Omaha, NE – Tax Executives Institute Baker & McKenzie Consulting LLC provides tax advisory and...

41

Omaha, NE – Tax Executives Institute Baker & McKenzie Consulting LLC provides tax advisory and economic services and does not provide legal advice or services. Baker & McKenzie LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker & McKenzie International, a Swiss Verein of member law firms around the world. In accordance with the common terminology used in professional service organizations, reference within the organization to a “partner” means a person who is a partner, or equivalent, in a member firm or its affiliate. Similarly, reference to an “office” means an office of the member firm or affiliate. State Income Tax Update January 20, 2008 J. Pat Powers [email protected] (650) 856-5526 John Paek [email protected] (212) 626-4232

-

Upload

jemimah-sanders -

Category

Documents

-

view

220 -

download

1

Transcript of Omaha, NE – Tax Executives Institute Baker & McKenzie Consulting LLC provides tax advisory and...

Omaha, NE – Tax Executives Institute

Baker & McKenzie Consulting LLC provides tax advisory and economic services and does not provide legal advice or services. Baker & McKenzie LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker & McKenzie International, a Swiss Verein of member law firms around the world. In accordance with the common terminology used in professional service organizations, reference within the organization to a “partner” means a person who is a partner, or equivalent, in a member firm or its affiliate. Similarly, reference to an “office” means an office of the member firm or affiliate.

State Income Tax Update

January 20, 2008

J. Pat [email protected](650) 856-5526

John [email protected](212) 626-4232

State Income Tax Update

©2009 Baker & McKenzie 2

Topics• California Update

• Massachusetts Update

• Related Party Transactions

State Income Tax Update

©2009 Baker & McKenzie 3

California Update

State Income Tax Update

©2009 Baker & McKenzie 4

California Update• Recent Legislation

• Dividends Received Deduction

• LLC Tax

• Treasury Receipts and Apportionment

• Hyatt Case – Audit Practices

• Sales/Use Tax Developments

• Budget Woes

State Income Tax Update

©2009 Baker & McKenzie 5

Recent Legislation• Net Operating Losses

• Substantial Understatement Penalty

• Estimated Tax Payment

State Income Tax Update

©2009 Baker & McKenzie 6

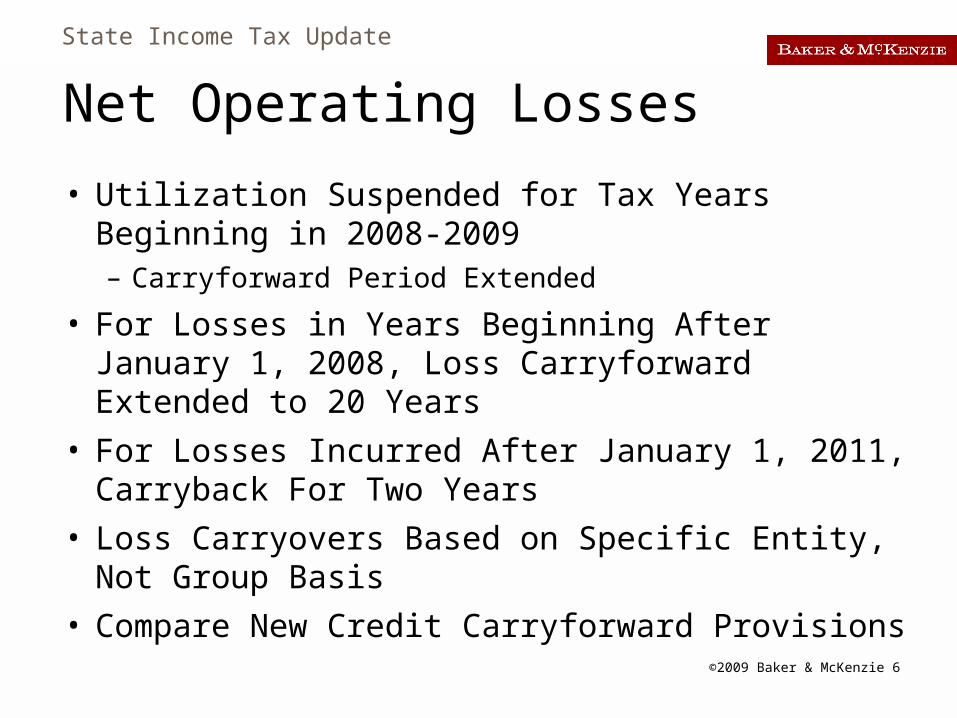

Net Operating Losses

• Utilization Suspended for Tax Years Beginning in 2008-2009– Carryforward Period Extended

• For Losses in Years Beginning After January 1, 2008, Loss Carryforward Extended to 20 Years

• For Losses Incurred After January 1, 2011, Carryback For Two Years

• Loss Carryovers Based on Specific Entity, Not Group Basis

• Compare New Credit Carryforward Provisions

State Income Tax Update

©2009 Baker & McKenzie 7

20% Substantial Understatement Penalty• For Understatement of $1 Million Determined on

Combined Group Basis– Automatic

– No-fault

– Applies to Years Beginning After January 1, 2003• Payment Before May 31, 2009 Relieves Penalty

– Taxpayer Dilemma

SFOIMAGE

State Income Tax Update

©2009 Baker & McKenzie 8

Estimated Tax Payment• Amounts of Estimated Payments Increased for

Both Corporations and Individuals

State Income Tax Update

©2009 Baker & McKenzie 9

Dividends Received Deduction (DRD)

• Dividends From Controlled Foreign Corporations– California Rev. & Tax. Code § 25106: Eliminate

Dividends From Income Included in Combined Report

– Background: Amdahl/Fujitsu Case (2004) Followed IRC § 959 on Previously Taxed Income

• Franchise Tax Board (FTB) Amended Regulation

• FTB and Board of Equalization Claimed That They Are Not Bound by Court of Appeal Decision in Amdahl/Fujitsu

• Apple Computer: Current Status

State Income Tax Update

©2009 Baker & McKenzie 10

Dividends From Unrelated Corporations

• Aftermath of Farmer Brothers

• Statutory Background– Rev. & Tax. Code § 24402: DRD for Dividends

Declared From Income Included in the Measure of Tax

• Farmer Brothers Struck Down Discrimination

• Abbott Laboratories Case– Is Discriminatory Provision Eliminated?

OR

– Is Entire Statute Gone?

State Income Tax Update

©2009 Baker & McKenzie 11

LLC Tax• As Originally Enacted, LLC “Fee” Was Based

On Gross Receipts Everywhere (Without Apportionment)

• LLC Tax Was Held To Violate Commerce Clause– Northwest Energetic

• FTB Pays Refunds to LLCs With No Receipts Apportioned to California

• Legislature Enacts Bill Apportioning Receipts, Purportedly On Retroactive Basis

State Income Tax Update

©2009 Baker & McKenzie 12

LLC Tax• Ventas Finance 1 LLC (2008): Court Limited

Refund As If Statute Provided Apportionment Formula

State Income Tax Update

©2009 Baker & McKenzie 13

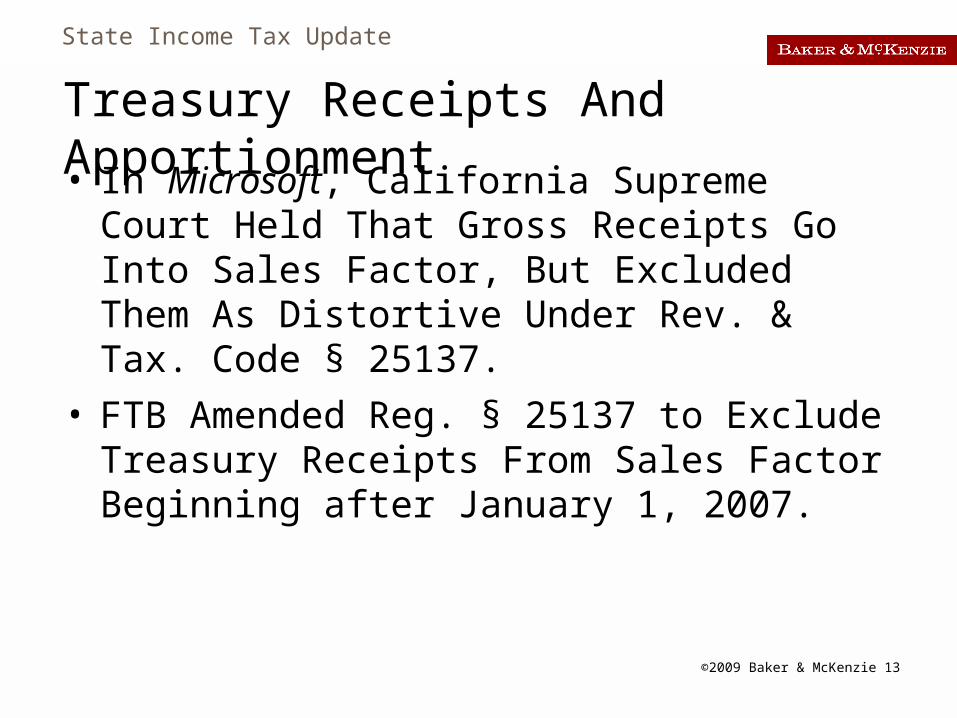

Treasury Receipts And Apportionment

• In Microsoft, California Supreme Court Held That Gross Receipts Go Into Sales Factor, But Excluded Them As Distortive Under Rev. & Tax. Code § 25137.

• FTB Amended Reg. § 25137 to Exclude Treasury Receipts From Sales Factor Beginning after January 1, 2007.

State Income Tax Update

©2009 Baker & McKenzie 14

Hyatt Case – Audit Practices• Hyatt v. FTB

– Las Vegas Jury Awarded Gilbert Hyatt $388 Million in Damages for Emotional Distress and Invasion of Privacy ($138 Million Compensatory and $250 Million Punitive)

– U.S. Supreme Court Ruled That Plaintiff Could Maintain Suit in Nevada Despite California Law Immunizing FTB From Tort Liability

– Abusive Audit Grew Out of Dispute as to When Mr. Hyatt Ceased to be California Resident

State Income Tax Update

©2009 Baker & McKenzie 15

Sales/Use Tax Developments• Dell Computer

• Patton Music

State Income Tax Update

©2009 Baker & McKenzie 16

Budget Woes• September 19, 2008 Budget Passed: Three

Months Late

• Budget Trailer Bills Enacted Without Adequate Review or Public Input

• Illusion of “Balanced Budget” Vanished Quickly

• Current: Deficit Projected Over Next 18 Months $42 Billion

• Political Problem Leading to Fiscal Disaster

State Income Tax Update

©2009 Baker & McKenzie 17

Massachusetts Update

State Income Tax Update

©2009 Baker & McKenzie 18

Overview• House Bill 4904 signed into law on July 3, 2008.

– Conformity to Federal Entity Classification Rules

– Combined Reporting Requirement• Shift from separate reporting jurisdiction to combined

reporting for unitary affiliates.

– Change in Public Law 86-272 Position

– Tax Rate Reductions

– Effective for tax years beginning on or after January 1, 2009.

State Income Tax Update

©2009 Baker & McKenzie 19

Entity Classification• As of 1/1/09, Massachusetts generally adopts

the federal “check-the-box” rules for entity classification.– Corrects historical disparity for Massachusetts

business trusts, S-corporation subsidiaries (QSubs), and certain partnerships

– Eliminates rules historically applicable to the taxation of Massachusetts business trusts

– Reclassifies non-conforming entities as of 1/1/09

State Income Tax Update

©2009 Baker & McKenzie 20

Reclassification Guidelines • Change from Partnership to Corporation

– Partnership deemed to contribute all its assets and liabilities to a new corporation.

– Then, partnership is deemed to liquidate and distribute the stock of the corporation to its partners.

• Change from Corporation to Partnership– Corporation deemed to liquidate and make

distribution to its shareholders.• Massachusetts gain may exist upon liquidation,

despite being a federal non-event.– Then, the shareholders are deemed to contribute

those assets and liabilities to the new partnership.

State Income Tax Update

©2009 Baker & McKenzie 21

Reclassification Guidelines

• Change from Corporate Trust to Corporation– Treated generally as a tax-free reorganization.

• Shareholders’ basis in stock shares is the same as in the former trust, except for a reduction for all “tax-free” earnings and profits of the former corporate trust that have not been previously taxed to the former trust or the shareholders.

• Change from Corporate Trust to Partnership– Treated as a tax-free reorganization.

• All “tax-free” earnings and profits of the former corporate trust must be taxable as dividend income to partners on first return after conversion.

State Income Tax Update

©2009 Baker & McKenzie 22

Reclassification Guidelines

• Change from Corporation to Disregarded Entity– Corporation deemed to liquidate and distribute all assets and

liabilities to shareholder.

– Massachusetts gain may exist upon liquidation, despite being a federal non-event.

• Change from Corporate Trust to Disregarded Entity– Corporate trust deemed to have liquidated.

– Generally no recognition of gain or loss; however, tax-free earnings and profits of the former trust must be recognized as taxable dividend income to the owner.

State Income Tax Update

©2009 Baker & McKenzie 23

Combined Reporting – Composition of Combined Group

• Unitary Business Principle– The term “unitary business” shall mean the activities of a group

of 2 or more corporations

• Under common ownership (50%)

• Sufficiently interdependent, integrated or interrelated through their activities so as to provide mutual benefit

• Producing a significant sharing or exchange of value among them or a significant flow of value between the separate parts.

– The term “unitary business” shall be construed to the broadest extent permitted under the United States Constitution.

State Income Tax Update

©2009 Baker & McKenzie 24

Combined Reporting – Composition of Combined Group

• Corporations – Group includes C corporations, S corporations, utility

corporations, financial institutions, REITs, RICs, and certain captive insurance companies.

• Security corporations, non-profits, and insurance companies will generally not be included.

• Partnerships– Any business conducted by a partnership will be treated as the

business of the partners.

• To the extent of the partner’s distributive share of the partnership’s income

State Income Tax Update

©2009 Baker & McKenzie 25

Combined Reporting – Composition of Combined Group

• “Water’s edge” reporting required unless an election is made to the contrary.

• “Water’s edge” report includes:– Corporations incorporated in the U.S.;

– Corporations incorporated outside the U.S., if the average of the property, payroll, and sales factors within the U.S. is 20 percent or more; and

– Corporations that earn “more than 20 percent of its income, directly or indirectly, from intangible property or service-related activities, the costs of which generally are deductible for federal income tax purposes,… but only to the extent of that income and the apportionment factors related thereto.”

State Income Tax Update

©2009 Baker & McKenzie 26

Combined Reporting – Alternatives to Water’s Edge Reporting• Worldwide Election

– Includes all corporations in the unitary group

• Affiliated Group Election– “Limits” the combined group to the federal affiliated group as

defined in IRC 1504, except it:• Includes corporations regardless of place of incorporation• Uses a 50% voting common ownership threshold (rather

than 80% vote and value)• Measures common ownership using the water’s edge group

– Group income is apportionable; no allocable income.

• Elections cannot be in effect simultaneously – Elections must be made on a timely-filed, original return– Binding for 10 years

State Income Tax Update

©2009 Baker & McKenzie 27

Combined Reporting - Mechanics

• Calculation of Group Tax Base– To be addressed in regulations:

• Elimination of intercompany transactions

• Treatment of net operating losses and credits

• Addback rules

– Working Draft of 830 CMR 63.32B.1 was issued for public comment on 11/6/2008

State Income Tax Update

©2009 Baker & McKenzie 28

Apportionment Mechanics• Apportionment Methodology

– Each member required to use its applicable apportionment formula

• Consider formulas applicable to general corporations, manufacturing corporations, financial institutions.

– Sales of non-taxable members attributed to taxable members

• Sales of non-taxable members attributed by ratio of taxable member Massachusetts sales to total Massachusetts sales of all taxable members.

– Sales factor uses a Finnigan approach

• Taxable member sales not subject to throwback where any group member has nexus with destination state.

State Income Tax Update

©2009 Baker & McKenzie 29

FAS 109 Deduction

• For any increase in a “net deferred tax liability” as a result of combined reporting

• Pro-rated over seven years starting in 2012

• Only available for public companies

• Must file statement with DOR by July 1, 2009, specifying the total amount of the deduction to be claimed

State Income Tax Update

©2009 Baker & McKenzie 30

Public Law 86-272• P.L. 86-272 generally prohibits states from

imposing income tax on entities whose business in the state is limited to the solicitation of sales of tangible personal property.

• As of 1/1/09, P.L. 86-272 does not protect taxpayers from the non-income measure of the Massachusetts corporate excise.– Massachusetts historically took the position that this

protection extended to the non-income measure of the corporate excise.

State Income Tax Update

©2009 Baker & McKenzie 31

Rate Reduction• Corporate excise rate (Net income measure) of

9.5% applicable to business corporations (other than S corporations) will be gradually reduced over three years to 8.0%.

• Financial institution excise rate of 10.5% will be gradually reduced over three years to 9.0%.

State Income Tax Update

©2009 Baker & McKenzie 32

Related Party Transactions

State Income Tax Update

©2009 Baker & McKenzie 33

Related Party Transactions• Combined/Unitary Reporting

• Statutory Intercompany Expense Add Backs

• Economic Nexus

State Income Tax Update

©2009 Baker & McKenzie 34

Combined/Unitary Reporting• Massachusetts: Effective January 1, 2009

• West Virginia: Effective January 1, 2009

• New York: Effective January 1, 2007

• Vermont: Effective January 1, 2008

State Income Tax Update

©2009 Baker & McKenzie 35

Statutory Intercompany Expense Add Backs• Alabama: VFJ Ventures, Inc. and Statutory

Change

• Ohio: Family Dollar Stores of Ohio

• Tennessee: Disclosure Statement and 50% Penalties

State Income Tax Update

©2009 Baker & McKenzie 36

Statutory Intercompany Expense Add Backs• Michigan

• Minnesota

• Rhode Island

• Wisconsin

State Income Tax Update

©2009 Baker & McKenzie 37

Adjustments to Economic Nexus• U.S. Supreme Court Developments

– West Virginia: MBNA American Bank, cert., Petition Denied

– New Jersey: Lanco, Inc., cert., Petition Denied

• Where Do We Go From Here?

State Income Tax Update

©2009 Baker & McKenzie 38

Adjustments to Economic Nexus• Louisiana: Geoffrey

• Maryland: Chicago Classics

• Alabama: Graduate Supply House

• New Jersey: Praxair

• Massachusetts: Capital One; Geoffrey

• New York: “Amazon” Law

State Income Tax Update

©2009 Baker & McKenzie 39

Adjustments to Formulary Apportionment• Trend Towards Single Sales Factor

• Sourcing Service Revenue: Cost Of Performance Versus Market-Based Sourcing

• Throw-Out Rule: New Jersey– Status Of Litigation

– Repealed July 1, 2010

State Income Tax Update

©2009 Baker & McKenzie 40

Other Developments• “Captive” REITS

– North Carolina: Wal-Mart Stores

– Massachusetts: Fleet Funding

• Disallowance of Dividends Paid Deductions

• Business/Non Business Income– MeadWestvaco v. Illinois

• Davis v. Kentucky– Sequel to Cuno v. DaimlerChrysler

– Implications for State Credits

Omaha, NE – Tax Executives Institute

Baker & McKenzie Consulting LLC provides tax advisory and economic services and does not provide legal advice or services. Baker & McKenzie LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker & McKenzie International, a Swiss Verein of member law firms around the world. In accordance with the common terminology used in professional service organizations, reference within the organization to a “partner” means a person who is a partner, or equivalent, in a member firm or its affiliate. Similarly, reference to an “office” means an office of the member firm or affiliate.

State Income Tax Update

January 20, 2008

J. Pat [email protected](650) 856-5526

John [email protected](212) 626-4232