Open Road Tolling (()ORT) The MDX Experience

14

4/14/2011 1 Open Road Tolling(ORT) The MDX Experience IBTTA Organization Management W kh Workshop April 11, 2011 SR 924 Gratigny Parkway SR 112 Airport Expressway SR 836 Dolphin Expressway SR 874 Don Shula & SR 878 Snapper Creek

Transcript of Open Road Tolling (()ORT) The MDX Experience

4/14/2011

1

Open Road Tolling (ORT)p g ( )The MDX Experience

IBTTA Organization Management W k hWorkshopApril 11, 2011

SR 924 Gratigny Parkway

SR 112 Airport Expressway

SR 836 Dolphin Expressway

SR 874 Don Shula &SR 878 Snapper Creek

4/14/2011

2

Why ORT?

• 5 of the most heavily traveled

expressways in Miami‐Dadep y

• Limited right‐of‐way restricting

ability to expand system

• Toll‐free movements

• Projected 21% growth over the next 20 years in Miami‐Dade County

• Need for increased revenue stream to fund future improvements

• ORT Master Plan – Board Approval 2006

– Set framework to convert entire MDX system to electronic

The ORT Evolution

ytoll collection

– Set the recommended scenario to “close the system” with a goal to provide fairness to all users

– Sought to maintain the rate per mile per corridor prior to conversion to minimize impacts on the system users

4

4/14/2011

3

• Toll Policy – Board Approval 2008

– All vehicular movements on tolled portions of the MDX System

The ORT Evolution

p yshall be tolled

– As MDX converts every roadway to ORT• Un‐tolled vehicular movements shall be eliminated

• Per mile toll rate (excluding any Surcharge) approximately the same over the length of such expressway prior to Conversion

– Surcharge

5

• Established from time to time by resolution of the Board• Sufficient to cover the cost to process and collect Toll By Plate transactions

• Approved concurrently with the Annual Operating Budget of the Authority

Laying the Foundation• Maximized SunPass usage

– Multi‐year, Multi‐level Outreach Program

• Maximized existing infrastructure to improve mobility

– Operational improvements

– Addition of auxiliary lanes

– Enhancements to existing interchanges

• Made provisions for user‐friendly technology

– Support of low‐cost transponder – accessible to ALL

– Protect user privacy ‐ transponder use anonymous

– Accommodate rental car users and taxis

– Accommodate tourists

4/14/2011

4

Benefits of ORT

• Better Service

• Safer Facilities

• Faster Travel Times

• Fuel Savings

• Increased through‐put

• Lower Carbon Emissions

• Lower Operating CostsLower Operating Costs

• Lower Future Construction Costs

• Funding for Future Improvements

The ORT Story

201455% of U

97% of Users will Pay

28% of Users Paid

42% of Users Paid

SR 924, SR 874, SR 878

2007

2010

2012

2013Users Pay

SR 112 Go‐Live

SR 836 East/West Go‐Live

SR 836 Central Go‐Live

,Go‐LivePilot ORT

SR 836 Extension

4/14/2011

5

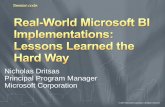

$207,562

$200,000

$250,000

Revenue Actual/Forecast

FY 2005 ‐ FY 2020(In Thousands)

$58,651

$142,185 $171,505

$‐

$50,000

$100,000

$150,000

$

Existing System Full ORT

SR 924 Before and After ORT

4/14/2011

6

SR 874 Before and After ORT

34,088,265

41,389,714

35 000 000

40,000,000

45,000,000

Transactions by RoadwayFY 2011 & FY 2010

6‐Months (July ‐ December)

6,315,736

12,715,769

11,410,926

6,206,750 5 354 267

32,862,971

13,670,638

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

6,206,750 5,354,267 00

SR112

Airport

SR924

Gratigny

SR836

Dolphin

SR874

South Dade

SR878

Snapper Creek

Transactions ‐ FY 2011 Transactions ‐ FY 2010

4/14/2011

7

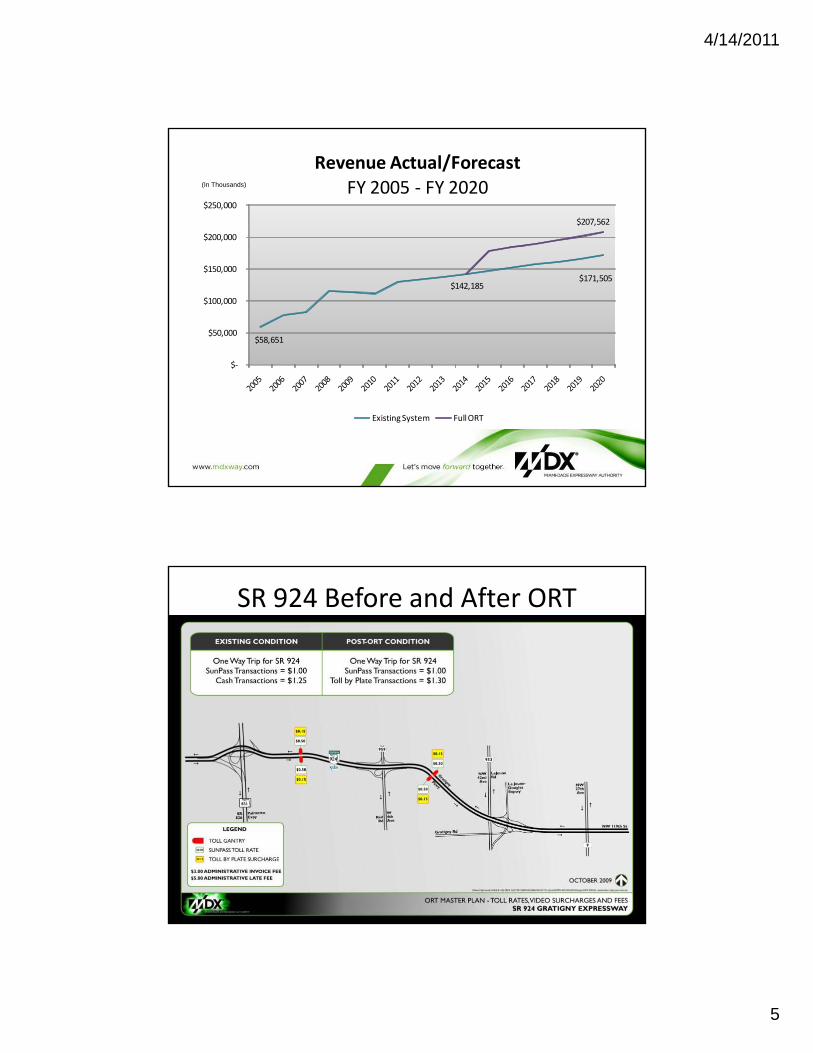

$30,253,459

$30,000,000

$35,000,000

Revenue by RoadwayFY 2011 & FY 2010

6‐Months (July ‐ December)

$7,281,771

$7,545,012

$16,607,042

$3,005,023 $6,470,114 $5,691,952

$25,638,990

$13,894,321

$‐$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

SR112 Airport

SR924 Gratigny

SR836 Dolphin

SR874 South Dade

SR878 Snapper Creek

Revenue ‐ FY 2011 Revenue ‐ FY 2010

$20,843,409

$20 000 000

$25,000,000

SunPass Revenue by RoadwayFY 2011 & FY 2010

6‐Months (July ‐ December)

$4,405,347 $5,724,724

$12,098,120

$2,262,753

$3,965,967 $4,060,994

$18,409,353

$8,851,692

$

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$‐$0

SR 112Airport

SR 924Gratigny

SR 836Dolphin

SR 874South Dade

SR 878Snapper Creek

SunPass ‐ FY 2011 SunPass ‐ FY 2010

4/14/2011

8

Revenue Distribution6‐Months (July to December)

FY 2010 FY 2011

$16,398,571 30%

$38,107,484 70%

FY 2010

$9,063,267 15%

$45,334,353 75%

$5,746,281 10%

FY 2011

Cash SunPass Cash SunPass Toll‐By‐Plate

Revenue CompositionFY 2011

Gross Revenue Adj d R

64.16%

21.70%

14.14%

Gross Revenue

75.37%

9.56%15.07%

Adjusted Revenue

SunPass Toll‐By‐Plate Cash SunPass Toll‐By‐Plate Cash

4/14/2011

9

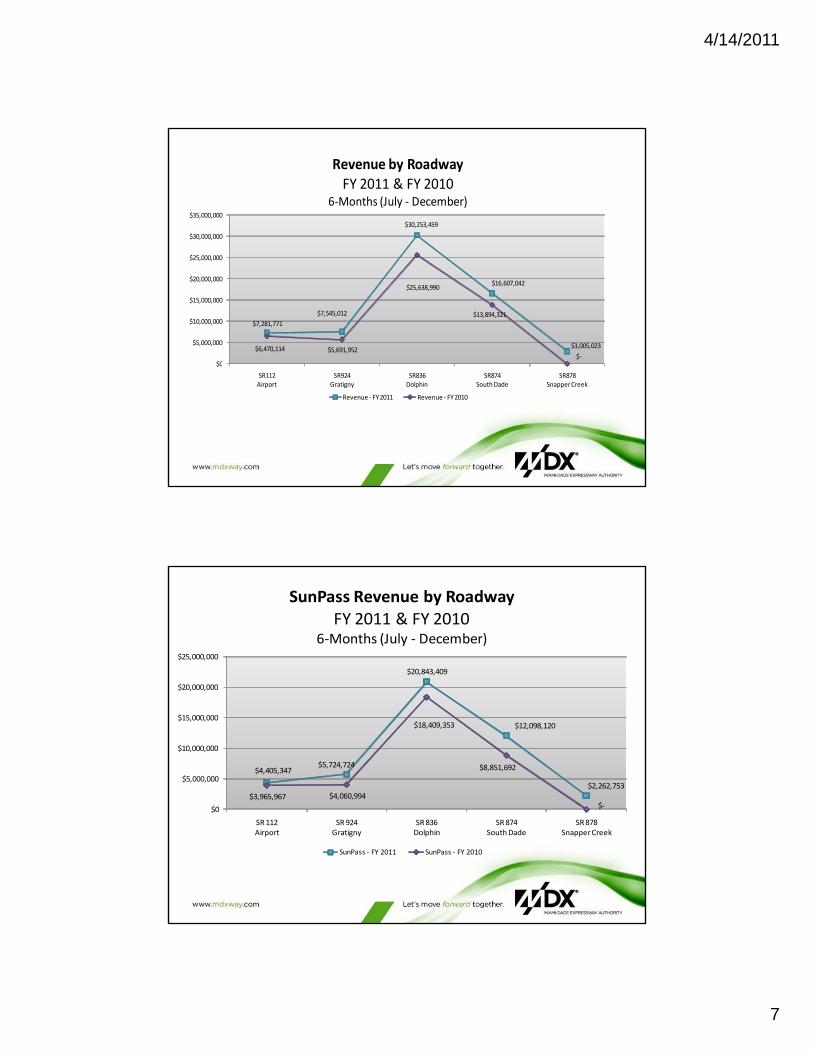

• Investor based outlook • Customer based outlook

Finance Operations

• Investor based outlook

• Data – Financial reporting

– Revenue impact

• Reconciliation– Payments by Location

– Receivables

D dli d i

• Customer based outlook

• Data

– Performance measures

– Transaction volume

• Reconciliation

– Amounts by payment type

– Customer accounts– Deadline‐driven

• Trend Analysis– Receivable allowance

– Revenue forecasting & coverage

17

Customer accounts

• Trend Analysis

– Traffic & revenue patterns

– Customer issues

• Investor based outlook

• Data – Financial reporting

• Customer based outlook

• Data

P f OperationsFinancial reporting

– Revenue impact

• Reconciliation– Payments by Location

– Receivables

– Deadline‐driven

• Trend Analysis– Receivable allowance

– Performance measures

– Transaction volume

• Reconciliation

– Amounts by payment type

– Customer accounts

• Trend Analysis

– Traffic & revenue patterns

One Common GoalBest Interest of MDX

Finance Operations

– Receivable allowance

– Revenue forecasting & coverage

Traffic & revenue patterns

– Customer issues

18

4/14/2011

10

Invoice / Enforcement Timeline

1st NoticeFee $3

(30 Days to P )

Late NoticeFee $5

(30 Days to P )

Toll Violation Notice (TVN)

$10 Fine + amt due(30 D t P )

Day 30

Day 60

Day 90

Day 190

Pay) Pay) (30 Days to Pay)

Day 120

Collection Agency

Registration

Uniform Traffic Citation (UTC)Registration Filing withg

Hold33% of amt due(60 Days to Pay)

gHold lifted

(30 Days to Pay)All fees & fines

Filing with M‐D Court

• SunPass

– Least expensive

T ll b Pl t

Toll Payment Options

• Toll‐by‐Plate

– Automatically captures the image of a vehicle’s license plate as the vehicle passes under toll gantry

• Images with no transponder read are sent to back office

Customers may pay INVOICES/TVN’s/UTC’s

– Web ‐ 33%Web 33%

– Lockbox (mail)– 41%

– Customer service representative – 25%

– Walk‐ins – less 1%

20

4/14/2011

11

• Charge covers the cost to process toll‐by‐plate transactions– Toll‐by‐Plate Charge = $0.15 / Gantry

• Administrative Invoice Fee covers the cost to mail in the

TBP Charge & Invoice Fee

invoice– Administrative Invoice Fee = $3.00

• Administrative Late Fee is associated with untimely payment of tolls and represents cost of funds– Administrative Late Fee = $5.00

• Third‐Party Collection Agency– NO cost to MDX ‐ small fee directly from customers

– Obtain payment from delinquent customers prior to moving to the UTC stage

– Maximize percentage of collected tolls

21

• S. 316.1001 Payment of toll on toll facilities required; penalties.–

Uniform Traffic Citation (UTC)

– Failure to pay a prescribed toll is a noncriminal traffic infraction, punishable as a moving violation under chapter 318.

– Mandatory $100 fine for each violation of s. 316.1001">316.1001 plus the amount of the unpaid toll shown on the traffic citation for each citation issued.

– 3 points assessed against driving record

– Suspension of Driver’s License for failure to pay

22

4/14/2011

12

Applicable Accounting Guidance

• General Accepted Accounting Principal

FASB SFAC. 5Earned

FASB SFAC. 5

• International Accounting Standard 18

IAS 18

• Security Exchange Commission

SAB 101 (SAB 104)

Measurable

• Non GAAP Collectable

• Enterprise Fund – Accrual basis of accounting

MDX General Accounting

g

• Revenue recognized when earned / services have been rendered – Lane exit date/Billed date

• Revenue measurable– Toll Rate Policyy

• Collectability is reasonably assured – % uncollectable

• Bad Debt – Balance Sheet Method

24

4/14/2011

13

Regulatory Environment• Reporting Requirements

• Policy & Procedures

• Internal Controls

– Segregation Duties

– Accuracy & Completeness

– IT Controls

• Risk Assessment

– Financial Risk

– Public Trust

What’s the Target?

Financial Planning &

Sound Policies

Public Trust

Good Management Practices

RevenueRevenue Assurance

4/14/2011

14

Q&A

Q&A

Thank You!