Pragmatic Insurance Option Pricing - International Actuarial

Upload

noel-francisCategory

view

236download

2

Operational and Actuarial Aspects of TakafulProduct Design and Pricing

(I) THE APPLICATION OF SHARIAH PRINCIPLES IN PRODUCT DESIGN

Actuaries in designing takaful products, need to be at least aware of the core principles which embody the shariah. The spriritual basis of the shariah is grounded in the shariah realizes benefits (maslahah) to mankind as a manifestation of that mercy;

This principle of realizing benefit to the individual and the Community is a fundamental value which runs throughout the entire shariah. The benefits which the shariah sets out to achieve are graded in three categories in a descending order of importance, i.e.,:

Daruriyyat masalih (essential);Hajiyyat masalih (Complementary);Tahsiniyyat masalih (embellishment);

2

A shariah complaint product like takaful should embody the same objectives as the Shariah itself. For example, the essential objectives of the Shariah are five such as:

Preservation of Faith

Preservation of Life

Preservation of Lineage

Preservation of Intellect and

Preservation of Property

The five essential objectives are essential to normal order in society and the neglect of it will lead to chaos and the

collapse of normal order in society;

Therefore, in coming up with new product , the consideration of a proposed product idea under the Shariah is a vital step, e.g., takaful product offering abortion benefits;

3

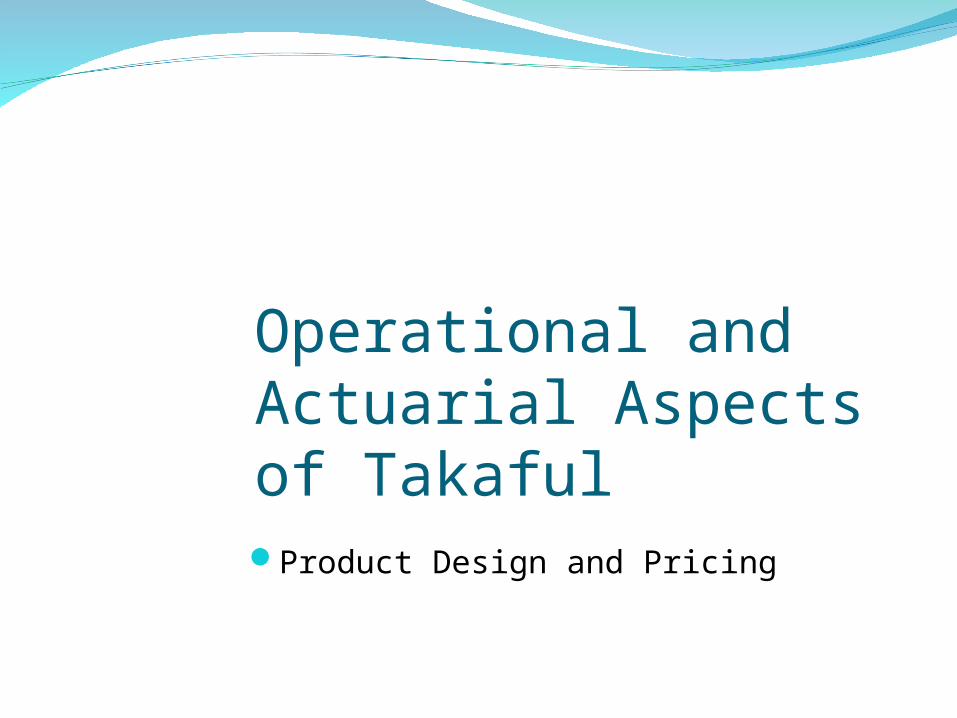

(II) MARKET IDEA SCREENING In a typical product development process, there will usually be the

following steps:

Product Development Process

4

Idea GenerationIdea Generation

Idea ScreeningIdea Screening

Product Product DevelopmentDevelopment

Shariah Advisory Shariah Advisory BoardBoard

Product Product Launch/Roll OutLaunch/Roll Out

Modify ProductModify Product

Compared to tangible products, takaful are legal contracts, therefore, contracts such as this will be viewed both by the Shariah Board as well as the court system; takaful contracts deal with risks which are ‘ long tail’ in nature;

The management of takaful operator therefore needs to carefully evaluate risks that the takaful fund will be exposed when the new product usually involves the underwriting, claims and actuarial departments.

The risk analysis will include;

Is the risk controllable Is the risk something that can be forecasted? Is the risk something the management can handle?

5

When new products could expose the takaful fund to high coverage amount, management needs to take precautionary measures through appropriate wording of contract terms and/ or risk management measures such as underwriting and takaful arrangements. Management should also need to evaluate the attractiveness of such plans in terms of profit potential and contribution volumes as opposed to cost (use of expertise, use of new systems to manage new product)

The takaful operator also needs to evaluate product viability from the perspective of safeguarding the solvency of the takaful fund; even though the operator is not guaranteeing the benefits, its acts as a fiduciary acting in the best interests of the participants; takaful products should not be launched which serve to maximize takaful operator profit at the expense of endangering the solvency of the takaful fund;

6

The actuary’s role in providing financial numbers reflecting market potential and risk exposures is valuable to a management wishing to objectively screen and identify products exhibiting the best return to both participants and shareholders alike.

7

(III) PRODUCT COMPLIANCE WITH SHARIAH / REGULATORY GUIDELINES

In compliance to shariah and the regulatory requirements, checks will be carried out at several points in the pathway from idea generation to product roll-out.

These checks include:

Preliminary checking on product concept;Once approved development of product may progress;Once product details and contract wordings are ready, submit it

to Shariah Advisory Board for approval; If not approved, products need to be amended;

Full disclosure and transparency of product features includes point of sale material and marketing brochures;

8

At the same time similar checks to meet regulatory requirements is also being made and this includes:

Preliminary submission of proposed contract wordings;

Marketing literature;

Benefit structure;

Contribution rates;

9

(IV) TYPICAL TAKAFUL PRODUCT DESIGN FEATURESThe product features would include:

Contingencies covered;Supplementary benefits covered;Wording of takaful contract;Profit sharing arrangement;Expense / benefit structure;Degree of risk assessment;Cancellation / Extension / Renewal features;Benefit Limitations / Exclusions;

(a) Contingencies Covered

For family takaful business, the main contingencies covered are risk of death, disability and other related contingencies such as diagnosis of critical illness, hospitalization;

10

For general takaful business, the contingencies are many and varied;

House owner Takaful – Physical damage to building and contents, due to fire, explosion, theft;

Comprehensive Motor Takaful – Physical damage to car as well as liability to third parties;

Personal Accident Takaful – Contingencies covered death, disability or minor bodily injury as well as hospitalization

expense;

Medical Takaful – Hospitalization expense due to any cause;

Marine cargo takaful – Financial loss arising from loss or damage of goods, stock or equipment while in transit;

11

(b) Supplementary Benefits

These are extra benefits added on the basic core benefit of the plan; it do not come free ; it would require extra contribution;

For example, medical takaful plan provides emergency and evaluation services; hospitalization and disability coverage to a basic family takaful benefit

It is optional in nature;

Coverage endorsement in general takaful contracts may be considered the general takaful equivalent of supplementary benefits in family takaful.

12

Wording of Takaful Contract

The nature of contract wording could be “tight” or “loose” in relation to other similar coverage products in the marketplace;

The following are examples of the wording of a Total and Permanent Disability (TPD) coverage under two separate contract;

(1) “Total and Permanent Disability (TPD) is disability such that the participant is unable, at the time the disability commences or at anytime thereafter to engage in occupation for wages, compensation or profit provided however at such disability must last for a continuous period of not less than six (6) months.

13

(2) “Total and Permanent Disability (TPD) is disability such that the participant is unable, at the time the disability commences or at anytime thereafter to engage in his or her own occupation provided however that such disability must last for a continuous period of not less than six (6) months”.

The first definition might require the participant to be practically bedridden in order to qualify; this definition would be considered “tight” ; number of disability cases would be narrowed down to just a few very severe disability cases; thus probability of paying disability benefits would be lower and hence risk contribution should be lower;

Under the second definition, the like hood of a participant qualifying for such a benefit would be much higher as even mild forms of disability may tender the participant incapable of engaging his or her own occupation.

Comparing the two above definition, it would be reasonable to expect a takaful contract covering TPD benefits under the ‘any occupation/ definition would require a lesser contribution compared to that of ‘own occupation’;

14

(d) Nature of Profit Sharing Arrangement;

In many cases, the takaful contract may permit sharing of investment profit and underwriting surplus;

Issue of sharing of underwriting surplus is still a moot point for many Shariah scholars; many operators especially in South East Asia have introduced products; which prominently features surplus sharing as a key feature of product design; sharing of investment profit and underwriting surplus with participants is done regardless of the operational model;

The ratio for the investment profit between operator and participants could be say 50:50 or 70:30 or any other ratios agreed.

The underwriting surplus would similarly be split on some pre-agreed ratio spelt out in the contract; the challenge to the actuary in this instance is first to determine the emergence of underwriting surplus and to determine its allocations;

15

(e) Expense / Benefit Structure

The way benefits are structured are left to the imagination and creativity of takaful operators so as to market products competitively; the actuary’s role is to make sure that benefits are structured fairly to participants, economically viable and operationally feasible;

There is no fixed way in which provisions for expenses are reflected in the pricing of the product; in a mudharabah model, operators expenses are recovered from direct charges to the takaful fund or from operators share of investments profit and underwriting surplus; in a wakalah model, an explicit fee will be used to recover operator expenses;

The variations in allocating and charging expenses to the participant / takaful funds are many and really depend on the operator:

16

Charge upfront wakalah fee for commission and management costs;

All management expenses are absorbed by the takaful operator;Commission and management expenses are borne by takaful fund

on an incurred basis;Upfront wakalah fee as percentage of tabarru’ charges;

Regardless of the underlying operational model, the anticipated expenses of marketing and operation is reflected in the product pricing process either directly in the form of an explicit expense margin or provision embedded in the contribution formula or implicitly in the cash flow tests carried out to assess the financial viability or profitability of a particular takaful product.

Expenses generally consists of:

(i) Variable costs – marketing costs, agency commissions

underwriting expense;

(ii) Fixed costs – fixed asset depreciation, staff salaries, overheads;17

In assessing financial viability of the product from operators perspective is the speed and magnitude the operators expenses and other sunk costs are recovered over time;

Tests of acceptable profitability (profit tests) to the operator as well as solvency within takaful fund are carried out by the actuary using cash flow models which are simplified representative s of the takaful fund over time;

In coming suitable contribution rates for a new product, the actuary need reliable data which would indicate the operators existing and projected costs of operating the business.

18

(f) Degree of Risk Assessment

In maintaining the principle of fairness, participants need to be assessed for the degree of risk that is potentially brought into risk pool through the process of risk assessment or risk underwriting;

It is fair and logical to expect that the lesser risks that a covered participant or asset brings into the risks fund the lower the contribution rate should be; likewise participants bringing in higher risks should be charged a higher takaful contribution;

A takaful product may be differentiated from the competition by simply either;

Having more extensive risk selection;

(low contribution for those who qualify)Reduced risk selection (simplified underwriting)

19

Example of case 1: Participant are charged super low contribution if he undergo and passed medical tests

beginning of each year (say 5 years);

Example of case 2: Issuance to a family plan made immediately upon answer 3 or 5 questions on the state of

health of the participant;

(g) Cancellation / Renewal Features

Many short duration products (medical plans) issued on an annual renewable basis would be subject to fresh risk selection; in such cases, operator may typically reserve the right to decline renewals or subject the renewal to an increase in contribution.

20

Non renewal of contracts is effectively a cancellation of coverage; hence, the value of continuity of coverage may be very valuable to a participants who suffers deteriorating health; thus, continuity of coverage may be a feature which can be used to advantage by operators; to fill such needs, medical takaful plans may for example be issued which offer guaranteed renewability of coverage up to some maximum age (e.g., 65 or 70 years)

From a product pricing perspective, care needs to be taken in pricing such guaranteed renewable plans; healthy participants would be more likely to drop out, leaving the takaful fund inhabited by not so healthy participants; this phenomenon is known as cumulative anti-selection;

21

(V) FULFILMENT OF PARTICIPANTS REASONABLE EXPECTATIONS (PRE)

Be an intangible product participants should be clear as to what they are entitled to under the contract should misfortune strike;

In conventional insurance, a concept in ethical business practice has developed of meeting the reasonable expectations of a participant known as PRE; therefore by virtue being Shariah complaint, takaful operator meeting the PRE requirement is already an in-built mechanism;

As such, contract documentation and especially marketing literature has to be clear so as to what the participant can reasonably expect in benefits from the takaful fund should the participant submit a claim.

22

The operators task in meeting expectation is two fold:

Firstly , the takaful operator needs to ensure that the pricing and design of takaful products is done on a basis that anticipates fulfillment of the product promise under all reasonable scenarios.

Secondly, care needs to be taken in marketing the product so that participant expectations are properly managed. Participant expectations are very much influenced by the actions of personnel marketing takaful products and the literature made available to participants.

23

(VI) THE ESSENTIALS OF PRODUCT PRICING(a) IntroductionProduct costs should not just reflect the ‘raw material’ cost of the risk

exposures to be covered in the contract but consideration of everything else that goes with the product. The various factors that need to be considered include:The risk contribution required to cover actual risk exposure only;Marketing expenses;Opportunity cost of capital needed to be retained in the takaful fund to

support the risks covered in the proposed product;Profit expectations of takaful operator;Retakaful expenses;Anticipated investment profit rate of return to be earned from

investment of takaful fund assets;

The last factor is especially important for long term takaful contracts; it will effect the takaful contribution amount due to the greater effect the opportunity cost of capital will have on evaluating cash flows a long time horizon.

l24

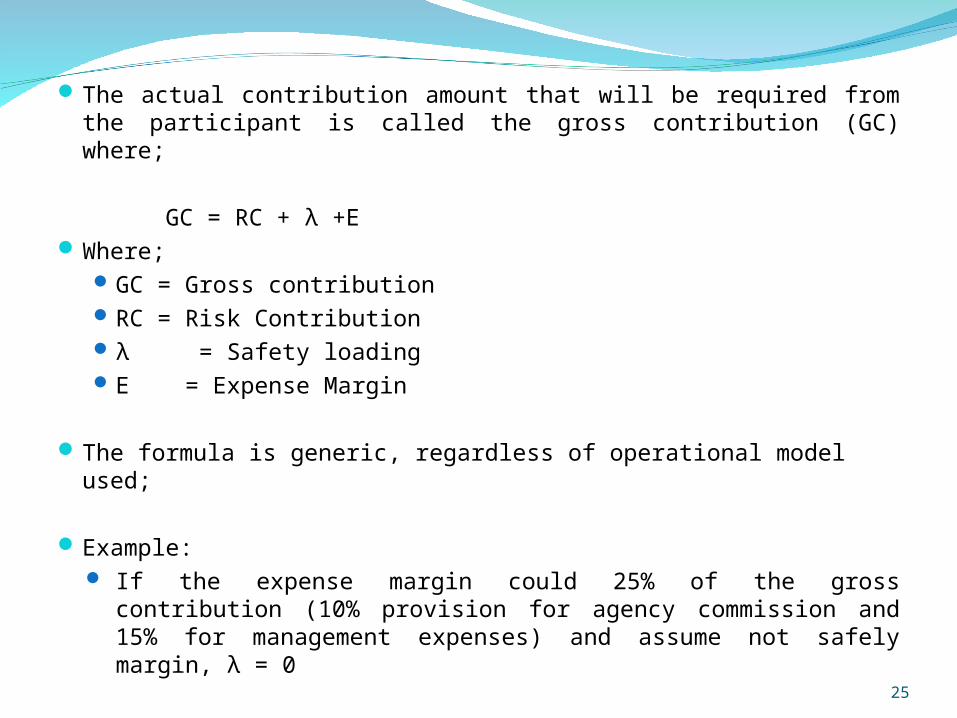

The actual contribution amount that will be required from the participant is called the gross contribution (GC) where;

GC = RC + λ +EWhere;

GC = Gross contributionRC = Risk Contributionλ = Safety loadingE = Expense Margin

The formula is generic, regardless of operational model used;

Example: If the expense margin could 25% of the gross contribution (10%

provision for agency commission and 15% for management expenses) and assume not safely margin, λ = 0

25

Therefore;G = RC + λ + E

= RC + 0 + 0.25 GC 0.75GC = RC

GC = RC / 0.75

If safety loading is placed at 10% of gross contribution;

Then;GC = RC + 0.1GC + 0.25GC

Therefore; GC = RC/ 0.65

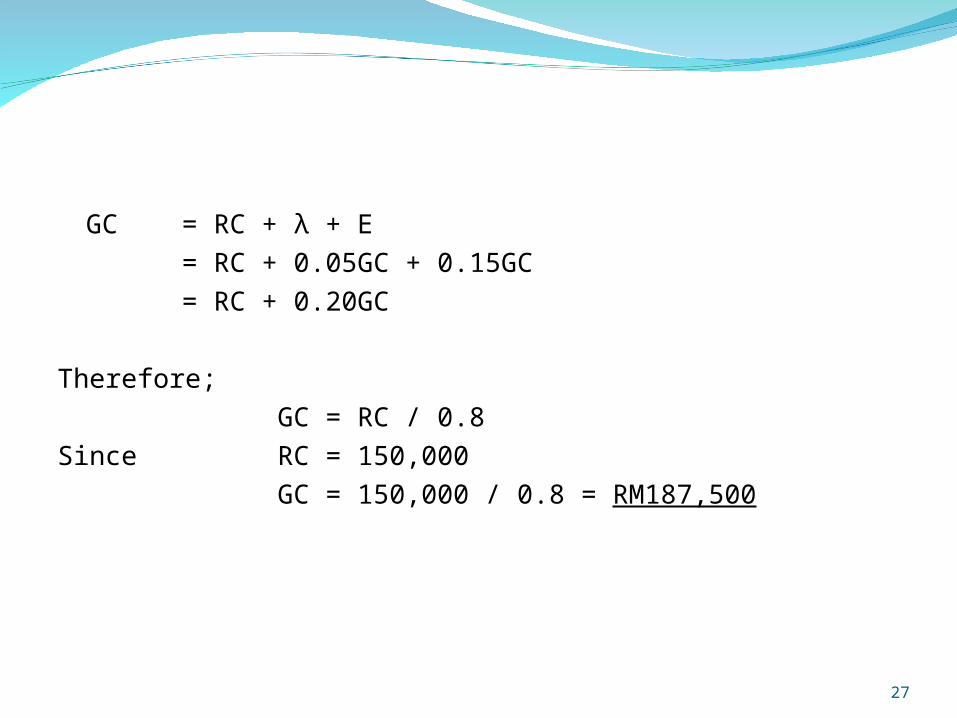

Example : A takaful scheme is proposed to cover a group of construction workers. The risk contribution is set for RM150,000. Calculate the gross contribution, where

the safety loading is 5% of gross contribution and marketing and management expenses is 15% of gross premium.

26

GC = RC + λ + E

= RC + 0.05GC + 0.15GC

= RC + 0.20GC

Therefore;

GC = RC / 0.8

Since RC = 150,000

GC = 150,000 / 0.8 = RM187,500

27

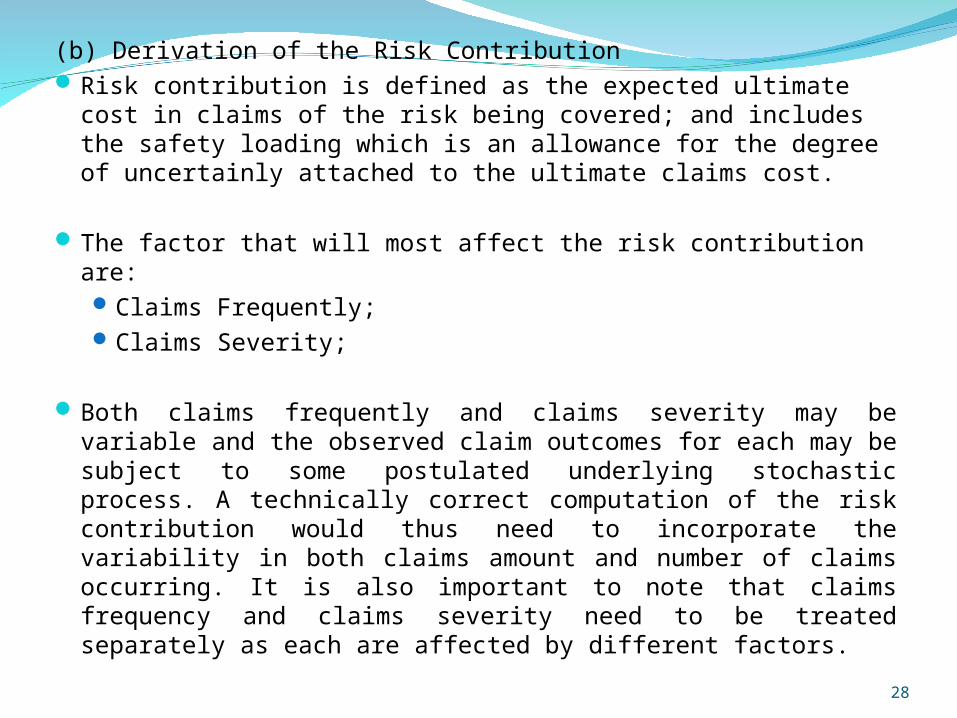

(b) Derivation of the Risk ContributionRisk contribution is defined as the expected ultimate cost in claims of

the risk being covered; and includes the safety loading which is an allowance for the degree of uncertainly attached to the ultimate claims cost.

The factor that will most affect the risk contribution are:Claims Frequently;Claims Severity;

Both claims frequently and claims severity may be variable and the observed claim outcomes for each may be subject to some postulated underlying stochastic process. A technically correct computation of the risk contribution would thus need to incorporate the variability in both claims amount and number of claims occurring. It is also important to note that claims frequency and claims severity need to be treated separately as each are affected by different factors.

28

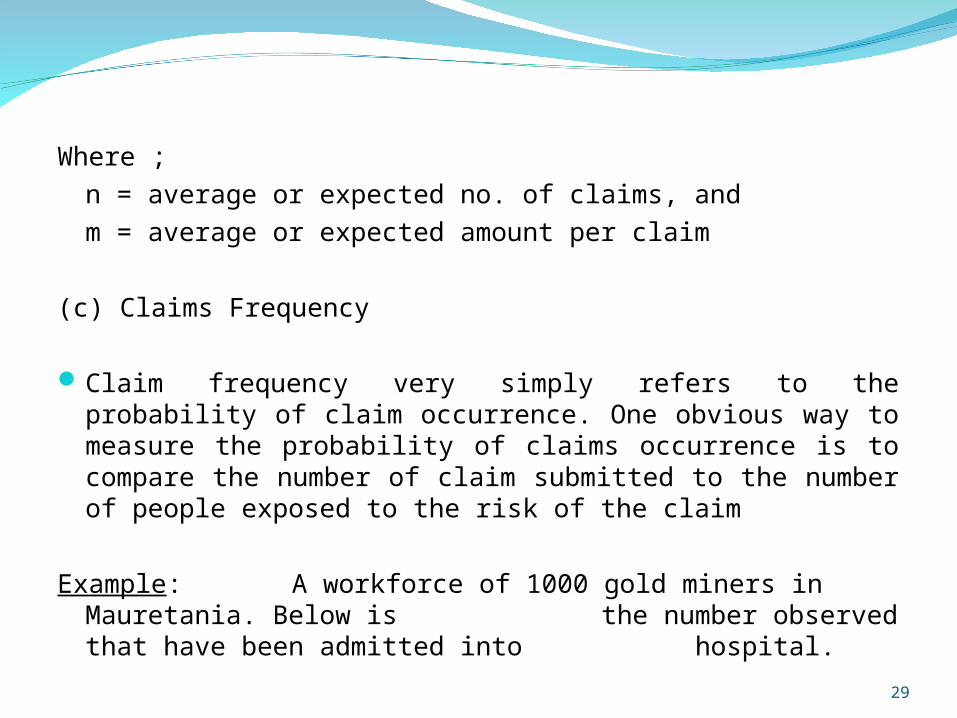

Where ;

n = average or expected no. of claims, and

m = average or expected amount per claim

(c) Claims Frequency

Claim frequency very simply refers to the probability of claim occurrence. One obvious way to measure the probability of claims occurrence is to compare the number of claim submitted to the number of people exposed to the risk of the claim

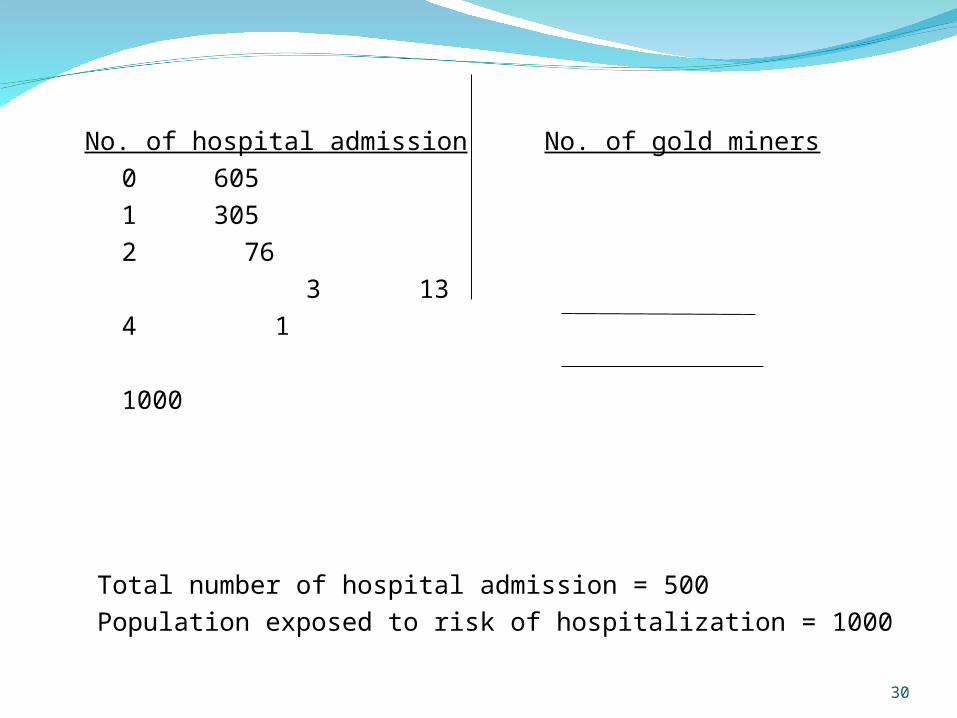

Example: A workforce of 1000 gold miners in Mauretania. Below is the number observed that have been admitted into hospital.

29

No. of hospital admission No. of gold miners

0 605

1 305

2 76

3 13

4 1

1000

Total number of hospital admission = 500

Population exposed to risk of hospitalization = 1000

30

Therefore, the average yearly claims frequency is

= 500/1000 = ½, half a hospital admission per miner per year. (one out of every two miners will make a visit to hospital)

If a takaful scheme were to be set up to provide hospitalization expense coverage and the gold mine management wished to fix a hospitalization takaful benefit of $100 per hospital visit, what should the fair contribution amount be for each gold miner covered under the takaful scheme

The Risk contribution RC = n x m

From above, RC = ½ x 100 = $50

In many practical cases, the estimation of claims frequencies will be hampered by lack of appropriate statistics.

31

(d) Usage of Statistical Distribution Patterns with Known Formulae

Based on limited or even unavailable data, it is often the case that practical calculations for purpose of takaful applications (such as contribution rates) need to be done with reference to assumed underlying claims frequency pattern.

For this purpose one of several statistical distribution patterns with known formulae would be used as the assumed statistical model for claim frequency; statistical distributions such as the Poisson distribution, Bionomical distribution and the Normal distribution may be used;

For the Poisson distribution which is frequently used to represent the pattern of claims frequency, have the following characteristics:

Average of claim frequency = λ

Variance of claim frequency = λ

Probability of n claims occurring = (λn e -λ) / n!

32

The process of formulating contribution rates needs to be prospective in nature, since takaful benefits are paid in the future;

Although historical data provide some guidance on trends in claim frequency, ultimately some judgment need to be exercised due to changes in the environment and the portfolio of risks;

Greater care needs to be taken in estimating claims frequencies for general takaful products as compared to family takaful products, unlike family takaful, in general takaful multiple claims are possible in the same year and in addition, the contract would typically cover range of different risks or perils.

(e) Claims SeverityClaim severity simply refers to the probability of claims size

occurrence. As in the case estimating claims frequency, reliable statistics can be difficult to obtain and resource will often need to be made to assuming a Statistical distribution with a known formula as the underlying statistical model.

33

Even in cases where sufficient claims statistics may exist, the use of the statistical distribution that fits the observed claims data may be preferable because:

It may be more convenient as the rates are easier to complete;

Working on related actuarial tasks become easier with a formula based statistical distribution;

Inferences about the underlying behavior of participants and the covered risks may be easier to discern with a formula based statistical distribution;

34

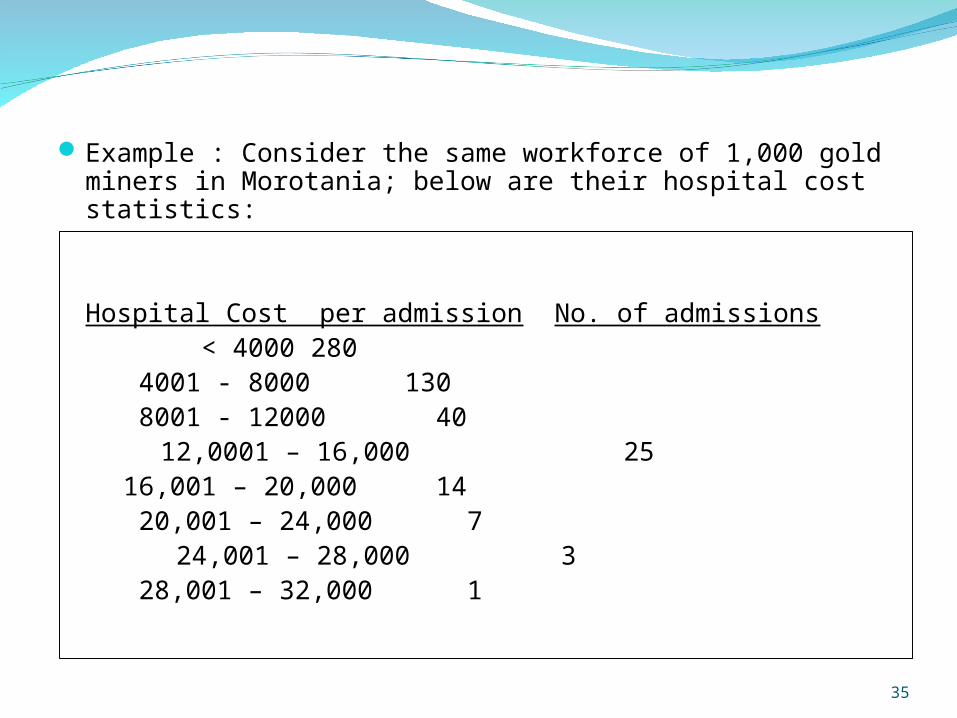

Example : Consider the same workforce of 1,000 gold miners in Morotania; below are their hospital cost statistics:

Hospital Cost per admission No. of admissions < 4000 280 4001 - 8000 130 8001 - 12000 40

12,0001 – 16,000 2516,001 – 20,000 14 20,001 – 24,000 7

24,001 – 28,000 3 28,001 – 32,000 1

35

What is the average hospitalization cost per admission for this group?

Total Hospital Cost = 2000 (280) + 6000 (130) + 10000 (40)14000 (25) + 18000 (14) + 22000 (7) +

26000 (3) + 30000 (1)

= $2,604,000

Since, there are 500 hospital admissions in the year;Average Hospitalization Cost = Total Hospitalization Cost /

number of admission

= 2,604,000 / 500

= $5,208

36

Therefore the appropriate risks contribution to be charge to each participant is;

RC = n x m

n = ½, m = 5208

Therefore;

RC = ½ x 5208 = $2,604

(f) The Importance of Understanding the Claims Severity Pattern

In working on claims amounts statistics, the underlying claims pattern and not just the average claims figure needs to be carefully looked at; an example of where care needs to be taken in studying claims severity is in considering the extremities of the observed data.

37

In the above example, the distribution of claims amount is skewed to the right with no claims exceeding $32,000, this does not mean there will be no claim exceeding $32,000.

In this instance the actuary in conjunction with professional claims and underwriting managers need to work out an allowance or provision for such contingency;

The distribution of claim amounts due to its highly skewed nature do have great influence on the pricing; getting an accurate picture of the tail is a challenge because of the scarcity of data; in this type of position operators with a small takaful fund was be at a disadvantage; even large operators are unlikely to have sufficient claim experience; retakaful or reinsurance companies would have the benefit of such claims experience;

As such, in many lines of general and family takaful business, guidance from retakaful operators and reinsurers in the setting of rates and contact wording is useful;

38

(g) Other Methods of Calculating the Risk Contribution

In the absence of data, a method known as ‘burning cost’ method can be used where in this case the risk contribution is the ratio of past reported or paid claims to some measure of the population or participants exposed to the risk; this method has some application to types of covered risks which generate larger number of claims with very little variation in claims size;

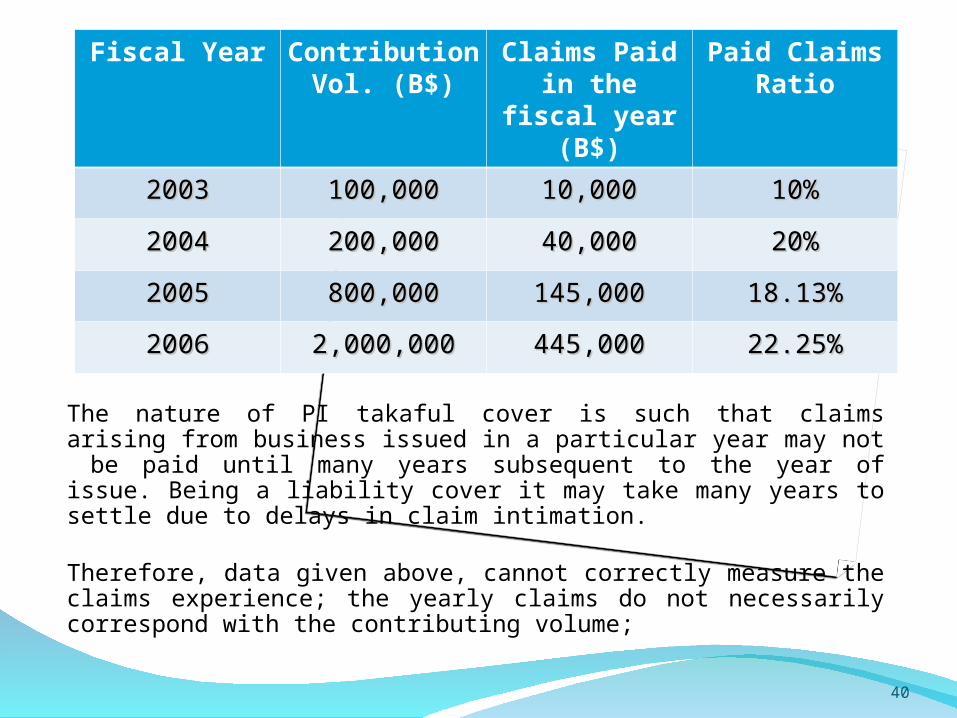

Example : A takaful operator in Buranda has been marketing Professional Indemnity (PI) contracts for the past 4 years. Since the business is perceived very safe the operator intends to reduce the PI contribution rate. Is

the data given below is sufficient to support the operators intention:

39

The nature of PI takaful cover is such that claims arising from business issued in a particular year may not be paid until many years subsequent to the year of issue. Being a liability cover it may take many years to settle due to delays in claim intimation.

Therefore, data given above, cannot correctly measure the claims experience; the yearly claims do not necessarily correspond with the contributing volume;

40

Fiscal Year Contribution Vol. (B$)

Claims Paid in the fiscal year (B$)

Paid Claims Ratio

20032003 100,000100,000 10,00010,000 10%10%

20042004 200,000200,000 40,00040,000 20%20%

20052005 800,000800,000 145,000145,000 18.13%18.13%

20062006 2,000,0002,000,000 445,000445,000 22.25%22.25%

Even though the claims ratio is low, the reliability of the result is suspect; in addition, the effects of inflation, changes in claims settlement practices as well as growth in new business is ignored;

In order to identify the actual claims pattern arising from each year of takaful business issued, claims data needs to be obtained that links the claims paid in a particular year with the year in which the contract generating the claim was originally issued.

The point of this example, besides indicating the danger of blindly applying the burning cost approach, is also to illustrate that the takaful operator needs to consider that the claims paid for a particular takaful product in any one year is a composite of many different claims which originate from different periods of coverage for all year up to the current year.

41

Example: From the previous example, let say the takaful operator have been to

obtain a more detailed claims information:

Describe the method of data tabulation. Is this information sufficient for you to check the validity of the managements conclusions? What conclusions can you draw from the tabulated data?

The above tabulation of claims is known as a claims triangulation; the tabulation makes it much easier to trace trends and identify the ultimate claims experience emerging on takaful business issued in any given year.

42

Year of Year of issueissue

Contribution Contribution VolumeVolume

Claims Paid Claims Paid Development Development

Year 0Year 0

Claims Paid Claims Paid Development Development

Year 1Year 1

Claims Paid Claims Paid Development Development

Year 2Year 2

Claims Paid Claims Paid Development Development

Year 3Year 3

20032003 100,000100,000 10,00010,000 20,00020,000 25,00025,000 35,00035,000

20042004 200,000200,000 20,00020,000 40,00040,000 50,00050,000

20052005 800,000800,000 80,00080,000 160,000160,000 -- --

20062006 2,000,0002,000,000 200,000200,000 -- -- --

The below is the Cumulative Paid Claims Triangulation

Cumulative claims up to the present year is derived by adding the claims paid in the current year to the sum of claims in all previous years for the same block of contract issued in a given year.

43

Year of Year of IssueIssue

Contribution Contribution VolumeVolume

Claims Paid Development Claims Paid Development

Year 0Year 0 Year 1Year 1 Year 2Year 2 Year 3Year 3

20032003 100,000100,000 10,00010,000 30,00030,000 55,00055,000 90,00090,000

20042004 200,000200,000 20,00020,000 60,00060,000 110,000110,000 --

20052005 800,000800,000 80,00080,000 240,000240,000 -- --

20062006 2,000,0002,000,000 200,000200,000 -- -- --

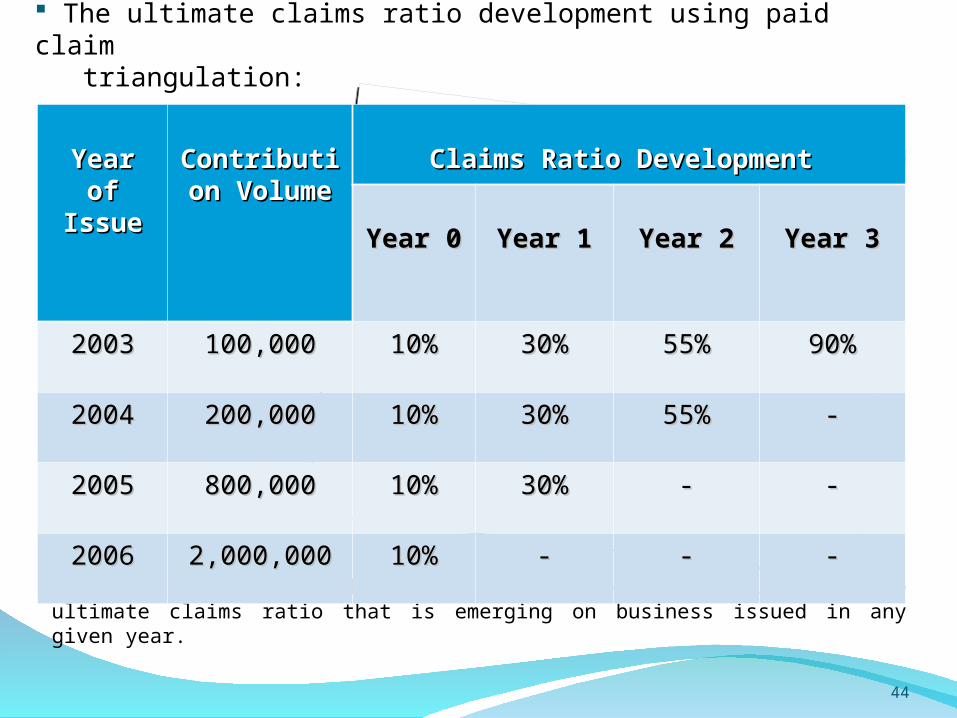

The ultimate claims ratio development using paid claim triangulation:

With the above triangulation, it is much easier to identify the ultimate claims ratio that is emerging on business issued in any given year.

44

Year of Year of IssueIssue

Contribution Contribution VolumeVolume

Claims Ratio Development Claims Ratio Development

Year 0Year 0 Year 1Year 1 Year 2Year 2 Year 3Year 3

20032003 100,000100,000 10%10% 30%30% 55%55% 90%90%

20042004 200,000200,000 10%10% 30%30% 55%55% --

20052005 800,000800,000 10%10% 30%30% -- --

20062006 2,000,0002,000,000 10%10% -- -- --

In the above case, it is obvious that the true claims ratio is not as low as the operator is given to understand. Based on the above triangulation, it can be concluded that the operator would be well advised to not reduce the takaful contribution rates for PI business at the present stage.

(h) Generalized Linear Modelling (GLM)One guiding assumption in using claims statistics to compute

contribution rates is that participants that share the same characteristics i.e., homogeneous, should likewise be exposed to the same risks. Unfortunately, the population exposed to risk are often not homogeneous; therefore by breaking down the claims data into smaller blocks originating from takaful participants with similar risk factors, a more valid determination of contribution rates can be made.

Once homogeneous data in a volume that sufficiently reliable is complied, statistical methods such the GLM may then be used to construct contribution rates that reflect the various rating factors.

45

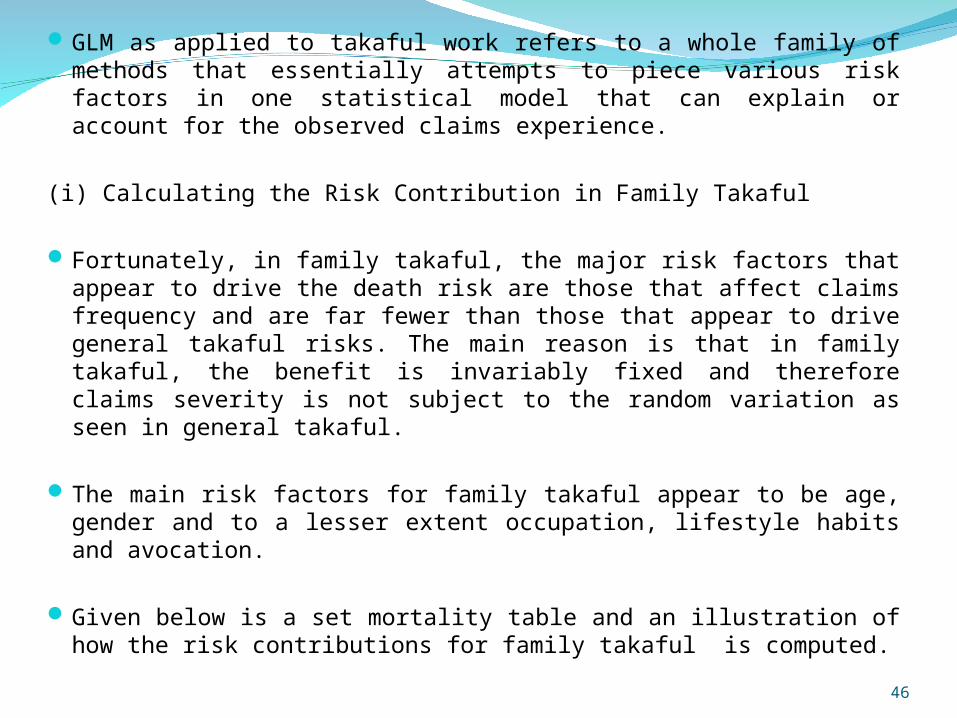

GLM as applied to takaful work refers to a whole family of methods that essentially attempts to piece various risk factors in one statistical model that can explain or account for the observed claims experience.

(i) Calculating the Risk Contribution in Family Takaful

Fortunately, in family takaful, the major risk factors that appear to drive the death risk are those that affect claims frequency and are far fewer than those that appear to drive general takaful risks. The main reason is that in family takaful, the benefit is invariably fixed and therefore claims severity is not subject to the random variation as seen in general takaful.

The main risk factors for family takaful appear to be age, gender and to a lesser extent occupation, lifestyle habits and avocation.

Given below is a set mortality table and an illustration of how the risk contributions for family takaful is computed.

46

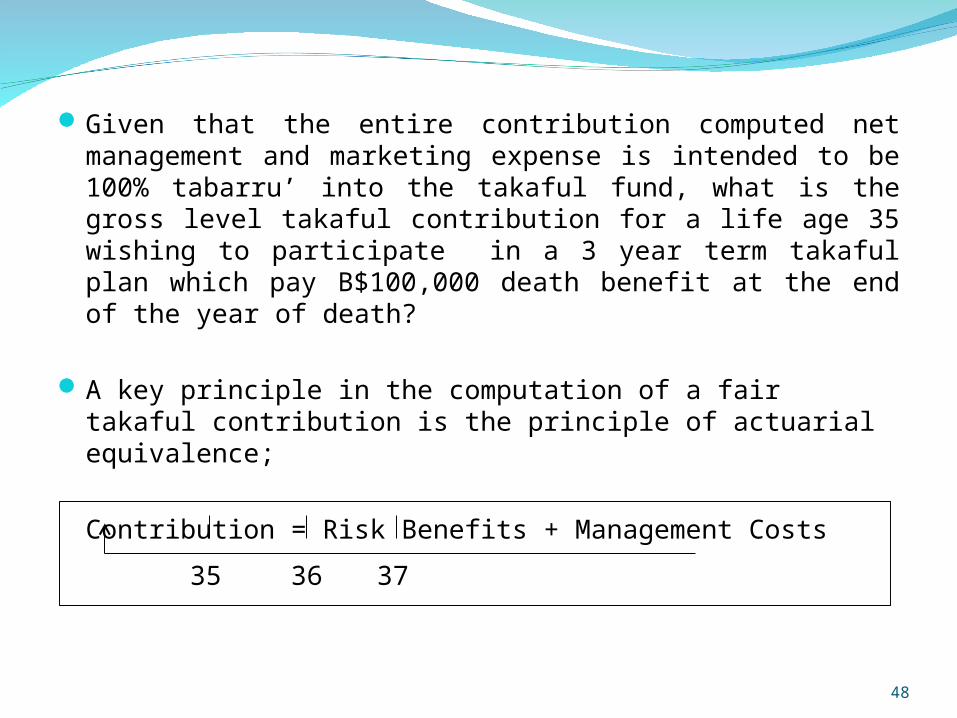

Example:Consider a 3 year level contribution term takaful product is

developed for Burunda. Given:(a) The mortality of participants is assumed to follow the table

below;(b) Management and marketing expenses costs = 45% of

gross contribution(c) The takaful fund is expected to generate 3% investment

profit per year

47

Exact AgeExact Age No. of livesNo. of lives No. of dyingNo. of dying Prob. of dyingProb. of dying Prob. of survivingProb. of surviving

3535 1,000,0001,000,000 1,550 1,550 0.001550.00155 0.998450.99845

3636 998,450998,450 1,6671,667 0.001670.00167 0.998330.99833

3737 996,783996,783 1,8041,804 0.001810.00181 0.998190.99819

3838 994,978994,978 1,9501,950 0.001960.00196 0.998040.99804

3939 993,028993,028 2,1252,125 0.002140.00214 0.997860.99786

4040 990,903990,903 -- -- --

Given that the entire contribution computed net management and marketing expense is intended to be 100% tabarru’ into the takaful fund, what is the gross level takaful contribution for a life age 35 wishing to participate in a 3 year term takaful plan which pay B$100,000 death benefit at the end of the year of death?

A key principle in the computation of a fair takaful contribution is the principle of actuarial equivalence;

Contribution = Risk Benefits + Management Costs

48

35 36 37

Therefore risk benefits;

= 100,000 [1/1.03 (0.00155) + ( 1/1.03 )2 (0.99845) (0.00167)

+ (1/1.03)3 (0.99845) (0.99833) (0.00181)]

= 100,000 [ 0.001505 + 0.001572 + 0.001651 ]= 472.76

The gross contribution;

= GC + GC (1/1.03 ) (0.99845) + GC (1/1.03 )2 (0.99845) (0.99833)

= GC [ 1 + 0.969369 + 0.941022 ] = GC [2.910391]

49

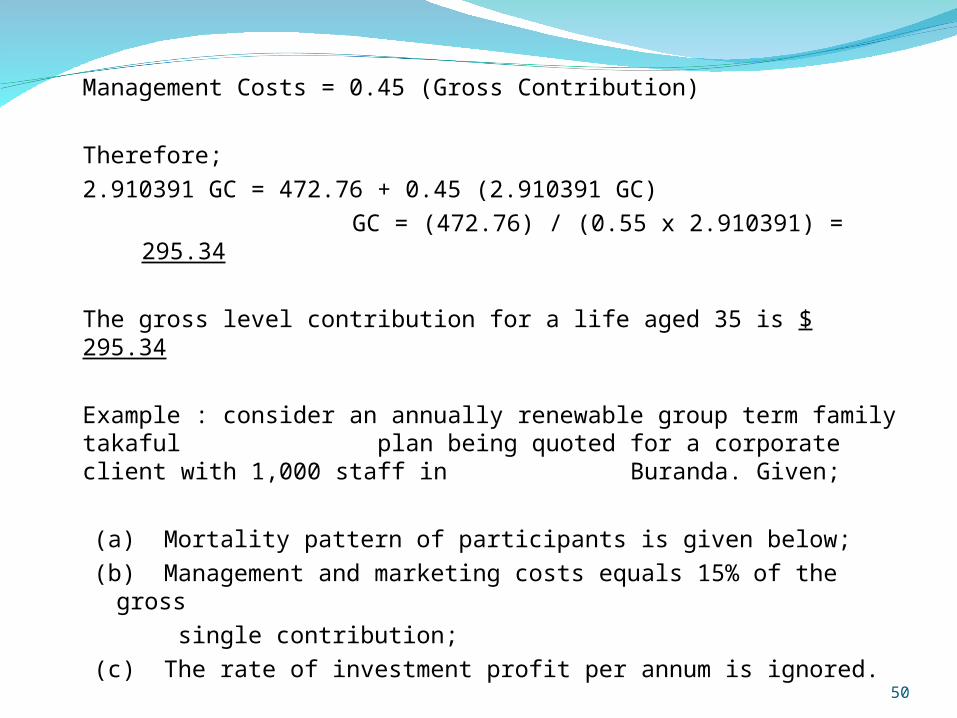

Management Costs = 0.45 (Gross Contribution)

Therefore;

2.910391 GC = 472.76 + 0.45 (2.910391 GC)

GC = (472.76) / (0.55 x 2.910391) = 295.34

The gross level contribution for a life aged 35 is $ 295.34

Example : consider an annually renewable group term family takaful plan being quoted for a corporate client with 1,000 staff

in Buranda. Given;

(a) Mortality pattern of participants is given below;

(b) Management and marketing costs equals 15% of the gross

single contribution;

(c) The rate of investment profit per annum is ignored. 50

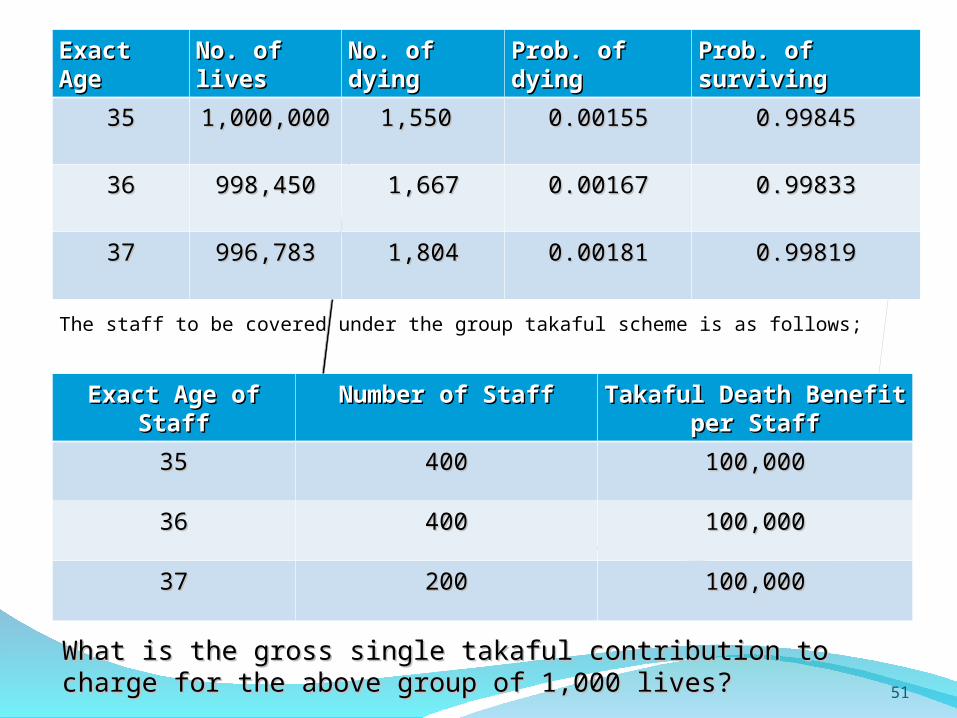

The staff to be covered under the group takaful scheme is as follows;

51

Exact AgeExact Age No. of livesNo. of lives No. of dyingNo. of dying Prob. of dyingProb. of dying Prob. of survivingProb. of surviving

3535 1,000,0001,000,000 1,550 1,550 0.001550.00155 0.998450.99845

3636 998,450998,450 1,6671,667 0.001670.00167 0.998330.99833

3737 996,783996,783 1,8041,804 0.001810.00181 0.998190.99819

Exact Age of StaffExact Age of Staff Number of StaffNumber of Staff Takaful Death Benefit per Takaful Death Benefit per StaffStaff

3535 400400 100,000100,000

3636 400400 100,000100,000

3737 200200 100,000100,000

What is the gross single takaful contribution to charge for the above What is the gross single takaful contribution to charge for the above group of 1,000 lives?group of 1,000 lives?

Risk Contribution (RC) = 100,000 [ 400 (0.00155) + 400 (0.00167) + 200 (0.00181)]

= 165,000

Gross Contribution (GC) = RC + 15% GC

Therefore; GC = RC/0.85 = 165,000/0.85 = 194,117.65

The sum total of assumptions used in the pricing of the product is known as the pricing basis

The parameters for the pricing basis would typically be derived from observed experience taken from inside and outside the takaful operator. In the case of a newly set up takaful operator and fund, since internal experience would be used as guidelines.

The above computation is relatively simplistic it ignores the effect of liability provision may have on the takaful fund and other effects.

52

(j) Cash Flow Method of PricingWith this approach, the contribution calculation does not just

consider expected cash flows of benefit and contribution payment but sensitivities to other factors as well such as the probability of withdrawal or disability benefits thereon.

This method also known as the method of profit testing, is set up to overcome the limitations of the formula method outlined earlier;

Other factors that can be explicitly incorporated into the cash flow model include specific operator profit targets, taxation, the effect of liability provisions, the opportunity cost of temporary loan injections by the operator, nature of the takaful operational model being used, etc.

53

The cash flow method is especially useful in analyzing operator profit as the sources of operator revenue may come from one or more of the following three sources of possible revenue as follows:

Management fees computed as a % of takaful funds managed, a flat yearly fee contract and a % of the contribution collected for the fund;

Share of yearly investmentShare of underwriting surplus

With the cash flow method, the specific revenue sources can be easily identified and product features such as contribution and benefit levels can be easily reconfigured to meet certain the operators goals for shareholders and participants.

54

(k) Various Profit Targets

There are several profit targets that a takaful operator may use in evaluating the attractiveness of a particular product for development.

The following are examples of possible profit targets that may be used;

Profit marginBreakeven YearReturn on Investment

55

End

56