Opportunities in the food & drinks sector in Spain for Irish companies

38

OPPORTUNITIES FOR NORTHERN IRISH FOOD & DRINKS COMPANIES IN SPAIN. 1 Your Global Partner

-

Upload

lewis-mcneice -

Category

Business

-

view

530 -

download

3

description

T

Transcript of Opportunities in the food & drinks sector in Spain for Irish companies

1

OPPORTUNITIES FOR NORTHERN IRISH FOOD & DRINKS COMPANIES IN SPAIN.

Your Global Partner

2www.mcneice-export.com

PRESENTATION OVERVIEW

This presentation has two objectives:

A. Highlight the opportunities that the Spanish market offers to the Northern Irish Food and Drink industry.

B. Provide a strategic and operational framework for the penetration of these sectors.

Presentation Structure

Defining the opportunity – Overview of the Spanish food and drinks industry.

Sales channels – Analysis of the principal channels to market in Spain.

Logistics – Cost comparison – UK versus Spain.

Export Strategy – How to penetrate the Spanish market.

Overview of McNeice Exports Service in Spain.

3

THE OPPORTUNITY

4www.mcneice-export.com

OVERVIEW OF THE SPANISH ECONOMY

State Structure: Constitutional Monarchy divided into 17 autonomous regions

Population: 46 Million

GDP 2009: 1.2 Trillion Euros

Exports 2009: 158B Euros

Imports 2009: 208B Euros

Principal Imports: Machinery & Equipment Energy Chemicals Semi finished goods Food Consumer goods Measuring & control instruments

Source: www.spainbusiness.com

THE FACTS THE OPPORTUNITY

9th Largest economy in the world

12th Largest importer in the world

5th largest supplier to the UK.

Gateway to North Africa & Latin.

16.5M British & Irish tourist visit Spain each year.

Excellent road, rail , air and maritime connections

Second most favorable fiscal system for SME’s en Europe

www.mcneice-export.com

SPAIN – BASIC OVERVIEW

BASIC FACTS

Spain is comprised of:

15 regions 2 island regions 2 African protectorates

Each region has a devolved government with varying degrees of independence from the central government in Madrid.

6www.mcneice-export.com

TOTAL FOOD & DRINK CONSUMPTION

Source: Spanish Ministry of Agriculture, Fishing and Rural Affairs.

Expenditure is expected to remain stable in 2010 Expenditure is expected to fall by 5% in 2010

7www.mcneice-export.com

SPAIN – THE OPPORTUNITY

Source: www.spainbusiness.com

8www.mcneice-export.com

PERSONAL HOUSEHOLD SPEND: FOOD & DRINK

An average Spanish family spends 4400 Euros per year on food and drink consumed at home.

UK average yearly food and drink spend is: 3195 Euros

(Source: http://www.statistics.gov.uk/downloads/theme_social/Family-Spending-2008/FamilySpending2009.pdf

9www.mcneice-export.com

CHANGING CONSUMER PATTERNS

Source: Spanish Ministry of Agriculture, Fishing and Rural Affairs.

Couples Without Children(Annual change 2008-09, + 10.8%)

• 7.3% of the population.• High level of discretionary spending.• Diet includes a high proportion of

precooked foods.• Eat out regularly.• Worried about their health.

Young & Single(Annual change 2008-09, + 10%)

• 4.9% of the population.• Innovate & impulsive.• Hedonistic, prices are not important.• Willing to pay for time saving

solutions.

Single Parent Families(Annual change 2008-09, + 3.6%)

• 5.3% of the population.• Value precooked products.• Little free time.

Emerging households

Pensioners(Annual change 2008-09, + 2.4%)

• 21.9% of the population.• Price sensitive.• Health conscious.• Traditional tastes.

Couples With Older Children Living At Home

(Annual change 2008-09, - 6.1%)

• 18.3% of the population.• Children’s advice influences weekly

shop.• Tight budgetary control.

Couples With Young Children(Annual change 2008-09, + 0.0%)

• 16.9% of the population.• Spend more on food than any other

group.• High levels of spending on time

saving solutions.

Established households

10www.mcneice-export.com

FOOD & DRINK CONSUMPTION BY PRODUCT

Source: Spanish Ministry of Agriculture, Fishing and Rural Affairs.

Page1 / 2

11www.mcneice-export.com

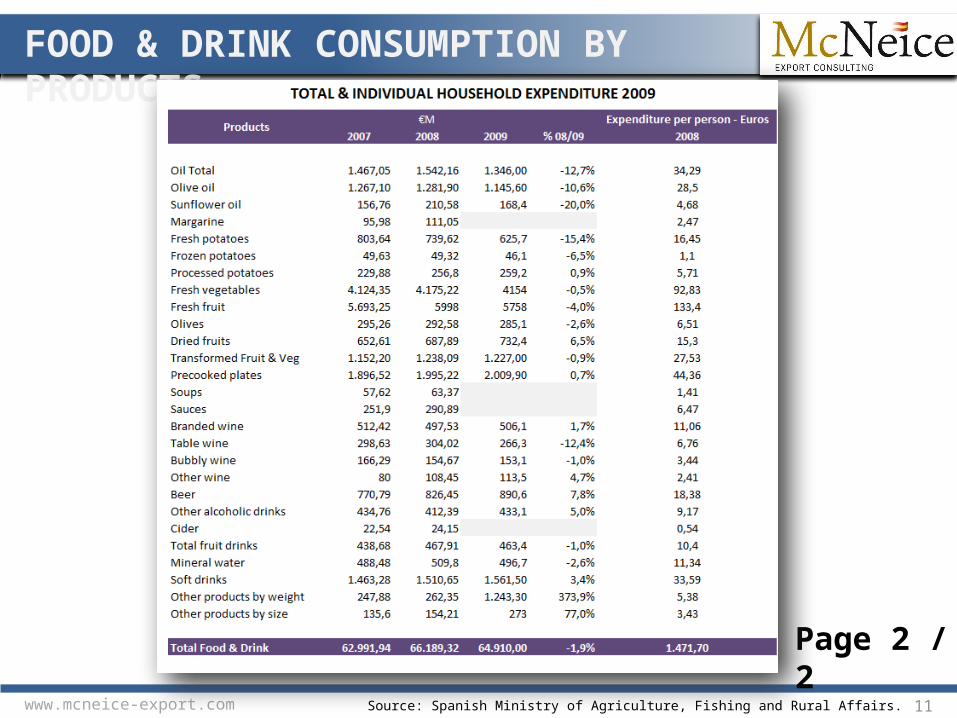

FOOD & DRINK CONSUMPTION BY PRODUCTS

Source: Spanish Ministry of Agriculture, Fishing and Rural Affairs.

Page 2 / 2

12www.mcneice-export.com

VARIATIONS IN FOOD & DRINK CONSUMPTION

Source: Spanish Ministry of Agriculture, Fishing and Rural Affairs.

*2007 – 2008 Growth rates – 2009 data not available.

13

SALES CHANNELS

14www.mcneice-export.com

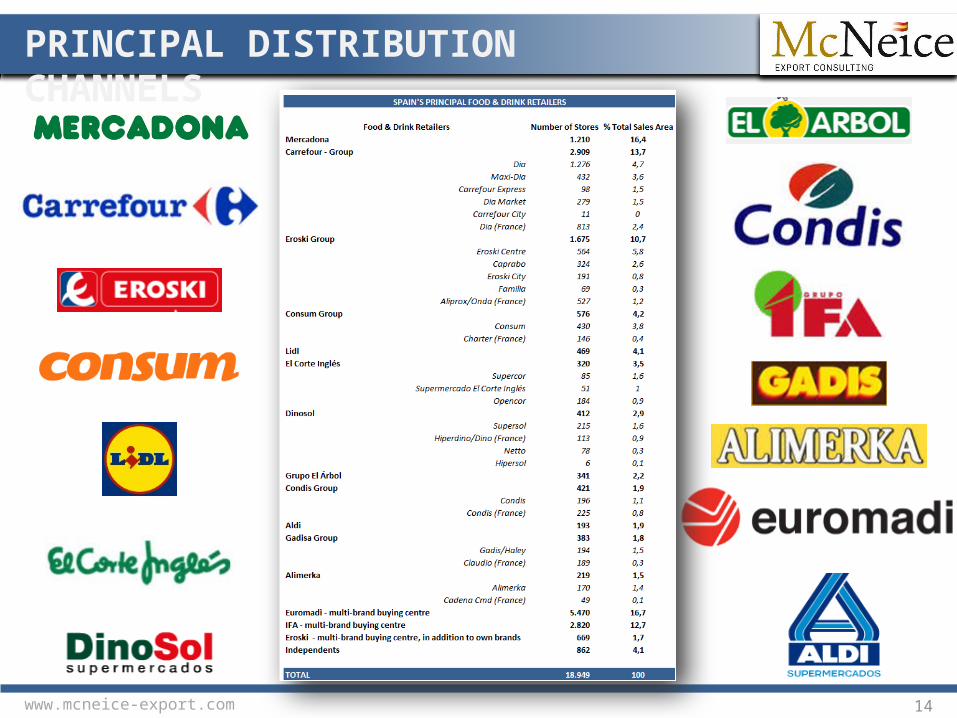

PRINCIPAL DISTRIBUTION CHANNELS

15www.mcneice-export.com

POINTS OF SALE BY SUPERMARKET

16www.mcneice-export.com

SALES GROWTH 2006 - 2008

Source: http://www.fomenweb.com/ - Note: The results of Carrefour, Euromadi El Corte Inglés are estimations.

Only 6 groups have consistently grown sales since 2006:

Mercadona IFA El Corte Inglés

Euromadi Lidle Consum

17www.mcneice-export.com

KEY REGIONAL SUPERMARKET PLAYERS

Source: Alimarket

18www.mcneice-export.com

74% OF ALL FOOD & DRINK SALES ARE CONTROLLED BY 10% OF SPAIN’S RETAILERS!

SALES CONCENTRATION

19www.mcneice-export.com

MARKET SHARE BY CHANNEL

20www.mcneice-export.com

OWN BRAND GROWTH

21

DISTRIBUTION CHANNELS

22www.mcneice-export.com

FOOD & DRINK DISTRIBUTION IN SPAIN

Abattoir

Wholesales

Co-ops

Middlemen

Transformation

Purchasing Centers

Co-ops** – Level 2

MERCAS* Networks

Distributors &

Wholesalers

Wholesalers

Traditional retailers

Superstores

Household & Trade

Consumption

Exports

PROD

UCERS

Trade only

Close To Customers

BulkClose To Producers

Packaging & some transformation. *MERCAS: Centers that group together wholesalers in the following

sectors: fresh fruit & vegetables (50%) , meat (25%) and fish (41%) sectors.

**Co-ops level 2: Distribute the products produced by their members, in addition to purchasing products from 3rd parties.

***Note: This model does not cover the distribution model of Fresh & Frozen fish.

23www.mcneice-export.com

FOOD & DRINK DISTRIBUTION IN SPAIN

Carrefour

END CONSUMER: HOUSEHOLD & TRADE

PRODUCERS

Auchan Eroski

El Corte Inglés Euromadi

Mercadona IFA

Lidl ConsumMakro

CONVINCE THEM TO BUY

POS MARKETING

PRINCIPAL PLAYERS IN THE SPANISH MARKET

24www.mcneice-export.com

LOGISTICS IN SPAIN

Most Spanish supermarket chains do not use centralized distribution. Preferring instead to use a regional structure, as can be seen in this map of Carrefour’s

logistic centers.

25

HOW TO SELL NORTHERN IRISH FOOD & DRINK IN SPAIN

26www.mcneice-export.com

NORTHERN IRELAND AS A BRAND

The experiences of the hundreds of thousands of Spanish children, students and adults who came to Ireland on holiday or to learn English.

St. Patrick Day celebrations in Spain’s numerous Irish pubs.

TV programs and Irish tourism campaigns on TV and in magazines.

In summary, Ireland and by default Northern Ireland are both highly regarded by the Spanish, especially for the warmth of it’s people and its natural beauty. Creating an enormous amount of brand equity for our

products and services.

Northern Ireland is not a well know brand in Spain, but the island of Ireland has a great deal of brand equity, stemming principally from:

27www.mcneice-export.com

N. IRELAND BRAND POSITIONING

We believe that food & drink from Northern Ireland should have a positioning strategy based on the following factors:

1) Taste & Quality - Our lush pastures produce food and drink of the highest quality.

2) Product Range / Innovation – Northern Ireland produces a huge range of quick and easy foods that complement a busy lifestyle. Spanish producers have been slow to adapt to this market.

3) Reputation – The Spanish have a high regard for the quality of Irish and British produce.

4) Novelty quality – Spanish consumers like to try new products.

THEREFORE THE OPPORTUNITY EXISTS, BUT HOW CAN IT BE CONVERTED INTO SALES?

28www.mcneice-export.com

Key Considerations

Is there a market for my products?

Is it logistically possible to sell in Spain?

Is it economically viable to sell in Spain?

Margin Payment terms

Who will distribute and resell my products?

How do I convince them to buy?

How do I keep them buying?

EXPORTING TO SPAIN – PRIOR CONSIDERATIONSEven though we believe that a clear opportunity exists for Northern Ireland’s products in Spain it is important to take into consideration the following:

29www.mcneice-export.com

DISTRIBUTING TO SPAIN

EXPORTS FROM BELFAST TO THE PORT OF BILBAO IN NORTHERN SPAIN TAKES 5 – 7 DAYS.

Bilbao is a key distribution hub for 2 key reasons:

1) 4 M people live within 200 KM

2) 16M people within 400KM.

16M Consumers @ 400KM

4M Consumers @ 200KM

30www.mcneice-export.com

KEY DISTRIBUTION FACTORSSHELF LIFE

If we consider that a minimal acceptable shelf life is 7 to 10 days and that transportation from Belfast to the shelves of Spanish supermarkets can take up to 10 days, then only products that have a minimum 17 - 20 day shelf life can be exported to Spain.

TRANSPORT COSTS

Costs can vary, but at the time of writing it costs £ 635 to ship a 20 FT container and £ 885 to ship a 40 FT container to Bilbao. However it is preferable to use 20 FT containers in order to reduce port costs. As 40 FT containers require repackaging for road transport.

REFRIGERATED FOODSTUFFS

The Port of Bilbao has over 23 000M2 of refrigerated storage in addition to ample dry goods storage.

31

HOW TO GET ON THE SHELVES OF A SPANISH SUPERMARKET

32www.mcneice-export.com

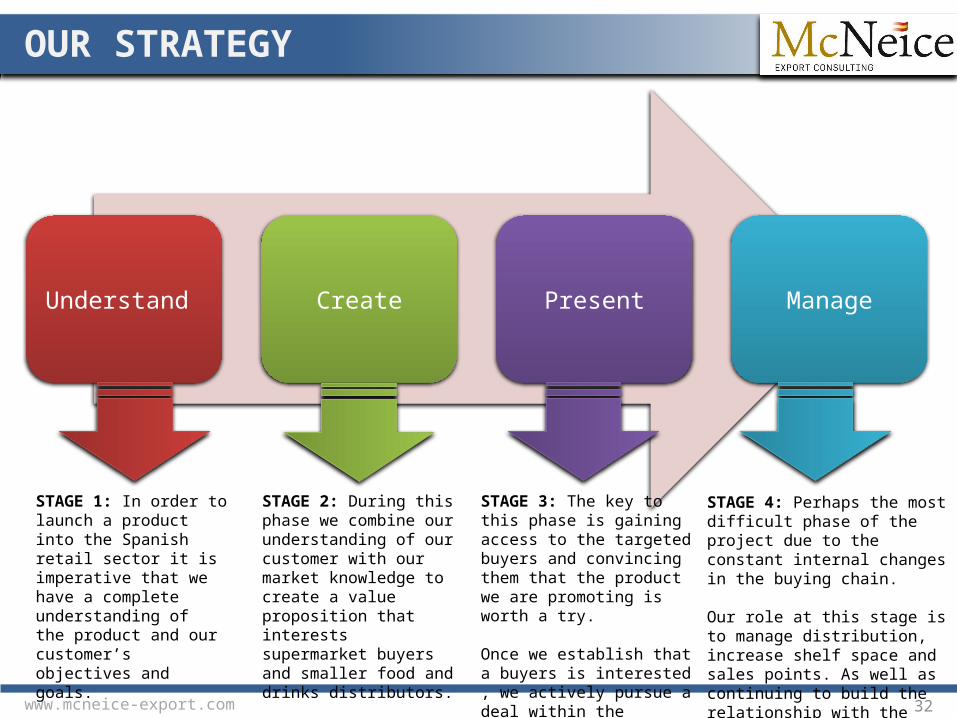

OUR STRATEGY

Understand Create Present Manage

STAGE 1: In order to launch a product into the Spanish retail sector it is imperative that we have a complete understanding of the product and our customer’s objectives and goals.

STAGE 2: During this phase we combine our understanding of our customer with our market knowledge to create a value proposition that interests supermarket buyers and smaller food and drinks distributors.

STAGE 3: The key to this phase is gaining access to the targeted buyers and convincing them that the product we are promoting is worth a try.

Once we establish that a buyers is interested , we actively pursue a deal within the framework defined by our customer.

STAGE 4: Perhaps the most difficult phase of the project due to the constant internal changes in the buying chain.

Our role at this stage is to manage distribution, increase shelf space and sales points. As well as continuing to build the relationship with the supermarket.

33www.mcneice-export.com

UNDERSTAND THE MARKETWe believe that the only way to gain access to grocery retailers is by:

Understanding the retail market in Spain i.e. the threat posed to traditional retailers by discounters, the growth of private labeling and the need to generate brand loyalty by improving the customer experience etc.

Understanding the pressures that buyers are under i.e. reduce prices, increase margins, reduce product lines, increase the range of own label products etc.

Understanding the economic , cultural and regional factors behind consumer behavior for example, the impact that more women in the workplace is having on the increasing demand for ready made foods.

Understanding the goals and objectives of our customers and assessing whether an opportunity exists or not.

Once these factors are understood we can then begin to create market entry strategy that will appeal to buyers and distributors on both a logical and emotional

level.

34www.mcneice-export.com

UNDERSTANDING THE BUYER

No matter what their Managing Director’s say, the principal objective of 99% of buyers is to reduce prices and increasing margins. Demoting all but the strongest of brands to the status of commodities.

However, the common strategy of Every Day Low Prices is not working the way it used to, and supermarket retailers are looking for new ways to engage and delight their customers which is forcing buyers to change their buying criteria.

Today Spanish buyers are looking for products that will not only help them to stay competitive and profitable but will also help them to recapture the customers they have lost to hard discounters and to grow their brand loyalty.

ANY SUPPLIER WHO HAS A PRODUCT THAT CREATES BRAND LOYALTY

WILL ALWAYS BE STOCKED.

35www.mcneice-export.com

BUILDING A VALUE PROPOSITION

During the value creation phase, we focus our efforts on putting together a presentation that will:

A. Grab the buyers attention by making the pitch experience different.

B. Help resolves their fears.

C. Offer something different that they have not previously been offered.

By carefully combining these ingredients, we create presentations that get noticed and which helps to get our customers products selected and

stocked.

Data Insights Customer Experience Brand Value Customer

Engagement

36www.mcneice-export.com

MANAGING THE RELATIONSHIP

The most important service that we can provide, is to help your company build a strong relationship with the distributor.

We achieve this by:

Organizing regular meetings with the distributor.

Conducting independent market research.

Visiting stores.

Offering ideas on how to improve sales.

We aim to add as much value as possible, as quickly as possible, in order to position the brands that we represent as INDISPENSABLE.

Good news or bad: Buyers change department every 9 – 12 months in Spain.

37www.mcneice-export.com

MCNEICE EXPORT SERVICE OVERVIEW

38www.mcneice-export.com

THANK YOU!

For more information on how we can help your company grow in Spain please contact:

www.mcneice-export.com

www.miagentecomercial.es/eng

Or give us a call: 00 34 942 04 95 75