OPTIONS -BASICS Terminology of Options Call Option Put Option

Upload

garey-hoodCategory

view

215download

0

Options

• This PowerPoint presentation consists of two examples.– Put Option– Call Option

• Options are part of a larger group of securities known as derivatives. In addition to options, derivatives consist of futures and swaps.

Stock Option• Stock options tend to be the easiest type of derivatives to grasp. In

addition to stocks, options exist for a host of financial assets. Even in the case of stocks, options may exist for individual stocks as well as some of the major indices. We will begin with an example for an individual stock (you should note, option prices are listed for individual stocks though typically sell in lots of 100 shares).

• Upon hearing some interesting news, suppose you believe IBM stock was about to sky rocket. You have some extra money to invest right now, but know that you’ll need the money – e.g., pay tuition – in three months. Thus, you plan to hold the stock for only three months – hence, we can ignore dividends and just focus on the capital gain or loss resulting from the price of the stock.

Stock Option• The IBM stock is currently selling for $50 per share. Ignoring any

transactions costs (e.g., brokerage fees), what are your potential gains and losses?

• The answer is pretty clear, but we’ll create a little table anyway. What would your profit and loss be if the price three months from now was $40? $45? $50? $55? $60?

Stock Option• The IBM stock is currently selling for $50 per share. Ignoring any

transactions costs (e.g., brokerage fees), what are your potential gains and losses?

• The answer is pretty clear, but we’ll create a little table anyway. What would your profit and loss be if the price three months from now was $40? $45? $50? $55? $60?

3 Month Current Profit or

Price Price Loss

$40 $50 -$10

$45 $50 -$5

$50 $50 $0

$55 $50 +$5

$60 $50 +$10

Now, plot this on a graph…

Stock OptionAlong the horizontal axis, plot the various prices of the stock. Along the vertical axis plot…

45 50 55 60 40 Price

Stock OptionAlong the horizontal axis, plot the various prices of the stock. Along the vertical axis plot…the profit (gain) and loss for each ending price. Now, plot the results from the table on a line and imagine doing it for all prices in-between…

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

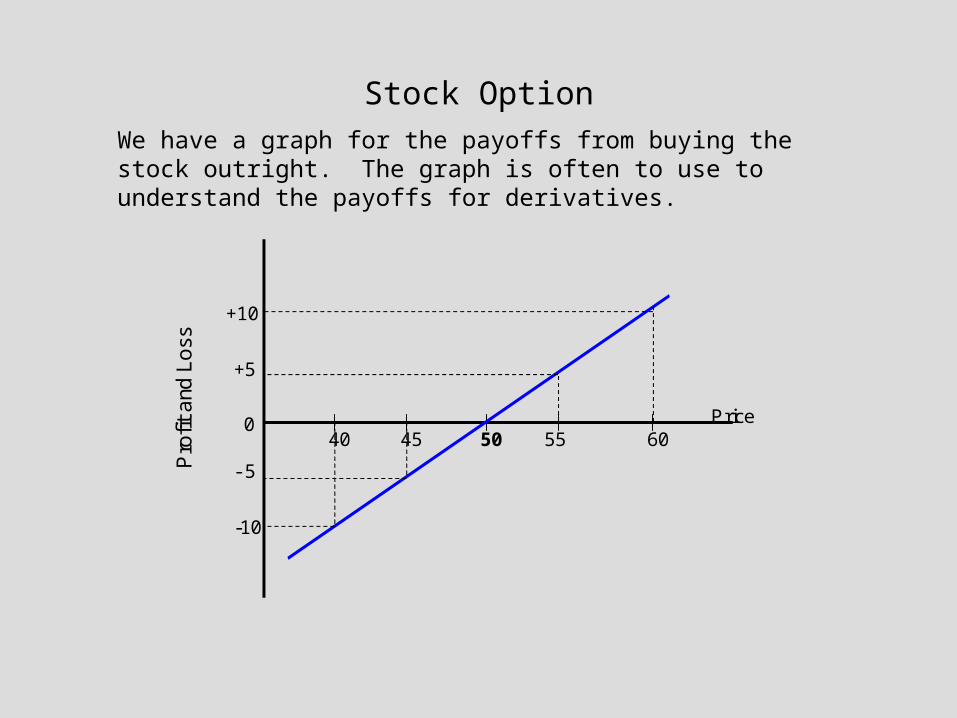

Stock OptionWe have a graph for the payoffs from buying the stock outright. The graph is often to use to understand the payoffs for derivatives.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

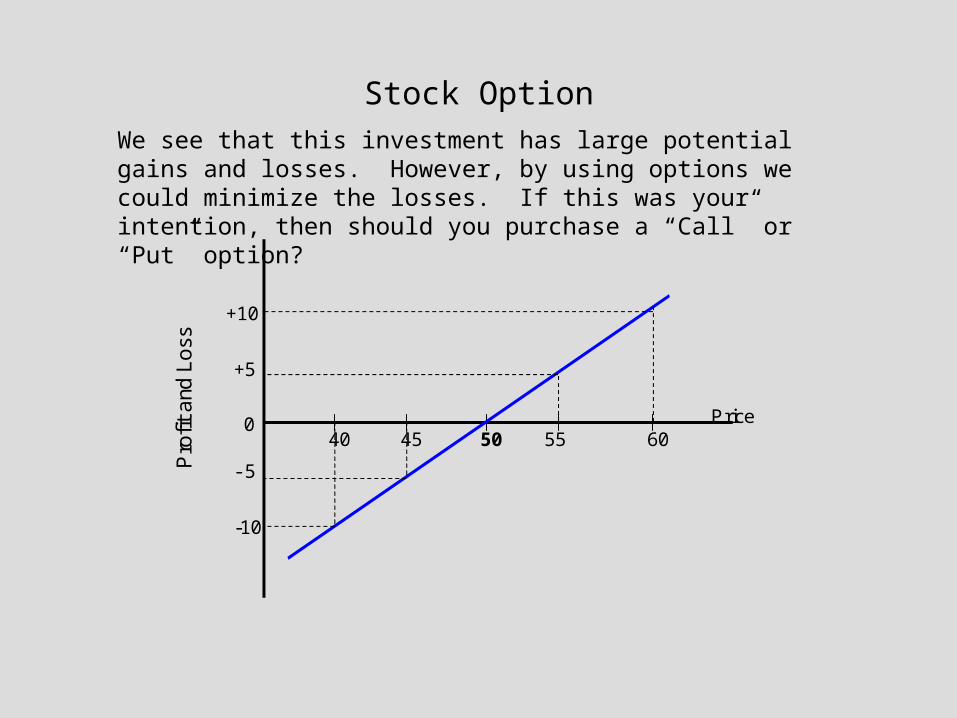

Stock OptionWe see that this investment has large potential gains and losses. However, by using options we could minimize the losses. If this was your intention, then should you purchase a “Call” or “Put” option?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Put OptionSuppose you purchased a Put Option at the same time you purchase this stock. Recall, a put option will give you the right – but not obligation – to sell the stock at the exercise price.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

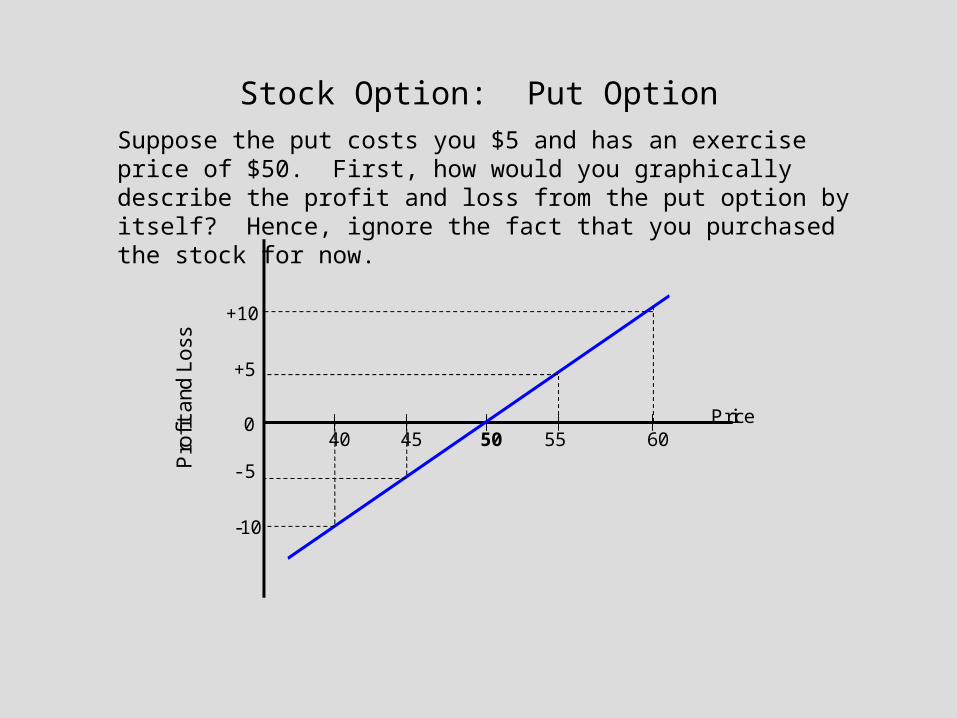

Stock Option: Put OptionSuppose the put costs you $5 and has an exercise price of $50. First, how would you graphically describe the profit and loss from the put option by itself? Hence, ignore the fact that you purchased the stock for now.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

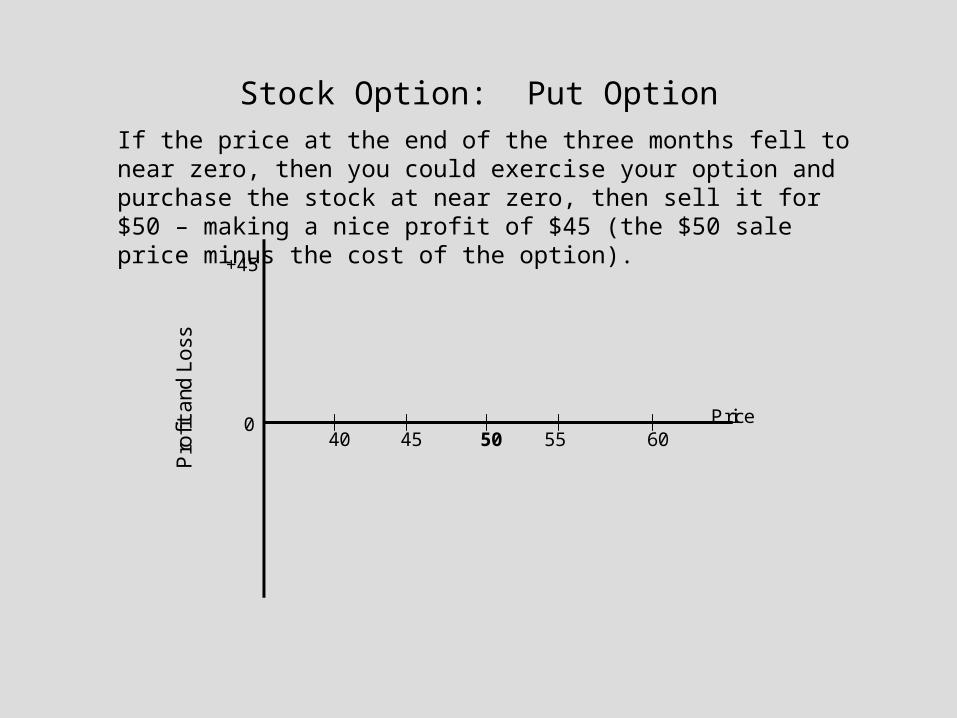

Stock Option: Put OptionIf the price at the end of the three months fell to near zero, then you could exercise your option and purchase the stock at near zero, then sell it for $50 – making a nice profit of $45 (the $50 sale price minus the cost of the option).

45 50 55 60 40 Price

Pro

fit a

nd L

oss

0

+45

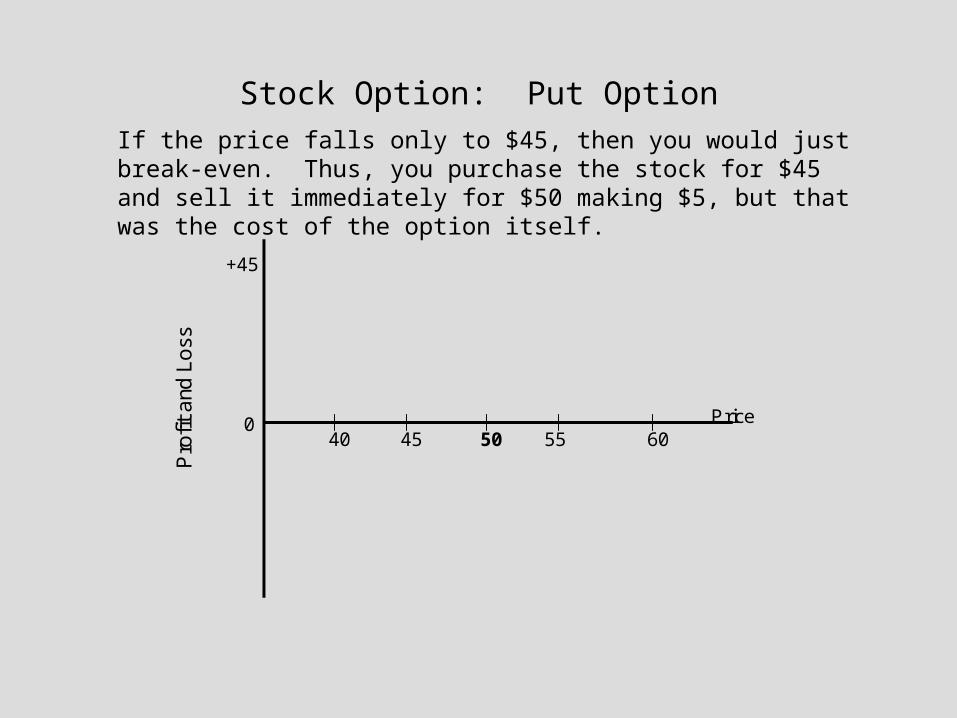

Stock Option: Put OptionIf the price falls only to $45, then you would just break-even. Thus, you purchase the stock for $45 and sell it immediately for $50 making $5, but that was the cost of the option itself.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

0

+45

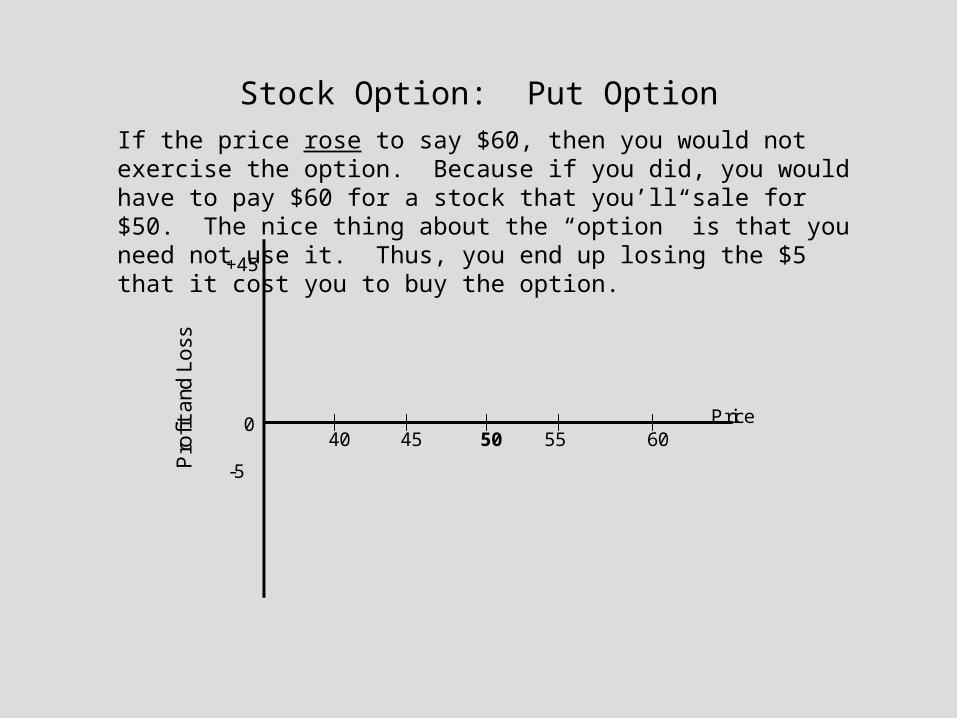

Stock Option: Put OptionIf the price rose to say $60, then you would not exercise the option. Because if you did, you would have to pay $60 for a stock that you’ll sale for $50. The nice thing about the “option” is that you need not use it. Thus, you end up losing the $5 that it cost you to buy the option.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

0

-5

+45

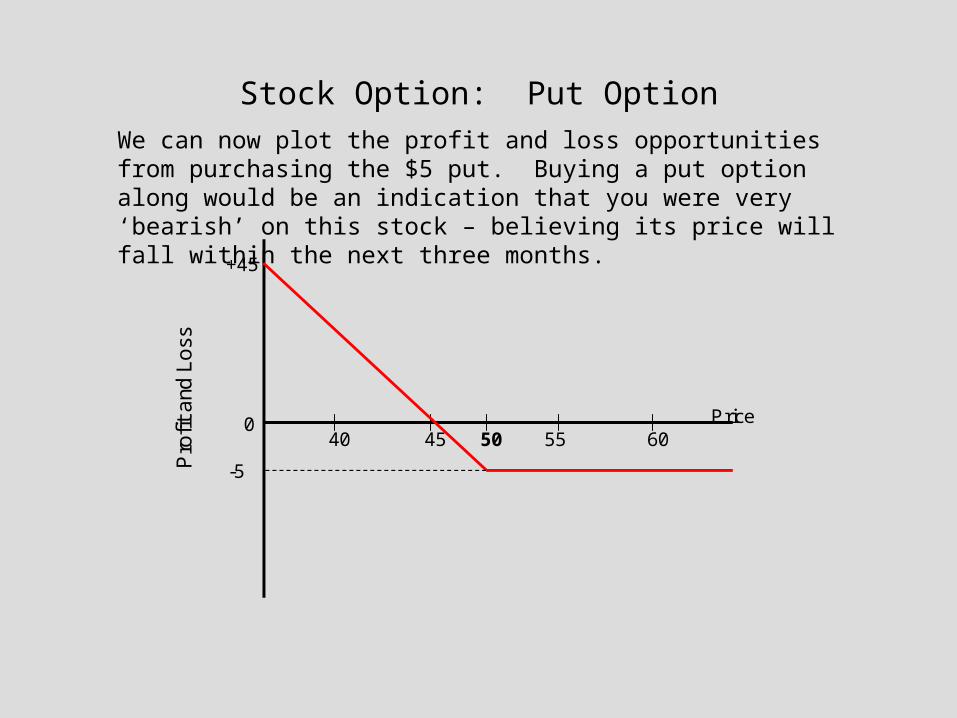

Stock Option: Put OptionWe can now plot the profit and loss opportunities from purchasing the $5 put. Buying a put option along would be an indication that you were very ‘bearish’ on this stock – believing its price will fall within the next three months.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

0

-5

+45

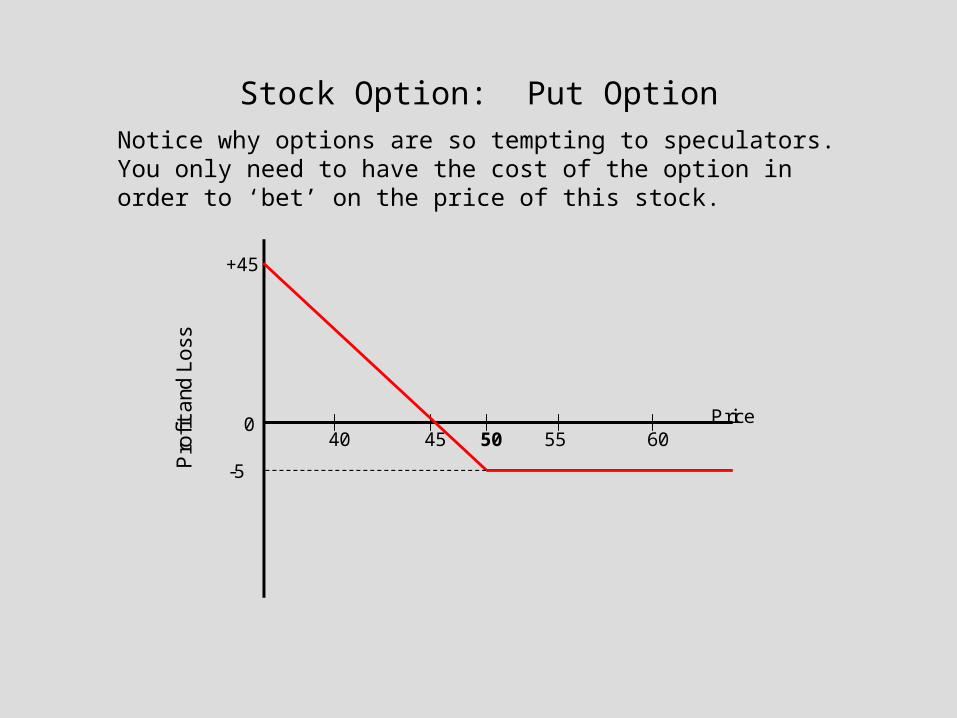

Stock Option: Put OptionNotice why options are so tempting to speculators. You only need to have the cost of the option in order to ‘bet’ on the price of this stock.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

0

-5

+45

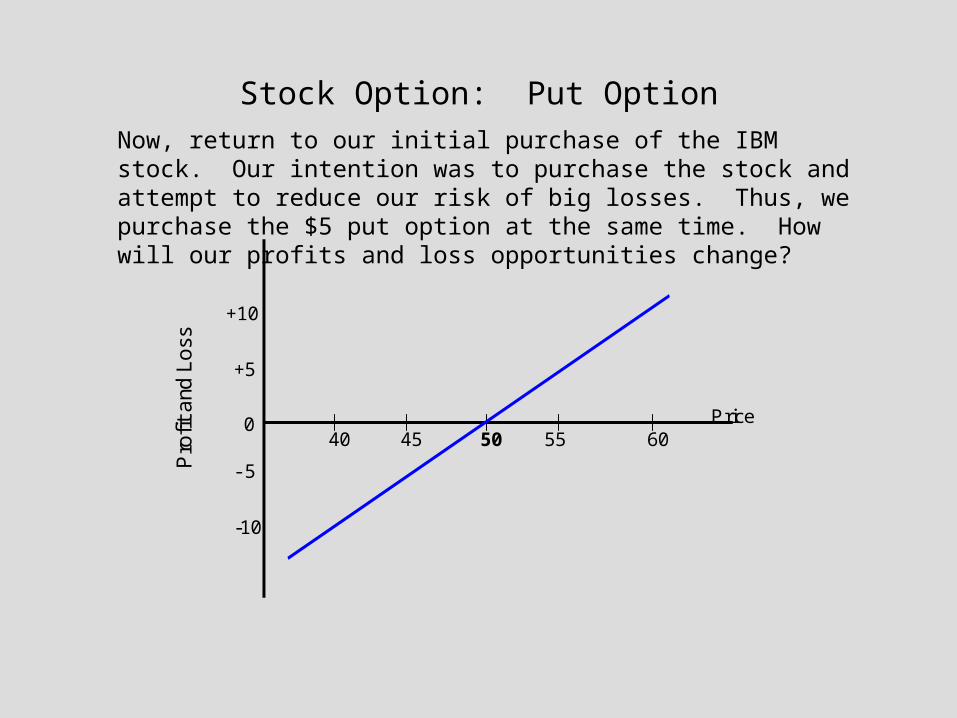

Stock Option: Put OptionNow, return to our initial purchase of the IBM stock. Our intention was to purchase the stock and attempt to reduce our risk of big losses. Thus, we purchase the $5 put option at the same time. How will our profits and loss opportunities change?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

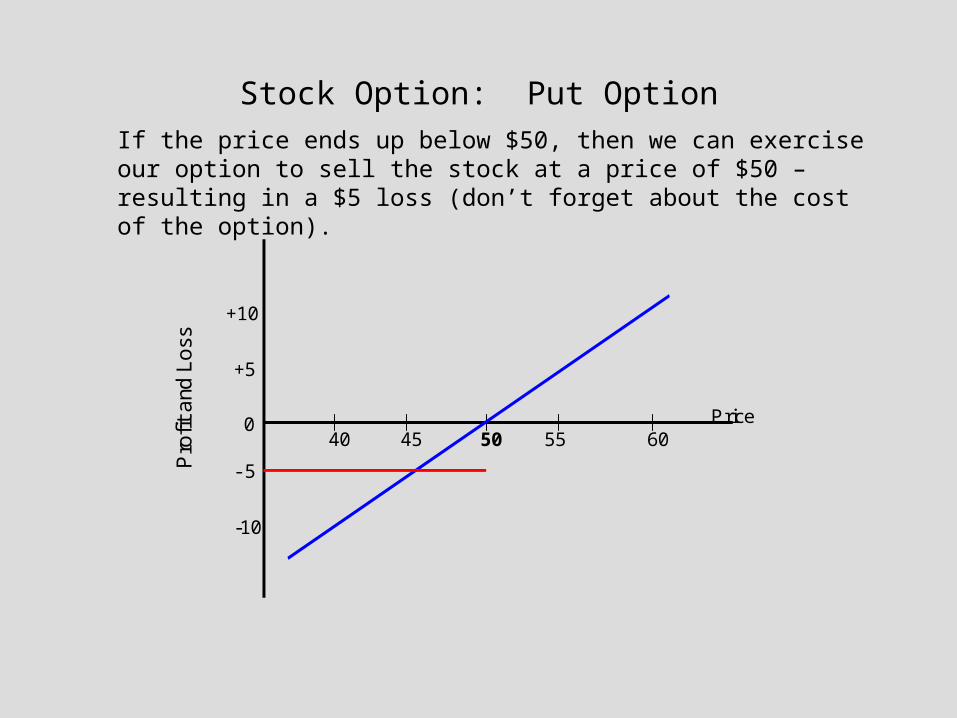

Stock Option: Put OptionIf the price ends up below $50, then we can exercise our option to sell the stock at a price of $50 – resulting in a $5 loss (don’t forget about the cost of the option).

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

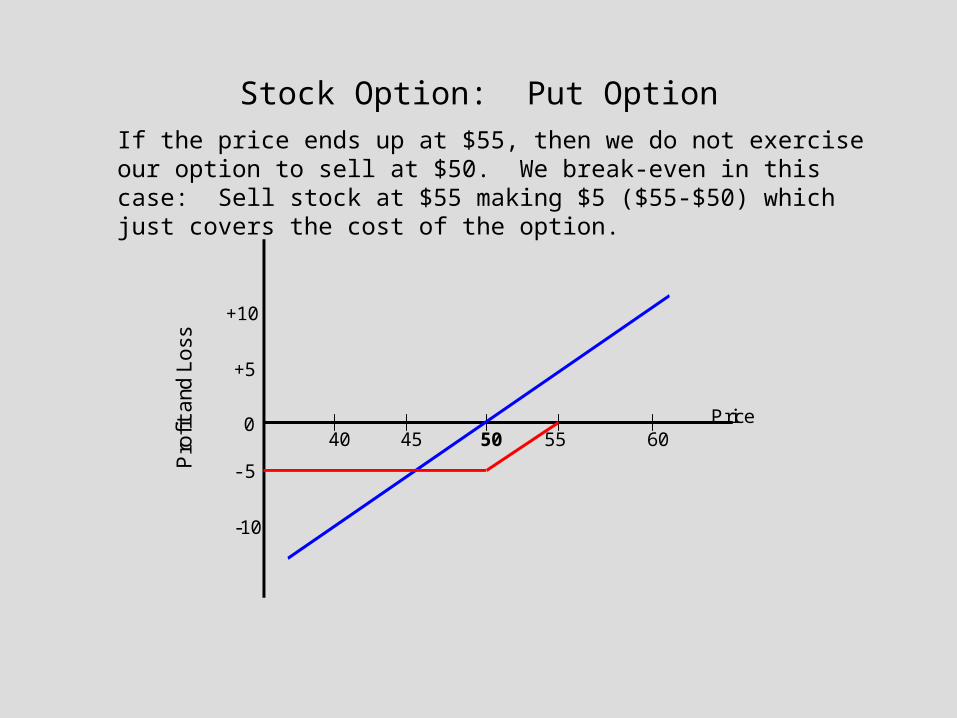

Stock Option: Put OptionIf the price ends up at $55, then we do not exercise our option to sell at $50. We break-even in this case: Sell stock at $55 making $5 ($55-$50) which just covers the cost of the option.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

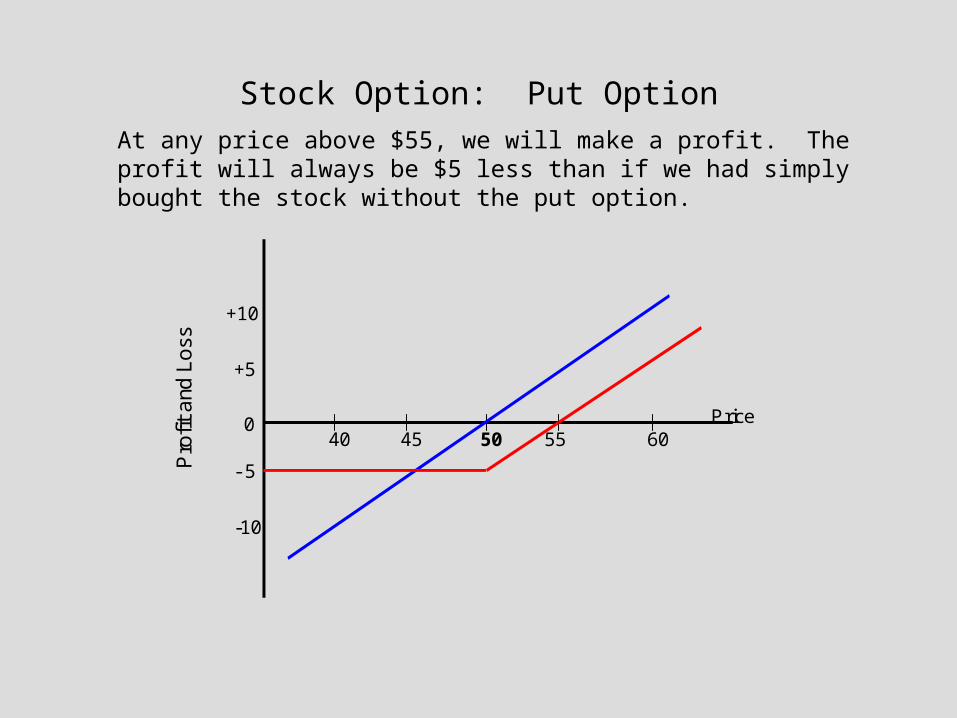

Stock Option: Put OptionAt any price above $55, we will make a profit. The profit will always be $5 less than if we had simply bought the stock without the put option.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

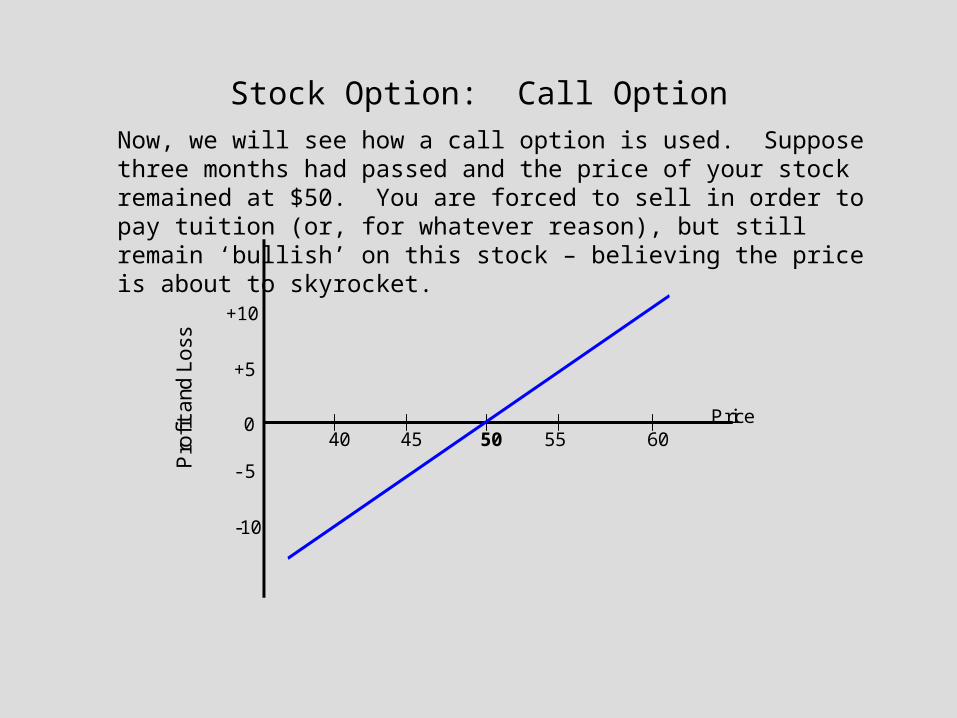

Stock Option: Call OptionNow, we will see how a call option is used. Suppose three months had passed and the price of your stock remained at $50. You are forced to sell in order to pay tuition (or, for whatever reason), but still remain ‘bullish’ on this stock – believing the price is about to skyrocket.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Call OptionYou don’t want to miss out on the increase in the price which you believe will occur soon. So, you take $5 from your sale and purchase a “Call Option”. Recall, a call option gives you the right – but not obligation – to buy an asset at the exercise price.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

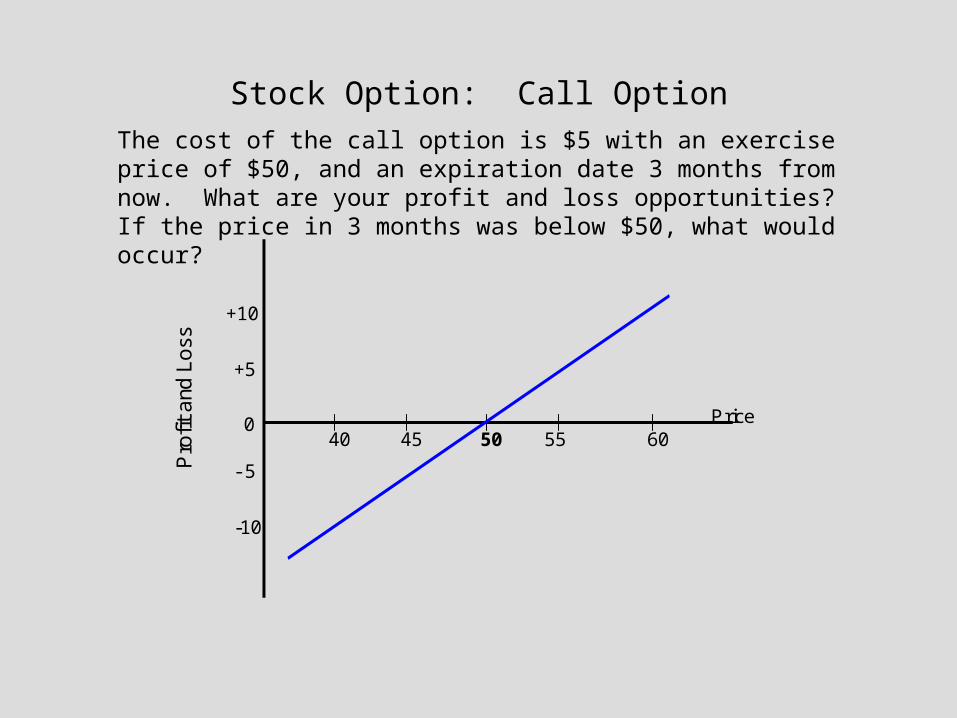

Stock Option: Call OptionThe cost of the call option is $5 with an exercise price of $50, and an expiration date 3 months from now. What are your profit and loss opportunities? If the price in 3 months was below $50, what would occur?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Call OptionIf the price in 3 months was below $50, what would occur? You would not exercise your right to buy the stock at $50 if the price at the time was below it. Thus, you would lose the cost of the option. If the price were between $50 and $55?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

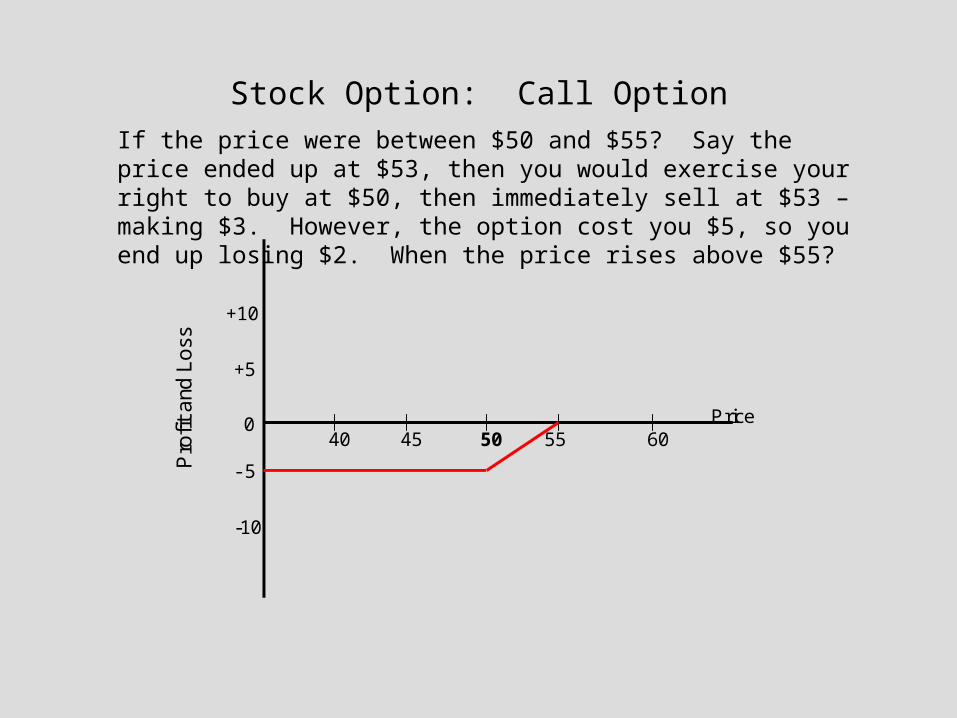

Stock Option: Call OptionIf the price were between $50 and $55? Say the price ended up at $53, then you would exercise your right to buy at $50, then immediately sell at $53 – making $3. However, the option cost you $5, so you end up losing $2. When the price rises above $55?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

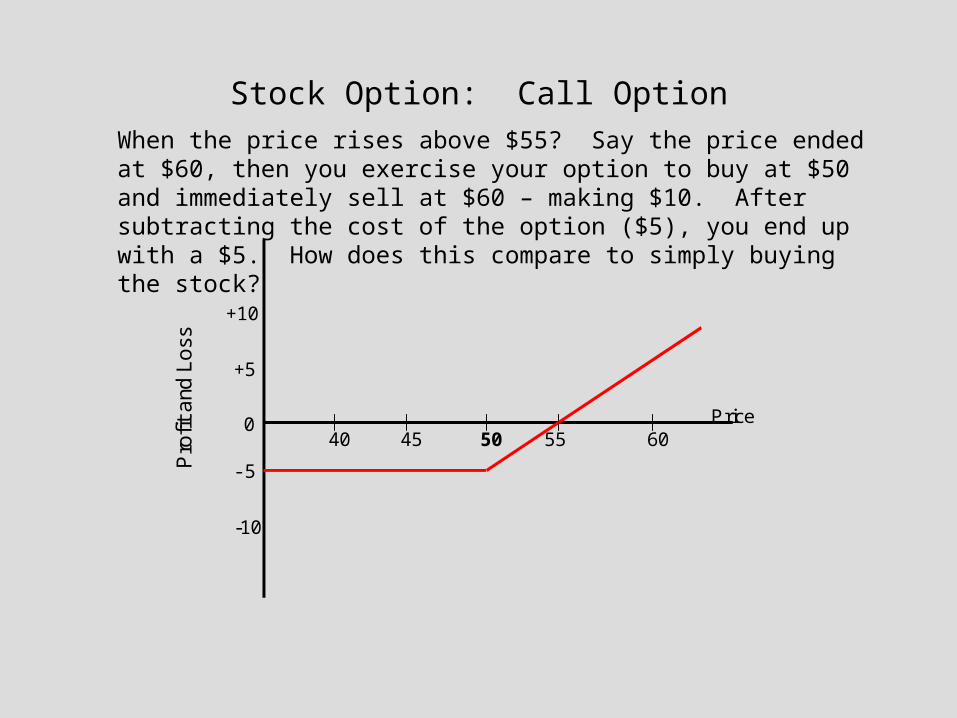

Stock Option: Call OptionWhen the price rises above $55? Say the price ended at $60, then you exercise your option to buy at $50 and immediately sell at $60 – making $10. After subtracting the cost of the option ($5), you end up with a $5. How does this compare to simply buying the stock?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Call OptionFor a $5 investment (the cost of the option), you have the opportunity to make large profits. Compared to simply buying the stock (or, in this example continuing to hold on to it and not pay tuition), your profit opportunities are always $5 less with the call option. However, …

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Call Optionyou can only lose the $5 cost of the option. The graph below is identical to the situation of buying the stock and a $5 put option. These will always be similar outcomes – though our numbers make them identical.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Selling a Call OptionOne last example might be useful. Suppose you had initially purchased the stock at $50 and instead of buying a put option, had sold a call option?

Stock Option: Selling a Call OptionOne last example might be useful. Suppose you had initially purchased the stock at $50 and instead of buying a put option, had sold a call option?

By selling a call option, someone else may call upon you to sell your stock to them. After all, in the previous example when you bought a call option – you purchased the right to buy an asset at the exercise price from someone. Now, the someone will be you. In essence, someone will have the right to buy the stock from you at the exercise price. The upside is that you will receive the cost of the option!

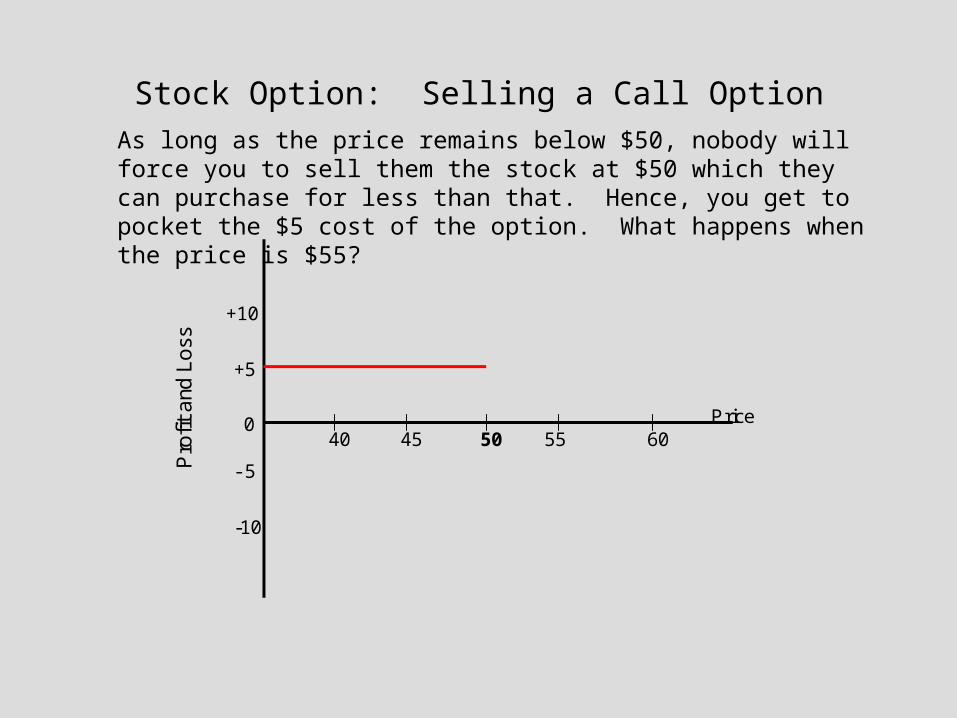

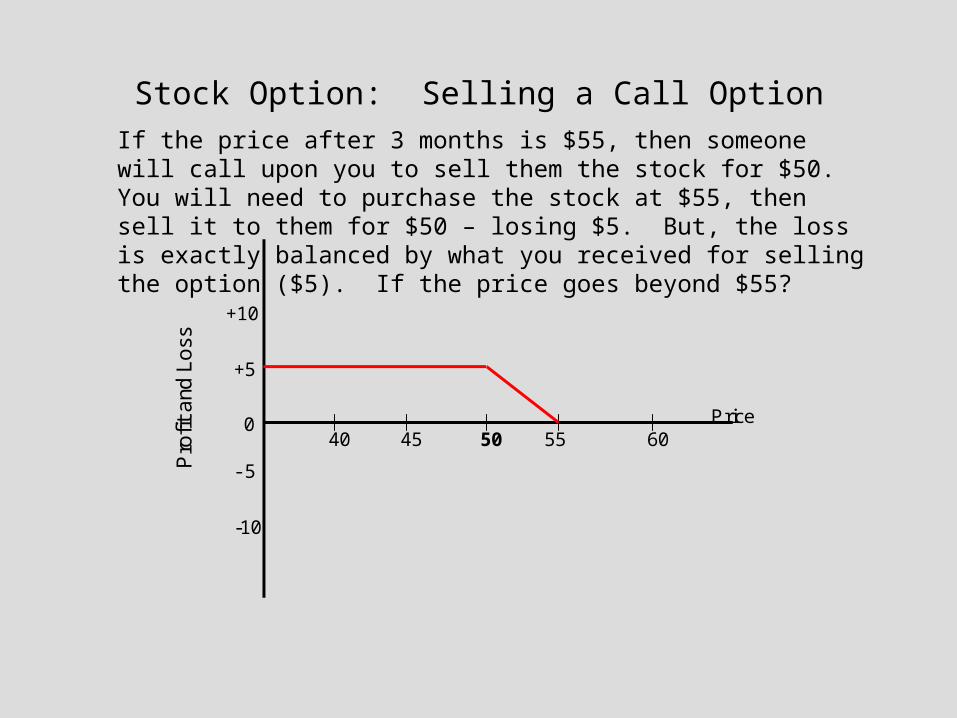

Stock Option: Selling a Call OptionAs long as the price remains below $50, nobody will force you to sell them the stock at $50 which they can purchase for less than that. Hence, you get to pocket the $5 cost of the option. What happens when the price is $55?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Selling a Call OptionIf the price after 3 months is $55, then someone will call upon you to sell them the stock for $50. You will need to purchase the stock at $55, then sell it to them for $50 – losing $5. But, the loss is exactly balanced by what you received for selling the option ($5). If the price goes beyond $55?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Selling a Call OptionIf the price should rise above $55, then you will begin making losses. Say the price was $60. You will need to purchase the stock at $60 and sell at $50, making a $10 loss which the cost of the option ($5) you received does not cover. The situation grows worse as the price rises.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

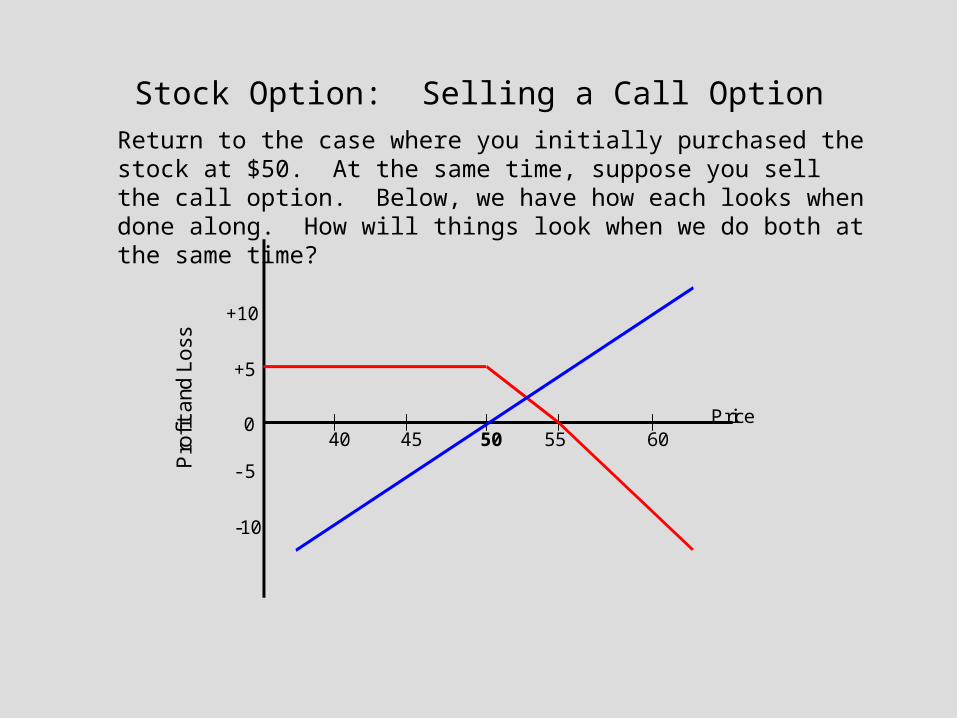

Stock Option: Selling a Call OptionReturn to the case where you initially purchased the stock at $50. At the same time, suppose you sell the call option. Below, we have how each looks when done along. How will things look when we do both at the same time?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Selling a Call OptionIf the stock ends up below $50, then the call option we sold will not be exercised. We will suffer losses on the stock we purchased, but the losses will not be as severe – by the amount of the $5 received from selling the call option.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock Option: Selling a Call OptionFor example, if the price had ended up at $45, then we lose $5 on our initial purchase of the stock at $50, but make up the loss from the sale of the call option at $5. Hence, we break even. What if the price ends at $50?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

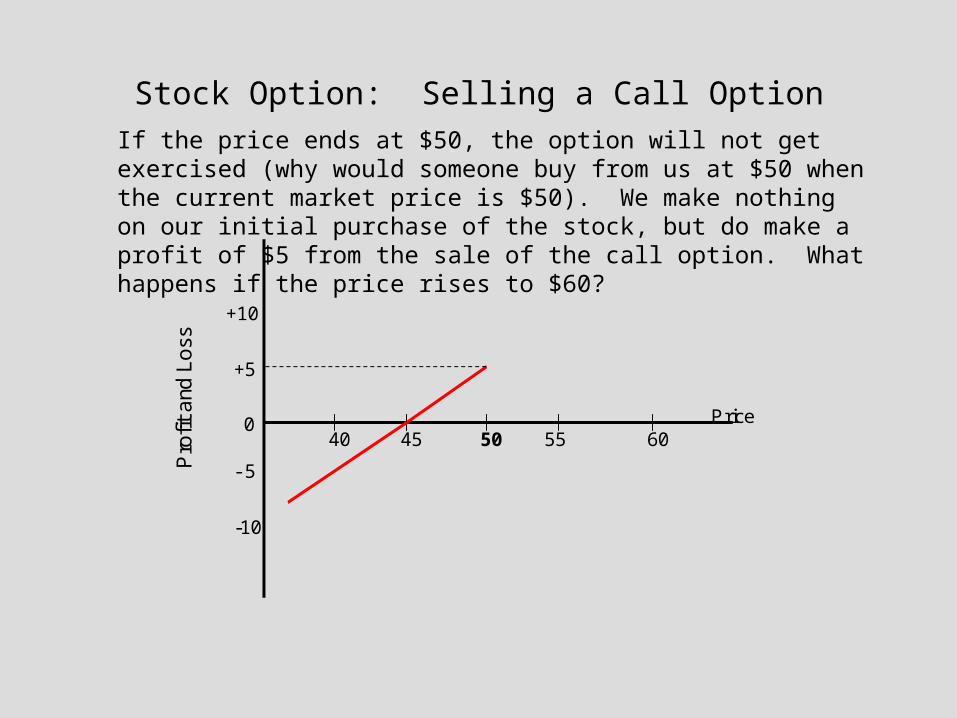

Stock Option: Selling a Call OptionIf the price ends at $50, the option will not get exercised (why would someone buy from us at $50 when the current market price is $50). We make nothing on our initial purchase of the stock, but do make a profit of $5 from the sale of the call option. What happens if the price rises to $60?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

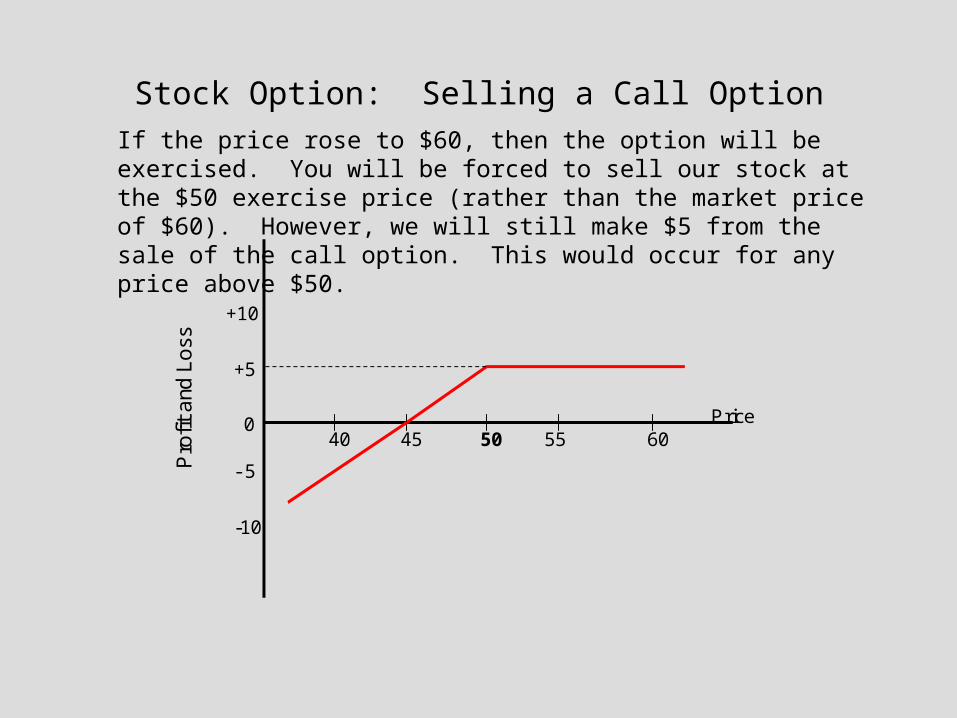

Stock Option: Selling a Call OptionIf the price rose to $60, then the option will be exercised. You will be forced to sell our stock at the $50 exercise price (rather than the market price of $60). However, we will still make $5 from the sale of the call option. This would occur for any price above $50.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

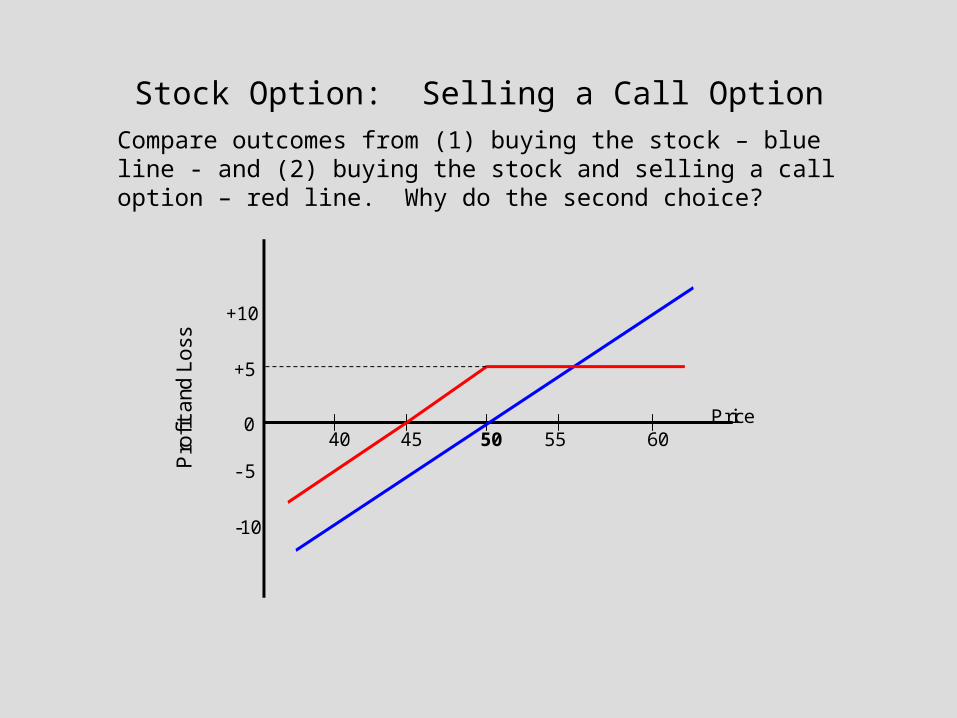

Stock Option: Selling a Call OptionCompare outcomes from (1) buying the stock – blue line - and (2) buying the stock and selling a call option – red line. Why do the second choice?

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

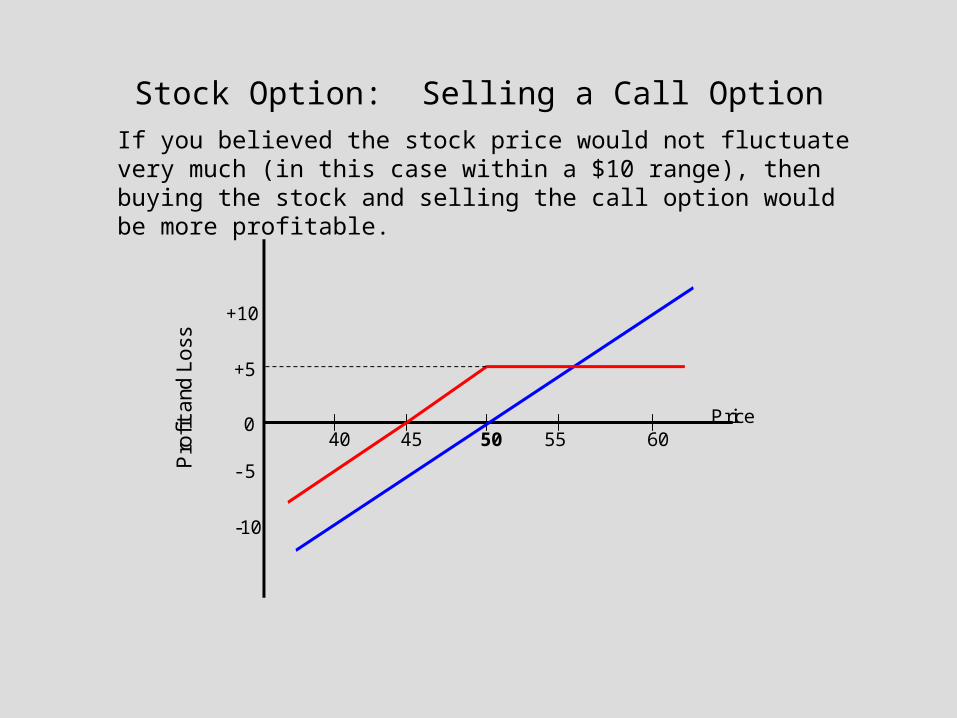

Stock Option: Selling a Call OptionIf you believed the stock price would not fluctuate very much (in this case within a $10 range), then buying the stock and selling the call option would be more profitable.

45 50 55 60 40 Price

Pro

fit a

nd L

oss

- 5

0

+5

+10

-10

Stock OptionThe analysis of stock options carries over directly to options in futures. We have only scratched the surface of how options and, more generally, derivatives are used. Hopefully, you have seen how they can be used to reduce risk. Also, you have seen why they are so tempting as a tool of speculation. We have not covered how one might value options. Of course, the market price of an option is determined like any other financial asset by the forces of supply and demand. When we talk about ‘valuing’ an option, we are interested in understanding the determination of its ‘intrinsic value’. The famous Black-Scholes pricing formula has played a dominate role in valuing options. This role has been extending as more assets (both financial and real) become conceptualized as options.