Community Club Partnerships: Increasing student opportunities through local partnerships

Upload

lizbeth-prestonCategory

view

214download

0

Opportunities forPublic-Private Partnerships in Railways

20th May 2006

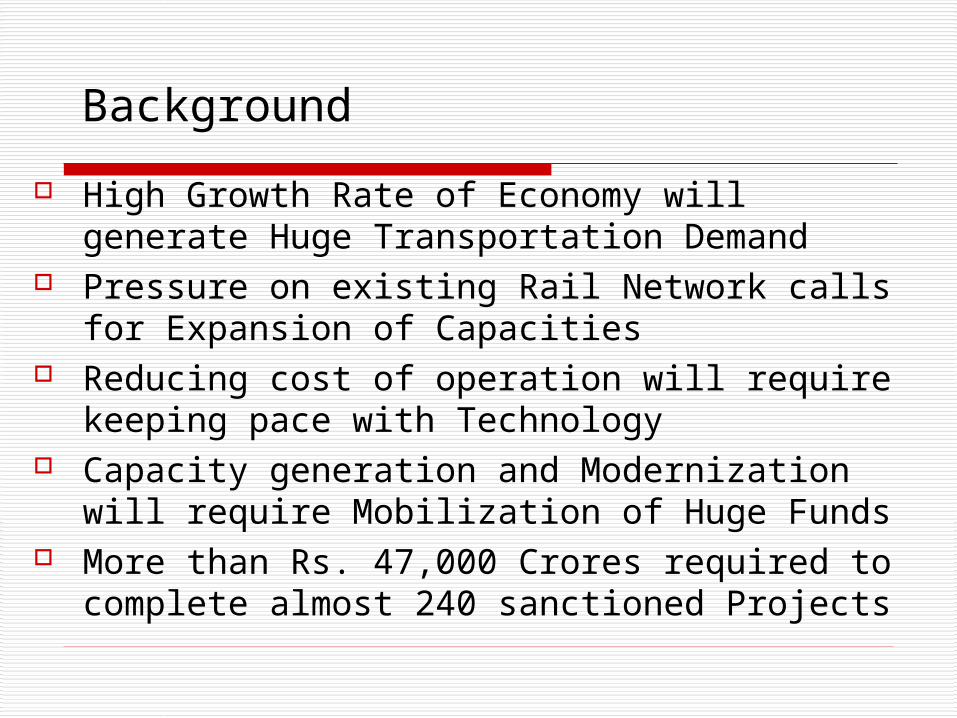

Background

High Growth Rate of Economy will generate Huge Transportation Demand

Pressure on existing Rail Network calls for Expansion of Capacities

Reducing cost of operation will require keeping pace with Technology

Capacity generation and Modernization will require Mobilization of Huge Funds

More than Rs. 47,000 Crores required to complete almost 240 sanctioned Projects

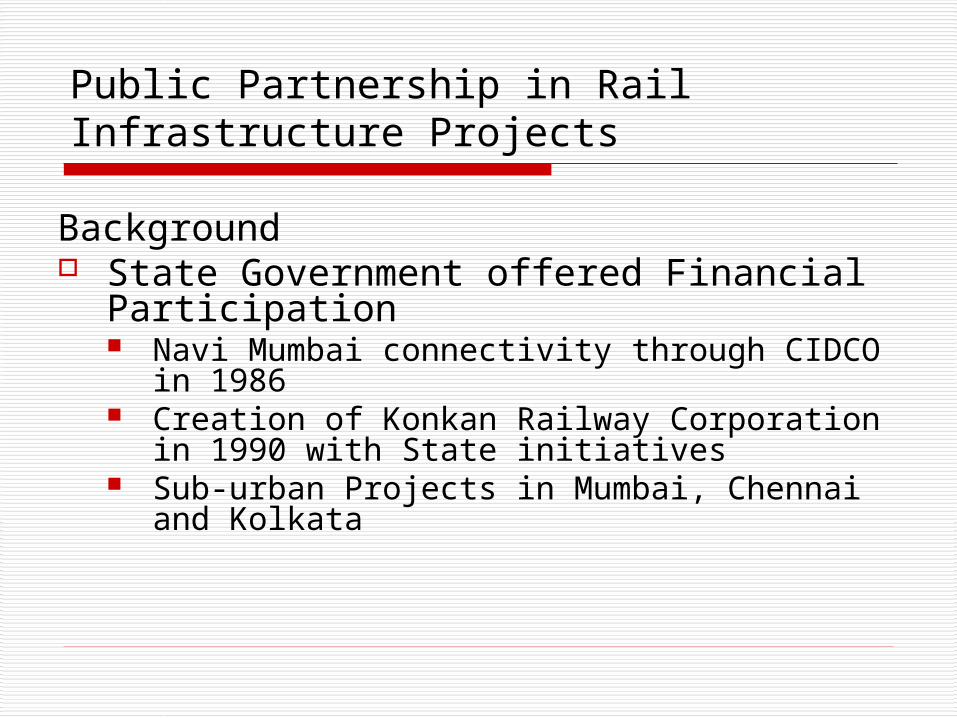

Public Partnership in Rail Infrastructure Projects

Background State Government offered Financial

Participation Navi Mumbai connectivity through CIDCO in

1986 Creation of Konkan Railway Corporation in

1990 with State initiatives Sub-urban Projects in Mumbai, Chennai and

Kolkata

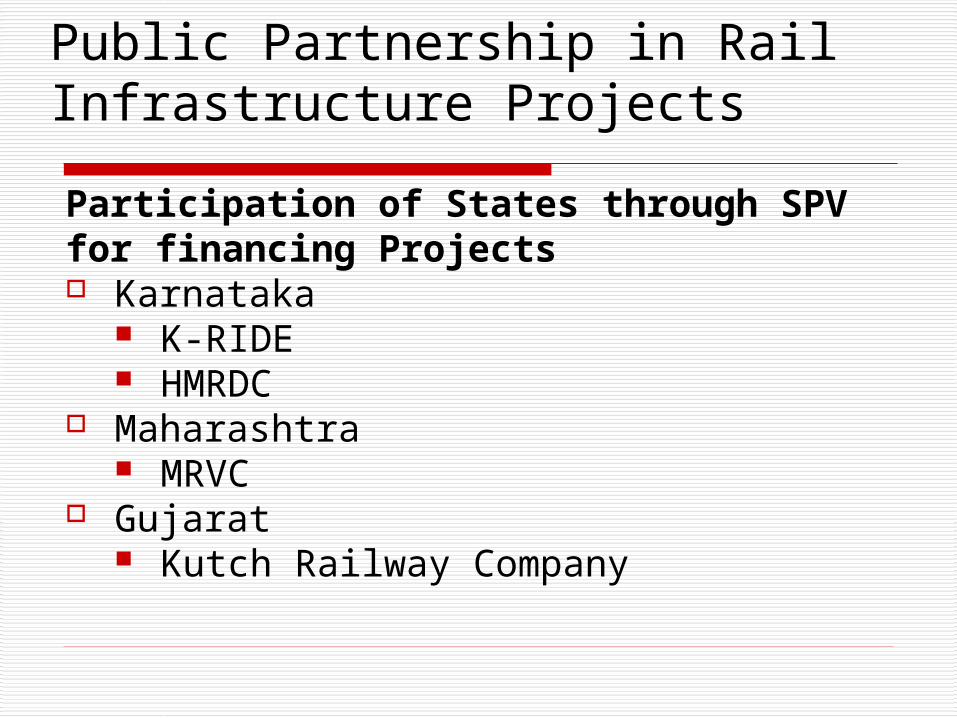

Participation of States through SPVfor financing Projects Karnataka

K-RIDE HMRDC

Maharashtra MRVC

Gujarat Kutch Railway Company

Public Partnership in Rail Infrastructure Projects

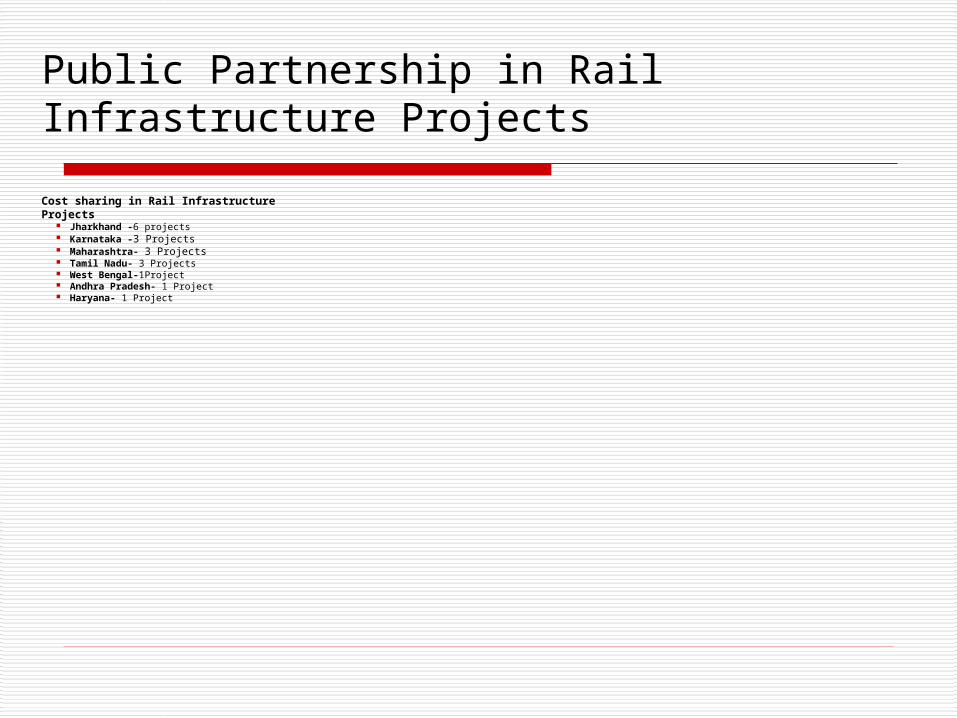

Cost sharing in Rail Infrastructure Projects

Jharkhand -6 projects Karnataka -3 Projects Maharashtra- 3 Projects Tamil Nadu- 3 Projects West Bengal-1Project Andhra Pradesh- 1 Project Haryana- 1 Project

Public Partnership in Rail Infrastructure Projects

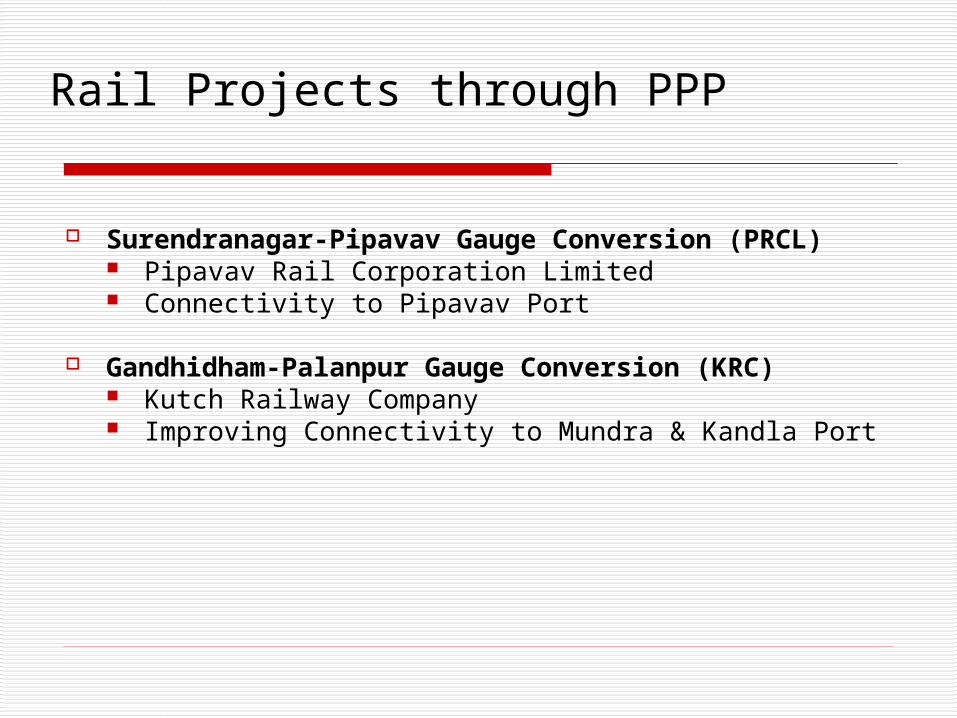

Rail Projects through PPP

Surendranagar-Pipavav Gauge Conversion (PRCL) Pipavav Rail Corporation Limited Connectivity to Pipavav Port

Gandhidham-Palanpur Gauge Conversion (KRC) Kutch Railway Company Improving Connectivity to Mundra & Kandla Port

Recent Initiatives

Private parties to run container trains Wagon Investment Scheme Development of Rail-side Warehouses &

Logistic Parks Strengthening Rail –Port Connectivities Development of Dedicated Freight

Corridors

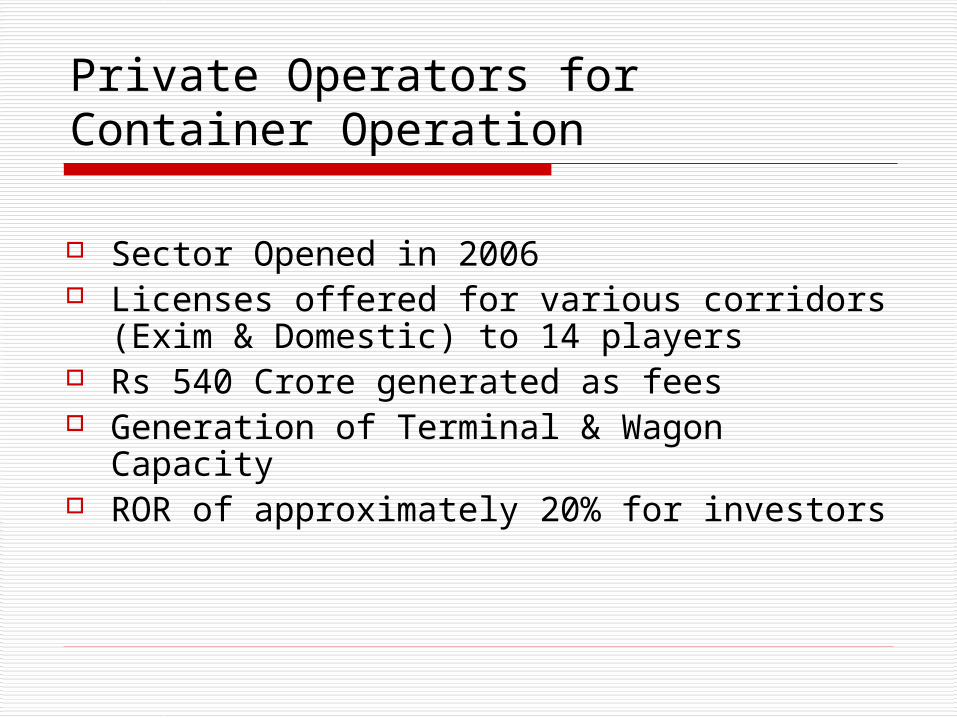

Private Operators for Container Operation

Sector Opened in 2006 Licenses offered for various corridors

(Exim & Domestic) to 14 players Rs 540 Crore generated as fees Generation of Terminal & Wagon

Capacity ROR of approximately 20% for investors

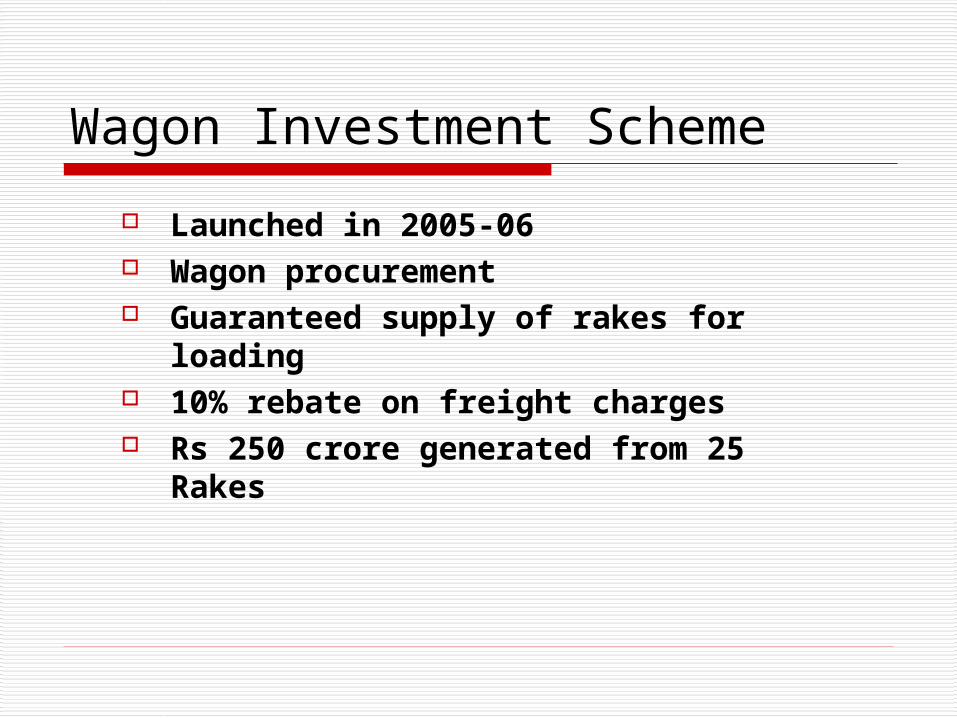

Wagon Investment Scheme

Launched in 2005-06 Wagon procurement Guaranteed supply of rakes for

loading 10% rebate on freight charges Rs 250 crore generated from 25

Rakes

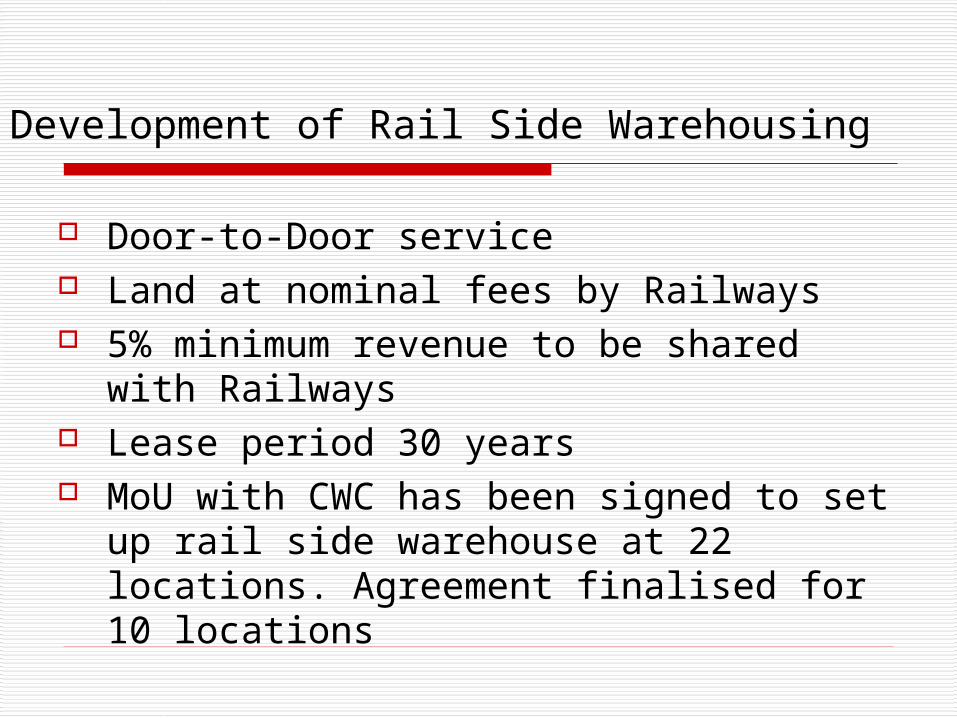

Development of Rail Side Warehousing

Door-to-Door service Land at nominal fees by Railways 5% minimum revenue to be shared with

Railways Lease period 30 years MoU with CWC has been signed to set up

rail side warehouse at 22 locations. Agreement finalised for 10 locations

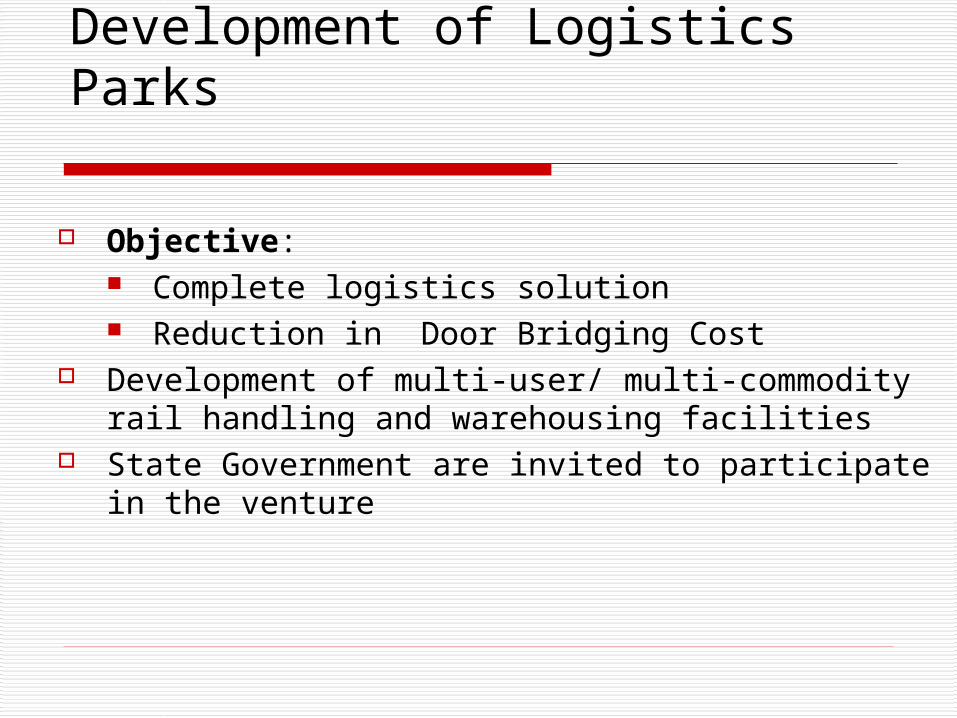

Development of Logistics Parks

Objective: Complete logistics solution Reduction in Door Bridging Cost

Development of multi-user/ multi-commodity rail handling and warehousing facilities

State Government are invited to participate in the venture

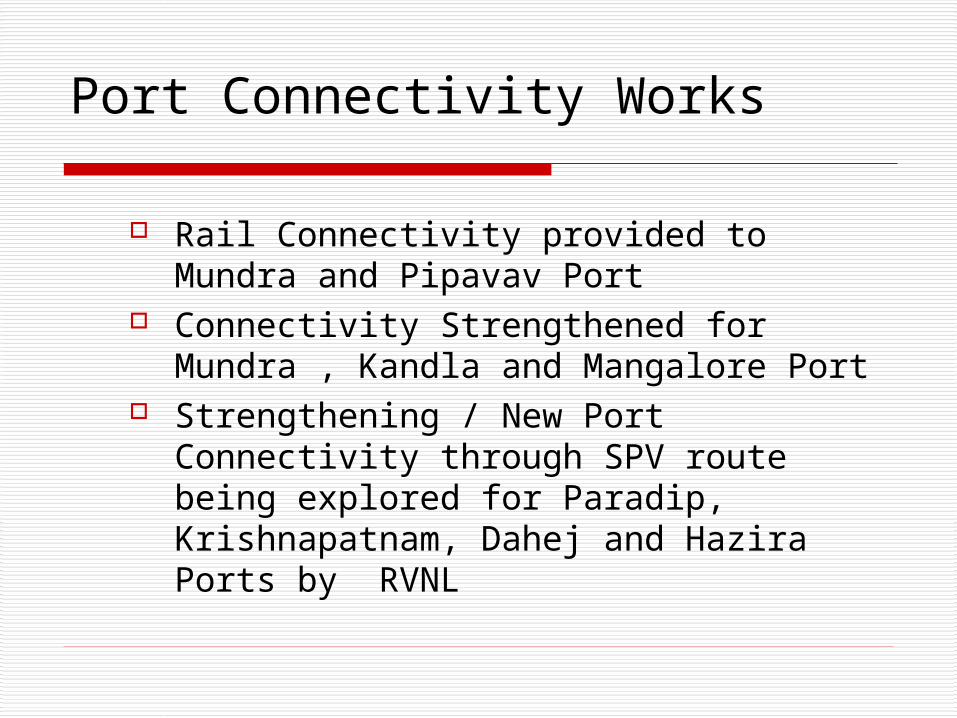

Port Connectivity Works

Rail Connectivity provided to Mundra and Pipavav Port

Connectivity Strengthened for Mundra , Kandla and Mangalore Port

Strengthening / New Port Connectivity through SPV route being explored for Paradip, Krishnapatnam, Dahej and Hazira Ports by RVNL

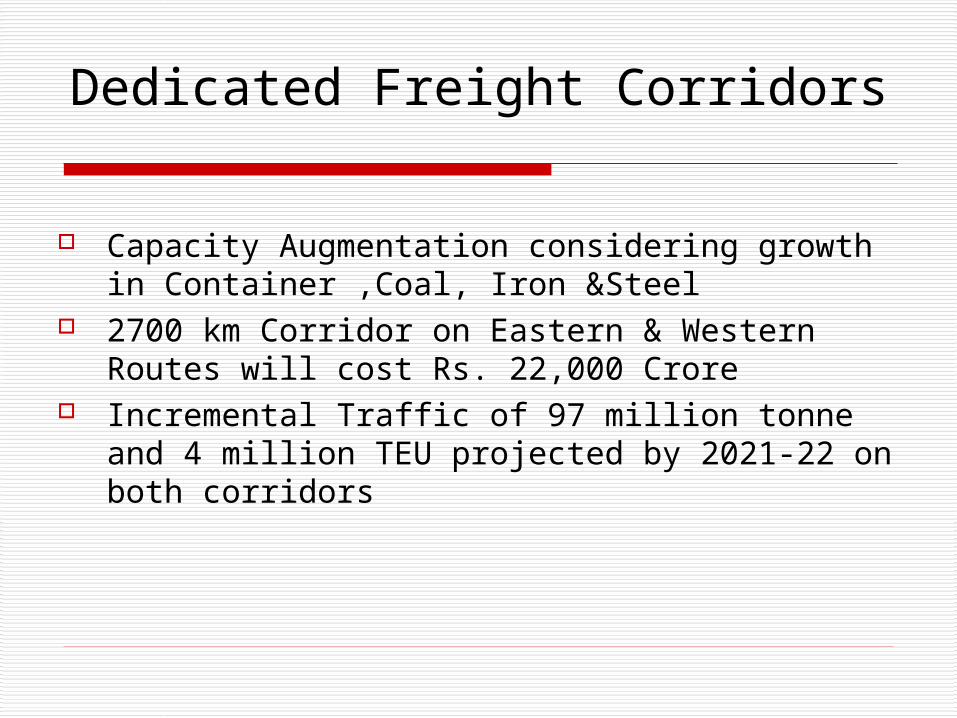

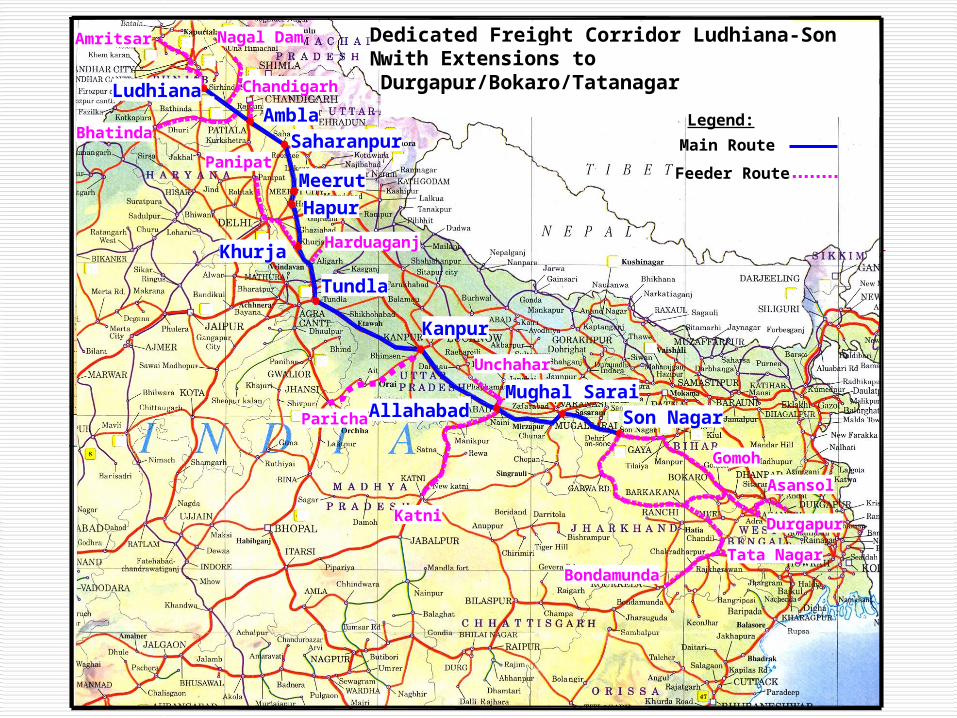

Dedicated Freight Corridors

Capacity Augmentation considering growth in Container ,Coal, Iron &Steel

2700 km Corridor on Eastern & Western Routes will cost Rs. 22,000 Crore

Incremental Traffic of 97 million tonne and 4 million TEU projected by 2021-22 on both corridors

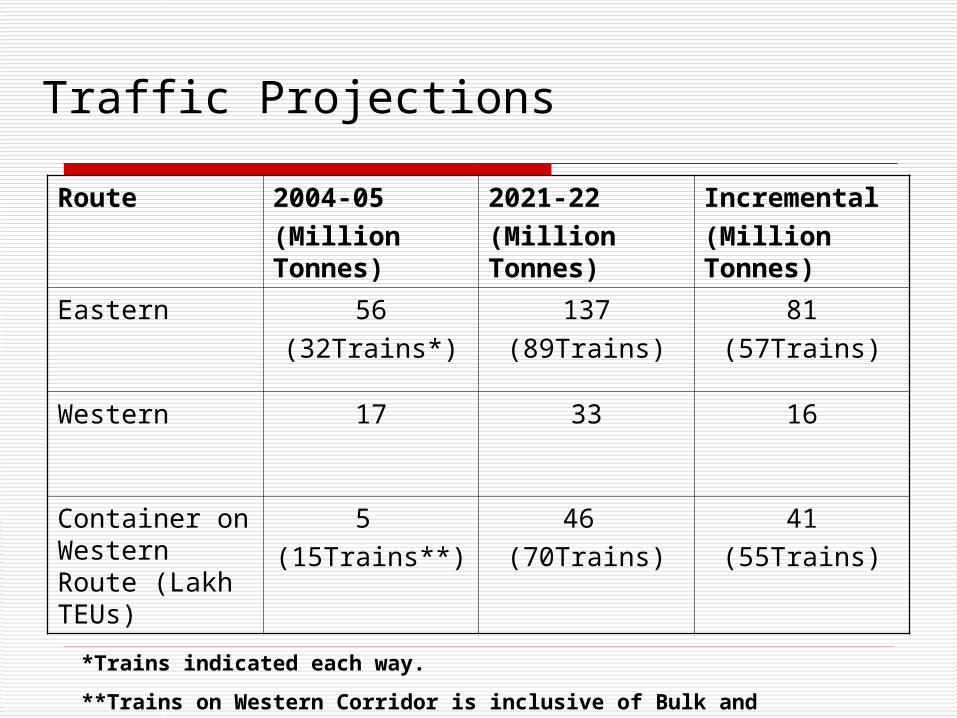

Traffic Projections

Route 2004-05(Million Tonnes)

2021-22(Million Tonnes)

Incremental(Million Tonnes)

Eastern 56(32Trains*)

137(89Trains)

81(57Trains)

Western 17 33 16

Container on Western Route (Lakh TEUs)

5 (15Trains**)

46 (70Trains)

41(55Trains)

*Trains indicated each way.

**Trains on Western Corridor is inclusive of Bulk and Container

Feeder Route

Main Route

Dedicated Freight Corridor Ludhiana-Son Nagar

Asansol

BondamundaTata Nagar

Durgapur

Mughal SaraiAllahabad

Kanpur

Tundla

Khurja

Hapur

Meerut

Saharanpur

AmblaLudhiana

Son Nagar

Gomoh

Unchahar

Katni

Nagal Dam

Chandigarh

Panipat

Harduaganj

Paricha

Amritsar

Bhatinda

with Extensions to Durgapur/Bokaro/Tatanagar

Legend:

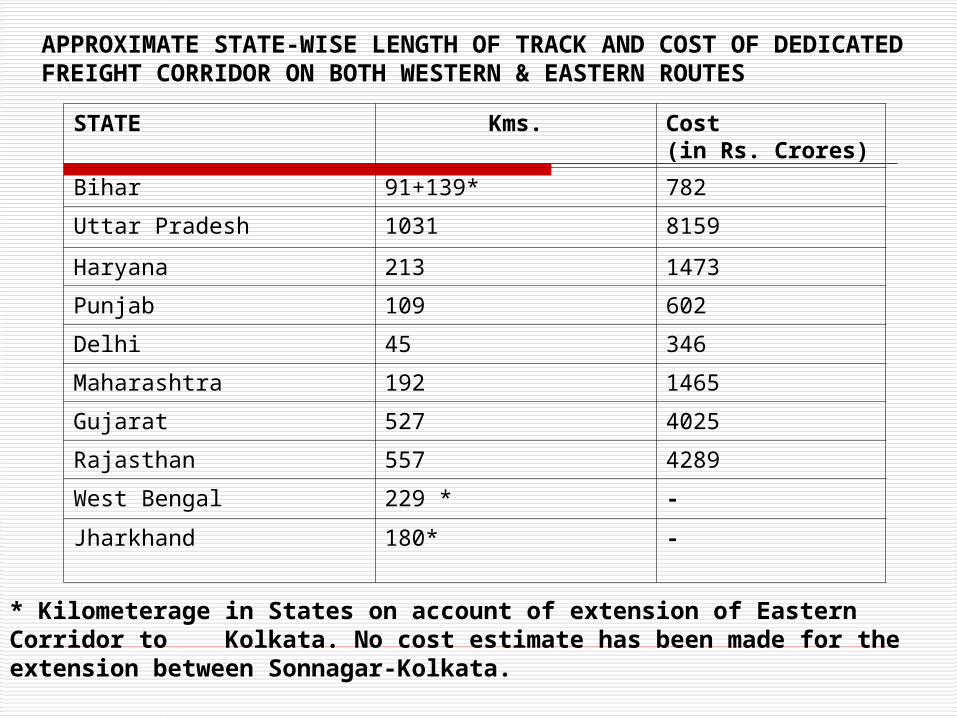

STATE Kms. Cost (in Rs. Crores)

Bihar 91+139* 782

Uttar Pradesh 1031 8159

Haryana 213 1473

Punjab 109 602

Delhi 45 346

Maharashtra 192 1465

Gujarat 527 4025

Rajasthan 557 4289

West Bengal 229 * -

Jharkhand 180* -

APPROXIMATE STATE-WISE LENGTH OF TRACK AND COST OF DEDICATED FREIGHT CORRIDOR ON BOTH WESTERN & EASTERN ROUTES

* Kilometerage in States on account of extension of Eastern Corridor to Kolkata. No cost estimate has been made for the extension between Sonnagar-Kolkata.

Challenges Ahead

Massive Capacity Augmentation ahead of Demand

Resource Mobilisation Induction of appropriate technologies in

Rolling Stock Reducing Unit Cost of Operation

Opportunities under PPP for State Governments

Rail Connectivity to SEZ Logistics Hubs Financing of remote area projects Warehousing/ICD’s ROB/RUB’s Rail Connectivity to Minor Ports

Thank You