Organised commodity markets SLBoado

41

1 Leonela Santana-Boado, Co-ordinator, Commodity Exchanges, Special Unit on Commodity, UNCTAD Leonela Santana-Boa do@unctad-org Introduction to Organized Commodity Markets Virtual Institute Study Tour, University of Dar-es-Salaam Geneva, 17 February 2010

Transcript of Organised commodity markets SLBoado

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 1/41

1

Leonela Santana-Boado,

Co-ordinator, Commodity Exchanges,

Special Unit on Commodity, UNCTAD

Leonela Santana-Boado@unctad-org

Introduction to Organized Commodity Markets

Virtual Institute Study Tour, University of Dar-es-Salaam

Geneva, 17 February 2010

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 2/41

Outline of presentation

• The Commodity Economy and the need for

Organized Commodity Markets

• Commodity exchanges: What are they?

• UNCTAD’s role in the area

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 3/41

3

The commodities economy and

poverty: There is a strong link between them

"75 per cent of the 1.2 billion peopleliving on less than $1 a day live and work

in rural areas. Moreover, about half of the

world's hungry people are from

smallholder farming communities,

another 20 per cent are rural landless and

about 10 per cent live in communities

whose livelihoods depend on herding, fishing or forest resources."

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 4/41

• Fragmented markets

• Inadequate infrastructure

• Information asymmetries

• Limited access to affordable credit

• Weak or absent sectoral support institutions• Globalising commodity supply chains with

rising barriers to small producer

participation

Poor rural development

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 5/41

Declining commodity prices

• Real prices have been diminishing over the

long term

• Price fluctuations are large and increasing

• Commodity price instability

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 6/41

Most recently: Domestic

liberalization• Unrealistic expectations

• Impact on farm gate prices is ambiguous

and uncertain

• Absence of functioning markets poses

unacceptable risks for producers

• Private sector has not filled the gap left by

marketing boards and other support systems

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 7/41

Need for organized markets

The liberalisation of agricultural trade and

the withdrawal of government support to

agricultural producers outside the OECD,recent years have seen the rapid creation

and growth of commodity exchanges in

developing countries and countries witheconomies in transition.

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 8/41

Need for organized markets

The former Chicago Board of Trade (CBOT) was

founded in 1848 by a group of Chicago merchants

keen to establish a central marketplace for trade.Before that time, farmers all too often had found

no buyers for the grain they had transported to

Chicago. Given the high transport costs, they had

been left with little choice but to dump the unsoldproduce in the lake.

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 9/41

Organized markets: Commodity

Exchange, What is it?

• “A market in which multiple buyers and sellers trade

commodity -linked contracts on the basis of rules and

procedures laid down by the exchange.”

• This includes: Spot trade for immediate delivery of the

commodity, forward contracts, warehouse receipts trading,

commodity-based futures and options contracts, and trade

facilitation services.

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 10/41

Commodity Exchanges

Over time, virtually all developed countryexchanges moved towards futures trade (a

mechanism for risk transfer), as theirservices in physical trade (spot and forward)became superfluous (most of the exchangesthat were not able to make this change

disappeared; the rare exceptions include theDutch flower auction and a cheeseexchange in the USA

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 11/41

THE WORLD’S MAJOR COMMODITY FUTURES

EXCHANGES

2008 2007

Rank 1 1 New York Mercantile Exchange

(NYMEX, US)

2 3 Dalian Commodity Exchange

(DCE, China)

3 2 Chicago Board of Trade

(CBOT, US)

4 4 ICE Futures

(formerly IPE, UK)

5 9 Zhengzhou Commodity Exchange

(ZCE, China)

6 5 London Metals Exchange

(LME, UK)

7 7 Shanghai Futures Exchange

(SHFE, China)

8 10 Multi Commodity Exchange

(MCX, India)

9 11 New York Board of Trade (NYBOT, US)

10 6 Tokyo Commodity Exchange

(TOCOM, Japan)

11 8 National Commodity & Derivatives Exchange

(NCDEX, India)

12 13 Chicago Mercantile Exchange

(CME, US)

13 12 Tokyo Grain Exchange

(TGE, Japan)

14 15 Euronext.LIFFE (EU)

15 16 Central Japan Commodity

Exchange (C-COM, Japan) 16 17 Kansas City Board of Trade

(KCBT, US)

17 18 Winnipeg Commodity Exchange

(WCE, Canada)

18 19 Bursa Malaysia Derivatives

(BMD, Malaysia)

19 14 National Multi-Commodity

Exchange (NMCE, India)

20 20 JSE/SAFEX

(South Africa)

21 22 Brazilian Mercantile & Futures

Exchange (BM&F, Brazil)

22 21 Minneapolis Grain Exchange (MGEX, US)

Exchange

Rank

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 12/41

THE WORLD’S MAJOR COMMODITY FUTURES

EXCHANGES

BY SECTOR (2008)

0m

150m

300m

450m

600m

750m

N u m b e r o f

c o n t r a c t s ( f u t u r e s & o p t i o n s )

Agriculture 200 313 93 223 64 - 4 6 18 13 8 - 4 - 3 3 0 3 1

Metals 86 - 126 - - 113 70 29 5 - - 5 - - - - 0 - -

Energy 339 - 62 - 153 - 21 6 1 - - - - - - - 3 - -

CME

GroupDCE SHFE ZCE

ICE

FuturesLME MCX TOCOM NCDEX

NYSE

EuronextTGE TAIFEX KCBT NMCE BMD

BM&F

BovespaC-COM

JSE/SAF

EXMGEX

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 13/41

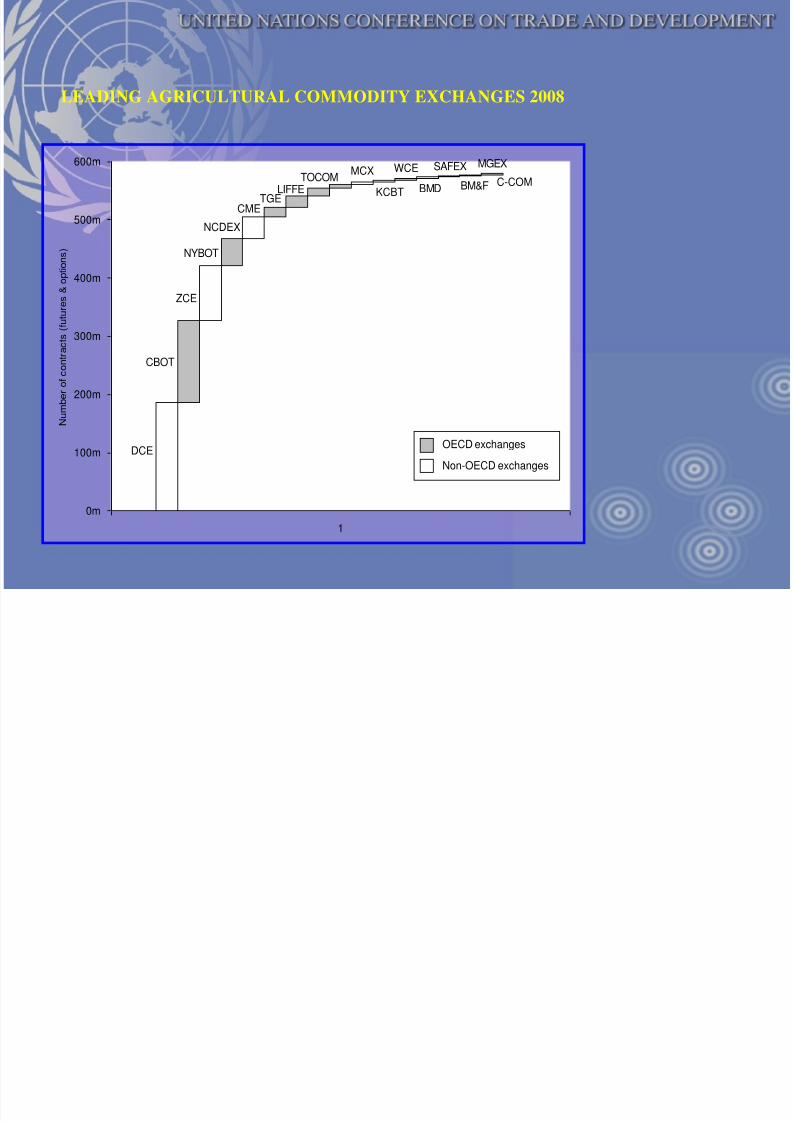

LEADING AGRICULTURAL COMMODITY EXCHANGES 2008

DCE

CBOT

ZCE

NYBOT

NCDEX

CMETGE

LIFFETOCOM

MCX

KCBT

WCE

BMD

SAFEX

BM&F

MGEX

C-COM

0m

100m

200m

300m

400m

500m

600m

1

N u

m b e r o f c o n t r a c t s ( f u t u r e s & o p

t i o n s )

OECD exchanges

Non-OECD exchanges

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 14/41

PRINCIPAL CONTRACTS OF THE MAJOR COMMODITY

EXCHANGES (2008)

4 0 m

3 7 m

2 8 m

2 0 m1 9 m

1 7 m1 3 m

1 1 m 1 1 m

0

10

20

30

40

50

D C E N o

. 1 s o y b e

a n

D C E

s o y b e a n

m e a l

C B O T c

o r n

C B O T

s o y b e a

n s

N C D E X g u a r s e

e d

Z C E s t r o n g

g l u t e n w h e

a t

N Y B O T s u g a r

1 1

T G E N o n - G M O s o y b e a n

s

Z C E c o t t o n

n o . 1

N u m b e r o f

f u t u r e s & o p t i o n s c o n t r a c t s ,

m i l l i o n s

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 15/41

MAIN GRAINS TRADED IN THE MAJOR

COMMODITY EXCHANGES IN THE WORLD

Dalian Commodity Exchange rice, corn, soyabeans

(DCE, China)

Chicago Board of Trade corn, soyabeans

(CBOT, US) wheat, rice

Zhengzhou Commodity Exchange wheat

(ZCE, China)

Multi Commodity Exchange cereals (maize)

(MCX, India)

New York Board of Trade wheat, barley

(NYBOT, US)

National Commodity & Derivatives Exchange rice

(NCDEX, India)

Tokyo Grain Exchange corn, soyabeans

(TGE, Japan) red beans

Euronext.LIFFE (EU) wheat, corns

Kansas City Board of Trade wheat

(KCBT, US)

Winnipeg Commodity Exchange wheat, barley

(WCE, Canada)

JSE/SAFEX maize, wheat,

(South Africa) soyabeans

Brazilian Mercantile & Futures corn, soyabeans

Exchange (BM&F, Brazil)

Minneapolis Grain Exchange wheat, corn,(MGEX, US) soyabeans

Exchange Main grains

Traded

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 16/41

Commodity Exchanges

In the developing world, a commodity exchange may actin a broader range of ways to stimulate trade in thecommodity sector. This may be through the use of

instruments other than futures, such as the cash or 'spot'trade for immediate delivery, forward contracts on thebasis of warehouse receipts or the trade of farmers'repurchase agreements, or 'repos'. Alternatively, it maybe through focusing on facilitative activities rather than

on the trade itself, as in Turkey where exchanges haveserved as a centre for registering transactions for taxpurposes.

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 17/41

EXCHANGES IN AFRICA:

The SAFEX Agricultural Products Division of the JSE Exchange, SouthAfrica is the continent’s only commodity futures exchange, and the onlycommodity exchange in Africa that has truly withstood the test of time.

OTHER EXCHANGES IN AFRICA

• MACE (Malawi); The Malawi Agricultural Commodity Exchange

• KACE (Kenya); The Kenya Agricultural Commodity Exchange

• UCE (Uganda); The Ugandan Commodities Exchange

• ECEX (Ethiopia); Ethiopia Commodity Exchange

• ZAMACE (Zambia); The Zambia Agricultural Commodity Exchange

• ASCE (Nigeria); Abuja Securities and Commodity Exchange• Ghanaian Commodities Exchange- in project

• ACE (regional, based in Malawi);

• Bourse Africa (Regional)

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 18/41

Bourse Africa

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 19/4119

AACP: An introduction

• The All ACP Agricultural Commodities Programme (AACP) is a jointproject involving: – the European Union (EU)

– the African, Caribbean and Pacific secretariat (ACP)

– five international organisations (IOs): UNCTAD, CFC, ITC, FAO and theWorld Bank

• A budget of €45 million has been set aside for actions by the IOs toaddress ACP stakeholders’ needs

• The Programme’s actions will be demand-driven, arising fromparticipatory consultative processes to ensure ownership by ACPstakeholders (national and regional)

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 20/4120

Potential benefits for developing countries

Market creation

Stimulating regional inte-

gration & South-South trade

Price discovery

Price risk management

Infrastructure enhancement

Market access

Facilitate provision of

finance

Price transparency

Reduced counterparty risk

Quality assurance/upgrade

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 21/4121

Caveat: Benefits do not automatically

flow from the establishment of acommodity exchange

• A domestic commodity exchange is not necessarily an appropriate policy

instrument for all markets and all commodities.

• An exchange is only one part of the policy framework – it is not a panacea and

it does not stand alone from other commodity policy interventions

• An exchange which is badly-structured or poorly-managed is unlikely to

deliver enhancements to underlying commodity sectors.

• The extent to which prospective enhancements are delivered in large part

depend on the services offered and the strategic priorities pursued by the

exchange.

• A well-functioning commodity exchange is predicated upon a robust legal-regulatory

framework

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 22/4122

UNCTAD and Commodity Exchanges

• UNCTAD is the major international organization supportingcommodity exchange development: 15 years of hands-on support

• Aims to: promote understanding; facilitate sharing of experiences,perspectives and ideas; enhance developing country capacity andexpertise; ensure viability and sustainability of exchange initiatives

• Expertise is concentrated in two areas:

– Direct technical assistance and advice, with involvement in theDominican Republic, Ghana, Kazakhstan, India, Indonesia, Malaysia,Nigeria, Russia, Sri Lanka, Turkey and Ukraine, as well as a regional

exchange for Africa – Awareness-raising through publications, presentations and the

organization of conferences

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 23/41

Commodity exchanges development: What

can UNCTAD do?

• To assess the relevance of existing commodity exchanges initiatives and

identify if it could be an appropriate solution and how to make themmore efficient and useful for farmers

• To scan and analyze the conditions depending on the type of CommodityExchange (physical commodity exchange, commodity futures exchanges,etc.);

• Creating a new commodity exchange is no easy matter – how is it to beorganized, what contracts are to be traded (UNCTAD has done severalfeasibility studies), what are the possibilities with respect to tradingplatforms, how does one target potential users, what types of regulationare required.

Exchange creation and

growth

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 24/41

What can UNCTAD do?

• UNCTAD is ideally placed to overcome the trust gap that oftenstill exists between the public and private sectors in developingcountries and which hinders investments in trade-relatedinstitutions.

• Identify the components of the legal-regulatory frameworksrequired for the functioning of different types of servicesprovided by a commodity exchange (rules, taxation)

A public-private

orientation

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 25/41

What can UNCTAD do?

• Organize Capacity building and training programmes that

addresses the needs of the various stakeholders;

• Visit to sucessfull Exchanges both inside and outside the region;

Bridging the

information gap

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 26/41

What can UNCTAD do?

Warehouses

Nationalexchangestied into apan-Africannetwork

Exchange of

Innovative ideas:

Regional Dimension

Creation of regional linkages

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 27/41

27

UNCTAD Analysis, 2009 – A Study of

Development Impacts of Commodity Exchanges

in Developing Countries• Aim: To identify, analyse and assess the impacts made by commodity futures exchanges

in developing countries on economic growth, development and poverty reduction, with

particular focus on agriculture

• Study undertaken in collaboration with leading exchanges in Brazil, China, India,Malaysia and South Africa

• Verified 66 positive impacts that commodity exchanges have made in the following

areas: price discovery, price risk management, venue for investment, facilitation of

physical trade, facilitation of finance and general market development

• Also identified versatility of exchanges across different contexts and in response todifferent challenges – existing and emerging – including in a context of smallholder

farming

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 28/41

28

Aim and Objectives

• Aim:

To identify, analyse and assess the impacts made by commodityexchanges in developing countries on development, poverty reductionand economic growth, with particular focus on the agricultural sector

and farmers

• Objectives: – Awareness-raising among governments and sector stakeholders

– Knowledge development about the impacts of agricultural commodityexchanges

– Best practice identification and promotion – Demonstrate worldwide applicability where it exists

– Exchange of information, experience and perspectives

– Network-building among South-based exchanges

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 29/41

29

Scope

• Commodity futures exchanges have been selected as the focus of thestudy because they tend to be the most sophisticated adaptation of acommodity exchange

– The array of impacts generated is potentially the broadest

– A commodity exchange that offers other services but not futurestrading is likely to generate impacts that feature only a sub-set of those generated by commodity futures exchanges

• However, this selection does not imply:_

– that a commodity futures exchange is always the appropriate form

of exchange to be established in every market or for everycommodity

– that every commodity futures market always in reality generates awider array of impacts than other forms of commodity exchange

– that a commodity futures exchange will always generate the samerange of impacts as those identified in this study

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 30/41

30

Approach

• Country case studies - a comparative review of agriculturalfutures exchanges in five key developing economies:

– Under what conditions they have emerged

– The factors that have driven their ongoing development

• Impact assessment research methodology:

– Designing a framework for analysing 81 potential developmentimpacts arising from agricultural futures contracts and supporting

services offered by commodity exchanges participating in theStudy Group

– Conducting an empirical investigation into these 81 impacthypotheses in each of the featured countries

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 31/41

31

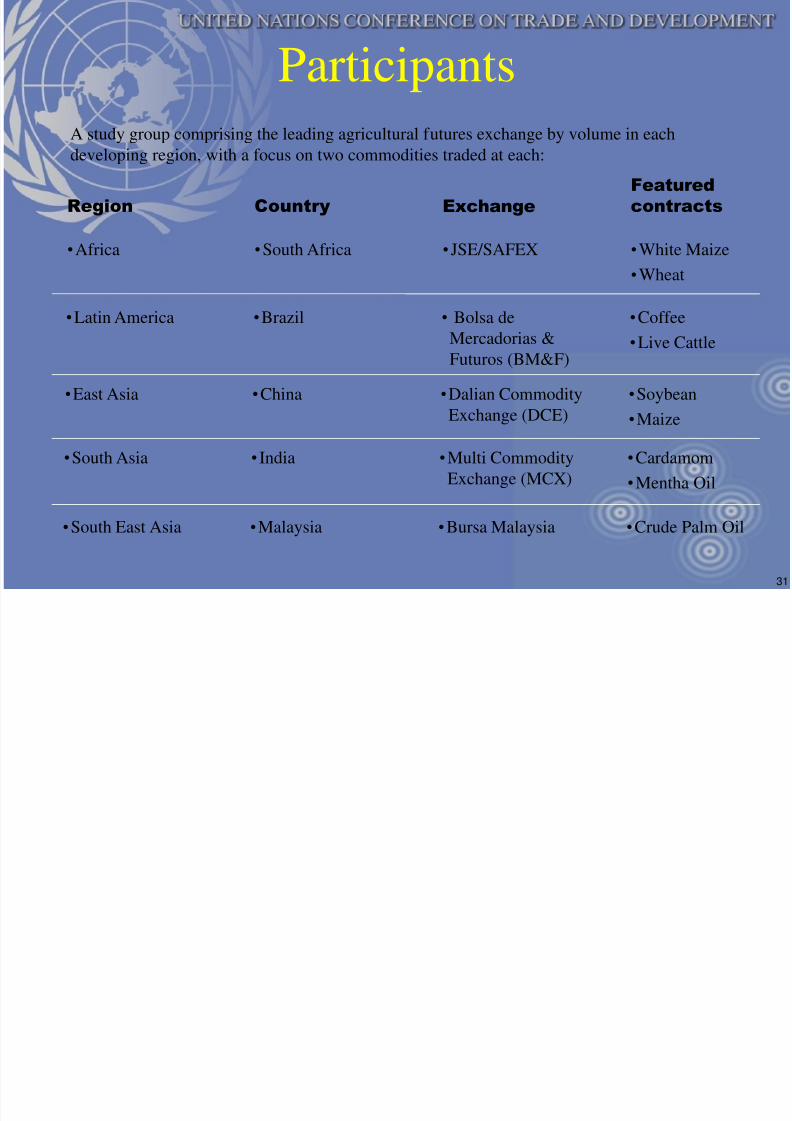

Participants

•Africa •South Africa •JSE/SAFEX •White Maize

•Wheat

Country Region Exchange

Featured

contracts

•Latin America •Brazil • Bolsa de

Mercadorias &

Futuros (BM&F)

•Coffee

•Live Cattle

•East Asia •China •Dalian Commodity

Exchange (DCE)

•Soybean

•Maize

•South Asia • India •Multi Commodity

Exchange (MCX)

•Cardamom

•Mentha Oil

•South East Asia •Malaysia •Bursa Malaysia •Crude Palm Oil

A study group comprising the leading agricultural futures exchange by volume in eachdeveloping region, with a focus on two commodities traded at each:

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 32/41

32

Impact framework (1)

Price discoveryPrice risk

managementInvestment

venue

More efficient priceformation

Wider supply ofmore accurate

information

Effective transfer ofprice risk

Improvedinvestmentenvironment

Core functions

14 hypotheses 8 hypotheses 14 hypotheses

Exchange functions

Benefits arising

Impacts on beneficiaries1

(81 in total)

1 Impact hypotheses are further split into potential impacts specifically or mainly for farmers (37) and potential impacts for the wider commodity sector or theoverall economy (44); and potentially positive impacts (76) and potentially negative impacts (5). The full list of impacts can be found in the working paper

version of the study, available at: www.unctad.org/commodities

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 33/41

33

Impact framework (2)

Exchange functions Facilitation ofphysical trade

Marketdevelopment

Facilitation offinancing

Improved spotreference price

generation

Reinforce cash markettransactions

Enhances storage &logistics infra-

structure

Upgrades qualitystandards

Education & capacity-building

International tradefacilitation

Technology upgrade& promotion

Industry growth

Enables bank lending& other modes of

financing

Wider functions

18 hypotheses 9 hypotheses 18 hypotheses

Benefits arising

Impacts on beneficiaries1

(81 in total)

1 Impact hypotheses are further split into potential impacts specifically or mainly for farmers (37) and potential impacts for the wider commodity sector or the

overall economy (44); and potentially positive impacts (76) and potentially negative impacts (5). The full list of impacts can be found in the working paper

version of the study, available at: www.unctad.org/commodities

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 34/41

34

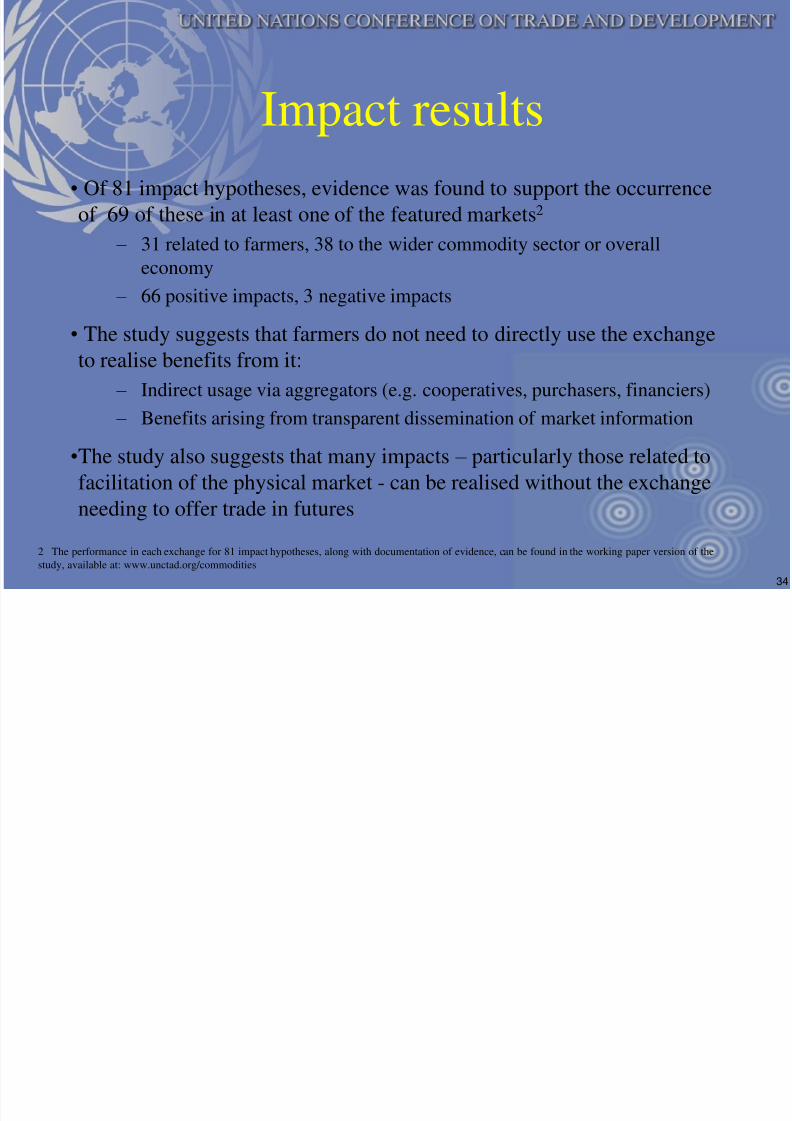

Impact results

• Of 81 impact hypotheses, evidence was found to support the occurrence

of 69 of these in at least one of the featured markets2

– 31 related to farmers, 38 to the wider commodity sector or overall

economy

– 66 positive impacts, 3 negative impacts

• The study suggests that farmers do not need to directly use the exchange

to realise benefits from it:

– Indirect usage via aggregators (e.g. cooperatives, purchasers, financiers)

– Benefits arising from transparent dissemination of market information

•The study also suggests that many impacts – particularly those related to

facilitation of the physical market - can be realised without the exchange

needing to offer trade in futures

2 The performance in each exchange for 81 impact hypotheses, along with documentation of evidence, can be found in the working paper version of the

study, available at: www.unctad.org/commodities

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 35/41

35

Bolsa de Mercadorias & Futuros,

Brazil (BM&F)Context

• Continuous commodity trading in Brazil since

early 20th century

• The exchange’s room for action squeezed by

varying levels of government intervention

• Agro-liberalisation and deregulation in the

1980s, and increased export orientation

Development impacts

• Distributed across core and wider functions

• Hedging and price discovery are prominent• The BM&F subsidiary, “Brazilian Commodity

Exchange” has integrated national cash markets

and enables financing and export promotion

possibilities for agro-participants

Key achievements

• Providing services that have supported the

commercialization of the agro-economy

e.g. enabling flow of capital into the sector;

enhancing efficiency and transparency of

government support; integrating the domestic

physical market; facilitating export markets

Relevance to smallholders

• BM&F mechanisms used by Government to

support smallholders schemes e.g. auctions tosupport government procurement; channeling

finance to smallholders and providing a

secondary market

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 36/41

36

Dalian Commodity Exchange, China

(DCE)Context

• Established during economic reform period as

Government looked to build market institutions

• The exchange as a mechanism to support

moves towards framework for market pricing

and market opening

Development impacts

• Focused primarily on core price discovery and

price risk management functions• Important emphasis also on capacity-building

for farmers to use market information

• Financing functionalities are nascent but have

strong growth potential

Key achievement

• Creating high levels of liquidity for key agro-

commodities

e.g. generated significant trading volumes in

strategic commodities; enhanced market

functioning; adapted to emerging dynamics in

important markets - liberalisation, GMO

Relevance to smallholders

Major training and capacity-building execerise

by DCE to help smallholders improve croppingand marketing decisions with market

information

DCE encourages downstream partners to pass

on hedging benefits to smallholders

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 37/41

37

Multi Commodity Exchange, India

(MCX)Context

• Heavy government intervention, including

prohibition on futures trading until 1980s

• Three national multi-commodity exchanges a

key element of Government plan to upgradefragmented and infrastructure-deficient

commodity markets

Development impacts

• Distributed across core and wider functions

• Price discovery and dissemination a key impact• Impacts arising from facilitation of physical

market and market development have been

high

Key achievement

• Catalyzing development of the wider

commodity ecosystem

i.e. as well as price risk management, has also

improved the flow of information, facilitatedphysical infrastructure development,

established reliable quality standards

Relevance to smallholdersHigh expectation for direct farmer participation

Current usage is low, but high impacts frominformation & physical market development

Indirect participation of small farmers via co-

operatives

Regulatory obstacles

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 38/41

India can lead the way in integrating farmers into national

and international market places using modern information

and communications technologies

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 39/41

39

Bursa Malaysia

Context

• Established in 1980 on the back of a well-

developed and strongly-regulated physical

market for crude palm oil

• The consummation of the Government’sdiversification strategy, originating in the early

1960s

Development impacts

• Mainly arising from core functions

• Price discovery and price risk management forworld palm oil industry

Key achievement

• Bringing pricing power to Malaysia for its key

export commodity

i.e. unique in establishing a benchmark

exchange in the developing world, ensuringpricing power for its key export commodity on

the world market.

Relevance to smallholders

• No observed smallholder focus - development

impact has been elsewhere• Many smallholders operates within government

support schemes

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 40/41

40

JSE/SAFEX, South Africa

Context

• Heavy government intervention in the agro-

markets until political transition brought on by

the demise of the apartheid regime

• Root-to-branch liberalisation in mid-1990sentrenched market pricing and an open,

unprotected and volatile grain sector

Development impacts

• Distributed across core and wider functions

• Price discovery and risk management key insupporting sector performance despite high

levels of price and production volatility

• High impact in enabling financing and

facilitating physical market development

Key achievement

• Filling the void left by sudden government

deregulation of the markets

i.e. has become a core institution in the

deregulated South African grain markets, forthe conduct of hedging, financing and cash

transactions

Relevance to smallholders

JSE/SAFEX supports smallholder capacity-

building programmes in partnership with otheragencies

Indirect usage of the exchange's market

information has been encouraged.

8/4/2019 Organised commodity markets SLBoado

http://slidepdf.com/reader/full/organised-commodity-markets-slboado 41/41

Conclusions

Exchanges are versatile instruments, capable of upgradingcommodity sector performance in a range of situations andaddressing emerging challenges as they arise

In general, exchange services are relevant for smallholders however, price risk management is not always an important - or

even relevant service - for smallholders compared with priceinformation and physical market services

The exchange is not a panacea, and has depended on anappropriate regulatory environment and other complimentary

policies and mechanisms