Optimization and Balance Sourcing Supply Chain Case … · Optimization and Balance Sourcing Supply...

24

Optimization and Balance Sourcing Supply Chain Case Study on Evaluation on Vietnamese Footwear Industry Robert Hiley Vice President, Asia Product Supply - Timberland Footwear,

-

Upload

hoangkhanh -

Category

Documents

-

view

216 -

download

2

Transcript of Optimization and Balance Sourcing Supply Chain Case … · Optimization and Balance Sourcing Supply...

Optimization and Balance Sourcing Supply Chain

Case Study on Evaluation on Vietnamese Footwear Industry

Robert Hiley

Vice President, Asia Product Supply - Timberland Footwear,

AS

IA

What external factors will drive change for Supply Chain?

What external factors will drive change for Supply Chain?

Global Economics

• Currency Fluctuations

• Political Disruption

• Big Data

• Global Terrorism

• Trade Agreements

• New US Administration

• Commodity Costs

• A Maturing China

• An Emerging Africa

What Drives Sourcing Decisions?

• Factory Capability

• Factory Partnerships

• Supply Chain Consolidation

• Political Stability

• Footwear / Material Infrastructure

• Productivity Levels

• Lead Times / Speed to Market

• Trade Agreements

• Corporate Social Responsibility / Responsible Sourcing

• Costs

Timberland Footwear – Sourcing Footprint

Bangladesh: 26%

Cambodia: 13%

China: 13%

Vietnam: 26%

Philippines: 6%

Dominican Republic: 16%

* by volume

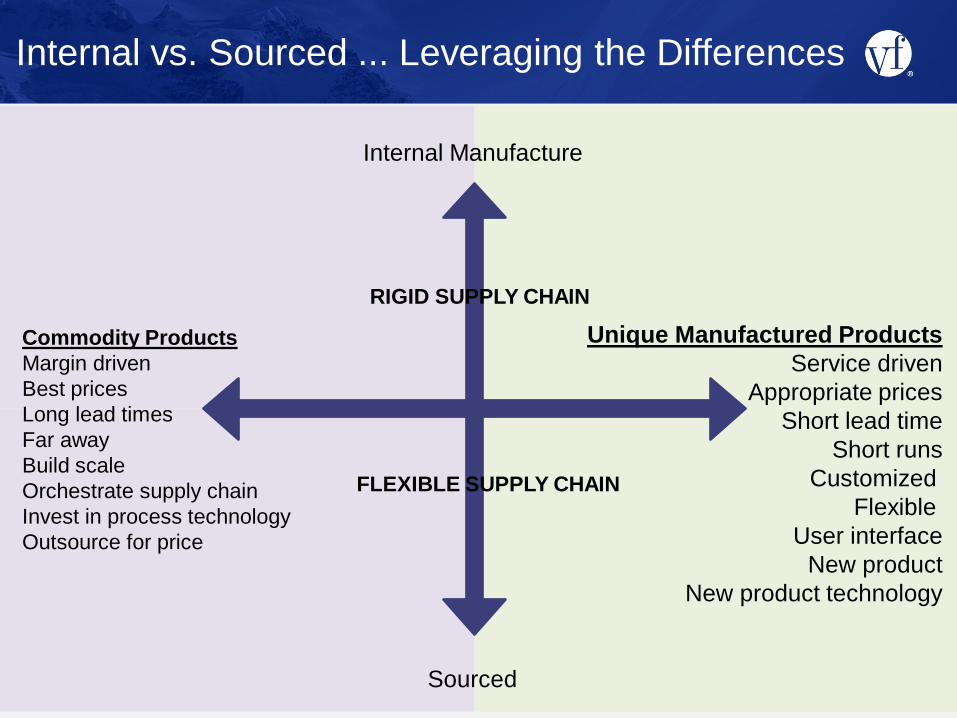

Internal vs. Sourced ... Leveraging the Differences

Sourced

Commodity Products

Margin driven

Best prices

Long lead times

Far away

Build scale

Orchestrate supply chain

Invest in process technology

Outsource for price

Unique Manufactured Products

Service driven

Appropriate prices

Short lead time

Short runs

Customized

Flexible

User interface

New product

New product technology

Internal Manufacture

RIGID SUPPLY CHAIN

FLEXIBLE SUPPLY CHAIN

Innovation and Automation

• Design to Manufacture

• Reduce Complexity

• Automation

• Product / Material Innovation

• Labor & Skill Reduction

• Production Efficiency

• Zero Waste

The Effect of Globalization on Design and Development

Offshore Design Development/

Sample Room Asia Production

What is the Landed Cost of a Shoe?

Factory FOB

$25 Shipping

$1

Insurance

$0.3 Customs/Duty

$2.5

Landed Cost

$28.8

Material $17.5 (~70%) Labor

$3.75

(~15%)

Overhead

$2.25

(~9%)

Profit

$1.5

(~6%)

FOB

Components

&

Split

Country Analysis

• Established footwear industry

• Materials infrastructure

• Stable workforce / Strong work ethics

• Low labor cost and high productivity

• Duty-friendly into the EU

• Political stability

• Availability of labor / Population size

• Rising labor costs / Rapid industrial growth

• Shallow talent pool / limited footwear skills

• Labor disputes

• Poor infrastructure

• Anticipation of Trade Agreement VIE

TN

AM

PROS CONS

• Established footwear Industry

• Footwear materials infrastructure

• Footwear expertize

• High productivity

• Politically stable

• Capacity and access to domestic market

• Rising labor costs

• Lack of investment

• High worker turnover

• Lack of footwear training

• No trade free agreements CH

INA

• Low labor costs

• Duty free into the EU/Canada

• Worker stability

• Footwear and leather training / Education

• Politically stable

• Political instability

• Terrorism

• Factory compliance

• Poor infrastructure

• Logistics and lead time

• Limited materials infrastructure

BA

NG

LA

DE

SH

Country Analysis

• Competitive labor rates

• Availability of labor / Population size

• Worker stability

• Duty-friendly into the EU

• Established footwear industry

• Worker stability

• Lack of footwear training

• Difficult labor laws

• Longer lead time

• Poor infrastructure

• Shallow footwear talent pool

• Raw material supply chain IND

ON

ES

IA

PROS CONS

• Worker stability

• Low labor rates

• Established footwear industry

• Politically stable

• Footwear and leather training

• Availability of labor/ Population size

• Poor infrastructure

• Limited good factory options

• Factory CSR compliance

• Limited footwear materials & components

• Labor unions

• Poor productivity

IND

IA

• Worker stability

• Availability of labor / Population size

• Lead time

• Footwear expertize

• Duty free into the EU

• Competitive labor rates

• Limited good factory options

• Poor infrastructure

• Raw material supply chain

• Political instability

• High logistics cost

• Low productivity PH

ILIP

PIN

ES

• Trade Agreements – Duty Free into the EU/ Canada/Japan

• Low worker turnover

• Limited industry

• Worker stability

• Small population / workforce

• Labor Disputes

• Unions

• Low productivity

• Political instability CA

MB

OD

IA

• Large labor pool

• Government

• Trade Agreements – Duty Free into the EU/ Japan

• Government support of the industry

• Limited industry

• Political instability

• Lead time

• Relatively high labor rates for a developing economy

• Low Productivity

• Poor infrastructure MY

AN

MA

R

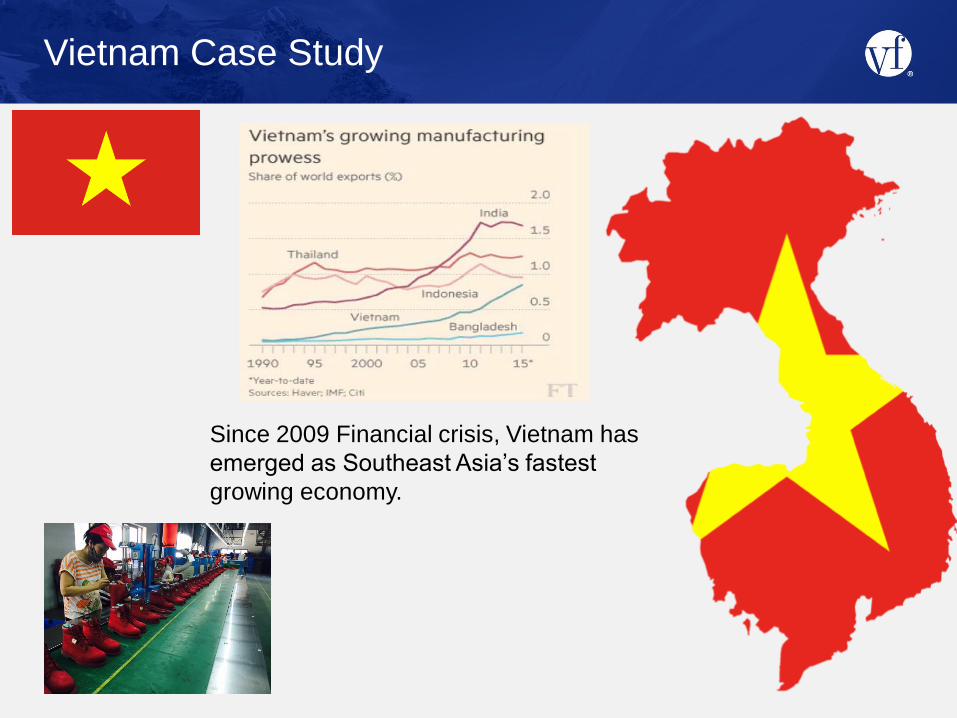

Vietnam Case Study

Since 2009 Financial crisis, Vietnam has

emerged as Southeast Asia’s fastest

growing economy.

Vietnam vs. China

Population Employed

Person GDP per

Capita Minimum

Wage Wages in

Manufacturing Inflation

2016

95 million 54 million USD2,111 USD145 USD240 >5%

1.3 billion 774 million USD7,925 USD320 USD700 2.32%

Vietnam Population

Source: Ministry of Health, Health Statistical Yearbook 2000

• The current population of Vietnam is estimated at 95,105,502 according United

Nations estimates.

• 34.7 % of the population is urban (33,121,357 people in 2017)

• The median age in Vietnam is 30.8 years.

• The population is growing at an average rate of approx.1% per year.

• As a result of immigration the population is expected to fall.

Vietnam - Inflation

Inflation:

2008 record high at 28%

2015 average below 1%

2016 average below 5%

2017 above 5% in Jan & Feb

Minimum Wage Inflation:

Wage growth has declined from 15.2% in 2014 to 7.3% in 2017

1 USD = 22,500 VND

0 ₫

500,000 ₫

1,000,000 ₫

1,500,000 ₫

2,000,000 ₫

2,500,000 ₫

3,000,000 ₫

3,500,000 ₫

4,000,000 ₫

2013 2014 2015 2016 2017

Minimum Wages in Vietnam

Region 1 Region 2 Region 3 Region 4

↑ 15.2%

↑ 14.3% ↑ 12.5% ↑ 7.3%

http://www.tradingeconomics.com/vietnam/inflation-cpi

http://www.wageindicator.org/main/salary/minimum-wage/vietnam

Region 1: cities and provinces with highest living cost

Region 2: next tier cities and provinces

Region 3: cites and provinces under development, still

need support to develop manufacturing

Region 4: remote cities and provinces that heavily need

support to provide jobs and improve the living

standard of its residents

Total Footwear Export Turnover in Vietnam

* Vietnam Leather and Footwear Association

Country 2016 Turnover in USD

2015 Turnover in USD

2016 vs. 2015

USA $ 4,483,340,500 35.0% $ 4,077,096,419 34.4% 9.96%

China $ 904,927,071 7.1% $ 754,185,864 6.4% 19.99%

Belgium $ 825,444,140 6.4% $ 723,555,968 6.1% 14.08%

Germany $ 764,676,582 6.0% $ 705,549,900 6.0% 8.38%

Japan $ 674,814,835 5.3% $ 597,579,005 5.0% 12.92%

UK $ 618,375,518 4.8% $ 693,587,418 5.9% -10.84%

The Netherlands $ 595,148,795 4.6% $ 533,738,850 4.5% 11.51%

Other Countries $ 3,960,371,064 30.9% $ 3,760,478,387 31.7% 5.32%

$ 12,827,098,505 $ 11,845,771,811

Vietnam – Footwear Industry

• 2016

• Total footwear exports in 2016 :

• Textile footwear : 46.7%

• Leather footwear : 33.3%

• Other Materials : 20%

• Foreign Direct Investment (FDI)

• 81%, mainly Taiwanese and Korean companies.

• FDI increased around 3% year on year in 2014-2016

• In 2016, the footwear sector in Vietnam grew only 8.2%, against a targeted 10% growth.

• This as mainly due to political uncertainty, particularly around the British separation from

the EU (BREXIT).

• Korean and Taiwanese manufacturers are starting to move production offshore

to Myanmar and Bangladesh.

Vietnam – Footwear Industry

2017 Forecast

• In 2017, production is expected to grow by 5% and export turnover is expected

to grow by 10% reaching US $18 billion in value

• China continues to advocate cutting investment incentives in the textile and

footwear sectors to focus on industries that have higher technology and value

add.

• Vietnam will be the main beneficiary of footwear moving out from China.

• Exports of FDI enterprises are expected to increase as enterprises continue to

expand their existing plant capacity and build new plants in Vietnam in

anticipation of the opportunities to reduce tariffs from trade agreements such

as EVFTA. In light of the recent European Union-Vietnam Free Trade

Agreement (EVFTA) for the EU markets about 80.3% of footwear tariff duties

will reduce to 0% when the FTA comes into effect, which is expected for early

2018. About 4.7% come to reduce to 0% after 3 years and the remaining will

be completed after 5-7 years.

Vietnam – Footwear Industry

Expected Challenge

• The Vietnam Leather and Footwear Association notes that the rapid

development of the leather and footwear manufacture in the country has

created concerns related to the environment, especially the production of

leather tanning and fabrics for shoes. More focus on this area from

governmental environmental agencies is expected going forward.

Strategic Sourcing Responsible Sourcing

Sustainable and Responsible Sourcing – Why it Matters.

https://undark.org/article/leather-tanning-bangladesh-india/

Supply Chain Risk – Business Continuity Planning

Potential Supply

Chain Disruption

Activity up, down and across the supply chain

Strategy

Plans

Urgency

Business survival

Document Set

Thank you for Listening!

![10 GSM BSS Network KPI (Uplink-Downlink Balance) Optimization Manual[1].Doc](https://static.fdocuments.in/doc/165x107/53f87678dab5ca0a678b4eda/10-gsm-bss-network-kpi-uplink-downlink-balance-optimization-manual1doc-558444c3ef615.jpg)