ODTK Theory and Algorithms

426

Orbit Determination Tool Kit Theory & Algorithms 1 James R. Wright, et al. May 1, 2013 1 c Analytical Graphics, Inc., 2002 through 2012. All Rights Reserved.

-

Upload

bala-murugan -

Category

Documents

-

view

274 -

download

16

description

Orbit determination

Transcript of ODTK Theory and Algorithms

Orbit Determination Tool KitTheory & Algorithms1

James R. Wright, et al.

May 1, 2013

1 c Analytical Graphics, Inc., 2002 through 2012. All Rights Reserved.

ii

Contents

0.1 Preface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xx0.2 Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . xx0.3 US Patents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xx

1 Introduction 11.1 Orbit Determination Classes . . . . . . . . . . . . . . . . . . . . . 1

1.1.1 IOD Methods . . . . . . . . . . . . . . . . . . . . . . . . . 21.1.2 LS Methods . . . . . . . . . . . . . . . . . . . . . . . . . . 21.1.3 SP Methods . . . . . . . . . . . . . . . . . . . . . . . . . . 21.1.4 "Batch Filter" (Sequential LS) Methods . . . . . . . . . . 31.1.5 Optimal Orbit Determination . . . . . . . . . . . . . . . . 3

1.2 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41.2.1 Coordinate Frames . . . . . . . . . . . . . . . . . . . . . . 41.2.2 Spacecraft Vectors and Components . . . . . . . . . . . . 71.2.3 Numerical Orbit Propagation . . . . . . . . . . . . . . . . 8

1.3 Mathematical Operators for SP Methods . . . . . . . . . . . . . . 91.3.1 Subscript Notation . . . . . . . . . . . . . . . . . . . . . . 91.3.2 Nonlinear Operators . . . . . . . . . . . . . . . . . . . . . 101.3.3 Linear Operators . . . . . . . . . . . . . . . . . . . . . . . 10

1.4 Document Partition . . . . . . . . . . . . . . . . . . . . . . . . . 11

I Optimal Orbit Determination 13

2 Optimal Orbit Determination (OOD) 152.1 De�nitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.1.1 State Estimate Reference for Linearization of SP Methods 152.1.2 Local Linearization . . . . . . . . . . . . . . . . . . . . . . 162.1.3 Global Linearization . . . . . . . . . . . . . . . . . . . . . 162.1.4 Observability . . . . . . . . . . . . . . . . . . . . . . . . . 162.1.5 Completeness . . . . . . . . . . . . . . . . . . . . . . . . . 162.1.6 Optimal Orbit Determination . . . . . . . . . . . . . . . . 162.1.7 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

iii

iv CONTENTS

3 Fundamental Theorem of Estimation 193.1 Gaussian Probability Density Function . . . . . . . . . . . . . . . 19

3.1.1 Sample Data . . . . . . . . . . . . . . . . . . . . . . . . . 193.1.2 Multidimensional Gaussian Random Variable . . . . . . . 19

3.2 Gaussian Cumulative Distribution Function . . . . . . . . . . . . 203.2.1 Central Limit Theorem . . . . . . . . . . . . . . . . . . . 213.2.2 Multidimensional Gaussian Random Variable . . . . . . . 22

3.3 Short Version of Fundamental Theorem . . . . . . . . . . . . . . 223.4 Complete Version of Fundamental Theorem . . . . . . . . . . . . 223.5 Comparison to Least Squares . . . . . . . . . . . . . . . . . . . . 23

4 Kalman�s Approach 254.1 Linearization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 254.2 State Estimate Error Model . . . . . . . . . . . . . . . . . . . . . 264.3 Integral Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4.3.1 Gauss-Markov Sequence . . . . . . . . . . . . . . . . . . . 274.4 Time Update Algorithm . . . . . . . . . . . . . . . . . . . . . . . 27

4.4.1 State Error Covariance for Filter Time Update . . . . . . 274.5 Measurement Update Algorithm . . . . . . . . . . . . . . . . . . 28

5 Optimal Sequential Filter 315.1 State Estimate Error Model . . . . . . . . . . . . . . . . . . . . . 315.2 Integral Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 325.3 State Error Covariance for Filter Time Update . . . . . . . . . . 325.4 Approximate Error-Model Solutions . . . . . . . . . . . . . . . . 33

5.4.1 Gravity Solution . . . . . . . . . . . . . . . . . . . . . . . 335.4.2 Air-Drag Solution . . . . . . . . . . . . . . . . . . . . . . 335.4.3 Solar Pressure Solution . . . . . . . . . . . . . . . . . . . 34

5.5 Filter Time Update Algorithm . . . . . . . . . . . . . . . . . . . 345.6 Filter Measurement Update . . . . . . . . . . . . . . . . . . . . . 34

5.6.1 Measurement Editing . . . . . . . . . . . . . . . . . . . . 345.6.2 Supplementary Editor . . . . . . . . . . . . . . . . . . . . 355.6.3 Filter Initialization . . . . . . . . . . . . . . . . . . . . . . 355.6.4 Filter Divergence . . . . . . . . . . . . . . . . . . . . . . . 35

6 Fixed Interval Sequential Smoother 376.1 Smoother Initialization . . . . . . . . . . . . . . . . . . . . . . . . 376.2 Notation for Smoother Nonlinear State Transition . . . . . . . . 386.3 Smoother Sequential Equations . . . . . . . . . . . . . . . . . . . 38

6.3.1 Transition Smoothed State Estimate Backwards . . . . . 386.3.2 Incorporate Filter Estimate and Covariance at Time tk . 386.3.3 Prepare to Calculate Smoother Covariance . . . . . . . . 386.3.4 Smoother Covariance . . . . . . . . . . . . . . . . . . . . . 386.3.5 Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 396.3.6 Example for k = L� 1 . . . . . . . . . . . . . . . . . . . . 39

6.4 Filter-Smoother Consistency Test . . . . . . . . . . . . . . . . . . 39

CONTENTS v

6.4.1 Test . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 406.5 Smoother Matrix Inversions . . . . . . . . . . . . . . . . . . . . . 40

7 Variable-Lag Sequential Smoother 417.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 417.2 General Application . . . . . . . . . . . . . . . . . . . . . . . . . 42

7.2.1 ODTK LEO Simulation . . . . . . . . . . . . . . . . . . . 437.3 Impulsive Maneuvers . . . . . . . . . . . . . . . . . . . . . . . . . 437.4 Required Properties . . . . . . . . . . . . . . . . . . . . . . . . . 447.5 Properties Available . . . . . . . . . . . . . . . . . . . . . . . . . 45

7.5.1 Linear . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 457.5.2 Extension . . . . . . . . . . . . . . . . . . . . . . . . . . . 467.5.3 Nonlinear . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

7.6 Kalman Filter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 477.6.1 Time Update . . . . . . . . . . . . . . . . . . . . . . . . . 477.6.2 Measurement Update . . . . . . . . . . . . . . . . . . . . 48

7.7 Carlton-Rauch Fixed-Epoch Smoother . . . . . . . . . . . . . . . 497.7.1 FES Initialization . . . . . . . . . . . . . . . . . . . . . . 497.7.2 Measurement at tj = tk+1 . . . . . . . . . . . . . . . . . . 507.7.3 Measurements at tj = tk+1; tk+2; : : : . . . . . . . . . . . . 51

7.8 Frazer Fixed-Epoch Smoother . . . . . . . . . . . . . . . . . . . . 517.8.1 FES Initialization . . . . . . . . . . . . . . . . . . . . . . 517.8.2 Measurement at tj = tk+1 . . . . . . . . . . . . . . . . . . 51

8 State-Space Changes 538.1 Problem De�nition . . . . . . . . . . . . . . . . . . . . . . . . . . 53

8.1.1 Structure of VLS Algorithms . . . . . . . . . . . . . . . . 548.2 Handling Discontinuities by the Filter . . . . . . . . . . . . . . . 54

8.2.1 State Contraction . . . . . . . . . . . . . . . . . . . . . . 548.2.2 State Expansion . . . . . . . . . . . . . . . . . . . . . . . 568.2.3 Simultaneous Contraction and Expansion . . . . . . . . . 568.2.4 Stability Properties of the Covariance Contraction . . . . 56

8.3 Smoothing Algorithms . . . . . . . . . . . . . . . . . . . . . . . . 588.3.1 Fixed-Interval Smoothing (RTS) . . . . . . . . . . . . . . 588.3.2 Fixed-Point Smoothing (Carlton-Rauch) . . . . . . . . . . 598.3.3 Fixed-Point Smoother (Meditch, Anderson-Moore) . . . . 598.3.4 McReynolds Multi-point Smoother . . . . . . . . . . . . . 62

8.4 Handling Filter Discontinuities with Smoothers . . . . . . . . . . 638.4.1 Fixed-Interval Smoothing with Discontinuities . . . . . . 638.4.2 Fixed-Point Smoothing (Carlton-Rauch) with Discontinu-

ities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 658.4.3 Fixed-Point Smoothing (Fraser) with Discontinuities . . . 668.4.4 Multi-Point Smoothing with Discontinuities . . . . . . . . 67

vi CONTENTS

9 Relative Orbit Errors 699.1 Simultaneous Orbit Determination . . . . . . . . . . . . . . . . . 699.2 Orbit Di¤erence Error Covariance . . . . . . . . . . . . . . . . . 70

10 Orbit Errors in Keplerian Variables 71

11 Time Grids 73

II Stochastic Sequences 75

12 Stochastic Sequences for OOD 7712.1 A Scalar Exponential Gauss-Markov Sequence . . . . . . . . . . . 77

12.1.1 Deterministic Transitivity with Time . . . . . . . . . . . . 7812.1.2 Stationary Variance . . . . . . . . . . . . . . . . . . . . . 7912.1.3 Propagation Time Extrema . . . . . . . . . . . . . . . . . 8012.1.4 Input Control . . . . . . . . . . . . . . . . . . . . . . . . . 8012.1.5 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . 8112.1.6 Stationarity . . . . . . . . . . . . . . . . . . . . . . . . . . 82

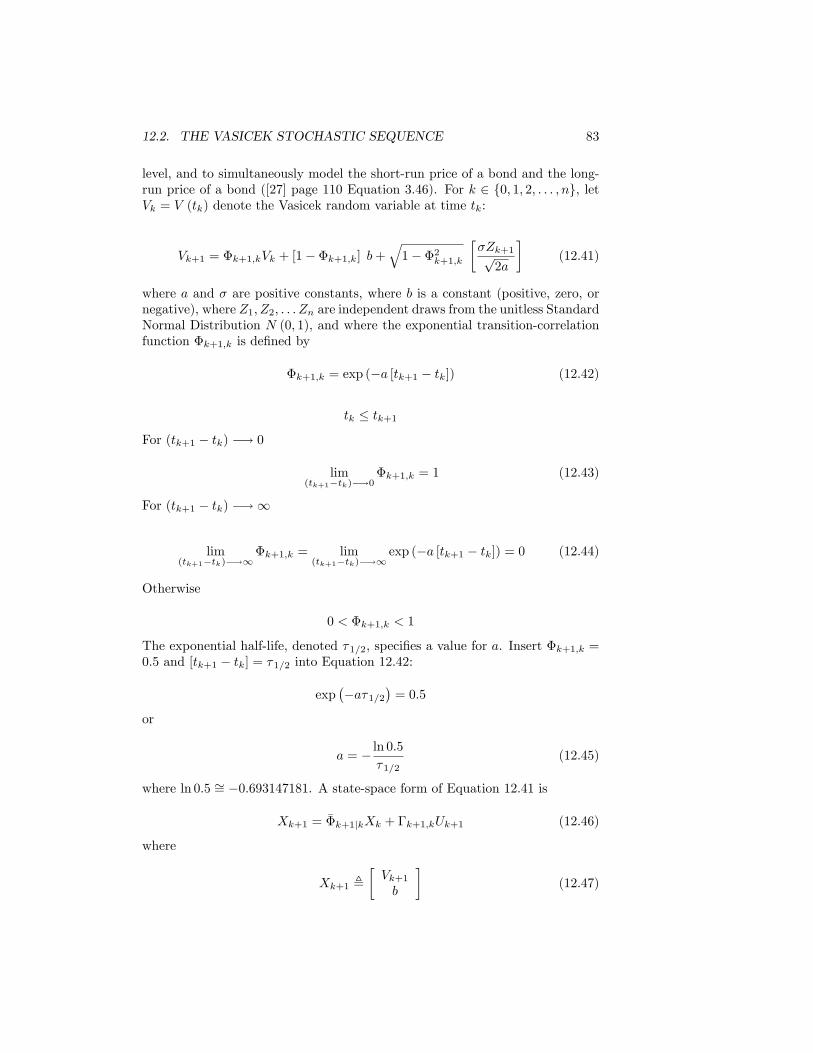

12.2 The Vasicek Stochastic Sequence . . . . . . . . . . . . . . . . . . 8212.2.1 Transition Matrix �� . . . . . . . . . . . . . . . . . . . . . 8412.2.2 Units . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8512.2.3 Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . 8512.2.4 Drift . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8512.2.5 Mean . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8512.2.6 Second Moments . . . . . . . . . . . . . . . . . . . . . . . 8512.2.7 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . 8712.2.8 Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8712.2.9 Sequential Estimation . . . . . . . . . . . . . . . . . . . . 88

12.3 Other Stochastic Sequences . . . . . . . . . . . . . . . . . . . . . 9212.3.1 Brownian Motion . . . . . . . . . . . . . . . . . . . . . . . 9212.3.2 White Noise . . . . . . . . . . . . . . . . . . . . . . . . . . 9412.3.3 Clocks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

III Accelerations 97

13 Accelerations 9913.1 Two Body Acceleration . . . . . . . . . . . . . . . . . . . . . . . 9913.2 Total Acceleration . . . . . . . . . . . . . . . . . . . . . . . . . . 99

14 Earth Gravity 10114.1 Geopotential . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10114.2 Legendre Functions . . . . . . . . . . . . . . . . . . . . . . . . . . 102

14.2.1 Legendre Polynomials of First Kind . . . . . . . . . . . . 10214.2.2 Associated Legendre Functions of First Kind . . . . . . . 103

14.3 Auto-Covariance Function on a Sphere . . . . . . . . . . . . . . . 103

CONTENTS vii

14.3.1 From Angle to Time . . . . . . . . . . . . . . . . . . . . . 10514.3.2 Covariance Function R (0) . . . . . . . . . . . . . . . . . . 10514.3.3 Auto-correlation Function . . . . . . . . . . . . . . . . . . 105

14.4 Acceleration Errors on a Sphere . . . . . . . . . . . . . . . . . . . 10614.4.1 Computational Problem . . . . . . . . . . . . . . . . . . . 10714.4.2 Solution to Computational Problem . . . . . . . . . . . . 10814.4.3 The Double Integral . . . . . . . . . . . . . . . . . . . . . 10814.4.4 Markov Property . . . . . . . . . . . . . . . . . . . . . . . 10814.4.5 Inertial Frame . . . . . . . . . . . . . . . . . . . . . . . . 10914.4.6 Stochastic Characterization . . . . . . . . . . . . . . . . . 11014.4.7 Implementation . . . . . . . . . . . . . . . . . . . . . . . . 110

14.5 Perigee-Apogee Weighting . . . . . . . . . . . . . . . . . . . . . . 11014.5.1 Weighting Functions . . . . . . . . . . . . . . . . . . . . . 111

14.6 New Method . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11214.6.1 Splines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11214.6.2 Sample Covariance Validation . . . . . . . . . . . . . . . . 11214.6.3 GRACE . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11214.6.4 EGM96 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

14.7 Simulate Gravity Coe¢ cient Errors . . . . . . . . . . . . . . . . . 11314.7.1 Covariance Matrix Representations . . . . . . . . . . . . . 11314.7.2 Simulation of x . . . . . . . . . . . . . . . . . . . . . . . . 11414.7.3 A Useful Example . . . . . . . . . . . . . . . . . . . . . . 115

15 Lunar Gravity 11715.1 Lunar Prospector . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

16 Atmospheric Drag and Lift 11916.1 King-Hele Unit Vector K . . . . . . . . . . . . . . . . . . . . . . 11916.2 Orthonormal Vector Basis [a] . . . . . . . . . . . . . . . . . . . . 12016.3 Drag-Lift Acceleration . . . . . . . . . . . . . . . . . . . . . . . . 12116.4 Air-Drag Acceleration . . . . . . . . . . . . . . . . . . . . . . . . 121

16.4.1 Drag Acceleration . . . . . . . . . . . . . . . . . . . . . . 12116.5 Ballistic Coe¢ cient Errors . . . . . . . . . . . . . . . . . . . . . . 12216.6 Atmospheric Density Errors . . . . . . . . . . . . . . . . . . . . . 122

16.6.1 Relative Error Base-Line Model on Air-Density . . . . . . 12316.6.2 Gauss-Markov Sequence on Air-Density Relative Error . . 12416.6.3 Propagation of State Estimate . . . . . . . . . . . . . . . 12416.6.4 State Estimate Error . . . . . . . . . . . . . . . . . . . . . 12516.6.5 Process Noise Covariance . . . . . . . . . . . . . . . . . . 12516.6.6 Transform From Perigee Height to Current Height . . . . 12716.6.7 Orbit Error Covariance . . . . . . . . . . . . . . . . . . . 128

viii CONTENTS

17 Solar Photon Pressure 13117.1 Coordinate Frame for Solar Pressure . . . . . . . . . . . . . . . . 13117.2 Solar Pressure Acceleration . . . . . . . . . . . . . . . . . . . . . 132

17.2.1 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13317.2.2 Conservation of Linear Momentum . . . . . . . . . . . . . 13317.2.3 Spherical Surface Di¤use Re�ection . . . . . . . . . . . . 13417.2.4 Spherical Surface Perfect Absorption . . . . . . . . . . . . 134

17.3 Eclipse Modeling . . . . . . . . . . . . . . . . . . . . . . . . . . . 13417.3.1 Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13417.3.2 Baker�s Dual-Cone Eclipse Model . . . . . . . . . . . . . . 13517.3.3 Earth Radius . . . . . . . . . . . . . . . . . . . . . . . . . 137

17.4 Stochastic Solar Pressure Error Model . . . . . . . . . . . . . . . 137

18 GPS Solar Pressure Models 13918.1 GSPM.04a . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13918.2 GSPM.04ae . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13918.3 AeroT20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13918.4 AeroT30 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14018.5 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 140

19 Spacecraft Thrusting 14119.1 Impulsive Maneuver Model . . . . . . . . . . . . . . . . . . . . . 141

19.1.1 Trajectory . . . . . . . . . . . . . . . . . . . . . . . . . . . 14119.1.2 Trajectory Error Covariance . . . . . . . . . . . . . . . . . 14219.1.3 Time of Centroid tC . . . . . . . . . . . . . . . . . . . . . 143

19.2 Impulsive Maneuver Error Covariance . . . . . . . . . . . . . . . 14419.2.1 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14419.2.2 Time Relations . . . . . . . . . . . . . . . . . . . . . . . . 14419.2.3 Covariance . . . . . . . . . . . . . . . . . . . . . . . . . . 145

19.3 Impulsive Maneuver Covariance . . . . . . . . . . . . . . . . . . . 14619.3.1 Discussion . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

19.4 Finite Maneuver Model . . . . . . . . . . . . . . . . . . . . . . . 14819.4.1 Kinematics . . . . . . . . . . . . . . . . . . . . . . . . . . 14819.4.2 Dynamics . . . . . . . . . . . . . . . . . . . . . . . . . . . 14919.4.3 Stochastic Sequences . . . . . . . . . . . . . . . . . . . . . 14919.4.4 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . . 150

IV Spacecraft Attitude 151

20 Attitude Modeling 15320.1 Antenna Phase Center Estimation . . . . . . . . . . . . . . . . . 153

CONTENTS ix

V State Error Transition 155

21 Transitive Partial Derivatives 15721.1 State Error Transition Function . . . . . . . . . . . . . . . . . . . 15721.2 Position & Velocity Partials . . . . . . . . . . . . . . . . . . . . . 157

21.2.1 Two-Body Transition Matrix . . . . . . . . . . . . . . . . 15821.2.2 Variational Equations Transition Matrix . . . . . . . . . . 158

21.3 Air-Drag Partials . . . . . . . . . . . . . . . . . . . . . . . . . . . 16121.4 Solar Pressure Partials . . . . . . . . . . . . . . . . . . . . . . . . 162

VI Ground Location Estimation 163

VII Measurements 167

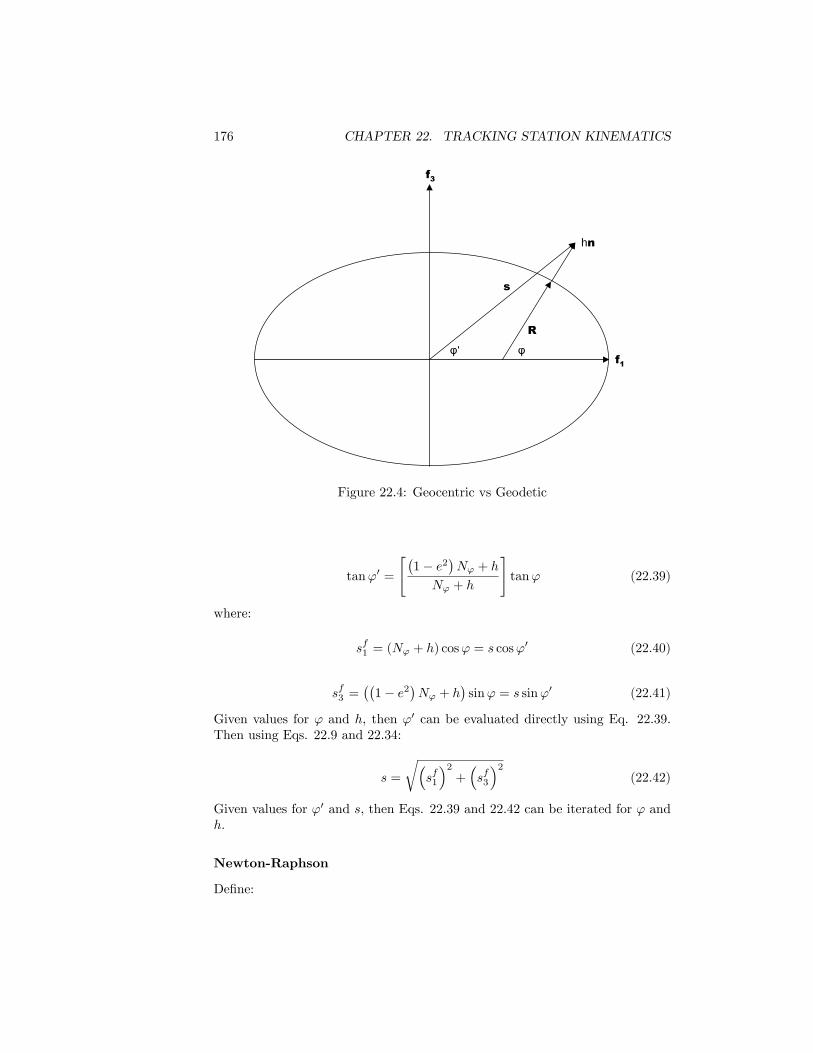

22 Tracking Station Kinematics 16922.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16922.2 The Earth-Centered Unit Sphere . . . . . . . . . . . . . . . . . . 17022.3 Ellipse in Plane of f1 and f3 . . . . . . . . . . . . . . . . . . . . . 172

22.3.1 Normal Vector n�pf�. . . . . . . . . . . . . . . . . . . . 173

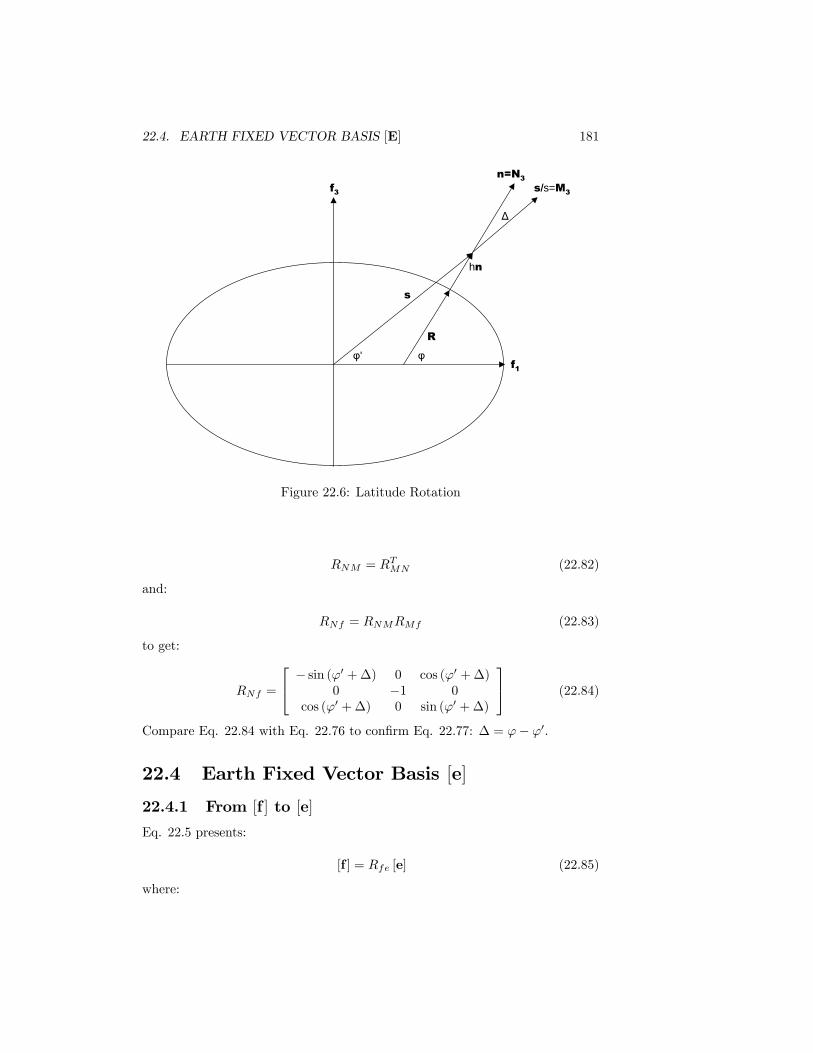

22.3.2 Geodetic Latitude . . . . . . . . . . . . . . . . . . . . . . 17322.3.3 Normal Vector n (') . . . . . . . . . . . . . . . . . . . . . 17422.3.4 Station Height Above Ellipse . . . . . . . . . . . . . . . . 17422.3.5 R . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17522.3.6 Geocentric vs Geodetic Latitude . . . . . . . . . . . . . . 17522.3.7 Topocentric Geodetic Vector Basis [N] . . . . . . . . . . . 17922.3.8 Topocentric Geocentric Vector Basis [M] . . . . . . . . . 180

22.4 Earth Fixed Vector Basis [e] . . . . . . . . . . . . . . . . . . . . . 18122.4.1 From [f ] to [e] . . . . . . . . . . . . . . . . . . . . . . . . 18122.4.2 The Ellipsoid . . . . . . . . . . . . . . . . . . . . . . . . . 18222.4.3 Station Vector . . . . . . . . . . . . . . . . . . . . . . . . 18322.4.4 Normal Vector n (') . . . . . . . . . . . . . . . . . . . . . 18322.4.5 R . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184

23 Angles 18523.1 Unit Range Vector . . . . . . . . . . . . . . . . . . . . . . . . . . 18523.2 Azimuth and Elevation . . . . . . . . . . . . . . . . . . . . . . . . 185

23.2.1 Construct L from Azimuth and Elevation . . . . . . . . . 18623.2.2 Construct Azimuth and Elevation from L . . . . . . . . . 18723.2.3 Partial Derivatives of Azimuth and Elevation . . . . . . . 18723.2.4 Construct Le from Azimuth and Elevation . . . . . . . . 18923.2.5 Construct Azimuth and Elevation from Le . . . . . . . . . 190

23.3 Direction Cosines . . . . . . . . . . . . . . . . . . . . . . . . . . . 19023.3.1 Construct Direction Cosines LF1 and L

F2 from L . . . . . 192

23.3.2 Partial Derivatives of Direction Cosines LF1 and LF2 . . . 192

x CONTENTS

23.4 X/Y Angles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19323.4.1 X/Y East-West Reference Frame . . . . . . . . . . . . . . 19323.4.2 X/Y North-South Reference Frame . . . . . . . . . . . . 19423.4.3 X/Y Z Reference Frame . . . . . . . . . . . . . . . . . . 19423.4.4 X and Y Angles . . . . . . . . . . . . . . . . . . . . . . . 19423.4.5 Partial Derivatives of X and Y Angles . . . . . . . . . . . 195

23.5 Ground Based Tracker . . . . . . . . . . . . . . . . . . . . . . . . 19523.5.1 Partials . . . . . . . . . . . . . . . . . . . . . . . . . . . . 195

23.6 Space Based Tracker . . . . . . . . . . . . . . . . . . . . . . . . . 19723.7 Earth Ellipsoid Values . . . . . . . . . . . . . . . . . . . . . . . . 197

23.7.1 NIMA/NASA EGM96 . . . . . . . . . . . . . . . . . . . . 19723.7.2 On the EGM96 Ellipsoid . . . . . . . . . . . . . . . . . . 198

24 Range 19924.1 Classical Two-Way Range . . . . . . . . . . . . . . . . . . . . . . 201

24.1.1 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20124.1.2 De�nitions . . . . . . . . . . . . . . . . . . . . . . . . . . 20124.1.3 Special Relativity . . . . . . . . . . . . . . . . . . . . . . . 20224.1.4 Calculation . . . . . . . . . . . . . . . . . . . . . . . . . . 20224.1.5 Complete Representation . . . . . . . . . . . . . . . . . . 203

24.2 Satellite to Satellite Two-Way Range . . . . . . . . . . . . . . . . 20324.3 Bi-Static Range (One-Way) . . . . . . . . . . . . . . . . . . . . . 203

25 Doppler 20525.1 Classical Two-Way Doppler . . . . . . . . . . . . . . . . . . . . . 206

25.1.1 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20625.1.2 De�nitions . . . . . . . . . . . . . . . . . . . . . . . . . . 20625.1.3 Expressions for Uplink Range-Rate . . . . . . . . . . . . . 20725.1.4 Expressions for Downlink Range-Rate . . . . . . . . . . . 20825.1.5 Two-Way Range-Rate . . . . . . . . . . . . . . . . . . . . 20925.1.6 Two-Way Doppler Frequency Equation . . . . . . . . . . 21025.1.7 Two-Way Phase Count Equation . . . . . . . . . . . . . . 21125.1.8 Observed Frequency . . . . . . . . . . . . . . . . . . . . . 21125.1.9 Measurement Names . . . . . . . . . . . . . . . . . . . . . 212

25.2 SCF ARTS Doppler . . . . . . . . . . . . . . . . . . . . . . . . . 21225.2.1 Complete Representation . . . . . . . . . . . . . . . . . . 21325.2.2 Partial Derivatives . . . . . . . . . . . . . . . . . . . . . . 213

25.3 NASA STDN Doppler . . . . . . . . . . . . . . . . . . . . . . . . 21425.3.1 Observed Range Rate . . . . . . . . . . . . . . . . . . . . 21425.3.2 Doppler Representation from the Observed Range Rate

Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 215

CONTENTS xi

26 Troposphere 21726.1 Troposphere Range . . . . . . . . . . . . . . . . . . . . . . . . . . 217

26.1.1 Zenith Component . . . . . . . . . . . . . . . . . . . . . . 21726.1.2 Mapping Function . . . . . . . . . . . . . . . . . . . . . . 220

26.2 Partial Pressure Measurements . . . . . . . . . . . . . . . . . . . 22326.3 Atmospheric Thermodynamics . . . . . . . . . . . . . . . . . . . 224

26.3.1 State Variables . . . . . . . . . . . . . . . . . . . . . . . . 22426.3.2 Ideal Gas Law . . . . . . . . . . . . . . . . . . . . . . . . 22526.3.3 Relative Humidity and Partial Pressures . . . . . . . . . . 225

26.4 Troposphere Range Error . . . . . . . . . . . . . . . . . . . . . . 22626.4.1 Propagation Variance for Relative Troposphere Range Error22726.4.2 Sequential Estimation . . . . . . . . . . . . . . . . . . . . 228

26.5 SCF �RC Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22826.5.1 Tropospheric Range Model (�RC) . . . . . . . . . . . . . . 22826.5.2 Doppler . . . . . . . . . . . . . . . . . . . . . . . . . . . . 229

27 Ionosphere 23127.1 Range . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23127.2 Doppler . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 232

27.2.1 SCF ARTS Doppler (Range-Rate) . . . . . . . . . . . . . 232

28 TDOA 23328.1 Ground-based TDOA (Ground to Spacecraft to Ground) . . . . . 233

28.1.1 Ground-based TDOA light time algorithm . . . . . . . . . 23328.1.2 Complete Representation . . . . . . . . . . . . . . . . . . 235

28.2 Ground TDOA (Spacecraft to Ground) . . . . . . . . . . . . . . . 23528.2.1 Ground TDOA light time algorithm . . . . . . . . . . . . 23528.2.2 Complete Representation . . . . . . . . . . . . . . . . . . 236

28.3 Ground-based single di¤erenced TDOA (Ground to Spacecraft toGround) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 236

28.4 Space-based TDOA (Ground to Spacecraft) . . . . . . . . . . . . 23628.4.1 Space-based TDOA light time algorithm . . . . . . . . . . 23728.4.2 Complete Representation . . . . . . . . . . . . . . . . . . 237

29 FDOA 23929.1 Ground-based FDOA (Ground to Spacecraft to Ground) . . . . . 239

29.1.1 Doppler shift . . . . . . . . . . . . . . . . . . . . . . . . . 23929.1.2 Frequency of arrival . . . . . . . . . . . . . . . . . . . . . 24029.1.3 Complete Representation . . . . . . . . . . . . . . . . . . 240

29.2 Ground FDOA (Spacecraft to Ground) . . . . . . . . . . . . . . . 24129.2.1 Frequency of arrival . . . . . . . . . . . . . . . . . . . . . 24129.2.2 Complete Representation . . . . . . . . . . . . . . . . . . 241

29.3 Ground-based single di¤erenced FDOA (Ground to Spacecraft toGround) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 241

29.4 Space-based FDOA (Ground to Spacecraft) . . . . . . . . . . . . 24229.4.1 Frequency of arrival . . . . . . . . . . . . . . . . . . . . . 242

xii CONTENTS

29.4.2 Complete Representation . . . . . . . . . . . . . . . . . . 242

30 TDOA Dot 24330.1 Ground-based TDOA Dot (Ground to Spacecraft to Ground) . . 243

30.1.1 Range rate . . . . . . . . . . . . . . . . . . . . . . . . . . 24330.1.2 Rate of change of time of arrival . . . . . . . . . . . . . . 24430.1.3 Complete Representation . . . . . . . . . . . . . . . . . . 244

30.2 Space-based TDOA Dot (Ground to Spacecraft) . . . . . . . . . 24430.2.1 Rate of change of time of arrival . . . . . . . . . . . . . . 24530.2.2 Complete Representation . . . . . . . . . . . . . . . . . . 245

31 FDOA Dot 24731.1 Ground FDOA Dot . . . . . . . . . . . . . . . . . . . . . . . . . . 247

31.1.1 Frequency of arrival rate . . . . . . . . . . . . . . . . . . . 24731.1.2 Complete Representation . . . . . . . . . . . . . . . . . . 248

32 DSN Range and Total Count Phase 24932.1 Sequential Range . . . . . . . . . . . . . . . . . . . . . . . . . . . 24932.2 Total Count Phase . . . . . . . . . . . . . . . . . . . . . . . . . . 24932.3 Doppler . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25032.4 Antenna Corrections . . . . . . . . . . . . . . . . . . . . . . . . . 25032.5 Media Corrections . . . . . . . . . . . . . . . . . . . . . . . . . . 25032.6 Solar Corona Model . . . . . . . . . . . . . . . . . . . . . . . . . 250

33 Clock Modeling 25133.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25133.2 Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252

33.2.1 Variable t . . . . . . . . . . . . . . . . . . . . . . . . . . . 25233.2.2 Constant � . . . . . . . . . . . . . . . . . . . . . . . . . . 252

33.3 ODTK Simulator Clock Time Update . . . . . . . . . . . . . . . 25233.4 ODTK Filter Clock Time Update . . . . . . . . . . . . . . . . . . 253

33.4.1 State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25333.4.2 Covariance . . . . . . . . . . . . . . . . . . . . . . . . . . 253

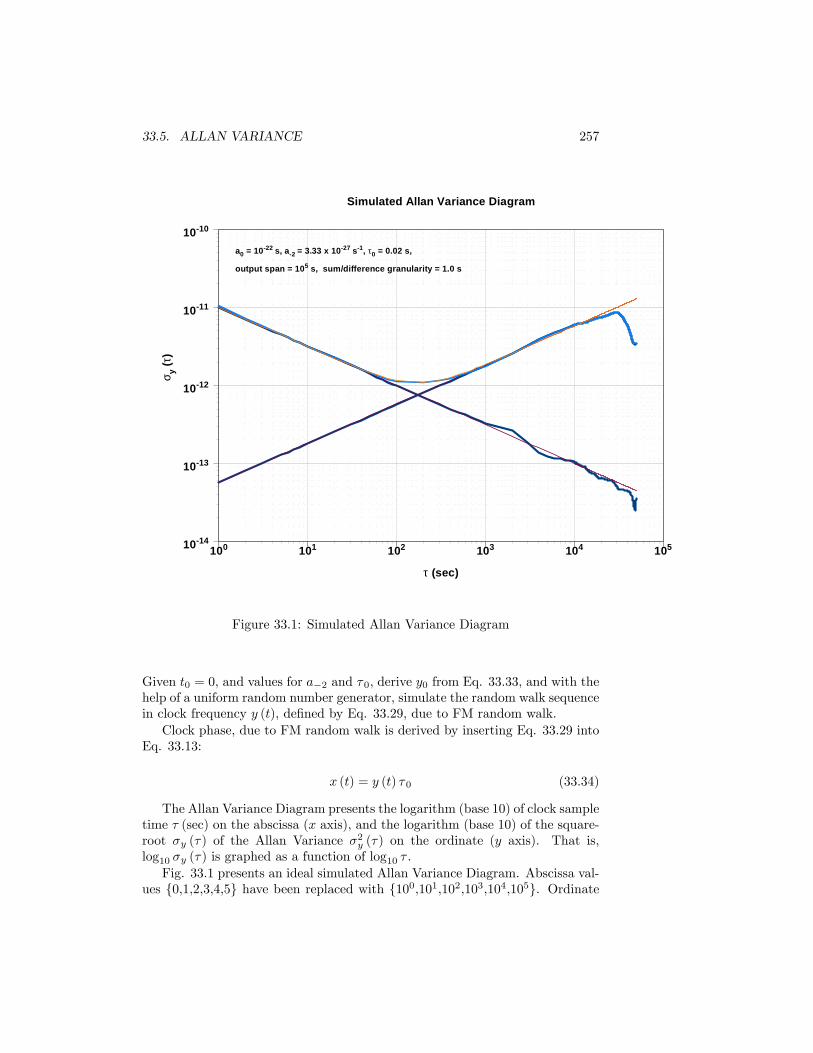

33.5 Allan Variance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25333.5.1 Covariance on Clock Phase . . . . . . . . . . . . . . . . . 25433.5.2 Simulations . . . . . . . . . . . . . . . . . . . . . . . . . . 25533.5.3 Filter Time Update for Clock . . . . . . . . . . . . . . . . 25833.5.4 State Estimate Parameters . . . . . . . . . . . . . . . . . 258

33.6 Zucca-Tavella Clock Model . . . . . . . . . . . . . . . . . . . . . 259

VIII Least Squares (LS) 261

34 LS Inputs 26334.1 Input Values . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26334.2 Initial Calculated Values . . . . . . . . . . . . . . . . . . . . . . . 264

CONTENTS xiii

34.2.1 Measurement Residuals . . . . . . . . . . . . . . . . . . . 26434.2.2 Partial Derivatives . . . . . . . . . . . . . . . . . . . . . . 265

35 Least Squares Solutions 26735.1 LS Normal Equation and Solution . . . . . . . . . . . . . . . . . 267

35.1.1 Linearization . . . . . . . . . . . . . . . . . . . . . . . . . 26735.2 Remove the Squaring Operation . . . . . . . . . . . . . . . . . . 26835.3 Solution by Triangularization of B . . . . . . . . . . . . . . . . . 269

35.3.1 Solution Overview . . . . . . . . . . . . . . . . . . . . . . 269

36 Least Squares Inadequacies 27136.1 LS Measurement Residuals . . . . . . . . . . . . . . . . . . . . . 27136.2 Incomplete LS Model . . . . . . . . . . . . . . . . . . . . . . . . . 27136.3 Least Squares State Error Covariance . . . . . . . . . . . . . . . 27136.4 Batch Simultaneity . . . . . . . . . . . . . . . . . . . . . . . . . . 27236.5 Schmidt�s Analysis of Least Squares . . . . . . . . . . . . . . . . 272

36.5.1 A Practical Experiment . . . . . . . . . . . . . . . . . . . 27236.6 Gibb�s E¤ect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 273

37 Tracking Data Editing 27537.1 Tracking Data Editor Identi�cation . . . . . . . . . . . . . . . . . 27637.2 Minimum Number of Data Sets Editor . . . . . . . . . . . . . . . 27737.3 Minimum Time Span Editor . . . . . . . . . . . . . . . . . . . . . 27737.4 Tracking Loop Flag Editor . . . . . . . . . . . . . . . . . . . . . . 27737.5 Gross Raw Data Editor . . . . . . . . . . . . . . . . . . . . . . . 27737.6 Minimum Elevation Editor . . . . . . . . . . . . . . . . . . . . . 27837.7 Sliding Raw Data Polynomial Editor . . . . . . . . . . . . . . . . 27837.8 Kepler Element Editor . . . . . . . . . . . . . . . . . . . . . . . . 278

37.8.1 Kepler Element Bounds Criterion . . . . . . . . . . . . . . 27937.8.2 m =M = 3 . . . . . . . . . . . . . . . . . . . . . . . . . . 28137.8.3 m =M = 4 . . . . . . . . . . . . . . . . . . . . . . . . . . 28137.8.4 m =M = 5 . . . . . . . . . . . . . . . . . . . . . . . . . . 28137.8.5 m � 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28237.8.6 Kepler Element Statistics Criterion . . . . . . . . . . . . . 282

37.9 Second Di¤erence Editor Using IOD . . . . . . . . . . . . . . . . 28337.10Convergence Criteria . . . . . . . . . . . . . . . . . . . . . . . . . 283

37.10.1Residual RMS Convergence Criterion Using IOD . . . . . 28337.10.2Residual RMS Convergence Criterion After First Correction284

37.11Residual Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28537.12Least Squares Solution . . . . . . . . . . . . . . . . . . . . . . . . 285

37.12.1Exceed Maximum Iteration Count Editor . . . . . . . . . 28537.13Manual Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28537.14Select A New Station Pass . . . . . . . . . . . . . . . . . . . . . . 28537.15Measurement Biases . . . . . . . . . . . . . . . . . . . . . . . . . 285

xiv CONTENTS

IX Initial Orbit Determination 287

38 IOD Methods 28938.1 Common Modeling Limitations . . . . . . . . . . . . . . . . . . . 289

38.1.1 Two-Body Dynamics . . . . . . . . . . . . . . . . . . . . . 28938.1.2 Measurement Outliers . . . . . . . . . . . . . . . . . . . . 289

38.2 Common Equations for IOD . . . . . . . . . . . . . . . . . . . . . 29038.2.1 Equation of Motion . . . . . . . . . . . . . . . . . . . . . 29038.2.2 Triangle Geometry . . . . . . . . . . . . . . . . . . . . . . 290

39 Herrick-Gibbs 29139.1 Position Vectors . . . . . . . . . . . . . . . . . . . . . . . . . . . 291

39.1.1 Taylor�s Series . . . . . . . . . . . . . . . . . . . . . . . . 291

40 Gooding 29540.1 Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 295

40.1.1 Guess Range Values . . . . . . . . . . . . . . . . . . . . . 29540.1.2 Lambert . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29540.1.3 Gooding . . . . . . . . . . . . . . . . . . . . . . . . . . . . 296

40.2 A Priori Orbit Information . . . . . . . . . . . . . . . . . . . . . 29740.2.1 Near-Circular Orbits . . . . . . . . . . . . . . . . . . . . . 29740.2.2 High Eccentricity Orbits . . . . . . . . . . . . . . . . . . . 298

40.3 White Noise . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29840.4 Tropospheric E¤ects . . . . . . . . . . . . . . . . . . . . . . . . . 29840.5 Inspection of Kepler Orbit Element Values . . . . . . . . . . . . . 29840.6 Multiple Solutions from Each Set of Distinct Measurement Sets . 29840.7 Least Squares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 299

X Tracking and Data Relay Satellite System (TDRSS)301

41 TDRSS Range and Doppler 30341.1 TDRSS Range Vectors . . . . . . . . . . . . . . . . . . . . . . . . 30341.2 Range Sum . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 304

41.2.1 Range Elements . . . . . . . . . . . . . . . . . . . . . . . 30541.2.2 Range Sum De�nition . . . . . . . . . . . . . . . . . . . . 30541.2.3 Range Sum Time Tag . . . . . . . . . . . . . . . . . . . . 30541.2.4 Construction of the Range Sum Representation . . . . . . 305

41.3 Range Sum Partial Derivatives . . . . . . . . . . . . . . . . . . . 30641.3.1 Eliminate Light-Time . . . . . . . . . . . . . . . . . . . . 30641.3.2 Simpli�ed Expressions . . . . . . . . . . . . . . . . . . . . 30741.3.3 Di¤erentials . . . . . . . . . . . . . . . . . . . . . . . . . . 30741.3.4 LEO Satellite Range Sum Partials . . . . . . . . . . . . . 30741.3.5 TDRS Range Sum Partials . . . . . . . . . . . . . . . . . 309

41.4 Doppler Measurements . . . . . . . . . . . . . . . . . . . . . . . . 31041.5 DopplerPartials . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311

CONTENTS xv

41.5.1 LEO Satellite Doppler Partials . . . . . . . . . . . . . . . 31141.5.2 TDRS Doppler Partials . . . . . . . . . . . . . . . . . . . 312

42 One-Way Return-Link Doppler 313

XI Global Positioning System (GPS) Low Earth Orbit(LEO) Receivers 315

43 Pseudo-Range Filtering 31743.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 317

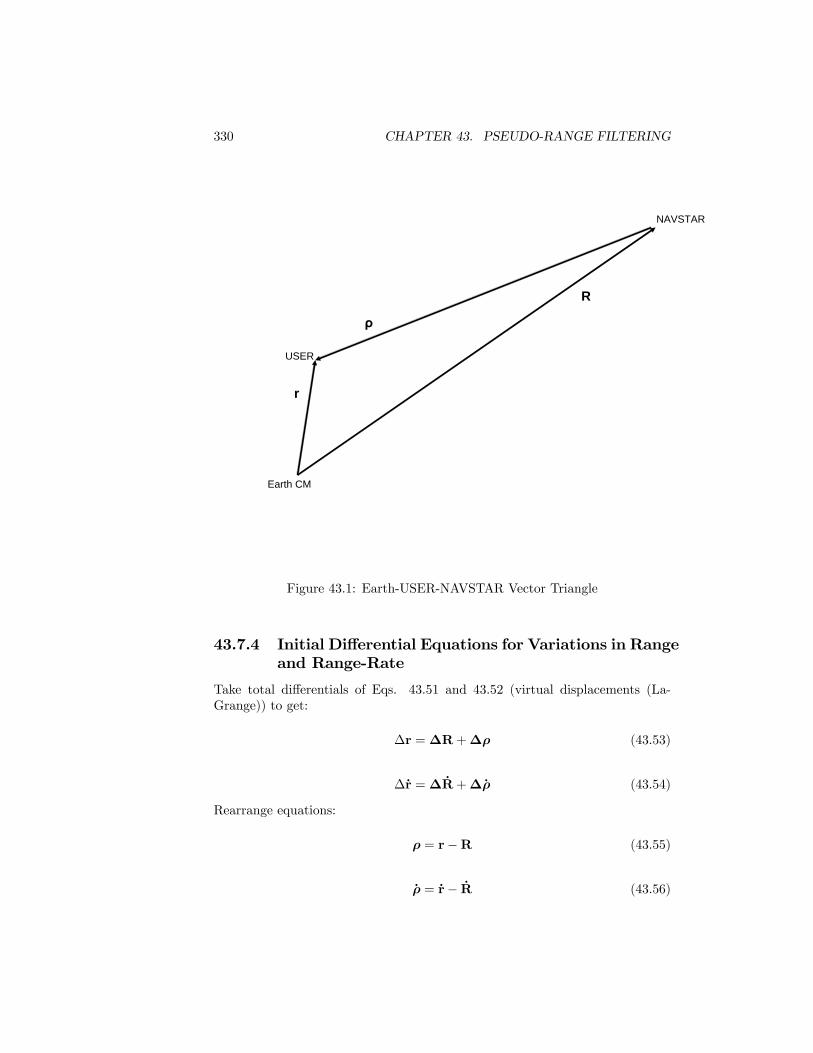

43.1.1 Pseudo-Range Option . . . . . . . . . . . . . . . . . . . . 31743.2 USER GPS Pseudo-Range . . . . . . . . . . . . . . . . . . . . . . 318

43.2.1 Pseudo-Range . . . . . . . . . . . . . . . . . . . . . . . . . 31843.2.2 Range Measurement Time Notation . . . . . . . . . . . . 31843.2.3 Time Di¤erences . . . . . . . . . . . . . . . . . . . . . . . 31843.2.4 Receiver Clock Errors . . . . . . . . . . . . . . . . . . . . 31843.2.5 Receiver Proper Time less Receiver Coordinate Time (User

Spacecraft) . . . . . . . . . . . . . . . . . . . . . . . . . . 31943.2.6 Coordinate Time Di¤erence . . . . . . . . . . . . . . . . . 32043.2.7 Transmitter Coordinate Time less Transmitter Proper Time

(NAVSTAR) . . . . . . . . . . . . . . . . . . . . . . . . . 32043.2.8 Transmitter Clock Error . . . . . . . . . . . . . . . . . . . 321

43.3 Schwarzschild Metric . . . . . . . . . . . . . . . . . . . . . . . . . 32243.3.1 Proper Time vs Coordinate Time . . . . . . . . . . . . . . 32343.3.2 Time Integrals . . . . . . . . . . . . . . . . . . . . . . . . 32343.3.3 JPL Model . . . . . . . . . . . . . . . . . . . . . . . . . . 325

43.4 Group Delay Di¤erential . . . . . . . . . . . . . . . . . . . . . . . 32543.5 Remove Ionospheric Range . . . . . . . . . . . . . . . . . . . . . 325

43.5.1 Proof . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32643.5.2 Phase Count . . . . . . . . . . . . . . . . . . . . . . . . . 326

43.6 GPS Range First-Di¤erences . . . . . . . . . . . . . . . . . . . . 32743.6.1 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32743.6.2 C/A Code Range Representation . . . . . . . . . . . . . . 32743.6.3 First Di¤erence . . . . . . . . . . . . . . . . . . . . . . . . 327

43.7 Partial Derivatives for HANU . . . . . . . . . . . . . . . . . . . . 32843.7.1 ICD-GPS-208 18 April 1983 . . . . . . . . . . . . . . . . . 32843.7.2 Partials . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32843.7.3 Map HANU Covariance P to GPS Measurement Covari-

ance Py . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32943.7.4 Initial Di¤erential Equations for Variations in Range and

Range-Rate . . . . . . . . . . . . . . . . . . . . . . . . . . 33043.7.5 Position and Velocity Variations in Inertial Component

Matrices . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33243.7.6 Partials . . . . . . . . . . . . . . . . . . . . . . . . . . . . 332

xvi CONTENTS

44 GPS Carrier Phase Count 33544.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 335

44.1.1 BlackJack GPS Receiver . . . . . . . . . . . . . . . . . . . 33644.2 Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . 336

44.2.1 Estimation of Clock Parameters . . . . . . . . . . . . . . 33644.2.2 L1 Phase Count Measurements . . . . . . . . . . . . . . . 33744.2.3 L1, L2 Phase Count Measurements . . . . . . . . . . . . . 33744.2.4 Partial Derivatives . . . . . . . . . . . . . . . . . . . . . . 337

44.3 Notation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33744.3.1 Time . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33744.3.2 Oscillator and Clock . . . . . . . . . . . . . . . . . . . . . 33844.3.3 Generalized Integral . . . . . . . . . . . . . . . . . . . . . 33844.3.4 Doppler Phase Count . . . . . . . . . . . . . . . . . . . . 33844.3.5 Two Types of Phase Count Error . . . . . . . . . . . . . . 339

44.4 Receiver Doppler Algorithm . . . . . . . . . . . . . . . . . . . . . 34044.4.1 NAVSTAR Frequencies . . . . . . . . . . . . . . . . . . . 34044.4.2 Doppler Frequency . . . . . . . . . . . . . . . . . . . . . . 34044.4.3 De�ne Phase Count . . . . . . . . . . . . . . . . . . . . . 34144.4.4 Doppler Shift . . . . . . . . . . . . . . . . . . . . . . . . . 34244.4.5 Phase Count Representation . . . . . . . . . . . . . . . . 34344.4.6 Approximations for �ij . . . . . . . . . . . . . . . . . . . 34444.4.7 USER Orbit Partial Derivatives . . . . . . . . . . . . . . . 345

44.5 Ionosphere . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34644.5.1 Physics . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34644.5.2 Total Electron Content . . . . . . . . . . . . . . . . . . . 34744.5.3 Validation . . . . . . . . . . . . . . . . . . . . . . . . . . . 349

44.6 Final Forms for Phase Count . . . . . . . . . . . . . . . . . . . . 34944.6.1 Alternate Representation . . . . . . . . . . . . . . . . . . 350

44.7 Ionosphere Removal . . . . . . . . . . . . . . . . . . . . . . . . . 35144.7.1 Ionosphere-Free White Noise Variance for �NEi

j (Cycles) . 35344.7.2 Ionosphere-Free White Noise Variance for �� (cm) . . . . 355

44.8 First Di¤erences on NEij . . . . . . . . . . . . . . . . . . . . . . . 358

44.8.1 Remove USER Clock Phase Perturbations . . . . . . . . . 35844.8.2 Root-Variance Mappings . . . . . . . . . . . . . . . . . . . 359

44.9 Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36044.10Partials and Covariance . . . . . . . . . . . . . . . . . . . . . . . 360

44.10.1Single Frequency . . . . . . . . . . . . . . . . . . . . . . . 36044.10.2Two-Frequency Ionosphere Removal . . . . . . . . . . . . 36144.10.3First Di¤erences on NEi

j . . . . . . . . . . . . . . . . . . . 36244.11Receiver Clock Error Model . . . . . . . . . . . . . . . . . . . . . 363

44.11.1Covariance on Clock Phase . . . . . . . . . . . . . . . . . 36344.11.2Simulations . . . . . . . . . . . . . . . . . . . . . . . . . . 36544.11.3Filter Time Update for Receiver Clock . . . . . . . . . . . 36644.11.4State Estimate Parameters . . . . . . . . . . . . . . . . . 367

CONTENTS xvii

45 GPS Navigation Solution 36945.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36945.2 Algorithm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 369

XII Global Positioning System (GPS) Ground Receivers373

46 GPS Composite Clock 37546.1 GOMA-E . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37546.2 Tutorial . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 375

46.2.1 Simulation Narrative . . . . . . . . . . . . . . . . . . . . . 37546.2.2 Similarity in Clock Parameter Variations . . . . . . . . . 37646.2.3 Optimal Estimation of the UVCC . . . . . . . . . . . . . 37746.2.4 Real World Application . . . . . . . . . . . . . . . . . . . 377

XIII Appendices 383

A. The Least Squares Quadratic 385

B. Sequential Least Squares 387

C. Ad-Hoc Batch Filter 391

D. Kalman�s Model Equation 395.0.5 Measurements at tj = tk+1; tk+2; : : : . . . . . . . . . . . . 395

xviii CONTENTS

List of Figures

3.1 Gaussian Density Function f(x) . . . . . . . . . . . . . . . . . . . 203.2 Gaussian Distribution Function F(x) . . . . . . . . . . . . . . . . 21

7.1 Variable Lag Smoother with EKF and FES . . . . . . . . . . . . 427.2 Estimation of Velocity at Fixed Epochs with EKF and FES . . . 43

12.1 Exponential Transition-Correlation Function and Half-Life Func-tion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

12.2 24 Unbiased Vasicek Sequences . . . . . . . . . . . . . . . . . . . 8912.3 24 Biased Vasicek Sequences . . . . . . . . . . . . . . . . . . . . . 89

16.1 Sigma for Relative Error in Air Density . . . . . . . . . . . . . . 123

17.1 Dual-Cone Eclipse Geometry . . . . . . . . . . . . . . . . . . . . 13617.2 Baker�s Solar Obscura . . . . . . . . . . . . . . . . . . . . . . . . 136

19.1 Unit Thrust Referred to Maneuver Frame . . . . . . . . . . . . . 148

22.1 Station Longitude Rotation . . . . . . . . . . . . . . . . . . . . . 17122.2 Geocentric Station Vector Basis . . . . . . . . . . . . . . . . . . . 17222.3 Station Position Vector . . . . . . . . . . . . . . . . . . . . . . . 17522.4 Geocentric vs Geodetic . . . . . . . . . . . . . . . . . . . . . . . . 17622.5 Vector Basis for Angles Measurements . . . . . . . . . . . . . . . 17922.6 Latitude Rotation . . . . . . . . . . . . . . . . . . . . . . . . . . 18122.7 Latitude Di¤erence Rotation . . . . . . . . . . . . . . . . . . . . 182

23.1 Azimuth-Elevation Description . . . . . . . . . . . . . . . . . . . 18623.2 Direction Cosines Description . . . . . . . . . . . . . . . . . . . . 19123.3 Unit Range Vector Right Ascension & Declination . . . . . . . . 196

33.1 Simulated Allan Variance Diagram . . . . . . . . . . . . . . . . . 257

36.1 Position Error vs Least Squares Fit Span . . . . . . . . . . . . . 272

41.1 Four TDRSS Range Vectors . . . . . . . . . . . . . . . . . . . . . 304

xix

xx LIST OF FIGURES

43.1 Earth-USER-NAVSTAR Vector Triangle . . . . . . . . . . . . . . 330

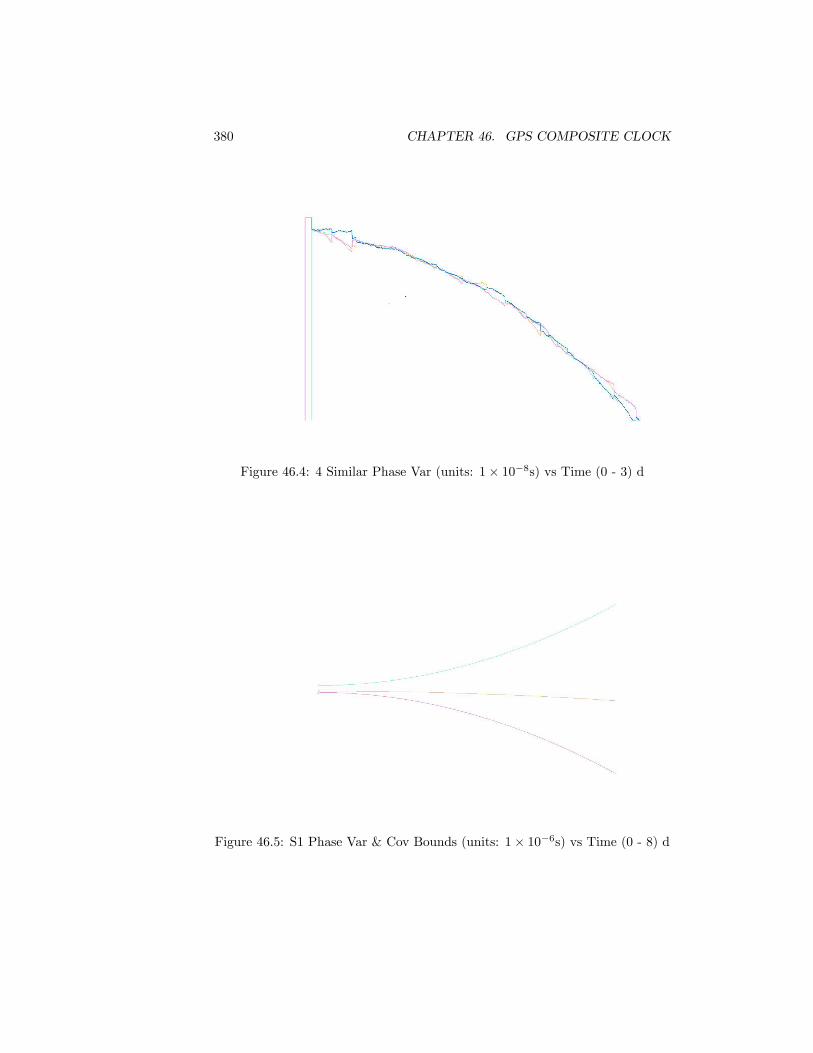

46.1 Sim Phase Dev (units: 1� 10�7s) vs Time (0 - 8) d . . . . . . . 37846.2 Sim & Est Phase Dev (units: 1� 10�7s) vs Time (0 - 8) d . . . . 37946.3 4 Similar Phase Var (units: 1� 10�7s) vs Time (0 - 8) d . . . . . 37946.4 4 Similar Phase Var (units: 1� 10�8s) vs Time (0 - 3) d . . . . . 38046.5 S1 Phase Var & Cov Bounds (units: 1� 10�6s) vs Time (0 - 8) d 38046.6 S1 Phase Var Reduced Cov (units: 1� 10�7s) vs Time (0 - 8) d . 38146.7 S1 Phase Var Reduced Cov (units: 1� 10�9s) vs Time (0 - 8) d . 38146.8 4 Similar Phase Var no IC (units: 1� 10�8s) vs Time (0 - 8) d . 382

0.1 Preface

Analytical Graphics presents here the mathematical speci�cations for its al-gorithms and software used to de�ne new capabilites for orbit determination.These capabilities are referred to as Orbit Determination Tool Kit (ODTK1).The initial purpose for this document was to enable the author to proceed

with the construction of new prototype software for the AGI ODTK methodsof orbit determination. Recording speci�c algorithm de�nitions, and their re-lations to appropriate hardware dynamics and spacecraft trajectory physics,enables and supports algorithm development, review, validation, modi�cation,and communication.This is a living document. Its secondary purpose is to provide relevant

mathematical speci�cations for ODTK users as the algorithms and software aredeveloped.This document is constructed and modi�ed using the Standard LaTeX Book

shell for Scienti�c Workplace 5.5 by MacKichan Software.

0.2 Acknowledgements

I am especially appreciative of the contributions by Dr. James Woodburn toODTK, and to this document. I thank Dick Hujsak and William Chuba foruseful suggestions in development of the �rst di¤erencing algorithm for GPSDoppler carrier phase count measurements.

0.3 US Patents

Patent No. US 6,708,116 B2, Method and Apparatus for Orbit Determination,was granted 16 March 2004.Patent No. US 7,050,002 B1, GPS Carrier Phase Measurement Representa-

tion and Method of Use, was granted 23 May 2006.

1ODTK was previously known as STK/OD.

Chapter 1

Introduction

Orbit determination refers to the estimation of orbits of small objects relativeto primary celestial bodies, given applicable measurements. All useful orbitdetermination methods produce orbit estimates that have errors.

1.1 Orbit Determination Classes

Orbit determination methods are partitioned by three classes: Initial orbit deter-mination (IOD), batch least squares di¤erential corrections (LS), and sequentialprocessing (SP). An orbit estimate output from IOD can be used as orbit esti-mate input to initialize LS, and an orbit estimate output from LS can be usedas orbit estimate input to initialize SP:266664

Initial Orbit Determination (IOD)+

Least Squares (LS)+

Sequential Processing (SP)

377775When there exists an orbit estimate su¢ cient to initialize SP, then IOD and LSare not required.

prior orbit est prior error cov size of est errors execution speedIOD No No Huge Very FastLS Yes No Small FastSP Yes Yes Small Fast Enough

Table 1.1: Compare Classes of OD Methods

1

2 CHAPTER 1. INTRODUCTION

1.1.1 IOD Methods

IOD methods input tracking measurements with tracking platform locations,and output spacecraft orbit estimates. No prior orbit estimate is required,and when used, it is assumed that no prior orbit estimate exists; however, or-bit estimation errors are usually very large. IOD methods are nonlinear andsix-dimensional. Measurement editing is not possible during IOD calculationsbecause no prior orbit estimate exists. IOD methods were derived by various au-thors: LaPlace, Poincaré, Gauss, Lagrange, Lambert, Gibbs, Herrick, Williams,Stumpp, Lancaster, Blanchard, Gooding, and Smith. The orbit determinationprocess is frequently begun, or restarted, with IOD.

1.1.2 LS Methods

The LS method requires the input tracking measurements with tracking plat-form locations and a prior orbit estimate. The LS method outputs a re�nedorbit estimate. Estimation errors are small when compared to IOD outputs.LS methods consist of a sequence of linear LS (di¤erential) corrections wheresequence convergence is de�ned a minimization of the (weighted) sum of squaresof measurement residuals. The sum of squares is represented by Eqs. 35.1, 35.5,and 35.7. Minimization is characterized by Eqs. 35.8 and 35.9. LS methodsproduce re�ned orbit estimates in a batch mode, together with error-covariancematrices that are optimistic; i.e., LS orbit element error variance estimates aretypically too small, relative to truth, by at least an order of magnitude. LSmethods require an inversion of an n � n LS information matrix for each LSiteration, where n is state estimate size. This inversion is problematic whenthe information matrix is ill-conditioned, which is frequently the case in orbitdetermination applications of LS. Operationally, LS may be the only methodused, or, it may be used to initialize SP. The existence of a prior orbit estimateenables operational measurement residual editing, but LS methods frequentlyrequire inspection and manual measurement editing by human intervention. LSalgorithms therefore require elaborate software mechanisms for measurementediting. Gauss reputedly developed LS as early as 1795 and used it to deter-mine the orbit of Ceres in 1801, although he did not publish his account of ituntil the method had already been independently developed and published byLegendre. [25].

1.1.3 SP Methods

SP methods require the input of tracking measurements with tracking plat-form locations, priori state estimates (including an orbit estimate), and a priorstate-error covariance matrix. SP methods output re�ned state estimates in asequential mode. SP �lter methods process forward in time, repeating a re-curring, two-step sequence of �lter time-update of the state estimate and �ltermeasurement-update of the state estimate. The �lter time-update propagatesthe state estimate forward, and the �lter measurement-update incorporates the

1.1. ORBIT DETERMINATION CLASSES 3

next measurement.The recursive sequence requires an important interval of �lter initialization.

Often the state-error covariance is unrealistic during the �lter-initialization timeinterval because the error covariance matrix associated with the a priori orbitestimate is unknown. A signi�cant number of observations must be processedto bring the covariance to a realistic scale. Conceptually, the �lter has beeninitialized once the state covariance becomes realistic; in practice, the �lter isconsidered initialized after having processed a prescribed number of observa-tions.No matrix inversions are performed during �lter calculations. SP smoother

methods process backward in time, repeating a pattern of state-estimate re-�nement using �lter outputs and backwards transition. Matrix inversions arerequired by the smoother algorithm. Computations for both �lter and smootherare dominated most signi�cantly by numerical orbit propagations. The searchfor non-stationary sequential processing was begun by Kalman [48], Bucy [9],Rauch [96], Meditch [76], and others.

1.1.4 "Batch Filter" (Sequential LS) Methods

The batch �lter (Appendix C), BF, is a hybrid algorithm that combines prop-erties of LS with properties of SP. The BF is suggested by inspection of thesequential form of batch least squares (Appendix B). This sequential form ismodi�ed ad hoc by in�ating the covariance associated with previous data. TheBF can be derived by adding a second term ad hoc to the LS quadratic form.The �rst term minimizes the sum of squares of weighted measurement residu-als, while the second term binds the new state estimate to the previous stateestimate. This two-term quadratic form is referred to as a maximum-liklihoodperformance function. Matrix inversion is required by the BF, as in LS. TheBF was proposed by Swerling [103].

1.1.5 Optimal Orbit Determination

Optimal orbit determination (OOD, de�ned in the sequel), depends on the useof an optimal sequential-�lter design. For current time and future time, thesequential �lter output is used directly. For past time, the �lter execution isfollowed by the execution of a �xed interval sequential smoother. The smoothedtrajectory estimates are more accurate than �ltered trajectory estimates.

Comparison of OOD with LS

It is useful to compare OOD with LS because many systems use LS to provideoperational end-products. Table 1.2 presents several operational capabilitiesthat distinguish OOD from LS. In particular, OOD allows for the estimationof time-varying parameters, compared to the estimation of static parametersfor LS. In defense of LS, a time-dependent sequence of static parameters maybe estimated with LS, thereby approximating a time-variable; however, this is

4 CHAPTER 1. INTRODUCTION

OOD LSReal-time orbit determination Yes No

Force model error structure Yes No

The more data the better Yes No

Realistic error covariance Yes No

Autonomous data editing Yes No

Realistic performance assessment Yes No

Estimate time-varying meas biases Yes No

Estimate time-varying atmospheric density Yes No

Estimate time-varying solar pressure Yes No

Estimate time-varying transponder bias Yes No

Minimize orbit estimate errors Yes No

Reinitialize for maneuvers No Yes

Table 1.2: OOD vs LS

done at the expense of increasing the LS state-estimate structure for each time-constant. This puts a burden on the analyst to ensure that each time constantis observable (otherwise there will be problems with the LS matrix inversion).OOD handles time-variability autonomously with a single state estimate para-meter, and the OOD �lter performs no matrix inverse. OOD smoother matrixinverses are invertable .Consider the estimation of an air drag parameter. The analyst cannot antic-

ipate when atmospheric density will respond to a coronal mass ejection (CME)during solar maximum, nor the time of �rst measurement following the timeof CME impact. Thus, there is no convenient way to appropriately partitionsequential time-constants for LS. For OOD, the �lter gain on the atmosphericdensity parameter estimate will be open due to its associated use of KP andF10:7 to drive the state-estimate error covariance. When the �rst measurementfollowing the time of CME impact is encountered, correction of the atmosphericdensity parameter estimate will commence at the time tag of that measurement.

1.2 Notation

1.2.1 Coordinate Frames

In the notation that follows, we shall align each vector basis with one of threedextral orthogonal coordinate frames: Inertial, Gaussian, and Frenét. That is tosay, each of the three coordinate axes of each coordinate frame shall be colinearwith one of the three unit vectors, for each associated vector basis. The origin ofeach vector basis shall also be coincident with its associated coordinate frame.The positive direction for each coordinate axis is de�ned by the direction of the

1.2. NOTATION 5

associated unit vector.

Inertial Vector Basis

Let us denote the Earth centered inertial (ECI) orthonormal vector basis forthe International Celestial Reference Frame (ICRF) by the "vectrix" [38]:

[i] =

24 i1i2i3

35 (1.1)

where:

[i]T= (i1; i2; i3) ; (1.2)

where i3 is coincident with the conventional pole (Z-direction) of ICRF, wherei1 and i2 are contained in equatorial plane of the ICRF (where i1 is in the X-direction), and where i2 = i3 � i1.1 It is convenient to associate the origin ofthe inertial vector basis with center of mass of the Earth.

Gaussian Vector Basis

Inertial spacecraft position and velocity vectors are denoted with r and _r. Theorthonormal Gaussian vector basis:

[u] =

24 u1u2u3

35 ; (1.3)

with origin at the spacecraft center of mass, is anchored to the ECI spacecraftposition vector r:

u1 � U = r=r = [i]T

24 U1U2U3

35 (1.4)

where:

r =pr � r (1.5)

Orbit angular momentum h:

h = r� _r (1.6)

enables de�nition of u3:

u3 �W = h=h = [i]T

24 W1

W2

W3

35 (1.7)

1Prior to ODTK 6, the Earth-centered inertial (ECI) frame was aligned with mean equatorand mean equinox at epoch J2000.

6 CHAPTER 1. INTRODUCTION

where:

h =ph � h (1.8)

The triad is completed with:

u2 = u3 � u1 = [i]T24 V1V2V3

35 (1.9)

The rotation 3 x 3 matrix Rui from [i] to [u] :

[u] = Rui [i] (1.10)

where:

Rui =

24 U1 U2 U3V1 V2 V3W1 W2 W3

35 (1.11)

Note that:

[u]T= [i]

TRTui (1.12)

It is convenient to associate the origin of the Gaussian vector basis with centerof mass of a space object.

Frenét Vector Basis

The orthonormal Frenét vector basis:

[f ] =

24 f1f2f3

35 ; (1.13)

with origin at the spacecraft center of mass, is anchored to the ECI spacecraftvelocity vector _r:

f2= _r= _s = [i]T

24 f21f22f23

35 (1.14)

where:

_s =p_r � _r (1.15)

In common with the Gaussian frame, adopt:

f3 = u3 = [i]T

24 f31f32f33

35 (1.16)

1.2. NOTATION 7

The triad is completed with:

f1 = f2 � f3 = [i]T24 f11f12f13

35 (1.17)

The rotation 3 x 3 matrix Rfi from [i] to [f ] :

[f ] = Rfi [i] (1.18)

where:

Rfi =

24 f11 f12 f13f21 f22 f23f31 f32 f33

35 (1.19)

Note that:

[f ]T= [i]

TRTfi (1.20)

It is convenient to associate the origin of the Frenét vector basis with center ofmass of a space object.

1.2.2 Spacecraft Vectors and Components

Position, Velocity, and Acceleration

The spacecraft position, velocity, and acceleration vectors are denoted with r,_r, and �r. Then 3� 1 matrices z, _z, and �z for spacecraft position, velocity, andacceleration components can be represented:

r = [i]Tz (1.21)

_r = [i]T_z (1.22)

�r = [i]T�z: (1.23)

where:

z =

24 z1z2z3

35 (1.24)

_z =

24 _z1_z2_z3

35 (1.25)

�z =

24 �z1�z2�z3

35 (1.26)

8 CHAPTER 1. INTRODUCTION

Position and Velocity Errors

Spacecraft position, velocity, and acceleration vector errors are denoted with �r,� _r, and ��r. Then 3� 1 matrices for instantaneous spacecraft position, velocity,and acceleration error components are represented with:

�r = [i]T�z = [u]

T�y (1.27)

� _r = [i]T� _z = [u]

T� _y (1.28)

��r = [i]T��z = [u]

T��y (1.29)

where:

�z =

24 �z1�z2�z3

35 =24 �r � i1�r � i2�r � i3

35 (1.30)

�y =

24 �y1�y2�y3

35 =24 �r � u1�r � u2�r � u3

35 (1.31)

and where the time derivatives follow by putting appropriate dots over �r;�z;and �y. Insert Eq. 1.12 into Eq. 1.27 to get:

�z = Riu�y (1.32)

�y = Rui�z (1.33)

where:

Riu = RTui (1.34)

1.2.3 Numerical Orbit Propagation

Notation

Concatenate the 3 x 1 position and velocity component arrays z and _z to formthe orbit substate:

Z =

�z_z

�=

26666664z1z2z3_z1_z2_z3

37777775 =26666664Z1Z2Z3Z4Z5Z6

37777775 (1.35)

where Z is dynamic: Z � Z (t).

1.3. MATHEMATICAL OPERATORS FOR SP METHODS 9

Let 'z denote the Variation of Parameters in Universal Variables orbit prop-agator. Given an initial time t0, a �nal time tf , and an acceleration modelu (Z (t) ; t), then 'z propagates Z (t0) from t0 to tf using u (Z (�) ; �) to obtainZ (tf ). This may be expressed as:

Z (tf ) = 'z ftf ; Z (t0) ; t0; u (Z (�) ; �) ; t0 � � � tfg (1.36)

If by 'z we always imply the use of u (Z (t) ; t), then we get a very compactnotation for Variation of Parameters in Universal Variables:

'z ftf ; Z (t0) ; t0g � 'z ftf ; Z (t0) ; t0; u (Z (�) ; �) ; t0 � � � tfg (1.37)

That is:

Z (tf ) = 'z ftf ; Z (t0) ; t0g (1.38)

Ideally, 'z satis�es the nested transitivity property:

Z (tk+2) = 'z ftk+2; Z (tk) ; tkg = 'z ftk+2; 'z ftk+1; Z (tk) ; tkg ; tk+1g(1.39)

Note that 'z is a column matrix with 6 elements:

'z =

2666664'z1'z2'z3...'z6

3777775 (1.40)

1.3 Mathematical Operators for SP Methods

1.3.1 Subscript Notation

State Matrices

The state estimate X is referenced at two separate times by using the notation[76]:

Xjji � X (tj jti) (1.41)

where i, j 2 f0; 1; 2; : : :g. The time tj to the left of the vertical bar denotesthe epoch of X which drives the �lter time-update function. The time ti to theright of the bar denotes the time-tag of the last measurement processed to formX, which drives the �lter measurement-update function. For example, X7j6refers to the state estimate at time t7, given the last measurement processedat time t6, whereas X7j7 refers to the state estimate at time t7, given the last

10 CHAPTER 1. INTRODUCTION

measurement processed at time t7. X7j6 was obtained by �lter time-update ofX6j6 from t6 to t7.Similar notation is used for the state-estimate correction:

�Xjji � �X (tj jti) (1.42)

and the state-estimate-error covariance matrix:

Pjji � P (tj jti) (1.43)

Measurement Matrices

We denote a measurement taken at time tj as yj . We also denote a conditionalmeasurement estimate (representation) at time tj as yjjh.

1.3.2 Nonlinear Operators

Nonlinear operators are required in the state estimate time update and the stateestimate measurement update for SP methods of orbit determination.

State Propagation

Let ' denote a nonlinear operator that propagates the state estimate Xijh fromtime ti to time tj :

Xjjh = 'ntj ; Xijh; ti

o(1.44)

Measurement Representation

Let y (�) denote a nonlinear operator that calculates the measurement represen-tation yjjh, given the state estimate Xjjh:

yjjh = y�Xjjh; tj

�(1.45)

1.3.3 Linear Operators

State Estimate Error Propagation

Let �j;i � � (tj ; ti) denote the linear operator that propagates the state errorestimate �Xijh from time ti to time tj

�Xjjh = �j;i�Xijh (1.46)

where

�j;i =

�@Xj

@Xi

�Xjjh

(1.47)

and where evaluation derives from Xjjh.

1.4. DOCUMENT PARTITION 11

Measurement Residual

Let �yj denote the linear operator that de�nes the measurement residual attime tj :

�yj = yj � yjjh (1.48)

which re�ects the discrepancy between the predicted measurement and theactual measurement at time tj . Some authors refer to �yj as "measurementinnovation".

Measurement/State Partials Jacobian

Let Hj denote the Jacobian of the measurement with respect to the state partialderivatives at time tj :

Hj =

�@yj@Xj

�Xjjh

(1.49)

where evaluation derives from Xjjh.

1.4 Document Partition

This document has the following ordered parts:

1. Optimal Orbit Determination

2. Stochastic Sequences

3. Accelerations

4. Spacecraft Attitude

5. State Error Transition

6. Ground Location Estimation

7. Measurements

8. Deep Space Network (DSN)

9. Least Squares (LS)

10. Initial Orbit Determination (IOD)

11. Tracking and Data Relay Satellite System (TDRSS)

12. Global Positioning System (GPS)

13. Appendices

12 CHAPTER 1. INTRODUCTION

Part I

Optimal OrbitDetermination

13

Chapter 2

Optimal OrbitDetermination (OOD)

As previously mentioned, orbit determination refers to the estimation of orbitsof small objects relative to primary celestial bodies, given applicable measure-ments. But what is optimal orbit determination? The purpose of this chapteris to answer the question.

The adjective optimal refers to most desirable, most favorable, or most sat-isfactory [112]. But most satisfactory to whom? There are choices to make fromavailable orbit determination methods. Should we prefer the fastest methodsor the most accurate? Should we prefer sequential methods or batch methods?Should we minimize the size of the weighted measurement residuals or the sizeof orbit errors? How should we model measurement residuals and orbit errors?

All orbit determination problems are multidimensional and nonlinear,butshould we attempt a multidimensional nonlinear solution directly? Or, shouldwe use a linearization method? If so, is there a preferred method for lineariza-tion?

2.1 De�nitions

2.1.1 State Estimate Reference for Linearization of SPMethods

Evaluation of the measurement representation yjjh de�ned by Eq. 1.45 requiresthe use of some prior state estimate Xjjh, where tj � th and where Xjjh is thestate estimate reference for linearization. A similar requirement is associatedwith Eqs. 1.47 and 1.49.

15

16 CHAPTER 2. OPTIMAL ORBIT DETERMINATION (OOD)

2.1.2 Local Linearization

Let tk and tk+1 � tk be the times of adjacent ordered measurements yk andyk+1, for k 2 f0; 1; 2; : : :g. That is, there are no measurements between yk andyk+1. Then the use of Xk+1jk as the state estimate reference for all linearizationsat time tk+1 de�nes local linearization at time tk+1.The use of any state estimate reference other than Xk+1jk at time tk+1 for

linearization is a non-local linearization at time tk+1.

2.1.3 Global Linearization

Given the integer variable k 2 f0; 1; 2; : : :g and given a �xed non-negative integerj, the use of Xkjj as the state estimate reference for linearization at time tk foreach k is known as global linearization.

2.1.4 Observability

A particular parameter is observable to a particular measurement if and onlyif the sequential processing of that measurement reduces the estimated errorvariance on that parameter.

2.1.5 Completeness

The state estimate structure is complete if and only if all parameters with un-known observable components are included in the state estimate structure.

2.1.6 Optimal Orbit Determination

By optimal orbit determination, the method used to calculate the state estimate(including the orbit estimate) satis�es the following conditions:

1. Sequential processing (SP) is used to account for force modeling errors andmeasurement information in the time order in which they are realized.

2. Sherman�s Theorem is applied [100],[101],[76],[48]. To summarize, theoptimal state estimate correction matrix �X is the expectation of thestate error matrix �X given the measurement residual matrix �y. Thatis: �X = E f�Xj�yg.

3. Linearizations of state-estimate time transition and state-to-measurementrepresentations are local in time, not global.

4. The state estimate structure is complete.

5. All state-estimate models and state-estimate-error model approximationsare derived from the appropriate physics of sensors and force modeling.

2.1. DEFINITIONS 17

6. All measurement models and measurement-error model approximationsare derived from the appropriate sensor hardware de�nitions and associ-ated physics, and measurement sensor performance.

7. Necessary conditions for real data include:

� Measurement residuals approximate Gaussian white noise[76][84]

� McReynold�s �lter-smoother consistency test is satis�ed.

8. For simulated data, the state-estimate errors agree with the state-estimateerror covariance function.

The �rst six conditions de�ne standards for optimal algorithm design andfor the establishment of a realistic state-estimate error covariance function. Thelast two conditions enable validation: they de�ne realizable test criteria foroptimality.

2.1.7 Discussion

Sherman�s Theorem

As a lemma to Sherman�s Theorem [76], one achieves minimum state-estimateerror variance (and thus, minimum orbit-estimate error variance). Of the variousextremalization criteria available, this one most directly addresses errors in theorbit elements.

Complete State Estimate

Consider any case where the state estimate structure is incomplete. Any com-ponent of an observable parameter neglected in the state estimate structure willalias into the estimated orbit elements, signi�cantly degrading them. Thus,one needs an appropriate place in the state estimate structure to put everyobservable e¤ect.

Gaussian White Noise

What is it? In one dimension, one may think of a Gaussian white noise se-quence as a sequence of ratios from a random walk sequence Rj , j 2 f0; 1; 2; : : :g.The numerator in each ratio is the di¤erence (Rj+1 �Rj) in the random walkfunctional across a speci�ed time interval [tj ; tj+1], and the denominator is theassociated time di¤erence (tj+1 � tj). The ratio limit (tj+1 � tj) �! 0 doesnot exist [18]. Thus, one must always use Gaussian white noise in a granularmanner. The Wiener-Levy (random walk) sequence developed in Papoulis [92]provides appropriate results for useful application, and is discussed in the sequel.

18 CHAPTER 2. OPTIMAL ORBIT DETERMINATION (OOD)

Relevance to Observations Gaussian white noise models are appropriatefor thermal noise associated with resistance in electronic circuits [98]. Thus,Gaussian white noise is used directly for modeling stochastic phenomena inclocks, transmitters, receivers, and sensors. Range and Doppler measurementscontain Gaussian white noise.Gauss used a Gaussian white noise model for orbit determination to represent

noise in angles right ascension and declination [25].

Applicability to Linear Systems Gaussian white noise is appropriate, in-directly, as a linear system input to develop a Gaussian stochastic output func-tional with particular serial correlation properties. This provides a convenientmethod to represent stochastic modeling errors in some cases. But in othercases, this method is useless; e.g., for acceleration modeling errors that derivefrom errors in modeling the geopotential.

"Colored" Spacecraft Acceleration Model Errors Acceleration model-ing errors that derive from errors in modeling the geopotential, atmosphericdensity, and solar photon pressure are random and nonstationary, but they arenot white. Correlation of errors in the time domain are sometimes said to be"colored" noise.

Chapter 3

Fundamental Theorem ofEstimation

Measurement-error processes and force-model-error processes are modeled asGaussian (normal) random functionals for orbit determination. Therefore, alldistributions considered herein are Gaussian. The Fundamental Theorem of Es-timation requires symmetry and left-hand convexity of the distribution functionused for estimation. Both requirements are satis�ed by Gaussian distributions.

3.1 Gaussian Probability Density Function

The Gaussian density function f (x) on scalar random variable x is de�ned by[25]:

f (x) =1

�p2�exp

�(x� �)2 =

�2�2��

(3.1)

where � is the mean value of x, and � is the root-variance of x about �. Figure3.1 displays f (x) for � = 0 and � = 1.

3.1.1 Sample Data

It can be di¢ cult to see whether a sample is normally distributed - especiallyif the sample size is small - unless an objective test is employed. For example,a histogram of 100 standard normal deviates cannot be expected to preciselyfollow Figure 3.1. Statistical hypothesis tests of the normality assumption areuseful in such cases [108].

3.1.2 Multidimensional Gaussian Random Variable

Let �X denote an n � 1 matrix Gaussian random variable, and let �X denotea particular realization of �X. Let us denote the mean value of �X with �,

19

20 CHAPTER 3. FUNDAMENTAL THEOREM OF ESTIMATION

3 2 1 0 1 2 3

0.1

0.2

0.3

0.4

x

y

Figure 3.1: Gaussian Density Function f(x)

and the covariance matrix of �X with P . Then the Gaussian density functionf (�X) � f�X (�X) on the multidimensional random variable �X is de�ned by:

f (�X) =1

(2�)n=2 jP j1=2

exp

��12(�X � �)T P�1 (�X � �)

�(3.2)

Equation 3.2 is also known as the multivariate normal distribution.

3.2 Gaussian Cumulative Distribution Function

The integration of the Gaussian probability density function Eq. 3.1 generatesthe Gaussian cumulative (probability) distribution function F (x) � Fx (x):

Fx (x) =

Z x

�1fx (w) dw (3.3)

so that:

Fx (x) = Pr fx < xg (3.4)

where Pr fx < xg is the "probability that x is less than x."Figure 3.2 displays F (x). Note that F (x) is symmetric about its mean

� = 0:

F (x) = 1� F (�x) (3.5)

and that F (x) is convex for all x � � (left-hand convexity)1 , � = 0:

1The right-hand side of Ineq. 3.6 speci�es an ordinate on a straight line, where thatline crosses F (x) at points x1 and x2. Given values for x1, x2 , and �, then the argument

3.2. GAUSSIAN CUMULATIVE DISTRIBUTION FUNCTION 21

3210123

1

0.8

0.6

0.4

0.2

0

Figure 3.2: Gaussian Distribution Function F(x)

F (�x1 + (1� �)x2) � �F (x1) + (1� �)F (x2) (3.6)

where 0 � � � 1.Symmetry and convexity properties are required for any cumulative distrib-

ution function that is a candidate for optimal estimation. The Gaussian distri-bution function satis�es these requirements, but so do many other cumulativedistribution functions. Thus, even if real distributions for orbit determinationwere not quite Gaussian, symmetry and convexity is often satis�ed.

3.2.1 Central Limit Theorem

Let random variable x be the bounded sum of many small independent compo-nents with zero means, but where each component may derive from any distri-bution. Then x will have the Gaussian distribution Fx (x) de�ned by Eq. 3.3[21]. The central limit theorem, together with the Fundamental Theorem ofEstimation, supports the use of Gaussian distributions for orbit determination.

Application: Thermal Noise

Davenport and Root[98] states (p. 185): "The randomness of the thermallyexcited motion of free electrons in a resistor gives rise to a �uctuating voltagewhich appears across the terminals of a resistor. This �uctuation is known asthermal noise. Since the total noise voltage is given by the sum of a very largenumber of electronic voltage pulses, one might expect from the central limit

x = �x1 + (1� �)x2 for F (x), on the left-hand side of Ineq. 3.6, provides a value for F thatcan be compared to the ordinate on the straight line. Ineq. 3.6 requires that F (x) lie belowthe straight line when x � �. Symmetry speci�es an upside-down convexity for the right-handside of F (x).

22 CHAPTER 3. FUNDAMENTAL THEOREM OF ESTIMATION

theorem that the total noise voltage would be a Gaussian process. This canindeed be shown to be true."

3.2.2 Multidimensional Gaussian Random Variable

The n-fold integration of the Gaussian probability density function Eq. 3.2generates the Gaussian cumulative distribution function F (�X) � F�X (�X):

F�X (�X) =

Z �X

�1f�X (w) dw (3.7)

so that for each element F�Xj(�Xj) of F�X (�X):

F�Xj (�Xj) = Pr f�Xj < �Xjg , j � f1; 2; : : : ; ng (3.8)

For optimal sequential estimation it is important to note, when jP j = 0, thatF�X (�X) exists even when f�X (�X) does not exist. Since P is a symmetricmatrix, its determinant is the product of its eigenvalues. When one of its eigen-values is zero F�X (�X) continues to exist, and the optimal sequential �lter isstable. But for this case, least-squares estimators fail due to the least-squaresrequirement for existence of P�1.

3.3 Short Version of Fundamental Theorem

Given that the state estimate error column matrix �X is Gaussian and themeasurement residual column matrix �y is Gaussian, then the optimal estima-tor of the state error �X is the expected value of the state error �X given themeasurements of y:

�X = E f�Xjyg (3.9)

That is, the optimal estimator is the conditional mean. For proof, see Meditch[76], Corollary 5.1, page 162.

3.4 Complete Version of Fundamental Theorem

Complete hypotheses for the Fundamental Theorem of Estimation (Sherman�sTheorem) are satis�ed by many cumulative distributions that are not Gaussian[101]. But since there is little justi�cation for us to consider non-Gaussiandistributions for the orbit determination problem, the Short Version is su¢ cient.For the Complete Version of this important theorem, see Meditch [76], Theorem5.1, page 160. The original proof of this theorem has been attributed by Kalmanto Sherman [100] [101].

3.5. COMPARISON TO LEAST SQUARES 23

3.5 Comparison to Least Squares

For least squares we minimize the sum of squares of weighted measurementresiduals. For optimal estimation we minimize the expected value of the rootsum of squares on state estimate errors.

24 CHAPTER 3. FUNDAMENTAL THEOREM OF ESTIMATION

Chapter 4

Kalman�s Approach

Kalman presented two �ltering algorithms, or theorems, for sequential estima-tion: a �lter measurement-update theorem and a �lter time-update theorem.

4.1 Linearization

Kalman�s measurement-update theorem requires that the measurement repre-sentation be linearly related to the state, and his time update theorem requireslinearity in the state transition with time. Unfortunately, orbit determinationis nonlinear in the representation of all real measurements from the state, andis nonlinear in the time transition of the complete state. However, the orbitdetermination problem can be linearized either globally or locally.Under global linearization, a reference trajectory is propagated from a single

state estimate and �xed as the global time reference for deriving measurementresiduals and state errors. Kalman�s linear measurement-update theorem isapplied to the mapping from state error to measurement residual, and Kalman�slinear time-update theorem is applied to the time transition of state errors. Thestate error is de�ned to be the superposition of two di¤erences: the di¤erencebetween the �lter state estimate and the reference-trajectory state estimate,and the di¤erence between the reference-trajectory state estimate and the true(unknown) state. The �xed global reference for a �lter may be obtained from abatch least-squares estimate. Global linearization may also be used iterativelyby batch least squares.Local linearization means that multiple state estimates are referenced for

deriving measurement residuals and state errors.1 A new state estimate andassociated reference trajectory is calculated sequentially at each measurementtime. There are as many state estimates and associated references trajecto-ries as there are measurements. Kalman�s linear measurement-update theoremis applied to the mapping from the state error to measurement residual, and

1Applied to the Kalman �lter, local linearization is sometimes called an extended Kalman�lter.

25

26 CHAPTER 4. KALMAN�S APPROACH

Kalman�s linear time-update theorem is applied to the time transition of stateerror. The measurement-update theorem and time-update theorem are bothapplied at the time of the new state estimate. The state error is de�ned to bethe di¤erence between the (unknown) true state and the �lter state estimate.Global linearization erects a formidable barrier not present with local lin-

earization. Namely, the global reference trajectory itself has persistent unknownerrors, whereas the errors in the local reference trajectory may be removed (inpart) by the next measurement update, and are described by a realistic stateerror covariance function. The Fundamental Theorem of Estimation is directlyapplicable to state estimate errors referred to the true unknown state, whereasit is not applicable to state estimate errors referred to a global reference whoseerrors are unknown and cannot be removed. In the sequel ,we shall thereforeexclusively use and refer to local linearization.

4.2 State Estimate Error Model

Kalman�s state estimate error model is de�ned by the "formal" linear stochasticdi¤erential equation:

d

dt�X (t) = A (t) �X (t) +B (t) �! (t) (4.1)

where �X (t) is an n � 1 matrix, where �! (t) is a p � 1 Gaussian white noisematrix, where A (t) is an n � n time dependent matrix, and where B (t) is ann � p time dependent matrix. Comparing Eq. 4.1 to the least squares stateestimate error model

d

dt�X (t) = A (t) �X (t)

we see that we apparently now have a model to account for acceleration modelingerrors; i.e., let �! (t) denote the resultant of gravity modeling errors, air-dragmodeling errors, and solar pressure modeling errors.Equation 4.1 appears to have great power, but there is a technical di¢ culty.