Office Network of Tvs Lucas

102

OFFICE NETWORK OF TVS LUCAS Lucas-TVS provides quality service to its customers with a comprehensive distribution and service network. The company reaches out to its customers, vehicle manufacturers as well as vehicle users, through a network of 100 branches spread throughout the country. The secret of Lucas-TVS' excellent services lies in its ability to respond to changing customer needs swiftly, effectively and consistently. An in-depth training programmed has been developed to provide effective after-market service to customers. This has led to increased appreciation of the commitment of Lucas- TVS to do service and support the end users. I would like to take this opportunity to thank all the people who helped me in completion of my management training and in the completion of this report. I would sincere thanks to Mr. Pradeep khaneja (Manager- Finance and Accounts Department) for providing me guidance at each and every step of the training. I would always be obliged to him because he shared his real-life experiences with me. I am thankful to the other members of the finance department who explained me finance work, solving queries and being there to help me whenever required Project Training is an important part of each management course. These studies cover what is left uncovered in the theoretical gamut. It exposes a student to valuable treasure of experience. My project is about µA study of Accounts Receivables Management in TVS Lucas.¶ The purpose of this project is to analyze the important dimensions of the efficient management of receivables within the framework of a firm¶s objectives of value maximisation. When a firm makes an ordinary sale of goods and services and does not receive payment, the firm grants trade credit and creates accounts receivable which would be collected in future. Thus, accounts receivabl e represent an extension of credit to customers, allowing them a reasonable period of time, in which to pay for the goods/services which they have received. It is an essential marketing tool, acting as a bridge for the movement of goods through production and distribution stages to

-

Upload

karnna-patil -

Category

Documents

-

view

227 -

download

0

Transcript of Office Network of Tvs Lucas

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 1/102

OFFICE NETWORK OF TVS LUCAS

Lucas-TVS provides quality service to its customers with a comprehensive distribution

and service network. The company reaches out to its customers, vehicle manufacturers aswell as vehicle users, through a network of 100 branches spread throughout the country.

The secret of Lucas-TVS' excellent services lies in its ability to respond to changing

customer needs swiftly, effectively and consistently.

An in-depth training programmed has been developed to provide effective after-market

service to customers. This has led to increased appreciation of the commitment of Lucas-

TVS to do service and support the end users.

I would like to take this opportunity to thank all the people who helped me in completion of my

management training and in the completion of this report.

I would sincere thanks to Mr. Pradeep khaneja (Manager- Finance andAccounts Department) for providing me guidance at each and every step of the training. I would always be obliged to him because he shared his real-lifeexperiences with me.

I am thankful to the other members of the finance department who explained me finance work,

solving queries and being there to help me whenever required

Project Training is an important part of each management course. These studies cover what is left

uncovered in the theoretical gamut. It exposes a student to valuable treasure of experience. My

project is about µA study of Accounts Receivables Management in TVS Lucas.¶

The purpose of this project is to analyze the important dimensions of the efficient

management of receivables within the framework of a firm¶s objectives of value maximisation.

When a firm makes an ordinary sale of goods and services and does not receive payment, the

firm grants trade credit and creates accounts receivable which would be collected in future. Thus,

accounts receivable represent an extension of credit to customers, allowing them a reasonable period

of time, in which to pay for the goods/services which they have received. It is an essential marketing

tool, acting as a bridge for the movement of goods through production and distribution stages to

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 2/102

customers. A firm grants trade credit to protect its sales from the competitors and to attract the

potential customers to buy its products at favourable terms.

The management of receivables involves crucial decision in threeareas : (i) credit policies, (ii) credit terms, and (iii) collection policies.

The credit policy of a firm provides the framework to determine whether or not to extend

credit to a customer and how much credit to extend. The two broad dimensions of credit policy

decision of a firm are credit standards and credit analysis. The term credit standards, represents the

basic criterion for the extension of credit to customers. The criterion and, therefore, standards can be

tight/restrictive or liberal/non-restrictive. The credit analysis component of credit policies includes

obtaining credit information from different sources and its analysis.

The second decision area in receivables management is the credit terms. The credit terms specify he

repayment terms, comprising credit period, cash discount, if any, and cash discount period.

The third area involved in the management of receivables is collection policies. It refers to the procedures followed to collect accounts receivable

when they become due. The two relevant aspects are the degree of efforts tocollect the overdues and the type of collection effort.

The framework of analysis of all the three decision areas in receivables management is to

secure a trade-off between the costs and benefits of the measurable effects on the sales volume,

capital cost due to change in accounts receivable, collection costs, bad debt, and so on. The

alternative will be selected when the benefits exceed the costs.

Receivable constitutes a substantial portion of current assets of several firms. For example, in

India, trade debtors, after inventories, are the major components of current assets. They form about

one-third of current assets in India. Granting credit and creating debtors amount to the blocking of

firm¶s funds. The interval between the date of sale and the date of payment has to be financed out of

working capital. This necessitates the firm to get funds from banks or other sources. Thus, trade

debtors represent investment. As substantial amounts are tied-up in trade debtors, it needs careful

analysis and proper management.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 3/102

OBJE

CTIV

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 4/102

ES

OF

ACC

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 5/102

OUN

TS

RECE

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 6/102

IVAB

LES

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 7/102

MAN

AGE

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 8/102

MEN

T

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 9/102

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 10/102

bles isdefinedas µdebt

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 11/102

ownedto thefirm by

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 12/102

customersarising

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 13/102

fromsale of goods

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 14/102

or servicesin the

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 15/102

ordinar ycourse

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 16/102

of business¶.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 17/102

When afirmmakes

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 18/102

anordinar y sale

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 19/102

of goodsor

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 20/102

servicesanddoes

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 21/102

notreceive paymen

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 22/102

t, thefirmgrants

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 23/102

tradecreditand

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 24/102

createsaccounts

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 25/102

receiva blewhich

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 26/102

could becollecte

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 27/102

d in thefuture.Receiva

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 28/102

blesmanagement is

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 29/102

alsocalledtrade

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 30/102

creditmanagement.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 31/102

Thus,accounts

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 32/102

receiva blereprese

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 33/102

nt anextension of

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 34/102

credit tocustomers,

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 35/102

allowing thema

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 36/102

reasona ble period

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 37/102

of timeinwhich

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 38/102

to payfor thegoods

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 39/102

received.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 40/102

Thesale of goods

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 41/102

oncredit isan

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 42/102

essential part of the

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 43/102

moderncompetitive

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 44/102

economicsystems

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 45/102

. Infact,credit

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 46/102

salesand,therefor

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 47/102

e,receiva bles,

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 48/102

aretreatedas a

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 49/102

marketing toolto aid

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 50/102

the saleof goods.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 51/102

Thecreditsales

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 52/102

aregenerally

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 53/102

madeon openaccount

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 54/102

in thesensethat

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 55/102

thereare noformal

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 56/102

acknowledgements of

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 57/102

debtobligations

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 58/102

throughafinancia

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 59/102

linstrument. As

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 60/102

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 61/102

they areintended to

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 62/102

promote salesand

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 63/102

thereby profits.Howev

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 64/102

er,extension of

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 65/102

creditinvolves risk

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 66/102

andcost.Manage

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 67/102

mentshouldweigh

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 68/102

the benefitsas well

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 69/102

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 70/102

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 71/102

blesmanagement.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 72/102

Theobjective of

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 73/102

receiva blesmanage

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 74/102

ment isµto promot

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 75/102

e salesand profits

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 76/102

untilthat point is

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 77/102

reachedwherethe

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 78/102

returnoninvestm

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 79/102

ent infurther funding

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 80/102

receiva bles isless

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 81/102

than thecost of funds

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 82/102

raisedtofinance

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 83/102

thatadditional credit

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 84/102

(i.e.cost of capital).COSTS ASSOCIATED WITH

ACCOUNTS RECEIVABLES MANAGEMENT

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 85/102

The major categories of costs associated with the extension of credit

and accounts receivable are :

Collection Cost

Capital Cost

Delinquency Cost

Default Cost

COLLECTION COST

Collection costs are administrative costs incurred in collecting the receivables from the

customers to whom credit sales have been made. Included in this category of costs are :

additional expenses on the creation and maintenance of a credit departmentwith staff, accounting records, stationery, postage and other related items;

expenses involved in acquiring credit information either through outsidespecialist agencies or by the staff of the firm itself.

These expenses would not be incurred if the firm does not sell oncredit. CAPITAL COST

The increased level of accounts receivable is an investment in assets. They have to be

financed thereby involving a cost. There is a time-lag between the sale of goods to, and payment by,

the customers. Meanwhile, the firm has to pay employees and suppliers of raw materials, thereby

implying that the firm should arrange for additional funds to meet its own obligations while waiting

for payment from its customers. The cost o the use of additional capital to support credit sales, which

alternatively could be profitably employed elsewhere, is, therefore, a part of the cost of extending

credit or receivables.

DELINQUENCY COST

This cost arises out of the failure of the customers to meet their obligations when payment on

credit sales become due after the expiry of the credit period. Such costs are called delinquency costs.

The important components of this costs are :

(a)

blocking-up of funds for an extended period,

cost associated with steps that have to be initiated to collect the overdues, such as, reminders and

other collection efforts, legal charges, where necessary, and so on.

DEFAULT COST

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 86/102

Finally, the firm may not be able to recover the overdues because of the inability of the

customers. Such debts are treated as bad debts and have to be written off as they cannot be realised.

Such costs are known as default costs associated with credit sales and accounts receivable.

ADMINISTRATION COSTS OF ACCOUNTS RECEIVABLES

MANAGEMENT

The costs relating to the administration of receivables is as follows :-

Screening the potential customers for granting credit.

Accounting, recording and processing costs of debtors balances.

Expenditure incurred for credit control checks.

Cost incurred for sending invoices and statements of accounts to individual

customers.

Chasing up slow paying debtors.

Cost incurred for classification of quaries.

Recording receipt of cash and processing on individual customer records.Use of office space, processing equipment and remuneration of sales force

involved in debtors collection etc

BENEFITS OF ACCOUNTS RECEIVABLES

MANAGEMENTApart from the costs, another factor that has a bearing on accountsreceivable management is the benefit emanating from credit sales.The

benefits are the increased sales and anticipated profits because of a moreliberal policy. When firms extend trade credit, that is, invest in receivables,

they intend to increase the sales. The impact of a liberal trade credit policy is likely to take two

forms. First, it is oriented to sales expansion. In other words, a firm may grant trade credit either to

increase sales to existing customers or attract new customers. This motive for investment in

receivables is growth-oriented. Secondly, the firm may extend credit to protect its current sales

against emerging competition. Here, the motive is sales-retention. As a result of increased sales, the

profits of the firm will increase.

COST BENEFIT TRADE-OFF

We all know that investments in receivables involve both benefits and costs.

The extension of trade credit has a major impact on sales, costs and

profitability. Other things being equal, a relatively liberal policy and,

therefore, higher investments in receivables, will produce larger sales.

However, costs will be higher with liberal policies than with more stringent

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 87/102

measures. Therefore, accounts receivable management should aim at a trade-

off between profit (benefit) and risk (cost). That is to say, the decision to

commit funds to receivables (or the decision to grant credit) will be based

on a comparison of the benefits and costs involved, while determining the

optimum level of receivables. The costs and benefits to be compared aremarginal costs and benefits. The firm should only consider the incremental

(additional) benefits and costs that result from a change in the receivables or trade credit policy.

While it is true that general economic conditions and industry

practices have a strong impact on the level of receivables, a firm¶s

investments in this type of current assets is also greatly affected by its

internal policy. A firm has little or no control over environmental factors,

such as economic conditions and industry practices. But it can improve its profitability through a properly conceived trade credit policy or receivables

management.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 88/102

PROCESS OF ACCOUNTS RECEIVABLES

MANAGEMENTThe following process will help in efficient management of the receivables :-

Take the opinion of the sales force and internal staff.

Frame the credit terms for the customer if credit is sanctioned.

Establish the initial creditworthiness.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 89/102

Check the credit before the despatch of consignment.

Close monitoring of the credit terms and customer compliance.

Review the customer credit, if required.

Develop the reports for internal appraisal of the customer.

CREDIT POLICY

A firm¶s investment in accounts receivable depends on :

the volume of credit sales, andthe collection period.

For example, if a firm¶s credit sales are Rs 30 lakh per day and customers, on an average, take 45

days to make payment, then the firm¶s average investment in accounts receivable is :

Daily credit sales× Average collection periodRs 30 lakh× 45 = Rs 1,350 lakhThe investment in receivable may be expressed in terms of costs

instead of sales value.

The volume of credit sales is a function of the firm¶s total sales and the percentage of creditsales to total sales. Total sales depend on market size, firm¶s market share, product quality, intensity

of competition, economic conditions, etc. The financial manager hardly has any control over these

variables. The percentage of credit sales to total sales is mostly influenced by the nature of business

and industry norms.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 90/102

There is one way in which the financial manager can affect the volume of credit sales and

collection period and consequently, investment in accounts receivables. That is through the changes

in credit policy. The term credit policy is used to refer to the combination of three decision variables :

credit standards

credit terms, andcollection efforts,

on which the financial manager has influence.

Credit Standards are criteria to decide the types of customers to whom

goods could be sold on credit. If a firm has more slow-paying customers, its investment in accounts

receivable will increase. The firm will also be exposed to higher risk of default.

Credit Terms specify duration of credit and terms of payment bycustomers. Investment in accounts receivables will be high if customers areallowed extended time period for making payments.Collection Efforts determine the actual collection period. The lower the

collection period, the lower the investment in accounts receivable and viceversa.

CREDIT POLICY VARIABLES

In establishing an optimum credit policy, the financial manager must consider the important

decision variables which influence the level of variables. The major controllable decision variables

include the following : Credit standards and analysis

Credit termsCollection policy and procedures

The credit policy of a firm may be administered by the financial manager or the credit manager. It

should, however, be appreciated that credit policy has important implications for the firm¶s

production, marketing and finance functions. Therefore it is advisable that the firm¶s credit policy be

formulated by a committee which consists of executives of production, marketing and finance

departments. Within the framework of the credit policy, as laid down by this committee, the financial

or credit manager should ensure that the firm¶s value of share is maximised. He does so by answering

the following questions :

What will be the change in sales when a decision variable is altered?What will be the cost of altering the decision variable?

How would the level of receivable be affected by changing the decisionvariable?

How are expected rate of return and cost of funds related?

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 91/102

The most difficult part of the analysis of impact of change in the credit policy variables is the

estimation of sales and cost. Even if sales and costs can be estimated, it would be difficult to

establish an optimum credit policy as the best combination of the variables of credit policy is quite

difficult to obtain. For these reasons, the establishment of credit policy is a slow process in practice.

A firm will change one or two variables at a time and observe the effect. Based on the actual

experience, variables may be changed further, or change may be reversed. It should also be noted that

the firm¶s credit policy is greatly influenced by economic conditions. As economic conditions

change, the credit policy of the firm may also change. Thus, the credit policy decision is not one time

static decision.

CREDIT STANDARDS

Credit Standards are the criteria which a firm follows in selecting customers for the purpose

of credit extension. The firm may have tight credit standards; that is, it may sell mostly on cash basis,

and may extend credit only to the most reliable and financially strong customers. Such standards will

result in no bad-debt losses, and less cost of credit administration. But the firm may not be able toexpand sales. The profit sacrificed on lost sales may be more than the costs saved by the firm. On the

contrary, if credit standards are loose, the firm may have larger sales. But the firm will have to carry

larger receivable. The costs of administering credit and bad-debt losses will also increase. Thus the

choice of optimum credit standards involves a trade-off between incremental return and incremental

costs.

CREDIT ANALYSIS Credit standards influence the quality of the firm¶s customers. Thereare two aspects of the quality of customers :(a)the time taken by customers to repay credit obligation, and(b)

the default rate

The average collection period (ACP) determines the speed of payment by customers. It measures the

number of days for which credit sales remain outstanding. The longer the average collection period,

the higher the firm¶s investment in accounts receivable. Default rate can be measured in terms of

bad-debt losses ratio ± the proportion of uncollected receivable. Bad-debt losses ratio indicates

default risk. Default risk is the likelihood that a customer will fail to repay the credit obligation. Onthe basis of past practice and experience, the financial or credit manager should be able to form a

reasonable judgement regarding the chances of default. To estimate the probability of default, the

financial or credit manager should consider three C¶s :

(a)

character,(b)

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 92/102

capacity, and(c)

condition.Character refers to the customer¶s willingness to pay. The financial or

credit manager should judge whether the customers will make honest efforts to honour their creditobligations. The moral factor is of considerable importance in credit evaluation in practice.

Capacity refers to the customer¶s ability to pay. Ability to pay can be

judged by assessing he customer¶s capital and assets which he may offer as security. Capacity is

evaluated by the financial position of the firm as indicated by analysis of ratios and trends in firm¶s

cash and working capital position. The financial or credit manager should determine the real worth of

assets offered as collateral (security).

Condition refers to the prevailing economic and other conditions which may

affect the customer¶s ability to pay. Adverse economic conditions can affect the ability or willingness

of a customer to pay. An experienced financial or credit manager will be able to judge the extent and

genuineness to which the customer¶s ability to pay is affected by the economic conditions.

Information on these variables may be collected from the customers themselves, their published

financial statements and outside agencies which may be keeping credit information about customers.

A firm should use this information in preparing categories of customers according to their

creditworthiness and default risk. This would be an important input for the financial or credit

manager in formulating its credit standards. The firm may categorise its customers, at least, in the

following three categories :

Good accounts; that is, financially strong customers.Bad accounts; that is, financially very weak, high risk customers.Marginal accounts; that is, customers with nmoderate financial health and

risk (falling between good and bad accounts).

The firm will have no difficulty in quickly deciding about the extension of credit to good accounts

and rejecting the credit request of bad accounts. Most of the firm¶s time will be taken in evaluatingmarginal accounts; that is, customers who are not financially very strong but are also not so bad to be

outrightly rejected. A firm can expend its sales by extending credit to marginal accounts. But the

firm¶s costs and bad-debt losses may also increase. Therefore, credit standards should be relaxed

upon the point where incremental return equals incremental cost.

CREDIT TERMS The stipulations under which the firm sells on credit to customers are

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 93/102

called credit terms. These stipulations include :(a)

the credit period, and(b)the cash discount.

Credit Period

The length of time for which credit is extended to customers is called the credit period. It is

generally stated in terms of a net date. For example, if the firm¶s credit terms are µnet 35¶, it is

expected that customers will repay credit obligation not later than 35 days. A firm¶s credit period

may be governed by the industry norms. But depending on its objective, the firm can lengthen the

credit period. On the other hand, the firm may tighten its credit period if customers are defaulting too

frequently and bad-debt losses are building up.

A firm lengthens credit period to increase its operating profit through expanded sales.However, there will be net increase in operating profit only when the cost of extended credit period is

less than the incremental operating profit. With increased sales and extended credit period,

investment in receivable would increase. Two factors cause this increase :

(a)

incremental sales result in incremental receivable and(b)

existing customers will take more time to repay credit obligation (i.e., the average collection

period will increase), thus increasing the level of receivable.

Cash Discount

A cash discount is a reduction in payment offered to customers to induce them to repay credit

obligations within a specified period of time, which will be less than the normal credit period. It is

usually expressed as a percentage of sales. Cash discount terms indicate the rate of discount and the

period for which it is available. If the customer does not avail the offer, he must make payment

within the normal credit period.

In practice, credit terms would include :(a)the rate of cash discount,

(b)the cash discount period, and

(c)

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 94/102

the net credit period.

For example, credit terms nay be expressed as µ2/10, net 30.¶ This means that a 2 percent discount

will be granted if the customer pays within 10 days; if he does not avail the offer he must make

payment within 30 days.

A firm uses cash discount as a tool to increase sales and accelerate collections from customers. Thus

the level of receivable and associated costs may be reduced. The cost involved is the discount taken

by the customers.

COLLECTION POLICY AND PROCEDURES

A collection policy is needed because all customers do not pay the firm¶s bills in time. Some

customers are slow-payers while some are non- payers. The collection efforts should, therefore, aim

at accelerating collections from slow-payers and reducing bad-debt losses. A collection policy should

ensure prompt and regular collection. Prompt collection is needed for fast turnover of workingcapital, keeping collection costs and bad debts within limits and maintaining collection efficiency.

Regularity in collections keeps debtors alert, and they tend to pay their dues promptly.

The collection policy should lay down clear-cut collection procedures. The collection

procedures for past dues or delinquent accounts should also be established in unambiguous terms.

The slow-paying customers are needed to be handled very tactfully. Some of them may be permanent

customers. The collection process initiated quickly, without giving nay chance to them, may

antagonise them, and the fir may lose them to competitors.

The responsibility for collection and follow-up should be explicitly fixed. It may be entrusted

to the accounts or sales department, or to a separate credit department. The co-ordination between

accounts and sales departments is necessary and must be ensured formally. The accounting

department maintains the credit records and information. If it is responsible for collection, it should

consult the sales department before initiating an action against non-paying customers. Similarly, the

sales department must

obtain past information about a customer from the accounting department before granting credit to him.

Though collection procedures should be firmly established, individual cases should be dealt

with on their merits. Some customers may be temporarily in tight financial position and in spite of

their best intentions may not be able to pay on due date. This may be due to recessionary conditions,

or other factors beyond the control of the customers. Such cases need special considerations. The

collection procedure against them should be initiated only after they have overcome their financial

difficulties and do not intend to pay promptly.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 95/102

The firm should decide on offering cash discount for prompt payment. Cash discount is a cost

to the firm for ensuring faster recovery of cash. Some customers fail to pay within he specified

discount period, yet they may make the payment after deducting the amount of cash discount. Such

cases must be promptly identified and necessary action should initiated against them to recover the

full amount.

In practice, companies may take certain precautions vis-a-vis collections. Some companies

require their customers to give pre-signed cheques. Bills discounting is another practice in India.

Unfortunately, it is not very popular with a number of companies. Some companies provide for penal

rate of interest for debtors who fail to pay in time.

So, while selling gods in the domestic market, the firm can have a number of different credit

practices. With respect to domestic market, LPS has a number of options to choose from :-

1)Direct Payment

This option includes direct payment of the amount by the customer to the selling party. In this type of

system, one of the following two options can be chosen :

Payment in Advance In this, the purchasing party has to give the payment in advance. The

amount to be paid is known as revolving amount. The purchasing party has to give the payment prior to taking the goods. For immediate payment, the purchasing party is also offered a cash discount, the

rate of which is based on certain factors.

Payment within 60 days In this, the customer has to make

the payment within 60 days of getting the goods. No cash discount is

offered on this type of payment.

2)OBC (Outward Bill Collection)

Under this option, along with the ordered goods, a lorry receipt (also known as goods receipt) is sent

to the customers. This receipt contains information such as number of packets/cartons, value of

goods sent, etc. This receipt is directly sent to the customer and the customer makes the payment

through the bank. For this purpose, the bank has to provide the customer with rest of the documents.

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 96/102

The bank charges some interest from the selling party for providing this facility. If the customer is

unable to make the payment, then the selling party can also take legal action. But the payment is not

confirmed under this option.

3)Bill Of Exchange

Under this option, the bank of the purchasing party sends a confidential letter to the bank of the

selling party. Along with Bill of Exchange, Hundi is also sent to the bank. The Hundi contains

certain terms &

conditions and bank stamp by customer. Under this option, the paymentis confirmed.

4)Hundi on Demand

This option involves receiving of payment by the bank. The Hundi is sent to

the customer¶s bank and payment is received immediately. So there is surity of

receiving the payment. There can also be Supply Discount Bills (SDBs). These

bills carry certain limits with them which may relate to the amount of bill, time for

discounting, etc.

Just as a firm has a no. of options about its credit policies & practices, similarly, the firm has

many alternatives regarding the credit practices while making exports also. Such as, the firm can

adopt a policy of FOBC (Foreign Outward Bill Collection) which is same as the OBC policy in the

domestic market. Similarly, there can be Foreign Discount Bills (FDBs) which are similar to the

SDBs used in the domestic market dealings. These bills have a certain limit within which they can be

discounted. Along with this time limit, the customer is provided with a maximum transit period of 25

days. Now a days, the firms usually have a system of electronic transfer between banks.

Rational of the Study:-

Today Accounts Receivables have become a standardized key to managingthe working

Capital of running business around the world. CFO, GM-Finance &

Finance managers,

all are concerned with this study. This study will throw some light on theimpact of the

accounts receivables on the working capital and currents assets as well, of the company& cost incurred therein.

ANALYSIS OF ACCOUNTS

RECEIVABLES MANAGEMENT & INTERPRETATION

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 97/102

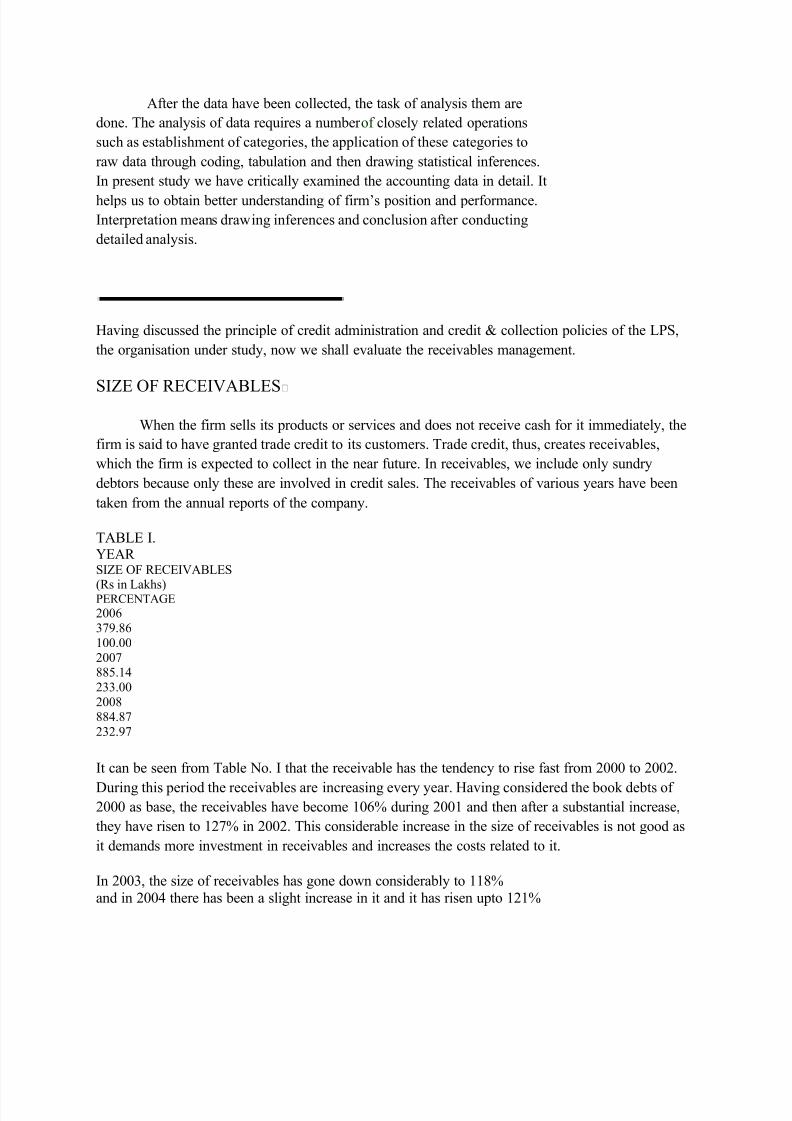

After the data have been collected, the task of analysis them are

done. The analysis of data requires a number of closely related operations

such as establishment of categories, the application of these categories to

raw data through coding, tabulation and then drawing statistical inferences.

In present study we have critically examined the accounting data in detail. It

helps us to obtain better understanding of firm¶s position and performance.

Interpretation means drawing inferences and conclusion after conducting

detailed analysis.

Having discussed the principle of credit administration and credit & collection policies of the LPS,

the organisation under study, now we shall evaluate the receivables management.

SIZE OF RECEIVABLES

When the firm sells its products or services and does not receive cash for it immediately, the

firm is said to have granted trade credit to its customers. Trade credit, thus, creates receivables,

which the firm is expected to collect in the near future. In receivables, we include only sundry

debtors because only these are involved in credit sales. The receivables of various years have been

taken from the annual reports of the company.

TABLE I.YEAR SIZE OF RECEIVABLES

(Rs in Lakhs)PERCENTAGE

2006

379.86

100.00

2007885.14

233.00

2008

884.87

232.97

It can be seen from Table No. I that the receivable has the tendency to rise fast from 2000 to 2002.

During this period the receivables are increasing every year. Having considered the book debts of 2000 as base, the receivables have become 106% during 2001 and then after a substantial increase,

they have risen to 127% in 2002. This considerable increase in the size of receivables is not good as

it demands more investment in receivables and increases the costs related to it.

In 2003, the size of receivables has gone down considerably to 118%

and in 2004 there has been a slight increase in it and it has risen upto 121%

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 98/102

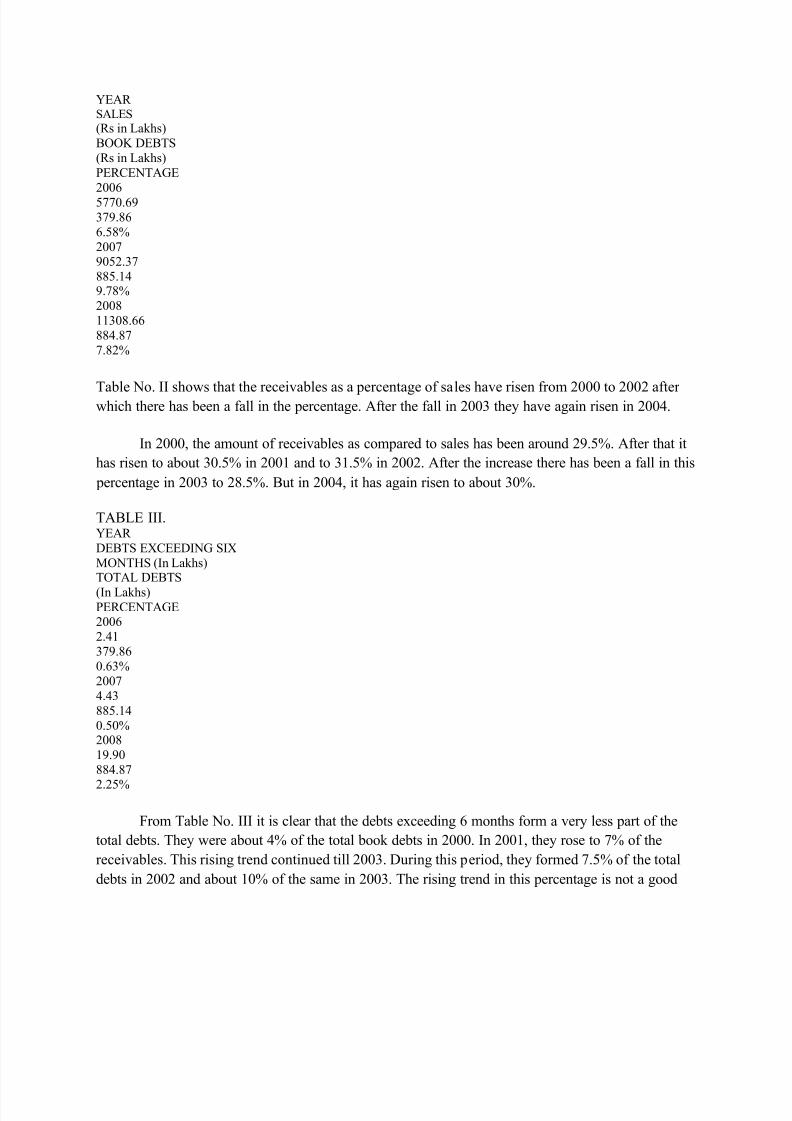

YEAR SALES

(Rs in Lakhs)

BOOK DEBTS

(Rs in Lakhs)

PERCENTAGE

2006

5770.69

379.86

6.58%

20079052.37

885.149.78%

2008

11308.66

884.87

7.82%

Table No. II shows that the receivables as a percentage of sales have risen from 2000 to 2002 after which there has been a fall in the percentage. After the fall in 2003 they have again risen in 2004.

In 2000, the amount of receivables as compared to sales has been around 29.5%. After that it

has risen to about 30.5% in 2001 and to 31.5% in 2002. After the increase there has been a fall in this

percentage in 2003 to 28.5%. But in 2004, it has again risen to about 30%.

TABLE III.YEAR

DEBTS EXCEEDING SIX

MONTHS (In Lakhs)TOTAL DEBTS

(In Lakhs)PERCENTAGE2006

2.41

379.86

0.63%

2007

4.43

885.14

0.50%2008

19.90

884.87

2.25%

From Table No. III it is clear that the debts exceeding 6 months form a very less part of the

total debts. They were about 4% of the total book debts in 2000. In 2001, they rose to 7% of the

receivables. This rising trend continued till 2003. During this period, they formed 7.5% of the total

debts in 2002 and about 10% of the same in 2003. The rising trend in this percentage is not a good

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 99/102

indicator as it may lead to more bad-debt losses for the firm because higher the time period for which

the receivables have been due, higher are the chances of those debts going bad

TABLE IV.YEAR

OTHER DEBTS (LESS THANSIX MONTHS) (In Lakhs)

TOTAL DEBTS

(In Lakhs)

PERCENTAGE2006

377.45

379.86

99.36%

2007

880.71

885.1499.50%

2008

864.97

884.87

97.75%

Table No. IV gives us the information about the percentage of debts less than six months to total

debts of the firm. From this percentage, we can see that these debts form most of the part of total

debts. Although their percentage has been decreasing in the past few years (except 2004 in which the

percentage has risen), yet they form the bulk of total debts. This means that the firm is able to collect

a major portion of its total debts within a period of 6 months. From 2000 to 2003, this percentage has

gone down from about 96% to 90%. Between this period, the percentage was between 92% and 93%.

In 2004, the percentage has again risen to around 93%.

TURNOVER OF ACCOUNTS RECEIVABLE

The analysis of efficiency of granting credit and collecting the dues can be done through the

turnover of accounts receivables. In fact, as suggested by Professor R.W. Johnson, the analysis of the

efficiency of granting credit has been done on the basis of computation of the turnover of accounts

receivables and the analysis of collecting the dues has been done on the basis of ageing of accounts

receivables. To find out the turnover of accounts receivables, the Average Collection Period (ACP)

will have to be calculated. The average collection period can be known only when we have sales and

receivable or book debts for various years. The formula with which average collection period can be

found out is ± Divide receivables by sales and multiply by 365 (days in a year). The average

collection period has been calculated in the following table :-

TABLE V.YEAR

SALES

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 100/102

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 101/102

The credit policy of the firm is determined by Board of Directors with

consultation of the marketing division of the firm. The financial division is

informed by the marketing division about the unrealised dues. The marketing

division handles the credit policies as credit sales have got direct bearing on the

total sales. A study has been conducted to find out the effectiveness of its credit

and collection policy. The credit period lies between 30 to 90 days depending on

the credit worthiness of the customer. The firm gives credit on selective basis after

analysing the 5 C¶s about the customer viz; character, capacity, capital, condition,

and collateral. The firm charges an interest equal to commercial bank rate @ 18%

at which bank generally extends cash credit / overdrafts etc. The firm extends

credit through bills of exchange which are paid within 10 to 15 days from he date

of issue.

The size of receivables of the firm from 2000 to 2004 has shown increasing

tendency throughout this period i.e. from 100% to 121%, except in the year 2003when it has decreased. The increase is almost every year which is not appreciable.

The increase is considerable from 2000 to 2002 but the rate of increase has gone

down in 2003 & 2004.

The sales of the firm have increased during the time period under

consideration. But the size of receivables as a part of sales has not risen

proportionately. From 2000 to 2002, this percentage has increased from 29.5% to

31.5%. But in 2003 there has been a decline in this figure in spite of the increase in

the amount of sales. This shows a collection policy which tends to emphasize on

the restriction of credit sales. But the condition has improved a little in 2004 withthe percentage showing an increase to 30%.

The debts of the firm which are outstanding for a period of more than 6 months

form a very less part of the total debts of the firm. But their percentage to total

debts has shown an increasing trend till 2003. This is not a good indicator as it may

lead to more bad-debt losses for the firm because higher the time period for which

the receivables have been due, higher are the chances of those debts going bad.

These debts have decreased in the year 2004 which shows that the firm has taken

certain measures

In contrast to the credit period of 30 to 90 days the average collection period varies

between 104 to 115 days during this period. The ACP has increased from 108 days

in 2000 to 115 days in 2002 which is not good for the firm. In 2004, after declining

8/9/2019 Office Network of Tvs Lucas

http://slidepdf.com/reader/full/office-network-of-tvs-lucas 102/102

to 104 days in 2003, it has gain risen to 110 days. The turnover of accounts

receivable for this period lies between 3 and 3.5.

The percentage of bad debts of the firm to its sales has been fluctuating during this

period. But it has increased steeply in 2004 which is not good. This shows that the

firm has got a weak collection policy. Similar is the case with the percentage of

bad debts to total debts. This percentage has also risen in 2004.

The percentage of book debts to current assets has declined gradually during this

period. This may be due to stringent credit policy of the firm. But a continuous

decrease in this percentage can have an adverse impact on the future sales of the

firm. The percentage of debtors to total assets has also shown a decline during this

period.

The ACP and the sales of the firm are negatively correlated. This means thatif ACP is decreased, the sales will show an increase.