Options and futures markets #3

40

1 ©All rights reserved to prof. Rafi Eldor Options and Futures Markets Class #3 26.3.2015 Prof Rafi Eldor Mr. Eitan Zeevi ©All rights reserved to prof. Rafi Eldor

-

Upload

- -

Category

Economy & Finance

-

view

109 -

download

1

Transcript of Options and futures markets #3

1

©All rights reserved to prof. Rafi Eldor

Options and Futures Markets

Class #3

26.3.2015

Prof Rafi Eldor

Mr. Eitan Zeevi

©All rights reserved to prof. Rafi Eldor

2

©All rights reserved to prof. Rafi Eldor

Put Option

Definition:

The buyer of a Put option (long Put) has the right (but not the

obligation) to Sell a predetermined amount of the underling

asset (notional) at a given price during specific period or at a

particular point in time against payment of premium

Comments:o Option value can not be negative

o The value of the option at expiration date is the difference between the

strike and underlying rate.

Put Option Fundamentals

3

©All rights reserved to prof. Rafi Eldor

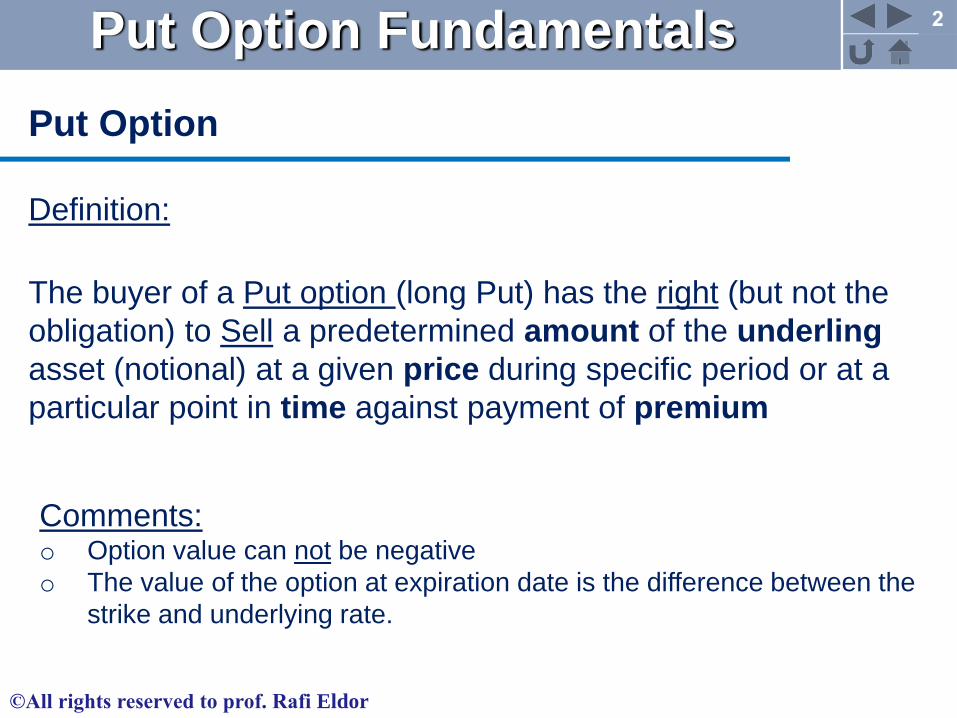

Underlying price at expiration date

Breakeven

Option value at expiration date

Payoff/Profit

Payoff at expiration date

Put option payoff as a function of the underlying price at

expiration date (for the buyer)

Put Option Fundamentals

4.003.98

4

©All rights reserved to prof. Rafi Eldor

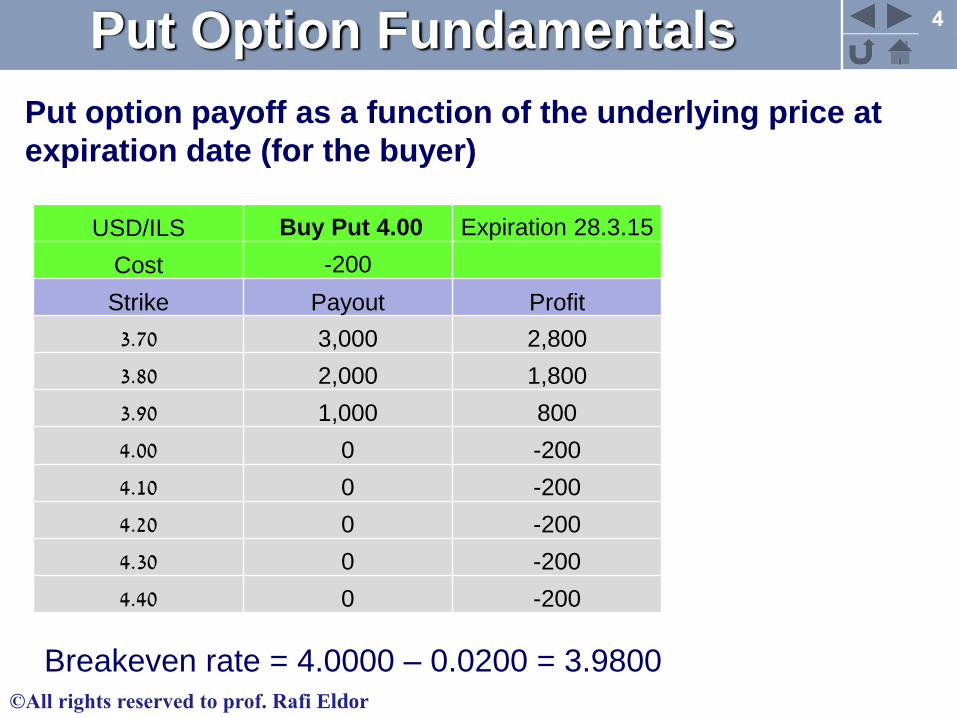

Put option payoff as a function of the underlying price at

expiration date (for the buyer)

Put Option Fundamentals

USD/ILS Buy Put 4.00 Expiration 28.3.15

Cost -200

Strike Payout Profit

3.70 3,000 2,800

3.80 2,000 1,800

3.90 1,000 800

4.00 0 -200

4.10 0 -200

4.20 0 -200

4.30 0 -200

4.40 0 -200

Breakeven rate = 4.0000 – 0.0200 = 3.9800

5

©All rights reserved to prof. Rafi Eldor

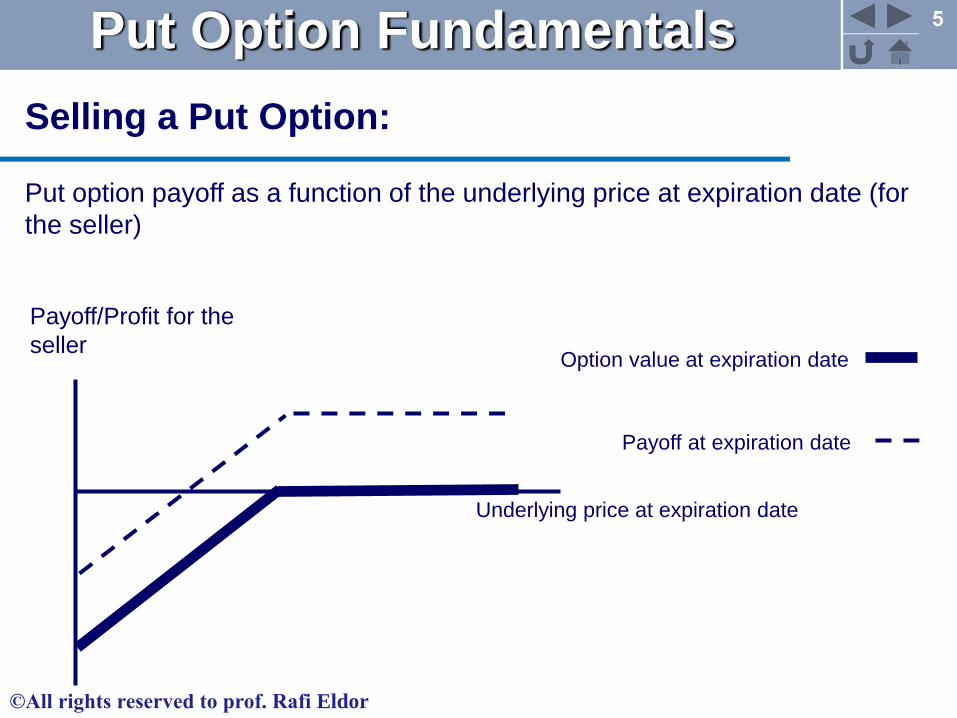

Underlying price at expiration date

Selling a Put Option:

Put option payoff as a function of the underlying price at expiration date (for

the seller)

Payoff/Profit for the

seller

Put Option Fundamentals

Option value at expiration date

Payoff at expiration date

6

©All rights reserved to prof. Rafi Eldor

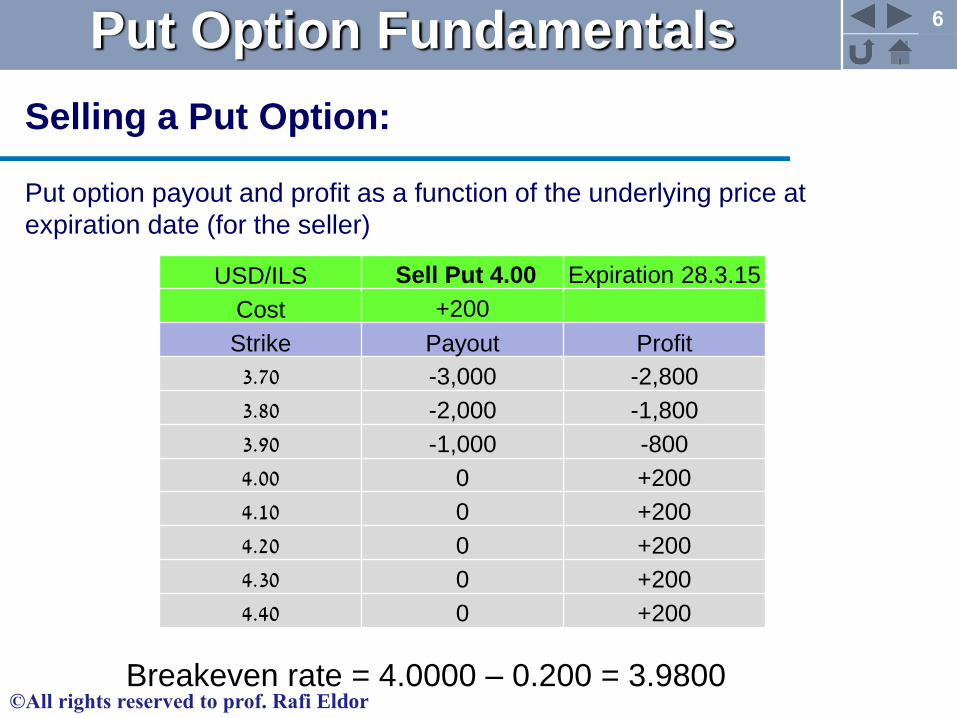

Selling a Put Option:

Put option payout and profit as a function of the underlying price at

expiration date (for the seller)

Put Option Fundamentals

USD/ILS Sell Put 4.00 Expiration 28.3.15

Cost +200

Strike Payout Profit

3.70 -3,000 -2,800

3.80 -2,000 -1,800

3.90 -1,000 -800

4.00 0 +200

4.10 0 +200

4.20 0 +200

4.30 0 +200

4.40 0 +200

Breakeven rate = 4.0000 – 0.200 = 3.9800

7

©All rights reserved to prof. Rafi Eldor

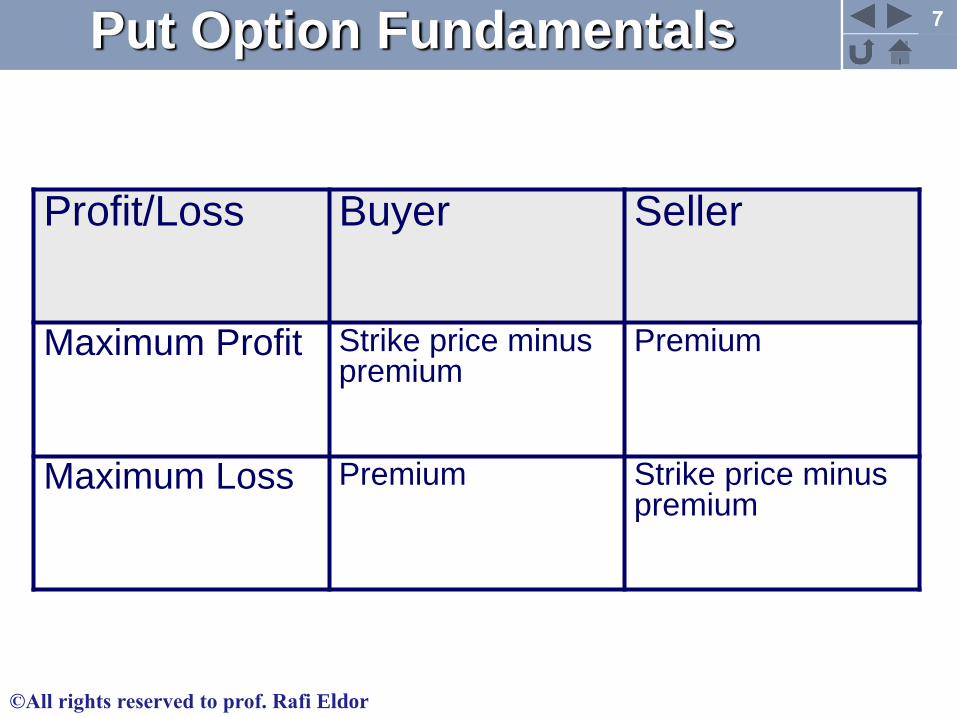

Profit/Loss Buyer Seller

Maximum Profit Strike price minus premium

Premium

Maximum Loss Premium Strike price minus premium

Put Option Fundamentals

8

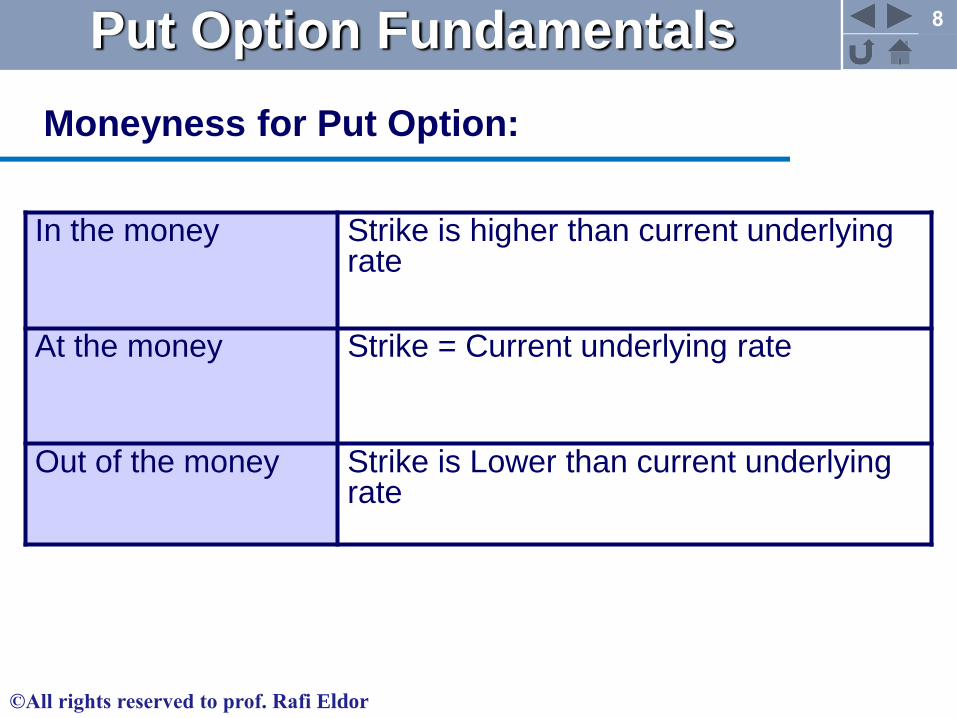

©All rights reserved to prof. Rafi Eldor

Moneyness for Put Option:

In the money Strike is higher than current underlying rate

At the money Strike = Current underlying rate

Out of the money Strike is Lower than current underlying rate

Put Option Fundamentals

9

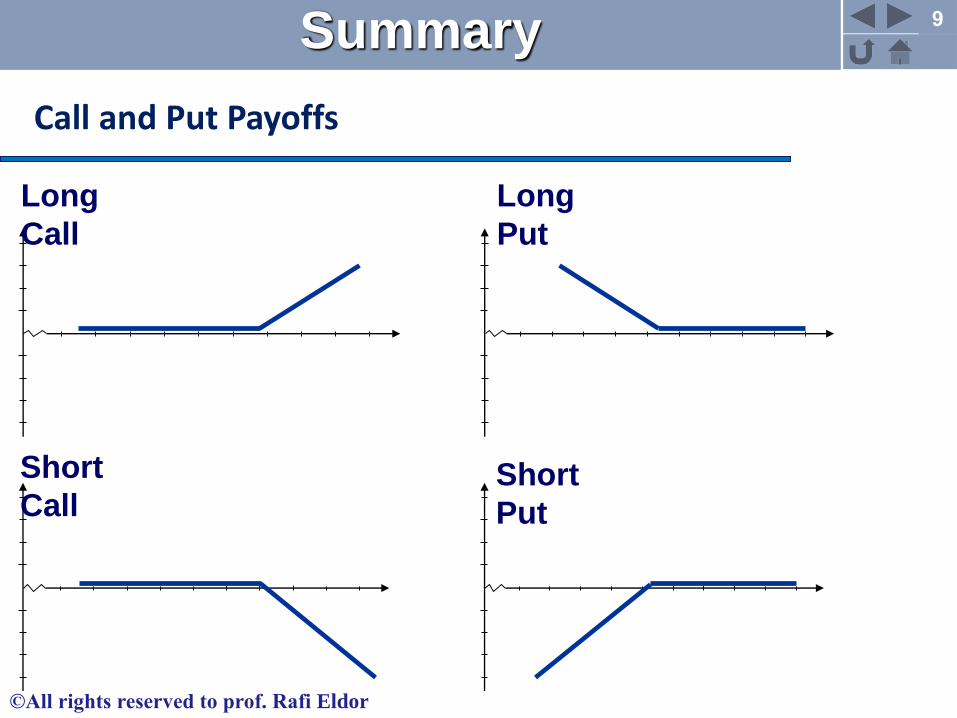

©All rights reserved to prof. Rafi Eldor

Spot

Profit

Spot

Profit

Long

Call

Short

Call

Spot

Profit

Spot

Profit

Long

Put

Short

Put

Call and Put Payoffs

Summary

10

©All rights reserved to prof. Rafi Eldor

Financial Alchemy With Options

Box Spread Strategy

Strategies: Bull Spread

Vanilla Strategies: Straddle, Strangle, Risk Reversal

Put Call Parity

Strategies

11

©All rights reserved to prof. Rafi Eldor

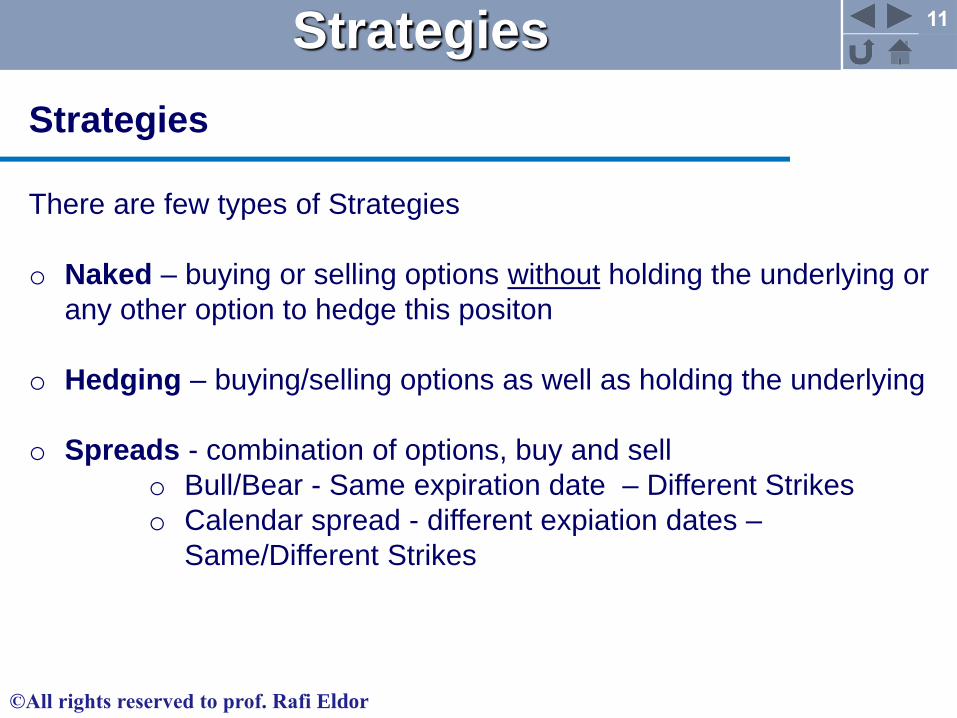

Strategies

There are few types of Strategies

o Naked – buying or selling options without holding the underlying or

any other option to hedge this positon

o Hedging – buying/selling options as well as holding the underlying

o Spreads - combination of options, buy and sell

o Bull/Bear - Same expiration date – Different Strikes

o Calendar spread - different expiation dates –

Same/Different Strikes

Strategies

12

©All rights reserved to prof. Rafi Eldor

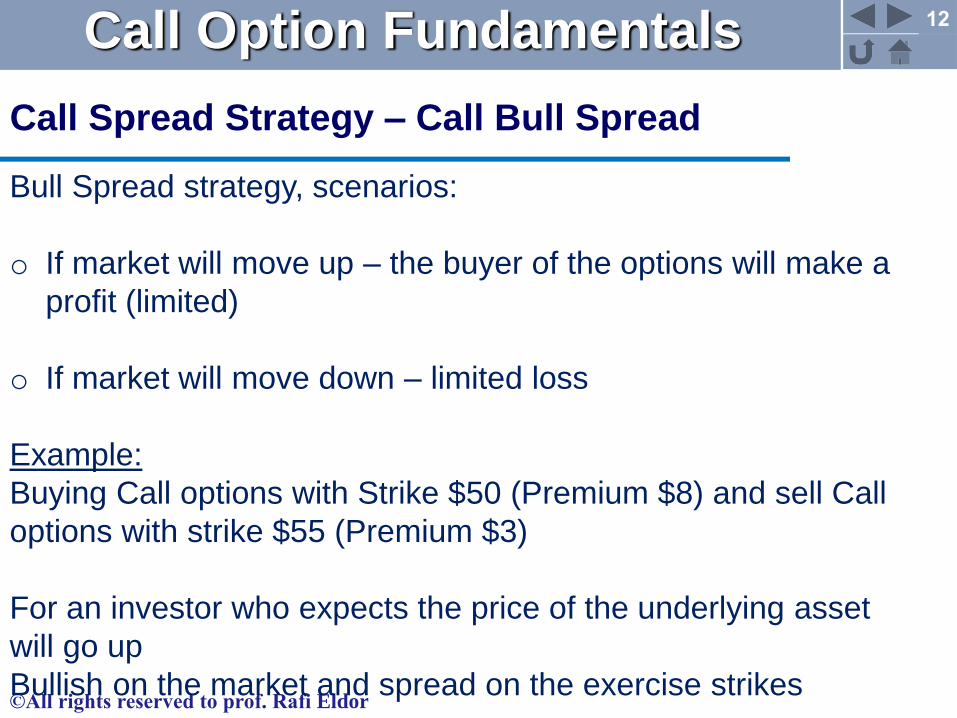

Call Spread Strategy – Call Bull Spread

Bull Spread strategy, scenarios:

o If market will move up – the buyer of the options will make a

profit (limited)

o If market will move down – limited loss

Example:

Buying Call options with Strike $50 (Premium $8) and sell Call

options with strike $55 (Premium $3)

For an investor who expects the price of the underlying asset

will go up

Bullish on the market and spread on the exercise strikes

Call Option Fundamentals

13

©All rights reserved to prof. Rafi Eldor

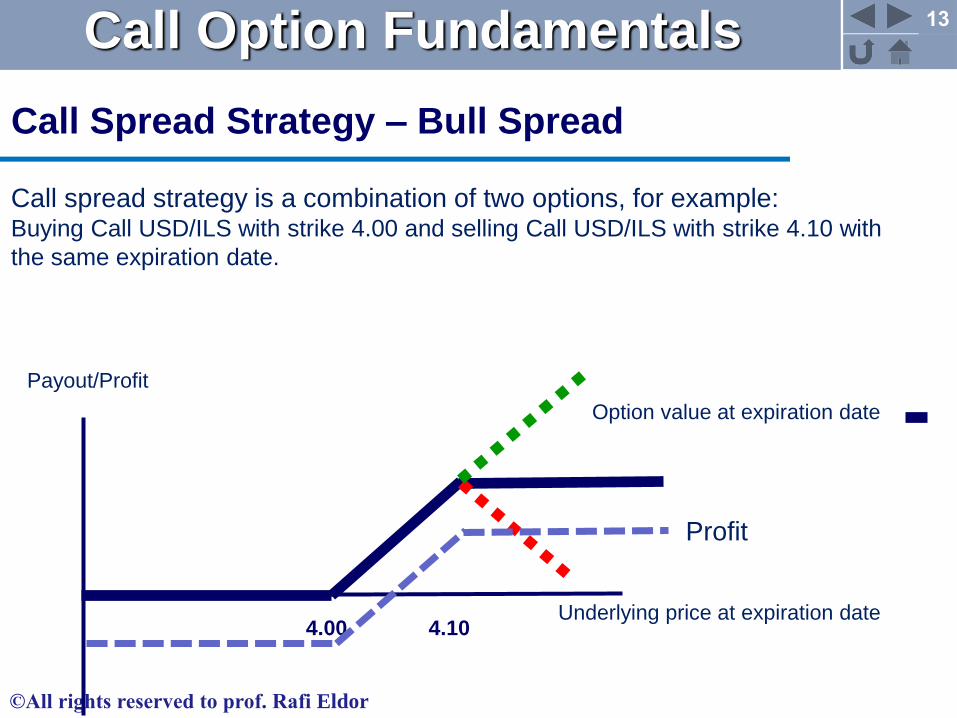

Call Spread Strategy – Bull Spread

Payout/Profit

Underlying price at expiration date

Option value at expiration date

Call spread strategy is a combination of two options, for example:Buying Call USD/ILS with strike 4.00 and selling Call USD/ILS with strike 4.10 with

the same expiration date.

Call Option Fundamentals

4.00 4.10

Profit

14

©All rights reserved to prof. Rafi Eldor

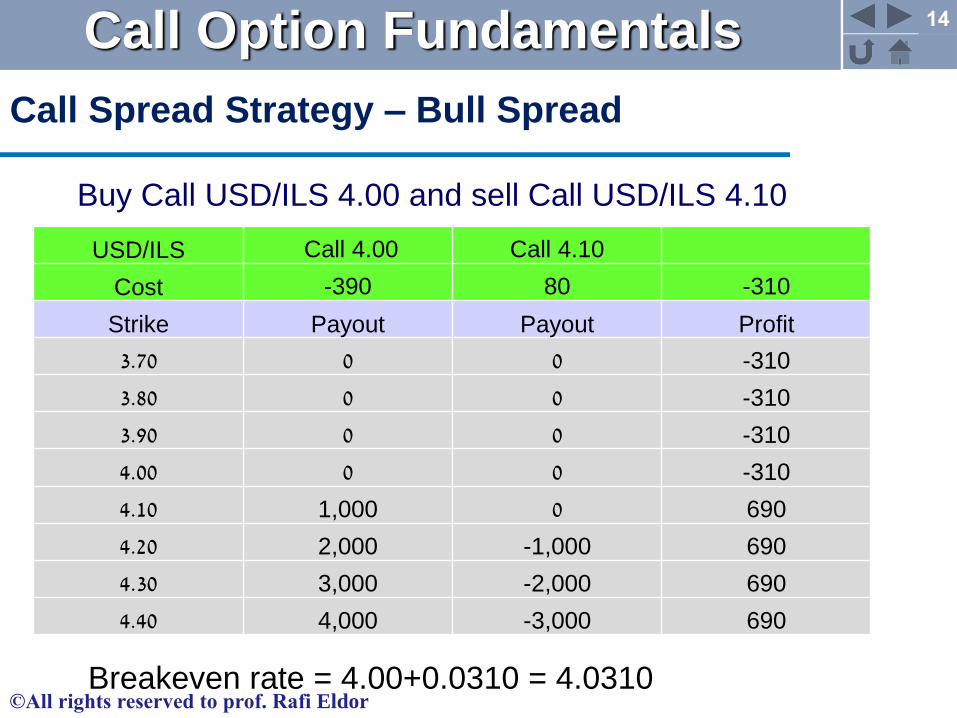

Call Spread Strategy – Bull Spread

Call Option Fundamentals

USD/ILS Call 4.00 Call 4.10

Cost -390 80 -310

Strike Payout Payout Profit

3.70 0 0 -310

3.80 0 0 -310

3.90 0 0 -310

4.00 0 0 -310

4.10 1,000 0 690

4.20 2,000 -1,000 690

4.30 3,000 -2,000 690

4.40 4,000 -3,000 690

Breakeven rate = 4.00+0.0310 = 4.0310

Buy Call USD/ILS 4.00 and sell Call USD/ILS 4.10

15

©All rights reserved to prof. Rafi Eldor

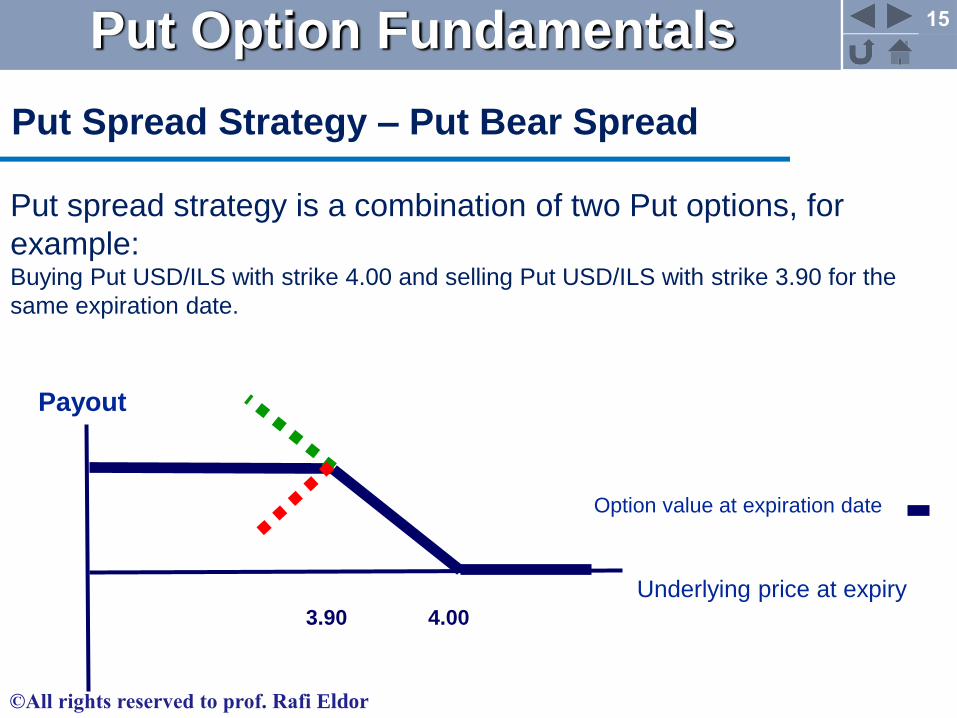

Put Spread Strategy – Put Bear Spread

Payout

Underlying price at expiry

Option value at expiration date

Put spread strategy is a combination of two Put options, for

example:Buying Put USD/ILS with strike 4.00 and selling Put USD/ILS with strike 3.90 for the

same expiration date.

Put Option Fundamentals

3.90 4.00

16

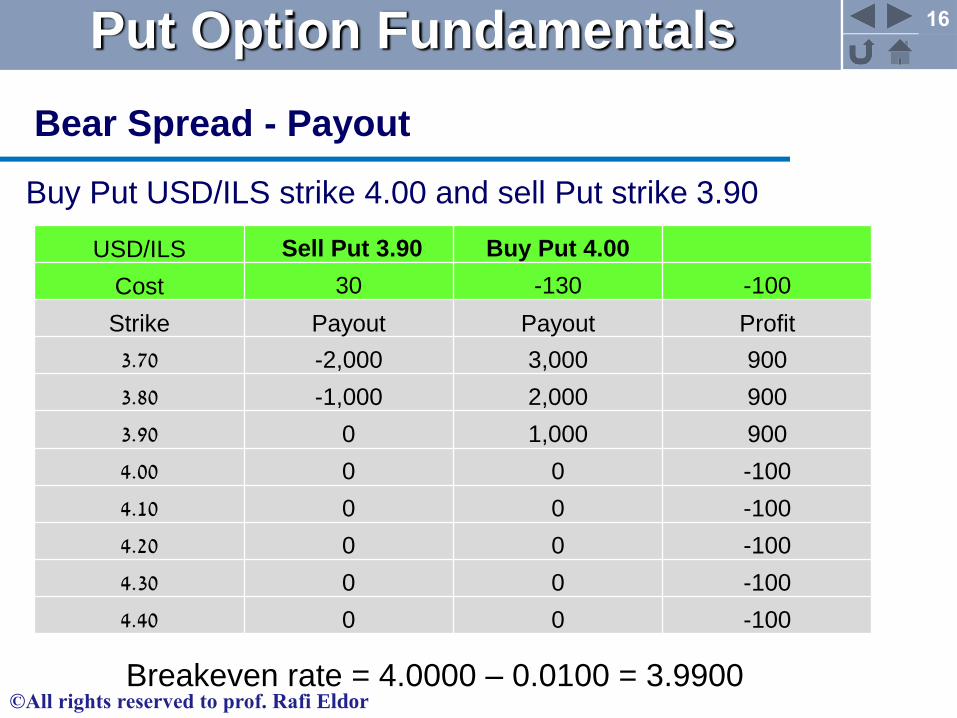

©All rights reserved to prof. Rafi Eldor

Buy Put USD/ILS strike 4.00 and sell Put strike 3.90

Put Option Fundamentals

USD/ILS Sell Put 3.90 Buy Put 4.00

Cost 30 -130 -100

Strike Payout Payout Profit

3.70 -2,000 3,000 900

3.80 -1,000 2,000 900

3.90 0 1,000 900

4.00 0 0 -100

4.10 0 0 -100

4.20 0 0 -100

4.30 0 0 -100

4.40 0 0 -100

Breakeven rate = 4.0000 – 0.0100 = 3.9900

Bear Spread - Payout

17

©All rights reserved to prof. Rafi Eldor

Straddle

A straddle is a vanilla strategy, it can be either of the following:

Buying a StraddleBuying a Call option and buying a Put option, both with the same

strike, expiration date and notional amount.

Selling a StraddleSelling a Call option and selling a Put option, both with the same

strike, expiration date and notional amount.

Strategies

18

©All rights reserved to prof. Rafi Eldor

Straddle

Long Straddle

Buying a Straddle (Long Straddle)

For an investor who wants to profit from a volatile market

Buy a Call option and a Put option with the same strikes,

same notional amount and for the same expiration date

For example: an investor will buy Call option with strike

$50 (premium $5) and a Put option with strike of $50

(premium $3), expiration date in 1 year.

19

©All rights reserved to prof. Rafi Eldor

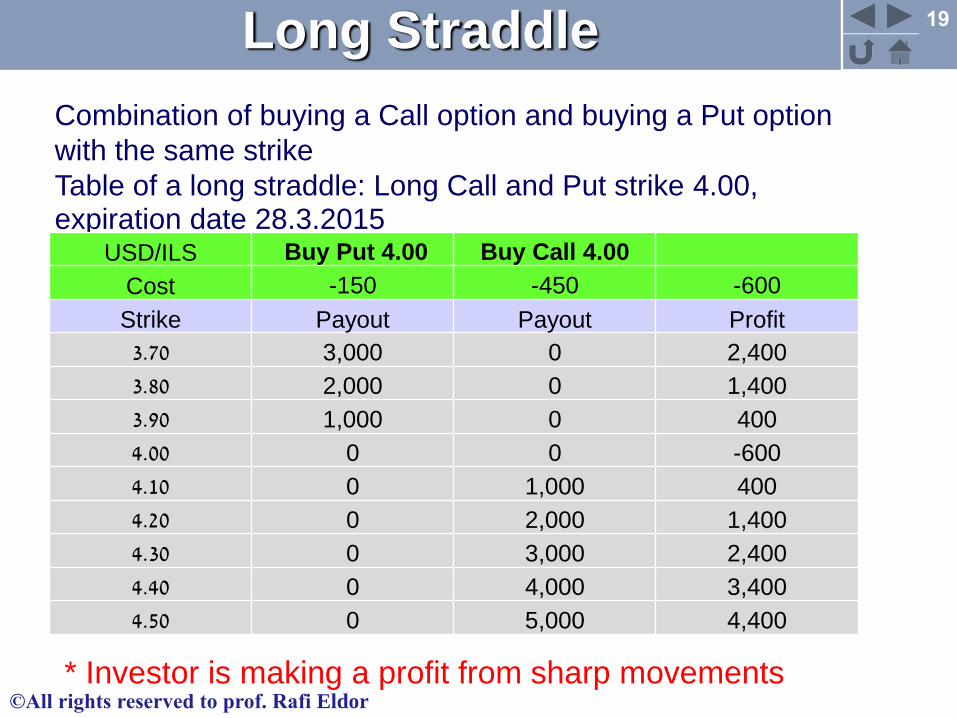

Long Straddle

Combination of buying a Call option and buying a Put option

with the same strike

Table of a long straddle: Long Call and Put strike 4.00, expiration date 28.3.2015

USD/ILS Buy Put 4.00 Buy Call 4.00

Cost -150 -450 -600

Strike Payout Payout Profit

3.70 3,000 0 2,400

3.80 2,000 0 1,400

3.90 1,000 0 400

4.00 0 0 -600

4.10 0 1,000 400

4.20 0 2,000 1,400

4.30 0 3,000 2,400

4.40 0 4,000 3,400

4.50 0 5,000 4,400

* Investor is making a profit from sharp movements

20

©All rights reserved to prof. Rafi Eldor

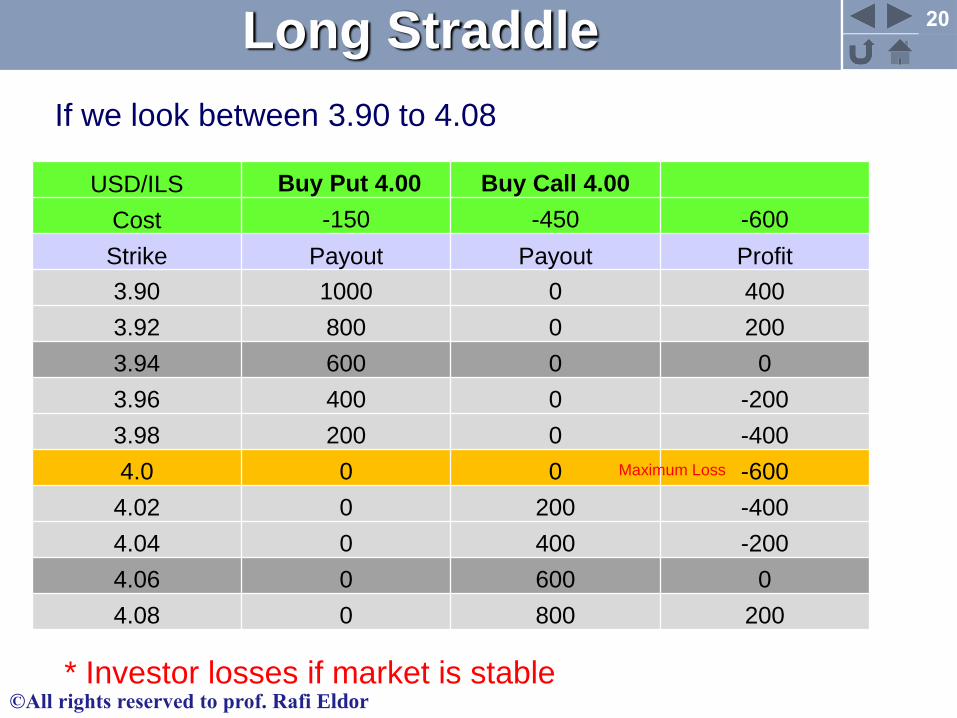

Long Straddle

If we look between 3.90 to 4.08

USD/ILS Buy Put 4.00 Buy Call 4.00

Cost -150 -450 -600

Strike Payout Payout Profit

3.90 1000 0 400

3.92 800 0 200

3.94 600 0 0

3.96 400 0 -200

3.98 200 0 -400

4.0 0 0 -600

4.02 0 200 -400

4.04 0 400 -200

4.06 0 600 0

4.08 0 800 200

Maximum Loss

* Investor losses if market is stable

21

©All rights reserved to prof. Rafi Eldor

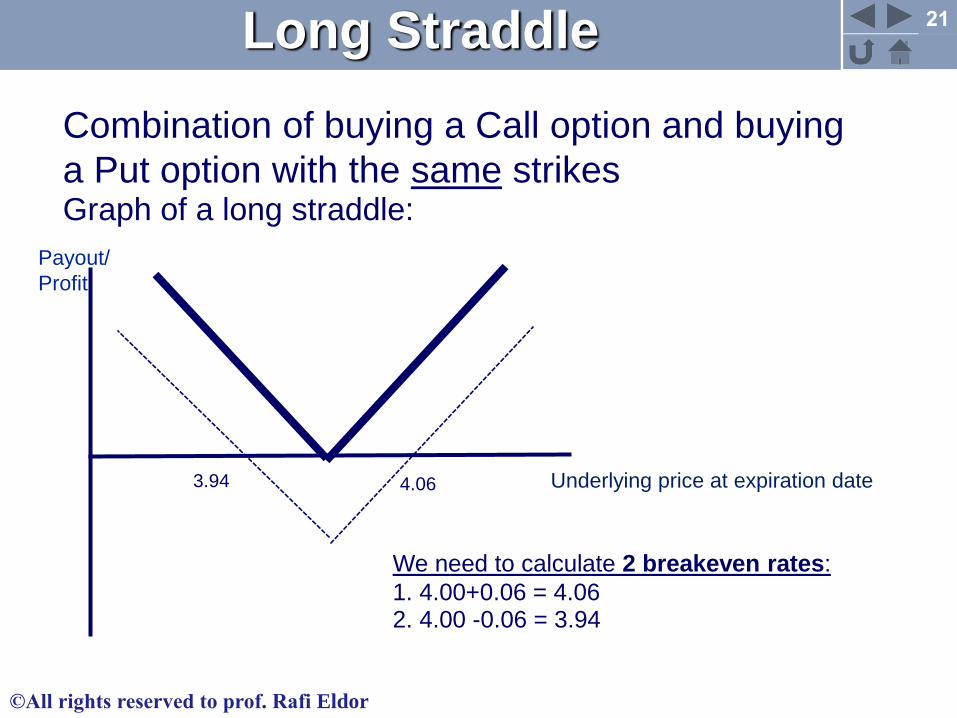

Long Straddle

Combination of buying a Call option and buying

a Put option with the same strikes Graph of a long straddle:

Payout/

Profit

Underlying price at expiration date

We need to calculate 2 breakeven rates:

1. 4.00+0.06 = 4.062. 4.00 -0.06 = 3.94

4.063.94

22

©All rights reserved to prof. Rafi Eldor

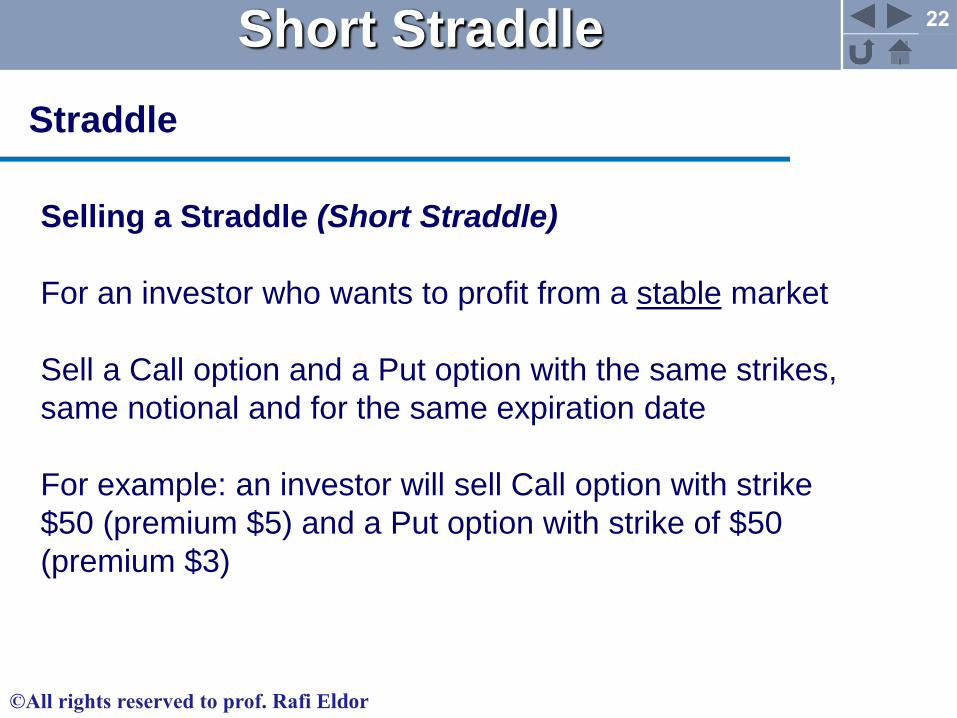

Straddle

Selling a Straddle (Short Straddle)

For an investor who wants to profit from a stable market

Sell a Call option and a Put option with the same strikes,

same notional and for the same expiration date

For example: an investor will sell Call option with strike

$50 (premium $5) and a Put option with strike of $50

(premium $3)

Short Straddle

23

©All rights reserved to prof. Rafi Eldor

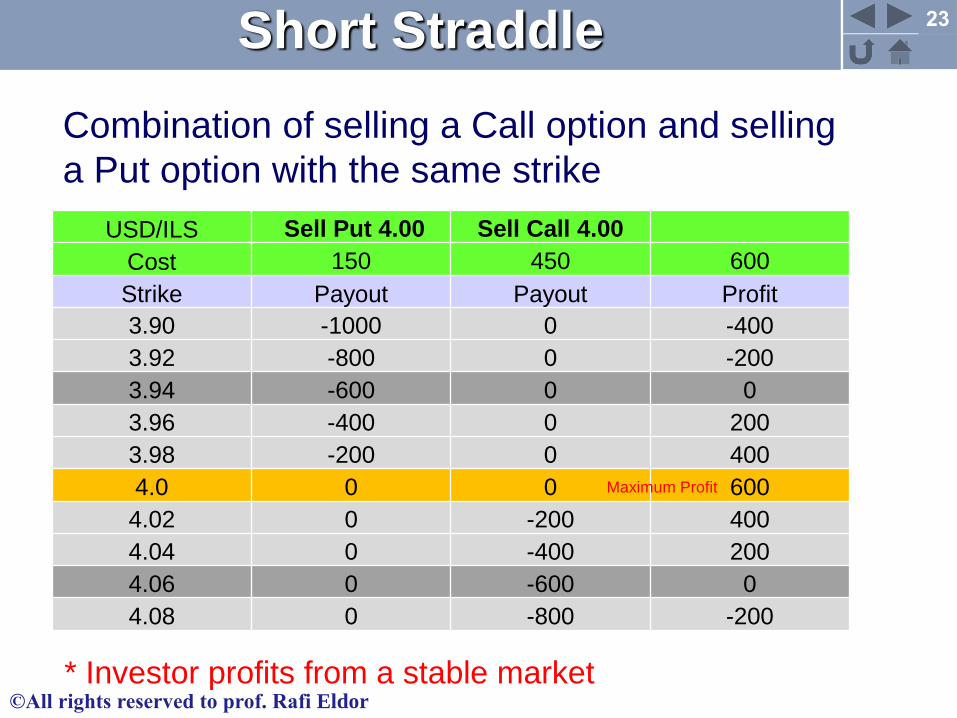

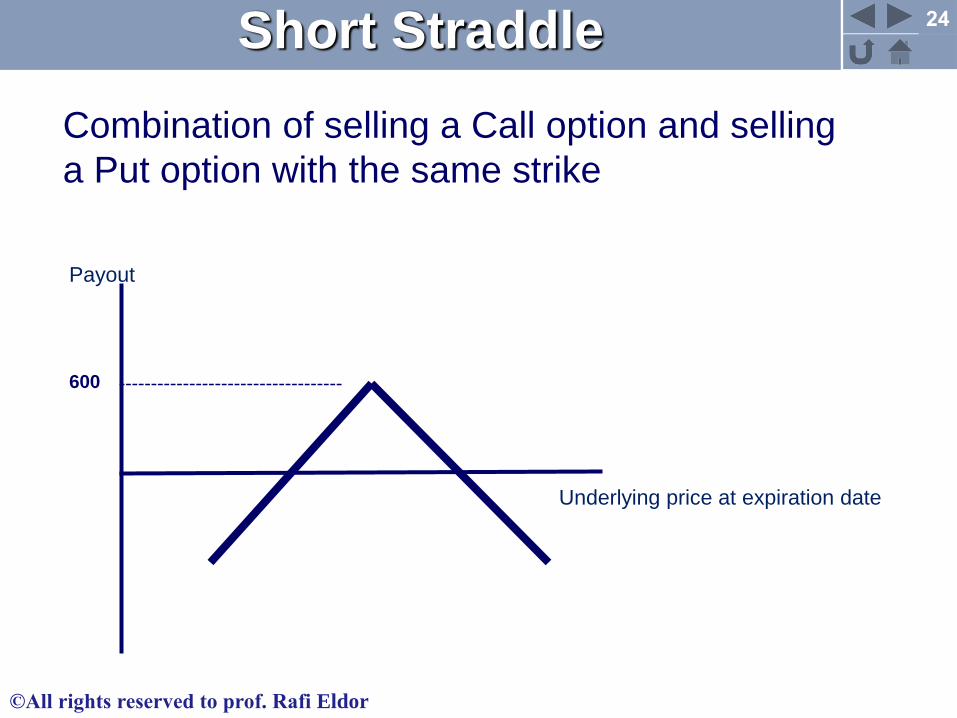

Short Straddle

Combination of selling a Call option and selling

a Put option with the same strike

USD/ILS Sell Put 4.00 Sell Call 4.00

Cost 150 450 600

Strike Payout Payout Profit

3.90 -1000 0 -400

3.92 -800 0 -200

3.94 -600 0 0

3.96 -400 0 200

3.98 -200 0 400

4.0 0 0 600

4.02 0 -200 400

4.04 0 -400 200

4.06 0 -600 0

4.08 0 -800 -200

Maximum Profit

* Investor profits from a stable market

24

©All rights reserved to prof. Rafi Eldor

Short Straddle

Combination of selling a Call option and selling

a Put option with the same strike

Payout

Underlying price at expiration date

600

25

©All rights reserved to prof. Rafi Eldor

Strangle

Strangle

A strangle is a vanilla strategy. It can be either of the following:

Long Strangle

Buying the Strangle. This involves buying a call option and

buying a put option, both with different strikes but with the same

expiration date and notional amount.

Short Strangle

Selling the strangle. This involves selling a call option and

selling a put option, both with different strikes but with the same

expiry date and notional.

26

©All rights reserved to prof. Rafi Eldor

Strangle

Strangle

Why buy a strangle?

Like the straddle, the long strangle position expresses a view

that the prices will move (in which direction is irrelevant).

However, because the price needs to move further than with a

straddle the strangle is cheaper.

Strangles are commonly described as 25 delta, 15 delta and so on, volatility

quotes for strangles are used as benchmarks to create a volatility surface

(we will discuss that later in the course).

27

©All rights reserved to prof. Rafi Eldor

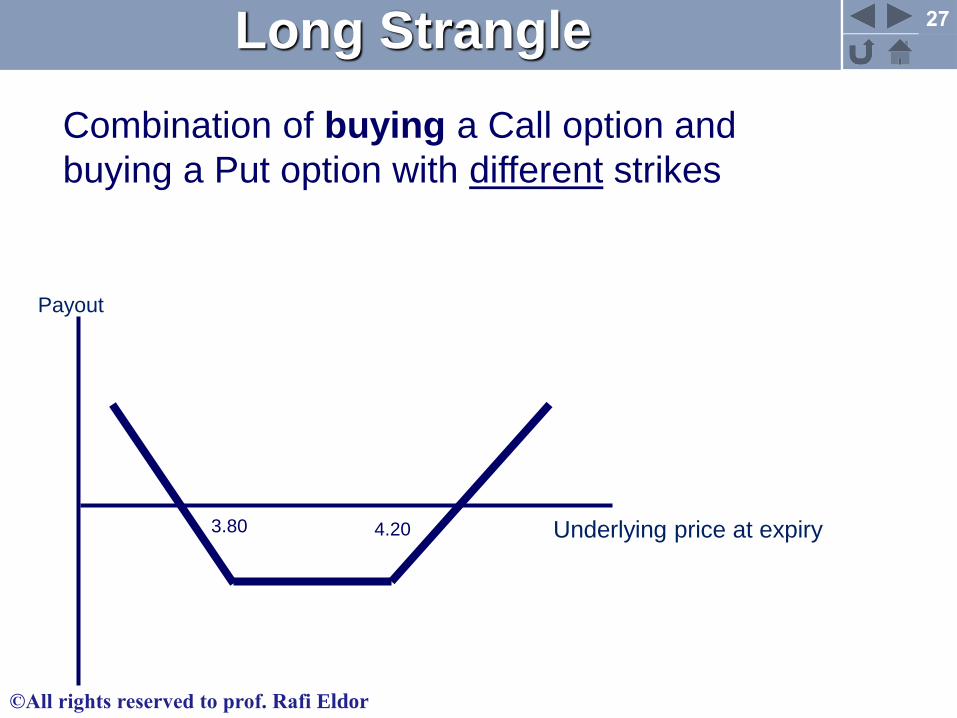

Long Strangle

Payout

Underlying price at expiry

Combination of buying a Call option and

buying a Put option with different strikes

4.203.80

28

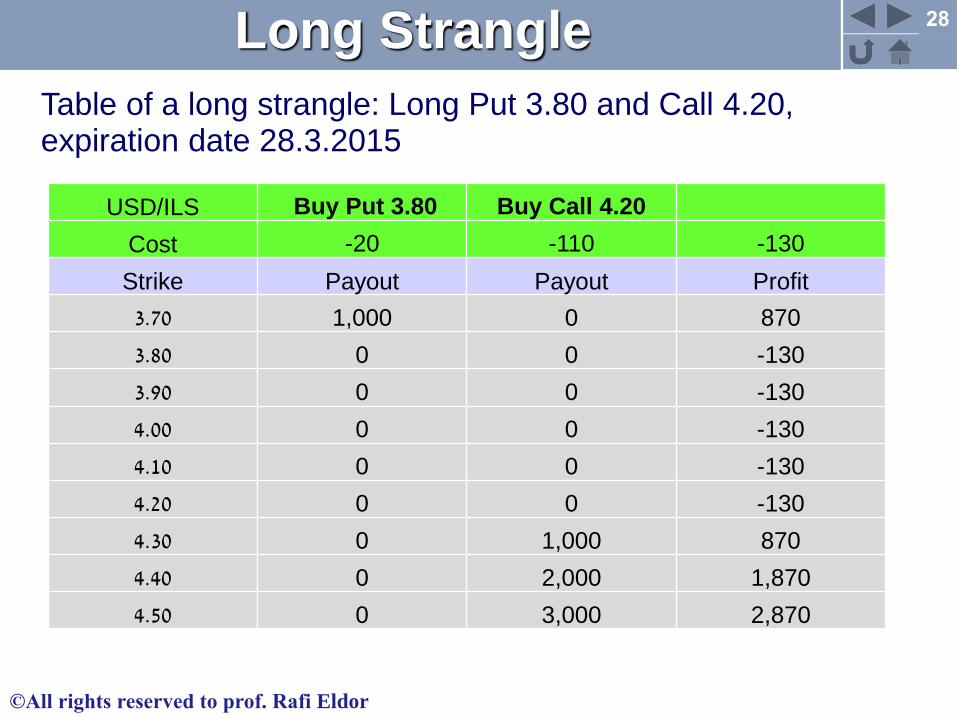

©All rights reserved to prof. Rafi Eldor

Long Strangle

USD/ILS Buy Put 3.80 Buy Call 4.20

Cost -20 -110 -130

Strike Payout Payout Profit

3.70 1,000 0 870

3.80 0 0 -130

3.90 0 0 -130

4.00 0 0 -130

4.10 0 0 -130

4.20 0 0 -130

4.30 0 1,000 870

4.40 0 2,000 1,870

4.50 0 3,000 2,870

Table of a long strangle: Long Put 3.80 and Call 4.20, expiration date 28.3.2015

29

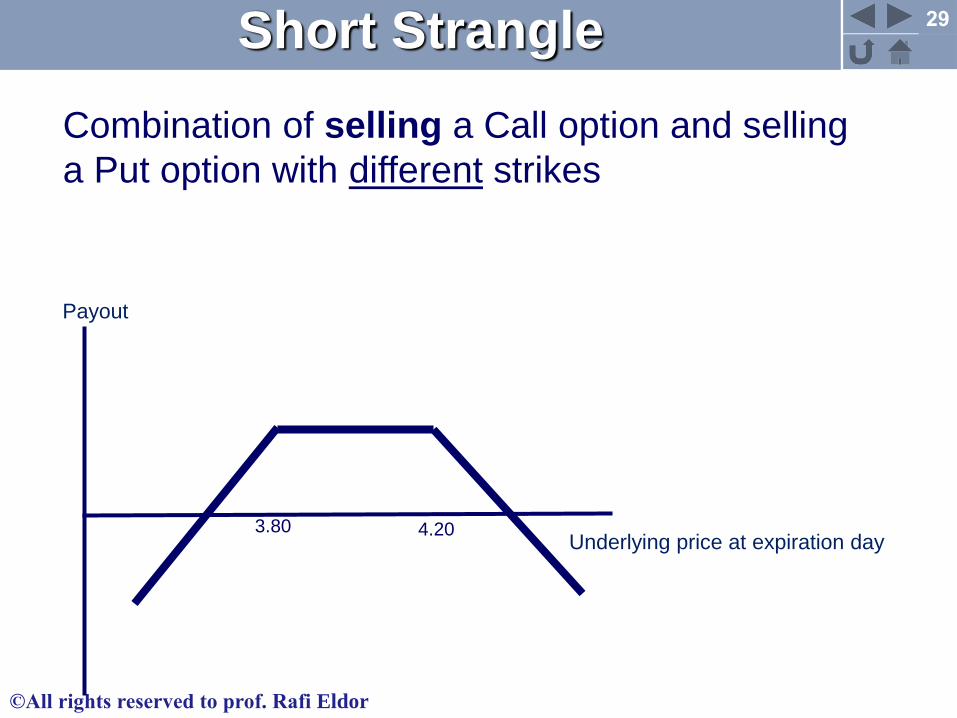

©All rights reserved to prof. Rafi Eldor

Short Strangle

Payout

Underlying price at expiration day

Combination of selling a Call option and selling

a Put option with different strikes

4.203.80

30

©All rights reserved to prof. Rafi Eldor

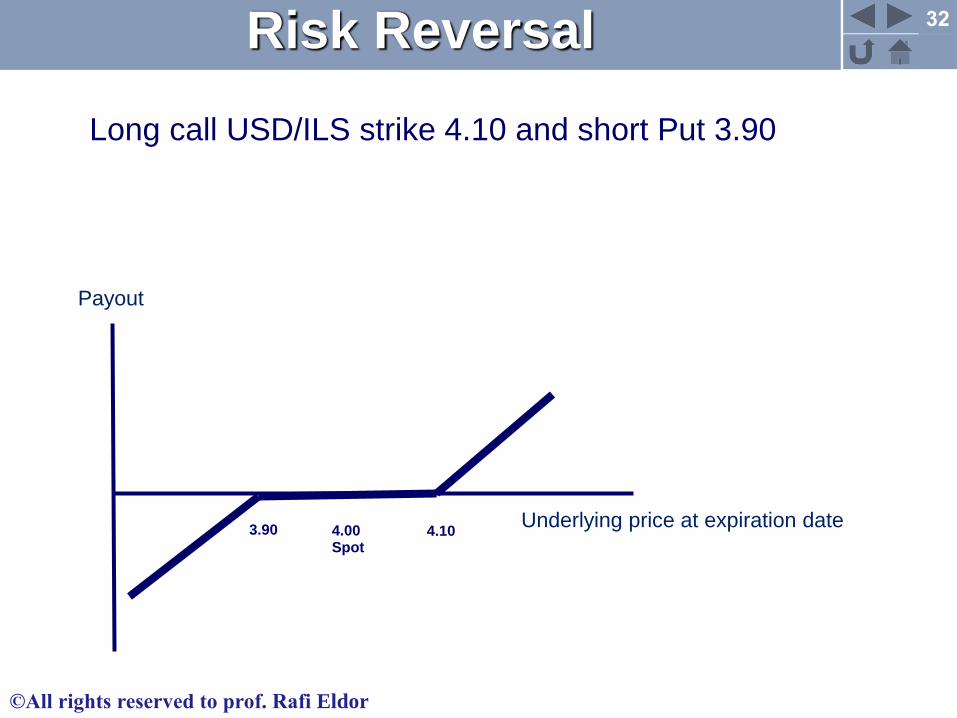

Risk Reversal

Risk Reversal

What is Risk Reversal?

A Vanilla Strategy combined from a long position on a Call

option and short position on a Put option (or vice versa), both

options with the same expiration date and with the same

notional amount.

Long Risk Reversal - Buy Call and sell Put with different strikes

Short Risk Reversal – Sell Call and buy Put with different strikes

31

©All rights reserved to prof. Rafi Eldor

Risk Reversal

Risk Reversal

Why use a Risk Reversal?

Hedge – the buyer of the Risk Reversal can hedge himself from

a higher spot rate.

Lower cost – buying a Risk Reversal is cheaper than buying

only a Call option.

“Zero cost Risk Reversal” – very popular, being used mostly by

corporates, combination of two options with the same premium.

32

©All rights reserved to prof. Rafi Eldor

Risk Reversal

Payout

Underlying price at expiration date

Long call USD/ILS strike 4.10 and short Put 3.90

4.103.90 4.00Spot

33

©All rights reserved to prof. Rafi Eldor

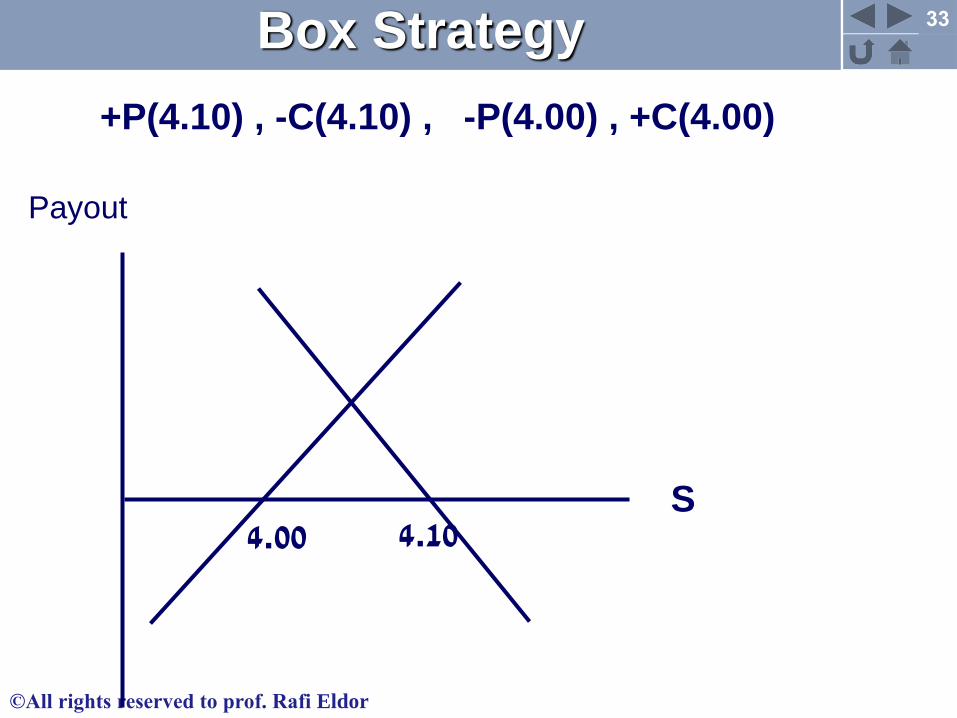

Box Strategy

+P(4.10) , -C(4.10) , -P(4.00) , +C(4.00)

S

Payout

4.00 4.10

34

©All rights reserved to prof. Rafi Eldor

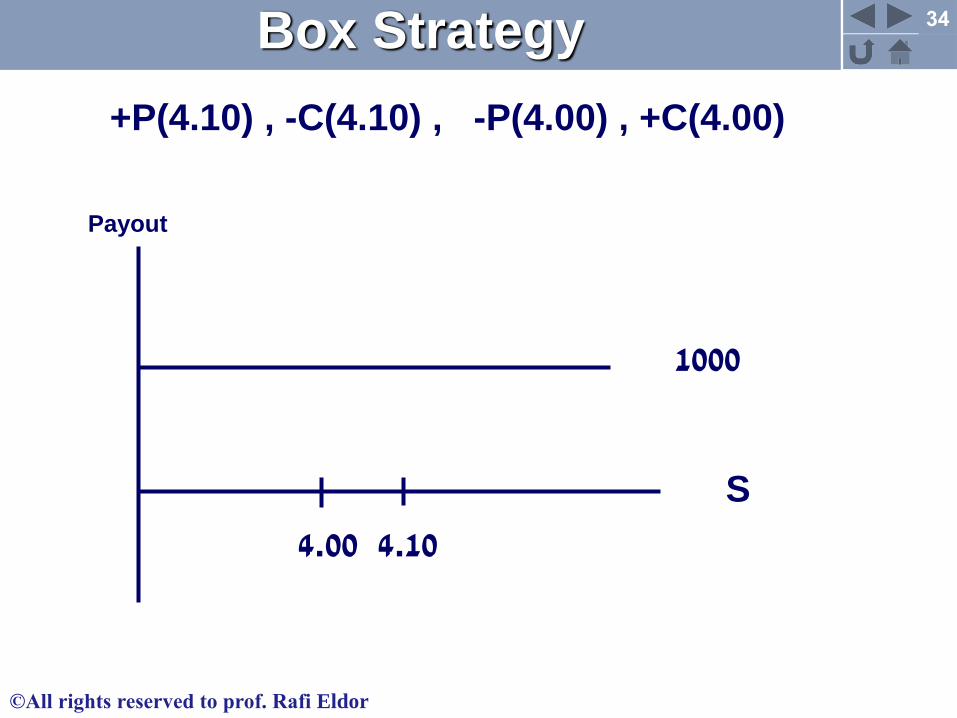

Box Strategy

+P(4.10) , -C(4.10) , -P(4.00) , +C(4.00)

4.00 4.10

S

1000

Payout

35

©All rights reserved to prof. Rafi Eldor

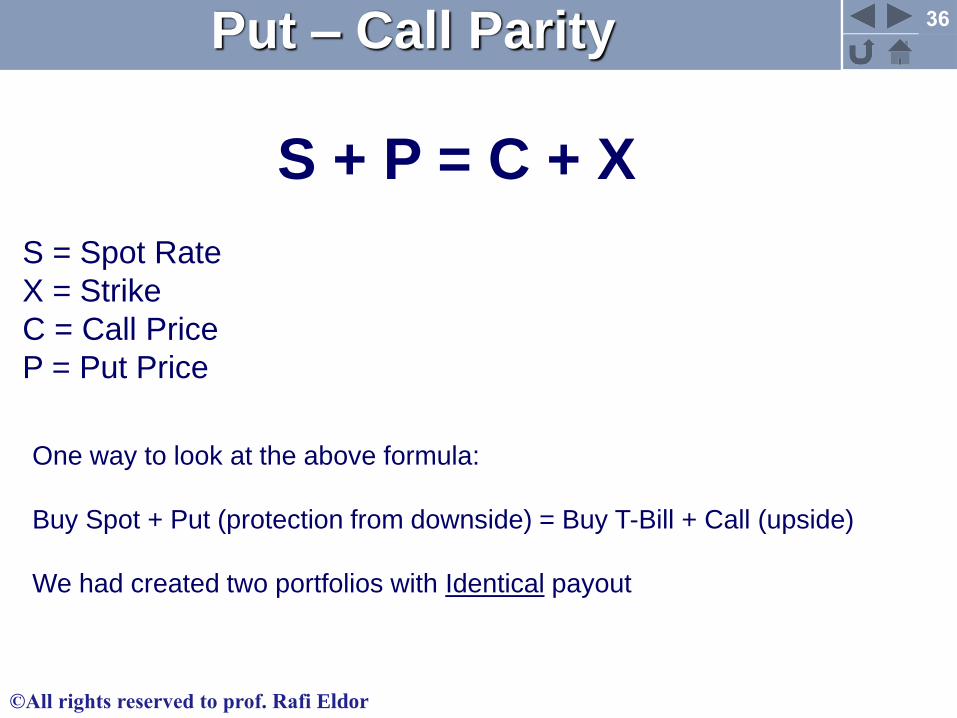

Put – Call Parity is a principle referring to the relationship between the

prices of European Call option and a Put option with the same strike,

expirations date and underlying asset.

If this relationship doesn’t exist => Arbitrage opportunity

We will compare to portfolios:

1. A portfolio comprising from a Call option and an amount of cash

equal to the present value of the option's strike price

2. A portfolio comprising from a Put option and the underlying asset

Both options have the same expiration date and strikes.

Put – Call Parity

Definition

36

©All rights reserved to prof. Rafi Eldor

S + P = C + X

S = Spot Rate

X = Strike

C = Call Price

P = Put Price

One way to look at the above formula:

Buy Spot + Put (protection from downside) = Buy T-Bill + Call (upside)

We had created two portfolios with Identical payout

Put – Call Parity

37

©All rights reserved to prof. Rafi Eldor

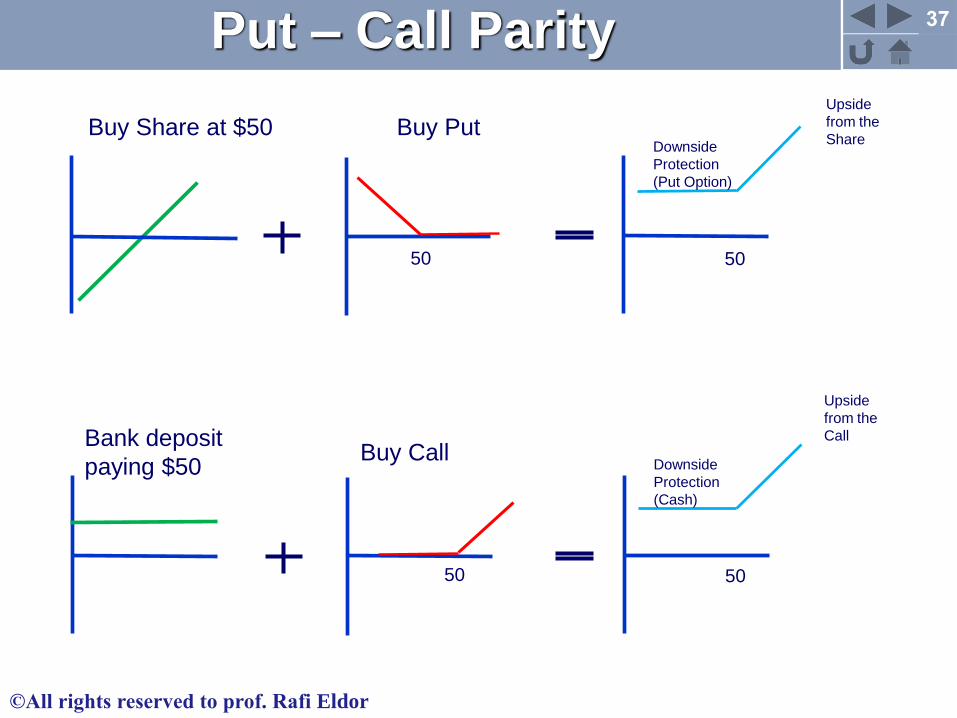

Put – Call Parity

Buy Share at $50 Buy Put

50

Downside

Protection

(Put Option)

Bank deposit

paying $50Buy Call

50

Downside

Protection

(Cash)

50

50

Upside

from the

Share

Upside

from the

Call

38

©All rights reserved to prof. Rafi Eldor

Practical use of Put Call Parity in USD/ILS

Market

Buy (or sell) synthetic forward and Sell (buy)

spot

*Remember Underlying is Forward not Spot

Transaction cost

Exchange options are Non- delivery

Put – Call Parity

39

©All rights reserved to prof. Rafi Eldor

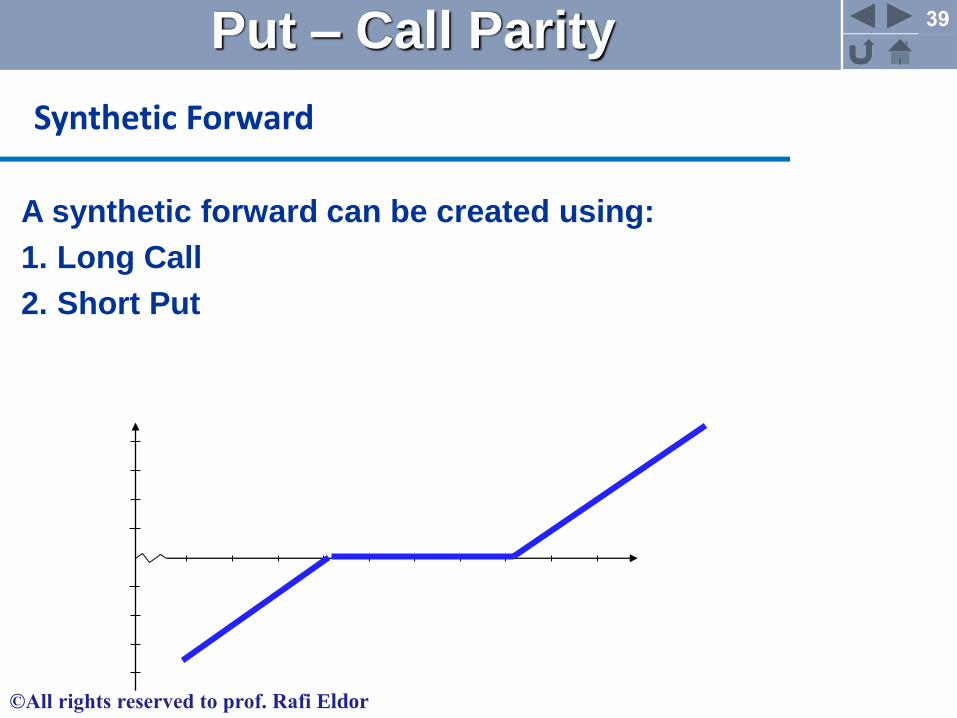

A synthetic forward can be created using:

1. Long Call

2. Short Put

Spot

Profit

Synthetic Forward

Put – Call Parity

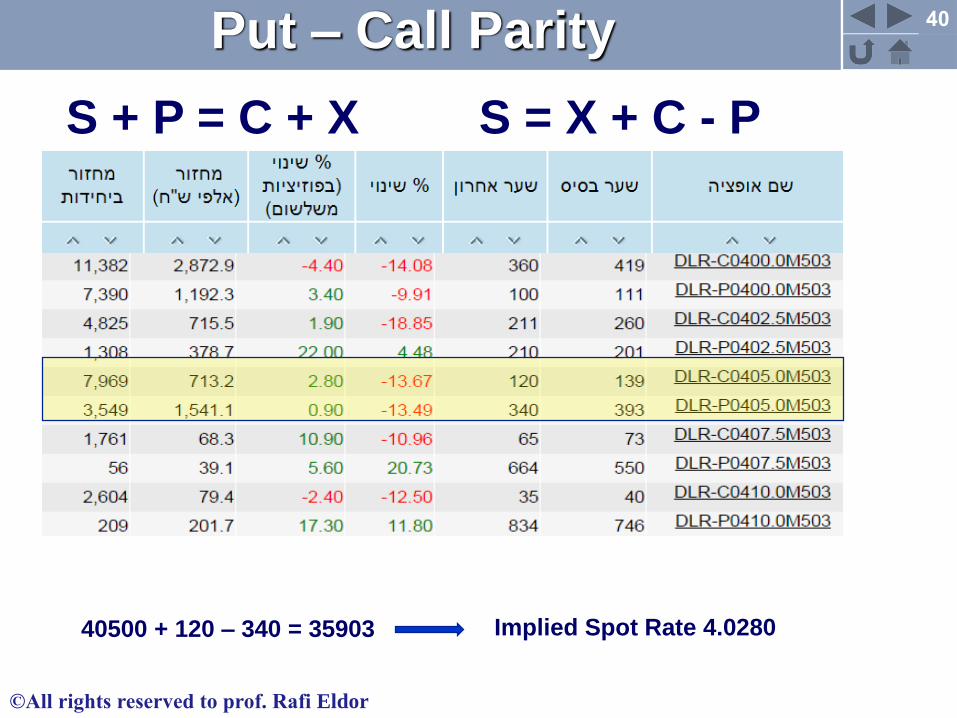

40

©All rights reserved to prof. Rafi Eldor

S + P = C + X S = X + C - P

40500 + 120 – 340 = 35903 Implied Spot Rate 4.0280

Put – Call Parity