Opportunities and challenges of fisheries globalisation ... · Seafood processing local sources,...

37

1 Seafood processing local sources, global markets Alda B. Möller, Seafood Industry Consultant, Iceland Opportunities and challenges of fisheries globalisation

Transcript of Opportunities and challenges of fisheries globalisation ... · Seafood processing local sources,...

1

Seafood processing local sources, global markets

Alda B. Möller, Seafood Industry Consultant, Iceland

Opportunities and challenges of fisheries globalisation

2

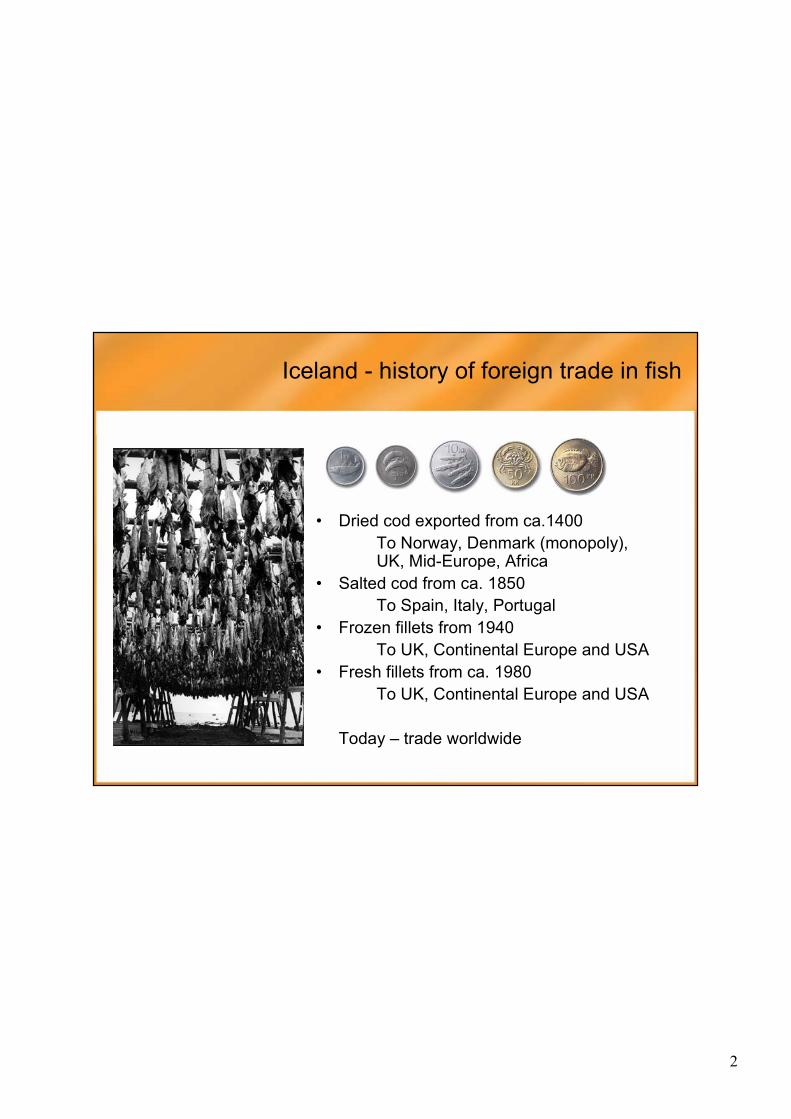

• Dried cod exported from ca.1400To Norway, Denmark (monopoly), UK, Mid-Europe, Africa

• Salted cod from ca. 1850To Spain, Italy, Portugal

• Frozen fillets from 1940To UK, Continental Europe and USA

• Fresh fillets from ca. 1980To UK, Continental Europe and USA

Today – trade worldwide

Iceland - history of foreign trade in fish

3

Iceland - Fisheries in the national economy 2005

• Fisheries create 6.8 % of GDP

• Employ 6.4 % of labour force –10,000 people

• Create 56.7 % of value of export commodities

• Landings were 1.7 million MT

• Exports were 750,000 MT

• Export value ISK 110 billion, equal ~USD 1,750 million

• Population now 310,000

4

Utilization of world fisheries production 1991 - 2004

0

20

40

60

80

100

120

140

1991 1993 1995 1997 1999 2001 2003

Mill

ion

MT

Fresh Frozen Salted/dried Canned Fishmeal Other

Fresh

Frozen

Fishmeal

Salted/driedCanned

Other

Source: FAO Fisheries Stats 2006

5

Fresh and frozen disposition of world fisheries production

26.723.0Frozen - world

54.935.5Fresh - world

12.013.0Frozen – developed countries

2.01.0Fresh – developed countries

14.710.0Frozen – developing countries

52.934.5 Fresh – developing countries

2004 million MT

Live weight

1994 million MT

Live weight

Source: FAO Fisheries Statistics, 2006, Commodities

6

Fresh and frozen disposition of world fisheries production - volume

26.723.0Frozen – world

54.935.5Fresh – world

12.013.0Frozen – developed countries

2.01.0Fresh – developed countries

14.710.0Frozen – developing countries

52.934.5 Fresh – developing countries

2004 million MT

Live weight

1994 million MT

Live weight

Source: FAO Fisheries Statistics, 2006, Commodities

7

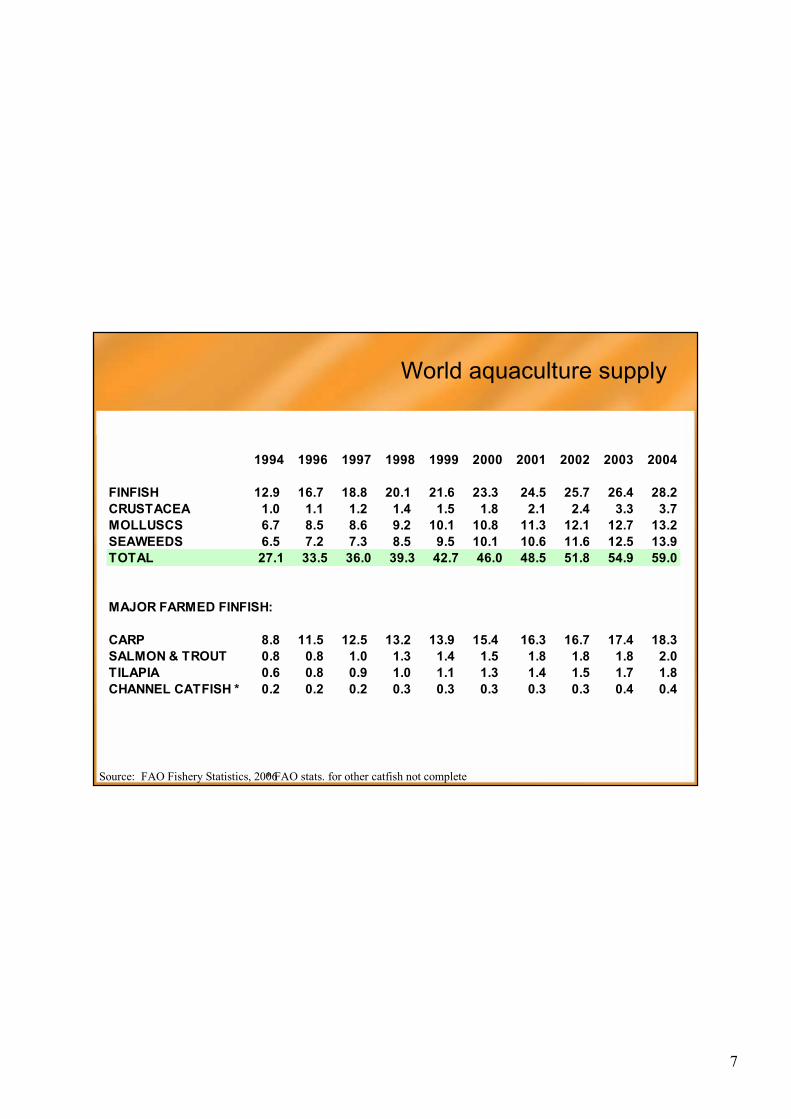

World aquaculture supply

1994 1996 1997 1998 1999 2000 2001 2002 2003 2004

FINFISH 12.9 16.7 18.8 20.1 21.6 23.3 24.5 25.7 26.4 28.2CRUSTACEA 1.0 1.1 1.2 1.4 1.5 1.8 2.1 2.4 3.3 3.7MOLLUSCS 6.7 8.5 8.6 9.2 10.1 10.8 11.3 12.1 12.7 13.2SEAWEEDS 6.5 7.2 7.3 8.5 9.5 10.1 10.6 11.6 12.5 13.9TOTAL 27.1 33.5 36.0 39.3 42.7 46.0 48.5 51.8 54.9 59.0

MAJOR FARMED FINFISH:

CARP 8.8 11.5 12.5 13.2 13.9 15.4 16.3 16.7 17.4 18.3SALMON & TROUT 0.8 0.8 1.0 1.3 1.4 1.5 1.8 1.8 1.8 2.0TILAPIA 0.6 0.8 0.9 1.0 1.1 1.3 1.4 1.5 1.7 1.8CHANNEL CATFISH * 0.2 0.2 0.2 0.3 0.3 0.3 0.3 0.3 0.4 0.4

* FAO stats. for other catfish not completeSource: FAO Fishery Statistics, 2006

8

Trade in world fisheries production

30.233.2Production – developed countries22.719.2Exports – developed countries

30.128.1Exports – developing countries110.379.7Production – developing countries

38%42%Proportion for export52.847.4Exports - world

140.5112.9Production – world

2004 million MT

Live weight

1994 million MT

Live weight

Source: FAO Fisheries Statistics, 2006, Commodities

9

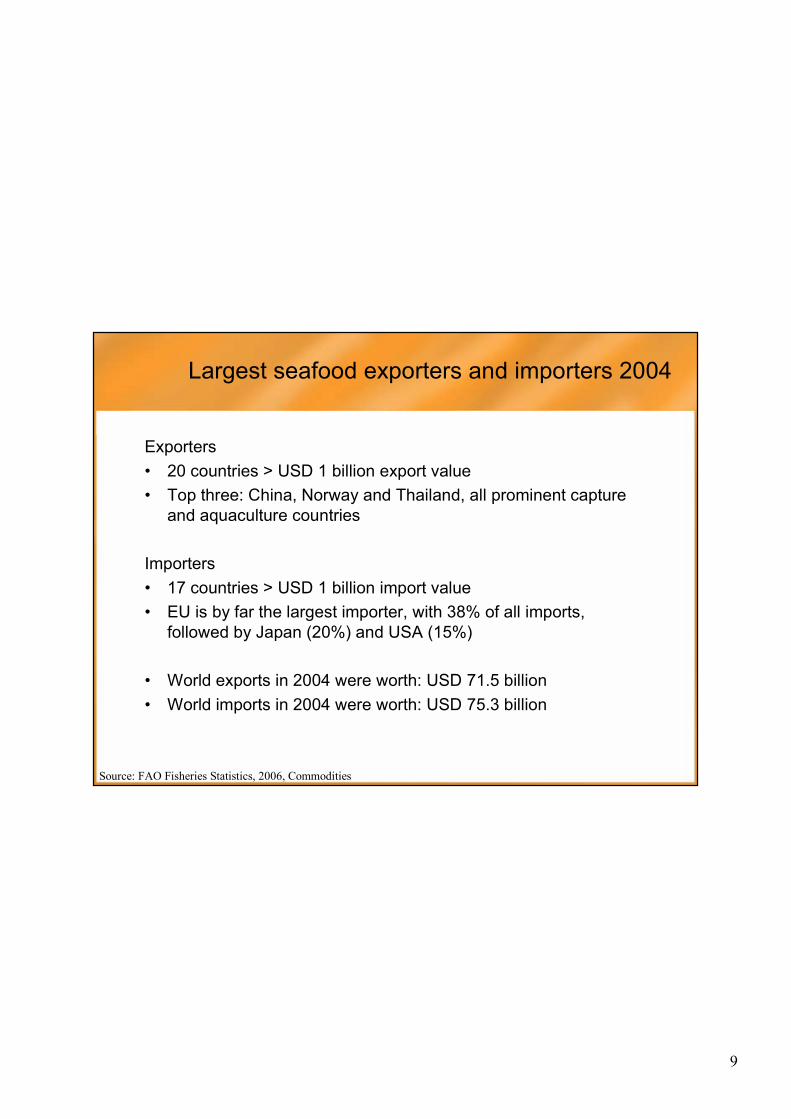

Largest seafood exporters and importers 2004

Exporters • 20 countries > USD 1 billion export value• Top three: China, Norway and Thailand, all prominent capture

and aquaculture countries

Importers• 17 countries > USD 1 billion import value• EU is by far the largest importer, with 38% of all imports,

followed by Japan (20%) and USA (15%)

• World exports in 2004 were worth: USD 71.5 billion• World imports in 2004 were worth: USD 75.3 billion

Source: FAO Fisheries Statistics, 2006, Commodities

10

Fisheries supply for top three importers2001-2003 average

7.6

9.3

11.1

Supply

1.5

0.4

6.4

-Exports

2913.75.4USA

1274.35.4Japan

38010.57.0EU (15)

PopulationMillion people

+Imports

Production

Volume in million MT

Based on: FAO Fisheries Statistics, 2006, Commodities –rounded figures. Non-food uses included

11

EU self sufficiency for fisheries products 1997-2006

0102030405060708090

100

1997 1998 1999 2000 2001 2002 2003 2004* 2005* 2006*

% s

elf s

uffic

ienc

y

Source: AIPCE report 2006, EU 15 1995-2003, EU 25 2004-2006 - *estimates

EU catches vs imports – products for human consumption40% self sufficiency

12

EU imports and own landings of groundfishpollock, cod, haddock, saithe, redfish, hake, hoki, plaice

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1998 1999 2000 2001 2002 2003 2004* 2005*

'000

MT

Imports

EU landings

Source: AIPCE report 2006, EU 15 1995-2003, EU 25 2004-2006 - *estimates

13

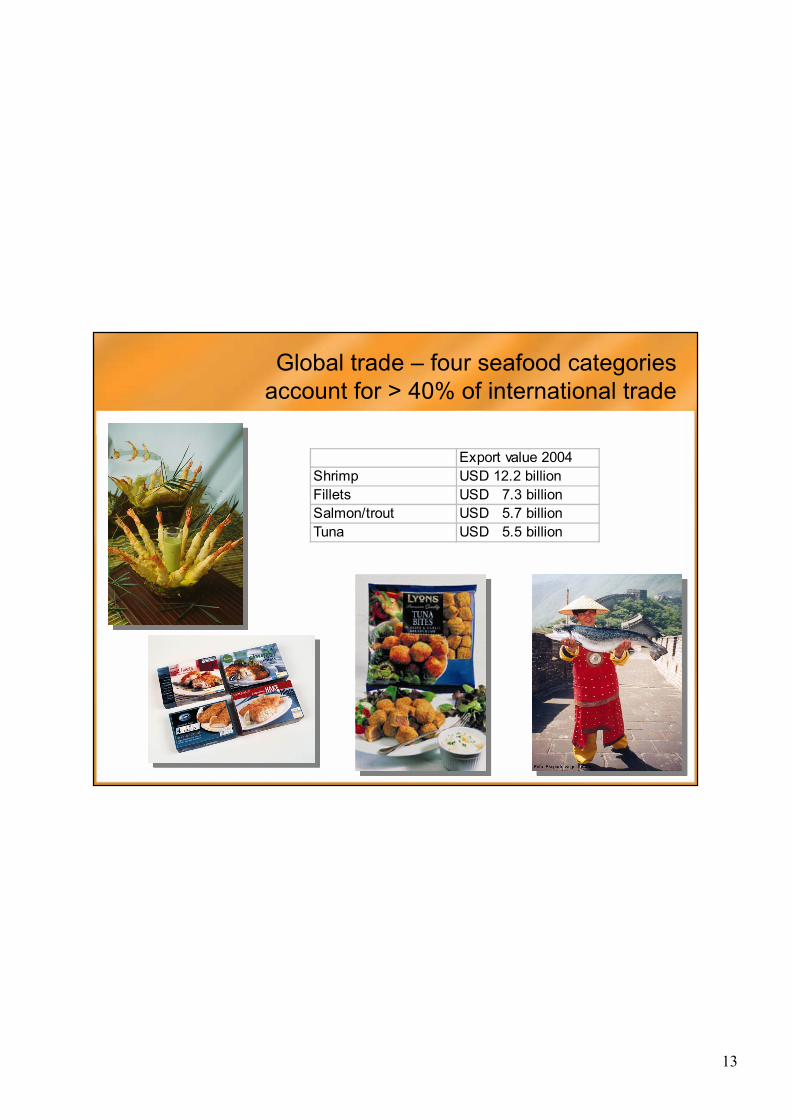

Global trade – four seafood categoriesaccount for > 40% of international trade

Export value 2004Shrimp USD 12.2 billionFillets USD 7.3 billionSalmon/trout USD 5.7 billionTuna USD 5.5 billion

14

Shrimp processing and trade

• 2004 global trade shrimp USD 12.2 billion– frozen USD 8.5 billion– canned USD 2.8 billion– other USD 0.8 billion

• Largest producers: Vietnam, Thailand, India - third of global volume• Largest importers US and Japan ~ 60% of traded volume• Shrimp is top category in US consumption

• Farmed supply dominates global trade• Whiteleg shrimp and black tiger most important traded species

15

Global production of farmed shrimp/prawn - saltwater

559 566 537 480 503 548 633 676 593 666 721

121 142 140 172 194 186 145280 431

10571386

0

500

1,000

1,500

2,000

2,500

3,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

thou

sand

mt

Black tiger shrimp White shrimp Other species

Source: FAO Fisheries Statistics, 2006, Aquaculture

16

Farmed production of white shrimp

0200400600800

1,0001,2001,4001,600

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

thou

sand

s M

T

China Thailand Brazil Equador Others

Source: FAO Fisheries Statistics, 2006, Aquaculture

17

• Shift from black tiger to white shrimp, • White 95% of Thailand producton

• Driven by production issuesImproved productivity for white

• New technology in processing,Automated size grading

• Increased value addition, cooked, peeled and breaded products

Thailand shrimp processing developments

Manual size grading top, automatic grading bottom (Marel)

18

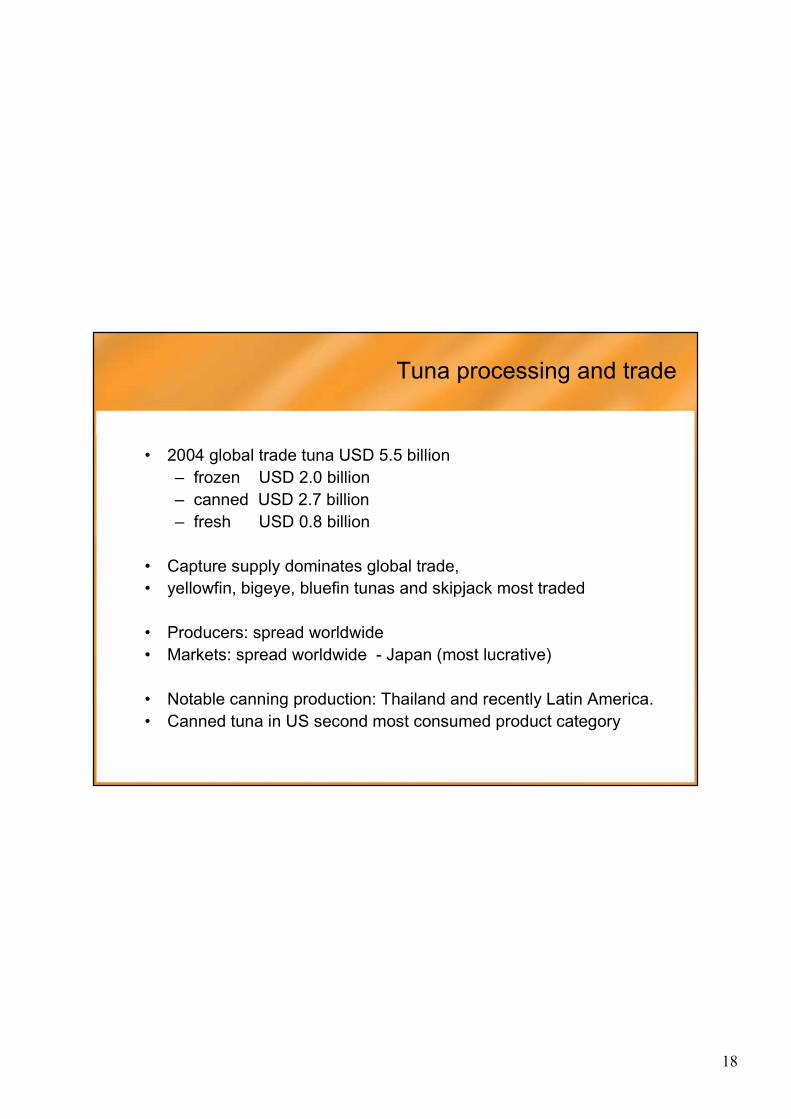

Tuna processing and trade

• 2004 global trade tuna USD 5.5 billion– frozen USD 2.0 billion– canned USD 2.7 billion– fresh USD 0.8 billion

• Capture supply dominates global trade, • yellowfin, bigeye, bluefin tunas and skipjack most traded

• Producers: spread worldwide• Markets: spread worldwide - Japan (most lucrative)

• Notable canning production: Thailand and recently Latin America.• Canned tuna in US second most consumed product category

19

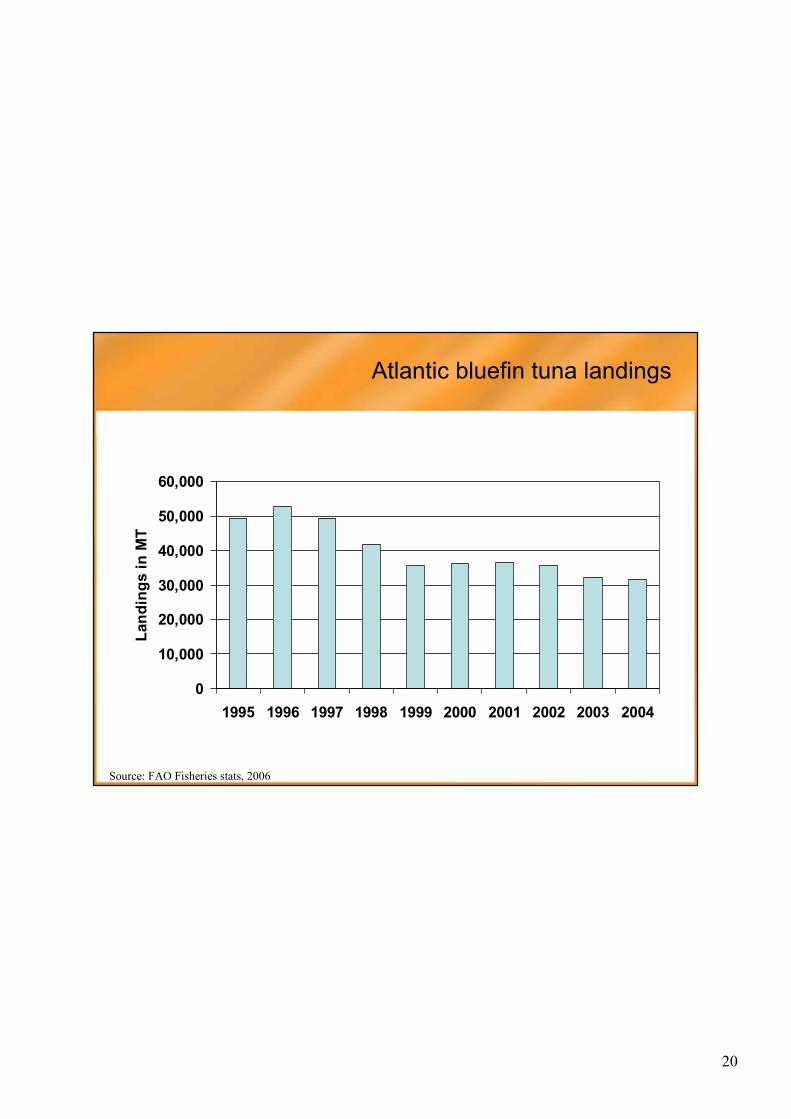

• Atlantic bluefin under great fishing pressure, landings decreasing

• Farming of bluefin tuna increasing, involves capture of small fish and on-growing to market size

• Producers: Spain, Croatia, Turkey • Freshly slaughtered full-size brought to

Japanese motherships for freezing in nitrogen.

• Production in 2004 was 6,500 MT, increasing rapidly

• 80% of Atlantic bluefin imports to Japan are reported to be farmed

Bluefin tuna processing developments

Harvesting farmed Atlantic bluefin tuna

Kali Tuna – Croatia, 2007

20

Atlantic bluefin tuna landings

0

10,000

20,000

30,000

40,000

50,000

60,000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Land

ings

in M

T

Source: FAO Fisheries stats, 2006

21

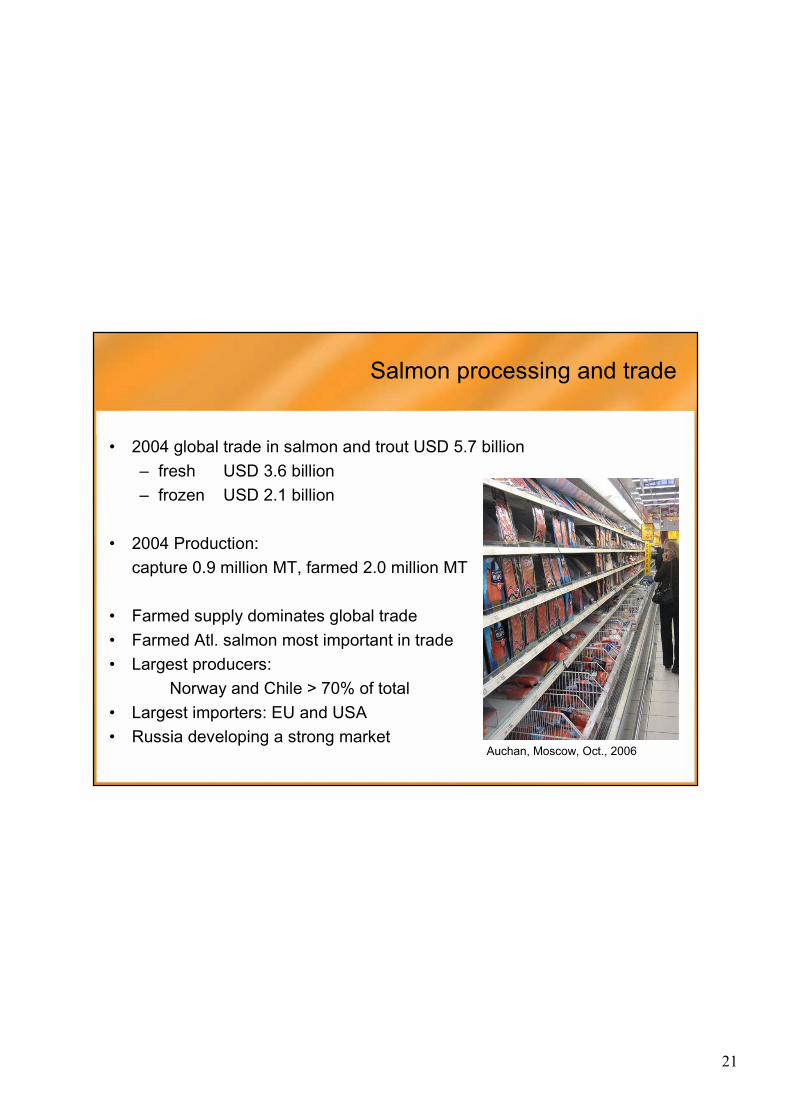

Salmon processing and trade

• 2004 global trade in salmon and trout USD 5.7 billion– fresh USD 3.6 billion– frozen USD 2.1 billion

• 2004 Production: capture 0.9 million MT, farmed 2.0 million MT

• Farmed supply dominates global trade• Farmed Atl. salmon most important in trade• Largest producers:

Norway and Chile > 70% of total• Largest importers: EU and USA • Russia developing a strong market

Auchan, Moscow, Oct., 2006

22

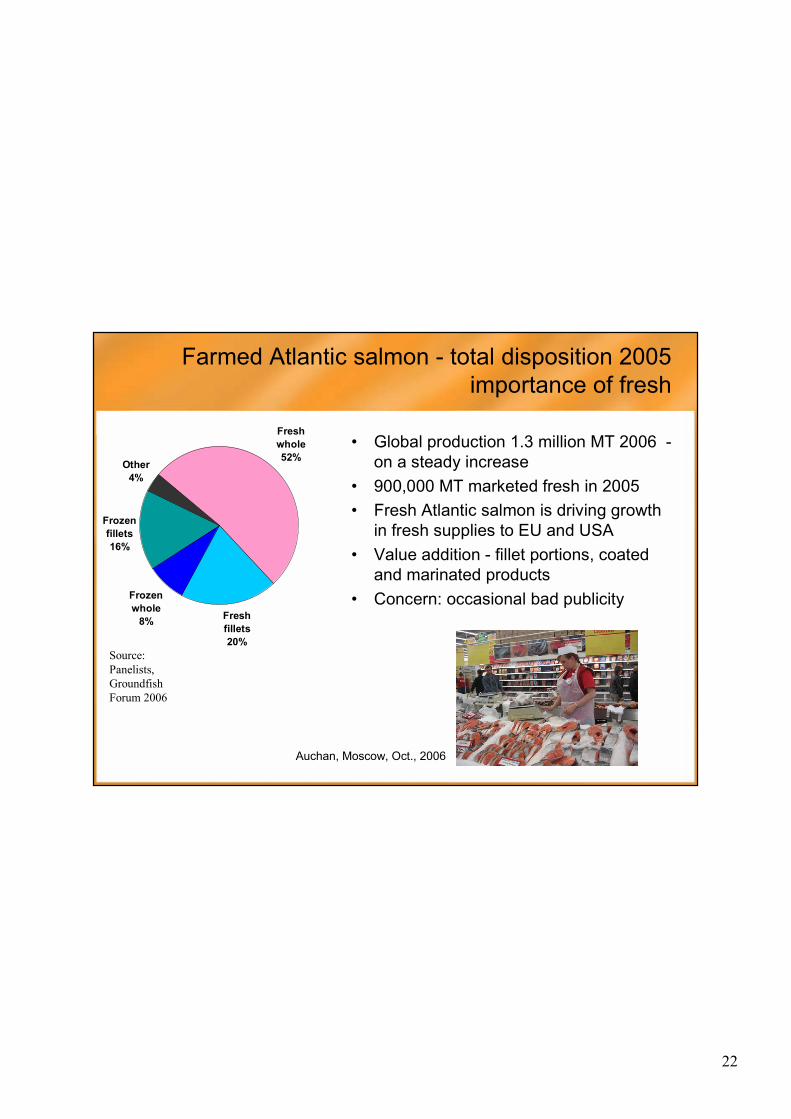

Farmed Atlantic salmon - total disposition 2005importance of fresh

• Global production 1.3 million MT 2006 -on a steady increase

• 900,000 MT marketed fresh in 2005• Fresh Atlantic salmon is driving growth

in fresh supplies to EU and USA• Value addition - fillet portions, coated

and marinated products• Concern: occasional bad publicity

Fresh whole52%

Fresh fillets20%

Frozen whole

8%

Frozen fillets16%

Other4%

Auchan, Moscow, Oct., 2006

Source: Panelists, Groundfish Forum 2006

23

Fish fillet processing and trade

• 2004 global trade fish fillets USD 7.3 billion– frozen USD 5.6 billion– fresh USD 1.7 billion

• Whitefish fillets dominate global trade

• Paper focuses on six case studies– Pangasius fillets from Vietnam– Hake from Namibia– Alaska pollock from the US– Alaska pollock from Russia– Chinese re-processing industry– Icelandic cod and haddock fresh fillet industry

24

Pangasius fillets from Vietnam

• Farmed whitefish from Vietnam• Production increasing rapidly• ~750,000 MT (LW) in 2006• Filleted and mostly exported

Pangasius hypophthalmus

0

100

200

300

400

500

600

700

800

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005* 2006*

'000

MT

Source: VASEP

25

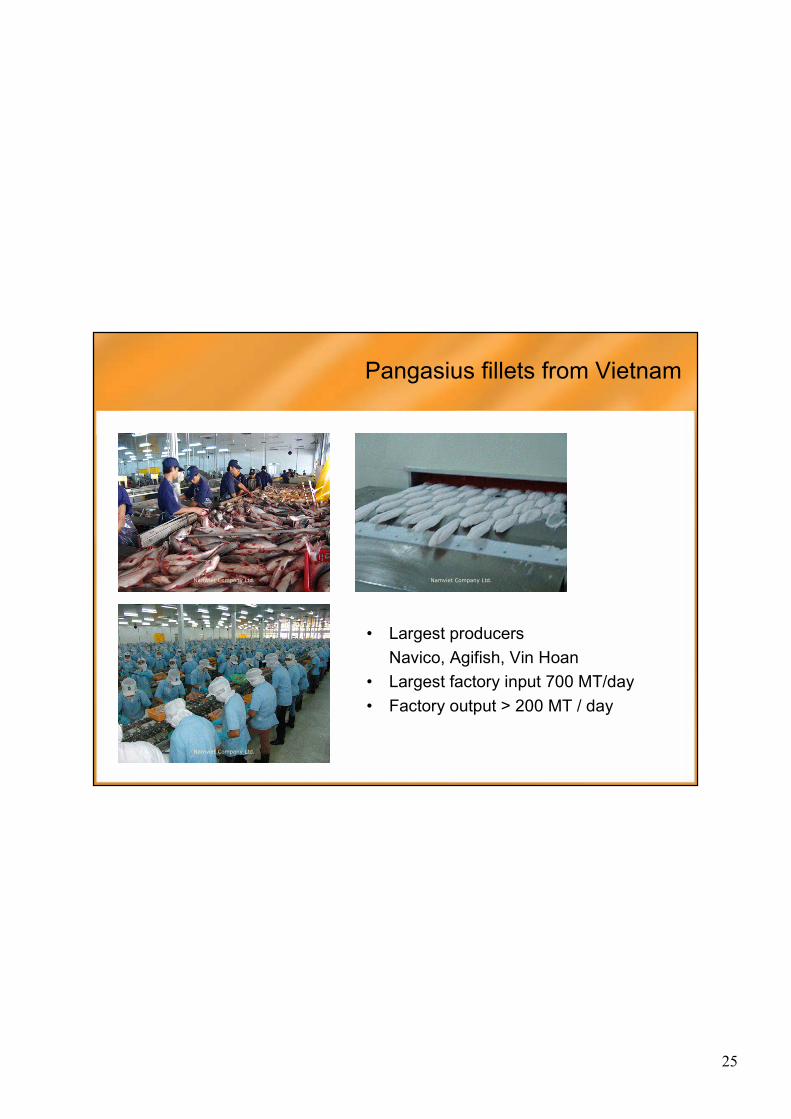

Pangasius fillets from Vietnam

Namviet Company Ltd.

Namviet Company Ltd.

Namviet Company Ltd.

• Largest producers Navico, Agifish, Vin Hoan

• Largest factory input 700 MT/day • Factory output > 200 MT / day

26

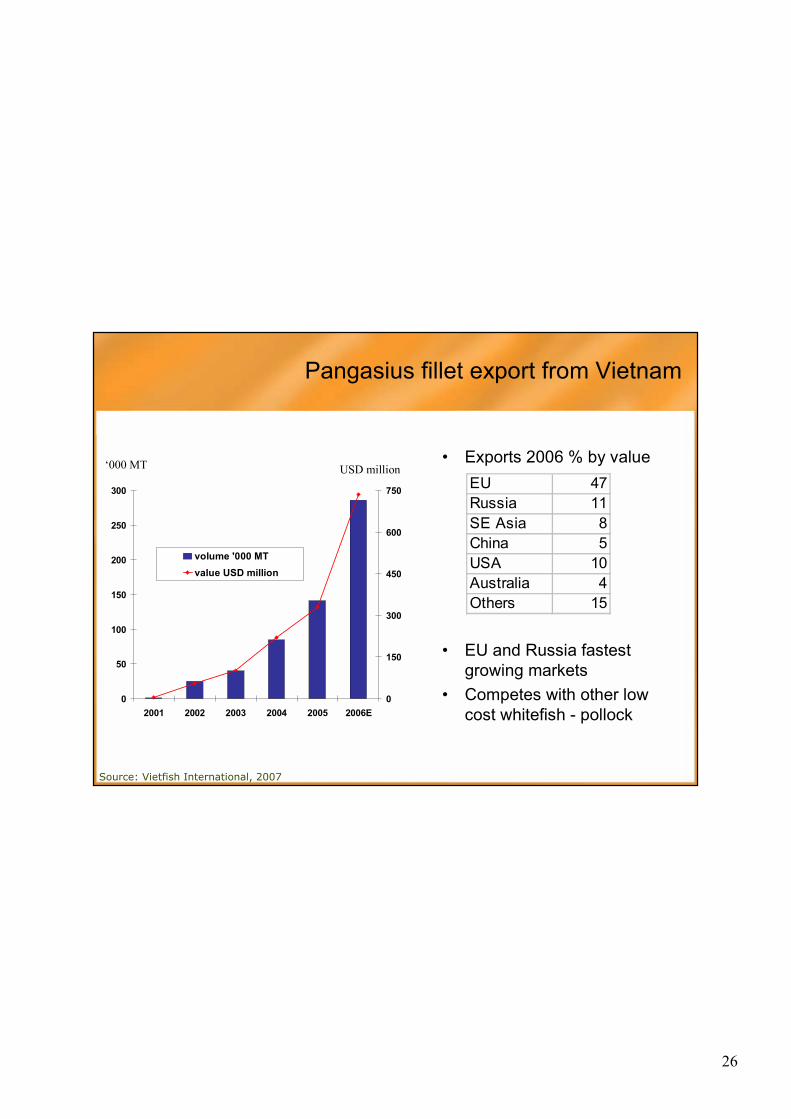

• Exports 2006 % by value

• EU and Russia fastest growing markets

• Competes with other low cost whitefish - pollock

0

50

100

150

200

250

300

2001 2002 2003 2004 2005 2006E0

150

300

450

600

750

volume '000 MTvalue USD million

Source: Vietfish International, 2007

EU 47Russia 11SE Asia 8China 5USA 10Australia 4Others 15

Pangasius fillet export from Vietnam

‘000 MT USD million

27

Drivers and challenges for Vietnamese pangasius

• Drivers:Abundance and moderate price, adequate quality

• Challenges for producers– Anti-dumping taxes in the US – Cost inflation– Possible shortage of labour– Food safety issues– Integration and consolidation

Namviet Company Ltd.

28

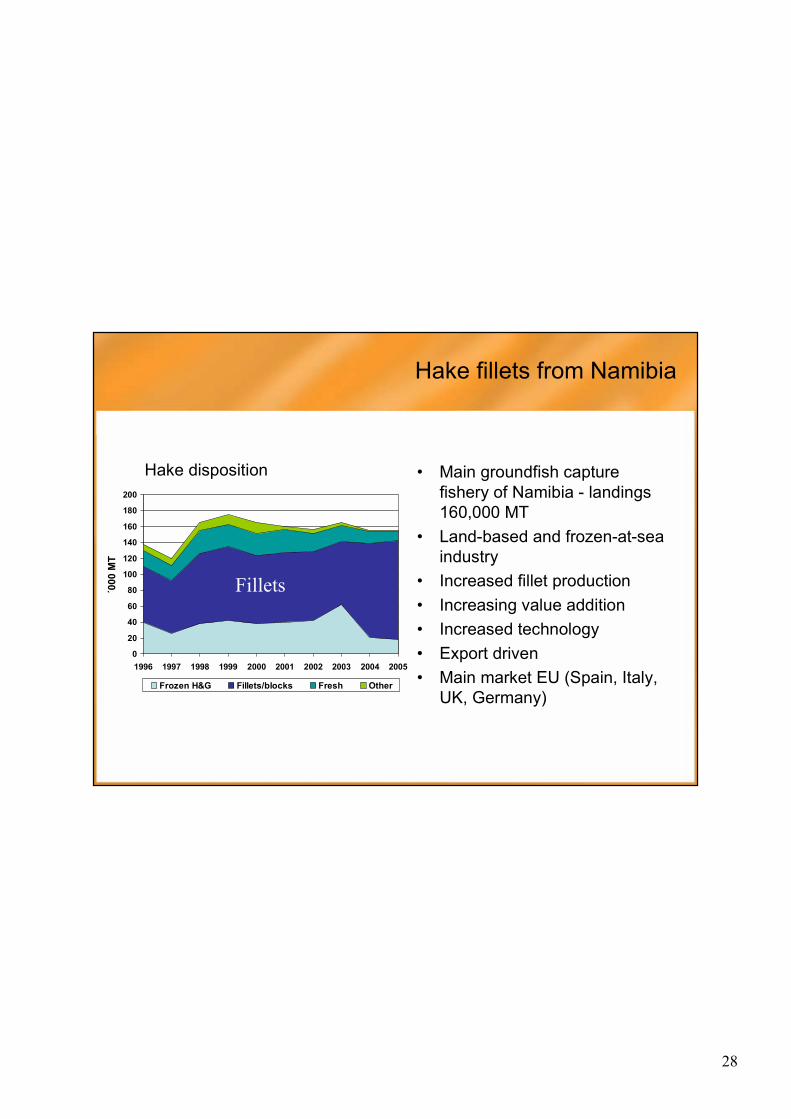

Hake fillets from Namibia

• Main groundfish capture fishery of Namibia - landings 160,000 MT

• Land-based and frozen-at-sea industry

• Increased fillet production • Increasing value addition• Increased technology• Export driven• Main market EU (Spain, Italy,

UK, Germany)

0

20

40

60

80

100

120

140

160

180

200

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

´000

MT

Frozen H&G Fillets/blocks Fresh Other

Fillets

Hake disposition

29

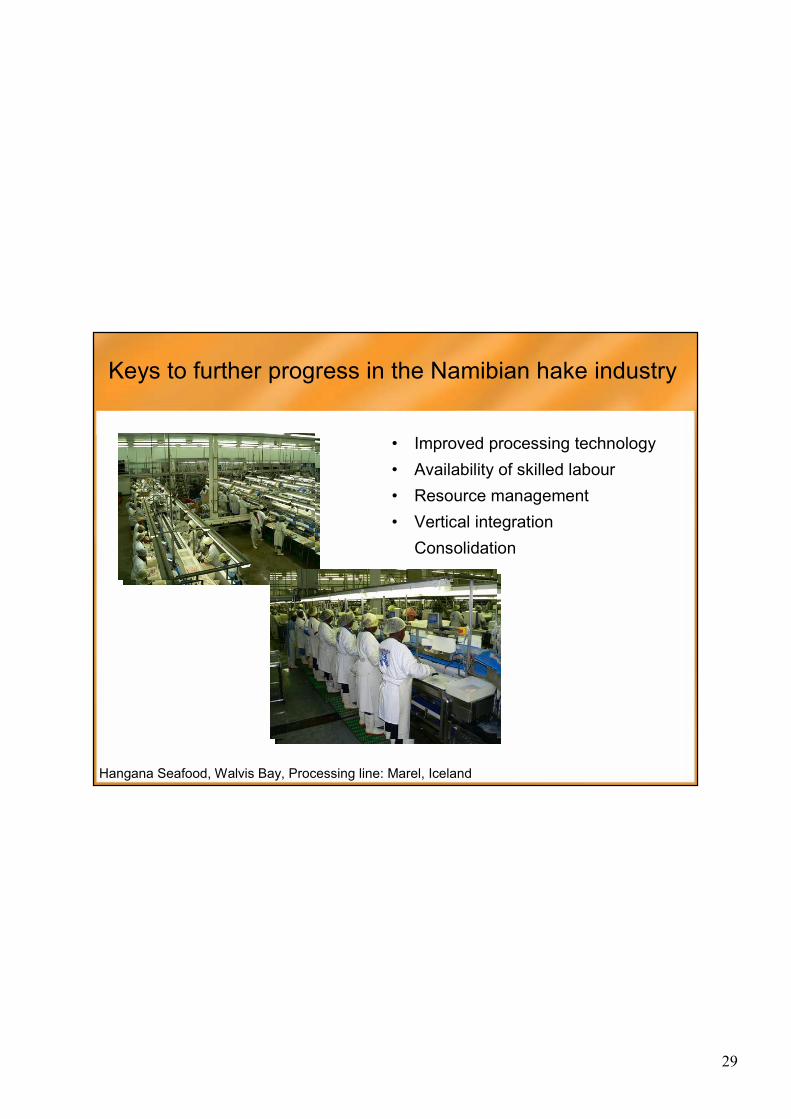

Keys to further progress in the Namibian hake industry

• Improved processing technology• Availability of skilled labour• Resource management • Vertical integration

Consolidation

Hangana Seafood, Walvis Bay, Processing line: Marel, Iceland

30

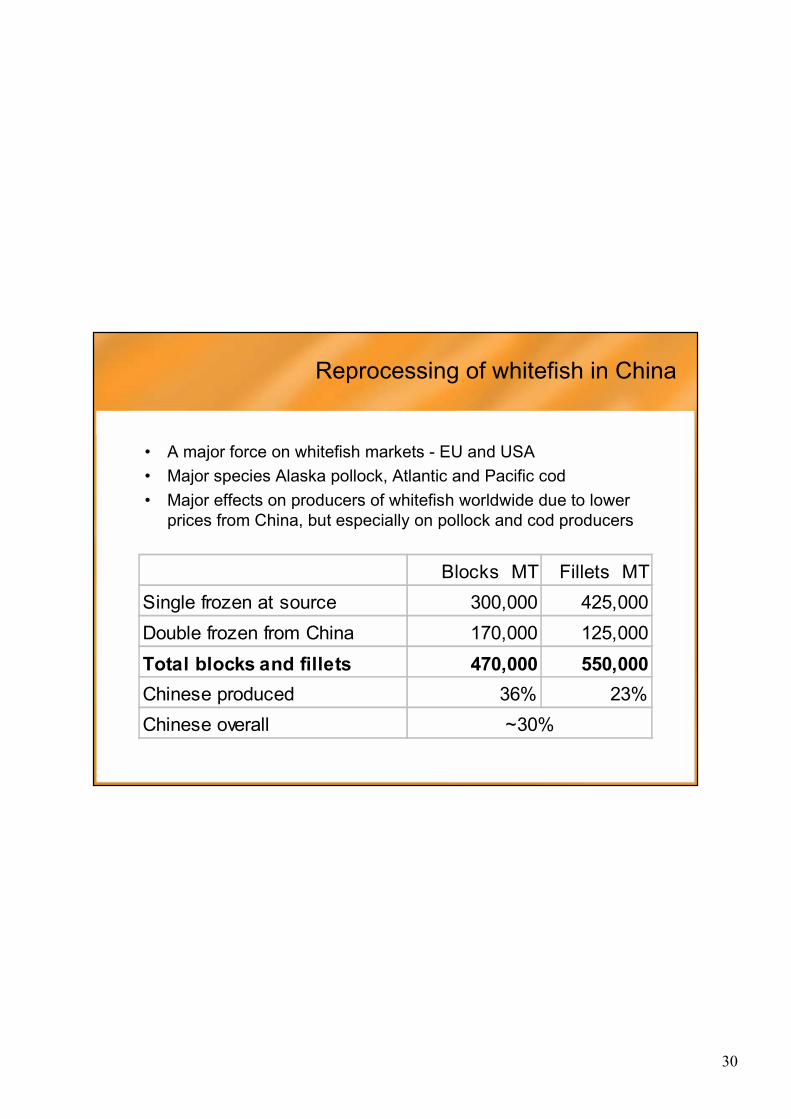

• A major force on whitefish markets - EU and USA• Major species Alaska pollock, Atlantic and Pacific cod• Major effects on producers of whitefish worldwide due to lower

prices from China, but especially on pollock and cod producers

Blocks MT Fillets MTSingle frozen at source 300,000 425,000Double frozen from China 170,000 125,000Total blocks and fillets 470,000 550,000Chinese produced 36% 23%Chinese overall ~30%

Reprocessing of whitefish in China

31

0

20

40

60

80

100

120

140

160

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

'000

MT

prod

uct w

eigh

t

EU USA

EU

US

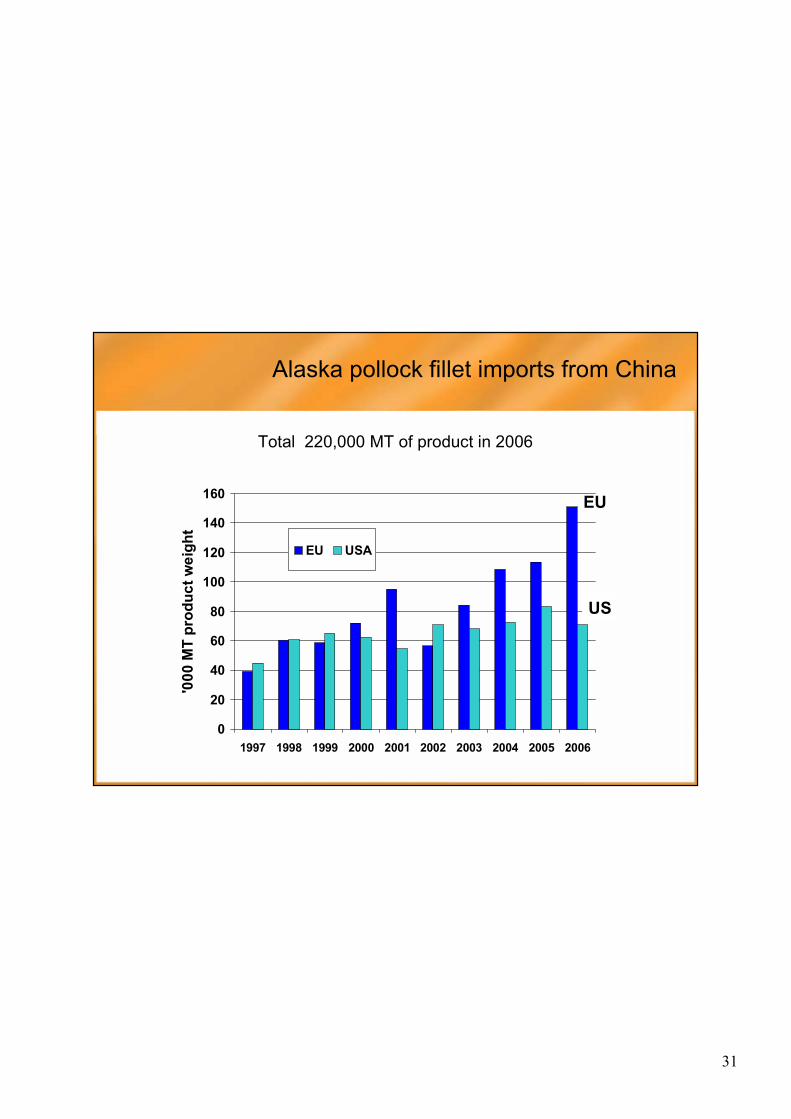

Alaska pollock fillet imports from China

Total 220,000 MT of product in 2006

32

0

10

20

30

40

50

60

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

'000

MT

prod

uct w

eigh

t

EU USA

EU

US

Cod fillet imports from China

Total 90,000 MT of product in 2006

33

• Drivers:Value addition in processing, increased number of species Abundance and moderate price, adequate quality

• Challenges for producers in China· Strength of the RMB · Increased overhead and labour costs· Labour shortage· Quality issues

Drivers and challenges for fillets from China

It is “glorious to get rich”Deng Xiaoping, 1980

34

02468

101214161820

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

'000

MT

prod

uct w

eigh

t

0

50

100

150

200

250

300

350

'000

MT

tota

l lan

ding

s

Fresh products Total catch

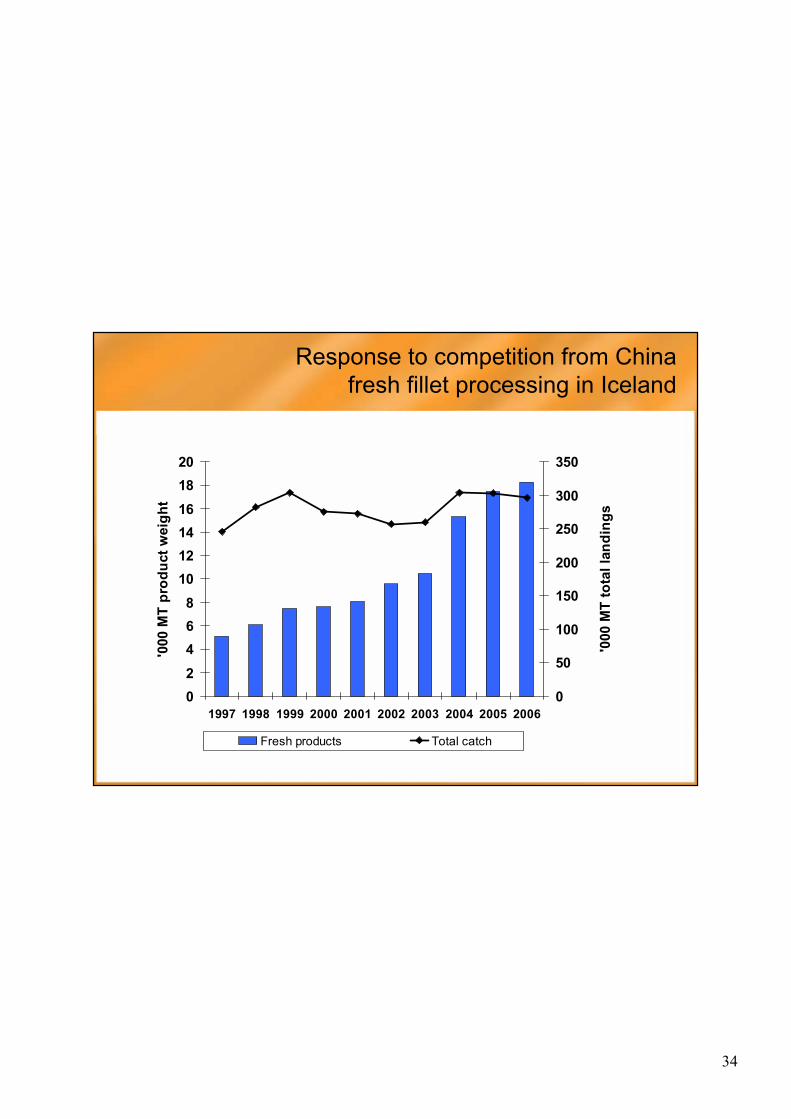

Response to competition from China fresh fillet processing in Iceland

35

0

200

400

600

800

1000

1200

1400

1992 1994 1996 1998 2000 2002 2004 2006

Mill

ion

GB

P

Frozen seafood

Chilled seafood

Fresh market development in the UK

Source: Seafish Industry Authority, UK

UK retail seafood value

36

Recognised drivers and seafood preferences

Universal drivers– Demographic and lifestyle trends– Consumer sophistication and knowledge

⇒ Seafood preferencesSimple preparationsStreet foodsFresh, healthy and functional,Diversification of flavoursEthical behaviour in food choices

37

Thank you

Opportunities and challenges of fisheries globalisation