Option Internationale du Baccalauréat (OIB), France Version ...

Upload

ngoc-nguyen-hongCategory

view

212download

0

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 1/159

SET50 Index OptionsSET50 Index Options

FIN 4931

SEMINAR IN INVESTMENT

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 2/159

SET50 Index OptionsHandbook: Unlocking the power

of profitable investment

Dr. Teerasak Naranong

(PhD in Finance, UK) Lecturer, Finance Department

Assumption University (ABAC)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 3/159

Topics

1. What is Option ?

2. SET50 Index Option

3. Factor affecting the SET50 Index Options

4. Investors in Options

5. In action (Investors’ Review)6. Trading Strategies in SET50 Options

- Basic Strategies

- Intermediate Strategies

- Advanced Strategies

7. Margin Calculation

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 4/159

Derivative trades in TFEX

SET50 Futures

28 April 2006

SET50 Options

SET50 Call Options SET50 Put Options

29 October 2007

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 5/159

Option → An option grants an investor (Option holder) the right to buy/not

buy or sell/not sell the underlying asset at fixed price (exercise price or strike

price) on or before a specific point in time (expiration date or exercise date)

→ Option holder pay the price of the option called “option price”

or “option premium”

1. What is Options?

Premium

Option (right)

Option writer

(Short position)

Option holder

(Long position)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 6/159

Components of Options

„ Call Options or Put Options

„ Underlying Asset, S

„ Exercise Price or Strike Price, X

„ Expiration date or Maturity Date, T)

„Contract Size

„ Option Premium

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 7/159

1. Call option→

An option (right) to buy an asset ( underlying asset )at a fixed price ( exercise price )

on or before the maturity date(expiration date)

→ No obligation for buyer or holder

2. Put option → An option (right) to sell an asset ( underlying asset )

at a fixed price ( exercise price )

on or before the maturity date(expiration date)

→ No obligation for buyer or holder

2 Types of Options (right)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 8/159

Right and Obligation

Call Options Put Options

Holder (Long) Writer (Short) Holder (Long) Writer (Short)

Right

And

Obligation

(RIGHT TO BUY)

(OBLIGATION

TO SELL)(RIGHT TO

SELL)

(OBLIGATION

TO BUY)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 9/159

When will we exercise ?

AT THE

EXPIRATION DATE ST> X S

T< X

Call Options

Put Options

EXERCISE

NO

NO

EXERCISE

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 10/159

the right to buy (Call) the right to sell (Put)

Profit when the price Profit when the price

increases decreases

St

St

Time Time

XX

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 11/159

1. European option

→ Option holder can exercise only on the expiration date

( SET50 INDEX OPTION )

Expiration date of Options

2. American option

→ Option holder can exercise any time up to and including the

expiration date

3. Pseudo American option

→ Option holder can exercise at the fixed interval date (eg at the end of

week, month or quarter.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 12/159

Expiration DateBegin Time to maturity

European Options (SET 50 Index Options)

American Options S&P 500

Pseudo-American Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 13/159

1) In The Money: ITM (Intrinsic Value > 0)

Call Option: ( Spot Price, S ) > (exercise price, X ) ;

Put Option: ( Spot Price, S ) < (exercise price, X )

2) At The Money: ATM (Intrinsic Value = 0) Call และ Put Options: (S) =( X )

3) Out of the Money: OTM (Intrinsic Value = 0)

Call Option: (S) < ( X ) ;

Put Option: (S) > ( X )

Intrinsic value of Option (Moneyness)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 14/159

Intrinsic value of option (Moneyness)

St > X St = X St <X

ITM Call or OTM Put ATM Call and Put OTM Call or ITM Put

ITM = In-the-money : Intrinsic Value > 0 ATM = At-the-money : Intrinsic Value = 0

OTM = Out-of-the-money : Intrinsic Value = 0

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 15/159

X INTRINSIC VALUE X INTRINSIC VALUE

490 490

500 500

510 510

Call Option Put Option

St = 500 B ATM = At-the-money

ITM = In-the-money

OTM = Out-of-the-money

ITM

OTM

ATM

ITM

OTM

ATM

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 16/159

2. SET50 Index Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 17/159

SET50 Index

„ SET50 Index is an index of 50 securities. Stocks in SET50Index have following qualification:

1) Market cap of the company must be high.

2) High liquidity stocks with regular high trading volume

3) Listed in the market at least 6 months

4) The Stock Exchange will adjust names of stocks selected for

calculation every 6 months (In June for last 6 mths and Dec.

for first 6 mths)

5) In calculating SET50 Index, weight of each stock will depend

on the market cap of that stock

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 18/159

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 19/159

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 20/159

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 21/159

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 22/159

SET50 Index Options

► Is a derivatives that has the underlying assets as SET50 Index

„ pay as cash settlement

Multiplier

To calculate into cash settlement

„ cash settlement = SET50 Index X Multiplier

100,000 Baht = 500 x 200

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 23/159

SET50 Index Futures VS SET50 Index Options

SET50 Index Futures Specifications

SET50 Index Options Specifications

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 24/159

SET50 Index Futures

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 25/159

►SET50 Index Futures

SET50 Index Futures

SET50 + FUTURES

=

SET50 INDEX FUTURES

SET50 Index

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 26/159

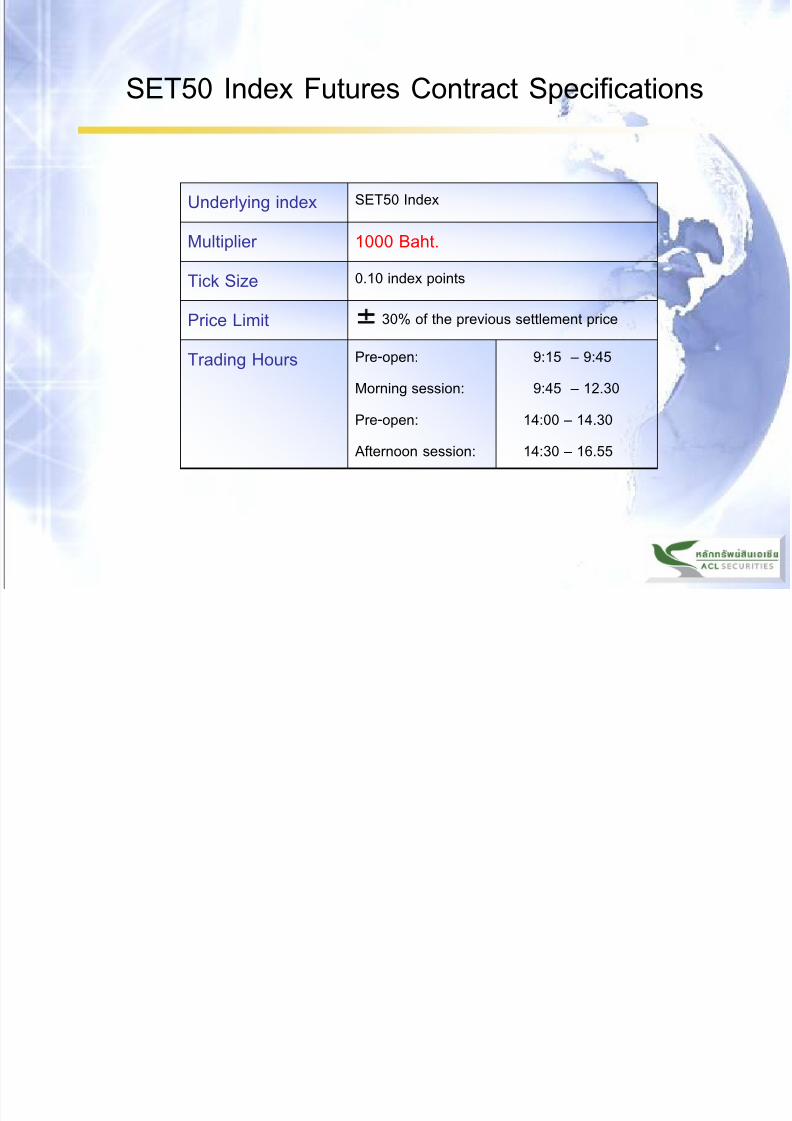

SET50 Index Futures Contract Specifications

Underlying index SET50 Index

Multiplier 1000 Baht.

Tick Size 0.10 index points

Price Limit 30% of the previous settlement price

Trading Hours Pre-open:

Morning session:

Pre-open:

Afternoon session:

9:15 – 9:45

9:45 – 12.30

14:00 – 14.30

14:30 – 16.55

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 27/159

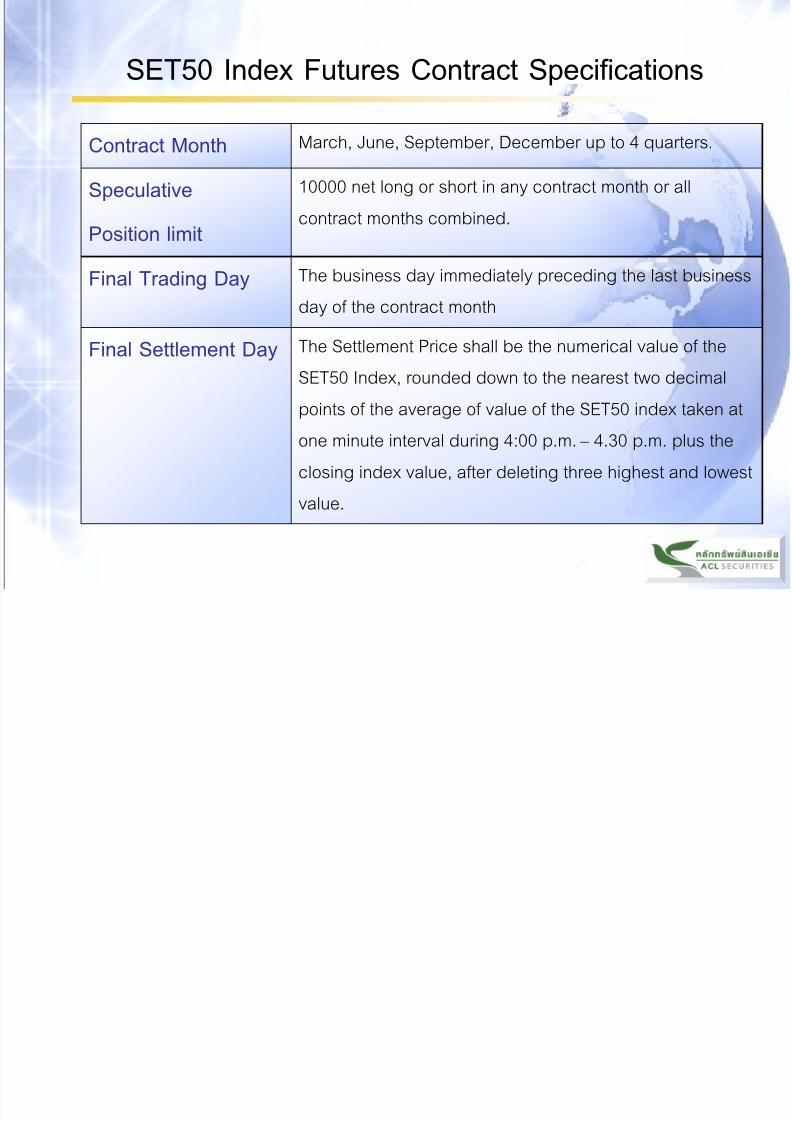

Contract Month March, June, September, December up to 4 quarters.

Speculative

Position limit

10000 net long or short in any contract month or all

contract months combined.

Final Trading Day The business day immediately preceding the last businessday of the contract month

Final Settlement Day The Settlement Price shall be the numerical value of the

SET50 Index, rounded down to the nearest two decimal

points of the average of value of the SET50 index taken atone minute interval during 4:00 p.m. ‟ 4.30 p.m. plus the

closing index value, after deleting three highest and lowest

value.

SET50 Index Futures Contract Specifications

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 28/159

SET50 Index Options

Specifications

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 29/159

Contract Specification

Underlying Asset SET50 Index

Multiplier 200 Thai Baht per Index Point

Exercise Style European Style

Contract Month March, June, September, December

Trading Hour Pre-Open: 9.15 a.m.-9.45 a.m.Morning Session: 9.45 a.m.-12.30 p.m.

Pre-Open: 14.00 p.m.-14.30 p.m.

Afternoon Session:14.30 p.m.-16.55 p.m.

Strike Price

Interval

10 Points. At the commencement of trading in a contract month, theExchange shall

List five series which are in-the-money and five series which are out-of-the-money plus one at-the-money series. New series are added tomaintain 5 strike prices above and strike price below the at-the-money strike

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 30/159

St(SET50 INDEX)= 500

March (H), June (M), September (U), December (Z)

Call OptionS50Z09C450 ITM

S50Z09C460 ITM

S50Z09C470 ITM

S50Z09C480 ITM

S50Z09C490 ITM

S50Z09C500 ATM

S50Z09C510 OTM

S50Z09C520 OTM

S50Z09C530 OTM

S50Z09C540 OTM

S50Z09C550 OTM

Put OptionS50Z09P450 OTM

S50Z09P460 OTM

S50Z09P470 OTM

S50Z09P480 OTM

S50Z09P490 OTM

S50Z09P500 ATM

S50Z09P510 ITM

S50Z09P520 ITM

S50Z09P530 ITM

S50Z09P540 ITM

S50Z09P550 ITM

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 31/159

Contract Specification

Tick Size 0.1 index points

Final Settlement

Price

The Final Settlement price shall be the average value of the SET50Index on the last trading day, taken at one-minute intervals from4:01 p.m. to 4:30 p.m. and the closing index value, excluding thethree lowest value, and rounded to the nearest two decimal points.

Last Trading Day The business day immediately preceding the last business day of the contract month.

Settlement Method Cash Settlement. An in-the-money options which has not been

liquidated or exercised on the expiration date shall be exercisedautomatically.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 32/159

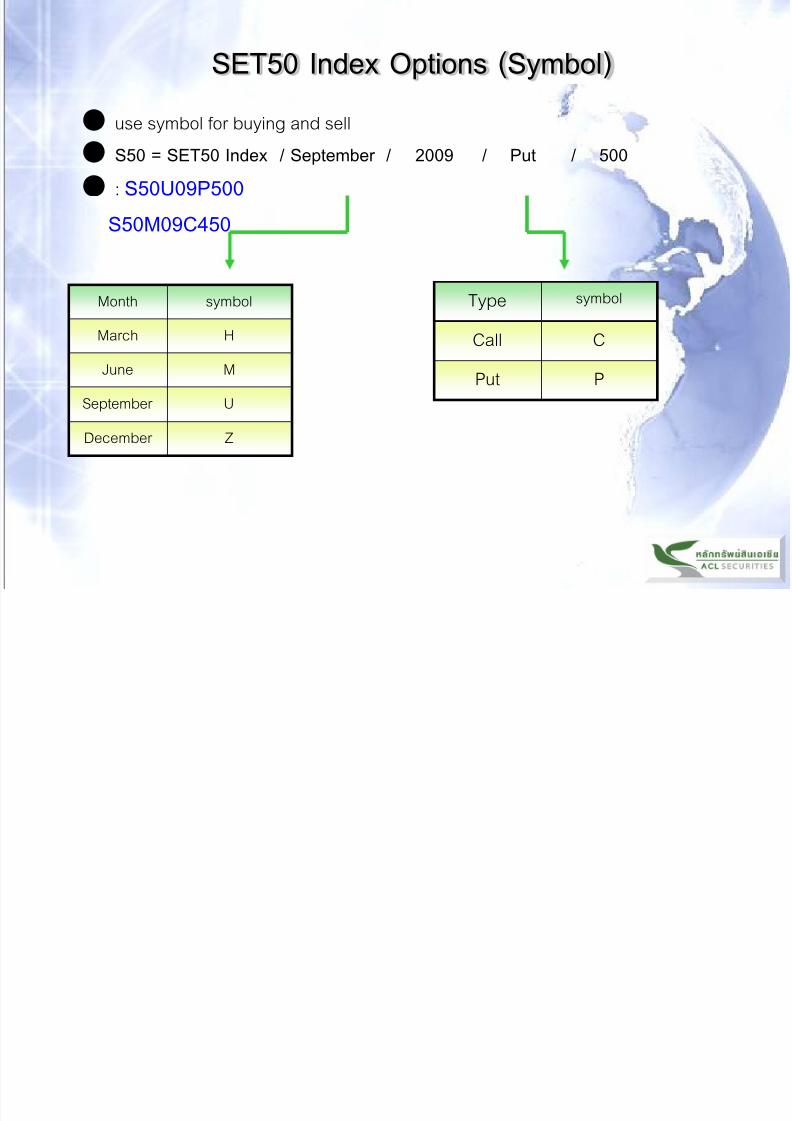

SET50 Index Options (Symbol)

● use symbol for buying and sell

● S50 = SET50 Index / September / 2009 / Put / 500

● : S50U09P500

S50M09C450

Month symbol

March H

June M

September U

December Z

Type symbol

Call C

Put P

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 33/159

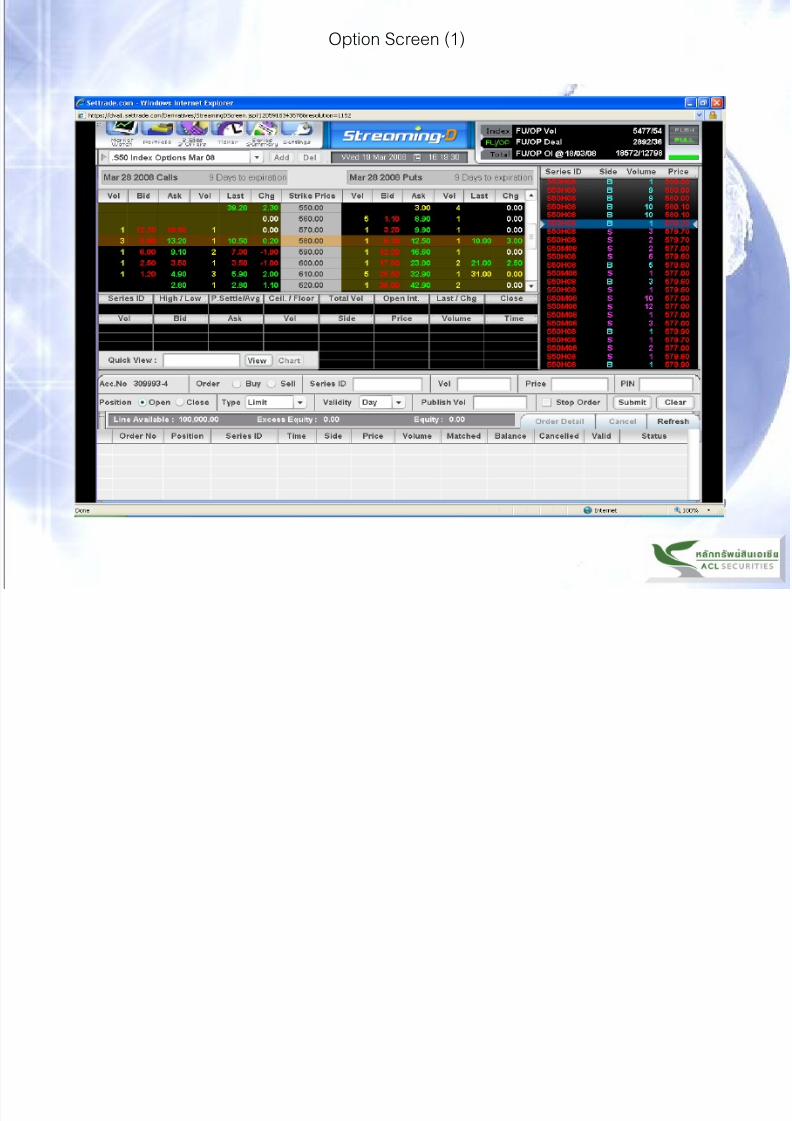

Option Screen (1)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 34/159

Option Screen (2)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 35/159

Multiplier

„ Example:

Mr A. long S50H09C500: 1 contract

pay premium 20 points

Payment = 20 * 200 = 4,000 baht

Assume investor long 3 contract

Payment = 20 * 200*3 = 12,000 baht

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 36/159

The obligation between 2 parties to

purchase and sale of the underlying

assets

Option holder has the right to buy or sell,

option writer is obligated to sell and buy

No payment made to the one who short

Futures (except commission fee)

Option holder must pay premium or option

price to option writer

Trade in Organized Securities Exchange Trade in Organized Securities Exchange

Standardized term Standardized term

Futures Options

Futures and Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 37/159

Daily settlement (marking to the market) Daily settlement (marking to the market)

Can earn a profit or loss on the position Can limit losses by choosing not to exercise

the option

Both parties have to pay margin Option writer (short position) must pay

margin

Futures Option

Futures and Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 38/159

3. Index Options Price

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 39/159

3. Index Options Price

1) Index Options Premium (Determinations)

2) Factors affecting price of SET50 Index Options

3) Theoretical Valuation of Index Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 40/159

1) Index Options Premium (Determinations)

► Components of SET50 Index Options Premium

„ (intrinsic value)„ (time value)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 41/159

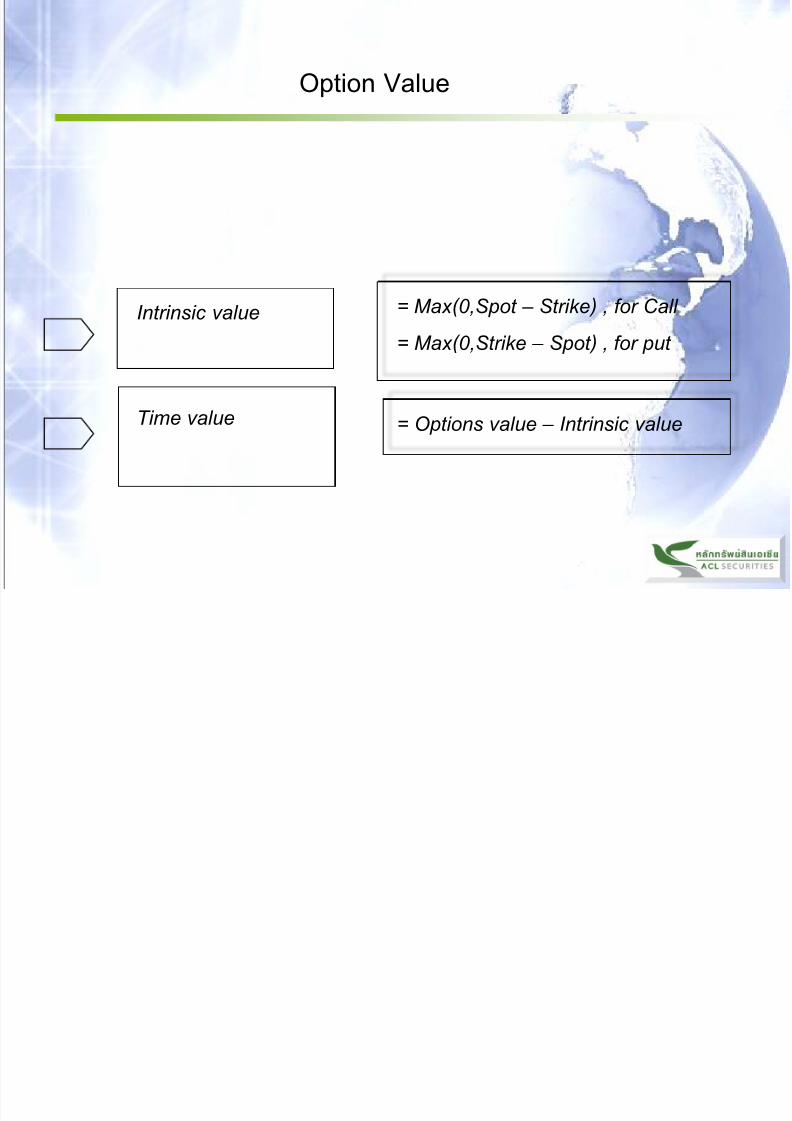

Option Value

Intrinsic value

Time value

= Max(0,Spot – Strike) , for Call

= Max(0,Strike – Spot) , for put

= Options value – Intrinsic value

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 42/159

1. Intrinsic and Time Value for Calls (S –X)

Stock price B55

Exercise price B50

Call Premium B6 (option price)

Expiration date 3 mths

Intrinsic Value: 55 – 50 = 5 Option price = IV + TV

6 = 5 + TV

Time Value = 1

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 43/159

2. Intrinsic and Time Value for Calls (S –X)

Stock price B45

Exercise price B50

Call Premium B6 (option price)

Expiration date 3 mths

Intrinsic Value: 45 – 50 = 0 Option price = IV + TV

6 = 0 + TV

Time Value = 6

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 44/159

3. Intrinsic and Time Value for Put (X –S)

Stock price B90

Exercise price B99

Call Premium B15 (option price)

Expiration date 3 mths

Intrinsic Value: 99 – 90 = 9 Option price = IV + TV

15 = 9 + TV

Time Value = 6

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 45/159

4. Intrinsic and Time Value for Put (X –S)

Stock price B110

Exercise price B99

Call Premium B15 (option price)

Expiration date 3 mths

Intrinsic Value: 99 – 110 = 0 Option price = IV + TV

15 = 0 + TV

Time Value = 15

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 46/159

2) Factors affecting price of SET50 Index Options

(Theoretical Factors)

► SET50 (St)

► interest rate

► exercise price (X)

► dividend

► Index volatility

► time to maturity

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 47/159

SET50 (St)

15

20

10

5

0

80 90 100 110 120

Call value

(St)

Put value

(St)

15

20

10

5

0

80 90 100 110 120

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 48/159

Call = S – X

S Call

Put = X – S

S Put

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 49/159

Exercise price (X)

15

20

10

5

0

80 90 100 110 120

Call value

(X)

Put value

(X)

15

20

10

5

0

80 90 100 110 120

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 50/159

Call = S – X

X Call

Put = X – S

X Put

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 51/159

Time to maturity

► The longer time to maturity the higher option value

Call and Put Value

Time to maturity

I d l tilit

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 52/159

(Long Call Options) (Long Put Options)

------Payoff

___Profit and loss

Index volatility

30

25

20

15

10

5

0

-5

-10

-15

35

470 480 490 500 510 520 530

30

25

20

15

10

5

0

-5

10

15

470 480 490 500 510 520 530

35

SET50 index at the expiration date SET50 index at the expiration date

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 53/159

Interest Rate

i Call Value

Put Value

i

Call Value

Put Value

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 54/159

Call = S – X e -rt

r PV of X Call

Put = X e-rt – S

r PV of X Put

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 55/159

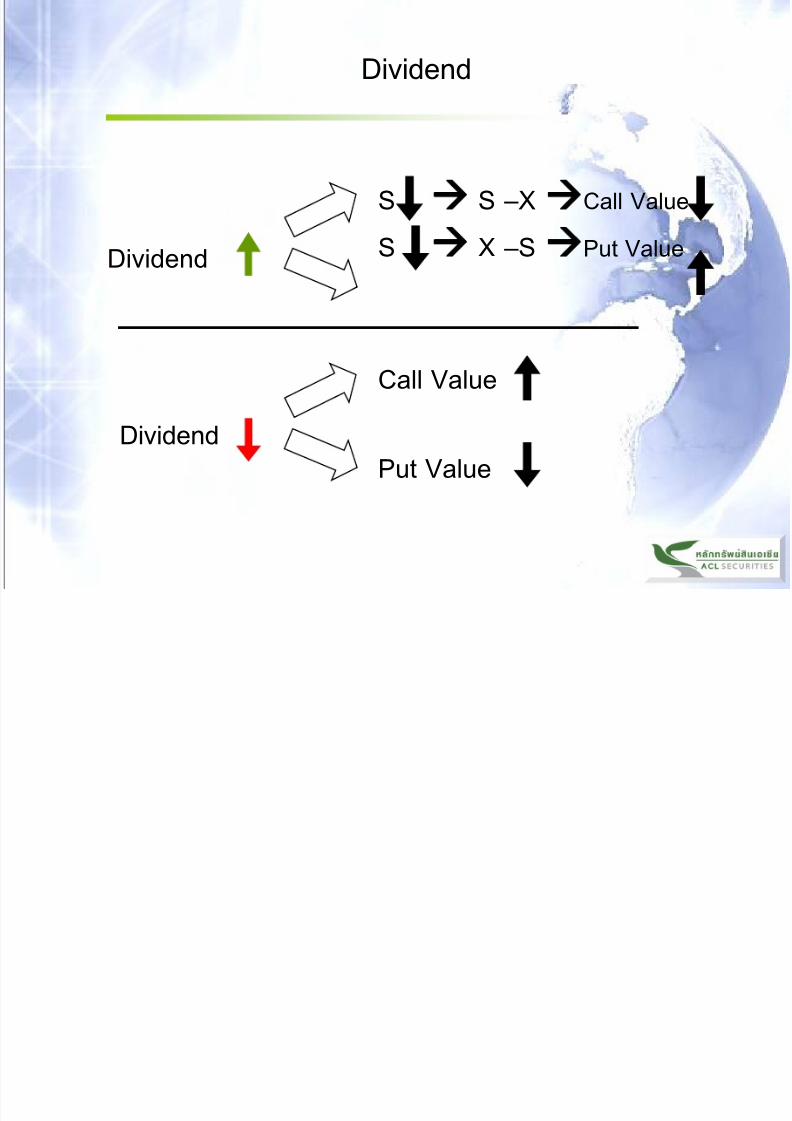

Dividend

Dividend

S S –X Call Value

S X –S Put Value

Dividend

Call Value

Put Value

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 56/159

The most important factors affecting option value

► SET50 (St)

► Index volatility

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 57/159

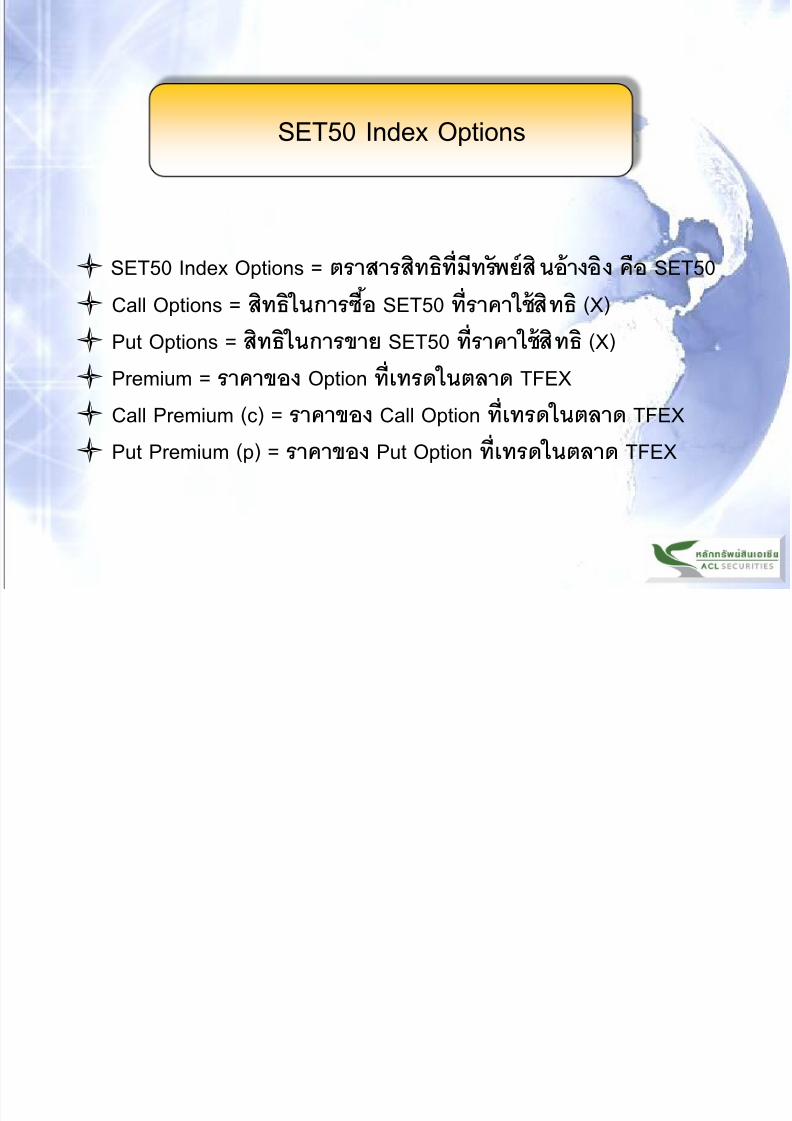

SET50 Index Options

SET50 Index Options = ตราสารสทิธิที มีทรัพย์สิ นอ้างอิง คือ SET50

Call Options = สทิธิ ในการซื อ SET50 ที ราคาใช้สิทธิ (X)

Put Options = สิทธิ ในการขาย SET50 ที ราคาใช้สิทธิ (X)

Premium = ราคาของ Option ที เทรดในตลาด TFEX

Call Premium (c) = ราคาของ Call Option ที เทรดในตลาด TFEX Put Premium (p) = ราคาของ Put Option ที เทรดในตลาด TFEX

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 58/159

3) Theoretical Valuation of Index Options

►Binomial Options Pricing Model

Black-Scholes Options Pricing Model

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 59/159

C = (European call option)

P = (European put option)

So

= (Spot price)

ST

= (Spot price at t)

X = (Strike price)

T = (Time to maturity)

r = (Risk-free interest rate)

q = (Dividend yield)

σ = (Volatility)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 60/159

Binomial Model

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 61/159

(One-period binomial model)

► (One-step binomial tree)

●

●

●

So

ƒ

Sou

ƒu

Sod

ƒd

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 62/159

Black-ScholesModel

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 63/159

Black-Scholes Model

c = SoN(d

1)-Xe-rTN(d

2)

p = Xe-rTN(-d2)-S

oN(-d

1)

d1 = InS

o

X+ σ

2

r +2

T

σ√TSo

X+

σ2

r -2

σ√T

d2

= In T = d1-σ√T

N(z) = Cumulative standard normal distribution

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 64/159

4.Types of Investors

4 Types of Investors: Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 65/159

1) Hedger

2) Speculator

3) Arbitrager

4.Types of Investors: Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 66/159

5. In action (Investors’ Review)

5 In action (Investors’ Review)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 67/159

5. In action (Investors Review)

Payoff Call Option = Max (O,ST

- X)

Payoff Put Option = Max (O,X - ST )

ST

> X ST

< X

Call Option exercise no

Put Option no exercise

1) Call option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 68/159

Jan. 1 X (INDEX) = 500 b

1) Mar.31 (St) = 520 b

call option “ exercise ” ( In The Money )

Pay off (profit) = 520-500 = +20 บาท (wihtout deduct option

Premium )

2) Mar.31 (St) = 480 b

→Do not exercise option (at 500 b)

Pay off (Loss) = option premium ( Out of The Money )

) p

Compare Long Call Option & Long Futures

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 69/159

+

- 500

( x )

+

- 500

Case 1 = +20

Case 2 = -20

p g p g

Long FuturesCall Option

2) Put option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 70/159

Jan. 1 X (INDEX) = 500 b

1) Mar.31 (St) = 520 b

put option " do not exercise ” ( Out of the Money )

loss = option premium

2) Mar.31 (St) = 480 b

Gain = 500-480 = +20 บาท (X ‟ ST)

2) Put option

Compare Long Put Option & Short Futures

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 71/159

+

-

+

- 500

(X)

500

Case 1 Loss = -20

Short Futures Case 2 Gain = +20

Option ITM OTM ATM

Call option ST

> X ST

< X ST

= X

Put option ST

< X ST

> X ST

= X

Moneyness

p g p

Put Option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 72/159

6. Trading Strategies: Options

6. Trading Strategies: Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 73/159

g g p

1. Trading Strategies: Options (Basic)

- Long call option

- Short call option

- Long put option

- Short put option

2. Stock –Option combination

3. Spreads

4. Put & Call options (Put-Call combinations)

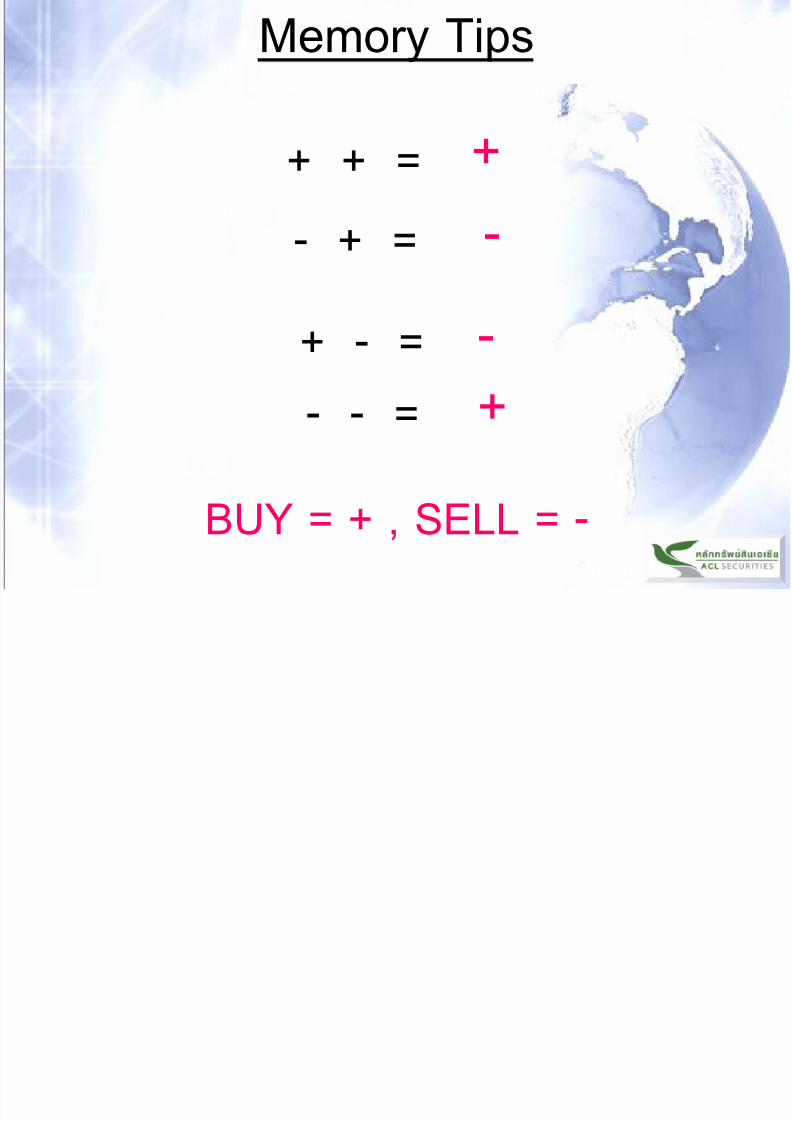

Memory Tips

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 74/159

y p

+ + =

- + =

+ - =

BUY = + , SELL = -

- - =

+ -

-

+

Profit and Loss: Options & Futures

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 75/159

+

-

+

-

500

500

A Long Call option

B Short Call option

500

+

-

+

-

C Long Put option D Short Put option

500

+

Long Futures / Stock

-

+

-

Short Futures / Stock

Trading Strategies: Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 76/159

Ex

Expect the price of St : increase → Long Call option/Short Put option

Expect the price of St : decrease → Short Call option/Long Put option

PART 1

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 77/159

Basic Strategies

1. Trading Strategies: Options (Basic)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 78/159

1.1 Long Call option :

P/L = Max( O,ST- X ) - Premium

Notes ST: Spot priceX : Exercise price

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 79/159

Table 1: Pay off and Profit/Loss : Long Call Option and

Long Stock and Futures

St Payoff

P/L(LongCall)

P/L

(Longstock/

Futures)

470 480

490

500

510

520

530

10

30

20

-10

-20

-30

470 480 490 500 510 520 530

Fig.1

ST

0 -10 -300 -10 -20

0 -10 -10

0 -10 0

10 0 10

20 10 20

30 20 30 P/L Long Stock/ Futures

P/L Long Call Option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 80/159

(Application): Long Call Option

→ Bullish market & high volatility

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 81/159

1.2 Short Call option :

P/L = Min ( O,X – ST

) + Premium

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 82/159

Table 2: Pay off and Profit/Loss :Short Call Option and

Short Stock or Futures

St Payoff

P/L(ShortCall)

P/L(Shortstock/

Futures)

470

480

490

500

510

520

530

0 10 30

0 10 20

0 10 10

0 10 0

-10 0 -10

-20 -10 -20

-30 - 20 -30

10

30

20

-10

-20

-30

470 480 490 500 510 520 530

Fig. 2

ST

P/L Short Stock/ Futures

P/L Short Call Option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 83/159

Application: Short Call Option

→ sideway to moderate bearish market & low volatility

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 84/159

1.3 Long Put option :

P/L = Max(O,X – ST) – Premium

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 85/159

Table 3: Pay off and Profit/Loss :Long Put Option and

Short Stock or Futures

10

30

20

-10

-20

-30

470 480 490 500 510 520 530

Fig. 3

ST

St Payoff

P/L(LongPut)

P/L(Shortstock/

Futures)

470

480

490

500

510

520

530

30 20 30

20 10 20

10 0 10

0 -10 0

0 -10 -10

0 -10 -20

0 - 10 -30 P/L Short Stock/ Futures

P/L Long Put Option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 86/159

Application: Long Put Option

→ Bearish market & high volatility

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 87/159

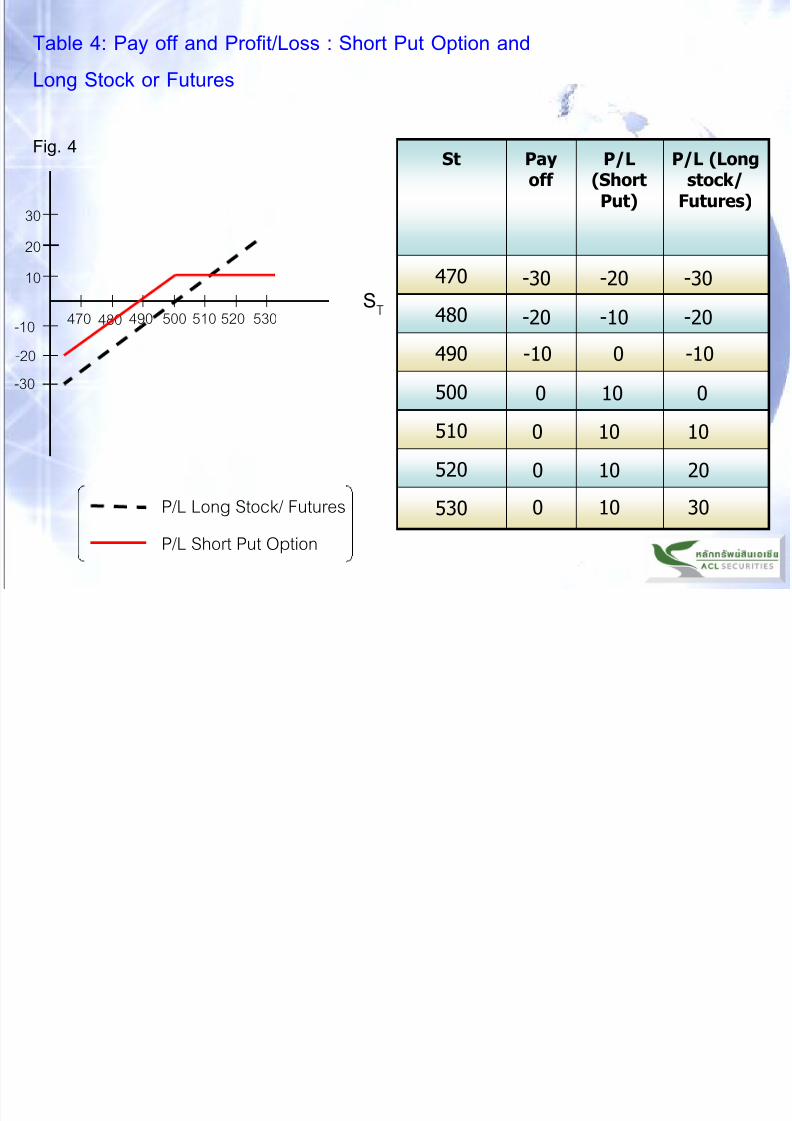

1.4 Short Put option :

P/L = Min(O,ST – X) + Premium

Table 4: Pay off and Profit/Loss : Short Put Option and

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 88/159

Long Stock or Futures

St Payoff

P/L(ShortPut)

P/L (Longstock/

Futures)

470

480

490

500

510

520

530

-30 -20 -30

-20 -10 -20

-10 0 -10

0 10 0

0 10 10

0 10 20

0 10 30

10

30

20

-10

-20

-30

470 480 490 500 510 520 530

Fig. 4

ST

P/L Long Stock/ Futures

P/L Short Put Option

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 89/159

Application: Short Put Option

→ sideway-up market & low volatility

PART 2

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 90/159

Intermediate Strategies

2) stock – option combination

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 91/159

2.1 Covered Call

- Long stock or Long Futures with Short call option

- sideway to moderate bullish market

stock – option combination

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 92/159

Ex Jan.1 St = 500 b

call option ( premium ) = 10 b

X = 500 b

St P/LShortCall

P/LLongStock

P/LCovered

Call

470

480

490

500

510

520

530

10 -30 -20

10 -20 -10

10 -10 0

10 0 10

0 10 10

-10 20 10

-20 30 10

10

30

20

-10

-20

-30

470 480 490 500 510 520 530

Fig. 1

St

P/L

P/L Short Call Option

P/L Long Stock

P/L Covered call

stock – option combination

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 93/159

2.2 Protective Put

- Long Stock and Long put option

- Bullish market: to hedge risk when the price decreases

Table 2: Protective Put

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 94/159

St P/LLongput

option

P/LLongStock

P/LProtectiveput

470

480

490

500

510

520

530

10

30

20

-30

70 80 90 100 110 120 130

Fig 2

St

P/L

P/L Long Put Option

P/L Long Stock

P/L Protective Put

20 -30 -10

10 -20 -10

0 -10 -10

-10 0 -10

-10 10 0

-10 20 10

-10 30 20

Note : Same as Long call option (put – call parity )

PART 3

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 95/159

Advanced Strategies

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 96/159

- buy and sell options, same underlying assets

→ Price spread or Vertical spread : buy and sell options, same underlying assets,

same expiration date, diff exercise price

→ Calendar spread or horizontal spread : buy and sell options,

same underlying assets, same exercise price, diff expiration date

3. Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 97/159

Price Spread

1) Bullish Spreads

- Debit Bullish Spreads (Call Option)

- Credit Bullish Spreads (Put Option)

2) Bearish Spreads

- Debit Bearish Spreads (Put Option)

- Credit Bearish Spreads (Call Option)

3) Butterfly Spreads (Long and Short)

- Call Option

- Put Option

Calendar Spreads (Long and Short)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 98/159

3.1 Bullish spreads : Debit &Credit Bullish spreads

(1) Bullish Spreads ( Call option ) or Debit Bullish Spreads

- Long call option at lower exercise price ( X 1 ) & short call option

at higher exercise price ( X 2 ) ( Buy low – sell high )

- same underlying assets and expiration date

- moderate bullish market

“ Optimistic and Be conservative”

- limited upside gain ( = X2-X

1) for limited downside loss

** Call = S – X X Call **

Ex.1 Jan.1 500 call option = 10 b.

510 call option = 6 b.

Table 1 Bullish Spreads (Debit)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 99/159

St P/LLong

500 call

(10 b.)

P/LShort

510 call(6 b.)

P/L BullishSpreads

470

480

490

500

510

520

530

-10 6 -4

-10 6 -4

-10 6 -4

-10 6 -4

0 6 6

10 -4 6

20 -14 6

30

20

10

0

-10

-20

-30

480470 490 500 510 520 530

P/L

St

Fig. 1

P/L Long 500call

P/L Short 510 call

P/L Bullish Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 100/159

Note : - Long call option at lower exercise price (higher option

premium) & Short call option at higher exercise price (lower option

premium)

-“ Debit Bullish Spreads “

Buy 10 b. Sell 6 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 101/159

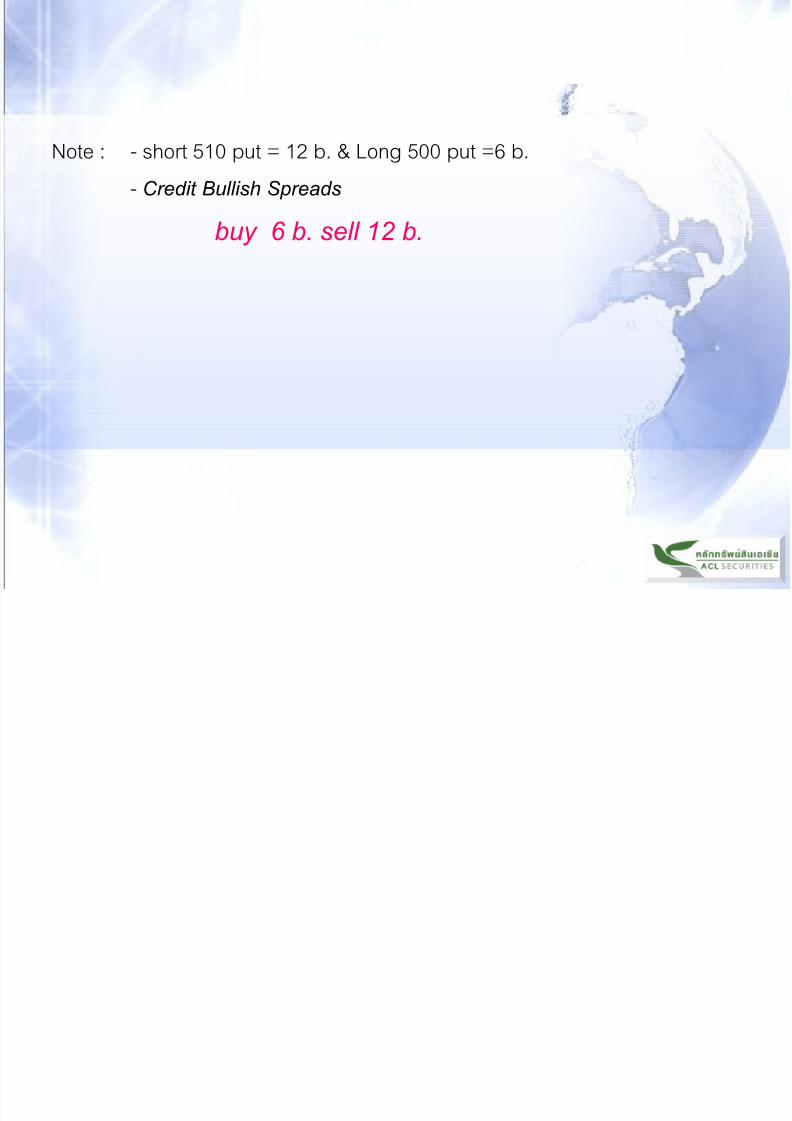

(2) Bullish Spreads (Put option)& Credit Bullish Spreads

- Long put option at lower exercise price (X 1 ),lower option premium

& Short put option at higher exercise (X 2 ),higher option premium

** Put = X – S X Put **

Ex.2 Jan.1 500 put option = 6 b.

510 put option = 12 b.

Table 2 : Bullish Spreads (Credit)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 102/159

30

20

10

0

-10

-20

-30

480470 490 500 510 520 530

St

Fig. 2

P/L Long 500 put

P/L Short 510 put

P/L Bullish Spreads

St P/LLong500 put

(6b.)

P/LShort510 put(12b.)

P/LBullishSpreads

470

480

490

500

510

520

530

24 -28 -4

14 -18 -4

4 -8 -4

-6 2 -4

-6 12 6

-6 12 6

-6 12 6

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 103/159

Note : - short 510 put = 12 b. & Long 500 put =6 b.

- Credit Bullish Spreads

buy 6 b. sell 12 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 104/159

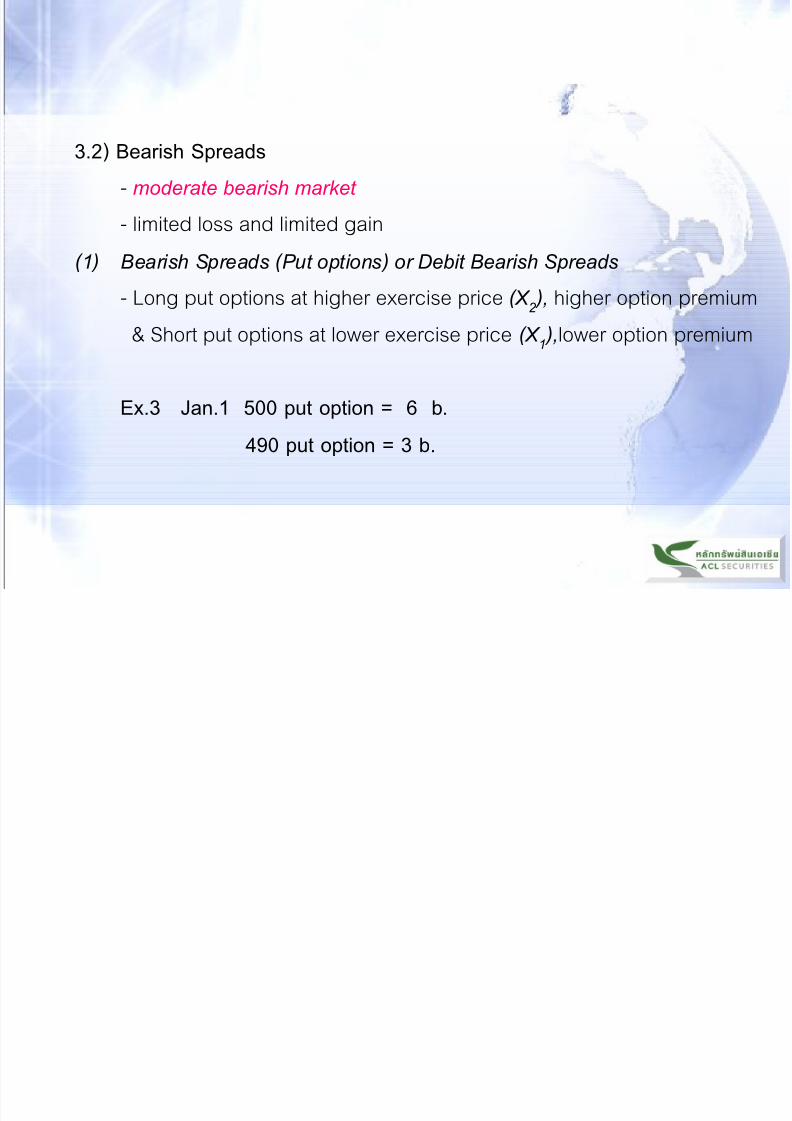

3.2) Bearish Spreads- moderate bearish market

- limited loss and limited gain

(1) Bearish Spreads (Put options) or Debit Bearish Spreads

- Long put options at higher exercise price (X 2 ), higher option premium

& Short put options at lower exercise price (X 1 ),lower option premium

Ex.3 Jan.1 500 put option = 6 b.

490 put option = 3 b.

Table 3:Bearish Spreads (Debit)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 105/159

30

20

10

0

-10

-20

-30

480

470

490 500 510 520 530

St

Fig. 3

x1

x2

P/L Long 500 put

P/L Short 490 put

P/L Bearish Spreads

St P/LLong

500 put

(6b.)

P/LShort

490 put(3b.)

P/LBearishSpreads

470

480

490

500

510 520

530

24 -17 7

14 -7 7

4 3 7

-6 3 -3

-6 3 -3

-6 3 -3

-6 3 -3

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 106/159

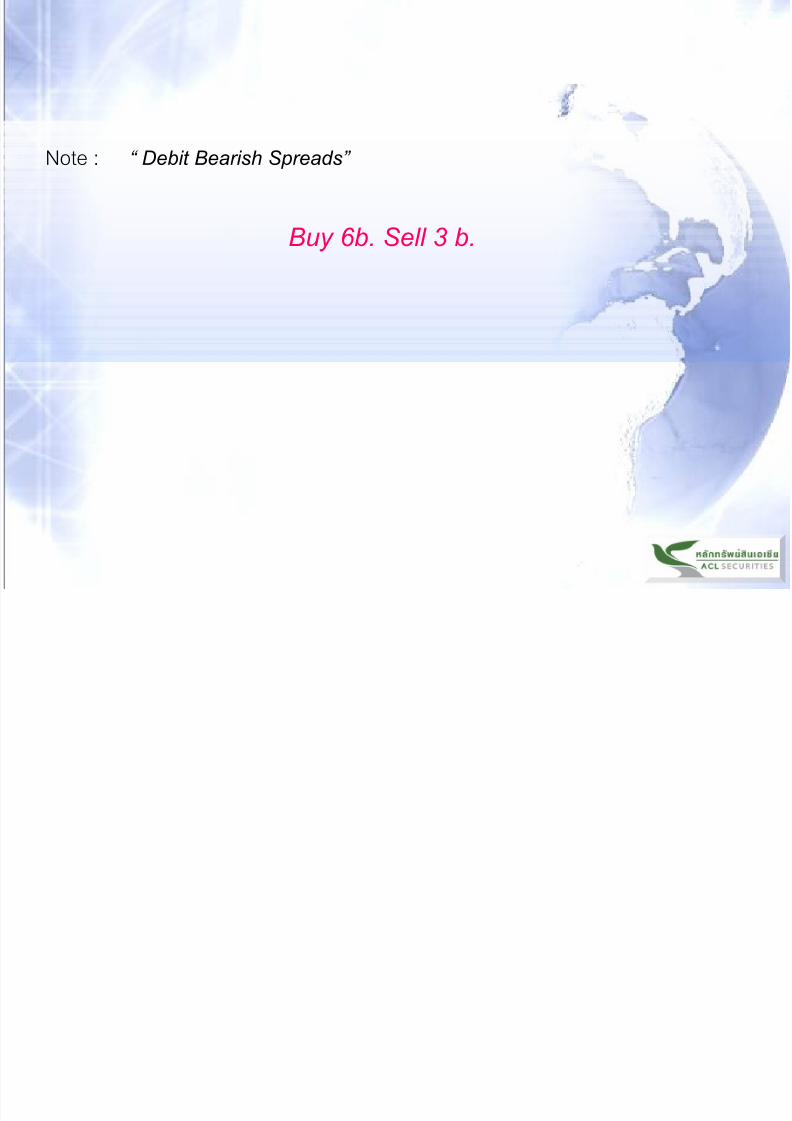

Note : “ Debit Bearish Spreads”

Buy 6b. Sell 3 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 107/159

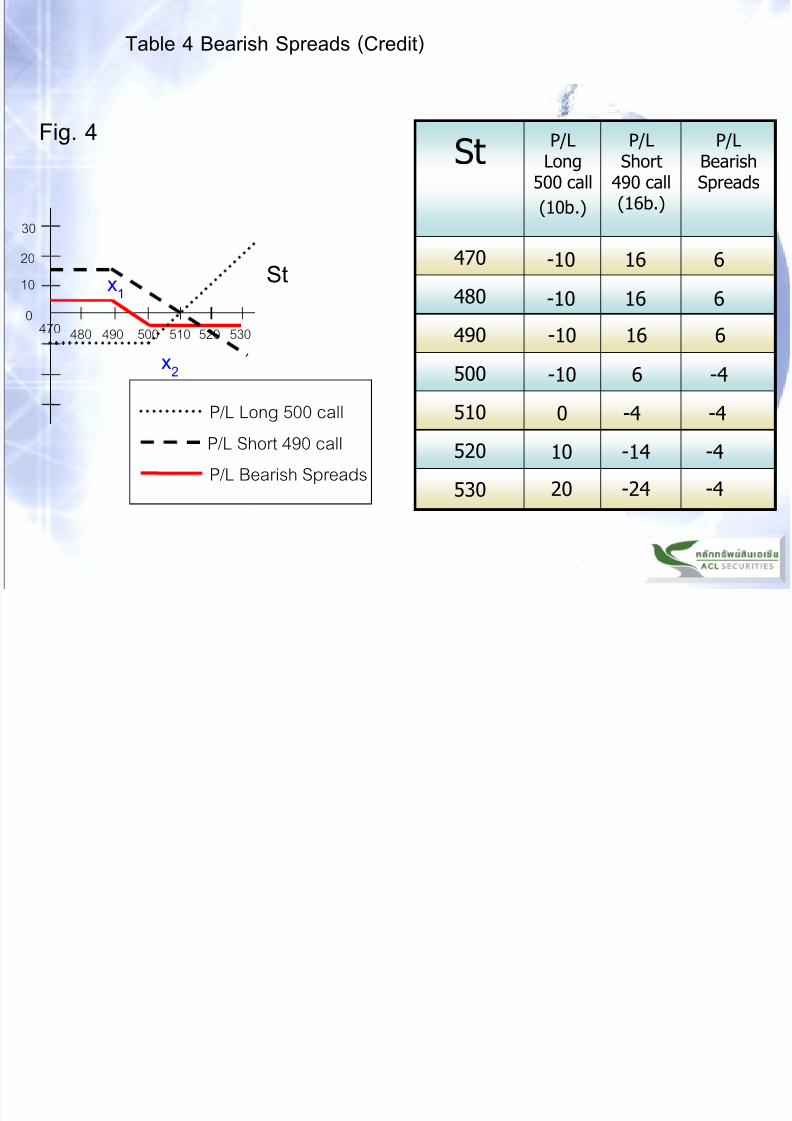

„ (2) Bearish Spreads (Call option) or Credit Bearish Spreads

- Long call option at higher exercise price (X2),lower option

premium & Short call option at lower exercise price (X1),higher

option premium

Ex.4 Jan 1 500 call option = 10 b.

490 call option = 16 b.

Table 4 Bearish Spreads (Credit)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 108/159

30

20

10

0

480470 490 500 510 520 530

St

Fig. 4

x1

x2

P/L Long 500 call

P/L Short 490 call

P/L Bearish Spreads

StP/L

Long500 call

(10b.)

P/L

Short490 call(16b.)

P/L

BearishSpreads

470

480

490

500

510

520

530

-10 16 6

-10 16 6

-10 16 6

-10 6 -4

0 -4 -4

10 -14 -4

20 -24 -4

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 109/159

Note : - Short 490 call option = 16 b. &

Long 500 call option = 10 b.

- “ Credit Bearish Spreads “

Buy 10b.Sell 16b.

3.3) Butterfly Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 110/159

- buy and sell options, 3 diff exercise price, same underlying asset,

and same expiration date(1) Call option : Long 1 unit of call option at low exercise price (X1)

Short 2 units of call option at medium exercise price (X2)

Long 1 unit of call option at high exercise price (X3)

- ( sideway market )

- limit loss at all option price

-Max. profit at medium exercise price ( X 2 )

Ex. 5 Jan 1 490 call option = 16 b.

500 call option = 10 b.

510 call option = 6 b.

Table 5 Butterfly Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 111/159

30

20

10

0

-10

-20

-30

480

470

490 500 510 520 530

P/L

St

P/L Long 490 call

P/L Short 500 call (2 units)

P/L Long 510 call

Fig 5

P/L Long Butterfly Spreads

x2

x1

x3

StP/L

Long

490call

(1 unit)

P/L

Short

500 call(2units)

P/L

Long

510call

(1 unit)

P/L

Long

ButterflySpreads

470

480

490

500

510

520

530

-16 20 -6 -2

-16 20 -6 -2

-16 20 -6 -2

-6 20 -6 8

4 0 -6 -2

14 -20 4 -2

24 -40 14 -2

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 112/159

(2) Put options : Long 1 unit of put option at low exercise price (X 1 )

Short 2 units of put option at medium exercise price (X 2 )

Long 1 unit of put option at high exercise price (X 3 )

Ex. 6 Jan 1 490 put option = 3 b.

500 put option = 6 b.

510 put option = 12 b.

Table 6 Butterfly Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 113/159

30

20

10

0

-10

-20

-30

480470 490 500 510 520 530

P/L

St

P/L Long 490 put (1 unit)

P/L Short 500 put (2 units)

P/L Long 510 put (1 unit)

Fig. 6

x1

x2

P/L Long Butterfly Spreads

x3

St P/L

Long490put

(1 unit)

P/L

Short500 put

(2units)

P/L

Long510put

(1 unit)

P/L

LongButterflySpreads

470

480

490

500

510

520

530

17 -48 28 -3

7 -28 18 -3

-3 -8 8 -3

-3 12 -2 7

-3 12 -12 -3

-3 12 -12 -3

-3 12 -12 -3

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 114/159

Note : - (1) and (2) Long Butterfly Spread use

call options & put options→ ( Sideway market)

- For Short Butterfly Spreads Up and down with low volatility

Ex. Short 1 unit of call option (or put option) at low exercise price (X 1 )

Long 2 units of call option (or put option) at medium exercise price (X 2 )

Short 1 unit of call option (or put option) at high exercise price (X 3 )

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 115/159

Ex. 7 Jan 1 490 call option = 16 b.

500 call option = 10 b.

510 call option = 6 b.

Table 7 Butterfly Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 116/159

30

20

10

0

-10

-20

-30

480470 490 500 510 520 530

P/L

St

P/L Short 490 call (1unit)

P/L Long 500 call (2 units)

P/L Short 510 call (1unit)

Fig. 7

x1

x2

P/L Short Butterfly Spreads

x3

St P/LShort

490call

(1 unit)

P/LLong

500call

(2 units)

P/LShort

510call

(1 unit)

P/L

Short

ButterflySpreads

470

480

490

500

510

520

530

16 -20 6 2

16 -20 6 2

16 -20 6 2

6 -20 6 -8

-4 0 6 2

-14 20 -4 2

-24 40 -14 2

3.4 Calender Spreads

Hori ontal Spreads options ith same e ercise price

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 117/159

- Horizontal Spreads : options with same exercise price,

diff.expiration date

- Sideway market & volatility expect to increase

Long Calendar Spreads

- Long call (or put) options at the longer maturity

- Short call ( or put) options at the shorter maturity

**Options with same underlying asset

& Same exercise price**

Ex.8 MAR 500 Call option = 10 b.

JUN 500 Call option = 14.50 b.

Table 8: Long Calendar Spreads

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 118/159

30

20

10

0

-10

-20

-30

480470 490 500 510 520 530

P/L

St

Fig. 8

P/L Long JUN 500 call

P/L Short MAR 500 call

P/L Long Calendar Spreads

St P/L

ShortMAR

500 call

P/L

LongJUN

500 call

P/L Long

CalendarSpreads

470

480

490

500

510

520

530

10 -14.12 -4.12

10 -12.48 -2.48

10 -9.33 0.67

10 -4.50 5.50

0 1.89 1.89

-10 9.53 -0.47

-20 18.07 -1.93

Table 8: Long Calendar Spreads

Notes :

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 119/159

Notes :

- The investor can Short Calendar Spreads

Short call (or put) options at the longer maturity &

long call (or put) option at the shorter maturity

- Sideway market & volatility expect to decrease

4. Put & Call options (Put-Call combinations)

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 120/159

→ Buy (or sell) call option and put option at the same time

4 Types: Straddle , Strip , Strap , and Strangle

4.1) Straddle- buy (or sell) 1 unit of call and put options, same exercise price,

same underlying asset, and same expiration date

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 121/159

1) Long straddle (Long call & put options) or “ Bottom Straddle”

- Market with high volatility in any direction (Up and down)

- (limited loss/ unlimited return)

Ex.1 Jan 1500 call option = 10 b.

500 put option = 6 b.

Table 1: Long Straddle

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 122/159

30

20

10

0

-10

-20

-30

480470 490 500510 520 530

P/L

St

P/L Long 500 call

P/L Long 500 put

P/L Long Straddle

Fig. 1St P/L

LongCall

P/LLongPut

P/L

LongStraddle

470

480

490

500

510

520

530

-10 24 14

-10 14 4

-10 4 -6

-10 -6 -16

0 -6 -6

10 -6 4

20 -6 14

Table 1: Long Straddle

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 123/159

2) Short Straddle (Short call & put option) or “ Top Straddle”

- Sideway market

Ex.2 Jan 1

500 call option = 10 b.

500 put option = 6 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 124/159

30

20

10

0

-10

-20

-30

480470 490 500510 520 530

P/L

St

Fig. 2

X

P/L Short 500 call

P/L Short 500 put

P/L Short Straddle

St P/LShortCall

P/LShort

Put

P/LShort

Straddle

470

480

490

500

510

520

530

10 -24 -14

10 -14 -4

10 -4 6

10 6 16

0 6 6

-10 6 -4

-20 6 -14

Table 2: Short Straddle

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 125/159

4.2) Strip and Strap

→ Strip : buy (or sell) 1 call option & 2 put options at the same exercise

→ Strap : buy (or sell) 2 call options & 1 put option at the same exercise

1) Long Strip (Long 1 call option and 2 put options)

- The price moves any direction: up or down (higher chance to decrease)

Ex.3 Jan 1

500 call option = 10 b .

500 put option = 6 b.

Table 3: Long Strip

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 126/159

30

20

10

0

-10

-20

-30

480470 490 500510 520 530

P/L

St

Fig. 3

P/L Long 500 call

P/L Long 500 put

P/L Long Strip

St P/LLongCall

Option(1 unit)

P/L LongPut

Option(2 units)

P/LLongStrip

470

480

490

500

510

520

530

-10 48 38

-10 28 16

-10 8 -2

-10 -12 -22

0 -12 -12

10 -12 -2

20 -12 8

Table 3: Long Strip

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 127/159

2) Long strap (Long 2 call options & Long 1 put option)

-The price moves any direction: up or down

(higher chance to increase)

Ex.4 Jan 1

500 call options = 10 b.

500 put options = 6 b.

Table 4: Long Strap

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 128/159

30

20

10

0

-10

-20

-30

480470 490 500510 520 530

P/L

St

Fig 4

P/L Long 500 call

P/L Long 500 put

P/L Long Strap

St P/L

LongCall

Option(2 unit)

P/L Long

PutOption

(1 units)

P/L

LongStrap

470

480

490

500

510

520

530

-20 24 4

-20 14 -6

-20 4 -16

-20 -6 -26

0 - 6 -6

20 - 6 14

40 - 6 34

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 129/159

3) Short Strip (Short 1 call option & Short 2 put options)4) Short Strap (Short 2 call options 4 Short 1 put option)

“ For sideway market ”

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 130/159

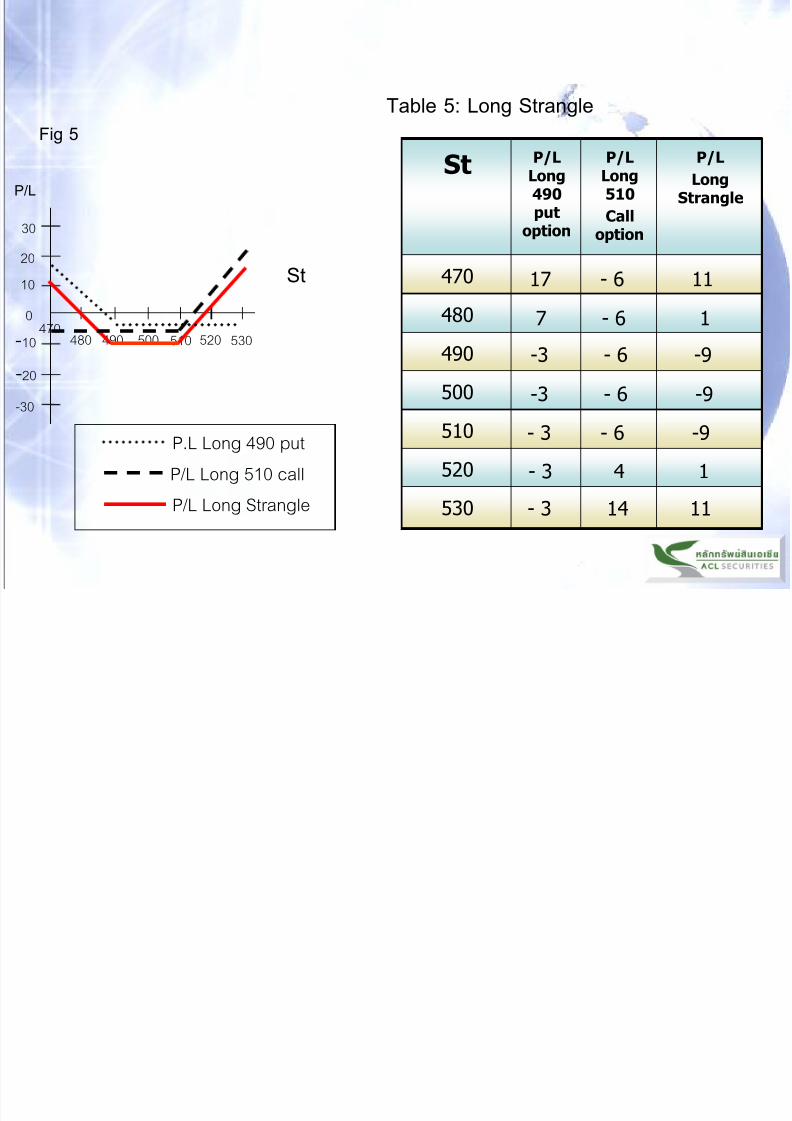

4.3) Strangle

- buy (or sell)) put option at the lower exercise price& buy ( or sell ) call option

at the higher exercise price (same underlying asset and expiration date)

1) Long Strangle (Long put option at lower exercise price

& Long call option at higher exercise price)

- (limited risk/unlimited return)

- Very high volatility (in any direction: up or down)

Ex.5 490 put option = 3 b.

510 call option = 6 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 131/159

30

20

10

0

-10

-20

-30

480470

490 500 510 520 530

P/L

St

P.L Long 490 put

P/L Long 510 call

P/L Long Strangle

Fig 5

St P/LLong490put

option

P/LLong510

Calloption

P/LLong

Strangle

470

480

490

500

510

520

530

17 - 6 11

7 - 6 1

-3 - 6 -9

-3 - 6 -9

- 3 - 6 -9

- 3 4 1

- 3 14 11

Table 5: Long Strangle

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 132/159

Note :

- quite similar to Long Straddle

- limited risk/unlimited return

(the wider gap comparing to Straddle)(profit increase when the price changes more )

- Low cost strategy

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 133/159

2) Short Strangle (Short put option at lower exercise price & Short call

option at higher exercise price)

Ex.6 490 put option = 3 b.

510 call option = 10 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 134/159

30

20

10

0

-10

-20

-30

480470

490 500 510 520 530

P/L

St

P/L Short 510 call

P/L Short 490 put

P/L Short Strangle

Fig. 6

St P/LShort490put

option

P/LShort510

Calloption

P/LShort

Strangle

470

480

490

500

510

520

530

-17 10 -7

-7 10 3

3 10 13

3 10 13

3 0 3

3 -10 -7

3 -30 -17

Table 6: Short Strangle

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 135/159

Note :

- Sideway market

- unlimited risk/limited return

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 136/159

7. Index Options

(Margin Calculation)

Trading Process: (Long) Index Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 137/159

„ Long SET50 Index Options – Call & Put

Open account with

Broker

Make an purchase

order

Pay Premium

Close the position

or

Let It Expire

The Buyer pay premium

(Long Open)

Trading Process: Short Index Options

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 138/159

„ Short SET50 Index Options – Call & Put

Open account with

Broker

Pay margin Make sell order

The Seller maintain margin

Close the position before

Or at the expiration date

Maintain Margin

Withdraw margin

Mark to Market

At Settlement price

(Initial Margin)

MARGIN

„ Initial margin เงินประกันเริ มต้น ท ีผ ู ้ลงทุนต้องวางเมื อซื อขายอนุพันธ์

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 139/159

„ Broker จะต้องคานวณสถานะและ mark to market เปรียบเทยีบ margin อยา่งน้อยทุก

สิ นวัน

„ Maintenance margin เงินประกันขันต าที ผ ู ้ลงทุนต้องดารงในบัญชีซือขายอนุพันธ์

„ กรณีมีการซือขายที สร้างฐานะแบบ spread strategy จะมีวิธีคานวณเฉพาะ

หลักประกันเริ มต้น

(Initial margin)

หลักประกันรักษาสภาพ

(Maintenance margin )

„ หากเงนิประกันในบัญชีต ากว่าระดับ หลักประกันรักษาสภาพ ( Maintenance margin) ต้องนาเงิ นมาวางเพ ิมให้ยอดเงินประกันในบัญชกีลับมาอย ู ่ท ีระดับ

หลักประกั นเริ มต้น (Initial margin )

TRADING CASES

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 140/159

„ Marketing (broker) has to send an Short Open order to open

the position

„ Investor pay margin to broker

„ Mark-to-the-Market at the end of day to realize profit/loss

CASE 1 Investor never Short SET50 Index Options

TRADING CASES

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 141/159

CASE 2 Investor had opened Long SET50 Index Options and

Willing to close the position by short option

Do investor need to pay margin and Mark-to-the-Market?

NO

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 142/159

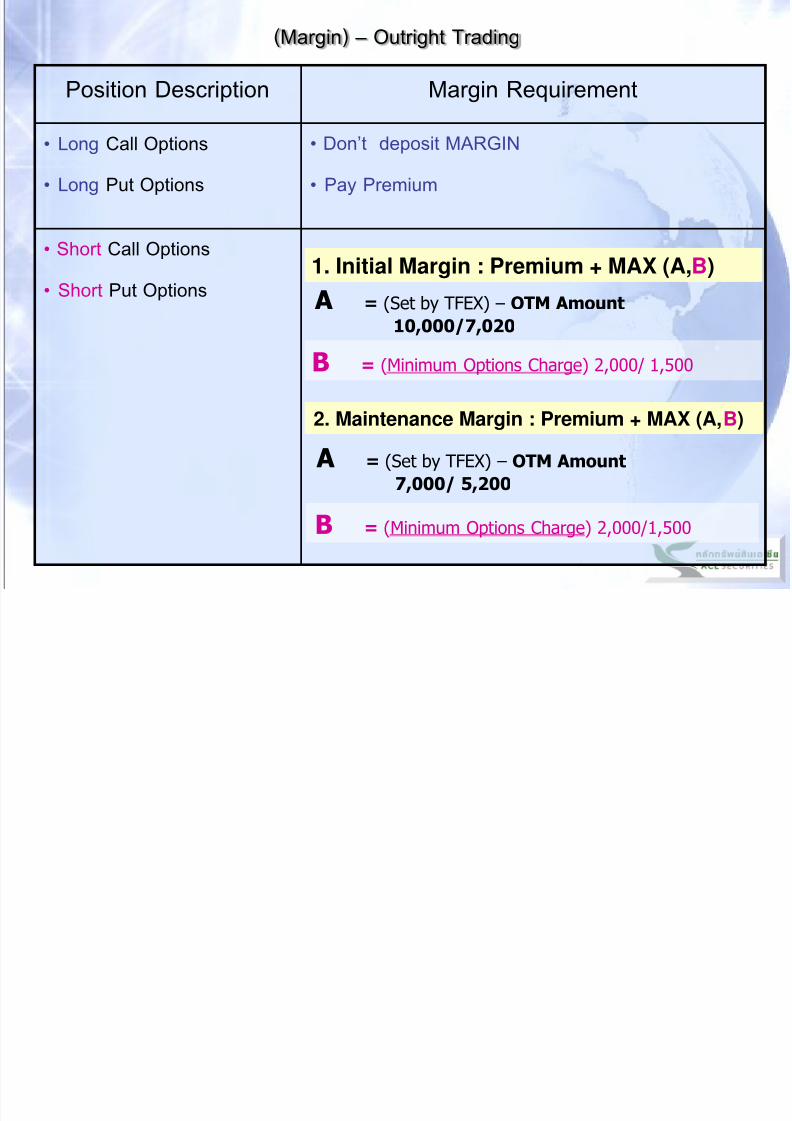

(Margin) – Outright Trading

(Margin) – Outright Trading

Position Description Margin Requirement

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 143/159

„ Long Call Options

„ Long Put Options

„ Don’t deposit MARGIN

„ Pay Premium

„ Short Call Options

„Short Put Options

1. Initial Margin : Premium + MAX (A,B)

A = (Set by TFEX) – OTM Amount10,000/7,020

B = (Minimum Options Charge) 2,000/ 1,500

2. Maintenance Margin : Premium + MAX (A,B)

A = (Set by TFEX) – OTM Amount

7,000/ 5,200

B = (Minimum Options Charge) 2,000/1,500

EX – Long Call Options (S – X – P)

Day 1: SET50 Index at 540 point

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 144/159

P/L (Baht)premiumSET50 (St)Transaction

22540 long Call at 22 pointsDay 1

(17 – 22) x 200 = - 1,00017530 (OTM)short Call at 17 points Anoon

1. Day Trade

P/L (Baht)premiumSET50Transaction

22540 long Call at 22 pointsDay 1

(24 – 22) x 200 = + 40024545 (ITM)short Call at 24 pointsDay 2

P/L (Baht)Final Sett.PriceSET50Transaction

540 long Call at 22 pointsDay 1

[ - 22] x 200 = -4,400 Limit loss500 500 (OTM)Option expire -no exerciseDec.31

2. Position Trade

3. Held to Maturity

P/L (Baht)Final Sett.PriceSET50Transaction

540 long Call at 22 pointsDay 1

[(575 – 540)-22]x200 = + 2,600575575 (ITM)Option expire - exerciseDec.31

Investor: Expect the price to increase

Action: Long SET50 Index Call Options, S50Z07C540

1 contract at premium of 22 points

EX– Short Call Options (X – S + P)

Day 1: SET50 Index at 540 points

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 145/159

P/L (Baht)premiumSET50Transaction

22540 Short call at 22 pointsDay 1

(22 – 17) x 200 = + 1,00017530long call at 17 points Anoon

1. Day Trade

P/L (Baht)premiumSET50Transaction

22540 Short call at 22 pointsDay 1

(22 – 24) x 200 = - 40024545long call at 24 pointsDay 2

P/L (Baht)Final Sett.PriceSET50Transaction

St Limit Gain540 Short call at 22 pointsDay 1

[ + 22] x 200 = + 4,400 500 500Option expire – no exerciseDec.31

2. Position Trade

3. Held to Maturity

P/L (Baht)Final Sett.PriceSET50Transaction

St Unlimit Loss540 Short call at 22 pointsDay 1

[(540 – 575)+22] x 200 = - 2,600575575Option expire - exerciseDec.31

Investor : Price will decrease

Action: Short SET50 Index Call Options, S50Z07C540

1 contract at premium of 22 points

How to calculate margin for Short Call

„ Suppose

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 146/159

‟ SET50 Call Options (Z series)

‟ A = 10,000 - OTM Value for IM

= 7,000 - OTM Value for MM

‟ B = 2,000 for IM & MM

Date SET50 Strike (x) Premium Moneyness Status OTM Value

Day 1 540 540 22 S-X=0 ATM 0

End of Day 1 530 540 17 S-X<0 OTM (540-530)*200=2,000

End of Day 2 545 540 24 S-X>0 ITM 0

End of Day 3 560 540 39 S-X>0 ITM 0

End of Day 4 575 540 55 S-X>0 ITM 0

Short call(1)„ Mr. A short S50Z07C540 at 22 points

‟ Mr. A get premium = 22*200 = 4,400 baht

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 147/159

Date SettlementPrice

Premium Margin

A ของ IM =

10,000 - OTM

B ของ IM IM = Max(A,B) + PremiumMargin

Day 1 22 4,400 10,000 - 0 = 10,000 2,000 IM=10,000+4,400 = 14,400

End of Day 1 17 3,400 10,000 - 2,000 = 8,000 2,000 IM= 8,000+3,400 = 11,400

End of Day 2 24 4,800 10,000 - 0 = 10,000 2,000 IM=10,000+4,800 = 14,800

End of Day 3 39 7,800 10,000 - 0 = 10,000 2,000 IM=10,000+7,800 = 17,800

End of Day 4 55 11,000 10,000 - 0 = 10,000 2,000 IM=10,000+8,800 = 21,000

Margin requirement (Short Outright) = Max (A,B) + Premium

Date SettlementPrice

Premium Margin

A ของ MM =

7,000 - OTM

B ของ

MMMM = Max(A,B) + Premium

Margin

Day 1 22 4,400 7,000 - 0 = 7,000 2,000 MM = 7,000+4,400 = 11,400

End of Day 1 17 3,400 7,000 - 2,000 = 5,000 2,000 MM = 5,000+3,400 = 8,400End of Day 2 24 4,800 7,000 - 0 = 7,000 2,000 MM = 7,000+4,800 = 11,800

End of Day 3 39 7,800 7,000 - 0 = 7,000 2,000 MM = 7,000+7,800 = 14,800

End of Day 4 55 11,000 7,000 - 0 = 7,000 2,000 MM=7,000+11,000 = 18,000

Short call(2)

i G

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 148/159

Day Transaction Prem. IM MM MARGIN

1 Short Call at 22 points: Depositmargin before trading

22 14,400 11,400 14,400

1 short order matched: get premium of 22 points (4,400 b)Excess margin = 4,400 b

22 14,400 11,400 18,800

1 Suppose: u withdraw Excessmargin = 4,400 b

22 14,400 11,400 14,400

Initial margin (IM) = 14,400 บาท

Maintenance margin (MM) = 11,400 บาท

Short call(3)

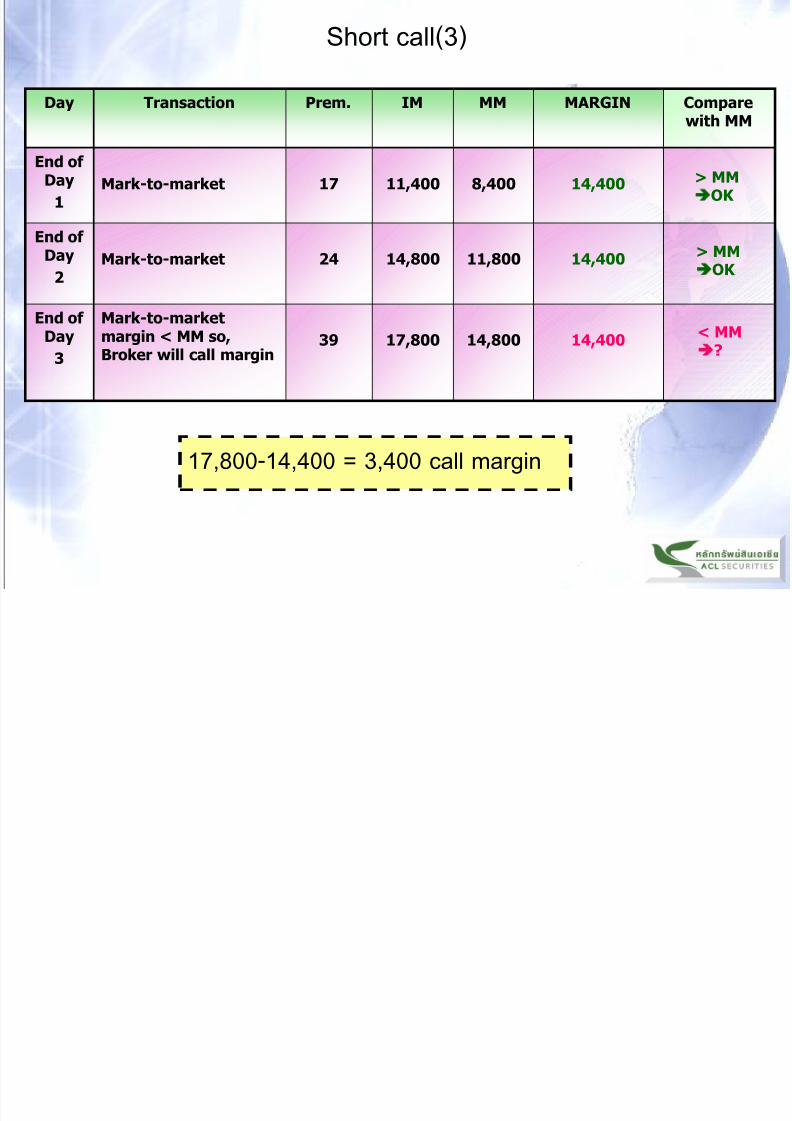

Day Transaction Prem. IM MM MARGIN Compare

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 149/159

y pwith MM

End of Day

1Mark-to-market 17 11,400 8,400 14,400

End of Day

2Mark-to-market 24 14,800 11,800 14,400

End of Day

3

Mark-to-marketmargin < MM so,Broker will call margin

39 17,800 14,800 14,400

17,800-14,400 = 3,400 call margin

> MMOK

< MM?

> MMOK

Short call(4)

Day Transaction Prem. IM MM MARGIN Comparewith MM

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 150/159

„ Refund margin = 17,800 - 56*200 = 6,600 b

„ ตรวจคาตอบ: เงินที ได้คืนหลังปิดสถานะ = เงินหลักประกันที ใส่เข้ามาก่อนเทรด + เงินที เตมิเข้ามาเพ ิมเมื อถูกเรียก ‟ ค่าพรีเมยีมจา่ยเพื อซื อคนืเพ ือปิดสถานะ = 14,400+3,400-11,200 = 6,600 บาท

„ Loss = (22 - 56)*200 = 6,800 b.„ ตรวจคาตอบ: ขาดทนุ = เงินที ได้คืนหลังปิดสถานะ - เงินที ใส่เข้ามาทังหมด

=6,600 - (14,400 - 4,400 + 3,400) = 6,800 บาท

with MM

Day 4 Pay margin before 3.55pm 17,800

End of Day

4

Mark-to-market

Margin < MM

so, Broker will call margin

55 21,000 18,000 17,800

Day 5 Investor long call to closeposition

56

< MM?

EX – Long Put Options (X - S - P)

Day 1: SET50 Index at 540 points

Investor: Price will decrease

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 151/159

P/L (Baht)premiumSET50Transaction

17540Long Put Options at 17 p.Day 1

(15 – 17) x 200 = - 40015555 (OTM)Short Put Options at 15 p.บา่ย

1. Day Trade

P/L (Baht)premiumSET50Transaction

17540Long Put Options at 17 p.Day 1

(32 – 17) x 200 = + 3,00032520 (ITM)Short Put Options at 32 pDay 2

P/L (Baht)Final Sett.PriceSET50Transaction

(ITM)540Long Put Options at 17 p.Day 1

[(540 – 500)-17] x 200 = + 4,600500 500 Option expire - exerciseDec.31

2. Position Trade

3. Held to Maturity

P/L (Baht)Final Sett.PriceSET50Transaction

(OTM)540Long Put Options at 17 p.Day 1

[ - 17] x 200 = - 3,400 Loss at Prem600 600Option expire –no exerciseDec.31

Investor: Price will decrease

Action: Long SET50 Index Put Options, S50Z07P540

at premium of 17 points

EX– Short Put Options (S - X + P)

Day 1: SET50 Index at 540 points

In estor Price ill increase

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 152/159

P/L (Baht)premiumSET50Transaction

17540Short Put Options at 17 p.Day 1

(17 – 15) x 200 = +40015555 Long Put Options at 15 p.บา่ย

1. Day Trade

P/L (Baht)premiumSET50Transaction

17540Short Put Options at 17 p.Day 1

(17 – 32) x 200 = - 3,00032520Long Put Options at 32 p.Day 2

P/L (Baht)Final Sett.PriceSET50Transaction

540Short Put Options at 17 p.Day 1

[(500 – 540) +17] x 200 = - 4,600500 500 Option expire - exerciseDec.31

2. Position Trade

3. Held to Maturity

P/L (Baht)Final Sett.PriceSET50Transaction

540Short Put Options at 17 p.Day 1

[+17] x 200=+ 3,400 Gain at Prem600600Option expire -no exerciseDec.31

Investor: Price will increase

Action: Short SET50 Index Put Options, S50Z07P540

at 17 points

„ Suppose

How to calculate margin for Short Put

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 153/159

Date SET50 Strike (x) Premium Moneyness Status OTM Value

Day 1 550 540 17 X-S<0 OTM (550-540)*200=2,000

End of Day 1 555 540 15 X-S<0 OTM (555-540)*200=3,000

End of Day 2 540 540 24 X-S=0 ATM 0

End of Day 3 520 540 32 X-S>0 ITM 0End of Day 4 505 540 42 X-S>0 ITM 0

‟ SET50 put options (Z series)

‟ A = 10,000 - OTM Value for IM

= 7,000 - OTM Value for MM

‟ B = 2,000 for IM & MM

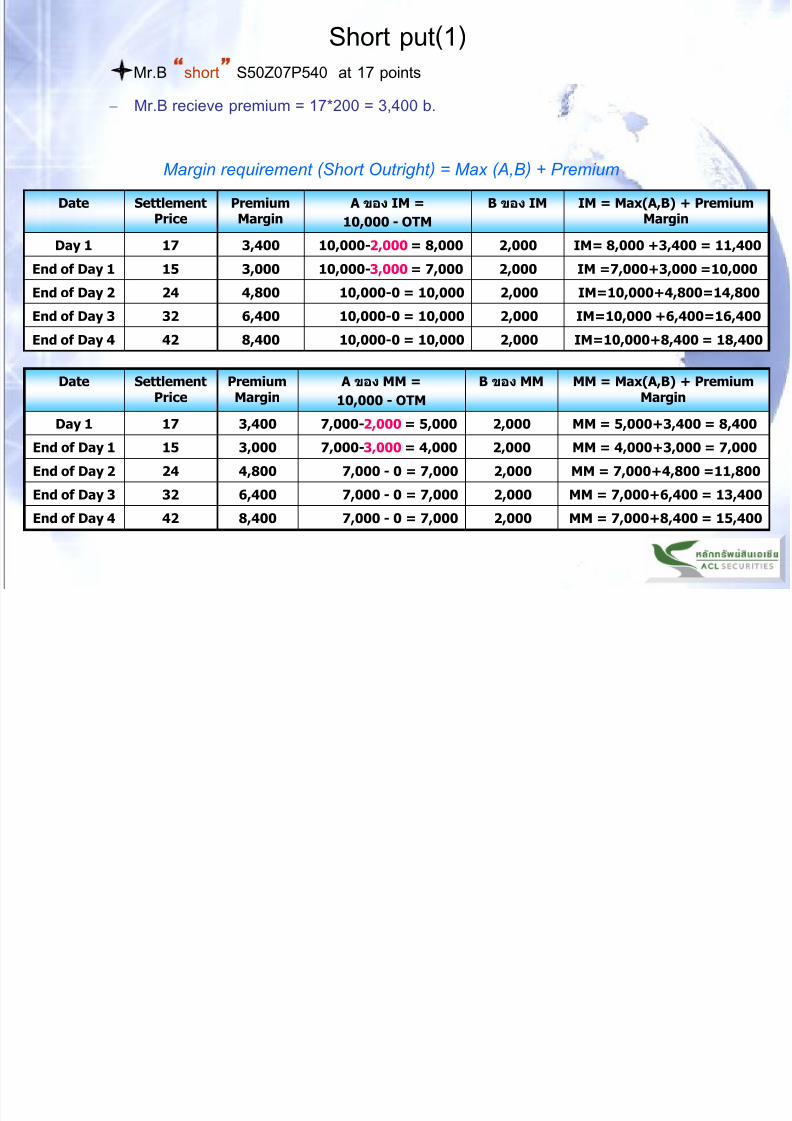

Short put(1)Mr.B short S50Z07P540 at 17 points

‟ Mr.B recieve premium = 17*200 = 3,400 b.

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 154/159

Date SettlementPrice

Premium Margin

A ของ IM =

10,000 - OTM

B ของ IM IM = Max(A,B) + PremiumMargin

Day 1 17 3,400 10,000-2,000 = 8,000 2,000 IM= 8,000 +3,400 = 11,400

End of Day 1 15 3,000 10,000-3,000 = 7,000 2,000 IM =7,000+3,000 =10,000

End of Day 2 24 4,800 10,000-0 = 10,000 2,000 IM=10,000+4,800=14,800

End of Day 3 32 6,400 10,000-0 = 10,000 2,000 IM=10,000 +6,400=16,400

End of Day 4 42 8,400 10,000-0 = 10,000 2,000 IM=10,000+8,400 = 18,400

p ,

Margin requirement (Short Outright) = Max (A,B) + Premium

Date SettlementPrice

Premium Margin

A ของ MM =

10,000 - OTM

B ของ MM MM = Max(A,B) + PremiumMargin

Day 1 17 3,400 7,000-2,000 = 5,000 2,000 MM = 5,000+3,400 = 8,400

End of Day 1 15 3,000 7,000-3,000 = 4,000 2,000 MM = 4,000+3,000 = 7,000

End of Day 2 24 4,800 7,000 - 0 = 7,000 2,000 MM = 7,000+4,800 =11,800

End of Day 3 32 6,400 7,000 - 0 = 7,000 2,000 MM = 7,000+6,400 = 13,400

End of Day 4 42 8,400 7,000 - 0 = 7,000 2,000 MM = 7,000+8,400 = 15,400

Short put(2)

Day Transaction Prem. IM MM MARGIN

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 155/159

1 Short Call at 17 points

Investor pay margin before trade

17 11,400 8,400 11,400

1 short order

Get premium 17 points (3,400 b.)

Excess margin = 3,400 b.

17 11,400 8,400 14,800

1 Suppose: u withdraw Excessmargin = 3,400 b

17 11,400 8,400 11,400

Initial margin (IM) = 11,400 บาท

Maintenance margin (MM) = 8,400 บาท

Short put(3)

Day Transaction Prem. IM MM MARGIN Comparewith MM

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 156/159

End of

1

Mark-to-market 15 10,000 7,000 11,400

End of

2

Mark-to-market

margin < MM

so, Broker will callmargin

24 14,800 11,800 11,400

Day

3

Pay margin of 3,800 b.before 3.55pm

11,400+

3,800=15,200

margin < MM put money at IM

= 14,800 – 11,400 = 3,400 b.

Suppose investor put 3,800 B. that is more than IM OK

> MM

OK

< MM?

Short put(4)

Day Transaction Prem. IM MM MARGIN Comparewith MM

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 157/159

End 3 Mark-to-market 32 16,400 13,400 15,200

End

4

Mark-to-market

margin < MM

so, Broker will call margin

42 18,400 15,400 15,200

5 Investor long put to close

position

46

„ Refund Margin = 15,200 - 46*200 = 6,000b.

„ ตรวจคาตอบ: เงินที ได้คืนหลังปิดสถานะ = เงินหลักประกันเริ มต้น + เงินที เติมเข้ามาเพ ิมเมื อถกูเรียก ‟ ค่าพรีเมียมจา่ยเพื อปิดสถานะ = 11,400 +3,800 - 9,200 = 6,000 บาท

„ Loss = (17 - 46)*200 = 5,800b.

„ ตรวจคาตอบ: ขาดทุน = เงินที ได้คืนหลังปิดสถานะ - เงินที ใส่เข้ามาทังหมด

= 6,000 ‟ (11,400 ‟ 3,400 + 3,800) = 5,800 บาท

> MMOK

< MM?

References

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 158/159

- Cohen,G.,2005, Options made Easy, 2ndedition, Prentice Hall, New Jersey

- Hull.,J.C., 2006, Options, Futures and other derivatives, 6thedition, Pearson,

New Jersey

- Hull.,J.C., 2005, Futures and Options market, 4thedition, Prentice Hall,

New Jersey

- Hull.,J.C., 2007, Fundamentals of Futures and Options markets, 5th edition,

Pearson

-TSI 2547, ความรู ้ เบื องต้นเกี ยวกับตราสารอนุพันธ์ (DR1)

- TSI 2548, การวเิคราะห์ตราสารอนุพันธ์ (DR2)

- เอกสารประกอบการสัมมนา TSI, โดย ดร.ธนาวัฒน์ สิริวัฒน์ธนกุล (19 ม.ค.2550)

- TSI 2548, การลงทุนในตราสารอนุพันธ์ (CISA)

References

7/29/2019 Option Completed version

http://slidepdf.com/reader/full/option-completed-version 159/159

- TSI 2550, SET50 Index Options, เอกสารประกอบการสัมมนา (ขั นตอนการ

ลงทุน และการวางหลักประกันในออปชัน)

- TSI 2550, SET50 Index Options, เอกสารประกอบการสัมมนา,

โดย คุณ กิติกร ลิ มมงคล

![Questions_On_Khums completed version[1]](https://static.fdocuments.in/doc/165x107/589052b51a28ab04208b699a/questionsonkhums-completed-version1.jpg)