ORGANISATION OF CONSULTANCY SERVICES -...

31

Chapter - 4 ORGANISATION OF CONSULTANCY SERVICES A well-conceived internal organisation design is absolutely necessary for achieving organisational objectives and delivering quality services to clients. Against this backdrop an indepth analysis is made of the socio-economic conditions of consultancy service firms in Kerala which would give an insight into the strengths and weaknesses of these firms. 4.1 Nature of Organisation - A consultancy organisation exists for making profits, achieving growth - by excelling competition and adding value to-- the clients. It may be organised like any other business as sole proprietorship, partnership, private limited company or public limited company. Table T2 shows the nature of organisation of consultancy services: Table T2 Nature of Consultancy Organisations Source : Research Data Nature of Organisation Sole Proprietorship Partnership Private Limited Company Public Limited Company Total No. of firms 78 38 69 15 200 Percentage 39 19 34.5 7.5 100

Transcript of ORGANISATION OF CONSULTANCY SERVICES -...

Chapter - 4

ORGANISATION OF CONSULTANCY SERVICES

A well-conceived internal organisation design is absolutely necessary

for achieving organisational objectives and delivering quality services to clients.

Against this backdrop a n indepth analysis is made of the socio-economic

conditions of consultancy service firms in Kerala which would give an insight

into the strengths and weaknesses of these firms.

4.1 Nature of Organisation

- A consultancy organisation exists for making profits, achieving growth -

by excelling competition and adding value to-- the clients. It may be organised

like any other business as sole proprietorship, partnership, private limited

company or public limited company. Table T2 shows the nature of organisation

of consultancy services:

Table T2

Nature of Consultancy Organisations

Source : Research Data

Nature of Organisation

Sole Proprietorship

Partnership

Private Limited Company

Public Limited Company

Total

No. of firms

78

38

69

15

200

Percentage

39

19

34.5

7.5

100

The table reveals that out of 200 consultancy firms studied, 78 firms

(39 per cent) are organised as sole proprietorship, 69 firms (34.5 per cent) are

private limited companies, 38 firms (19 per cent) are partnerships and the

remaining 15 firms (7.5 per cent) are public limited companies. It is evident

that sole proprietorship is the dominant form of organisation for consultancy

services. This is because of the fact that most of the consultancy firms are

organised on a small scale basis and they prefer to be self-employed. Architects,

tax consultants, engineering and project consultants mainly organise their

services as sole proprietorship. However, a good number of consultancy firms,

for example, software and human resources consultancy firms are now organised

as private limited companies.

Public Limited Company

7.5%

Private Limited M e Proprietorship

company 39.0%

34.5%

Partnership 1 9. P/o

Soie Proprietorship

I Private Lktlited Ccmpny

Fig. F8 Nature of Consultancy Organisations

4.2 Age of Consultancy Organisation

Table T3 shows the distribution of consultancy firms on the basis of

the number of years of their existence since their inception.

Table T3

Age of Consultancy Organisations

Source : Research Data

Age in Years

Less than 5 years

Between 5 and 10 years

Above 10 years

Total

The study reveals that the majority of the consultancy firms

(68.5 per cent) have been in existence for less than ten years. The average age

No. of firms

57

80

63

200

of consultancy firms is approximately 7.65 years. Therefore, it is concluded

Percentage

28.5 .

40

31.5

100

that organised consultancy services in the State are of recent origin and are still

in their developing stage. It is realised that it is only of late that the economic

scenario became more complex and diversified in the State of Kerala and

clients felt the need for expert advice on their business matters.

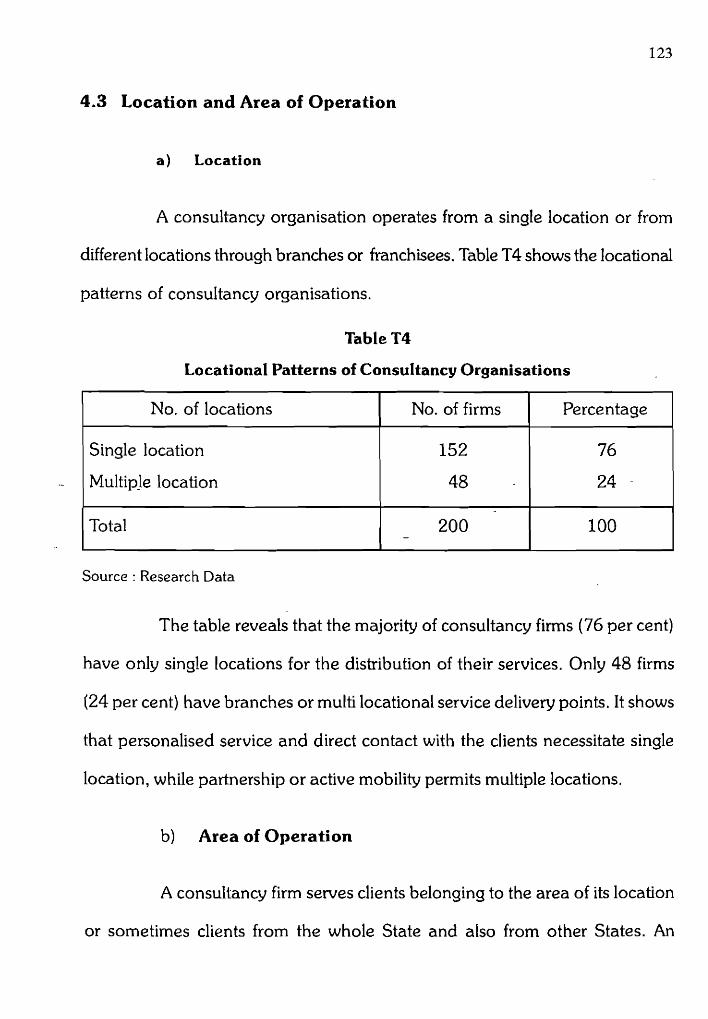

4.3 Location and Area of Operation

a) Location

A consultancy organisation operates from a single location or from

different locations through branches or franchisees. Table T4 shows the locational

patterns of consultancy organisations.

Table T4

Locational Patterns of Consultancy Organisations

Source : Research Data

No. of locations

Single location

Multiple location

Total

The table reveals that the majority of consultancy firms (76 per cent)

have only single locations for the distribution of their services. Only 48 firms

(24 per cent) have branches or multi locational service delivery points. It shows

that personalised service and direct contact with the clients necessitate single

location, while partnership or active mobility permits multiple locations.

b) Area of Operation

No. of firms

152

48

200 -

A consultancy firm serves clients belonging to the area of its location

or sometimes clients from the whole State and also from other States. An

Percentage

76

24 -

100

analysis of the nature of area of operation of consultancy firms is presented in

Table T5.

Table T5

Area of Operation of Consultancy Organisations

Within the District

Within the State

Outside the State also

-

Source : Research Data

,-

~ h e table shows that the majority of the consultancy firms

(84 per cent) serve clients belonging to the same District or State in which they

are located. It indicates the regional nature of the area of operation. Only 32

firms (16 per cent) have operations outside the State and few respondents,

most of them software consultancy firms, have clients from overseas. It reveals

that consultancy firms mainly focus on satisfying the needs of local clients,

thereby ensuring quality of services.

4.4 Areas of Consultancy Sewices

The areas of consultancy services are vast and wide. These are

grouped under eight broad categories for the purpose of the study. Many

125

consultancy organisations offer more than one line of consultancy services.

Management consultants simultaneously offer tax consultancy, investment

consultancy, project consultancy etc. Similarly some software consultancy firms

also carry out computer training and education. Therefore, consultancy firms

are classified on the basis of their important service in the service product line.

Table T6 gives the composition of respondents from different areas of consultancy

services.

Table T6

Distribution of Consultancy firms based on Nature of Consultancy Services

Source : Research Data

Area of Consultancy Services -

Management Consultancy

Investment Consultancy

ProjectIEngineering Consultancy

Software Consultancy

Employment/Educational Consultancy

Architechts / Interior Design Consultancy

Tax Consultancy

Others

Total

No. of firms

48

2 0

32

24

14

30

24

8

200

Percentage

24 -

10

16

12

7

15

12

4

100

The table reveals that management consultancy, projecvengineering

consultancy and architecture /interior design consultancy together come to

55 per cent of the total consultancy services in the State. This shows that these

three are the major consultancy services commonly practiced in the State. Of

these management consultancy occupies 24 per cent of the total consultancy

services. This is owing to the fact that it is an area having wider scope of

services like organisational restructuring, capital reorganisation, financial

collaboration, amalgamation, takeovers, rehabilitation, cost management,

quahty control, marketing research, protection of patent rights and trade marks etc.

The table also indicates that other consultancy services like investment --

consultancy, software consultancy and tax consultancy are also actively

- practised in the Sate since they share 34 per cent of the total consultancy

services in the State.

The category of 'others' in the table includes consultancies in the

areas of event management, travel and tourism, advertising and immigration

services.

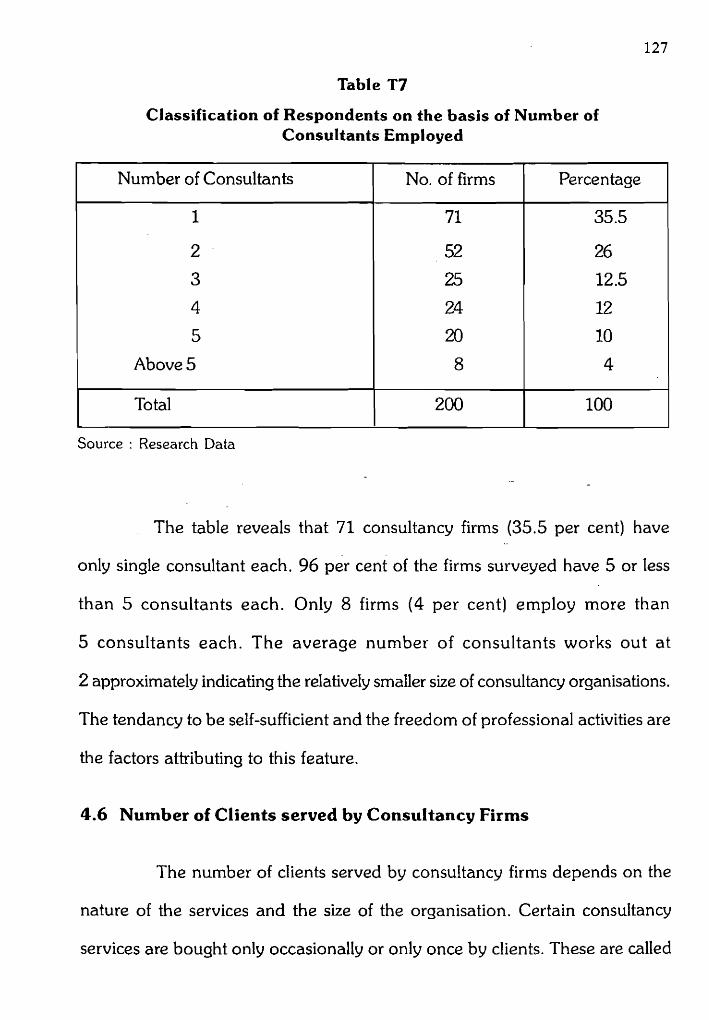

4.5 Number of Consultants Employed

Table T7 shows the number of consultants employed by consultancy

organisations.

Table T7

Classification of Respondents on the basis of Number of Consultants Employed

Source : Research Data

Number of Consultants

1

2

3

4

5

Above 5

Total

- The table reveals that 71 consultancy firms (35.5 per cent) have

only single consultant each. 96 per cent of the firms surveyed have 5 or less

than 5 consultants each. Only 8 firms (4 per cent) employ more than

5 consultants each. The average number of consultants works out at

2 approximately indicating the relatively smaller size of consultancy organisations.

The tendancy to be self-sufficient and the freedom of professional activities are

the factors attributing to this feature.

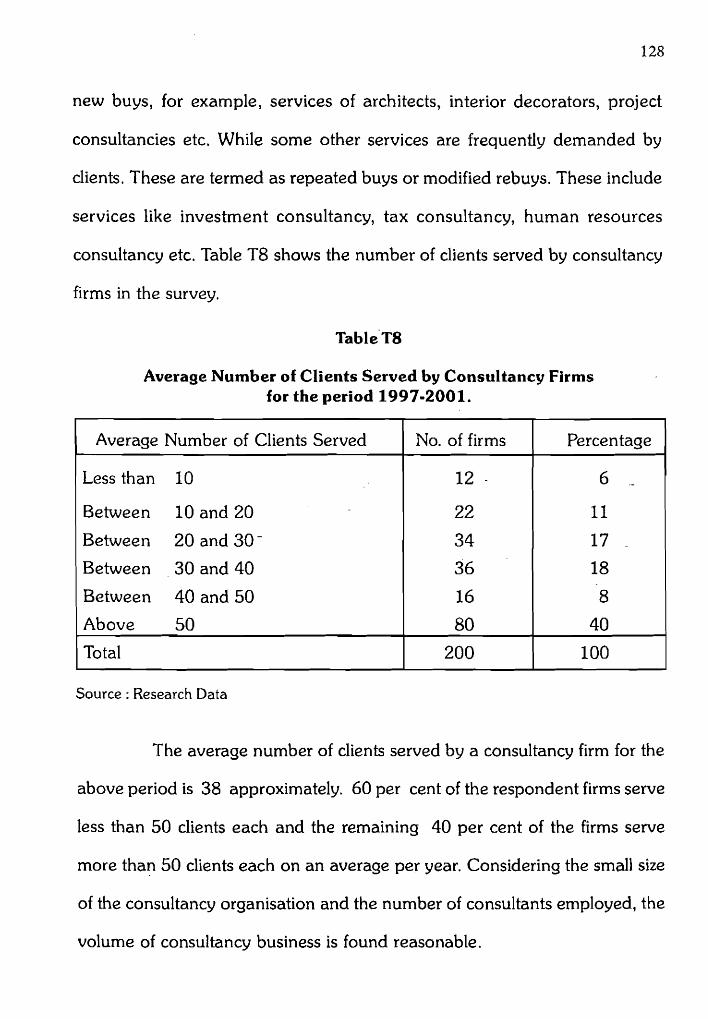

4.6 Number of Clients served by Consultancy Firms

No. of firms

71

52

25

24

20 8

The number of clients served by consultancy firms depends on the

nature of the services and the size of the organisation. Certain consultancy

services are bought only occasionally or only once by clients. These are called

Percentage

35.5

26

12.5

12

10

4

F I 200 100

new buys, for example, services of architects, interior decorators, project

consultancies etc. While some other services are frequently demanded by

clients. These are termed as repeated buys or modified rebuys. These include

services like investment consultancy, tax consultancy, human resources

consultancy etc. Table T8 shows the number of clients served by consultancy

firms in the survey.

Table T8

Average Number of Clients Served by Consultancy Firms for the period 1997=2001.

Source : Research Data

Average Number of Clients Served

Less than 10

Between 10 and 20

Between 20 and 30-

Between 3 0 and 40

Between 40 and 50

Above 50

Total

The average number of clients served by a consultancy firm for the

above period is 38 approximately. 60 per cent of the respondent firms serve

less than 50 clients each and the remaining 40 per cent of the firms serve

more than 50 clients each on an average per year. Considering the small size

of the consultancy organisation and the number of consultants employed, the

volume of consultancy business is found reasonable.

No. of firms

12 -

22

34

36

16

80

200

Percentage

6 .-

11

17 ..

18

8

40

100

4.7 Capital Investment in Consultancy Firms

Table T9 gives the classification of consultancy firms on the basis of

capital investments as on the date of the survey.

Table T9

Capital investment in Consultancy Firms

Source : Research Data -

Investments (Rs. in lakhs)

Less than 2

Between 2 and 5

Between 5 and 10

Above 10

Total -

The average investment (median) in consultancy firm is

approximately Rs. 4.46 lakhs. It indicates the relatively low investment required

by consultancy organisations.

It is found in the study that capital investment in consultancy service

firms includes cost of office building, equipments, furniture and other

infrastructure for delivering the services. Capital investment again depends on

the nature of services offered and the size of operation. Consultancy

organisations like that of tax consultants, architects, placement services etc.

require as little investpent as Rs. 50,000 or so. There are also firms having

investment ranging into crores of rupees in the consultancy services.

No, of firms

45

67

42

46

200

Percentage

22.5

33.5

21

23 100

4.8 Number of Employees in the Organisation

Consultancy services are highly people-oriented. There is high degree

of personal contact in the service delivery process. Table TI0 shows the number

of persons employed in consultancy organisation as on the date of the

survey.

Table TI0

Table Showing Number of Employees in Consultancy Organisations

Source : Research Data

Number of Employees

Less than 5

Between 5 and 10

Between 10-and 15 -

Between 15 and 20

20 and above

Total

The table reveals that out of 200 firms studied 79 firms (39.5 per

cent) have less than 5 employees in their organisations. 84.5 per cent of the

consultancy firms have less than 20 employees in their organisations. The

average number of persons employed is approximately 10. This clearly indicates

the lean structure of consultancy organisations. The number of service personnel

employed is low on account of the small size of consultancy firms.

No. of firms

79

45

20

25

31

200

Percentage

39.5

22.5

10

12.5

15.5

100

4.9 Revenue Earned by Consultancy Organisations

Fees charged from clients for consultancy services constitute- the

source of revenue of consultancy firms. Income from sale of products supporting

the services and also from other lines of services are not considered under

revenue. Table TI 1 gives the average revenue earned by consultancy firms

for the period 1997-2001.

Table TI1

Average Revenue Earned by Consultancy Organisations

Source : Research Data

Average Revenue (Rs. in lakhs)

Less than 5 - -

Between 5 and 10

Between 10 and 15

Between 15 and 20

20 and above

Total

The average revenue earned by a consultancy organisation for the

above period is Rs. 9,70,000. 34 per cent of the firms are earning revenue

below Rs. 5 lakhs and 60 per cent of the firms are earning revenue below

Rs.10 lakhs. It is realised that the present revenue earned by the consultancy

firms under survey are sufficient to recover fully all the costs of operations,

leaving a reasonable amount of surplus.

No. of firms

- 68

52

30

24

26

200

Percentage

34

26

15

12

13

100

4.10 Factors Contributing to the Growth of Consultancy Services

Several factors contribute to the growth of consultancy services.

Sophistication in human life, complexities of modern business, increasing

opportunities, changes in economic/technological environment are the

important factors contributing to the development of consultancy services.

The respondents evaluation of these factors is presented in Table T12.

Factors Contributing to the Growth of Consultancy Services

Source : Research Data

Total

200

200

200

200

Factors

Sophistication in human life

Complexities of problems

Increasing opportunities

Environmental/ Technologica. changes

Total

No. of Respondents

Ran king I

30

141

18

I1

200

11

135 ..

19

6

40

200

- III.

15

30

124

31

200

- IV

20

10

52

118

200

Table T12A

Ranking of the Factors Contributing to the Growth of Consultancy Services

Source : Research Data

Factors

Sophistication in human life

Complexities of problems

Increasing opportunities

Environmental/ Technological changes

Complexities of problems is stated as the most important reason for

the growth of consultancy services in the study. Out of 200 respondents 141.

Mean Score

2.875

3.455

1.95

1.72

(70.5 per cent) consider it as the most important. 30 respondents (15 per cent) --

consider sophistication in human life as the most important reason, 18 ,

Rank

I1

i

111

IV

respondents (9 per cent) consider increasing opportunities as the most important

reason, while 11 firms (5.5 per cent) say that environmental/ technological

changes as the most important reason contributing to the growth of consultancy

services.

The second important reason is sophistication in human life. 135

respondents (67.5 per cent) consider it as the second important reason for the

growth of consultancy services.

124 respondents (62 per cent) consider increasing opportunities in

education, employment, business or profession as the third important reason

for the growth of consultancy services.

Environmental/technological changes is considered as the fourth

important factor by 118 respondents (59 per cent).

4.11 Extent of Competition in Consultancy Services

Competition in consultancy services leads to better quality of service

and wider choice to clients. Table TI3 shows the opinion of respondents

regarding the nature and extent of competition in consultancy services.

Table T13

Extent of Competition in Consultancy Services

Source : Research Data

All the respondents agree that there is competition in the field of

consultancy services. 42.5 per cent of the respondents state that there is severe

competition, 35.5 per cent are of opinion that the competition is moderate and

the remaining 22 per cent state that there is only limited competition in the

field of consultancy services. It is noted that it is the increase in the number of

consultancy organisations that has resulted in severe competition. It is inferred

Percentage

42.5

35.5

22 .O

0

100

Extent of Competition

Severe competition .-

Moderate competition

Limited competition

No competition at all

Total

No. of firms

85

71

44

Nil

200

that the high degree of competition calls for high professionalism and greater

efficiency on the part of the consultants in order to survive successfully in their

field.

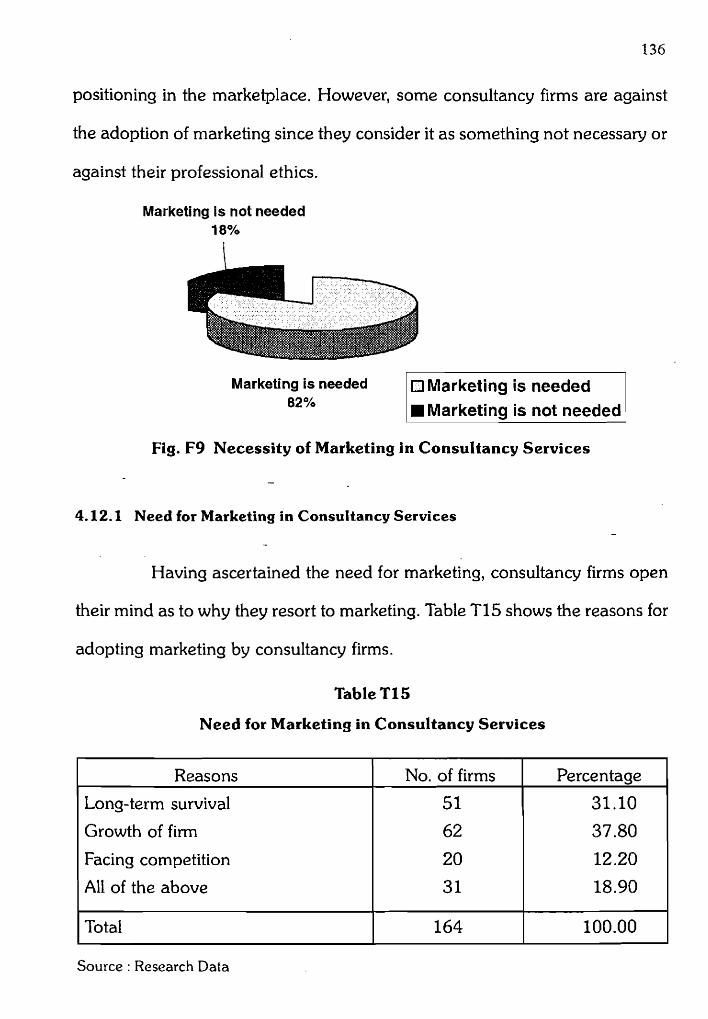

4.12 Acceptance of Marketing Principles by Consultancy Organisations

It is a pertinent question to be analysed in detail whether there is a

need for applying marketing principles to consultancy services. Table TI4

shows attitudes of respondents towards adopting marketing principles for their

consultancy services.

Table TI4

Attitudes of Consultancy Firms towards adopting Marketing

Source : Research Data

The table reveals that most of the consulting firms (82 per cent)

recognise the need for adopting marketing in consultancy services. It indicates

that consultancy firms are generally proactive to marketing because of the

multifarious benefits it offers to them. It is seen that marketing is now increasingly

being applied by many consultancy firms for excelling competition and better

Percentage

82

18

100

Particulars

Marketing is needed

Marketing is not needed

Total

No. of firms

164

36

200

positioning in the marketplace. However, some consultancy firms are against

the adoption of marketing since they consider it as something not necessary or

against their professional ethics.

Marketing is not needed 18%

I

Marketing is needed 1 Marketing is needed I 82% 1 Marketing is not needed (

Fig. F9 Necessity of Marketing in Consultancy Services

4.12.1 Need for Marketing in Consultancy Services -

Having ascertained the need for marketing, consultancy firms open

their mind as to why they resort to marketing. Table TI5 shows the reasons for

adopting marketing by consultancy firms.

Table TI5

Need for Marketing in Consultancy Services

Source : Research Data

Reasons

Long-term survival

Growth of firm

Facing competition

All of the above

Total 164 100.00

No. of firms

51

62

20

31

Percentage

31.10

37.80

12.20

18.90

The table reveals that out of 164 respondents who consider marketing

as necessary, 62 firms state that marketing is necessary for the growth of firms,

51 firms account it for long-term survival, 20 for facing competition and 31 for

all of these reasons. It is inferred from the analysis that the consultants realise

that the consultancy firms need appropriate marketing strategies for retaining

existing clients and attracting new prospects.

All of the above 18.90% Long-term su wiva l

Facing competition 12.20%

1

Growth of firm 37.80%

Long-term survival Growth of firm

/ Facing competition /

Fig. F10 Reasons for Adopting Marketing in Consultancy Services

4.12.2 Reasons for not Recognising Marketing Function

The consultancy firms which do not support marketing state that it is

against ethics, not relevant or the firm is too small to afford a separate marketing

department. Table TI6 shows reasons for not recognising marketing by some

consultancy organisation.

Table TI6

Reasons why Marketing is not Necessary

Source : Research Data

Reasons

Marketing is against ethics

Marketing is not relevant

Firm is too small

Total

The table indicates that out of 36 respondents who consider marketing

as not necessary for consultancy service firms, 20 firms are of the opinion that

No. of firms

20

3

13

36

marketing is against ethics and hence not necessary, 13 firm.^ account it for the

smallness of the firm and the remaining 3 firms account it for the irrelevance of

marketing concept in the context of consultancy services. However, the arguments

Percentage

55.56

8.33

36.11

100

against marketing are not tenable in the context of liberaiised thinking and

professional freedom according to the opinions of the majority of consultants

who support marketing.

4.13 Classification of Activities (Departmentalisation) in Consultancy

Services

Departmentalisation is the process of grouping of operating tasks into

jobs, the combining of jobs into effective work groups and the combining of

groups into divisions called departments. Activities of a consultancy organisation

are classified on the basis of functions, products (services), areas or clients,

Table TI7 shows the classification of activities of consultancy organisations.

Table TI7

Classification of Activities of Consultancy Organisations

Source : Research Data

The table reveals that 98 firms (49 per cent) organise their activities

on the basis of functions, 80 (40 per cent) on the basis of services provided

and 22 (11 per cent) on the basis of their clients. No firm is found organising

its activities based on the geographical area of its services. It is seen that most

of the consultancy firms classify their activities on the basis of functions or

services mainly because of simplicity, flexibility, ease of co-ordination, operation

and control.

Basis of Classification

Functions

Services

Areas

Clients

Total

4.14 Number of Departments in Consultancy Organisations

Table 18 shows the number of departments in consultancy

organisations.

No. of firms

98

80

Nil

22

200

Percentage

49

40

Nil

11

100

Table T I 8

Number of Departments in Consultancy Organisations

Source : Research Data

Departments

Service Department

Marketing Department

Finance Department

Accounting Department

Personnel Department

(N = 200)

- The table indicates that 169 firms (84.5 per cent) have service

departments in their organisations. Only 56 firms (28 per cent) have separate

No. of firms

i69

56

45

33

4

marketing departments in their organisations. 45 firms have finance

departments, 33 have accounting departments and only four firms have

personnel departments in their organisations.

Percentage

84.5

28

22.5

16.5

2

Thus it is found that the activities of a consultancy organisation are

organised under departments each in charge of a function like service, marketing,

finance, accounting and personnel. A large consultancy organisation has more

departments depending upon the importance of these functions in the

organisation. In a small consultancy organisation all these functions are

discharged by a single department, most probably by the service department.

Servlce deparment Marketing Flname department Accounting Personnel department department department

- DEPARTMENT

Fig. F11 Departments in Consul tancy Organisat-ions

4.15 Delegation of Authority in Consultancy Organisations

In consultancy firms it is found necessay to delegate adequate authority

to lower levels so that the persons responsible for delivering the services can

effectively interact with the clients. At the same time the consultant retains

some key functions so as to ensure quality of service and better client satisfaction.

Only a decentralised consultancy firm can meet customer expectations effectively.

It is revealed in the study that all the consultancy organisations practise

delegation of authority to lower levels for better operational efficiency. There is

good extent of decentralisation of activities in almost all the firms and staff at

lower levels are fully motivated to deliver the clients best of their services.

4.16 Organisation Structure in Consultancy Services '

Organisation structure is primarily concerned with the allocation of

tasks among members of the organisation. According to the different practices

of allocation of authority and responsibility among persons, several types of

organisation structure have been evolved. These are the departmental and

line organisation, line and staff organisation, functional organisation and

committee organisation. Table T I 9 shows the organisation structure of

consultancy oiganisations.

Table TI9

Organisation Structure of Consultancy Firms

Source : Research Data

32 per cent of the respondents state that the organisation structure is

not clearly defined. These are either proprietary concerns or consultancy

Percentage

40 5.5

22.5 Nil 32

100

Nature of Organisation Structure

Departmental and line organisation Line and staff organisation Functional organisation Committee organisation Not clearly defined

Total

No. of firms

80 11 45 Nil 64

200

organisations with few number of members. 40 per cent of the consultancy

organisations follow the departmental and line organisation. 22.5 per cent of

the firms follow the functional form of organisation structure while 5.5 per cent

follow the line and staff form. It is revealed in the study that no firm follows the

committee form of organisation structure. Thus it is inferred from the analysis

that consultancy organisations, generally being organised on a small scale with

limited area of operation, follow a simple form of organisation structure with

clear cut line of authority and responsibility.

4.17 Organisation Chart in Consul tancy Organisations

Organisation chart is a diagrammatic representation of the network

of relations between the various positions in an organisation. Table T20 shows -

the classification of consultancy organisations on the basis of organisation charts.

Table T20

Classification of Consultancy firms on the basis of Organisation Charts

Source : Research Data

Particulars

Firms having organisation charts

Firms not having organisation charts

Total

The table indicates that 52 per cent of the consultancy organisations

have organisation charts and the remaining do not have any organisation charts.

No. of firms

104

96

200

Percentage

52

48

100

It is known from the study that in small consultancy organisations like that of

architects or project consultants, the consultant himself is the chief executive or

organisational head. The authority descends to the lower levels through systematic

assignment of functions to each person in the organisation. In large consultancy

firms, the consultant acts as a departmental head supervising the specific

functions of his department. He may also act as a 'Staff' with advisory roles in

certain organisations. In software consultancy, the consultants are employed as

'Staff' functionaries to develop specific software for serving the needs of clients.

4.18 Manpower Requirements and Training in Consultancy

-- Organisations

~onsultants are well qualified professionals in the area of their

services. Some of them are also members of professional bodies like Council

of Architects, Institute of Chartered Accountants, Institute of Cost Accountants

etc. Consultants may practice independently or may join any consultancy firm

as employees or partners.

4.18.1 Procedure for Selection of Consultants

From interviews and discussions with respondents it is pointed out

that most of the consulting firms have been recruiting consultants through

direct interview method. A few of them especially the software consulting

firms use the campus interview method for selection of consultants. Consultants

are appointed taking into consideration their qualifications, work experience,

motivations, aspirations, ability to communicate and leadership qualities.

4.18.2 Training of Consultants

It is found in the study that consultants are first appointed at assistant

or junior levels in many consultancy organisations. They are given adequate

training at this level. The respondents state that the methods of training include

on the job training, attending seminars, workshops and oral presentations. In

large consultancy firms, consultants appointed are given opportunities to grow

from the level of Assistant Consultants to a Senior-Consultant and goes on to

become a Service Head or a Regional Head. 1t is also revealed in the study -

that some consultancy firms offer very elaborate career design programmes to

those who have proven their worth at the entry level.

4.18.3 Manpower Planning in Consultancy Services

Planning of future requirements of consultants is very essential for

efficient operation and facing competition in the long run. However, this aspect

is totally ignored and little or no planning is done to meet future requirements

of consultants by most of the consultancy firms. It is revealed by some

respondents that the firm hires a person when a consultant quits or the need

arises. Such practices often lead to poor choice of consultants.

It is revealed in the study that there has been no difficulty in getting

qualified consultants by these firms. Consultants are suitably rewarded and

career development prospects are also bright in most of the consultancy firms.

It is also reported that labour turnover is very low in the field of consultancy

services.

It is necessary to give a certain degree of autonomy and discretion to

consultants while taking up client problems. Professional freedom and '

independence are required for delivering better quality services. The study

reveals that most of the consultancy organisations give necessary authority

and freedom to consultants to take up independent assignments and offer -

expert advice or solutions to clients' needs or problems. -

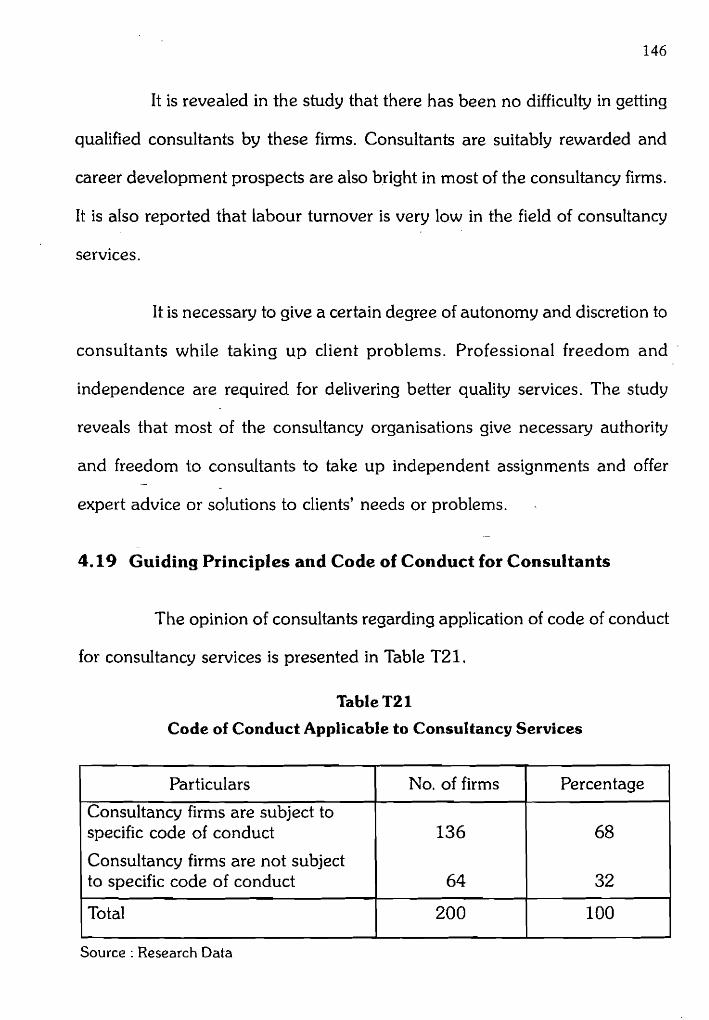

4.19 Guiding Principles and Code of Conduct for Consultants

The opinion of consultants regarding application of code of conduct

for consultancy services is presented in Table T21.

Table T21

Code of Conduct Applicable to Consultancy Services

Source : Research Data

Particulars

Consultancy firms are subject to specific code of conduct

Consultancy firms are not subject to specific code of conduct

Total

No, of firms

136

64

200

Percentage

68

32

100

136 respondents (68 per cent) in the study state that consultants are

subject to specific code of conduct in their services, while the remaining 64

firms (32 per cent) state in the negative. It is revealed that there is no uniform

code of conduct or universally accepted guidelines applicable to all consultants.

These are governed mostly by conventions and the Rules of professional bodies

to which they are associated. Some of these are codified and found in the

respective Acts like the Chartered Accountants Act, 1949, The Companies

Act, 1956, T h e Securities and Exchange Board of India Act, 1992 etc.

Consultancy firms are not subject to specific code of

conduct

conduct 68%

Consultancy firms are subject to specific code of conduct Consultancy firms are not subject to s~ecific code of conduct

Fig. F12 Code of Conduct for Consultants

Consultants are unanimous in their opinion regarding service quality

and client satisfaction. They state that a consultant must be competent,

trustworthy, of good integrity and caring for clients. He must maintain secrecy

regarding operations of client and adhere to the time schedule agreed upon.

Some of the comments of consultants interviewed in this respect are:

- 'the services of the consultant must be result-oriented.'

- 'the consultant shall render the best services possible according

to the expectations of his clients.'

- 'he must give the best value for the fees paid.'

4.20 Liability of Consultants to Clients

Consultants are expected to give expert advice or solutions to clients' -

problems. They shall not be negligent in their duties and responsibilities to

their clients. Consultants have only advisory roles and they may not often

engage in the implementation of the recommendations. Therefore, whether

the consultants have any personal liability towards the clients for deficiency of

services is yet to be settled. Some of the recent judgements of the consumer

courts in the country point to the fact that service providers are liable for

deficiency of services. Therefore, it is beyond doubt that consultants are liable

for proved misconduct or deficiency in their services.

The opinion of consultants in this respect is, however, not unanimous

as shown in Table T22.

Table T22

Classification of Respondents on the basis of Liability of Consultants for Deficiency of Services

Source : Research Data

The table reveals that 80.5 per cent of the respondents favour the

view that consultants are personally liable to clients for the deficiency of services.

The remaining -19.5 per cent state-that the consultants are not liable.

Percentage

80.5

19.5

100.0

Particulars

Consultant is liable

Consultant is not liable

Total

The nature of liability, as stated by the respondents who support the

view, includes damages for loss arising to the clients, refund of fees or loss of

clients. Penalties, disciplinary actions or even removal of membership from

professional bodies are also stated as the consequences of dishonest acts by

consultants.

No, of firms

161

39

200

Upon an indepth analysis of the organisation of consultancy services

it can be concluded that the ability of a consultancy organisation to respond to

the changing requirements of a liberalised economic environment and increasing

expectations of clients depends on its internal strength. The organisation design

must be well-structured to meet these challenges. It must be simple, proactive

to changes and based on accepted principles with complete delimination on

authorities and responsibilities. The object of the organisation design in

consultancy services must be better client service, faster decision-making and

improvement in productivity and profitability.

It is found in the analysis that many consultancy organisations lack

the internal strengths and vibrant organisation structures. Though there is an

increasing awareness among consultancy organisations regarding the role of

marketing many of them are found reluctant in applying marketing in their

organisations. It is not the number of consultants or service personnel but the

qualitative skills and professionalism that determine the efficiency of the

organisation. But not much attention is given to strengthen the skills of -

consultants..and service personnel in the organisations as revealed in the study.