OPTfMALMANAGEMENTOP TJiE.WOc)t.ageconsearch.umn.edu/bitstream/147483/2/1993-03-01-03.pdf ·...

25

OPTfMALMANAGEMENTOP TJiE.WOc)t. DESTAND rHEWOOL La Trobe university The collapseo! ilt Febrtl4ry199ilej'ttite Au.ttraUan wool lrnlustry h()/dlnga 4.73 millian baI4st(JckplleofwtJot. close toa normal yearts productitm. 8etween 1989 and 1991 Ihc IndustrY had spent more Ihan $4.S billiOt, in U.s UHSl4cCt,fslul attempt to .rupPQrt thcpr/cd, and had accumulated a Goyernment gU(J.l'ut1 ' /eed debt Of $2.7 bllllon. the Wool ReaitsatiQn Comml'sstoli was created by the Government fit 1991 to t«ke over Ihe debts and (1JselJ of the Wool It the tMk of selling the SICCk.r, collecting (he wool tax qnd repaying the debt, The Oovernment has set down tn legislarton a ttmettwle which the minimum rate at which debt mllSt be repaid. Managing the waDI (leht and the wool ,vtockpiJe Is an IhtrifJSlcally dytwmfc problem bec(tl.lse tlte rates at which wool Is sold and debt repaid affect the world prIce of waof. In thl.t paper an apttmal comra! l11Qdcl is used to determine the debt and J'lOck tttafUlgemem which nm.xtmtse the we(!are of the wool industry wlztle respearing the requirements lor debt repaymem. It IS /tmnd that the Jeglsltlled debt repayment program Is nUlrc rapid than would be chosen by the trnlustry 10 meet the 1998 target lor repayml!nt of (t/l debtt but the industrY's pre/erred time palh would be riskier for the Ooyernmem. The wool lax and sale Qf stocks arc both re(luired to repay Ihe debt. but the balance between these twO Instruments depends among other lhings upon Ihe elastiCity oj demmJd. The most sttikfng result Is the low shadow price or economic value o/wool it.t the sUJckpiJe. This means IIUi/1t would be very profitable /0 jimJ aliernmive uses or markets/or wool In the stockpile. even at quite low prices. To dtJ so would Mt be easy. bcccwse it would be t!ssemiallo cn.$ure th4t this wool did not the world market. However very large sums of mcmcy 'ftC Involved. and a significahte/lart to explore tltis option w()ukJb.cworthwlu'le. 1 Paper presented at the ,\Js/'tua/ Cmtj'erence 0/ tIlt Au.$tralian A8ficultutal #conornics Society. Sydney University /993.

Transcript of OPTfMALMANAGEMENTOP TJiE.WOc)t.ageconsearch.umn.edu/bitstream/147483/2/1993-03-01-03.pdf ·...

OPTfMALMANAGEMENTOP TJiE.WOc)t. DESTAND rHEWOOL stoc~PILet

La Trobe university

The collapseo! w()()lp~IC~$t4iblilsati()n ilt Febrtl4ry199ilej'ttite Au.ttraUan wool lrnlustry h()/dlnga 4.73 millian baI4st(JckplleofwtJot. close toa normal yearts productitm. 8etween 1989 and 1991 Ihc IndustrY had spent more Ihan $4.S billiOt, in U.s UHSl4cCt,fslul attempt to .rupPQrt thcpr/cd, and had accumulated a Goyernment gU(J.l'ut1

'/eed debt Of $2.7 bllllon. the Wool

ReaitsatiQn Comml'sstoli was created by the Government fit 1991 to t«ke over Ihe debts and (1JselJ of the Wool Co~pt),.atl()h. It h~ the tMk of selling the SICCk.r, collecting (he wool tax qnd repaying the debt, The Oovernment has set down tn legislarton a ttmettwle which 8ov~rns the minimum rate at which debt mllSt be repaid.

Managing the waDI (leht and the wool ,vtockpiJe Is an IhtrifJSlcally dytwmfc problem bec(tl.lse tlte rates at which wool Is sold and debt repaid affect the world prIce of waof. In thl.t paper an apttmal comra! l11Qdcl is used to determine the debt and J'lOck tttafUlgemem p(lth,~ which nm.xtmtse the we(!are of the wool industry wlztle respearing the aovernm~nt's requirements lor debt repaymem.

It IS /tmnd that the Jeglsltlled debt repayment program Is nUlrc rapid than would be chosen by the trnlustry 10 meet the 1998 target lor repayml!nt of (t/l debtt but the industrY's pre/erred time palh would be riskier for the Ooyernmem. The wool lax and sale Qf stocks arc both re(luired to repay Ihe debt. but the balance between these twO Instruments depends among other lhings upon Ihe elastiCity oj demmJd.

The most sttikfng result Is the low shadow price or economic value o/wool it.t the sUJckpiJe. This means IIUi/1t would be very profitable /0 jimJ aliernmive uses or n~'W markets/or wool In the stockpile. even at quite low prices. To dtJ so would Mt be easy. bcccwse it would be t!ssemiallo cn.$ure th4t this wool did not te~tmter the world market. However very large sums of mcmcy 'ftC Involved. and a significahte/lart to explore tltis option w()ukJb.cworthwlu'le.

1 Paper presented at the ,\Js/'tua/ Cmtj'erence 0/ tIlt Au.$tralian A8ficultutal #conornics Society. Sydney University /993.

OPTIMAL MANA«lEMENt OF 1ftE WOQLP~Br ANI) THE WOOL $TOCKPILEZ

I In.tmduc:tl~n

Over the last twenty years the Au.~traUan wool mdUstry ha,~ mtervenedlntlle w()Ol market~ buying and sellitlg subsrontlal qUllfilitic$ of wool in otQ¢t to "proVid~ ~t\tet stabUityof wool prices at maximum sus~ble levels. subject to the costs of Stockholding" (AWe 199(». Oespite the·jnitial skepticism orman), economic commentators. Ute Reserve rrice Scheme s¢¢me4 to work tea$Ollably w~ll throughout the 1910's and most of the 1980's. Price instability W~S JUdged by MOst observers to be nQticcnbl~ reduC¢d. Government involvement in this grower funded scheme appeared to 00 mWmait nnd the Governmertt seemed to have avoided beinS drawn intp wholesaIcsubsidisadott of the industry.

However. towards the nOd oflhe 19S(ys things began to go ~riCIUsty wrong, In 1981 .. 88 wool prices rose rapidly as stocks ntH down. 'n10 Wool Corporation tteated the pric~ change as pennanem and raised th~ Reserve Prir,¢ to a level well above any reasooable long t<mn eXp¢cUltion. By the end of 1989 the Cotl'ONttion was buying hcavUy to support this price. Overt1:te m~xt eighteen months more Ulan half Of all wool offered for sale was bought by the Corporation. Stock$ rose from 9 thousand bales f.l1 June 1988 to 4.6 million bales a.t the end of 1990. mot\1 than double proVious histOrical peaks. Over this peliod the Corporation spent mom than A$4.S billlon defending the prlOO. Figures I to 4 show the history ()t~prlceSt stocks, debt and butYcrstock support from 1974 to \992.

In February 1992 the Oovemment imervened nod the attempt to stabilise the price oame to an end. Prices fclllmmediately from 700 c/kg to 430 elkg. 'fhe Wool Corporation was restrucrured and the C;Ovemmcnt established the Wool Realisation CommJssion to take over and manage the main assets and liabLlities of the Corporation. PrinCipal amon~ these were a 4.73 OliWon bale stockpile of wool, and a debt of AS'},.? billion which by now bore u fonnal Government guarantee. 111c political economy ~nd the economic factors contribUting· to the ~Uapse of wool price stubilisatlon will nOl be discussed here (for an anillysis of these see aIU'dsJ~y 1992 and Watson 1900).

2rWQutd like It) thank a humber of cQlIeagues.including in particular 000(( Edwards, Jobn OICQnnor. Bab Richardson and AUswJt WatSon for holptu! di$CU$$fon$~ l would like to. thank red Sieper for helpful c(jmments on spe(:ulaUvc ~u~k at an ANt] semlnar.l would like to Oumk Roben P~teim and Elil.abeth Brett fot resenroh QSslStilnce Md the Wool Rese,wh and Pevelopmen~ CpilX>ruUon fot rlJ\llllcial support..

tnthis p~per 1 $ball.C(Ytl$idct the qU~~9nQr how 'me Wool R¢aIisaUQf4 Commission sbould manl1ge the wool debt and th;w()(l!$WCkpUe. The.CQfilmts$ioo ha$ tW0!n$~uent$ whlcb it can \t$C. tbe tirnt (jf~ is t1~ rute at; wlUc~UlestockpU" Is S<)hl mw the world mwk(:L ltl$ genentUy"gteC4 Ul1lt AustntllB h~ some matk¢t power. $()$eUh1~ dOwn$~ks hi1$ the¢f(ect Qf depf¢$SiUgtl1~ wOQl pri~t\$ well itS scnetaUng rev~nQc wbich. ctm be US«it~r~bt~du¢ti~.11lC $CcondJn$uumcnt ls the Wool Ta%. an;1(J ViUQnml,~ whicb 1s l~vi«! cn wool JlrtXiucU~ln. Tm Wool TaxrniSC$U~ c.onsumcr pdc.c, lowers the. producer pdc-e. Mdgenemt~tevctll1e whlch¢~ ~' used fot debt tWuctkm~ Strledy spe~ng. theReaU$a~onCQmml~$lort does not have the i\utbotity to vnrytJ'.c Wool T4X but it is inUuenUalln advlsingUlt) Ooy~mm¢ntm thQ ltW¢lofthe TaxfMU It will ,be assutne<l here thUt tffi$lrt.~tn~rn¢nt is under 'the. ~ntrQl Qr th¢COfntnissioo.

TheR.¢aUSiltlOn Com.rmS$ion is in a pP$itionUke that of the re~iVK!r of nn WsolventbOdy. ru-.d ha$ responsibUides bmh «> the Oovcnunent ~. to Ole woolindusU'y, It is thus rt\~ wUh p!:)t¢tltially tnCOtlSt$Wnt :,uldcon!UCt1tl8 objectives. ThQ· Oovetntnent wishes to $e¢ Ute wool ~btNpmd promptly Md ~'Wtety by ·tbe· iOOU$try. f{owevetpoUCie$ which.leadtornpld debt repaymetU h4ve tlleeffect of reducing the ru·tlduc~r price Md ~uemg Ul¢ mC9mcof the woorlndtl$bj\ The toW value 0(: the usset depends QnUi¢ tlmc path o(:dispo$~. Jtnd .~~. time path which mwmiScs th~ value of the t\SSCt may impose severe though ttafi$icntadjUStnlenlCOSf! on Ule wool i.ndustty* In $Ctting up the ReaUsation Cottunis~ioo the Oovcrnment was v~ry COOcttl1ed to resolve this potential con,tllct or obj¢ctives.

1991~92

1992 .. 93

1993,,94

1994--95

1995·96

Of!bt n~llyrr,cnt Re<lulr~d

($m)

300

soo S,SO

If'

1996.,91 r~--------~------~--~----~~------------~~------~ 550

1997;;98

--~--------------------~-----.------------~----~ n h~lS been shown~y IJatdsley 1992 thut the ultimate SQUt'CC QfU,ls ~lcort$istenu)' is Umt the Government hrus ~tUaromccd the wool debt. eitherexpUcitly oritupUciuy. but the cost of this 1,Warantechas tltx been passw on Je) th'" mQustr)', ·lbe indUSUYUIUSCQeS tl<>t see the lilUcost ofits debt ~U does not rnce the in~nUves which, wQUldlead it ~ choose n socially op~ima.l dcbt management pollcy, A ~bt guatan~ is a contingerU .aSSCJ, .~ aamsley has shown how fO pri~ thiS ~e.t uSing option pricing methOds which fake ulto account t«¢ paUl d~pendent vtuue Qr the asset. one approach which mighthuve ~n tflkrmby tbcOovctnmcm. would be to huvc charged the

R¢mt~aQonCommi$$iontbe appropd~ pdte fOJ~theOQvemm¢nttnl~eeQf 11$ debt, TIle C()1nntt~siQrt cowd then havo b¢en$at~ly ~tQmaximi~fll¢ wetr~i'¢ of me wool !ndustryl l1Je lndUr~ wOtlld fC¢Q~se •. Uuo\lshthcCQst of th.el0;in.rJ~tt¥ blrmptie.e it w~~payIDg fOrit$ debt and wouldtnatlaStHh~ debt·Md th¢$ttJ¢kpUe in t\$oclallyr:ftiCicntway.

this i$ not th¢(l,pproach. which wasadopt~~ ruth~r than adju.pri~~ t,O¢Qm.'!~t fora missing matket1 th~ .OQvemment chQSQ. to regu!atequantiijc$, it ~tdown Itll¢$i$laUooa dcbl~d~ctit)t) sch¢dole which the CommisSioo .1$. rt:quimdtOfflect. This has me ~dvtmt4geofbein~$ttrught forward. cleat and very Vi$ibl~ (see table t).FoUoWinS this spiritt UWU1·\:». ~sumed in ibis papet that the obJecUve anne R¢~lsati()n Commission islo rn~mtseUlc. WQlfate orUle wool indUstry subject to the CQnstnunt of thu d¢btrepaymentsch¢4Q.l~s¢t etU in Table 1.

The optimal ttl anagement of wool stooks b~ already bce~ COOSidet-ed ins¢veral Swdi~ (BturlSll!Y 1991. 1992, Stoeckel el a11990. AU ARE 1990. 1991 ).\Vhatdiff¢rcn~3te$ th!s pap¢rfrom carner work is the recogrtition that debt and stO¢~ lnan~gcOl¢nt are mtimat¢t~biterlmkedt income raIsed by sclUng off ~ wool stocks Cml not be ~tt~medto wool growers by a lump $Wll. tmnsret. tt must be used either to pay o(t Ule wool debt or: retum~ Vi~ jl Qi$tornooary m¢chaniSm of ot}csort or another. [n the abS~nce Of a lump SUtn rcdi$ttibuuve mecl'ulni~m the shadowJ)rtccsof debt Md Qf wool in st~k arc interconnected. Some preliminary wont related to thlslssue wil~repo(ted tn BardSley and Pereha (19(1).

II An Optltnal Control model

Managing the wool stockpUe is aninuinsu:aUy dynamic problem, If wool is sold too mpidly. then the price may l:K~ driven dO\"ll excessively. The industry would like to ¢>;.tmct some benefit from its rnatket power by reducing supply. On the other hiU1<!, slow sates mcur st.or.1ge nnd fUlan~ng costs. These rmancmg costs dcpcndon the level of the debt if thc~ is ft risk premium as$()clawd With hJ~h oorroWing levels or if, us in the present ease. thoro ate constraints on future. debt levelS. to understand this pnlblcm it is us<:ful to express it as an optimal ct,ntrol problem.

The state variables are a, the Jevel of debt. and 'II the level of stoc~.s; Associn~d wifh these ShUt} variables are CQstate variables or sh~dow prices yand <1. The shadow price 'Y is the marginal value of M extra bale of wool added to stocks. This "'ill genelil11y be less thanth~ market price because rele~ing wool ontO the markctraiS¢s revenue butft also has Ute undesitable slde effect of reducing the market price and loweling the eupitru value of the stock. 1be sh~dow price a is (he value to the wool industry 0: ·$1 in revenue allocnr.eu to a reduc~on in fbe wool dobt, this will generally be less than 1 (wh.ich would be thl,) valu~~ or a $1 lump bl1m tmnsfer) because the induStry. II not constrained by the l~payment schedule. might not choose to aUoca~ Uus revenue to debt repayment.

The control irt~trl1mcntS in Ulc hands of the Commission are Ule nne of stock release Md the Wool fax. but it is more convenient. insetting up the model to take as control vruiables the producer pril'.e ~ and the consumer price p. Th¢ Comtnissiprlcan manipulate 1t Md P by appropriate choIce of the stock rolet1$e.and tax m~thlments.Oivcn the control yarlnbh~st the sune evolves according to th~ (alloWing equations of motion.

(I)

4

Sere) ;:::: 1 + e(1r~ 1)

O(p)= l~l1(P~l) (3)

(4)

are the supply of w®lby the Austtallan wcol mc.tlJsu-y MQ the world cJcmiUld fot wQOlnetot produCtion outSide Au~trana\ TIlt; supply and demand curves ate us~umedto be Uneru- in Ul¢ reglon of'i(ue~st andpti.ces atl4qu~~ties·ru'e nonnaliS¢d·.so.thattn ¢quUlbrlum. whentheprnduC(!r price equals the consumer pricc. prir;es andqutmdties ~ au ~ual· to unity. e and 11 ~ .tl1e. supply and dem.and ela.\ticit)¢$at this· ¢qUUibriumprl~,

The ntSt of Ule equations of motion states thatU1e mt(tat wlJjchStoCk$gTOW is. giycnbylbe tmbattm.~ between $Uppty n.nq dem~nd! ~mes¢cond states that debt is wCt¢a$eQ by mwr.eat charges and storage costs, arldthat it is dccreasedby revenue (rom $fOCkpUe s~es and QY fi!VCrlUC from t.,~ wool tax leVied on lUPwcrs. This equatiOh also descrU)¢$ bow any ptoUtsfrom sellfngstQCk$.ate returned to growers as t.l negative tax or productipnsubsidyOnce nIl Ule debt is pald Qfft

TIle ccnstraint$oopoUoy are that stockS mu.~t be non negative, tU14 thatd¢bt roust be nQrt tl¢gattv¢ and less thatllhe credit limit (U imposed by tCgishlPon. (JJ is a step function that de~rt;Me$through time as set out in Table 1. With each of these thXl.!eC(lnstmints is usSOch1tedaLttSlittlgemuJUpU(!r (J.h A.1I Of )."a> which measures how UghUy the CQt1Str~t bJnQs. The Objective fllJi~UOn which the Renlt~ttf;ion Commission is assumed to m~imtse is the uetpresent valuo Of producer surplus liubj(:Ci 10 aU these static and dynnmlc oonstmi!l~. This objective cun be described by the cummt val ueU.wuUtOhian

j(

It = I S(~)dz +y(S(~) .... D(p»-C(ld +Sq- pD(p)+ 7tS(1t»+~+ ~ld+A.~«(t)-d). (5) o

To maXimise this objective one must solve !l tWO $Wfe optimal control problem wi.th i -quaUty constraiftts on the state variabJes. 1'he objective function is quadrc1uC but the control equation (2) is not Unear, so standard lJnear.qundr'.1QClllethOds do not apply, ProblemS of this type axe quite difficult:. and both the conttt>l variables and the cosuue vUrlubles can Jump discontinuously (CW31lg 1992, Chaptet 10), acforr; fonnally solving the model. it may 00 useful to dJScuss some of the things which have ~n left out.

I1rst of aU, tbcte is no lU1CCttlPniY. there is a SlMdatd triok whichaUows one to handle uncertainty in Url¢M quadradc models, but It. does not work here beCtlUSC of .000 Une4rityil'l the control equations and {)ecauseo.f the state spn~ cOfi$tt'iUnl$. ToiJltrQduce uncetUUnty wOlud nda .greatly to UlcdiffiCulty of sulvfng ti1e mOdel. To some cxt¢nt f.be ef(ec;t ofuo(l.¢tt.a1my can be cxplotcd by vatyin$ Patamc~f$teJUtCd to the smmgthof the, matketin ot(lerto tl.~.~ how tho optimal t¢spoo..'iC may chtUlg~J Secondly. th~rc.tU'C no production or consumpdtlr\ dynamics! Pnxlucets and COflSumers at\l a$swll¢d to m()veb~tant:me®slyooJO the.lr $Upply or demMd curves nnd Q.U dynamic cf«:t;t$ ilro inUt>du~d t.h.rougll tong Uv~ stQCk tul(l. debt vanabt(;S. 'Ole effect of tbts omisSion is tOunderesUmtllC adJustment COSt$, leading to solUtion pam~ whicb maybe cxcestdvcly

vari~te~,PzWtl~Qn ~yP~C$COu1dbe,lntmduPe4cith¢rbYintra4ucms $Qi;tt~wfultad b9C a~J~¢nt14i$ (whlchm~~. W~lf~~"QlIliC$ ~tOmteJPrct), Pt~rhaps llY mttQd~¢inga UUtdSUite vanaPle (thenumberQ($~p)~. nl~ would ,a1$om~ ~ mot;i~lm~bbatd¢tIQ ¢Stimale, ThttaIYinom;l¢~<lmlQot exch~$Q J;lt.e.efft~1Sa~~dettd.~ourthty.~ w()Q( mark¢t·~pf COtt!1eIDUCh m¢re~mpU~ tbwl bM~n$UlnlC!$~d bert.m partiCUlMw wool lsoot ahqmQS~It..Qus~m~tY~·u.04 botbUlQ$upply ·andd¢niant\eb~tiStiC$ pf.tlnewbPls are differcntfrotnIDQ$C of CQiU~r w()Ols\

rimUly thenl isotleMsumPQOn wbtchi$~pUctt ln~Ar)aly$ist 1b1$.1$: that 'tilt"'· .l$·nQpriV(ifC stock: holdiugm ,~sY~1ett1f.lt is weUlmPwn ~.privmc, ~cUl3m.-swUl putchflSeStQ¢k$ imme(!i4telyltpriccs ·~UIlddpa~tQmcre~m a ·~tc}t~at¢ .. ti'@l. nl~ rtskAdj\ls~mtctestti.lw. ayaom~ so.$~cutat()rsutldermm.e tbe;l$~(JptiQns Q(UleJU9de~ ~d alt<!rUi¢.COUi'$cOf pnt(!$ {Salam. 1983)1 lnmosl or the Bim~atlQn$ ·Pt'¢$dl~b¢.lQWUl¢m ,is' in f~t .~jUmpmUle ,¢('n$Ufflet price whenstoclts.tun out which WQUl~ bwite ~ ~cul1.\tlYeat4lQ"; In prinCipleM~ could ~dd a COt1.t{U'ai,nt to .~. moocl whicb prevel1tedptic.eSrl$ingf~1¢r marnhe blt¢test raWl Qn(!. ~U1d alsQ eV~\.tateU1c w~lfare'effect$ pfaUQwtng a s~cutauv¢atttL¢k m w.k¢p1acc• This .ha$. n(lt~n done. patUy beC:;lU$t it wOUld. add we:lUY ta the ~mpte:dty of ~ mOdt:l anci part1yb¢Ctu,t.~ if one wished to· study UUSi$$Uepropenyone ought ats() toincluQe thcmter11CUonof fU~v.re$marlcct$ with specu!adve Ilttack. to practice. if the RealiSation ComlntS$ion wiShed to avoid the d~k Qf speculaUy.e attack it wouJdtl1etcly need to UlpeJ' off tha )1l1e of stOCk sw,es as the. stockpile wa~ exhausted

All models le:.lVC some thing$OU~ either \)eC;lUSC they areinessen,nl\l and. obscure the main meSS,age Of ~cal\se wey are too ~ffioult to include. The streng11lS and Utnitations of tht: cuttCtU mOdel Will 00 di$Cuswd latcr when tesu!t.~ ar{1 cOnsldcred.

m Sohingtbe model

By differentiating the Hamiltonian with res~ct lOthe control variables One calculate,s the first order condiUons

(1~(1)SOt)+(y-<m)S;(1t)=O

('iD(p)+(y-qp)f)'(p) ;::0,

'fh¢se can be solveQ to express the conttol variables us a funCtion of thecostatc variables

(1 ~O')(l""e)+ye n=·· ... , ......... -(1 .... 2a)

6

(6)

(7)

(8)

(9)

'me ucood order cooditlQIlS whIch ~~~u~tM~ the .HamiltomlUl.l$to~YJ11~S«f·al·".$atisn¢d

provided tUtU' (f>~.1bf$(;Ondi~o.l ~Ql¢t bl·~··~ numerl~ .$tmtllattot1Spt¢$Cn~41atet in the paper,

In order to y,nde~'mq tb~(ir$t P(det tonditiotlS, CQnsi~r {it$t ~ C?.$e wl1erethe sbadQW priee'111~ set equ~ to urnty. 1bey~an thenbetewri~ll .

~~r .. ...... ,-1 .. i p - dt!ftt4hdt/(l$t/clry f

These atl~ sU1rlght fotw:ttdCOlldiUotl$.for u .mooot)Q1YfiUPpU¢t, The flf$t$~teS th~ th¢ CO$t$Q.r producing wool on the f~tmsb041d .b¢~~ted.aUbe MntSitl; wUh.ltlf~<C()~1S of t¢1~asb18 it [rom h10Ck (themargmal, vuh,1e'of wootin $~k· beingmeastH'e(i byitS$hadowpri¢e'Y).1be Seccmd St:it¢s ,Um~ lhemonopoUstfsmark up should 00 reJ~ted in the usual way to tb~4¢1n~¢hl~UCfty~ However a is not. ingener~ ~U;U to unity. and when. th~~ is t~cnJnto ~oum one $et,S thtMt order conQiUOfl$ 0.) and (2)t S¢¢FigUN S. which sh()wsdj~gnunmatfcauy·lh¢ tQst of me¢iWg supply and Figure 6, wblctt ~hows thecQttlpOJlCnts oft¢venue weigfU«tby lbcirshUdOW vaJue to the wooliIlaustry. .

The di!fetCn~a.t equations uescribing th¢dynumics of th~ ~ viltiables can·b(! derivcQby diff¢renUating the Hamiltonian Wfal re~1?Cct to the costate valiables,. ttnsslmpty recovers equations (1) and (2) which h;'V\1 already been st4t¢d. 1becqu~UQf1$ descnbing the evoluuon of the cOState vadables. which can be derived by tUffe~nUaxin~ the· ffamU«>rnan WiUl r¢sp¢ct to·rh~ SlAte variables. a.re

y =ry .... eq .... ~ (0)

6 ;:; (r .... l)a .... A (ll) where r is the ~~ount rate I and ~ and h:':~l .. A,2 at\! I.tugrange multipliers. The state variables the Lugtililge mulupUets satisfy complementary KUhn Tucker ineqqaUties

q~O

JlaO

qJl== 0

O~d$C1)

A~Olfd;:O

A,~Otfd:#cu

~ ~ 0 if 0 <: d < (I),

'7

p

s

trigureS C()$Is

ItflWre (} Revenue

D

J)

1bf!litst of these codyn:.tm!o equations stmcs !hat whU,,·cverstock$ rcm;tln a.bQvc Ule posiUve con.~tralnt theshaQowpti~ of wool fol1Qw$ a HotelUns type offule. If the .stQrJge cost e is zero tben the shadow Price rises Iltthe n\te orbile.~sh ire is hQt1~ro tben y chMges u~ a rate which makes Ole pupital aain from holding stocks equal to the interest rate.

~$«ond equtltSQn$tate$ that It~btf$UJ1@S~ U}(!nq,.~W$elPQn¢ntf~y at~. ra~~v¢n by tl1¢ dlf!e~rt¢e '~tw"nth~d1$~unt~l4 ancHbe fut~~t f'Jt~.Jt tPA diSC()Wlftlt¢ ~d uw inte~st r,~te .~. U\est\lncthena·J# ¢()t~tUltOuthiim"'j but it $~e)llS u(slikely ~'lhis willI»· $(), st~ th~int~re$tra~l~ OO~: wlUchi$ ap~ropti~~J~ OQv#mment$$~.~·dc;bt·wbU~.~ ~@Yntrnte uppro(Hi3te.lQ wQOlatQw~{$ WQul4dIt(er fJQn\ ,UU$ bi .. It)l$k premium .~pprwrin~ w priya~ btlrrowing or lfiVC$UUent. HQw~yerthl$.Ho~Wns tYp¢,Nla~Qrt$hJp b<'ild$ QJlly wMn~L;igrMg~ muldpllerA. L~ zcro# It seems pJa~lbl~tltattt~ wUl alttto$tn~v¢r PCCUf jJlU4~problemstudJ¢4 'be~ since it s~m$llJ(¢ly Ut\tUl¢ d¢bt wUl oe ~~ nlQU of the tinle by Ul¢Oovernrn¢ntlinPQSed repayment s¢he(h~c.

k,Vn,en'Ultgitnll 'Valpeot $tO~k5

A monQpoll$t faCfns nninelU$ti~ Q(!IDandtl}l!,\ht actually ·wtstHo destroy stQQk$. ~dl)CiogsU,)m8c cos~~ Md toruing up pd~~.For such n mQJlQpolt~tlhe shadowpricc of wool wOtUd~ negative. Crut tMt happen here? Som~~nformtUtQn. Qunoo gruned bY1OQ~sat an rutUlCi.~ st~'ldy stu~ where stoolt.s and debt ~. constr4ln¢d to be 1~ro IUld supply. demand! producer price and CQn.~llmer pnec arc aU unity. It 1$ c~~)'to show that

Three regimes are possible. if demand is inel4.~itic and the c4pit\!iscd stofJge COSfS Ute low

e .' l"n lspecUlcully if ..... <; -- }t U1Ct) boUl me Lugrdngc MulUpUcr 1 and tllC shadow price A(tH'C r n

hegative. In this situation Ule steady state cor1t~tr41nl is binding sux:k.-, fr<>nlUbovc. tnll~S th~' steady state can never be an equlHbriUffi Clnd it is opUmal for stocks to srow witIlout bound. Itt this regime of explosive growth it is tm,fUnblc n)r stOCk-purchases to IX! f\mded by the wool ttlx. Costs nSCJ bu~ revenues rim at a frt~ter ,...-tc. The l11te of stock I1cqldsftitm is sucb UUlt oonsumet pricea rise tnt.O the region where demanubeeomcs eltl.~tiQ (secl:igutO 1). The ShJlOOWpnCO is negulivc t)fJCtlUSC an addition to wool tltQCk..~ ccnUibtH¢$ only rut ttlfifdt~ stream ofswr~ge CO$f$W the c~h flow. It should b¢ cmphM~~d Ul"~ this tendency to jlccumulate stocks OCClJm onlybccAuselho~ is nt, policy Jhstrument (such (1.' a production quota) whl.cheould be used to res trl ct supply, und Ulcre is no lump sum in.~trutnent to redL~trlbUt(} la>t rcv~ntle to wool growers.

1) S

Ji1gure7

'fhe c/ft'(:tof st(~*ucqufsiUon itdemand I$jheh~1lc

tn the second regime where dcmimd is ioolnstJe but storage costs are relaUvely higher. yi8 nl!gnUY~ but h. Is positive. Stot'llgl,'. cost~ rcstroJn the growth of stooks and the steady staw is lin e'luUibnurtl. To suy that y l~ negative mCfUlS that cosUess destruction of stocks would ~ protlUible. 11lts is itl comrnst to the first rogime where it i>J profitable in effect to destroy stock.~ even by the reJAUvcly expensive method of storing them fOr tU1 infinite period. In thu third ~gimc demand is clastic. the b1CIldy slam \;) (Ul equilibrium. and stocks have uposftiv¢ value even at Ole margin~

tn aU 01e numetical ~imuhujons presented oolow only the second two m8imes occur. tn some cJl.~es the shadow pnco o.f stocks is negnuvc. but never to the potnt where explosivu stock accumulatJotl becomes uttracUve.

V Calibrating mad solving tlle model nUlucrlcaUy

Bec."use of the mm Uneruity t)r me contn)l equations and th¢ prc$en~ of inequality COtl.,trIliIlUi on the states.lt is not possible to solve the model analytict\lly. One common approach to the mnturieta soluuon or conU'Ol problems is to solve the system of dyt4'UUiQ differentia.l equatiOtt~ forwnrd In time :md the cooynamic eqtJatlons describing tb~ evolution of tM· cos~te variables backwards in time. nnd to patch together thfs ~wo point boumJAty problem, U Js neccssary to pay attention to boundary values. aod tt) SM lhnt kinks Md comers in thl) solution arc handled appropriately (sce ChilUlg 1991), Unfortunately there are many tWists. tum$ Md kink.q in the wool problem. CoJt~tntints switch on Md off in a complicated varlcty of wuys, Md the mef.hod based on differential equations provw ImmctAble.

lO

._ ..•. ,

fort\ltln~ly. amorc ~ctt~¢lmlquc WA$SUC~$$rUl.,llprov~ t<l~ po$$iblttQilpptoxID1Atetl}Q pn>blem byu Qj$ct¢t¢ppumiS~tiQnprobl~Q\ WiUlalargeb\1tfinitQJlumb¢t of$\ate vartable$ Md con@l vadabt~$, ttii$ (iJScn;(¢probt¢m Was SUticeS$M!y solv(!(i tfi OAOS.SU$mg nqm~ri¢at hUt cli.mbifigmetllcxl$,To ¢nsun>Ul~t agcnu.in¢ $Olut{QnWatt ob1nlne4 tome Original p,robl¢ID,.pri@$. shi.\dow priCQ$ (Uld L~snm8~ multipUet$ were c~l~ul"ted n\lrn~ric~uy n,ndlt WM velitied lhnt~ nrstord¢t cottditiOml did in filet bOld along the opUntldp~at 1"geJt$t1tQ Ul~t Ul~ ~lg9rithm wa.~ finding u toem muxunum the eigenvalUes Of the H¢S$bm wore otUculal¢dMdi~p.;¢tCd

In setting up til¢ mod¢l. the following PSSumpdOltS w~~made3. T'h¢ wool market is volatile and. chnngos from day to day.rulu any U$$UmP~Ons0rtthe state ofth¢ m~rktlt nm somcwh~tID'bitnU)'l For me rJurposeot thi$ study u snapshot of diQiOOU$try \'1M taken I)t{hecnd of June 1992. At Ulat, time the level of $lock$ WAS ubout 416tnUUon bUlc$. or800k4 ~ml UtO wool debt we~~ nbou:,. $211 billion. Th(: R¢aUS~UOJl Commission has oU~<;r MsclSbesldes wOOl; ln4Wy l1)al C$tate And wool Stf,)1'eS. 1'\cs.c~sc's nre Just M difUcuU ti) vntu¢ U$ me wool. t have used (l value or $~SO mUlion, which is intcmH~dlAte bCtw¢<m hlslm1cnl vnlucs and Ii tire sal~ vt11~laUon, ~nd ( Mve deducted Uds umoum from me wool ~bt

'nlet\! is n good deul ofunccrtninty about Ule '!emand and s.upplYQltlSU~iU¢s for.wool (sec AbAAB 199 i). f huv~ U$!d d supply elasticfty of .6 "0 d Ii rdOgc of demand elasticities or t85. t Md t 12. It is necessary to specify not only the slope but ~~) thQ~id{)n or the supply @ddcmandcurvesl Aft¢r talking to industry e~pens 1 have u.ssumed that Ule \Jrldedying equUlbrlum values which would b¢ observcd i r there were no imcrvenUon into me mlltket to be a quantity of 850 kt per y(~ar and a price of 650 elkg. I hnve ulso used a mON pessm1isUc price or 500 elkg. f have ussutned I.hut 010 physical stol1lge cost for Ute wool i$ ()J1 nvcrosc $8 p¢r bale per year (UliS docs not include :my fi.rumcing (tOS1S)

f haVe assumed an int~rest nne of 7% real, which is an estimnt~ Qf the nvcnlgc intl!rost fatc on A WRC borrowings in July 1992; After cClnsidcring tile prime rute tot commcootru oottowing I have used Q renl discount rote of 10% for woolgrowers4•

Vl l;']cxlbJo debt repaynll:nt

A:, n first st~p in undcrstnnding whnt Ull optimttl policy mighllook liko. con';ldQr n policy envIronment which coosttttins the industry uS UUJc n$ possible, Lcg~~.tltfon requires that the wool debt be repu.id by June 1998. Let us Impose Ule cot1strllim thnt thQ debt must 00 t~ro an~r thIs dttl~t but make no assumptions about how it is ~paid other tho.n to suy that it CMn()t grow too big (say to double U.s initlnl value),

Figure 8 shows ttm opUmal time path of stm*s nnd 4cbtf t.he opUmru t,lX mte and r~tG of selling b1()C,~~ (exprcss~d as n market sluu'Q), and tl'o time pnt.h of producer price. CQnsulb~r price and produc~r surplU$ under thiS nssumptioo, All optimi$tio wool poce ($6.Slkg) and unitnry QlnstiCity

31 would like 1.0 thMk Bob Rtchtu'dsoo, John O'Connor lUlU "he sWf of Ul~ AusttnHtU\ Wool COf)lOrUUQO nnct· th¢ AustrilUpn Wool R~lisaUQn CQillmi$sjon (or a numb¢r of uscfulcQnv~rs:.lUons ,_botH th~sc parometcn. They of course taka no rc~potlmtbnity (ar my Jud&ementsor errof$~

41 would liko lO UlMk RUb¢rt Pctulro for ¢4tc"1~Un8 these estlmntcs tor me,

11

• .. : ... ·f' .... ht ,r

Qf d¢m~ ttt"MSumed.but' Ute l1¢neml rCAtU(CS t;t the· solutloo anl not s¢Mitiv~ to thc~ t\SsumpUon$~

r:: :" ......:: .•..•....•.... :···rflserr}rt~te:8~~ut.tl~r~.·.··.··: Thg first tlUng to observe fa tllAl ~.debt ropnym~mtputh chosen by the lildusttyoom no tes¢mblnnce at aU to thntjm~$CdbylcSi~l(lijotl, the $OluUPJ1 paUlls quite ¢xtt¢m~jMd would impOSC t¢chrticaUy Ut)(l ccQnomi~auylmpo$$ibler"te~ Of"dJu$Ull¢tlton Utel iUdustry.Debt tepaytllcntis dcfe~dt and in fact fUrther debt undlncf(:ps¢u··S(ook$ ~. run Uptapidly to the inttiru ycnt$, tn the Inuw y~tut u dgOrou$ Progmtn i$lmpOncd In order to meet the debt $crvicitlg dettdUue. the tM tate ri~$ t() M impluUSible lSO%und sates from Ute s~kpUe m.~t 40% of denlund.

Clearty U1cse poliCies aN t<JQ .extreme tel betukcn ~rlQU$ty. but Ul~Y dQ mUstmte $~ver~l points. 1110 industry would Uke tu d¢fcr rel'nyttlg Ule wool debt. eVQn ~nlh~ cost of a very ~~8.tcs$iYe tilX u,nd sales polley wht~h would eventually be necessary, However it S¢crt\s likely thlsllpprouch, evert if it were moderoted torcquire more rt!tUisUc f'4tes of ndjuStnlCllt. would lead tQ poUtirally infeasible tntos of debt ~pa)1llem towar~ the end orth~ ~riod. ttqUU be Mti¢ipaf,ed that prcsStU"C$ for msphcduUng U11,l Jjcbt tcp~ymcm wQuldUlen become very stronSr eSp.;!t,.iully If Ute wool market w~!(U weak tmu the dlfficulUcs could b4 attributed to unrotc$C~abte specit*J, cu'C\,unsUUlces. Of coume if Ulcre Were any expectation that debt might be reschedUled Ulell Ute tendenoy to defet I1Zpaymetll would 00 ev\!n stronuer.

~nle oUter point of filtcrcst is the stability of the consumer price, n was shown nbove by u Ulcoret!cal nnalysis ~hut if Ule d~bt and stocl< con.~U1Ui1fS do not bind then it is optimal to keep the con.~um¢r prl~e steady nnd nsine at ~ rate which is retated to the tnte of interest and to 0', the shndow price of debt. Figure 8 shrJWS this pt)Ucy in practfc¢. Virtually aU Ute ftt.~tabllity is reflected in Ule producer prtcO:I not Ule consumer price. l1u~ reason for stnbillsil1g the price to custolUers 1s not conrtect¢d wUh rL~k av~rsion.lt is simply that a b1nble price path is beSt for extracting the maximum in monopoly roms from the wool market.

In order to nchlovo U'us result the two polley in.~trumcnt~~ 4ro used togeUlcr. no~ as sub~titUfCS. 1116 sUff tllX imposed between yenn; four Md six would be expected to cause n cptkc U1 the comrnnler plica, but it is matched with" surge in stock snles Which cancels OUt the consumer price spike,

Vll Munuglng unrler the debt constraint

Figures 9 to l6 show optimal poUe}' puths under the debt repayment cQn.~tl'Uint bnposcd by legial"t.lon~ 111000 pathS arc calculated under a t4tlge of wmumpUons ntx)ut the underlying price level (the stnte onhc mnrket) unci t.h~ demAlldelasticit)'. Othervariubles are also bnportam but thtH«l tuu the most bignUlcn.nt of the mode! pur"uncrcrs.

Consider first the time l1aths for stoc~~ and debt, Deb~ repayment is d~tenn1ned in e$s~nce entirely by tho rl:paymcnt consUulnt imposed by legislation. Only in the very last period ts them any tcndCftcy to rcptW mON quIckly th~n i$ required this behaviour is in accord With Ule tendenoy fCvealed in tUn uncon$tmJn~q mod¢l. to dc((;: d¢b~ repayment. 11n~ ~havi()ur of stocks vAries considcroble d¢p¢.ndlng on Ule demand Qln.~Ucity nod to t\ lesser degree on the level of prices. If the olu.~tlclty of~ dcrtltuld L~ 1 or mom, stoc14~ nrc liquidated in bQtween 4,10 "flO 7.S y~nrsl However if

12

U1t~ elastiCitY is QVCtl.tl tittle below 1 U,en s~ks ru'e. sold v¢ry slowly, tll thel~1pnncl of Figtlt'Q 9. only nbOuthnlf the st~kpiJflhns. been sold after ten ycoxs.

'tb~ $cttlngs of the polley inSf.t1.mlcnts vnrynl$o i\ccofiU,ogto the demaIld ~lflSticlty ~ JU$~M m the uneonsttain(!d CliSC both insltUments atcU$¢Qtog~met. but tM. balance betw~n U1¢m vn.riC$. tt~ elasticltyis 1 or gltnt¢r. thQ~ r~le tgndsto be b¢ltlW 10 pQr~nt whUcstock sales nle¢t rnQN than 1 0 pet cent of dem~q. If theelMuQityis b¢lowI th~n U» w.x rate is mQre thtm 1 () p¢r cent while stock sales nrt·lcss than 10 per~nt ThQ .. tAA rate b¢cotncs negutive (n proctUQuonsubsidy) once debt is repaid if there at'!! Stock$ stUlunsold.

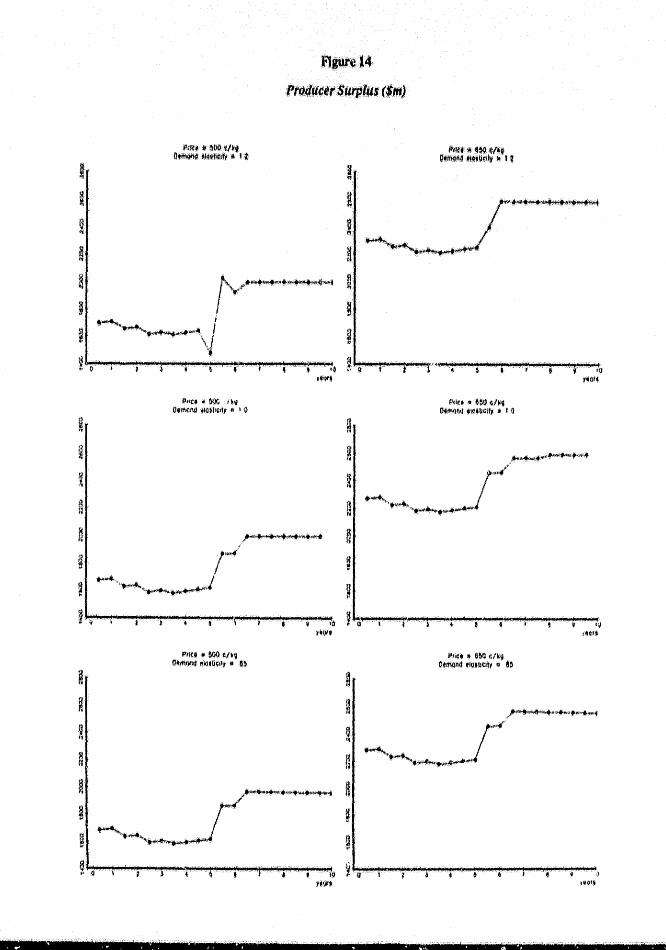

Prices (\to generally deptes~d ~tld VMi.ublc until stocks and debttlre bOUt cleuro<h 111C consumer pri~ shows leSS vntinbillty from ~tiod t~ period Ulan the produc.er prl~, but U1c~ L~tl prlC¢SICP when stocks ute exhausted'. Producer Sun,!lis is d4presSed until th~ wool debt isrepllidMu (In the cuse ofless elustiQ d~tmmd) WhUCCVM UlcstOCkpUc hangsovct tho market,. The rate of adjUSUti¢fU is much lcsscxtreme thtm in Ute uncon~tntIned case.

l1lC shndow prices y nod (1 orstocks nnd debt rut shown in rit,1Ul'eS 15 and t6i As tll!!Ory suggeSts, (j is Vllfh\ble nnd lies bctwr.cn IS and 1. while y npproaches 1.\ steady state value which depends atl the elasticity of ~mund. Even if the demtu'ld ela~ticitY is gn:aterth~1 t. tilO shttdow pttqe of stOCks is stiU negnUve until debt Is reprud. 711i8 is b¢cnu$Ctev~n though uclllng stocks produc~s nut revenue. thh revenue is nllocated to the relatively uJtnttrn,ctive goal of ~bt ~ducUon, ~nle low nnd in mnny caSeS negative shndow price of stoc~~ is $tti}dng.

VII ItnpUc.uUuns for poU~y

It is apparent Wilt the t f~tinml mllnugemem of the wool debt and the wool stockpile is u complicated mutter. 'n10 mouel which hus neon developed ttl this pilper ignores adjustment COsts, Uvcst(Xlk dynamfrs. risk and uncortainw, product heterogeneity and UlC poSSibUUy of speculaUve Iltluck ns stocks are nm downl and it is already difficult enough to solve. Bccnus¢ t)f these dlfOcultJes, n more thrm usual dogree or judgement ~md cnutlon should be excn.+ised in dmwing lessotL~ for poUcYt One mustuxpross some respect for the marulgutS wbo mIl have to form n View on aU of U1cse matters as well as to resolve Ule confUcUng pressures ot"Oovernment und the woollndustfy llnd to confront t.rn~ realities of the wool m,ltkct.

The fU'St implication which one might draw is that it is probnbly not optitnlll to repay the wool debt ahead of schedule. 111Q unconstrain~d model suggests that the industry would have n strong preference not to repay too quickly. tllld thiS also seems to be opUmul under the repayment cotlstr~nt, 'The not~ of ct\ution one might Add is Umt if the wool mArket wen:; to dctedomlc ilt some swge in Ul~ futUre thr.n U\c poUc;;y !Jottings which would be l'C<luired to mrunuun the required payments might be poUUcuUy infcnsiblc. Early repayment provides n m~tlSute ot'inSllrtU1ce to tlle OOVCmmctll that thL'J wUl not huppen. It could b¢ ru'gued, however. thut the Oovemm~mt has already t4)$CssW thls risk in setting me tepaymunt schedUle, If the industry }11\5 shown goOd flUUl by

13

malnUdning hs~paymenlSmen the risk of nt1~ major m~t downturn should "bQ shared by thQ industrY and the Q1>vemment. .

It is also w~rth h¢ting tbl\t quite high $¢ttillgs of Ute. wool tax may Utl~f some <.it¢umstMCcs be n~C¢$sary, The w('X)l ~is$et in legislation audit 1$' mucn easi~r to lowc;r i~ manto mise It, It i$ inlpm13tlt '0 maintain the option to se~~ blgh wool tax in the future even lOt i$llot required IlOW (conhider panel 1 of l1gu1'e lD,ll nhoU1cl be made pl4\in toindustr)'tbat Ulerem two ways to ndse debt serviclllS revenue. an<! these ·nrc s¢Uing wool, Iln~ tAXing .t.helndusttyl BoUl acu®s lower producer prices nnd rcduce;'producerin«>mes, n,aisin$a $iverlMlQUntofrevenuc by warton may cnuS¢ less paln to the industry than to do so by sclUngwool. becnu.~¢ some pt the tax burd¢tl is passed on t<' ~On.'iumersj In general a miXture of taxation and stock sales is best.

The eXflct mix of stock sales and t.1XIlQOn is n ueUc;\te maUet, as it dcp¢O<.t$ bl quite ~.' SQnsitive way Oft the demand cittSticitY i To add to the. dUl1culty t llnc wOPls MdcQlmiet wQOls a~ in many ways <tuite diffet,¢ot commodities with diffe~nt demand elasticitic5f from It thCQ~~tical perspective. th¢ ~imptest APP(,()~lCb might be ~o form a view. bllSCd on cc~idcrntion of elustiCid,cs. of th~ opUml1l time fmm~ ()I ¢t which to seU down various ~alcgQrles of wool (see Figttte 9). Stock.1:; would be f\!duced in n steady and predictable way. nnd ale tAXtnte would ~ adju$teQ rrom titne to time us clrcurnstanc~.s changed to mf!e~ the debt SCrviC',llg ~ds, Figu~s 11 and 12 seem gener11l.ly con~istem With sllch tUl Ilpproach. untortUnnt~ly. tax rates nrc much harder to adjust. than is th¢ rote of sales. so the oppoSite approach rnay be wllUt we Will $CC in PruCti~1

In conclusion. Ule most striking fcn,uro of these results ls the very low and SOlJletimc$ negative tnarginal value of stock'), 111C v~"ue of stoc'-.s is lowoocnuse sal~~ from the s«xkpUc dcpn:lsS lh(! world price. reducing the ~uphal vt\luc of the stOCk. nod lowering producer incomes. If stock.~ tU"C WOM very little at the margin then it is profitable to scllinto se,condt\ry mllltc1S even at vct)' low prtces. It may be difficult to find such opportunities. tiS it is neCessary to be su~ that the wool docs not tlnd its way baCk into the world market etlhet~ directly or in lightly processed form. However large potential pront-iS tlN at stnk.e. It would seem to tx! sensible for lhe Rcali.~t\lion CommisSion to devote higniflcant resources to seeking out nnu evaluating joint ventures. conccsSiont\l credit nmmgements. commodity swaps, nnd other innovative marketing appronche.~.

14

OlbUugraphy

AQARE, Submission to theWoQl rUv/~v Carnmtttc~, AU$trnUanbu.~au Qf Agrl¢ulhl~ fUld ResOUrc4ecOnQmiCSt 1m. AIlAnE,MaraaRtng the Dtsp()saJ qf AUJtralla~ lVool Stockpile. AUSU"AUanau~au of AgriculwfC and R¢sou~ Ucom>mics. Cartbe~1 1991.

A Wet Annual report. Austr~Unn Wool COflXlrnUoo.MelbOumc. 1900.

nardsf~Yt P., U Woot on the brink. U~Q publiccO$t of underwrltin, the w~t mlltketu.~(1pt!r presemed at IheAustralll:Ut A/JJ/mlltural Economics Society ibmw.# C(Jltf~rehCet 1991.

nnrd~ley. P., H'nu~ CoUapso of the AI,lStrnl1an Wool f(e.selVa Price Schemuu• La Trobs UniVersity

Eca1tf)tnlcs /)t/>flrttnem DhrcilJs/on Paper. 1992t 17/92,

n~trd$ley, P. and R. P~reirut "OpUmat MM:~gemem.()rAlU!'ttaUn's Wool $tQCkpUe ·ProviSioruU Results" t Paper prest'tnteJ at the Conference 01 the. Au..tttalian ErX)ftOmics SOcielY. 1992,

Chiang. A.C •• e/~ments oIDynamt'~ Opt/milatlon, Mcamw~HU1. Singapore. 199Z.

Suhmt. S.W~. Hthe vulncrnbiUty of price sutblUsalim sch¢mes to bwoulaUve ntt"ckt'. Journal of

Polittcal EcotWmy. 1983.91(1)1 1 f3S.

Smeck~l, A~~ notr~lt Of and Quirke. 1,)., Woo/lmo the 2/st' century: fmplic:ntitJns/or markcttng <Md profitability, Centro far ImeMuHiotla! EcononHcs. CanOOrrJ. 1900.

\Vatsem, A.S,t UntavelJihg tntervenrttm in the w{)ollndWlry, Cenfre fot Uldcpendem Studies. Sydney. 1990.

15

I ~ t

'$.0;[, -u .. ,

.~O

II

• ;;!!!:3.0 <)

lI1 oc2S o

E;I,C ~

l~

~.(\'

o,,~.

figure1: '\'{cotStocks

f

I o

~~ fJ-

1 .. \.

u Xa~nDa~.Q~_a_O_U_fln

l"ce:

Fi9ure 3:: nebt

-tlSc'

,t;,.", ____ ... ~ . ___ , ______ - _' _

r.;

:C &1-, .9 g~ "0 2~ a 'O;JO; ~

~2G o ~ t,,~ -

,-,

figure 2.:. Market Support BufferStockAcqws,;tio~s

2 o· ~ \' ,. I ~ ~ l' ~,. 1 ' , ,F~ • i - t t

~ ~ 2$ .. ::J:t. Ji" _~ta:: alMal A~"M~ ~' attl:

?-Ul ~"~f

_Jnl

lHmf .•. tCOOf 900

Year ¥

Fig~e 4~ WOOt Prices rhef~t' Priee:and'theMo.rket indiOlmf' Price:

':*'-, "

? Buu II

# ~ j f : I ~ .. o

o 2 700

• r : :.tii} j' . ~~~. -~~- I : I~;

5! ..;;: 606

"'" Q

C <IU ~),

400. , .•. '. ."" .""..,-.~~ .. ,'".',.,.,. ~. ' , .. ,. _,1 ' ;utu .,.~-' •.• sf 2W·'-".....t

l:,t Ii 1"1 18 19 au 81 al a.' l 84,85 8b ~1 tia8~ 9'0 91 9.~2 I .. · .• y~ ~

j

I P*+" • ..J

/

"gqi~.8

Fk;ilbllDebtll,paymtht

~

~

R

(I '. ( e r III

~ / ~

1 ~ '. '(I

lil~\lttt $lItjlIl.!l

'ril

1.0 It '.

/lIfI(, :III &:oQ~,~~ l),~ .~'I;(j.11 " I t'I

PriG' .\Ii! to 501l1~9 \)'IMM .Ic)JlI<II';" ~$

n • •

FtgtU1'

If''i:!j$wc~l(kJ)

• a

¥

a

~

!

I WI)" ... "'rl,,, ~ . ~, 'II l~l!!_

/,!11U .. 6~lI;/1\9 o.ttl\\l;w.!!t.~pIY .. i fJ

Ptlt, .~ ~lW ;;j"1J (l'/fu'IM iIll),II(:lll ". U

•. ! .. ~ ... ,

~d!"" ~ ·~·ifl~(I t':lf~ ,lqUlttl, .~ t:

\.

Pt\f., iii ~M~~ {l.iNm~ .lI1f\!.r;tt .. ~ i'.l

11."

Flgurel.,

tNt Wqt)IJ)~fit.($m)

l e !Or

a I § ."'.

U , 1:1

tl,) !f

'lilli' f!f~jI ~ .~ l/liq

Ctlm.\lI4tl<).~';ilY II t ~

Q~~~~~~~--~--~~\~.~-~~~~~~~~~~~ ~$} ~-~Tf.t .F. I.U : '~, -\: t.;tijj~ d ".I.~,: .t':·r~ 6 ~ ~~~. ~i~~.~J~~"~'~'P~.~~i--~'-.·~'~'7~~~I~~~~~.~~

IIllet it ~ t"~ Qt/M1'!4 .li.\'lj'II'(" A~

"

,,!1', Pt!(t III i$ao: ¢'J~¢

O'/!I4h1,f ~,I,!:~i\y " n

I'JOU

iltllft if, ~() 1iI.1 n.i'V~ ilfllU(ifl" • 0

Ftguretl

»fhtWtwl t"{-x,)

It

I I 10

U;;ji'J III

, q

Pf~." iS~O c/~~ 0,11\41\4 tllll\,id!Y i! I C

Plin .. t$~ I'!l~9 O.fMM '1Ii.\I~111 • ""

I'IiUr , ~.IJ!l i;lV,

v.It\(III4.tllt!:(;~ .. '\ 0

,~~'t"'~".", • ....., ,11->4<'«'

Pit!';. '!! MlU <;1.1; VtM411!1 .1li.11\ti!yit ~

f1gijt~12'

Sal¢t UtlNt fit' $tq¢tpllf

(tr~tklt$h4t'~)

Ptlt, ;jI' ~riO t/~ O.!lWII\I JkI,Uf.lty lit l!)

PII(,. 'feO !l/t~ 010'1\1)1\1.1 ~14.\il!lty , 11.5

§ ¢

I 9 ..

~

I

~ , i

~ I . ~

pnu \It $\)~ '/~. l.l.'MM ;i!I'~r.,~" \#

""'1:." tJl)/.) ~H9 Q,lI'lI)!l4 '1!l$lJt!1y f1 I {}

.1(1UR13

WO(J1 Pritf$ (c/~r)

(ptoil,",,. prk:fl tW/kI"tllJ

!

:~~ .~

~

9

t

f)rl(~ '" o~n ¢i~~ OMWil4, Ikl.fVllltj lOt \ i)

.~r· i~ ~ !l t· ·1I'QIt

PtlfJ

a,/rIOIlQ 0'1.'

r . ~ . • ~. ,Ii t4 t.gtt

f

%

• I

~ , i' t

i

(lilt, !It ~!,\o cl ~~ (l,i\\ul'll1 .i~.~~\I,.. jU

""""~"""'~,"""""~""""",,,,,,,,",,~~"".!-l '""""""!""" ....... !"""""~ • .,.i .... ' ~,tff4.

IttJ"

P(~f 1# ~Oj) '/.9 n,~ ,,14'!jCil'r~ l ~

Ji1a~"14

Pm(/:(lcCftSurplU$ ($",j

I

:~--

§ !"',>"."'>tlil'....,..~,~~~.

I .~

D , f~ i

i ................. - ... \~ ~~()!"'-..,..,.,....~""""" ....... ~~~~~..", ....... ~~~It

P"(.f ~ fiOIi il~q C'fI\(f'.\I "l(Itl!~111 II I Q

~ /w-4' ~ "4"..,..,..,'r0~"" .• "",~

•• 1)1* ~~I1 ..... ~l"'!"""""""~........,.l·''''I'\''..,.I·i ........ ~ ...... ~~··~~ ...... """""" ...... ~ .. ·~4

'~I)"

Plitt ·11 no I;/~i O'!TIIl1I\! +1C_1Ii;!\'1 II I I)

f~y·,~~~--~--~~~~'~~~~I.~~~~ !~Q~·~~ •• ~r •. ~~~lf~:"~;~·.~I,_t~.~~_j'~' __ ~~I~

'.

PfIU .. me/.lj Oilit1(liW "l4n'~II, ill f~

1 I ~

t

I.

J.W' '~~I.

,i!)

"91"'

V ,-\I

¥flill. If IS~ Il!li9 O,Ii\\)/Iit fIO.II¢11y • ~~

,

J)tI~j\ ill eO~Ii/)~ O.!Il4M jI'gUiCI!y ~ ,,~

finn f;j \Y.\!)I!n~ /l!1lfiQM .11,.\1(111 " , 0

I. T ~, ~."

•. , ...... ~ •. "'+j

Ilfe ... ~ !l/~1 a.ff1ll-14 .lilfll!llly II 6$

l'1WrfJ 1$

The Sh«dqwfrlc, ql.~/i)c~ y(clkg)

~

~~qr.·~~:'-r,:,~::~~::;:;:f-~~"~--1r:Y.~4t~ ?

; .-', 1-.. .. ;7······ , ~......," ..••. '1>~~~, ..

~ g ,

Pfll't '" MO l!t/~~ O.m/l1111 .'olllltl!y It 11$

.................. ~1''''.''''''~...,~.~...,..,.,~ ,

9 , g I

H. I

'±ri

Ft~~16

thlf SlmdQw Pritt IJ/ $tQck$ <1

fll'1U .i't M~ ¢/~~ O.i1'Ii\l'\it .lcWi~ltt " t ~

r ........... ""., .. , '0 i" • . ,~~j,~.'

~~~~"~~ __ ~ ____ ~~~~~~"~i~i'_~~~ __ ~!l ~~~~~~~ __ ~~~.~"~~~ __ I!W~ ____ ~··~!~~ __ ~I f) (J 'I~ ft I I,)

,tQtJ U~I.

~tll:. jI ~ ~,H~ ().~ .'",.Iltlly '" ! 0

....... ' ........................ ~. I ""' .......

, ......... ~.,.,.~ I

I'tlu .. ~il/~9 Otrl'lllM .W'"tll~. I))

~~~~~~~~~~~~~~~----~~~~~~~.~~~. ,.i)tJ

1'111(:' • t'SQ 0/)9 \It!l\tll'l~ .'i,j$U'lty .. I Q

'U "" ............ . ~ !

., ... +"" ........................ -~.. . l ~ ",... ............ .".",....,~ tI . . ' Il

Pllet .. lSilO ~/~Q O«lnqnq .h1l!i¢I!r 'II as