Online Grocery Shopping Research FINAL

25

Javelin Group | 200 Aldersgate Street | London EC1A 4HD | United Kingdom | +44(0)20 7961 3200 | www.javelingroup.com Online Grocery Shopping Research 03/07/15

-

Upload

max-naylor -

Category

Documents

-

view

23 -

download

1

Transcript of Online Grocery Shopping Research FINAL

Javelin Group | 200 Aldersgate Street | London EC1A 4HD | United Kingdom | +44(0)20 7961 3200 | www.javelingroup.com

Online Grocery Shopping Research

03/07/15

2

Contents

Online Grocery Shopping Research

03/07/15

Max Naylor

Work experience

1. Background on me

2. Online Grocery proposition and current market

3. Online Grocery Proposition Summary

4. Conclusions

5. What I have learned

3

Background on me

Who am I and what do I do

My name is Max and I am doing work experience at Javelin Group

I go to The Latymer School, Edmontono I have recently finished my GCSE’s

A-Level topics

Hobbieso Sporto Musico Volunteering

I have an interest in going into management consultancy or law in the future

4

What I wanted to gain from this week

During this week I had hoped to achieve certain aims

o To gain experience of working in an office environment

o To learn more about management consultancy

o To find out how various members of the team got to where they are

o To make connections with people

o To add some substance to my CV

5

Contents

Online Grocery Shopping Research

03/07/15

Max Naylor

Work experience

1. Background on me

2. Online Grocery proposition and current market

3. Online Grocery Proposition Summary

4. Conclusions

5. What I have learned

6

Grocery summary

Wiki and Forbes

Firstly, what is Proposition and how is it important for a business

USP – Unique Selling Point A proposition is what makes the business stand out from its competitors in the market to the customers

For a business having a USP isn’t enougho Standing out from the crowd o A customer needs to see the value of your product or service

As a business your propositions determine who you areo Certain propositions will attract certain customer bases and then you will be know for those by your customerso for example, Waitrose are known for a higher quality of product which is more expensive o so that appeals to a certain market segment and that forms and contributes to their brand image.

Having clear propositions as a business is important o as your customers or potential customers will know what you are selling or offering as a serviceo that will help them decide whether to choose you.

7

Grocery Summary

What is it that customers want from their grocers

Value for money o Tesco losing to ALDI and Waitrose

Time efficient shoppingo they want to be able to shop quickly and often

Healthy, low fat, alternativeso consumers have access to more information, and that’s leading them to demand moreo for example, more than 70 percent of consumers now read food labels often

and nearly half want to see food products rated by “healthfulness”

Wide product rangeo Due to globalisation and containerisation, importing and exporting foods has become easier and cheapero Consumers now demand a variety of products and are no longer satisfied with basics

Good customer serviceo consumers recognize that grocers are gathering information about who they are and what they buy

they expect you to use that information to give them a better shopping experienceo they no longer want you to simply sell them food

they expect you to help them achieve their goal of a healthy lifestyle for themselves and their families.

8

Grocery Summary

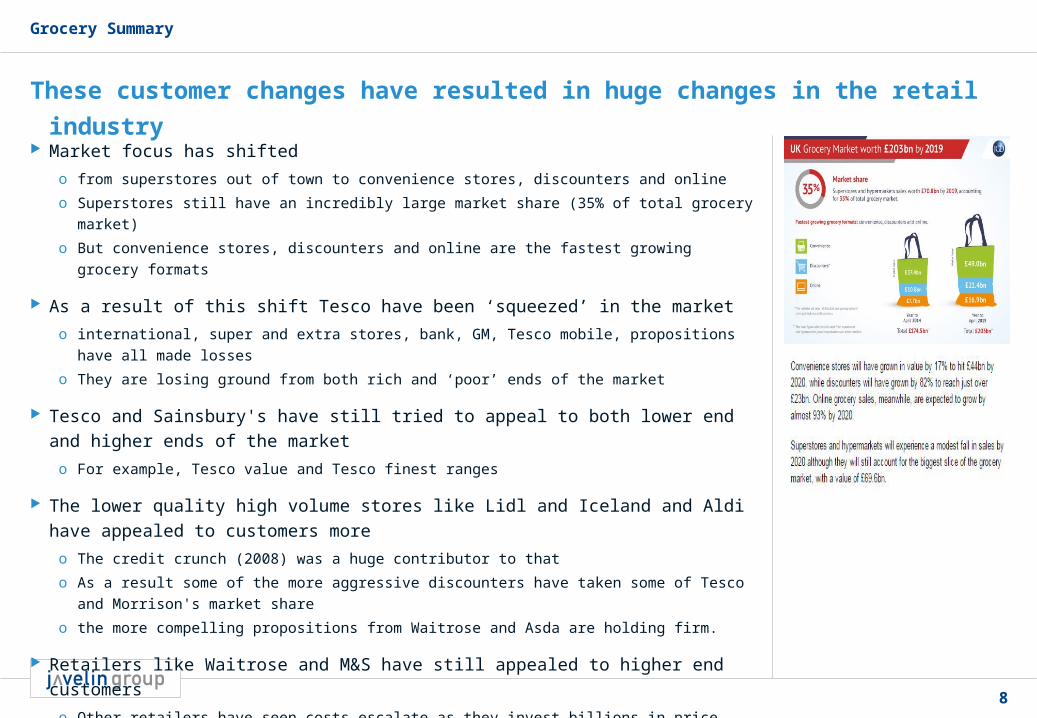

These customer changes have resulted in huge changes in the retail industry

Market focus has shiftedo from superstores out of town to convenience stores, discounters and onlineo Superstores still have an incredibly large market share (35% of total grocery market)o But convenience stores, discounters and online are the fastest growing grocery formats

As a result of this shift Tesco have been ‘squeezed’ in the market o international, super and extra stores, bank, GM, Tesco mobile, propositions have all made losseso They are losing ground from both rich and ‘poor’ ends of the market

Tesco and Sainsbury's have still tried to appeal to both lower end and higher ends of the marketo For example, Tesco value and Tesco finest ranges

The lower quality high volume stores like Lidl and Iceland and Aldi have appealed to customers moreo The credit crunch (2008) was a huge contributor to thato As a result some of the more aggressive discounters have taken some of Tesco and Morrison's market shareo the more compelling propositions from Waitrose and Asda are holding firm.

Retailers like Waitrose and M&S have still appealed to higher end customerso Other retailers have seen costs escalate as they invest billions in price matching and slashingo Waitrose’s margins remain healthy thanks to their unique, quality-led proposition.

9

Grocery Summary

Consumer behaviour developments have forced grocery retailers to respond

Over the past few years we have becomeo Tighter on time and budget

Our once 3-4 hour £200 weekly shop has now been reduced to cheap and often oneso Ease-orientated

As a consumer we have began shopping online, on the move, in our spare time i.e. on the way home We often look for simple and easy meal solutions

o Price Conscious We continue to demand high value without compromising quality

o As a consumer many retailers seem to struggle to grasp this concepto Savvy

We shop around and buy according to our particular circumstances Loyalty is to a grocer is becoming less frequent and is becoming more easily broken by consumers

In response to this grocers are o Heading back to the high streets and opening increasing numbers of convenience stores

This results in increasing competitiono Managing overheads burdened by big and expensive stores and complex operationso Squeezing margins and investing in price reductionso Polarising their positions

responding to the growth of the discounters such as Aldi and Lidl raising quality standards is one solution, this would earn them a premium or fighting the ‘price plus quality’ battle.

10

Contents

Online Grocery Shopping Research

03/07/15

Max Naylor

Work experience

1. Background on me

2. Online Grocery proposition and current market

3. Online Grocery Proposition Summary

4. Conclusions

5. What I have learned

11

Grocery summary | Market map | Venn Diagram

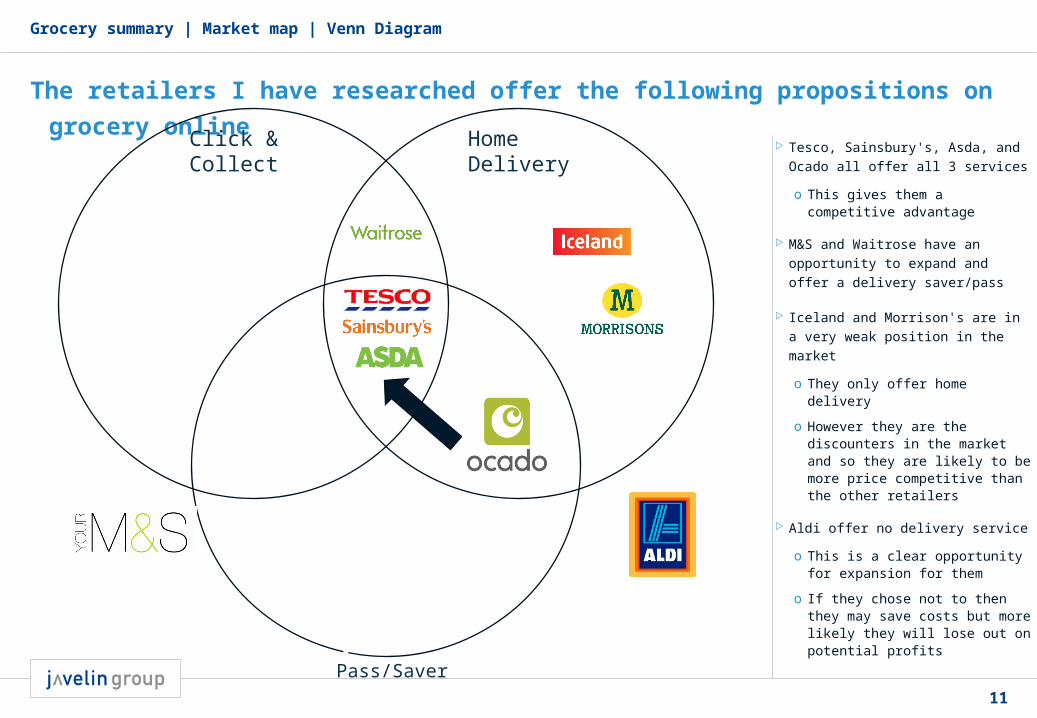

The retailers I have researched offer the following propositions on grocery online

Tesco, Sainsbury's, Asda, and Ocado all offer all 3 services

o This gives them a competitive advantage

M&S and Waitrose have an opportunity to expand and offer a delivery saver/pass

Iceland and Morrison's are in a very weak position in the market

o They only offer home delivery

o However they are the discounters in the market and so they are likely to be more price competitive than the other retailers

Aldi offer no delivery service

o This is a clear opportunity for expansion for them

o If they chose not to then they may save costs but more likely they will lose out on potential profits

Click & Collect Home Delivery

Delivery Pass/Saver

12

Grocery Summary

Here are the Click and Collect locations available for the 6 retailers who offer that proposition

Waitrose have introduced 7 new temperature-controlled Click & Collect lockers o These are at service, train, and tube stations

Ocado are trailing 2 tube collection pointso but these have seen limited success with Tesco and JS pulling out of the C&C proposition

13

Grocery Summary

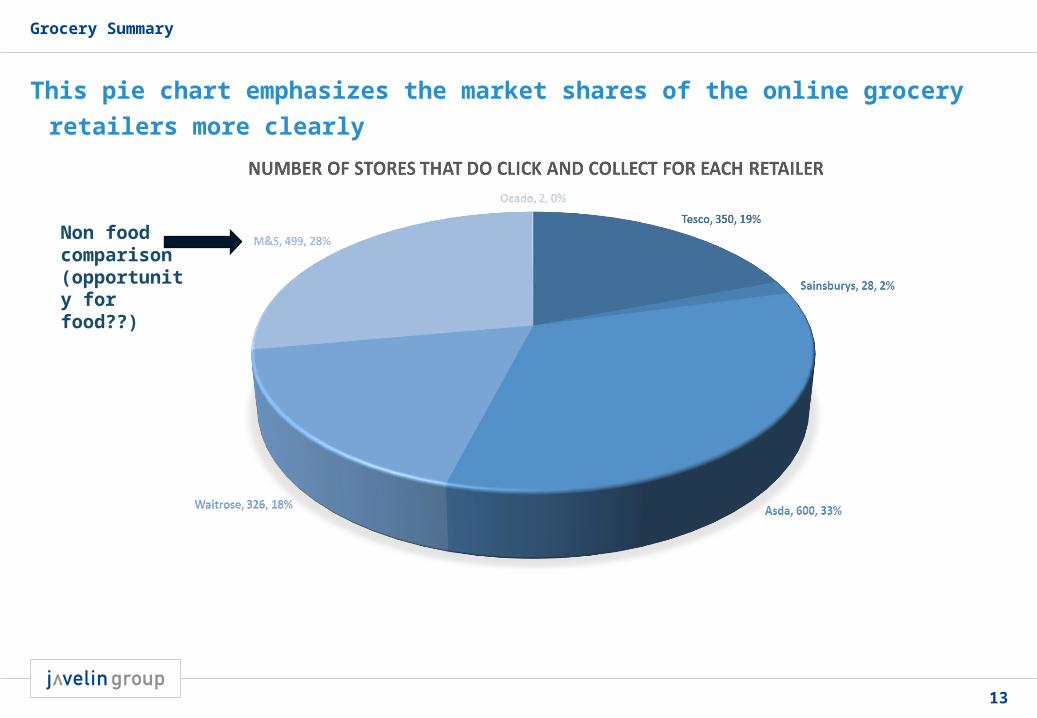

This pie chart emphasizes the market shares of the online grocery retailers more clearly

Non food comparison(opportunity for food??)

14

Grocery Summary

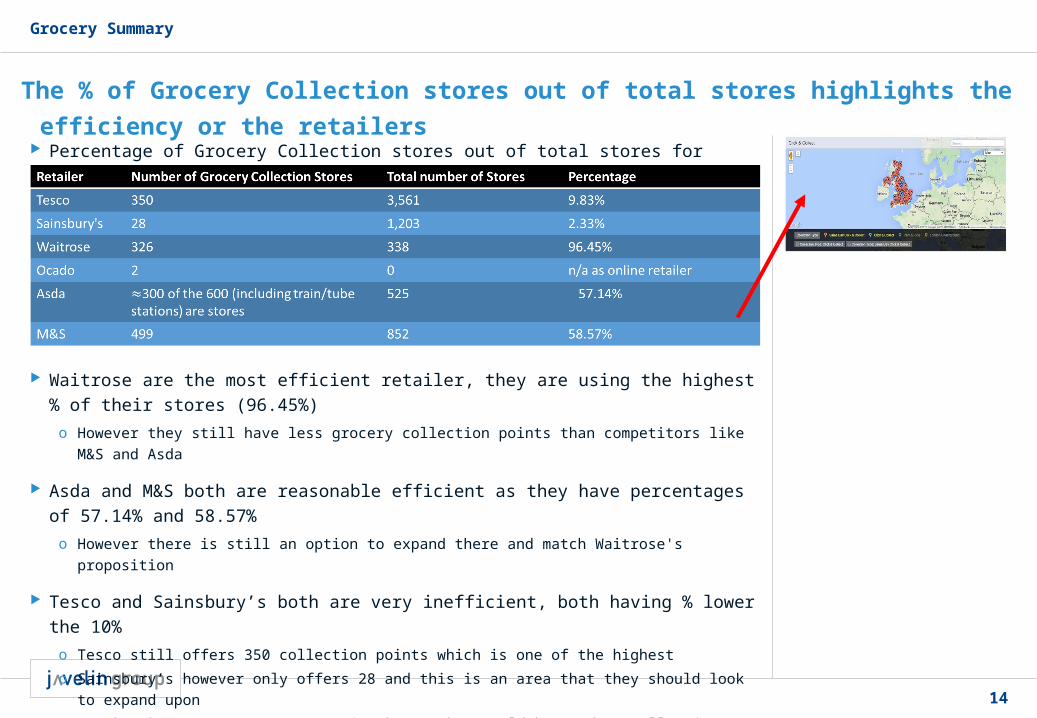

The % of Grocery Collection stores out of total stores highlights the efficiency or the retailers

Percentage of Grocery Collection stores out of total stores for click and collect

Waitrose are the most efficient retailer, they are using the highest % of their stores (96.45%)o However they still have less grocery collection points than competitors like M&S and Asda

Asda and M&S both are reasonable efficient as they have percentages of 57.14% and 58.57%o However there is still an option to expand there and match Waitrose's proposition

Tesco and Sainsbury’s both are very inefficient, both having % lower the 10%o Tesco still offers 350 collection points which is one of the highesto Sainsbury’s however only offers 28 and this is an area that they should look to expand upon

They have over 1,203 stores in the UK that could be used as collection points

Ocado have no stores and so have had to try something to compete with rivals for C&Co So they have trailed tube station pick ups but Tesco and JS found this unsuccessful

15

Grocery Summary

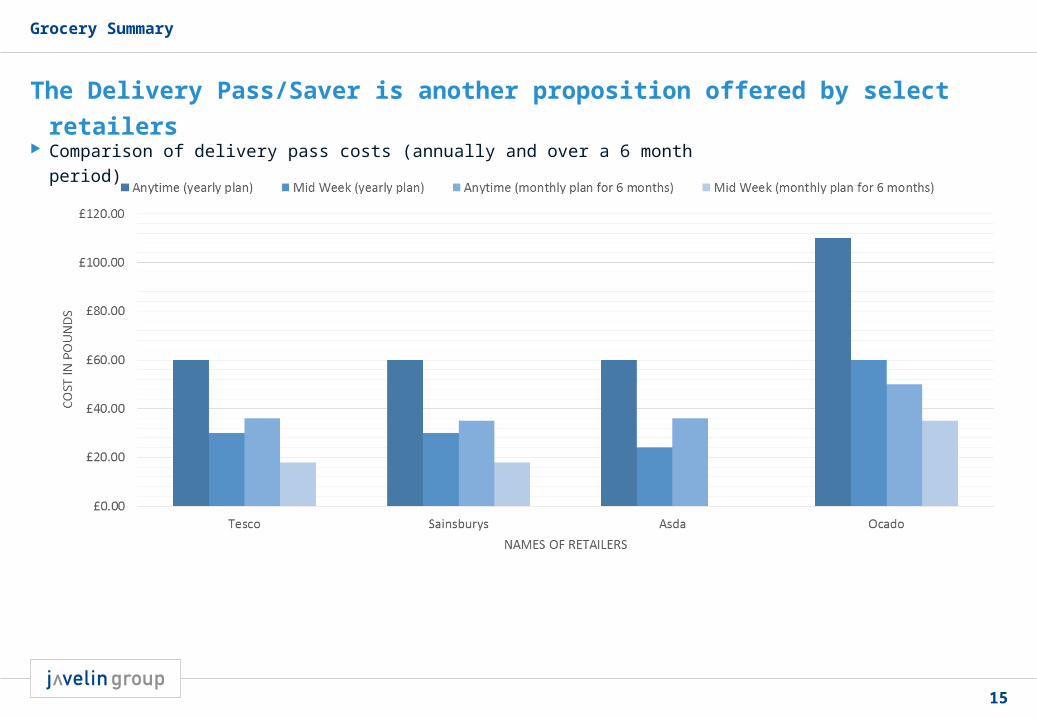

The Delivery Pass/Saver is another proposition offered by select retailers

Comparison of delivery pass costs (annually and over a 6 month period)

16

Grocery Summary

Home Delivery is the final of the 3 propositions that I have researched

Home Deliveryo A comparison of costs for each time of delivery for each retailer

17

Grocery Summary

18

Grocery Summary

19

Grocery Summary

20

Grocery Summary

The minimum spend on online grocery varies considerably between retailers

C&C = click and collect

HD = Home Delivery

DP = Delivery Pass

C&C = click and collect

HD = Home Delivery

DP = Delivery Pass

21

Grocery Summary

The cut off times for changes or cancellations are reasonably similar though throughout

22

Contents

Online Grocery Shopping Research

03/07/15

Max Naylor

Work experience

1. Background on me

2. Online Grocery proposition and current market

3. Online Grocery Proposition Summary

4. Conclusions

5. What I have learned

23

From this research that I have done, I can conclude that

Everything that is going on in the market now is a result of changing customer habits o As their needs change the grocers must adapt quickly in order to stay ahead of their competitorso Whilst Tesco are being squeezed, aggressive discounters are thriving on these changing demands

Of the 3 key propositions, (C&C, HD, DS) only 4 of the 9 major online grocery retailers offer all 3o This means less competition for Tesco, JS, Asda and Ocadoo However this is also an opportunity for the other retailers to seize a larger market share of online grocery

Which is predicted to grow by 93% by 2020 – from £7.7bn in 2014 to £16.9bn in 2019o An example would be for Lidl, who currently offer none of the 3 propositions to invest in a click and collect system

This would be cheaper than starting with a home delivery service which would require them to hire or buy trucks They already have 600 UK stores for customers to collect from, and C&C gets customers into stores were they are likely to buy additional items

o It is the same for Ocado and Sainsbury's who offer very few click and collect locations compared to their rivals, they are missing an opportunity

The delivery pass saver costs almost exactly the same from Tesco, Asda and Sainsbury’s – however ocado is almost double the price They do this because they offer a ‘smart pass’ which gives customers discounts, free delivery's, anniversary gifts and so on. The delivery pass saver is effectively guaranteeing the retailer a loyal customer for that period

o this is useful as customer loyalty is becoming increasingly non-existent as they often look for the cheapest price

24

I can also see that

Home delivery prices vary considerably depending on time and retailero Morrison’s are almost consistently the cheapest excluding Waitrose, Ocado and Iceland who offer free deliveryo JS are often the most expensive of the retailers o Tesco and Asda fluctuate between being relatively expensive or cheapo Fridays, Saturdays and Sundays show very similar trends from all the retailers who charge money

There is a negative correlation with minor fluctuations o Monday to Thursdays show us that they have very different prices at in the morning but generally by the afternoon they all merge to form a visible trend

(Sainsbury’s expensive, Tesco and Asda average and Morrison’s cheap) in the mornings

Minimum spend shows no trend for any of the 3 propositions o They all have different amounts and fees if under

Cut off times however are between 10pm and midnight the night before delivery They are all very competitive here and try to offer the latest possible time There is perhaps an opportunity here for a rival to be aggressively competitive and offer a cut off time say 2 hours before delivery or something similar

o However this is an unrealistic option as that would cost the retailer too much and so the profit margins wouldn’t be improved enough by the ‘better’ customer service

Slot lengths are very similar here as they all are either 1 hour long or 2 hours long.

o There is a gap in the market for a half hour delivery slot and this would give that retailer a serious advantage and they could charge a high premium for it

o An example would be Amazon who have launched ‘Prime now’ which delivers the product within 1 hour of ordering to certain London postcodes and they charge a premium price of £6.99

25

QUESTIONS?