“Operational Risk Model Framework – the (Missing?) Heart ...

56

“Operational Risk Model Framework – the (Missing?) Heart of Basel II Advanced Measurement Approach (AMA)” ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.) ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering) ๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

Transcript of “Operational Risk Model Framework – the (Missing?) Heart ...

“Operational Risk Model Framework – the

(Missing?) Heart of Basel II Advanced

Measurement Approach (AMA)”ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)

ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

[2]

… (Missing?) Heart of Basel II Advanced Measurement Approach …

๑. ภูมิหลัง นิยาม และแนวคิด (introductory)

– อะไรคือความเสี่ยงดานปฏิบตัิการ? กรอบการบริหารจัดการ/กระบวนการจําลองแบบ?

๒. แนวทางการจําลองแบบ (conceptual)

– คณิตศาสตร สถิติศาสตร แบบจําลองความเสี่ยงดานปฏิบตัิการ หนาตาเปนอยางไร?

๓. เทคนิคและระเบียบวิธี (technical)

– การจําลองแบบความเสี่ยงดานปฏิบัติการแตกตางจากในดานอื่นๆ หรือไม อยางไร?

๔. เกณฑการกาํกับดูแล (practical)

– การดํารงเงินกองทุนเพื่อรองรบัความเสี่ยงดานปฏิบัติการ? ธรรมภบิาล? วิทยาการ?

๑. ภูมิหลัง นิยาม และแนวคดิ

ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)

๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

[4]

… 2548 …

[5]

… 2549 …

[6]

… 2553 …

[7]

… เรามานิยามความเสี่ยงกันดีกวา …

Risk ความเสี่ยง

– Certainty ทราบวาอะไรจะเกิดขึ้นแน ๆ

– Risk ทราบวาอะไรสามารถเกิดขึ้น และ ดวยความนาจะเปนเทาใด อีกทั้ง ซาบซึ้งในผลกระทบ

POSSIBILITY ความเปนไปได PROBABILITY ความนาจะเปน UTILITY อรรถประโยชน

– Uncertainty ไมทราบวาอะไรจะเกิดขึ้น แต พอจะทราบไดวาอะไรสามารถเกิดขึ้น

– !@#$%^&* ไมทราบวาอะไรจะเกิดขึ้น และ ไมทราบวาอะไรสามารถเกิดขึ้น

Financial Risk ความเสี่ยงทางการเงิน

– … where utility proxied/measured in monetary unit

– … arise from movements of financial variables

– … mitigated by financial means/instruments

– … intrinsic to financial market/institution

[8]

… ทฤษฎอีรรถประโยชน …

Risk has upside as well as downside, so why is it undesirable?

Utility Theory [Neumann & Morgenstern (1947)]

– Certainty Equivalence Principle:

– 100%Pr(1ล.บ.) + 0%Pr(0ล.บ.) expected is equivalent to 1ล.บ. sure thing U(1ล.บ.) = 1

– 90%Pr(1ล.บ.) + 10%Pr(0ล.บ.) expected is equivalent to 0.5ล.บ. sure thing U(0.5ล.บ.) = 0.9

– 1%Pr(1ล.บ.) + 99%Pr(0ล.บ.) expected is equivalent to 10,000บ. sure thing U(10,000.บ.) = 0.01

– .02%Pr(1ล.บ.) + 99.98%Pr(0ล.บ.) expected is equivalent to 400บ. sure thing U(400บ.) = 0.0002

– 0%Pr(1ล.บ.) + 100%Pr(0ล.บ.) expected is equivalent to 0ล.บ. sure thing U(0ล.บ.) = 0

– Risk Appetite/Attitude/Aversion:

– U(0.5ล.บ.) = 0.9 > 0.5 = E[50%Pr(1ล.บ.) + 50%Pr(0ล.บ.)] risk averse

– U(10,000บ.) = 0.01 = 0.01 = E[1%Pr(1ล.บ.) + 99%Pr(0ล.บ.)] risk neutral

– U(400บ.) = 0.0002 < 0.0004 = E[.04%Pr(1ล.บ.) + 99.96%Pr(0ล.บ.)] risk seeking

[9]

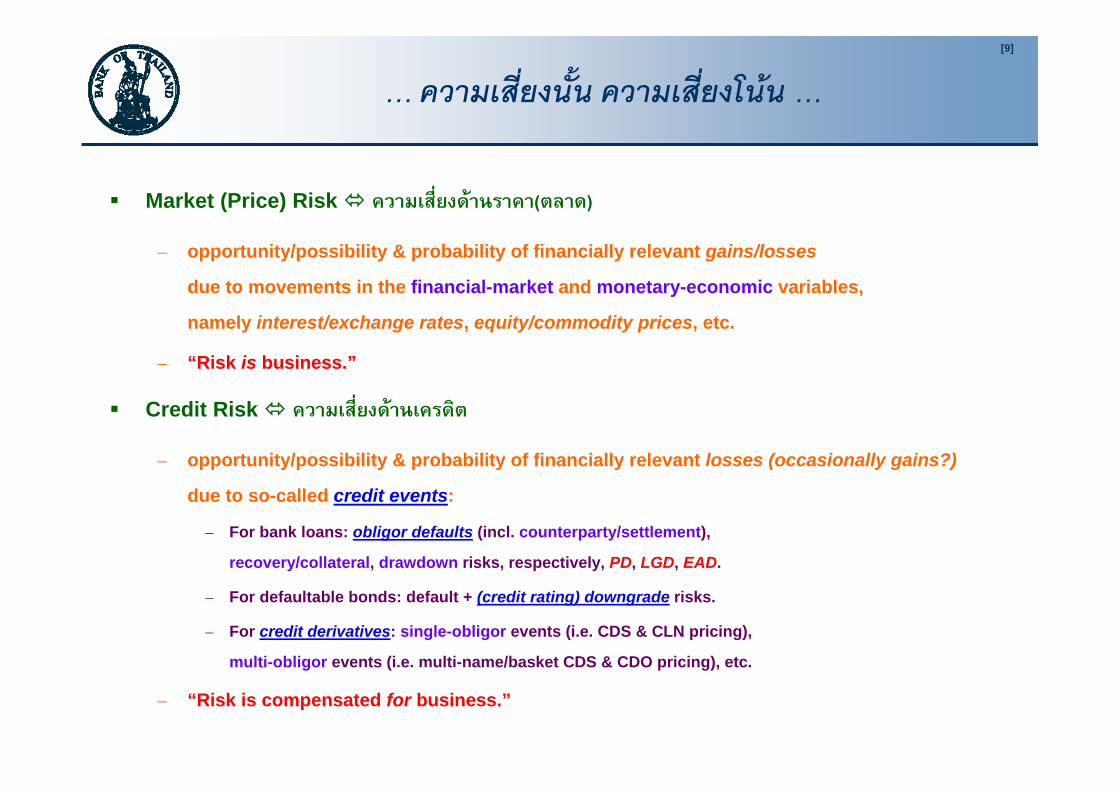

… ความเสี่ยงนั้น ความเสี่ยงโนน …

Market (Price) Risk ความเสี่ยงดานราคา(ตลาด)

– opportunity/possibility & probability of financially relevant gains/losses

due to movements in the financial-market and monetary-economic variables,

namely interest/exchange rates, equity/commodity prices, etc.

– “Risk is business.”

Credit Risk ความเสี่ยงดานเครดิต

– opportunity/possibility & probability of financially relevant losses (occasionally gains?)

due to so-called credit events:

– For bank loans: obligor defaults (incl. counterparty/settlement),

recovery/collateral, drawdown risks, respectively, PD, LGD, EAD.

– For defaultable bonds: default + (credit rating) downgrade risks.

– For credit derivatives: single-obligor events (i.e. CDS & CLN pricing),

multi-obligor events (i.e. multi-name/basket CDS & CDO pricing), etc.

– “Risk is compensated for business.”

[10]

… ความเสี่ยงนี้ …

Operational Risk ความเสี่ยงดานปฏิบัติการ

– refers to the opportunity, possibility, and probability of preventable occurrence of failures,

frauds or errors together with non-preventable events in the form of random accidents, natural

catastrophes, as well as man-made disasters, whence resulting in material losses, disruptions,

and/or various infractions, thereby severely and adversely impacting financial condition,

business conduct, and institutional integrity overall

หมายถึง โอกาส ความเปนไปได และความนาจะเปน ที่จะเกิดความบกพรอง การทุจริต หรือความผิดพลาด ซึ่งเปน

เหตุการณที่ปองกันได กับทั้งเหตุสุดวิสัยทัง้ในรูปอุบัติเหต ุภัยธรรมชาต ิรวมถงึภัยคุกคามโดยมนุษย อันจักนําไปสู

ความเสียหาย ความชะงักงัน และ/หรือการลวงละเมิดกฎเกณฑตาง ๆ กระทั่งเปนผลรายและรุนแรงตอสถานภาพทาง

การเงิน การดาํเนินธุรกิจ และความมั่นคงนาเชื่อถือของสถาบันโดยรวม

– “Risk comes with being in business.”

– For Basel II, operational risk is defined as the risk of loss resulting: [i] from inadequate or failed

internal processes, people and systems or [ii] from external events (+legal -reputational -strategic).

[11]

… เราเขาใจ ‘หลักการบริหารความเสี่ยง’ กันอยางไร …

(Financial) Risk Management การบริหารจัดการความเสี่ยง(ทางการเงิน)

Basel Committee on Banking Supervision (BCBS) –Sound Practices for the Management and Supervision of Operational Risk (2003) 10 Principles

– Risk Management Framework กรอบการบริหารจัดการความเสี่ยง

P.1,2,3GOVERNANCE ธรรมาภิบาล

TECHNOLOGY วิทยาการ

RESOURCES ทรัพยากร

– Risk Management Process กระบวนการบริหารจัดการความเสี่ยง

P.4IDENTIFY กําหนด

P.4,5MEASURE วดั

P.6,7MITIGATE ขจดั

REVIEW ทบทวน

๒. แนวทางการจําลองแบบ

ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)

ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)

๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

[13]

[14]

[15]

[16]

[17]

[18]

[19]

[20]

๓. เทคนิคและระเบียบวธิี

ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)

ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)

๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

[22]

[23]

[24]

[25]

[26]

[27]

[28]

[29]

[30]

[31]

[32]

[33]

[34]

[35]

๔. เกณฑการกํากับดแูล

ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)

ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)

๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)

[37]

[38]

[39]

[40]

[41]

[42]

[43]

[44]

[45]

[46]

[47]

[48]

[49]

[50]

[51]

[52]

[53]

[54]

[55]

ขอบพระคุณครับผม

Q&A

ดร.พูมใจ นาคสกุล (Poomjai Nacaskul, Ph.D.)ทีมแบบจําลองเชิงปริมาณและวิศวกรรมการเงิน (Quantitative Models & Financial Engineering)

๒๘ ตุลาคม ๒๕๕๓ (28-Oct-2010)