partner breaks this agreement, his contravening act is not binding on the firm if

the third party involved had notice of the agreement.

Business Organization Corporations

9

RD says there is recent SCC jurisprudence holding that if you believe yourself to be contracting with an individual person, you can’t turn around and sue the firm: Vieweger Construction Co v Rush & Tompkins Construction Ltd (1965

CA/SC).

Case/Statute Juris. P Key Points Ernst & Young v Falconi 1994 ON/GD 99 In interpreting the [Ontario] liability for wrongs section, the court interprets the

phrase “ordinary scope of business”, which is similar to “carrying on business in the usual way”.

LIABILITY As well as attracting tort liability due to Agency (above), the BC Partnership Act has a number of provisions on

liability:

s 11: A partner is jointly liable with the others for all debts and obligations incurred while he is a partner…

o Note that this doesn’t include debts incurred before or after…

o This includes judgment debts…

ss 12–14: Together these paragraphs make a partner jointly and severally liable for:

o Torts committed by a partner acting in the ordinary course of business of the firm or with the

authority of the other partners…

o Money of a third person “misapplied” by a partner or the firm

Note that s 12 clearly covers torts but doesn’t seem to cover the case of torts committed by an employee. See

Employment (below) for more on that case.

Case/Statute Juris. P Key Points Ernst & Young v Falconi 1994 ON/GD 99 In interpreting the [Ontario] liability for wrongs section, the court interprets the

phrase “ordinary scope of business”, which is applicable to… Partnership Act s 12 RSBC 1996 135 …liability for tortious acts “in the ordinary course of business” of the firm.

PERSONAL CREDITORS Personal creditors of a partner can satisfy a judgment against a partner in his personal capacity out of that partner’s share of the partnership assets if it cannot be fully satisfied from the partner’s personal assets.

PARTNERSHIP CREDITORS Because a partner is jointly liable for debts and obligations incurred (BCPA s 11) while he is a partner, any partner’s personal assets may be at stake if an obligation is incurred that cannot be satisfied by the partnership assets.

PARTNERSHIP PROPERTY While the common law doesn’t regard a partnership as a legal person—and thus property owned by the partnership

must be legally owned by the individual partners or some other legal person—it is still considered to be held jointly.

Thus, no partner has a right to a division of the property in specie. Instead, they have a right to a division of the

profits, and to a sale and division of the proceeds of sale on dissolution after discharge of liabilities.

See text pp 80–1 in Kamex. BCPA s 6 defines partnership property, and s 23(2) says that legal owners of partnership

property hold it upon trust for the partnership as a whole.

TAX TREATMENT The Income Tax Act, as distinct from other laws, treats a partnership as a single entity for the purpose of determining

overall P&L. At this point, however, P&L is divided among the partners according to their share in the firm and flows

Corporations Business Organization

10

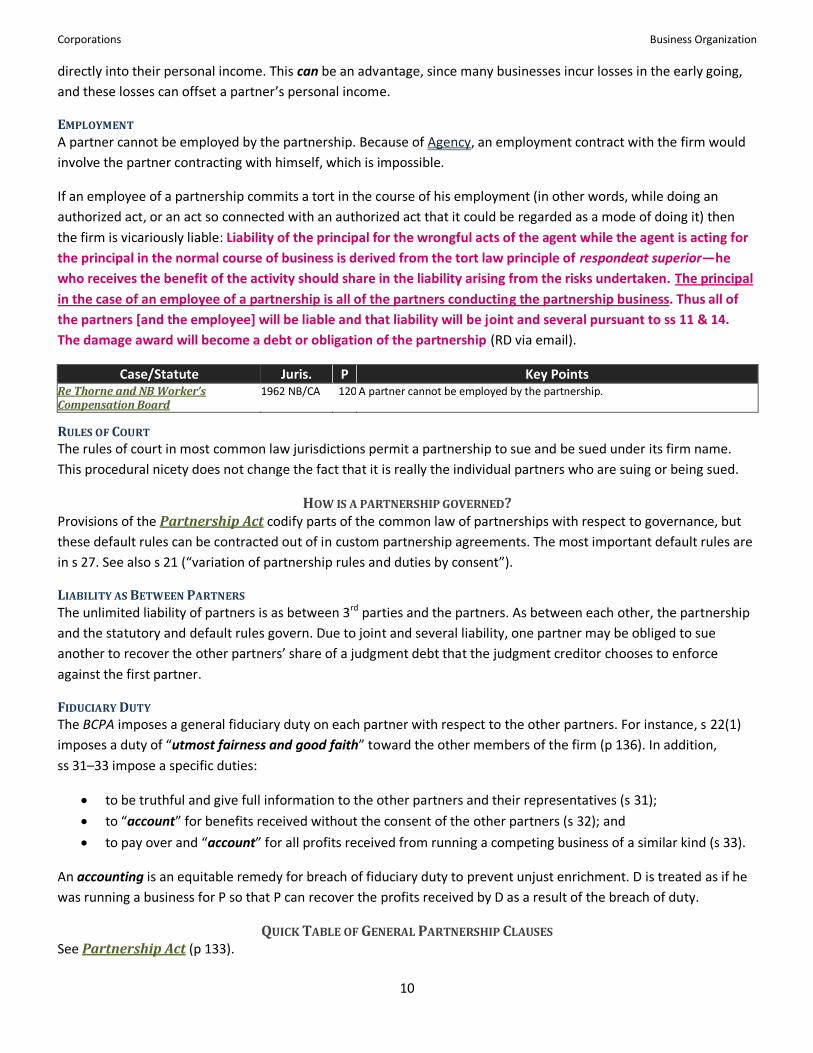

directly into their personal income. This can be an advantage, since many businesses incur losses in the early going,

and these losses can offset a partner’s personal income.

EMPLOYMENT A partner cannot be employed by the partnership. Because of Agency, an employment contract with the firm would

involve the partner contracting with himself, which is impossible.

If an employee of a partnership commits a tort in the course of his employment (in other words, while doing an

authorized act, or an act so connected with an authorized act that it could be regarded as a mode of doing it) then

the firm is vicariously liable: Liability of the principal for the wrongful acts of the agent while the agent is acting for the principal in the normal course of business is derived from the tort law principle of respondeat superior—he who receives the benefit of the activity should share in the liability arising from the risks undertaken. The principal in the case of an employee of a partnership is all of the partners conducting the partnership business. Thus all of the partners [and the employee] will be liable and that liability will be joint and several pursuant to ss 11 & 14. The damage award will become a debt or obligation of the partnership (RD via email).

Case/Statute Juris. P Key Points Re Thorne and NB Worker’s Compensation Board

1962 NB/CA 120 A partner cannot be employed by the partnership.

RULES OF COURT The rules of court in most common law jurisdictions permit a partnership to sue and be sued under its firm name.

This procedural nicety does not change the fact that it is really the individual partners who are suing or being sued.

HOW IS A PARTNERSHIP GOVERNED? Provisions of the Partnership Act codify parts of the common law of partnerships with respect to governance, but

these default rules can be contracted out of in custom partnership agreements. The most important default rules are

in s 27. See also s 21 (“variation of partnership rules and duties by consent”).

LIABILITY AS BETWEEN PARTNERS The unlimited liability of partners is as between 3rd parties and the partners. As between each other, the partnership

and the statutory and default rules govern. Due to joint and several liability, one partner may be obliged to sue

another to recover the other partners’ share of a judgment debt that the judgment creditor chooses to enforce

against the first partner.

FIDUCIARY DUTY The BCPA imposes a general fiduciary duty on each partner with respect to the other partners. For instance, s 22(1)

imposes a duty of “utmost fairness and good faith” toward the other members of the firm (p 136). In addition,

ss 31–33 impose a specific duties:

to be truthful and give full information to the other partners and their representatives (s 31);

to “account” for benefits received without the consent of the other partners (s 32); and

to pay over and “account” for all profits received from running a competing business of a similar kind (s 33).

An accounting is an equitable remedy for breach of fiduciary duty to prevent unjust enrichment. D is treated as if he

was running a business for P so that P can recover the profits received by D as a result of the breach of duty.

QUICK TABLE OF GENERAL PARTNERSHIP CLAUSES See Partnership Act (p 133).

Business Organization Corporations

11

Clause Meaning P Relevant Case(s) Rules for determining the existence of a partnership

2 Definition of partnership 133 Cox & Wheatcroft, Pooley, Kamex, Lansing, Backman

3 Corporations not partnerships 133 4 Rules for determining partnership 133

(a) Co-owners not necessarily partners even if sharing profit 133 Kamex, Lansing (c) Profit evidence of partnership except where not (rebuttable

presumption). There are qualifications: 133

(i) Receipt of debt or other liquidated amount not necessarily partner

133 Cox & Wheatcroft v Hickman, Pooley v Driver

(ii) Employee getting profit not necessarily partner 133 (iii) Annuity paid to relatives of deceased partner doesn’t

necessarily make them partners 133

(iv) Lending to firm doesn’t necessarily make you partner 134 Cox & Wheatcroft v Hickman, Pooley v Driver

(v) Person who sold his share in return for an annuity or share in profits (see s 34, also, p 139) not necessarily partner

134

Partners are agents of one another 7 Liability of partners (and agency) 134 8 Acts or instruments in the firm name 134 9 No pledge of credit for non-firm business 134 10 Notice of restriction of power of partner 135 16 Person representing himself as partner 135 17 Partner’s evidence 136

No limited liability status Creditor can go after the assets of any one of the partners

11 , 19(1–2) Liability of partners for firm debts 135 12 Liability for wrongs 135 13 Liability for misapplication of funds 135 14 Joint and several liability under ss 12–3 135 15 Liability for trust funds 135

Partners owe each other a fiduciary obligation 22 Duty of fairness and good faith 136 31 Partners must render true accounts and full information 138 32 Partners must account for benefits 138 33 Profits of partner carrying on a similar business 139

Partnership property 6 Defines partnership property 134 23 Application of partnership property 136

(1) Partnership property must be held by partners exclusively for the partnership…

136 Inconsistent with A.E. LePage Ltd v Kamex Developments Ltd

(2) Legal owners of partnership property are trustees 136 Also inconsistent with Kamex 24 Property bought with firm money belongs to partnership 137 26 Execution against partnership property requires judgment

against firm 137

Rules of conduct for partnerships 27 Default rules for partnership 137 28 Majority cannot expel partner 138

Partnerships can be ended 29 Ending the partnership 138 30 Continuation of a partnership after expiry 138 35 Dissolution of the partnership 139

Partnerships with more than 2 partners can continue after dissolution

Corporations Business Organization

12

Clause Meaning P Relevant Case(s) 36 Dissolution by bankruptcy, death, or dissolution of partner

or charging order 139

Partners can exclude one of the partners through the courts 38 Power of court to decree dissolution in certain cases 140

Dissolution/change in firm constitution 39 Change in firm 140 40 Dissolution 141 41 Authority of partners after dissolution 141

Rights of outgoing partners 45 Rights where partnership dissolved by death or retirement 141 46 Debts at date of dissolution or death 142

Partnership property is divisible on dissolution 47 Settlement of accounts on dissolution 142

Limited Partnerships Unlike partnerships, which arose at common law and were later codified, limited partnerships are statutory beasts

that were created to provide an option to alleviate the extremes of unlimited liability inherent in partnerships. As such, limited partnerships can’t just arise by operation of law! In British Columbia, a limited partnership can only be

formed by filing a certificate in the correct form, as stipulated in s 51 of the BCPA.

Note that, at least for the purposes of having a partnership recognized under tax law, it probably isn’t enough to file

the certificate in the correct form. While s 51 says that the limited partnership “is formed when” the certificate is filed, in Backman v Canada, the alleged partnership was supposed to be a limited partnership. Thus, similar

formalities to those required in BC had likely been followed. Yet the Supremes held that the entity created was not a

partnership at all and thus the “partners” could not take advantage of their tax loss under the Income Tax Act.

REMAINDER OF THE ACT APPLIES Note that the provisions of the BCPA discussed under General Partnerships apply to limited partnerships unless

otherwise contracted out of or contradicted by the provisions of Part 3.

AT LEAST 2 PARTNERS A limited partnership needs at least two partners, a limited partner and a general partner. See s 50.

LIMITED LIABILITY Under s 57 of the Partnership Act, the liability of a limited partner for obligations of the limited partnership is

limited to the amount of his investment. However, a limited partner can lose the benefit of this limitation by taking

part in the “management” of the business (see s 64 on p 145).

CORPORATE GENERAL PARTNERS What exactly does “management” entail? Clearly, it involves more than exercising the rights accorded to limited partner under s 58. But what if the general manager of a limited partnership is a corporation, and the directors and

officers of the corporation are limited partners of the partnership? RD says the ratio of the following cases is identical.

Case/Statute Juris. P Key Points Haughton Graphic Ltd v Zivot 1986 ON/HC 103 Zivot found liable as a general partner.

He held himself out to be the “president” of the limited partnership, including printing this on business cards, the magazine masthead, and when introducing himself to people.

AB statute used the word “control”, not “management” as in s 64…

Business Organization Corporations

13

Case/Statute Juris. P Key Points Nordile Holdings Ltd v Breckenridge 1992 BC/CA 111 Ds found NOT liable as a general partner.

An agreed statement of facts stated that Ds participated in managing the partnership “solely in their capacities as directors and officers of the general partner, Arbutus”.

Many limited partnerships have a single corporate general partner, and that corporation in turn is purposefully set up

to have very few assets. However, the directors of a corporation have a fiduciary duty to act in the best interests of

the corporation, which in turn has fiduciary duties as general partner, so the actions of the directors of the corporate

general partner are still constrained.

SEPARATION OF OWNERSHIP AND CONTROL: LIMITED PARTNERSHIPS From the textbook, p 122:

Limited liability facilitates having a large number of investors, and many of them will have relatively small stakes in the business. They will accordingly have limited incentive to carefully monitor the management of the business. In limited partnerships, the incentive is further decreased as a result of provisions in the statute that make investors potentially liable as general partners if they take part in the management of the business.

Limited partnerships, and limited liability partnerships, like corporations, tend to create “separation of ownership from control”. The limited partners often contribute the bulk of the capital and are often referred to as “owners” of the business, although RD and the textbook are sceptical about this, since the BCPA effectively prevents limited

partners from controlling the business (without attracting liability as general partners). This can potentially place the

limited partners at the mercy of the managers of the business. Unlike corporation law, which has numerous statutory

requirements designed to protect the investors, it is up to the limited partners to ensure adequate disclosure and

other requirements are drafted into the partnership agreement. The BCPA is silent.

QUICK TABLE OF LIMITED PARTNERSHIP CLAUSES Clause Meaning P Relevant Case(s)

Is composed of both general and limited partners 50 Indicates that at least 2 people required: a general partner

and a limited partner. 143

Can only be formed by filing a certificate 51 Formation of limited partnership (requires certificate) 143

Has a name that complies with restrictions 53 Requires “Limited Partnership” suffix and can’t contain

names of limited partners. 144

Provides limited liability to people who do not take part in the management of the firm 56 Rights of general partners…Some acts require unanimous

consent of limited partners. 144

57 Liability of limited partner is limited to amount of investment.

144

58 Rights of limited partners. 145

64 Limited partners not liable unless they take part in management.

145 Haughton Graphic Ltd v Zivot and Nordile Holdings Ltd v Breckenridge

Corporations Business Organization

14

Limited Liability Partnerships Not examinable this year.

A Relationship of Trust and Confidence Davis is at pains to remind us that a partnership is a relationship of trust and confidence. The agency and unlimited

liability aspects; the fiduciary duties; and the fact that limited partners are essentially at the mercy of general

partners are examples of this phenomenon. To enter into a partnership is to trust one’s partners implicitly. This is one aspect in which, at least in theory, a partnership may differ significantly from a corporation.

Partnerships Example Problem See: L04 -- 20110919 -- Jerry's Cherry [under Review/Fact Patterns]

Introduction to Corporations Corporations

15

2. Introduction to Corporations

Concept Cases/Statutes Three Theories of Corporations

o Nexus of Contracts o Mediating Hierarchy Peoples Department Stores Inc (Trustee of) v

Wise o Public Institution

Incorporation and Its Consequences o The Corporation as a “Separate Legal Person” Salomon v Salomon & Co Ltd, Lee v Lee’s Air

Farming Ltd, Macaura v Northern Assurance Co Ltd and others

o Limited Liability Agency Costs

The Process of Incorporation CBCA ss 6(1), 8, 9 Piercing the “Veil”

o Insurable Interests Cases Macaura v Northern Assurance Co Ltd and others, Kosmopoulos v Constitution Insurance Co

o Fraud and Reasons of Justice Clarkson Co Ltd v Zhelka, Big Bend Hotel Ltd v Security Mutual Casualty Co, 642947 Ontario Ltd v Fleischer

o Tax Liability De Salaberry Realties Ltd v MNR, Alberta Gas Ethylene Co v MNR

o Enterprise Liability De Salaberry, AGEC, Gregorio v Intrans-Corp o Tort Liability Gregorio, Walkovszky v Carlton, Wolfe v Moir

The Said v Butt Exception Said v Butt, AGDA Systems International Ltd v Valcom Ltd

Pre-Incorporation Contracts o Common Law of Pre-Incorporation Contracts Kelner v Baxter, Newborne v Sensolid (Great

Britain) Ltd, Black et al v Smallwood & Cooper, Wickberg v Shatsky

o CBCA Statutory Regime CBCA s 14, Sherwood Design Services Inc v 872935 Ontario Ltd, Canbar West Projects Ltd v Sure Shot Sandblasting & Painting Ltd

o BCBCA Statutory Regime BCBCA s 20, Wickberg v Shatsky Agency

o Defective Appointments CBCA s 116 o Indoor Management Rule CBCA ss 17, 18, 116, Royal British

Bank v Turquand, Sherwood, Canadian Laboratory Supplies Ltd v Englehard Indus. of Canada Ltd

o Management Hierarchy: CBCA CBCA ss 102, 115, 121 Ultra Vires: Boundaries on the Corporation’s Capacity to Act

o Ultra Vires Doesn’t Really Exist Anymore Ashbury Ry Carriage & Iron Co v Riche o Modern Restrictions on Management Authority CBCA ss 6(1)(f), 15, 16(2–3), 247

Constitutional Considerations o Federal vs Provincial Incorporation BNA Act, 1867 ss 91 & 92(11)

Federal Incorporation BNA Act, 1867 s 91, Citizens Ins Co v Parsons Extra-Provincial Licensing BNA Act, 1867 s 92(11), Bonanza Creek Gold

Mining Co v The King, BCBCA s 375 Continuation

o Charter Rights Ford v Québec, R v Big M Drug Mart, Canadian Egg Marketing Board Agency v Richardson

Corporations Introduction to Corporations

16

THREE THEORIES OF CORPORATIONS The textbook presents three “theories” of the corporation:

1. Wealth maximization/nexus of contracts (see pp 41–3 of the textbook)

2. The corporation as mediating hierarchy (see pp 43–7)

3. The corporation as public institution (see pp 48–57)

We are supposed to keep these “theories” in view as we go through the course learning the law on corporations. Past RD exams don’t have essay components, but these might be the kind of thing that would support a “public policy argument” on an exam…

Nexus of Contracts The nexus of contracts theory (proposed by William Bratton, p 41) is that the firm serves as a nexus for a set of

contracting relations among individual factors of production. The theory is meant to stand in contrast to a

management centred conception. The firm springs out of contracts in markets for corporate securities, managers,

and other labour. Since the contracts are bilateral, management power and corporate hierarchy, as previously

conceived, disappear. In a firm of bilateral contracts between free market actors, both parties possess equal power to contract someplace else.

The theory applies the principle of natural selection and posits that rational economic actors solve problems in the

process of pursuing wealth maximization. One component of the theory is that firm contracts take forms

determined by the imperative of agency cost reduction. Since rational economic actors know about agency costs,

they charge these costs against their contracting partners ahead of time. Given competition, the party that most

reduces agency costs has the edge. Thus the lowest cost contract forms survive. Within the nexus of contracts

theory, managers act as agents of shareholder principals and attempt to maximize shareholder wealth.

Mediating Hierarchy The mediating hierarchy theory (proposed by Blair & Stout on p 43 of the textbook) “builds on” the “contractarian” thinking of the nexus of contracts theory by “acknowledging the limits of what can be achieved by explicit

contracting”.

Blair & Stout argue that an essential but frequently overlooked “contract” fundamental to public corporations is the “pactum subjectionis” under which shareholders, managers, employees, and other groups that make firm-specific

investments yield control over both the investments themselves and the resulting output to the corporation’s internal governing hierarchy. They say that the notion that shareholders “own” corporations is incorrect because shareholders rights are of such limited value that they are unlikely to influence the outcome except in extreme cases.

Corporate law thus leaves boards of directors free to pursue whatever projects and directions they choose.

The mediating hierarchy is a “team production analysis” of the public corporation. If corporate law is not designed

primarily to protect shareholders—if, instead, it is designed to protect the corporate coalition by allowing directors

to allocate rents among various stakeholders, while guarding the collation as a whole only from gross self-dealing by

directors—then the rules of corporate law begin to make more sense.

Public Institution The theory of the corporation as public institution is advanced by Greenfield (p 48). It goes way out into cuckoo left

field and says that contract and property rights “are not best perceived as natural, pre-legal, or non-political, but

Introduction to Corporations Corporations

17

rather should be seen as tools to be utilized in furtherance of social good, however defined” (p 50). To this end,

Greenfield sets out 5 “principles”:

1. The ultimate purpose of corporations should be to serve the “interests of society as a whole”. (p 51)

2. Corporations are distinctively able to contribute to the “societal good” by creating financial prosperity. (p 51)

3. Corporate law should further principles 1 & 2. (p 52)

4. A corporation’s wealth should be shared “fairly” among those to contribute to its creation. (p 53)

Here, of course, Greenfield includes labour and consumers, as well as shareholders and creditors. He also

includes that most successful investor of all, the Government.

5. Participatory, democratic corporate governance is the best way to ensure “sustainable” creation and “equitable” distribution of corporate wealth. (p 54)

Among the many ingenious proposals here is allowing employees and “communities in which the company employs a significant percentage of the workforce” to propose representatives on the board.

Case/Statute Juris. P Key Points Peoples Department Stores Inc (Trustee of) v Wise

2004 CA/SC 114 SCC seems to endorse a mediating hierarchy (or is it public institution?) view of corporations, rather than the wealth maximization theory.

RD: according to the SCC, no one has a right to complain about a decision of the directors since it “may be” legitimate to consider the interests of various groups, of which the shareholders are only one.

INCORPORATION AND ITS CONSEQUENCES The Corporation as a “Separate Legal Person” The following cases are considered in more detail in the section on Piercing the “Veil” (p 20):

Case/Statute Juris. P Key Points Salomon v Salomon & Co, Ltd 1896 Eng/HL 123 A corporation is a separate legal person. Even a “one-man company” is a

separate entity, not an agent of the controlling shareholder/director. Lee v Lee’s Air Farming Ltd 1961 NZ/PC 107 A corporation is distinct from its controlling shareholders/directors and can

contract with them in their personal capacity. Macaura v Northern Assurance Co Ltd and others

1925 Eng/HL 107 A corporation owns its own property, and neither a shareholder nor a creditor has any legal interest in it.

This case should not be considered in isolation from Kosmopoulos v Constitution Insurance Co (p 106). See the Insurable Interests Cases.

Limited Liability

AGENCY COSTS According to the textbook (p 149), “an economic analysis of the situation posits that the separation of ownership and control in widely held corporations introduces what is known as an ‘agency cost’ problem, since all firm managers (as

agents) have imperfect incentives to maximize the interests of all claimholders (as principals).” In other words, the costs of doing poor work are shifted from the economic agent to another person, the shareholder. Agency problems

can include:

Effort Shirking

Asset Diversion

Corporations Introduction to Corporations

18

THE ROLE OF CORPORATE LAW Corporate law addresses issues of shirking and diversion by providing general parameters for behaviour by insiders

and by establishing a governance structure in statute. Corporate law regulates the relationship between insiders and

outsiders with the objective of protecting the legitimate interests of the participants while retaining the advantages

of the firm.

See also: L06 -- 20110926 -- The Firm

EASTERBROOK & FISCHEL, “LIMITED LIABILITY AND THE CORPORATION” In an article on p 149 of the textbook, Frank Easterbrook and Daniel Fischel argue that limited liability actually

reduces the agency costs of the separation and specialization inherent in a large firm. They give the following

reasons:

1. Limited liability decreases the need to monitor. This is because it makes diversification and passivity a more rational investment strategy (RD) than active monitoring, thus decreasing the cost of operating the

corporation. Investors can also price their agency cost risk into the shares (RD).

2. Limited liability reduces the costs of monitoring other shareholders. In a non-limited liability world,

shareholders would have to monitor each other since the greater any shareholder’s wealth, the more likely he will be to get stuck paying a judgment cost due to joint and several liability. Limited liability makes the

identity of other shareholders irrelevant, thus avoiding these costs.

3. Limited liability promotes free transfer of shares, increasing managers’ incentives to act efficiently. Under a rule of unlimited liability, shares are not liquid (RD) since the identity of the shareholder must be factored

into the price. With limited liability, shares are fully liquid (RD) and the price reflects the value of the firm as

reflected by the specialized agents. Poorly-run firms will attract new investors who can assemble large blocks

of shares and install a new managerial team, so there is an incentive to run the firm well to keep the price up.

4. Limited liability makes it possible for market prices to impound additional information about the firm.

With unlimited liability, this information would be obscured since the identity of the shareholder factors into

the price.

5. Limited liability allows “more efficient” diversification. Investors can minimize risk by diversifying and firms

can raise capital at lower costs because investors need not bear the special risk associated with non-

diversified holdings. Unlimited liability makes diversification risk increasing instead of risk reducing!

6. Limited liability facilitates optional investment decisions. Firm managers can maximize investors’ welfare by investing in any project with net present value, including riskier ventures, since investor risk is hedged via

diversification.

PROTECTING THE BUSINESS CAPITAL: PERSONAL LIABILITY While corporations protect the personal assets of shareholders from the liability of the corporation, they also protect

the business capital of the corporation from the personal liability of the investors. If a shareholder’s share in the business is taken, he loses the shares, but the paid-in capital from those shares cannot be withdrawn. The

shareholder’s rights under the shares are merely reassigned to his judgment creditor.

Consider, for example, the case of Clarkson Co Ltd v Zhelka (p 96): if the trustee was smart, he would have gone

after Selkirk’s shares. But even if the trustee had acquired them, he wouldn’t have been able to take the business assets of the firm. (Except that this is a foolish example, since the trustee would have become the sole shareholder,

installed himself as director, and conveyed the land to Selkirk’s personal creditors. But that’s beside the point!).

Introduction to Corporations Corporations

19

THE PROCESS OF INCORPORATION We went over pp 251–261 very rapidly at the end of L06. The process and requirements of incorporation obviously

aren’t that important.

A corporation is formed by:

1. filing articles of incorporation;

2. filing a notice of the registered office of the corporation;

3. filing a notice of directors; and

4. paying the prescribed fee.

Under the CBCA, step 1 is done using “Form 1” and steps 2–3 are done using “Form 2”.

Articles of Incorporation The articles of incorporation for simple CBCA corporations are prepared by filling out Form 1. The current Form 1

requires the following specific information about the proposed corporation, pursuant to s 6(1) of the CBCA:

Item CBCA Section Description

(a) Name 6 (1)(a) 10 (5–6)

Name must be unique, which requires a name search except for numbered companies. Name must include a suffix such as “Ltd”, “Inc”, or “Corp”. For speed, a numbered company can be incorporated (instead of a name, bureaucracy assigns you a number, such as 12345 Canada Limited. Law firms often keep a stable of numbered “shelf” companies for quick use by clients. (see, e.g., Sherwood Design Services Inc v 872935 Ontario Ltd). Within limits of s 10, these numbered companies can carry on business under a “firm name or style”.

(b) Registered office 6 (1)(b) Articles only require province of registered office. Street address must be given separately in Form 2.

(c) Classes and maximum number of shares

6 (1)(c) Small issuers will most often be incorporated with common shares only, with no special rights or privileges attaching to the share, although there may be restrictions on ownership or transfer (see below). There is no requirement to stipulate the maximum number of shares a CBCA corporation is authorized to issue: it is optional.

(d) Restrictions on ownership or transfer

6 (1)(d) Securities legislation may give substantial advantages to “private companies”, which generally need to restrict the right to transfer shares and limit the number of shareholders.

(e) Number of directors 6 (1)(e) 102 (2)

The articles must set out the minimum and maximum number of directors. Every CBCA corporation requires at least one director, and “distributing corporations” (i.e. public companies) require at least three.

(f) Restrictions on business of company

6 (1)(f)

This is completely unnecessary but can be provided.

When Does a Corporation Begin to Exist? Under the CBCA, the Director (of the CBCA bureaucracy) is required to issue a certificate of incorporation when the

articles of incorporation are received: section 8. Section 9 (“effect of the certificate”) states clearly:

Corporations Introduction to Corporations

20

A corporation comes into existence on the date shown in the certificate of incorporation.

See also: L06 -- 20110926 -- Form 1, Articles of Incorporation

L06 -- 20110926 -- Form 2, Initial Registered Office and First Board of Directors

Pre-Incorporation Contracts (p 24)

PIERCING THE “VEIL” a.k.a. Court Intervention to Extend Liability beyond the Corporate Form

Despite the firmly-entrenched Salomon principle, in extraordinary circumstances courts have proven willing to ignore

the separate legal existence of the corporation and impose liability on controlling shareholders of corporations.

These controlling shareholders may, of course, be natural persons or may themselves be corporations. This process is

sometimes described as “lifting” or “piercing” the corporate veil.

Rough Taxonomy of Reasons The casebook sets out an attempt to categorize the cases where courts have found it appropriate to disregard the

separate legal personhood of a corporation, at p 168. These are:

1. cases that involve allegations of fraudulent conduct or objectionable purposes on the part of a company’s principals;

2. cases where a company existed as a “shell” and was clearly undercapitalized to meet its reasonable financial

needs;

3. cases that involve tort claims against the company, particularly those where a director, shareholder, or

employee has committed an intentional tort, or the tort of inducing breach of contract;

4. cases where the company was not incorporated for bona fide business reasons but for other purposes, often

to avoid taxation;

5. cases that involve non-arm’s-length transactions between parent and subsidiary companies; and

6. cases where the courts determine that equity or the interests of justice are better served by disregarding the

corporate form.

I would personally add a seventh category:

7. cases where the shareholders/directors of “one-man” companies disregard the formalities required under

corporations legislation

The following table attempts to categorize the cases studied according to the above organization.

Case Pierce On

(1)

(2)

(3)

(4)

(5)

(6) (7) Salomon v Salomon & Co, Ltd No Lee v Lee’s Air Farming Ltd No Macaura v Northern Assurance Co Ltd and others No

Introduction to Corporations Corporations

21

Case Pierce On

(1)

(2)

(3)

(4)

(5)

(6) (7) Kosmopoulos v Constitution Insurance Co No*

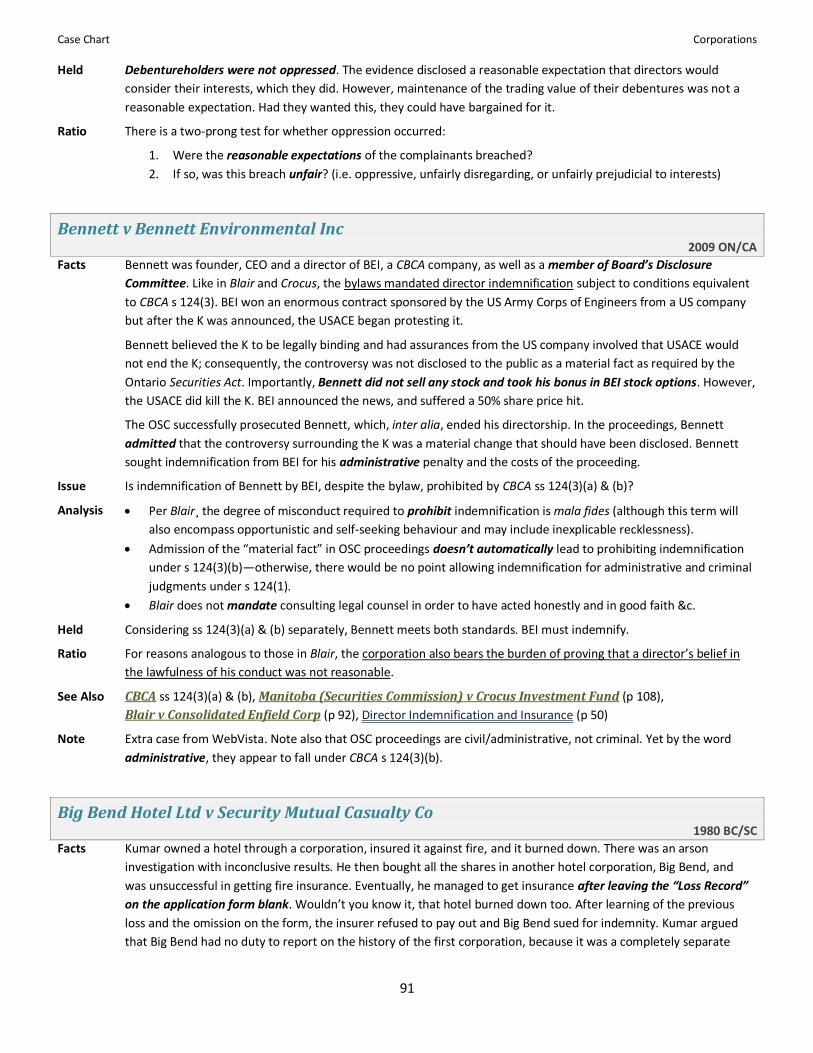

Clarkson Co Ltd v Zhelka No Big Bend Hotel Ltd v Security Mutual Casualty Co Yes

# Individual

Rockwell Developments Ltd v Newtonbrook Plaza Ltd No

642947 Ontario Ltd v Fleischer Yes† Individuals De Salaberry Realties Ltd v Minister of National Revenue Yes Enterprise

Alberta Gas Ethylene Co v Minister of National Revenue No

Gregorio v Intrans-Corp No Walkovszky v Carlton No Wolfe v Moir Yes Individual ‡ AGDA Systems International Ltd v Valcom Ltd No

@ Individuals

*: But Macaura principle overruled #: Not necessary in Big Bend: RD †: Decision pertained to costs only ‡: Formalities not complied with @: Liability was imposed in AGDA, but not as a result of veil-piercing!

When the Veil Won’t Be Pierced RD says that veil lifting is NOT available to give shareholders ownership of the corporation’s assets. Separate legal

personality implies full ownership rights.

Insurable Interests Cases In Macaura v Northern Assurance Co Ltd and others (p 107), the court discussed the moral hazard that arises if

the shareholders are allowed to insure the assets of a corporation. An incentive is created to have the corporation

borrow to buy assets and then destroy the assets, since this screws over the creditors and enriches the shareholders,

who collect on the insurance. In its theoretical reasoning, the House of Lords ignores the fact that Macaura was

virtually the only creditor of Irish Canadian Saw Mills Ltd.

Fast forward to Kosmopoulos v Constitution Insurance Co (p 106). Here, the sole shareholder’s insurable interest arose out of his employment using the assets in question, so that there was no moral hazard (note however that

SCC says it did not lift the veil). According to RD:

1. Macaura wasn’t binding on the SCC. 2. The equities were all on the side of Mr Kosmopoulous since his broker made a mistake; he lost his livelihood;

and he paid the premiums and they were accepted by the insurance company on the basis that everything

was insured, but then the insurers refused to pony up. “The insurance company had no equities on its side”. 3. The problem of multiple shareholders is hard to fit into the Kosmopoulos ratio. For instance, what if one of

five shareholders insures the whole value of the assets himself? Now his insurable interest greatly exceeds

his actual interest. Now there is definitely a moral hazard. RD says maybe…if you just insured your own interest, you could “jam” your claim into the ratio.

Corporations Introduction to Corporations

22

Keep in mind Lord Buckmaster’s reasoning in Macaura as well that the shareholder is only has a residual claim on

distribution of the assets when the corporation is wound up, and it is impossible to calculate how much the

destruction of any given asset reduces this amount.

Fraud and Reasons of Justice The following cases seem to fall under either fraud or reasons of justice:

Case/Statute Juris. P Key Points Clarkson Co Ltd v Zhelka 1967 ON/HC 96 The veil was not pierced, because the wrongs Selkirk’s trustee in bankruptcy was

pleading weren’t wrongs against Selkirk’s personal creditors. Big Bend Hotel Ltd v Security Mutual Casualty Co

1980 BC/SC 91 The court claimed it was piercing the veil, but RD sees this as unnecessary to achieve the result, and I agree.

642947 Ontario Ltd v Fleischer 2001 ON/CA 85 Laskin JA pierced the veil in justifying not awarding costs to Halasi and Krauss, saying that if the injunction they procured had caused damages, they would have been personally liable because they knowingly tendered a worthless undertaking to the court.

Tax Liability The short rule for tax appears to be “your corporate organization will be construed against you for tax purposes”. If it is convenient for the tax collectors to consider your whole group of companies as one enterprise, they will do so. If it

is convenient for them to look at each company in isolation, they will do that. RD seems to confirm this: “when it comes to taxes, you’d better have a good reason for a certain arrangement, better than minimizing tax liability”.

Case/Statute Juris. P Key Points De Salaberry Realties Ltd v Minister of National Revenue

1974 CA/FCA 98 Court argues that it can’t tell what the business of a subsidiary is without considering it in the context of the whole group of companies.

Alberta Gas Ethylene Co v Minister of National Revenue

1989 CA/FCA 88 Court says “one has to ask for what purpose and in what context is the subsidiary being ignored”, en route to refusing to ignore the separate existence of ASCO, the Delaware-incorporated loan conduit.