Operational Budgeting Operational Budgeting Exercises ACTG 321 Agenda for Lecture 15.

38

• Operational Budgeting • Operational Budgeting Exercises ACTG 321 Agenda for Lecture 15

-

Upload

solomon-todd -

Category

Documents

-

view

221 -

download

1

Transcript of Operational Budgeting Operational Budgeting Exercises ACTG 321 Agenda for Lecture 15.

• Operational Budgeting

• Operational Budgeting Exercises

ACTG 321Agenda for Lecture 15

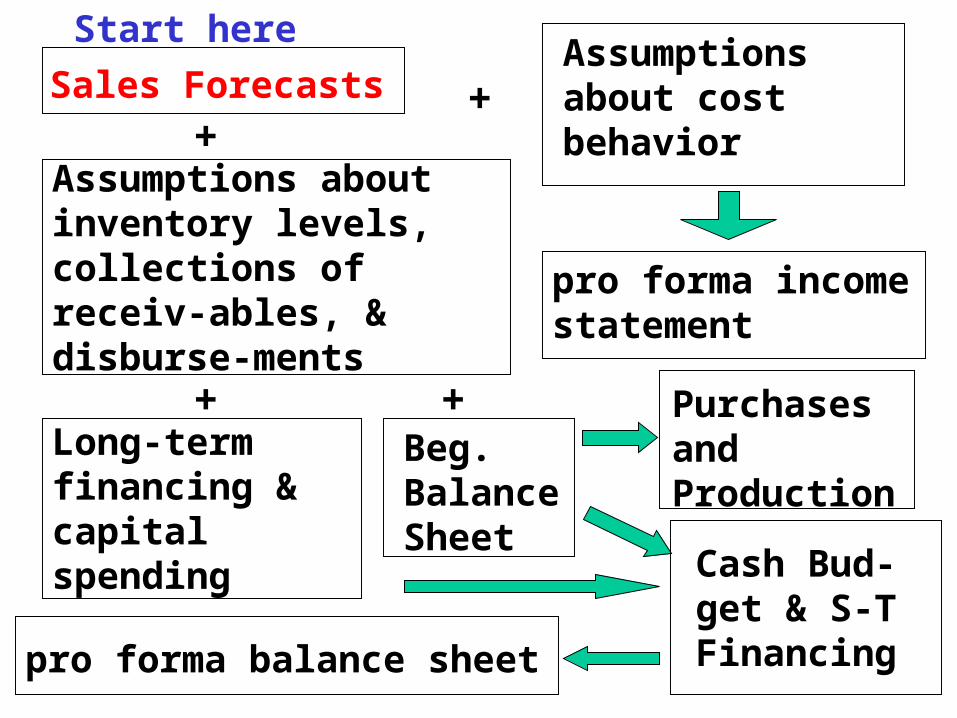

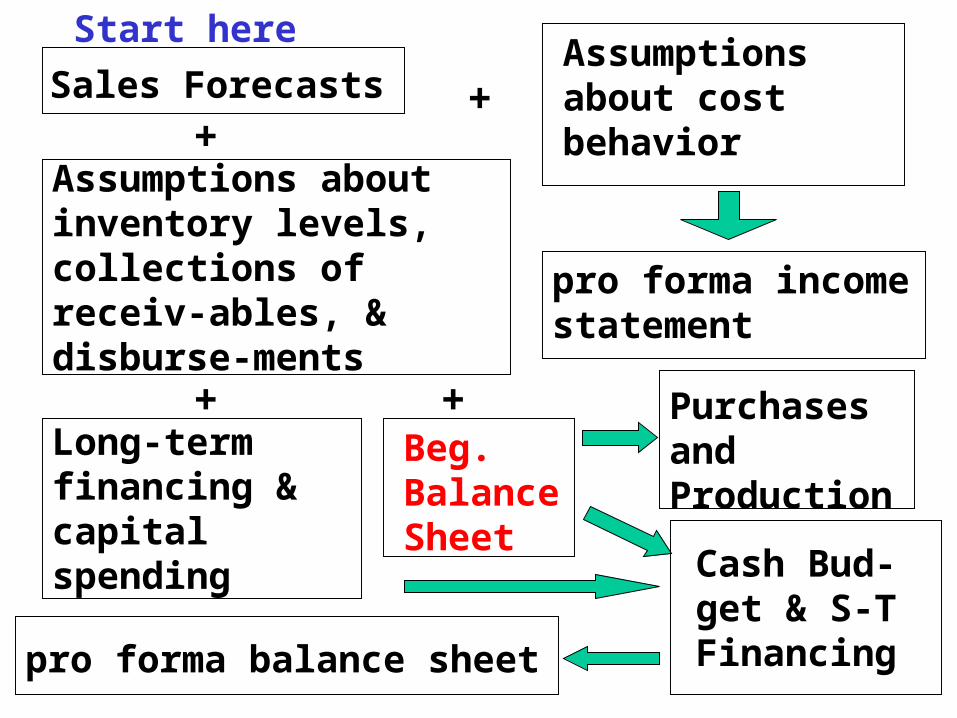

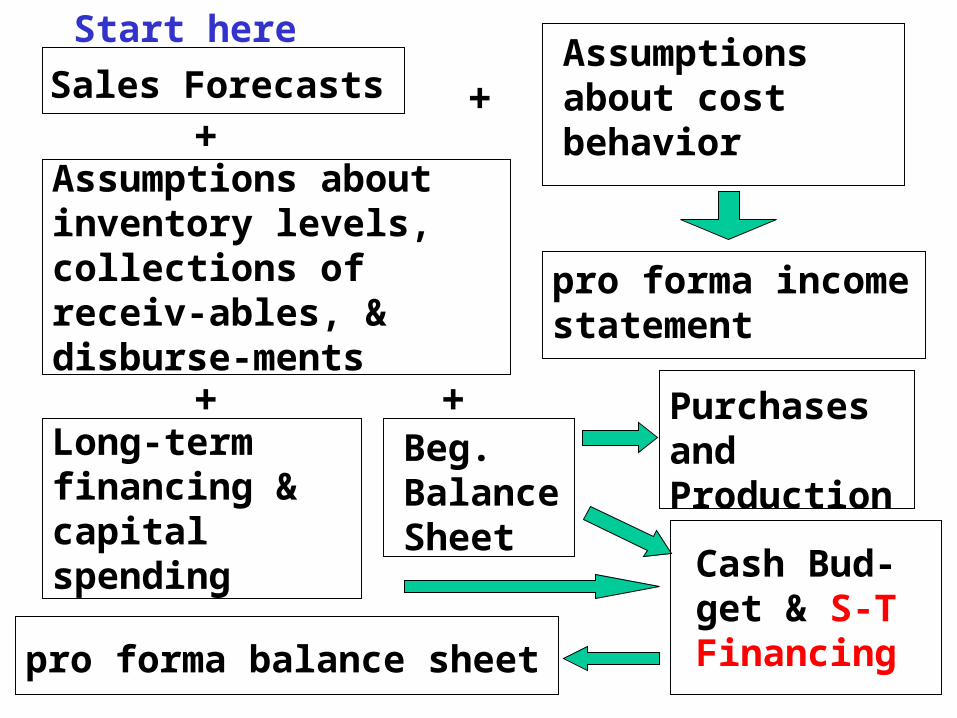

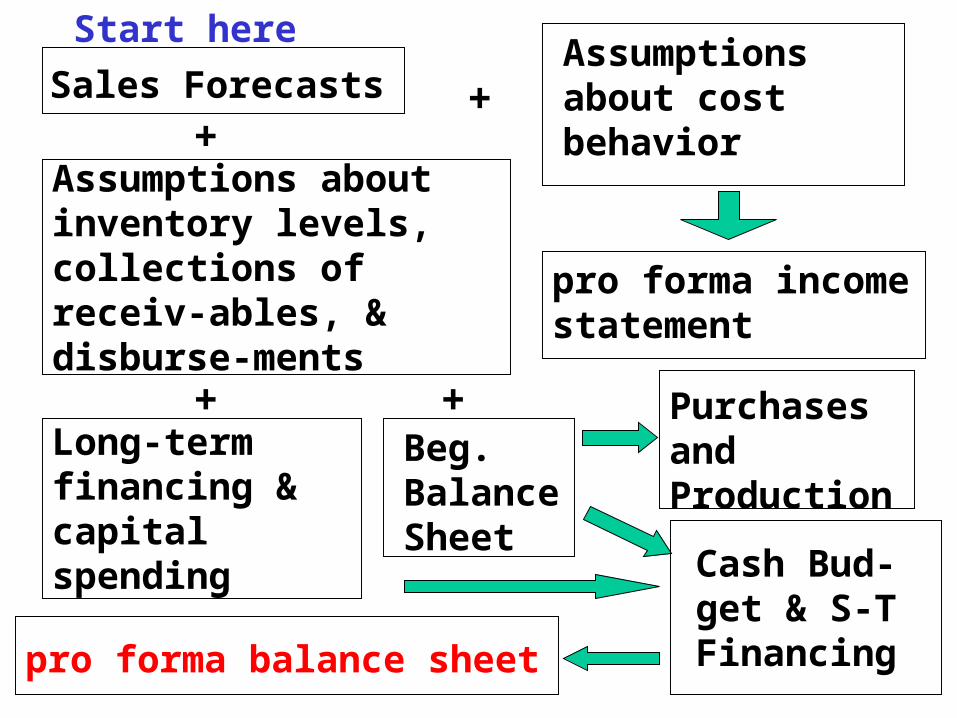

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

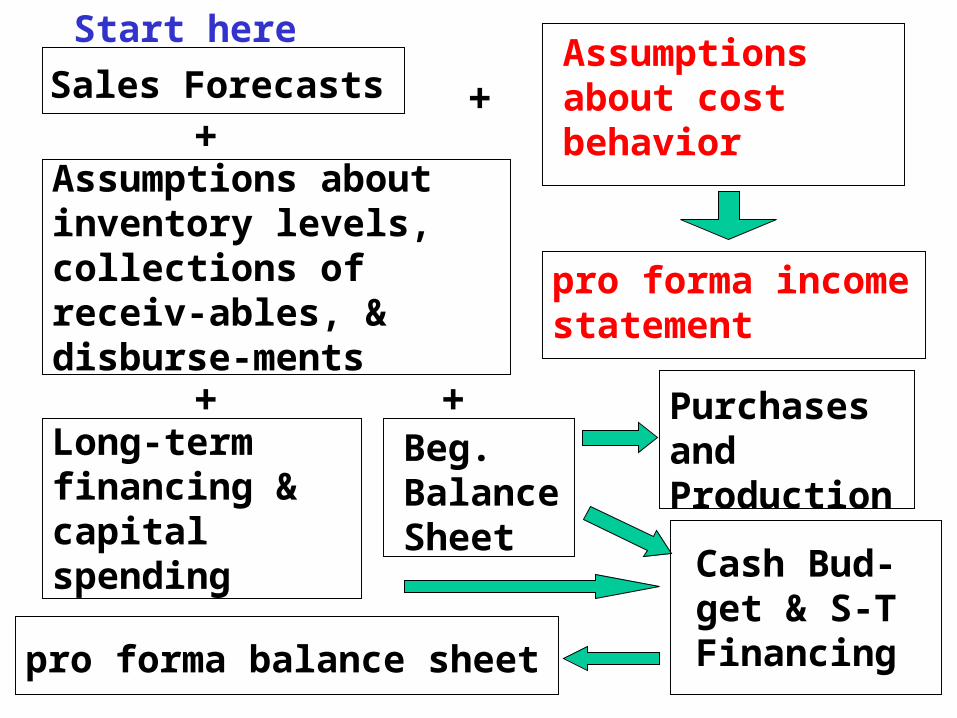

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

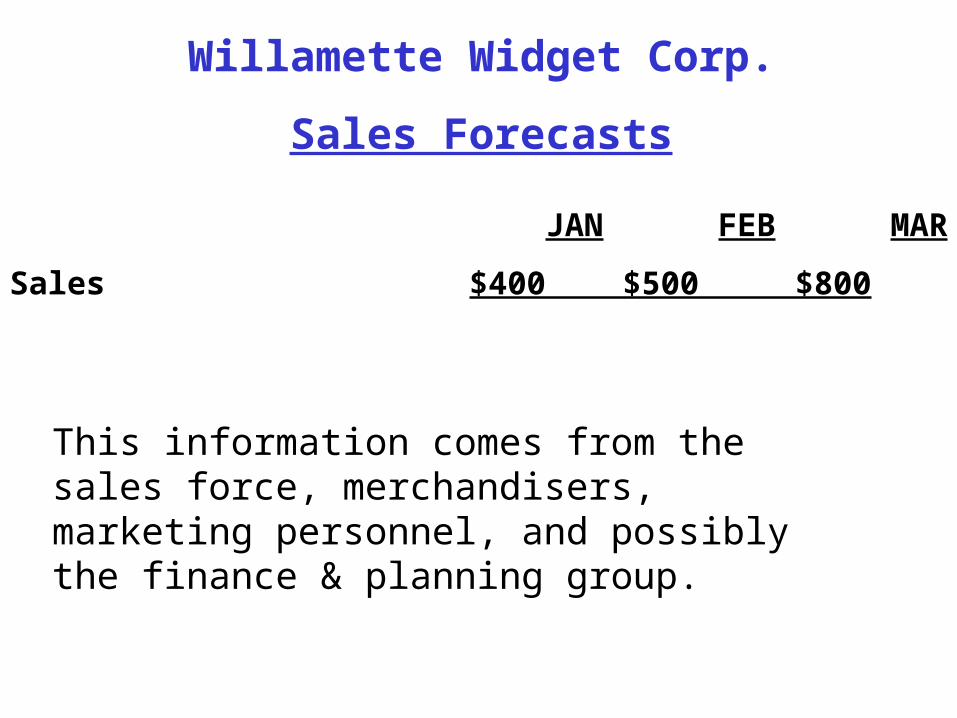

Willamette Widget Corp.

Sales Forecasts

JAN FEB MAR

Sales $400 $500 $800

This information comes from the sales force, merchandisers, marketing personnel, and possibly the finance & planning group.

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

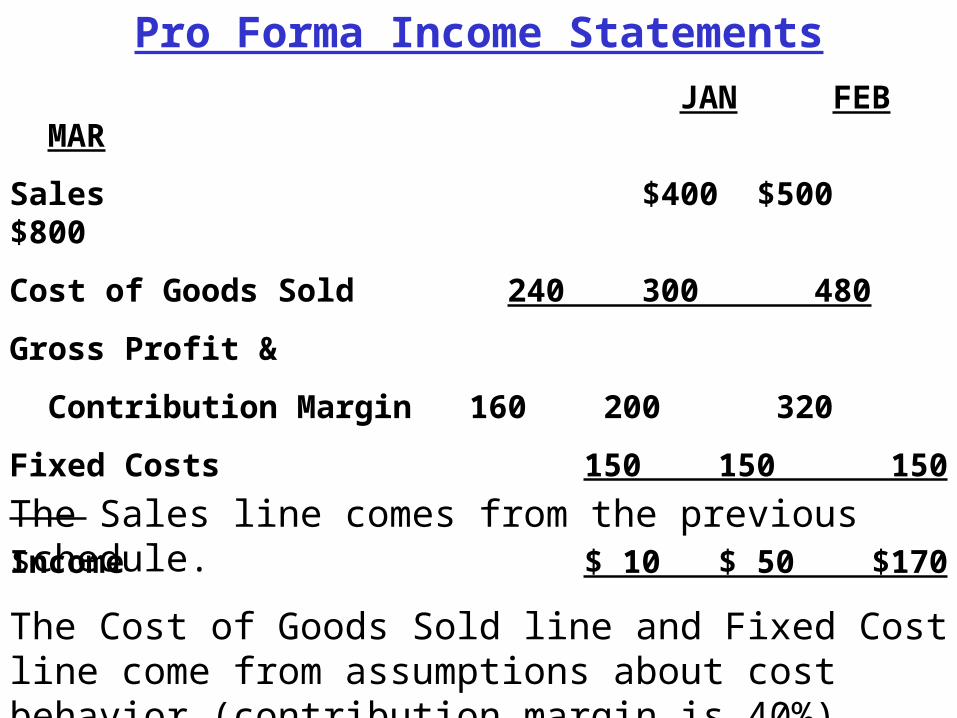

Pro Forma Income Statements JAN FEB MAR

Sales $400 $500 $800

Cost of Goods Sold 240 300 480

Gross Profit &

Contribution Margin 160 200 320

Fixed Costs 150 150 150

Income $ 10 $ 50 $170

The Sales line comes from the previous schedule.

The Cost of Goods Sold line and Fixed Cost line come from assumptions about cost behavior (contribution margin is 40%).

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

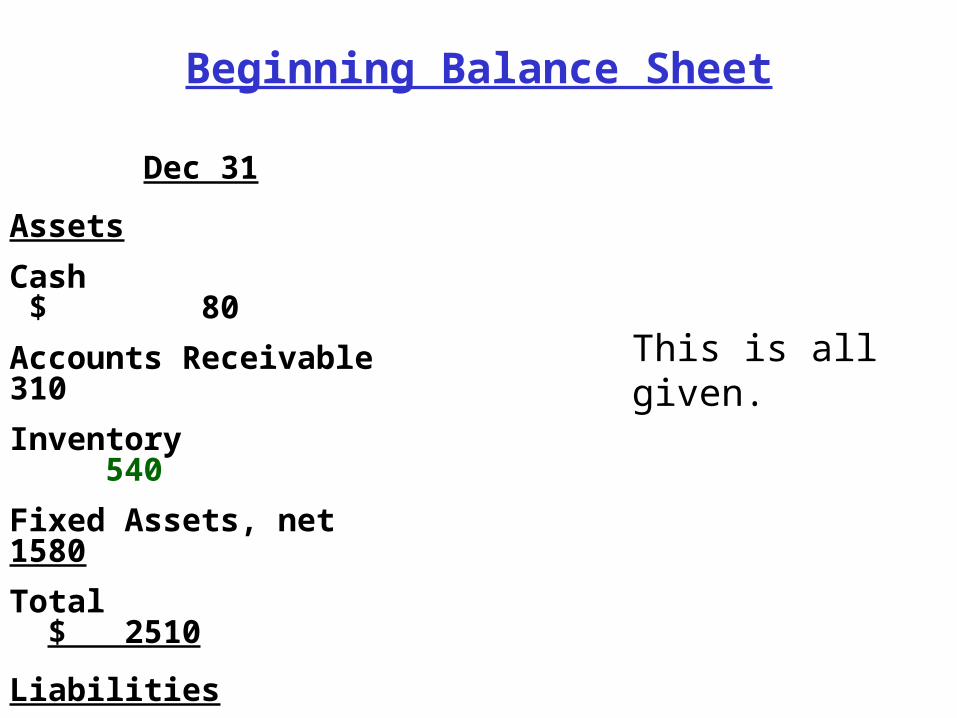

Beginning Balance Sheet Dec 31

Assets

Cash $ 80

Accounts Receivable 310

Inventory 540

Fixed Assets, net 1580

Total $ 2510

Liabilities

Accounts Payable $ 195

Stockholders’ Equity 2315

Total $ 2510

This is all given.

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

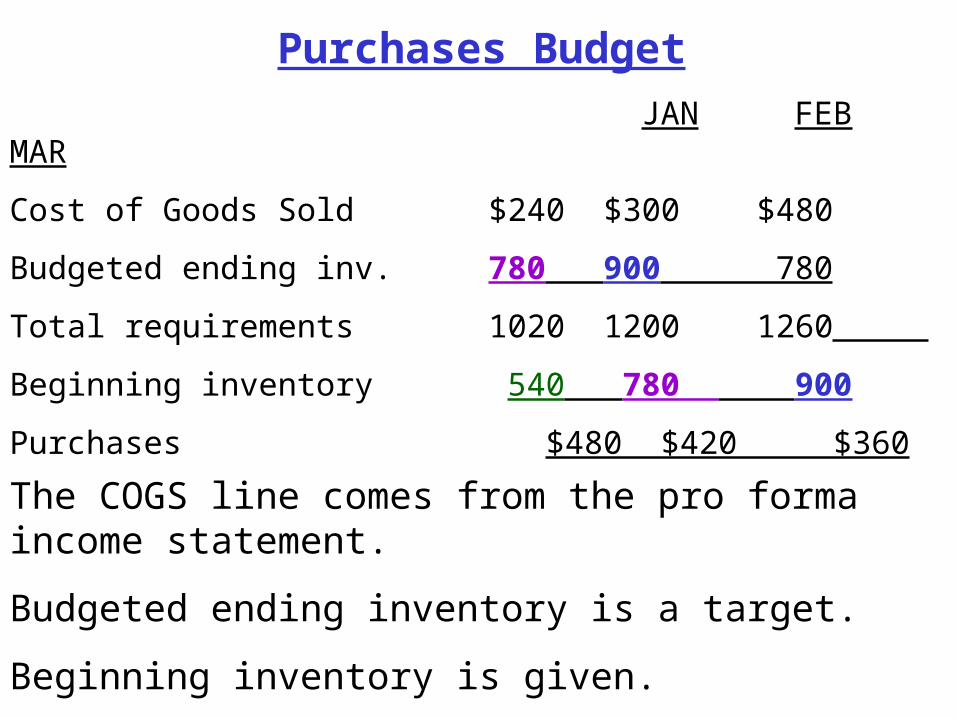

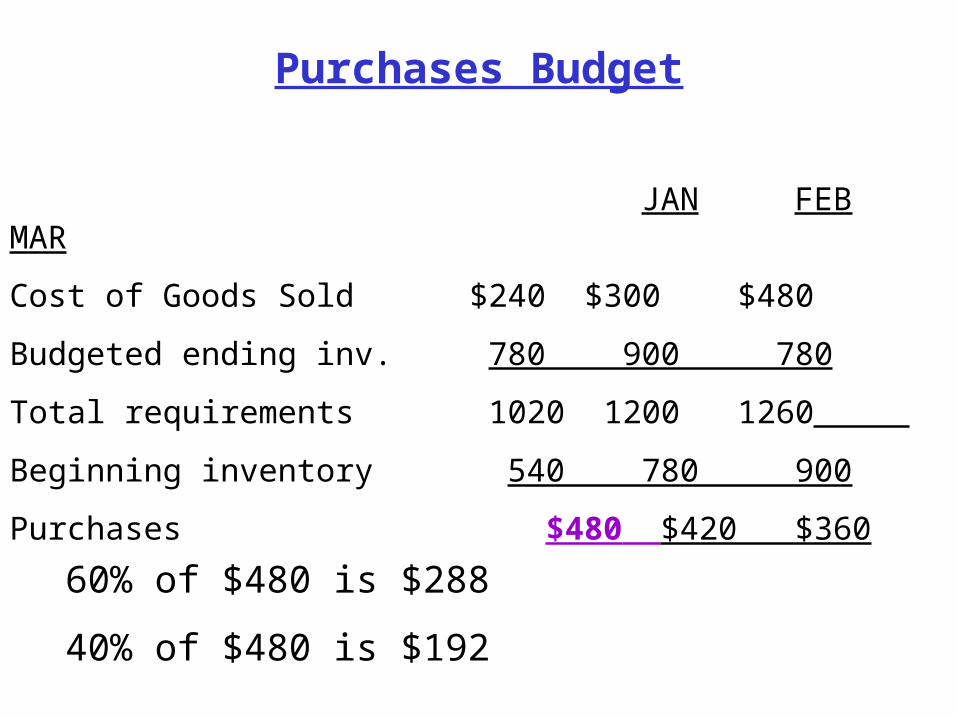

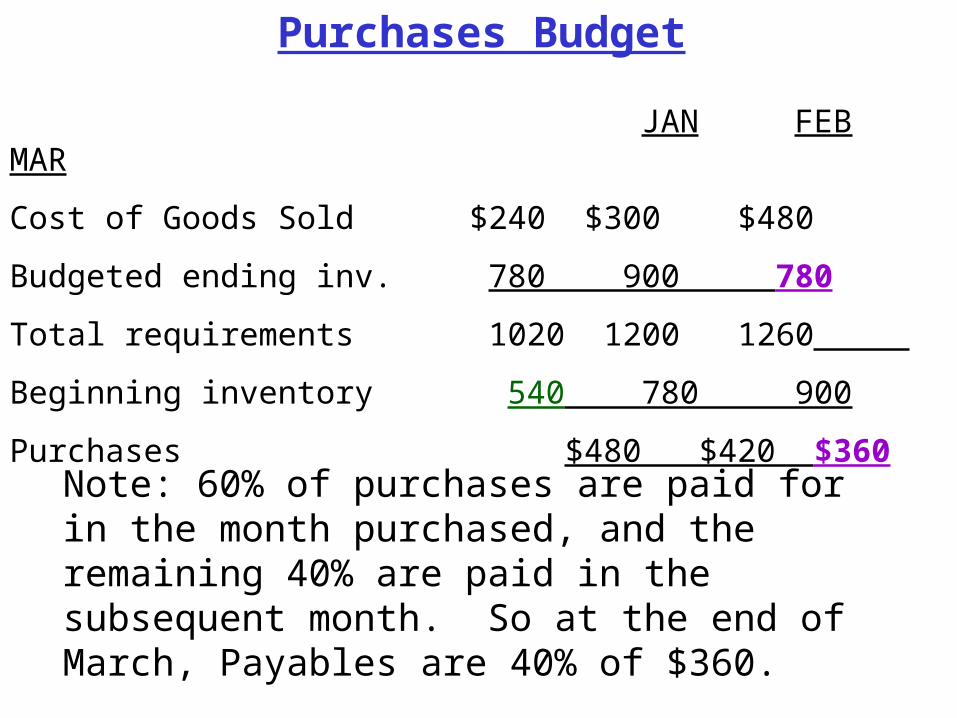

Purchases Budget JAN FEB MAR

Cost of Goods Sold $240 $300 $480

Budgeted ending inv. 780 900 780

Total requirements 1020 1200 1260

Beginning inventory 540 780 900

Purchases $480 $420 $360

The COGS line comes from the pro forma income statement.

Budgeted ending inventory is a target.

Beginning inventory is given.

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

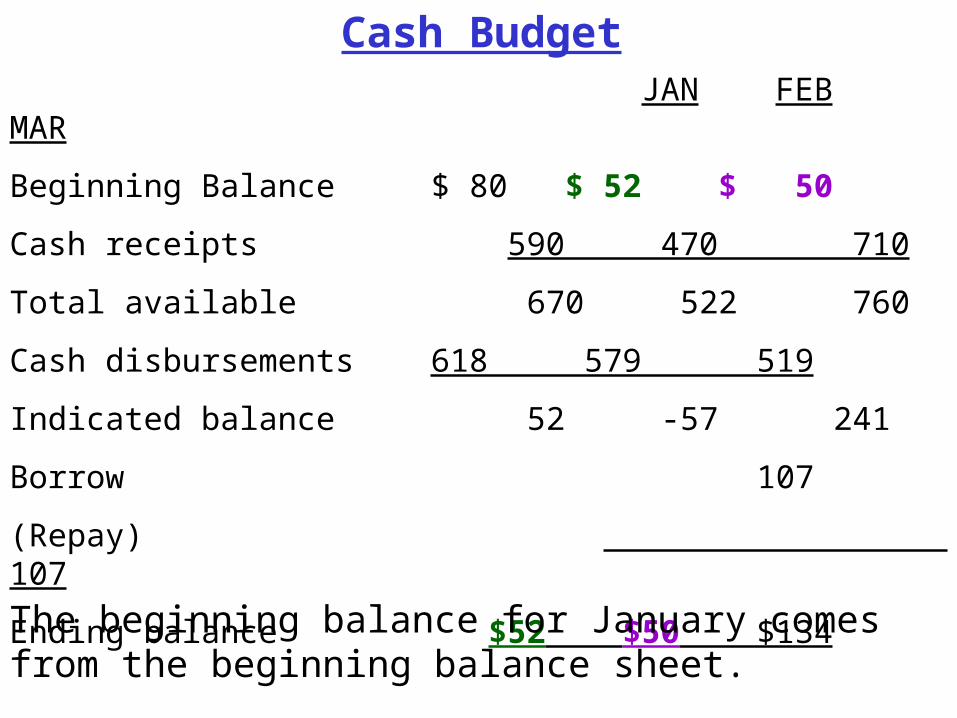

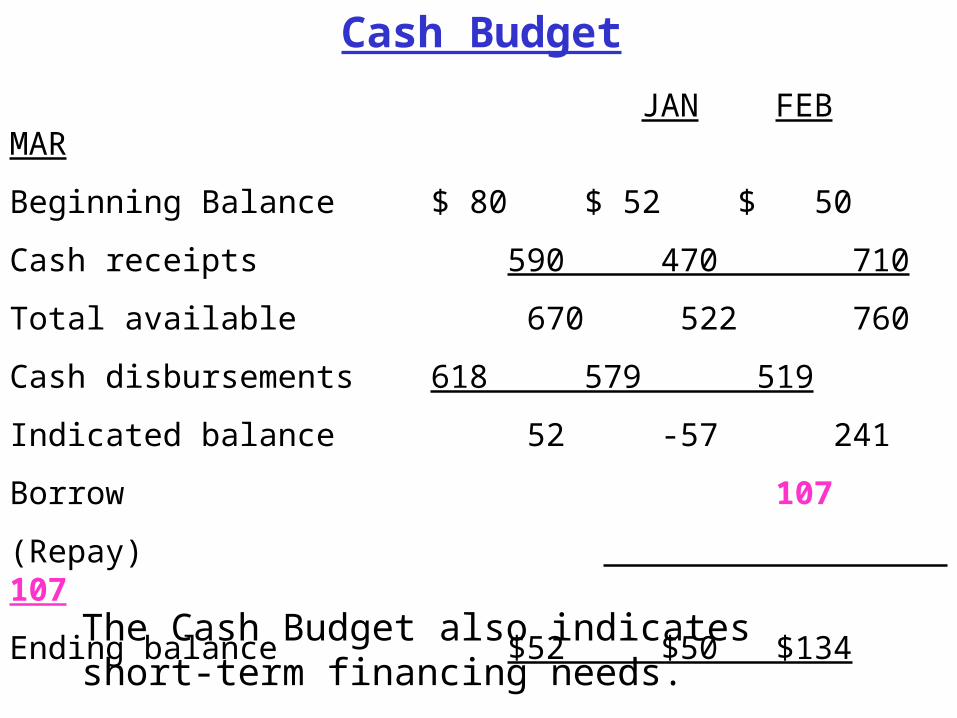

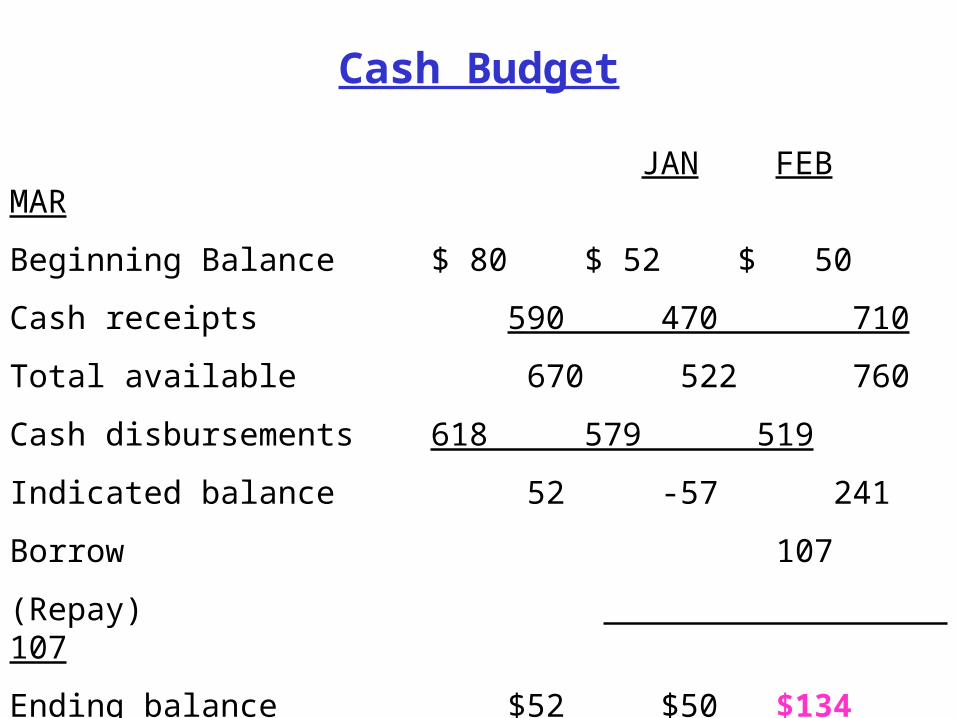

Cash Budget JAN FEB MAR

Beginning Balance $ 80 $ 52 $ 50

Cash receipts 590 470 710

Total available 670 522 760

Cash disbursements 618 579 519

Indicated balance 52 -57 241

Borrow 107

(Repay) 107

Ending balance $52 $50 $134

The beginning balance for January comes from the beginning balance sheet.

Cash Budget

JAN FEB MAR

Beginning Balance $ 80 $ 52 $ 50

Cash receipts 590 470 710

Total available 670 522 760

Cash disbursements 618 579 519

Indicated balance 52 -57 241

Borrow 107

(Repay) 107

Ending balance $52 $50 $134

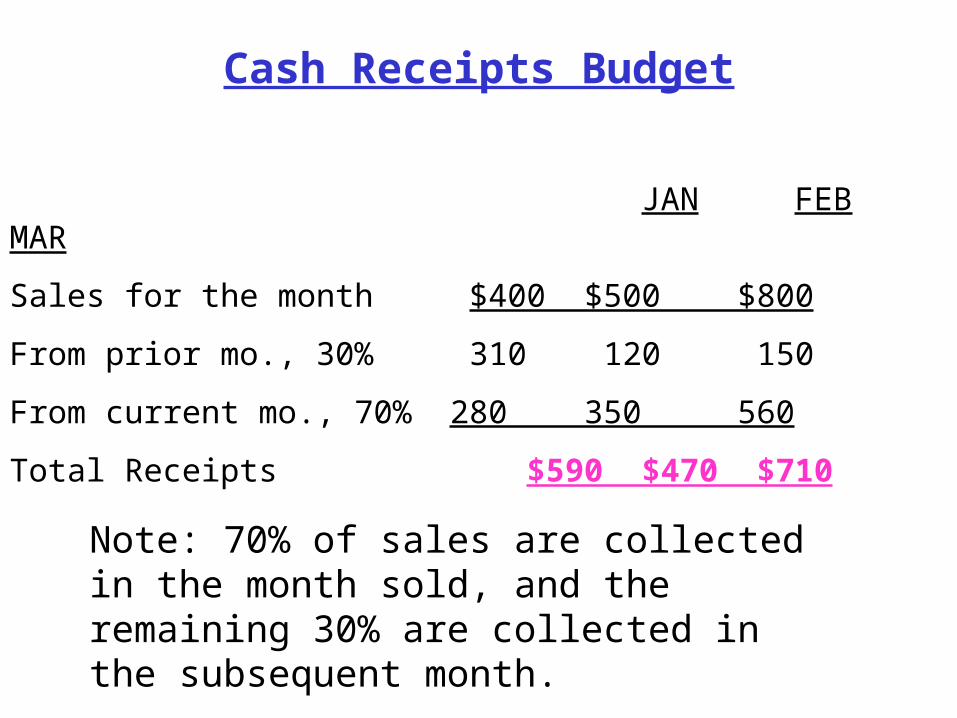

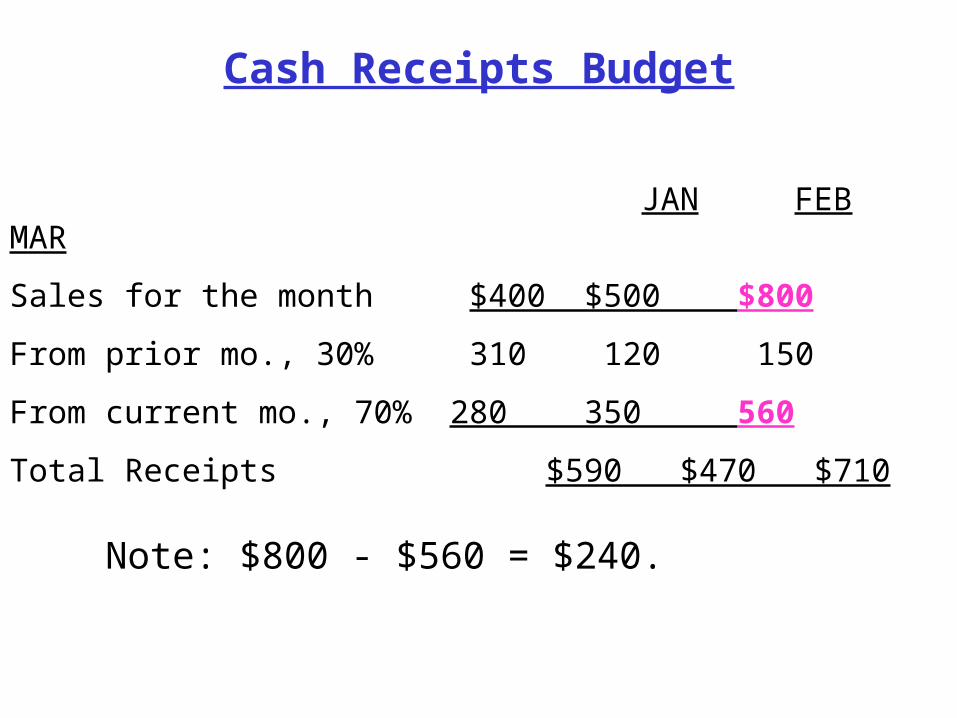

Cash Receipts Budget

JAN FEB MAR

Sales for the month $400 $500 $800

From prior mo., 30% 310 120 150

From current mo., 70% 280 350 560

Total Receipts $590 $470 $710

Note: 70% of sales are collected in the month sold, and the remaining 30% are collected in the subsequent month.

Cash Budget

JAN FEB MAR

Beginning Balance $ 80 $ 52 $ 50

Cash receipts 590 470 710

Total available 670 522 760

Cash disbursements 618 579 519

Indicated balance 52 -57 241

Borrow 107

(Repay) 107

Ending balance $52 $50 $134

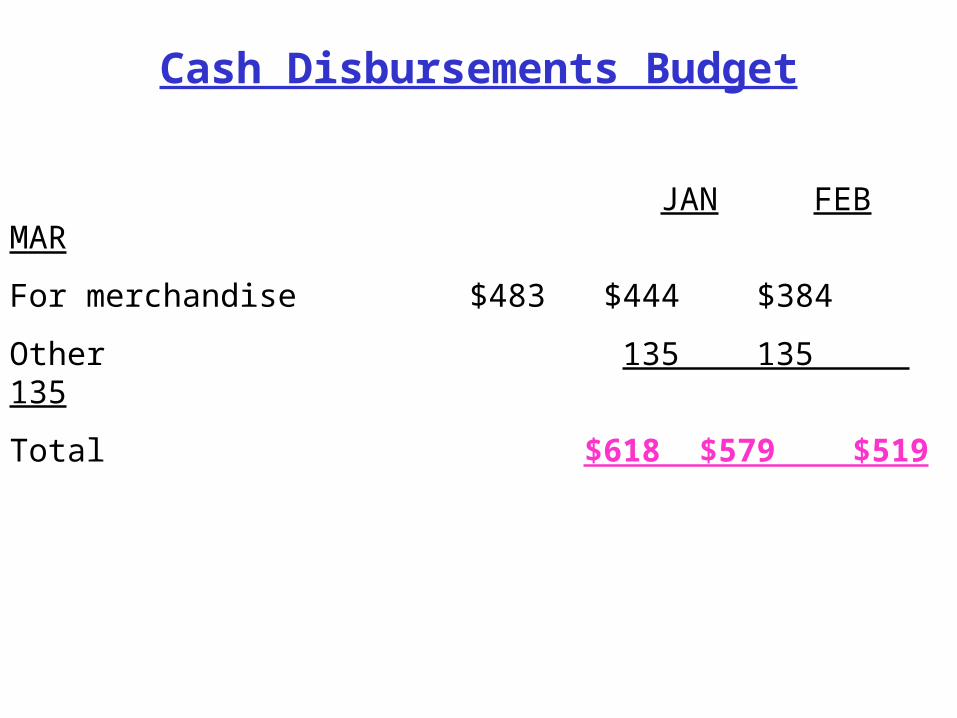

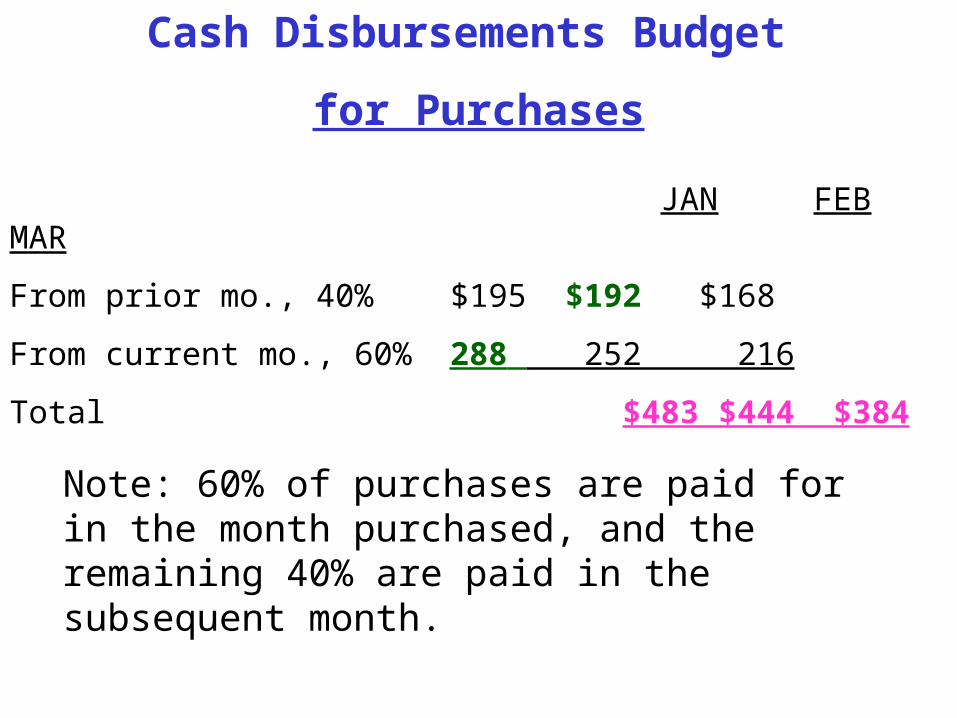

Cash Disbursements Budget

JAN FEB MAR

For merchandise $483 $444 $384

Other 135 135 135

Total $618 $579 $519

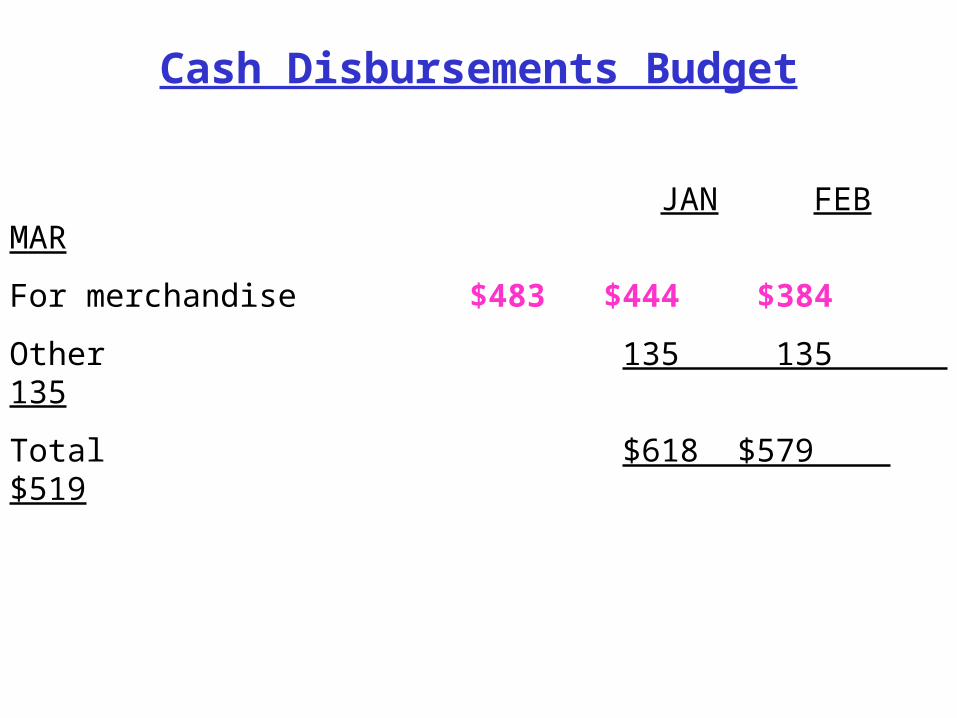

Cash Disbursements Budget

JAN FEB MAR

For merchandise $483 $444 $384

Other 135 135 135

Total $618 $579 $519

Cash Disbursements Budget

for Purchases

JAN FEB MAR

From prior mo., 40% $195 $192 $168

From current mo., 60% 288 252 216

Total $483 $444 $384

Note: 60% of purchases are paid for in the month purchased, and the remaining 40% are paid in the subsequent month.

Purchases Budget

JAN FEB MAR

Cost of Goods Sold $240 $300 $480

Budgeted ending inv. 780 900 780

Total requirements 1020 1200 1260

Beginning inventory 540 780 900

Purchases $480 $420 $360

60% of $480 is $288

40% of $480 is $192

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

Cash Budget

JAN FEB MAR

Beginning Balance $ 80 $ 52 $ 50

Cash receipts 590 470 710

Total available 670 522 760

Cash disbursements 618 579 519

Indicated balance 52 -57 241

Borrow 107

(Repay) 107

Ending balance $52 $50 $134

The Cash Budget also indicates short-term financing needs.

Sales Forecasts+

+

++

Assumptions about cost behavior

pro forma income statement

Assumptions about inventory levels, collections of receiv-ables, & disburse-ments

Long-term financing & capital spending

Beg. Balance Sheet

Cash Bud-get & S-T Financing

Purchases and Production

pro forma balance sheet

Start here

Pro Forma Balance Sheet March 31

Assets

Cash $ 134

Accounts Receivable 240

Inventory 780

Fixed Assets, net 1535

Total $ 2689

Liabilities

Accounts Payable $ 144

Stockholders’ Equity 2545

Total $ 2689

Cash comes from the Cash Budget.

A/R is 30% of March sales.

Inventory is from Purchases Budget.

A/P is 40% of March purchases.

Cash Budget

JAN FEB MAR

Beginning Balance $ 80 $ 52 $ 50

Cash receipts 590 470 710

Total available 670 522 760

Cash disbursements 618 579 519

Indicated balance 52 -57 241

Borrow 107

(Repay) 107

Ending balance $52 $50 $134

Cash Receipts Budget

JAN FEB MAR

Sales for the month $400 $500 $800

From prior mo., 30% 310 120 150

From current mo., 70% 280 350 560

Total Receipts $590 $470 $710

Note: $800 - $560 = $240.

Purchases Budget

JAN FEB MAR

Cost of Goods Sold $240 $300 $480

Budgeted ending inv. 780 900 780

Total requirements 1020 1200 1260

Beginning inventory 540 780 900

Purchases $480 $420 $360

Note: 60% of purchases are paid for in the month purchased, and the remaining 40% are paid in the subsequent month. So at the end of March, Payables are 40% of $360.

• Operational Budgeting

• Operational Budgeting Exercises

ACTG 321Agenda for Lecture 15

1. K-Mart expects sales of $100,000 in April, $145,000 in May and $250,000 in June. Sales are collected 30% in the month of sale with the remainder collected the month after sale. What will accounts receivable be on May 31?

1. K-Mart expects sales of $100,000 in April, $145,000 in May and $250,000 in June. Sales are collected 30% in the month of sale with the remainder collected the month after sale. What will accounts receivable be on May 31?

70% of $145,000 = $101,500

2. Sam’s Club expects to make purchases of $100,000 in April; $240,000 in May; $350,000 in June; and $230,000 in July. Purchases are paid 30% in the month of purchase and 70% in the month after purchase. What would accounts payable be at the end of May?

2. Sam’s Club expects to make purchases of $100,000 in April; $240,000 in May; $350,000 in June; and $230,000 in July. Purchases are paid 30% in the month of purchase and 70% in the month after purchase. What would accounts payable be at the end of May?

70% of $240,000 = $168,000

3. Costco expects sales of $100,000 in January, $150,000 in February, $180,000 in March, and $200,000 in April. Cost of Sales is 70% of sales. Ending inventory is expected to equal 40% of the next month's unit sales. How much inventory would be purchased in March?

3. Costco expects sales of $100,000 in January, $150,000 in February, $180,000 in March, and $200,000 in April. Cost of Sales is 70% of sales. Ending inventory is expected to equal 40% of the next month's unit sales. How much inventory would be purchased in March?

In March Costco would purchase 60% of March cost-of-sales and 40% of April cost-of-sales.

(60% of $180,000 x .7)+(40% of $200,000 x .7)

= $75,600 + $56,000

= $131,600

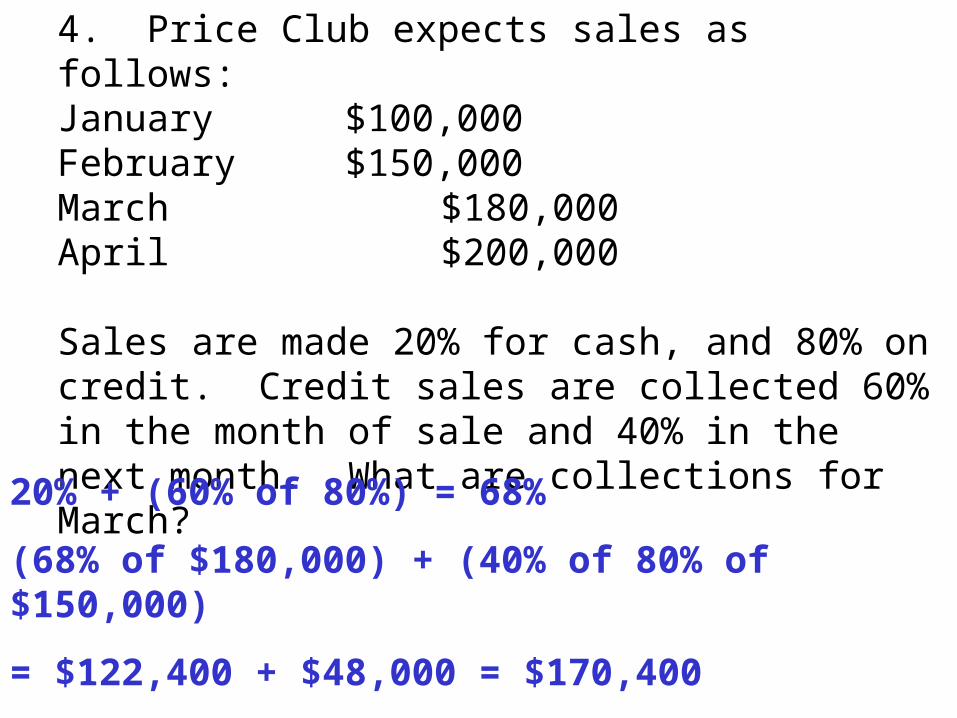

4. Price Club expects sales as follows:

January $100,000February $150,000March $180,000April $200,000

Sales are made 20% for cash, and 80% on credit. Credit sales are collected 60% in the month of sale and 40% in the next month. What are collections for March?

4. Price Club expects sales as follows:January $100,000February $150,000March $180,000April $200,000

Sales are made 20% for cash, and 80% on credit. Credit sales are collected 60% in the month of sale and 40% in the next month. What are collections for March?

20% + (60% of 80%) = 68%

(68% of $180,000) + (40% of 80% of $150,000)

= $122,400 + $48,000 = $170,400

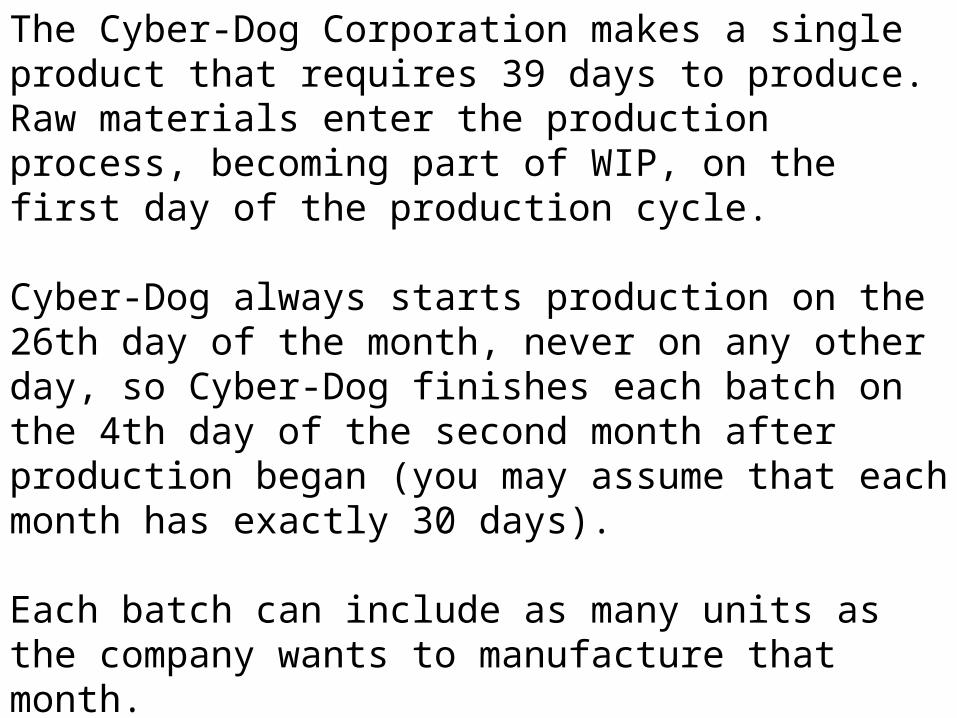

The Cyber-Dog Corporation makes a single product that requires 39 days to produce. Raw materials enter the production process, becoming part of WIP, on the first day of the production cycle.

Cyber-Dog always starts production on the 26th day of the month, never on any other day, so Cyber-Dog finishes each batch on the 4th day of the second month after production began (you may assume that each month has exactly 30 days).

Each batch can include as many units as the company wants to manufacture that month.

Cyber-Dog expects sales of 1,000 units in January, and expects sales to increase by 100 units each month for the indefinite future (i.e., 1,100 units in February, 1,200 units in March, etc.). Cyber-Dog wants 60% of each month’s sales on hand as finished goods at the beginning of the month.

Each unit requires 7 lbs of raw materials. Cyber-Dog wants 130% of each month’s raw materials requirements on hand at the beginning of the month.

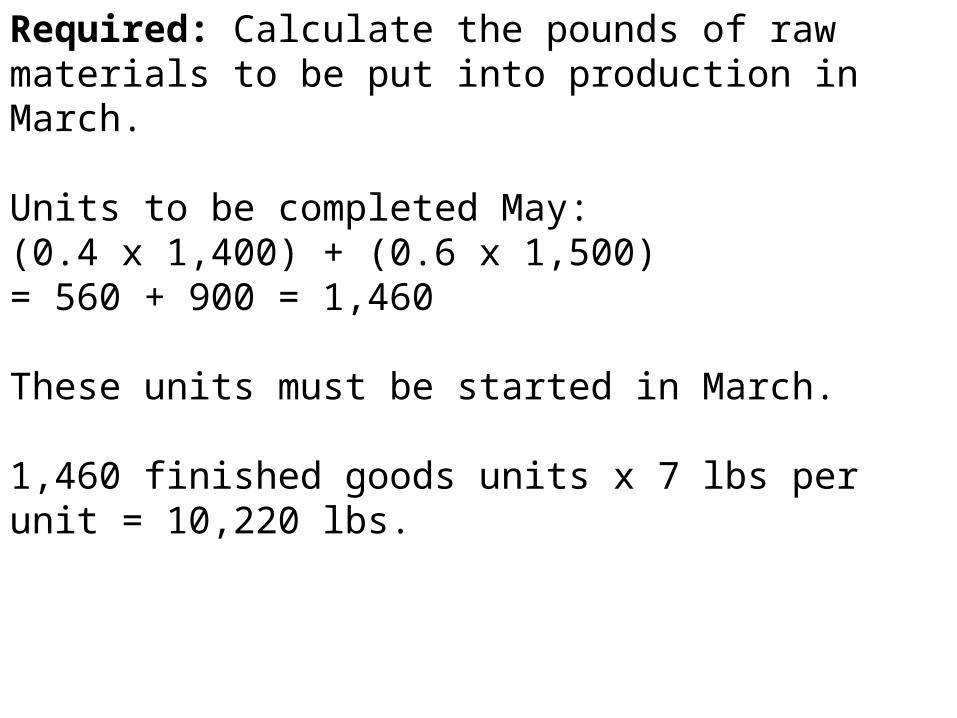

Required: Calculate the pounds of raw materials to be put into production in March.

Required: Calculate the pounds of raw materials to be put into production in March.

Units to be completed May: (0.4 x 1,400) + (0.6 x 1,500) = 560 + 900 = 1,460

These units must be started in March.

1,460 finished goods units x 7 lbs per unit = 10,220 lbs.

![CPA PREP 2013 - 2015 - ONCAT | CATON - Home prep 2013-15.pdfM1 ACTG 1P11 & ACTG 1P12 M7 ACTG 3P11 M2 ACTG 1P11 & ACTG 1P12 M8 [ACTG 3P41 & ACTG 4P41 & ACTG 4P42] or ACTG 4P40 (see](https://static.fdocuments.in/doc/165x107/5af6e4407f8b9a4d4d910972/cpa-prep-2013-2015-oncat-caton-prep-2013-15pdfm1-actg-1p11-actg-1p12-m7.jpg)