Ole Beier Sørensen Chief of analysis, Strategy and SRI [email protected] Keep your eyes on the ball -...

25

Ole Beier Sørensen Chief of analysis, Strategy and SRI [email protected] Keep your eyes on the ball - design, cost and risk Good pensions at best possible costs - towards a well-funtioning pension market? FAFO, Oslo 11 February 2009

-

Upload

amice-townsend -

Category

Documents

-

view

214 -

download

0

Transcript of Ole Beier Sørensen Chief of analysis, Strategy and SRI [email protected] Keep your eyes on the ball -...

Ole Beier SørensenChief of analysis, Strategy and [email protected]

Keep your eyes on the ball- design, cost and risk

Good pensions at best possible costs- towards a well-funtioning pension market?FAFO, Oslo11 February 2009

www.atp.dk 2

The rating of the industry is not impressive….

Source: Danish National Consumers Agency, 2008

Consumerconfidence

Trans-parency

Complaintsaccess

Index 2007

Index 2006

Index 2005

Charter travel 10 2 17 1 2 2Entertainment 2 3 37 2 4 3Air travel 21 9 21 8 3 14Funeral services 4 41 2 17 26 5Driving instructors 23 31 30 27 15 8Real estate agents 42 35 7 32 39 43Pharmaceuticals 12 46 45 43 46 50Pension providers 43 50 19 44 48 48

Lotteries & casinos 33 21 47 46 44 34Cosmetics 44 30 49 50 50 47Auto repair shops 46 44 51 51 51 51

The Danish Consumer Relationships Index 2007 - 51 industries

www.atp.dk 3

…reflecting a notoriously bad reputation…

A closed and introvert industry

Products nobody understands

Complex and very technical information

“Credible advisors are hard to find!”

www.atp.dk 4

…but it is nevertheless sadly astonishing!...

Currently app. € 300 bio. – and counting

12-21 pct. of wages

The largest and most important financial transaction for

most households

A low interest area

Recent survey by F&P:

- “People know they are paying…

- …but they only have faint ideas as to what they get”

www.atp.dk 5

…and it may call for government intervention

Strong pressure on the industry to inform…

…and to increase the quality of its’ information

Politicians:

- ”If the industry does not succeed, government may become helpfull”

A new industry initiative based on a look through principle

is to enhance transparency

- administration costs

- investment costs

www.atp.dk 6

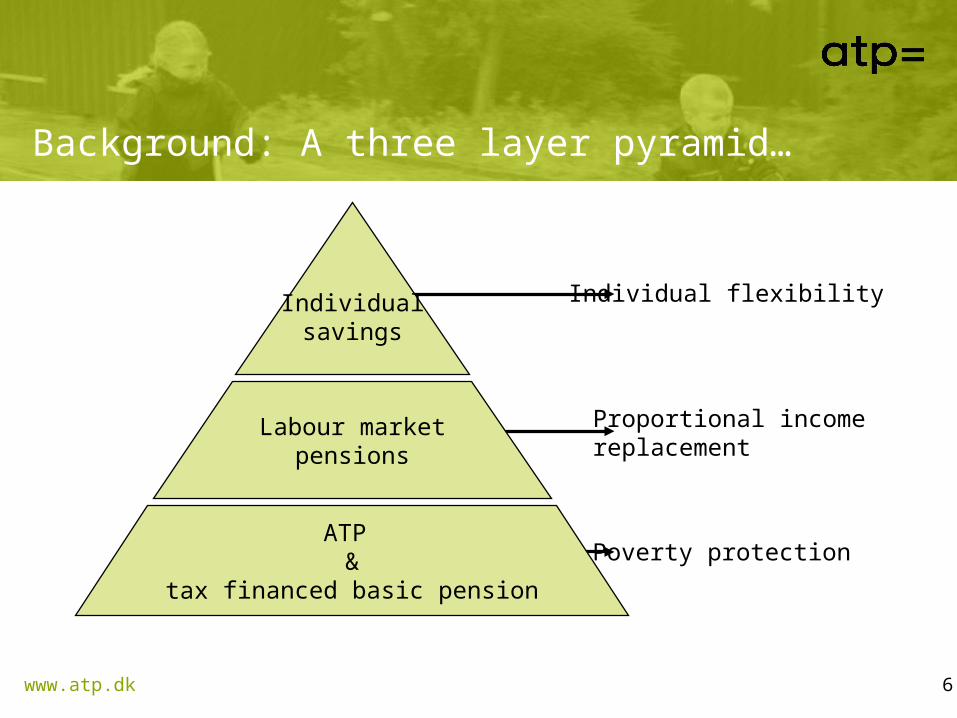

Background: A three layer pyramid…

Individualsavings

ATP &

tax financed basic pension

Labour marketpensions

Poverty protection

Proportional income replacement

Individual flexibility

www.atp.dk 7

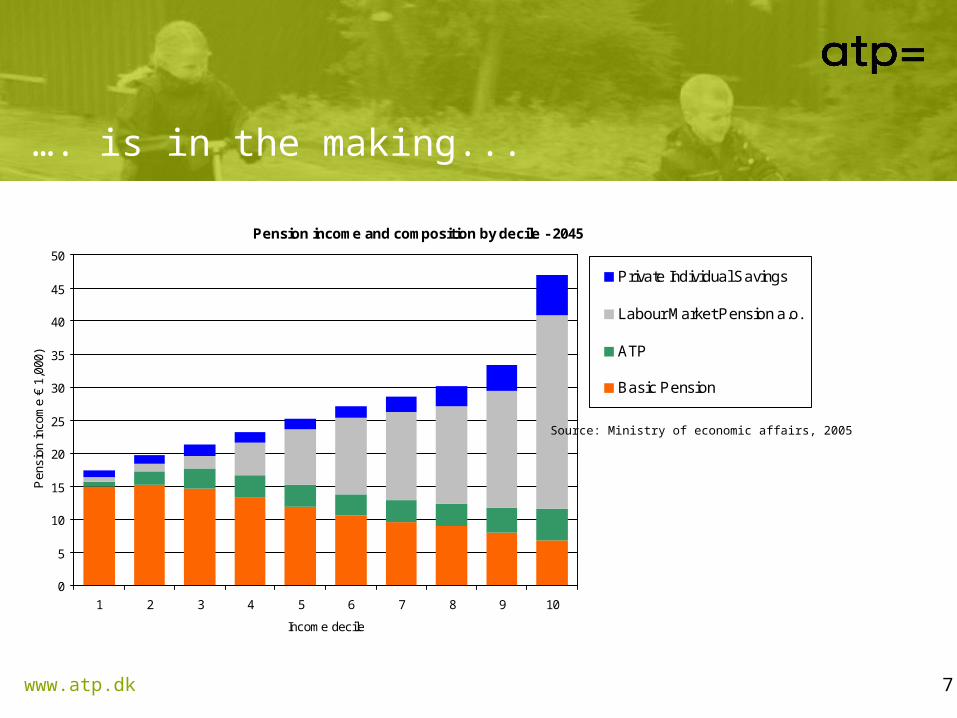

…. is in the making...

Pension income and composition by decile - 2045

0

5

10

15

20

25

30

35

40

45

50

1 2 3 4 5 6 7 8 9 10

Income decile

Pen

sion

inco

me

€ 1,

000)

Private Individual Savings

Labour Market Pension a.o.

ATP

Basic Pension

Source: Ministry of economic affairs, 2005

www.atp.dk 8

… driven by labour market schemes

Mostly industry wide schemes set up by the social

partners

Outside general collective agreements similar

schemes may be set up at company level

App. 80 pct. of all pension contributions are

compulsory…

… and they are collected by pension providers

designated by the social partnes

www.atp.dk 9

Administration costs vary greatly

Administration cost per member 2007 (€)

0

50

100

150

200

250

300

FSP

Norde

aPFA AP

Danica

Bankp

ensio

n

Avera

geJØ

PDIP M

P LP

PenSam PBU KP

Pensio

nDan

mar

k

PKA IPATP

www.atp.dk 10

Simple products => lower costs – and vice versa

”Higher costs reflects more complex products and the

access to individual advise”

- product complexity drives cost while customer demand demand and need is questionable

”Higher cost levels in the commercial sector reflect

marketing costs”

- the market is almost saturated – at least as far as attractive segments are concerned -…

- hence, market shares can almost only be won by aquisition and by selling-up on existing clients

www.atp.dk 11

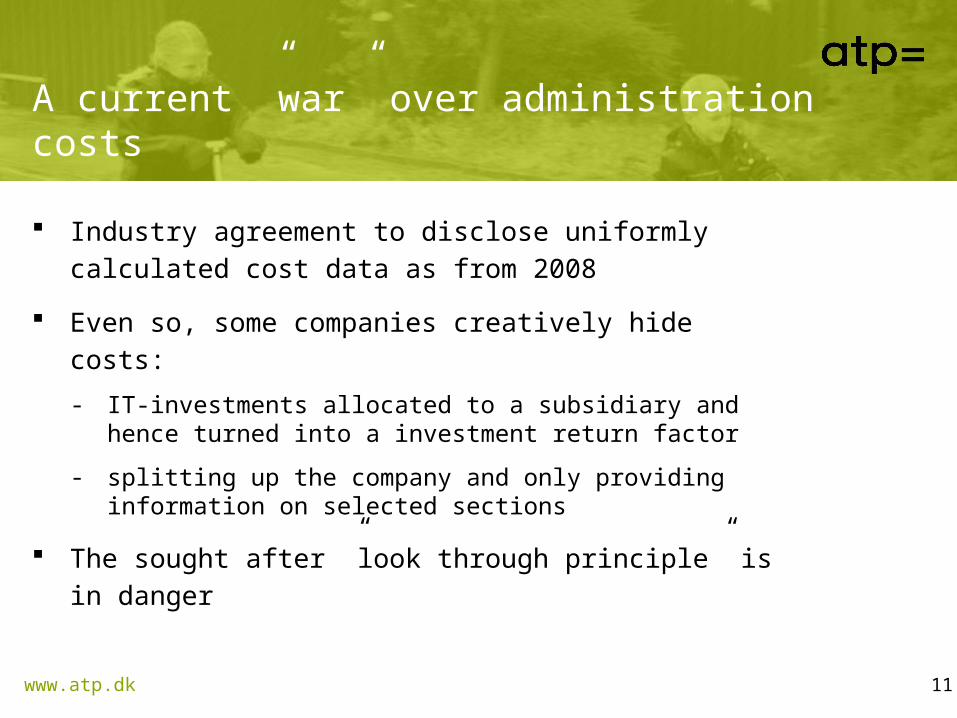

A current ”war” over administration costs

Industry agreement to disclose uniformly calculated cost

data as from 2008

Even so, some companies creatively hide costs:

- IT-investments allocated to a subsidiary and hence turned into a investment return factor

- splitting up the company and only providing information on selected sections

The sought after ”look through principle” is in danger

www.atp.dk 12

Operational prices: Instructive examples

Traditional standard letter: € 1,5

Electronically distributed standard letter: € 0,15

Individual letter: ??

Receiving a phone call (call center): € 1.2 per minute

Face to face counceling: ??

Payment by bank transfer: € 0.1 per transfer

Payment by check: € 4 per transfer

www.atp.dk 13

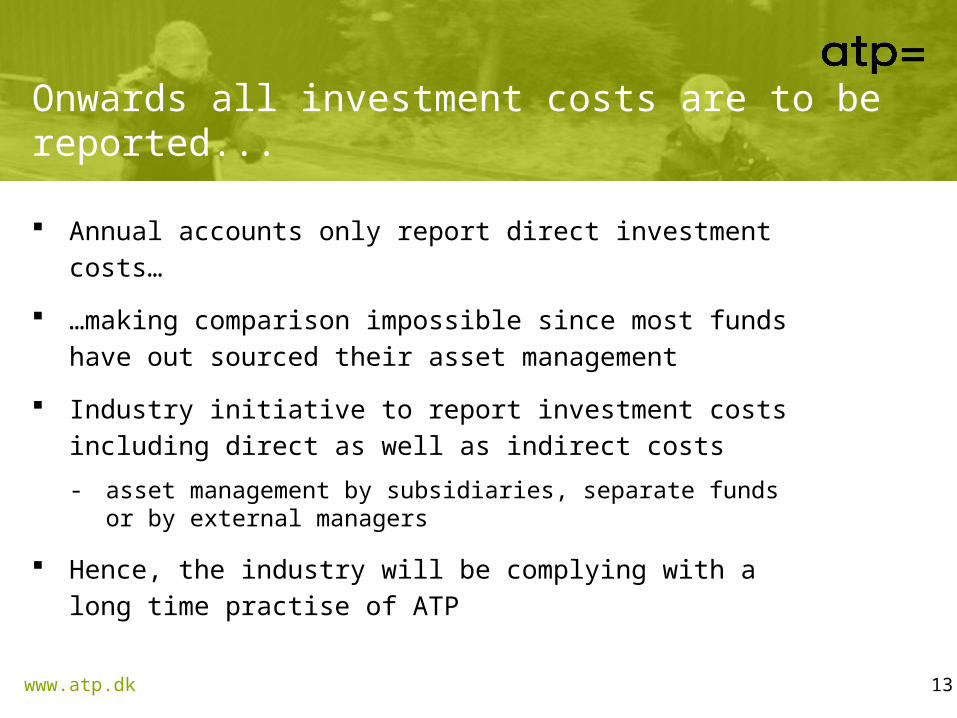

Onwards all investment costs are to be reported...

Annual accounts only report direct investment costs…

…making comparison impossible since most funds have out

sourced their asset management

Industry initiative to report investment costs including direct

as well as indirect costs

- asset management by subsidiaries, separate funds or by external managers

Hence, the industry will be complying with a long time

practise of ATP

www.atp.dk 14

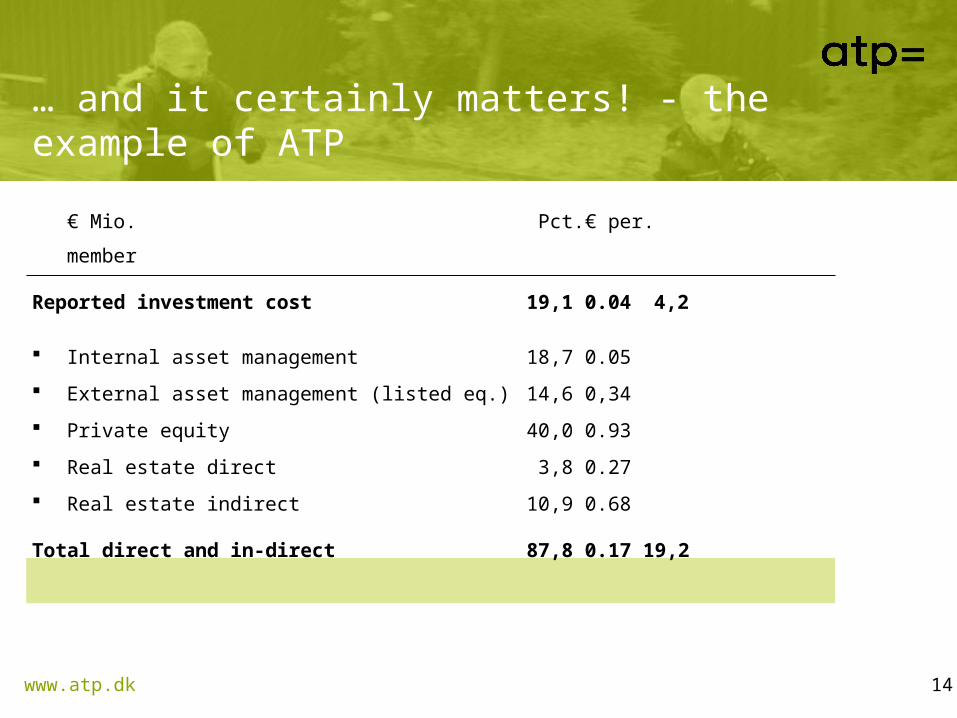

… and it certainly matters! - the example of ATP

€ Mio. Pct. € per.

member

Reported investment cost 19,1 0.04 4,2

Internal asset management 18,7 0.05

External asset management (listed eq.) 14,6 0,34

Private equity 40,0 0.93

Real estate direct 3,8 0.27

Real estate indirect 10,9 0.68

Total direct and in-direct 87,8 0.17 19,2

www.atp.dk 15

Few things can be said with some certainty…

Size matters greatly to investment costs…

…and so does implementation style

- ATP is app. 30 pct. below peer group level

Cost levels and return levels do not correllate…

…if they do it is probably a negative one

www.atp.dk 16

…and economies of scale matter more than ever

New regulatory demands and new client demands put

smaller funds under pressure

- e.g. asset management is increasingly being outsourced

Formation of joint administration operations

Market consolidation in the longer term?

www.atp.dk 17

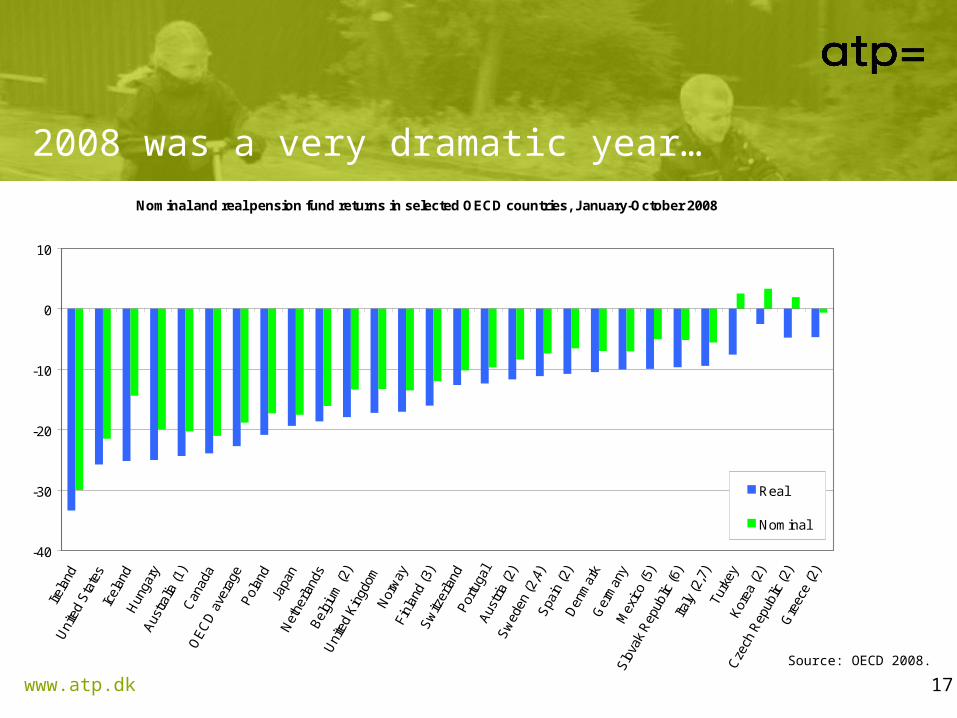

2008 was a very dramatic year…

Nominal and real pension fund returns in selected OECD countries, January-October 2008

-40

-30

-20

-10

0

10

Irela

ndU

nite

d S

tate

sIc

elan

dH

unga

ryA

ustra

lia (1

)C

anad

aO

EC

D a

vera

geP

olan

dJa

pan

Net

herla

nds

Bel

gium

(2)

Uni

ted

Kin

gdom

Nor

way

Finl

and

(3)

Sw

itzer

land

Por

tuga

lA

ustri

a (2

)S

wed

en (2

,4)

Spa

in (2

)D

enm

ark

Ger

man

yM

exic

o (5

)

Slo

vak

Rep

ublic

(6)

Italy

(2,7

)Tu

rkey

Kor

ea (2

)

Cze

ch R

epub

lic (2

)G

reec

e (2

)

Real

Nominal

Source: OECD 2008.

www.atp.dk 18

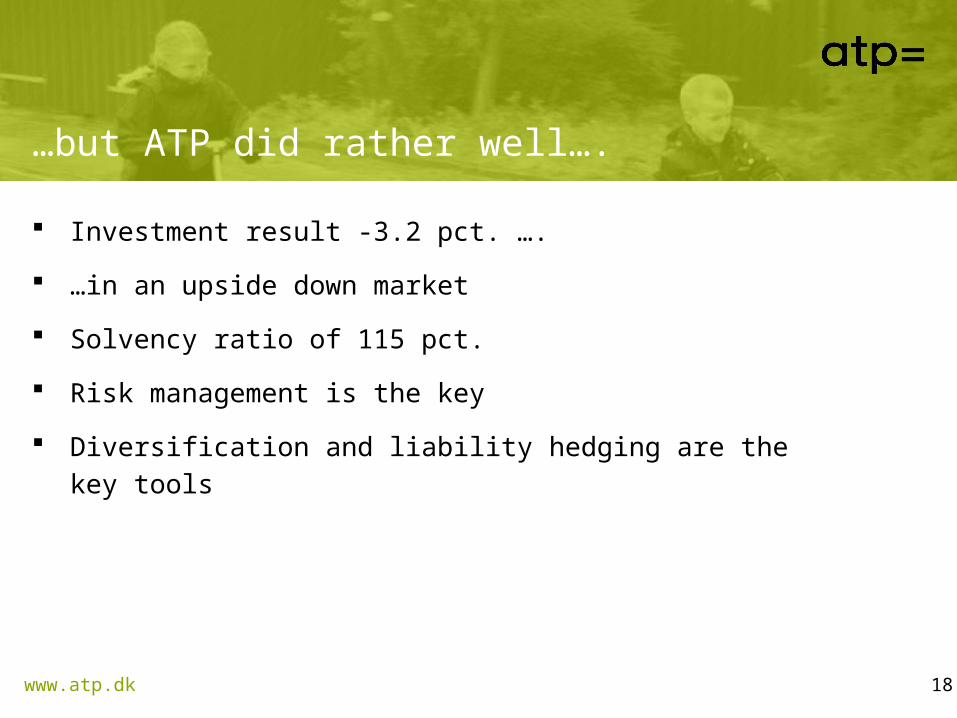

…but ATP did rather well….

Investment result -3.2 pct. ….

…in an upside down market

Solvency ratio of 115 pct.

Risk management is the key

Diversification and liability hedging are the key tools

www.atp.dk 19

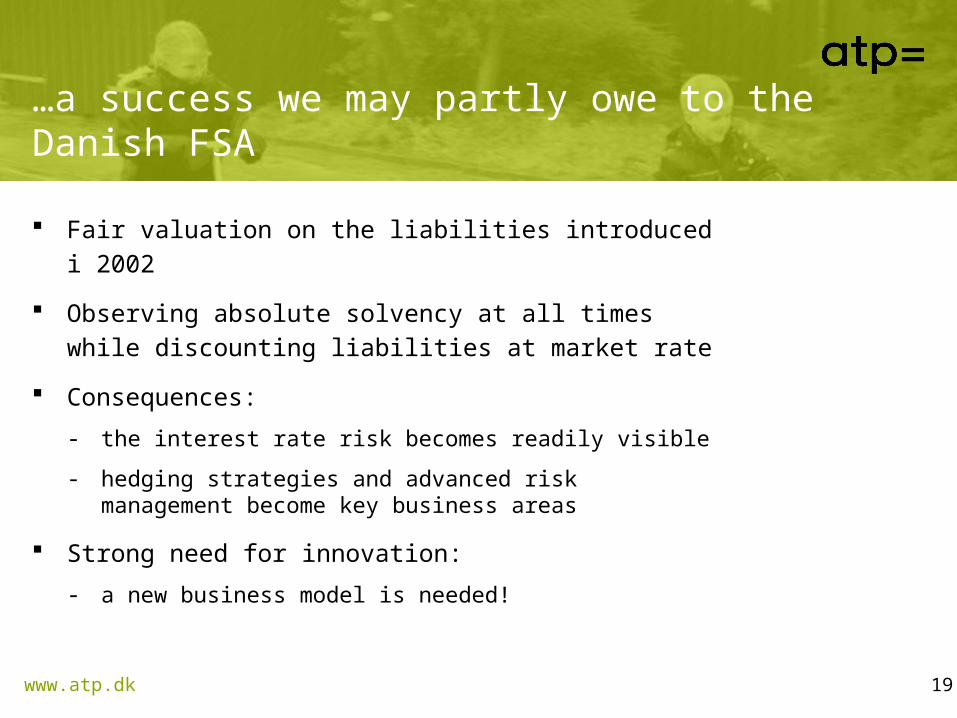

…a success we may partly owe to the Danish FSA

Fair valuation on the liabilities introduced i 2002

Observing absolute solvency at all times while

discounting liabilities at market rate

Consequences:

- the interest rate risk becomes readily visible

- hedging strategies and advanced risk management become key business areas

Strong need for innovation:

- a new business model is needed!

www.atp.dk 20

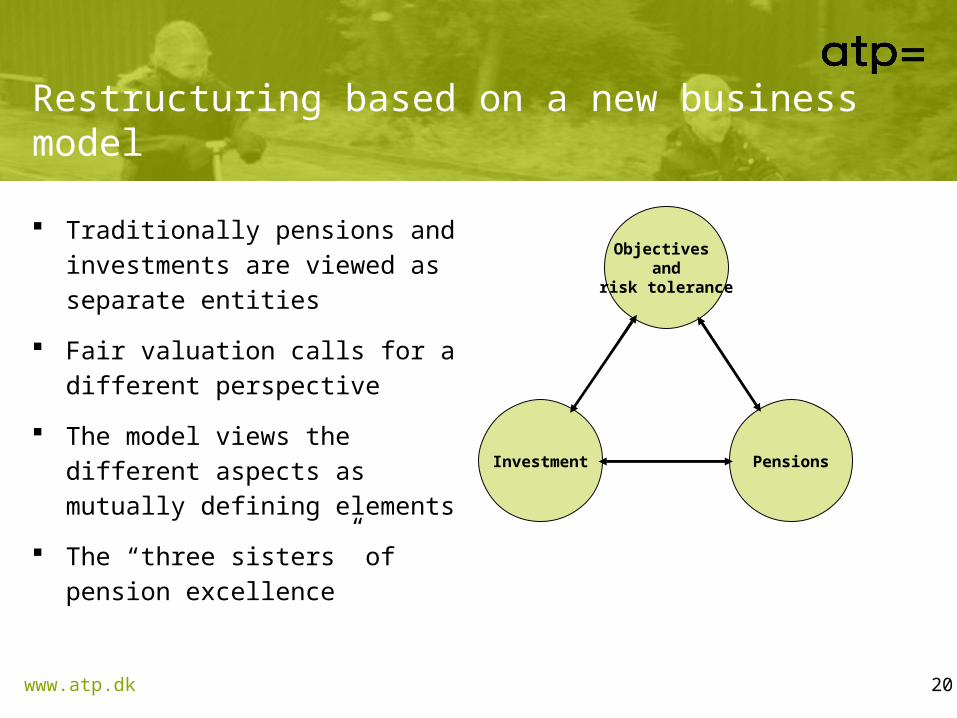

Restructuring based on a new business model

Traditionally pensions and

investments are viewed as

separate entities

Fair valuation calls for a different

perspective

The model views the different

aspects as mutually defining

elements

The “three sisters” of pension

excellence

Objectives and

risk tolerance

PensionsInvestment

www.atp.dk 21

0%

5%

10%

15%

20%

25%

30%

35%

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

after-tax interest rate match

risk

of c

ompa

ny e

xper

ienc

ing

inso

lven

cy

25% equity 45% equity 65% equity

Fair valuation: Explicit need for a new strategy

Q3 ’01

Q4 ’01

Q1 ’03

Q1 ’04Q3 ’02

Q1 ’02

3Q 2001

www.atp.dk 22

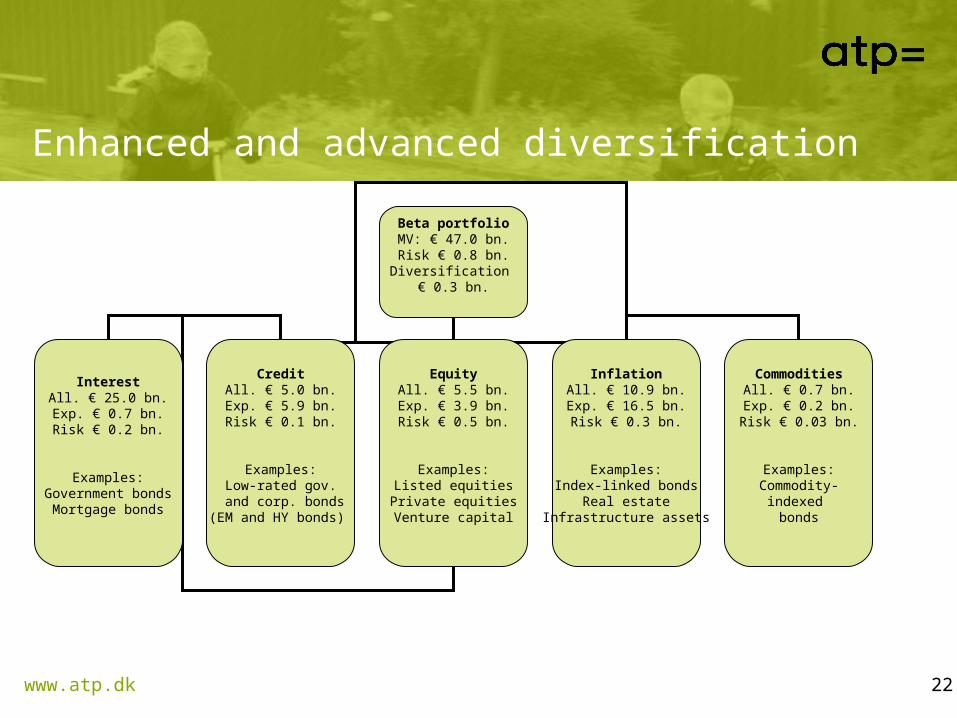

Enhanced and advanced diversification

Beta portfolioMV: € 47.0 bn.Risk € 0.8 bn.Diversification

€ 0.3 bn.

InterestAll. € 25.0 bn.Exp. € 0.7 bn.Risk € 0.2 bn.

Examples:Government bonds

Mortgage bonds

CreditAll. € 5.0 bn.

Exp. € 5.9 bn.Risk € 0.1 bn.

Examples:Low-rated gov.

and corp. bonds(EM and HY bonds)

EquityAll. € 5.5 bn.

Exp. € 3.9 bn.Risk € 0.5 bn.

Examples:Listed equitiesPrivate equitiesVenture capital

InflationAll. € 10.9 bn.

Exp. € 16.5 bn.Risk € 0.3 bn.

Examples:Index-linked bonds

Real estateInfrastructure assets

CommoditiesAll. € 0.7 bn.

Exp. € 0.2 bn.Risk € 0.03 bn.

Examples:Commodity-

indexed bonds

www.atp.dk 23

New pension model

Incoming contributions are split in two:

- a bonus contribution of 20 pct.

- a guarantee contribution of 80 pct.

The latter is used to buy new guaranteed pension rights…

… while the former is transferred to ATPs bonus potential

- the bonus potential serves as an investment buffer allowing ATP to pursue a return seeking investment strategy

- it returns to the membership by way of future indexations

The bonus contribution is a “payment for future indexations”

www.atp.dk 24

Better pensions

www.atp.dk 25

Shifting risk onto individuals?

The ATP strategy is slightly unique

Strong provider-driven drive towards ”market products”

- traditional preference for guaranteed products – DC-based defereed annuities is to some extent abandoned

- investment risk and longevity risks are shifted onto the individual

Disturbing,..?

- there are strong alternatives allowing return seeking investment strategies and guarantees to co-exist

Keep your eyes on the ball!