Option Combinations and Positions. Insuring Long Asset: Protective Put Investor owns asset Investor...

16

Option Combinations and Positions

-

Upload

robert-alexander -

Category

Documents

-

view

214 -

download

0

Transcript of Option Combinations and Positions. Insuring Long Asset: Protective Put Investor owns asset Investor...

OptionCombinations

andPositions

Insuring Long Asset: Protective Put

• Investor owns asset• Investor also buys (holds) a put on the asset• Guarantees investment portfolio proceeds are at

least equal to the exercise price of the put• Similar to net position of asset+insurance• Protective put = long asset + long put = long call

+ lending (shape same as long call, but up)

+ =

Insuring Short Asset

• Investor shorts asset• Investor also buys (holds) a call on the asset• Limits downside of short asset position• Short asset + long call = long put + borrowing

(shape same as long put, but shifted down)

+ =

Selling Insurance: Covered Call

• Investor purchases asset• Investor also sells (writes) a call option on the

asset• Option position is “covered” by owning the

underlying asset itself• Similar to shifted written put• Provides additional (premium) income

+ =

Other Option Positions

• Naked call– Short call option– No position in underlying asset– Potentially unlimited loss

• Covered put– Short put + short asset– Shape: short call, but shifted down

Put-Call Parity

• General formula:

C – P = PV(F) – PV(K)where: C = call price P = put price

F = forward price K = strike priceSame K, T, and U/L asset for call, put

• For non-dividend-paying U/L asset:

C – P = S – PV(K)

where: S = current price of U/L asset

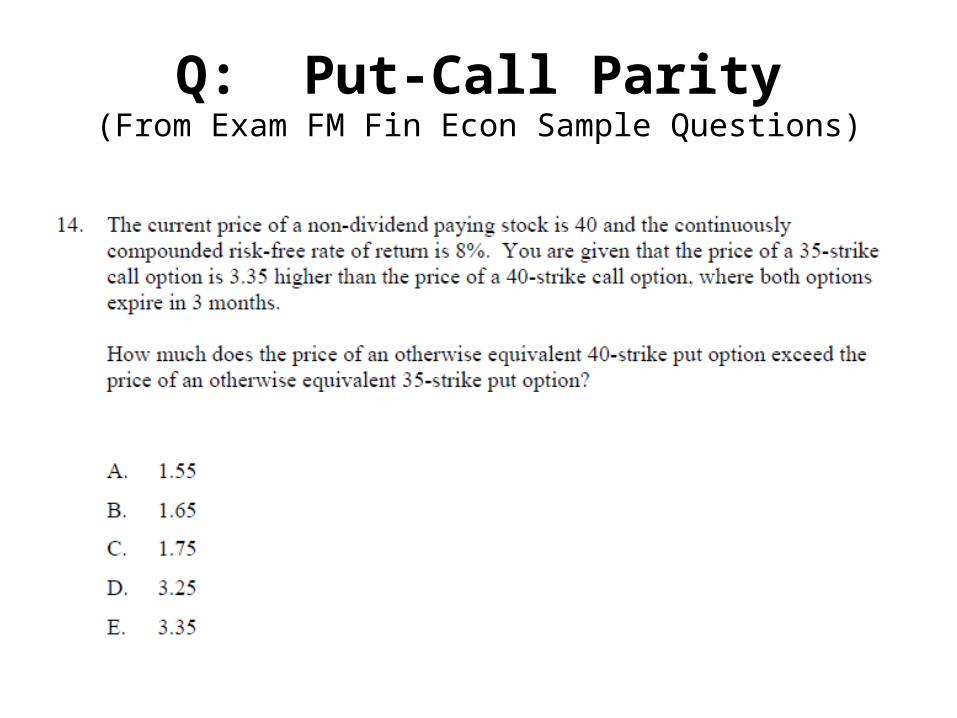

Q: Put-Call Parity(From Exam FM Fin Econ Sample Questions)

Q: Put-Call Parity(From Exam FM Fin Econ Sample Questions)

Option Combinations

• Synthetic forward– Long call plus short put (same exercise price K)– Guarantees buying asset at K

• Spread (also see subsequent slide)– Bull: long C(K1), short C(K2) (K1 < K2)– Bear: short C(K1), long C(K2) (K1 < K2)– Box: combination of bull and bear spreads– Ratio: unequal numbers of the different options

• Collar:– Long P(K1), short C(K2) (K1 < K2)

Option Combinations (cont.)

• Straddle– Long P(K1), long C(K1)

• Written straddle– Short P(K1), short C(K1)

• Strangle– Like straddle, but use less expensive out-of-the-

money options

• Butterfly spread– Written straddle + long Cs and Ps (out-of-the-money)– Asymmetric: unequal numbers of options

Generally use at-the-money options

Spread

• Combination of options– Two or more calls, or– Two or more puts

• Horizontal spread: sale and purchase of options with different expiration dates

• Vertical spread: simultaneous sale and purchase of options with different exercise prices -- e.g.,

+ =K1

K2

K1 K2

Q: Relationship Between Derivative and Underlying Asset

(From Exam FM Fin Econ Sample Questions)

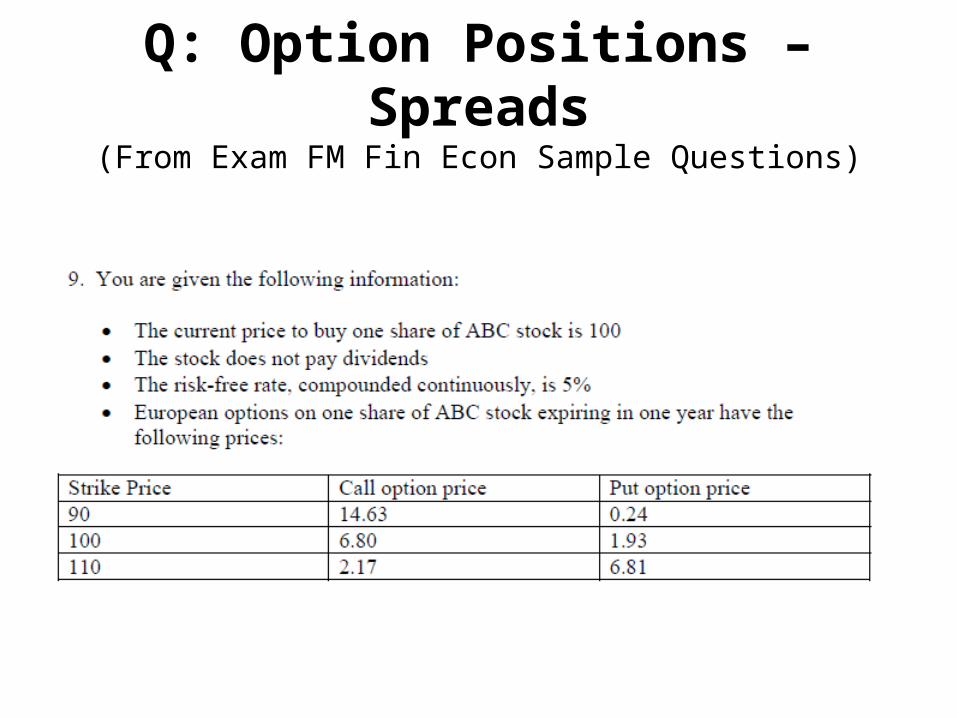

Q: Option Positions – Spreads(From Exam FM Fin Econ Sample Questions)

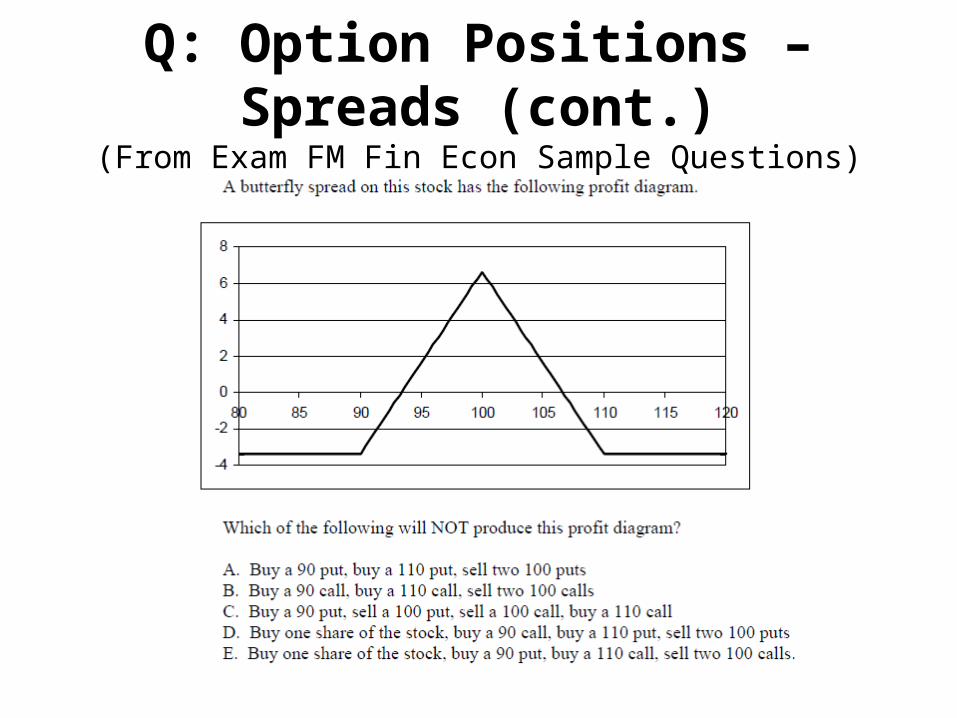

Q: Option Positions – Spreads (cont.)(From Exam FM Fin Econ Sample Questions)

Q: Option Positions - Straddles(From Exam FM Fin Econ Sample Questions)

Q: Option Positions – Collars(From Exam FM Fin Econ Sample Questions)