One flight many apps - Business Finland · One flight many apps Drone Market & Opportunities Tero...

22

Aug 26, 2015 One flight many apps Drone Market & Opportunities Tero Heinonen

Transcript of One flight many apps - Business Finland · One flight many apps Drone Market & Opportunities Tero...

Aug 26, 2015

One flight many appsDrone Market & Opportunities

Tero Heinonen

ADVERTISEMENT

Peter van BlyenburghUVS [email protected]

uvs-international.org

www.rpas-regulations.com

Back to the future – we have seen this before

1993Window to the

world ofcomputers

2015 Window to thephysical world

© 2015 Sharper Shape – All Rights Reserved

What are drones?

Drones

RPASRemotely PilotedAircraft System

UAVUnmanned Aerial

Vehicle

UASUnmanned Aerial

System

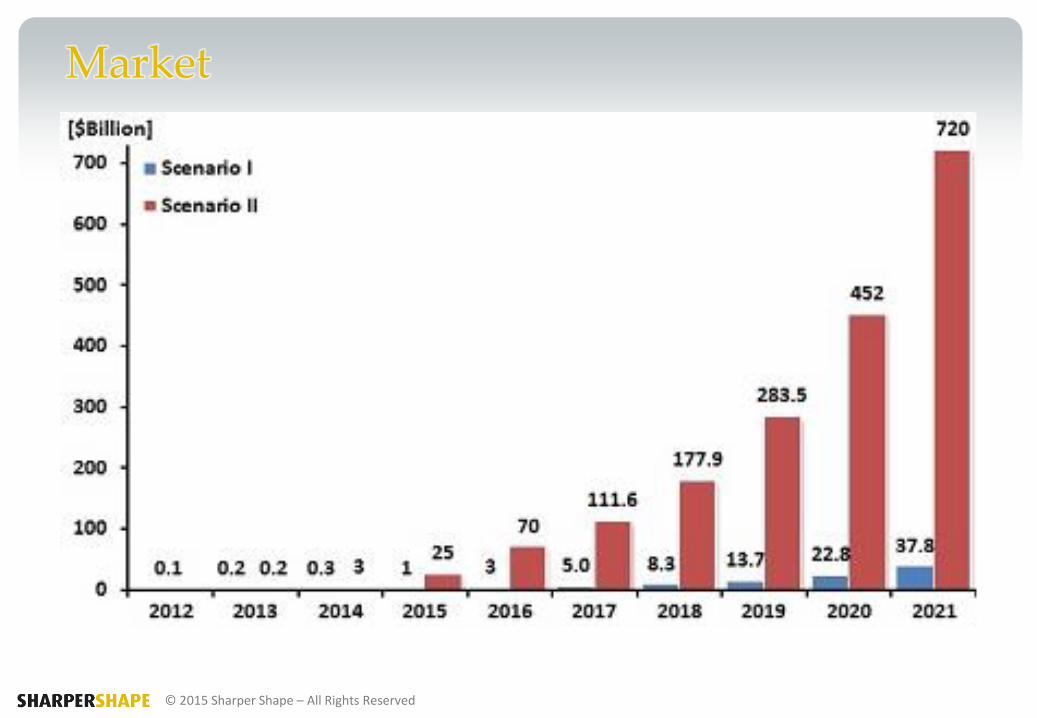

Market

© 2015 Sharper Shape – All Rights Reserved

Market – key take-outs

• Total expected new market growth > $100 bn in 10 years

• The services related to drones are expected to exceed the value of equipment

• Today drones are primarily used for military, but civilian applications will drive the market growth

• The regulation allowing civilian applications is being prepared on global, European and national levels and will be established between 2015 and 2025

© 2015 Sharper Shape – All Rights Reserved

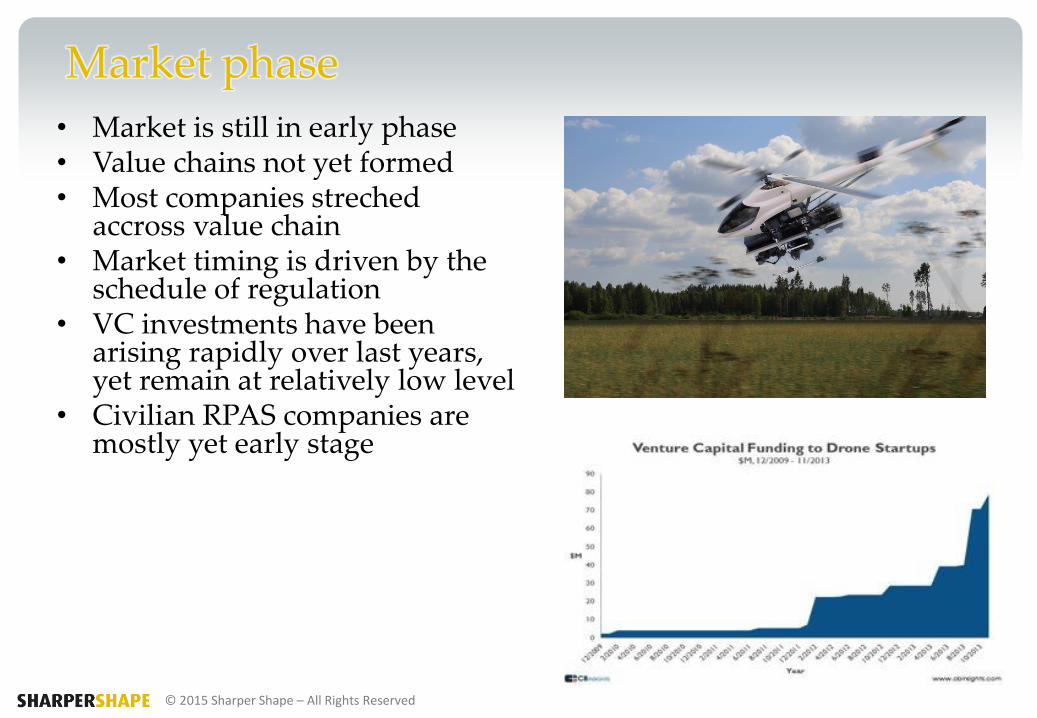

Market phase

• Market is still in early phase• Value chains not yet formed• Most companies streched

accross value chain• Market timing is driven by the

schedule of regulation• VC investments have been

arising rapidly over last years, yet remain at relatively low level

• Civilian RPAS companies are mostly yet early stage

© 2015 Sharper Shape – All Rights Reserved

Market phase – Investment Focus

© 2015 Sharper Shape – All Rights Reserved

Market phase – A handful of well-capitalized

© 2015 Sharper Shape – All Rights Reserved

Market phase – Attempt to classify companies

© 2015 Sharper Shape – All Rights Reserved

Chris McCann in medium.comAug 13, 2015

medium.com/@mccannatron/drone-market-ecosystem-map-a8febf0ca8fd

Convergence of industries

Google, Amazon, Project Loon, Titan Aerospace, Sharper Shape and DJI are registered trademarks of their respective owners

Convergence of regimes

UNMANNEDSPACE

UNMANNEDAVIATION

MANNEDSPACE

MANNEDAVIATION

Technologies

Platforms

Services

Av

iati

on

and

Sp

ace

con

ver

gen

ce

Manned and Unmanned Convergence

Law and Regulation

© 2015 Sharper Shape – All Rights Reserved

Competitive borderlines

TraditionalAviation &

Defence

Silicon Valleyand

Startups

National/ EU

Global

© 2015 Sharper Shape – All Rights Reserved

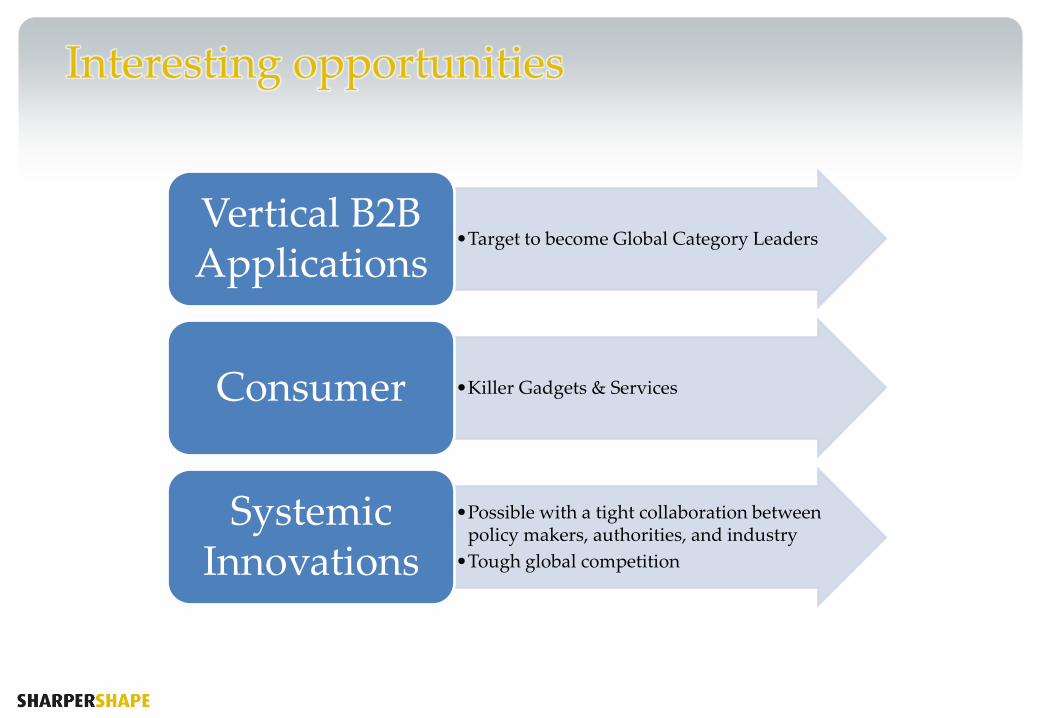

Interesting opportunities

•Target to become Global Category LeadersVertical B2B Applications

•Killer Gadgets & ServicesConsumer

•Possible with a tight collaboration betweenpolicy makers, authorities, and industry

•Tough global competition

SystemicInnovations

From VLOS to BVLOS to Suborbital to SpaceToday Tomorrow 2020 2020-2030

”VLOS Era” ”BVLOS Era” ”Integrated Era” ”Converged Era”

Small drones flying simpleapplications near the pilot. Drones are in isolation.

Many size of drones in differentiated applications. First systemic solutionsstart to emerge.

Systemic innovationsenabled regular integrateddrone ops. Value chainsformed. Category leadersestablished.

Aviation, suborbital, and space converged. Apps and services detached fromunderlying deliverytechnology. Multimodalops supporting many apps.

90% of B2B civ apps areVLOS

>50% of civ apps B2B revenue is from BVLOS.

VLOS and BVLOS termsrendered obsolete, alltraffic integrated. A largepart of civ apps revenuefrom established (global orlocal) category leaders.

Traffic revenues primarily in LE. Service and apprevenues diversified, including global categoryleaders & niche or localSME.

95% of companies are SME 90% of companies are SME, Increasing part of apprevenue is in moreestablished companies(some migrated from otherindustries, some successfulstartups maturing).

Global and local trafficproviders emerge.Separation of traffic and apps and services.

Majority of traffic and opsprovided by LE,Service innovationcontinues in SME & startups.

Source: Sharper Shape Drone Industry Analysis, 2015© 2015 Sharper Shape – All Rights Reserved

© 2015 Sharper Shape – All Rights Reserved 17

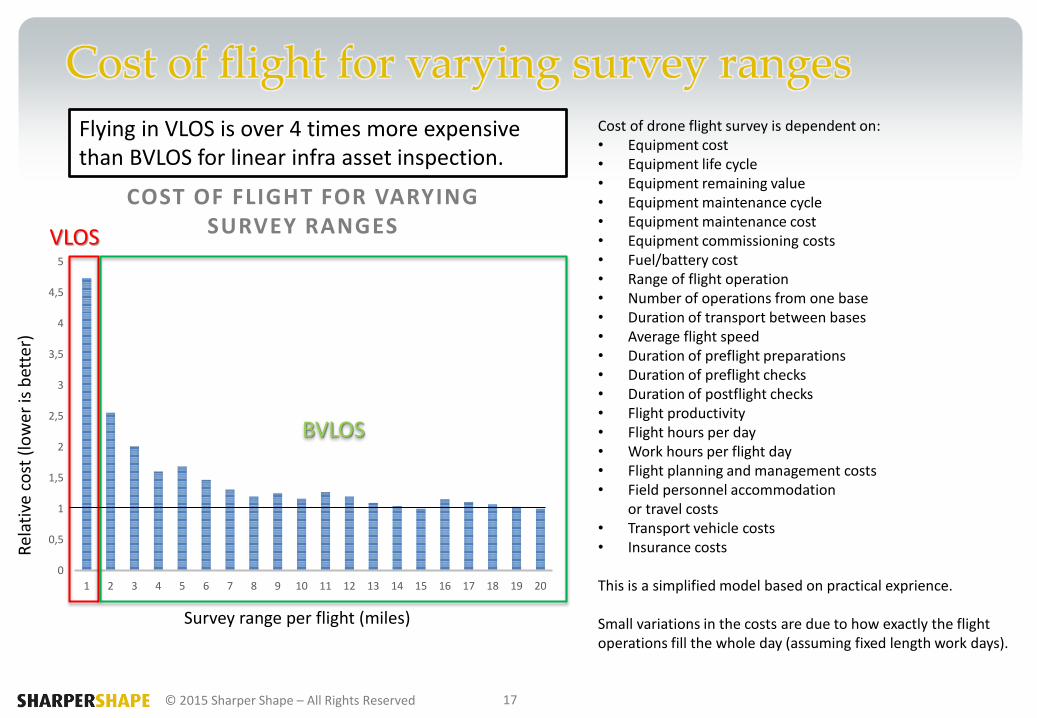

Cost of flight for varying survey ranges

0

0,5

1

1,5

2

2,5

3

3,5

4

4,5

5

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

COST OF FLIGHT FOR VARYING SURVEY RANGES

Survey range per flight (miles)

Rel

ativ

e co

st (

low

er is

bet

ter)

BVLOS

VLOS

Cost of drone flight survey is dependent on:• Equipment cost• Equipment life cycle• Equipment remaining value• Equipment maintenance cycle• Equipment maintenance cost• Equipment commissioning costs• Fuel/battery cost• Range of flight operation• Number of operations from one base• Duration of transport between bases• Average flight speed• Duration of preflight preparations• Duration of preflight checks• Duration of postflight checks• Flight productivity• Flight hours per day• Work hours per flight day• Flight planning and management costs• Field personnel accommodation

or travel costs• Transport vehicle costs• Insurance costs

This is a simplified model based on practical exprience.

Small variations in the costs are due to how exactly the flightoperations fill the whole day (assuming fixed length work days).

Flying in VLOS is over 4 times more expensive than BVLOS for linear infra asset inspection.

© 2015 Sharper Shape – All Rights Reserved 18

Elimination of barriers – open opportunities

Globallyharmonizedregulation

In progress: EU Commission, EASA, ICAO, JARUS, EU MS,FAA

Technology gaps

C2 links

Sense and Avoid

Consensuson the

concept of operations

NASA, Google, Amazon

Startups

(Aviation Industry)

The barriersare all interconnected.

Solutions need to beinterconnected.

Understanding themarket requiresinherently globalperspective.

Quick nationalimplementation of themissing pieces will givethe local industry trulyglobal advantage.

The opportunity for systemic innovation ona global scale requiresdecisive and harmonizedsteps throughout allregimes.

© 2015 Sharper Shape – All Rights Reserved 19

Finland’s advantages and opportunities

Unique BVLOS capabilities

Non-congested airspaceallows for flexibleairspace use

Excellent collaborationbetween the industryand authorities

Comparatively simplepolicy-makingenvironment

Well-established position in the relevantinternational and EU level rule-makingorganizations

Regulator and policy-makerscommitment to business

Wireless communication

Electronics, optoelectronics

Big data analytics, …

Aviation relatedindustries

Good base of relevant technologycompanies

No barriers to becomethe first to implementcomplete concept for integrated drone ops(ahead of globalprogress)

Needs to be aligned withthe global future trends

Requires tightparticipation in theinternational forums: to influence, align and follow

Potential for LE & SME & research collaboration

Needs to be supportedby the highest levelpolitical endorsement & allocation of resources

Opportunity to implement systemicinnovations

© 2015 Sharper Shape – All Rights Reserved 20

Proposal: Finland the first to adopt UAS Traffic Management (UTM)

In full alignment withthe global inititativessuch as NASA.

Safely enable civilianlow-altitude operationswithin 5 years in near-terms, and

Develop autonomousUAS traffic Management (UTM) to accommodatemassive scale traffic.

© 2015 Sharper Shape – All Rights Reserved 21

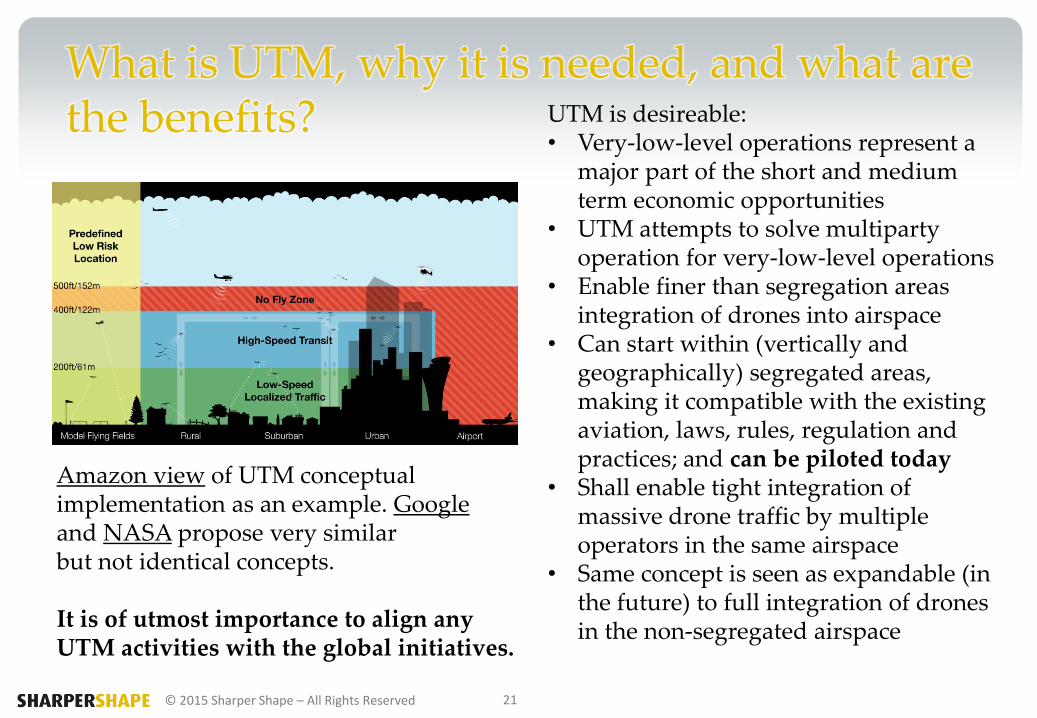

What is UTM, why it is needed, and what are the benefits? UTM is desireable:

• Very-low-level operations represent a major part of the short and medium term economic opportunities

• UTM attempts to solve multiparty operation for very-low-level operations

• Enable finer than segregation areasintegration of drones into airspace

• Can start within (vertically and geographically) segregated areas, making it compatible with the existingaviation, laws, rules, regulation and practices; and can be piloted today

• Shall enable tight integration of massive drone traffic by multipleoperators in the same airspace

• Same concept is seen as expandable (in the future) to full integration of dronesin the non-segregated airspace

Amazon view of UTM conceptualimplementation as an example. Googleand NASA propose very similarbut not identical concepts.

It is of utmost importance to align anyUTM activities with the global initiatives.

© 2015 Sharper Shape – All Rights Reserved 22

Roles and policy-making related to UTM

Political

Policy-making

Regulatory

Industry

Decide, endorse, and allocate resources.

Mandate and ensure the alignment of therelevant stakeholders. Remove legal barriersthough future law-setting.

Work together with the industry to implementregulatory and process framework to support theoperations. Set the framework and requirementsfor UTM operations. Ensure fair competitiveenvironment for UTM operators.

Implement, validate and operate UTM solutionsin a NON-MONOPOLISTIC arrangement.