October 2016 - Indo American Chamber of Commerce American Chamber of Commerce - GST...Transfer of...

17

Indo-American Chamber of Commerce Getting GST Ready! Sachin Agarwal October 2016

Transcript of October 2016 - Indo American Chamber of Commerce American Chamber of Commerce - GST...Transfer of...

Indo-American Chamber of Commerce

Getting GST Ready!

Sachin Agarwal

October 2016

Page 2

Contents

► Current Indirect Taxes Landscape

► GST Snapshot

► GST – Where we stand?

► Model GST Law

► Impact of GST

► GST Transformation: People,

Process, Tax & Technology

► Learnings from GST

implementation across the globe

► GST Implementation Roadmap

Page 3

Current Indirect Tax Structure in India

State TaxesEntertainment

tax

Electricity duty

Luxury tax

VAT 5 % to 14.5%

Customs duty -effective rate

29.4%

Central excise duty

12.5%

cesses

Service tax

15%

Central

Taxes

CST

Under the current tax system, multiplicity of taxes and cascading effect results in the overall increase of

the cost of the product and services

Entry tax

Local Body Taxes

Page 4

Broad base of taxation

Dual rate tax

Taxing principle

► Tax on supply of both goods and services

► Subsumed - Central Excise, Service Tax, VAT, Entry tax, CST,

etc.

► Dual GST - CGST & SGST levied on common base

► RNR rate ~ 18-20% (GST Council meeting- 6,12,18 & 26% plus

Central Cesses)

► IGST on inter-state supplies and import

► Decentralized registration and compliances

► Shift to destination based tax - Place of Supply Rules

► Seamless flow of input tax credit

► Threshold limit for Registration- INR 20 Lakhs / 10 Lakhs

GST –Key featureThe Tectonic Shift

Page 5

Existing Vs. Proposed FrameworkGeneral

TaxPresent Taxable

Event

Excise Manufacture

Service

Tax

Provision of Taxable

Service

VATIntra-State Sale of

Goods

CSTInter-State Sale of

Goods

TaxProposed Taxable

Event

GST Supply

Particulars Current tax regime Under GST Regime

Taxability

► Import of goods - Custom duty

► Domestic clearance of goods -

VAT/CST

► Providing of services - Service Tax

► Export of goods and services - No

tax

► Stock transfers against statutory

forms - No tax

► Import of goods – Basic custom

duty & IGST

► Sale of goods and provision of

services – CGST/SGST/IGST

► Stock transfers becomes taxable

► Statutory forms – likely to be

discontinued

► Export to be zero rated

Compliances► State wise for VAT

► Centralized for service tax

► Multiple State registrations

depending upon the State of

Supply

► Multiple returns e.g. inward

supplies, outward supplies etc.

Place of

Supply

► Goods are taxed in the State of

Origin

► Services are taxed as per Place of

Provision of Service rules

► Goods and Service location is

determine as per Place of

Supply Rules

Input Tax

Credit

► No cross utilization of taxes is

permitted and ultimately is a cost► Free Flow of Credit

Page 6

GST TimelineWhere we stand

► All legislative bills to be

passed in the winter session

of the Parliament and the

State assemblies

(November/

December 2016)

► Establishing Goods and

Services Tax Network

(GSTN) framework by

November 2016

► Testing of software with live

transactions by January

2017

► Outreach program as a part

of change management to

be completed by March 2017

► Go-live date is expected to

be 1 April 2017

GST likely rollout timeConstitutional Amendments

8 Sep 20161

Order appointing date for giving effect to

provision relating to Formation of GST

Council

12 Sep 2016

2

Formation of GST council

► Representation of Centre & States

► Finalizing Model Law and allied matters

including threshold, rates & exemptions

(60 days from the Order)

3

Passage of CGST/ IGST Bills by Parliament

(Centre)

&

Passage of SGST Bill by respective States

(Winter Session - Nov / Dec 2016)

4

Page 7

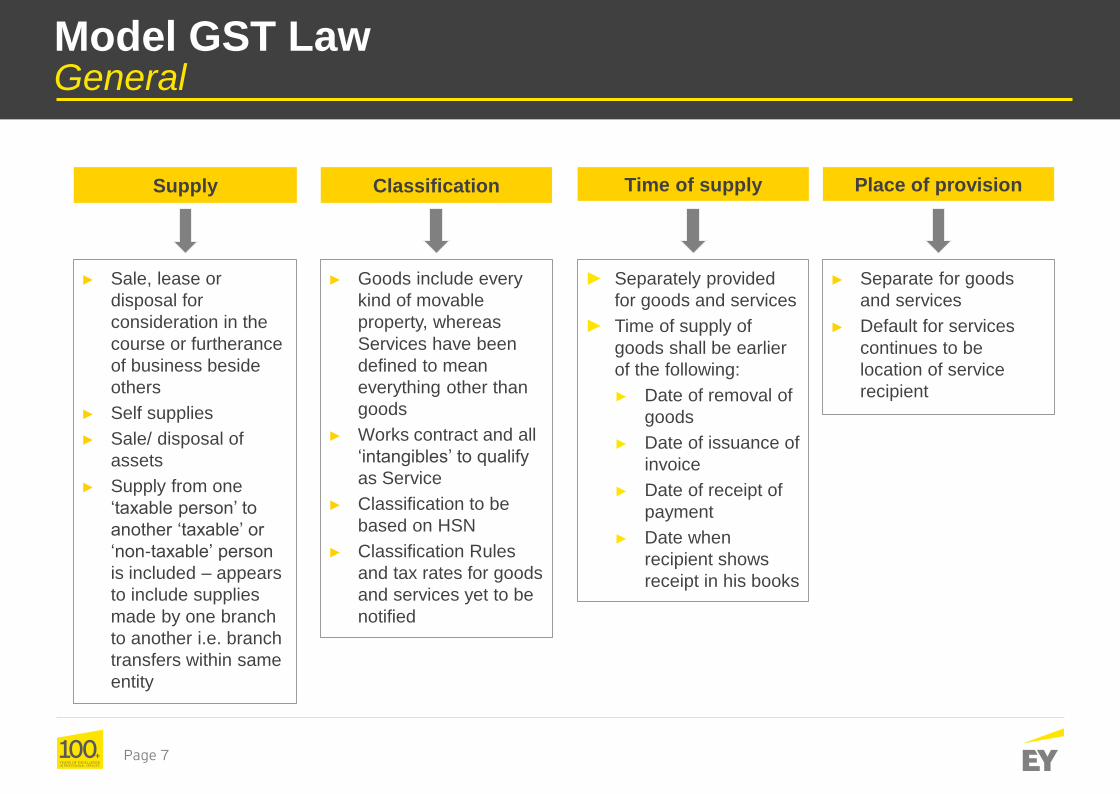

Model GST LawGeneral

► Separate for goods

and services

► Default for services

continues to be

location of service

recipient

Place of provisionTime of supply

► Separately provided

for goods and services

► Time of supply of

goods shall be earlier

of the following:

► Date of removal of

goods

► Date of issuance of

invoice

► Date of receipt of

payment

► Date when

recipient shows

receipt in his books

► Sale, lease or

disposal for

consideration in the

course or furtherance

of business beside

others

► Self supplies

► Sale/ disposal of

assets

► Supply from one

‘taxable person’ to

another ‘taxable’ or

‘non-taxable’ person

is included – appears

to include supplies

made by one branch

to another i.e. branch

transfers within same

entity

Supply

► Goods include every

kind of movable

property, whereas

Services have been

defined to mean

everything other than

goods

► Works contract and all

‘intangibles’ to qualify

as Service

► Classification to be

based on HSN

► Classification Rules

and tax rates for goods

and services yet to be

notified

Classification

Page 8

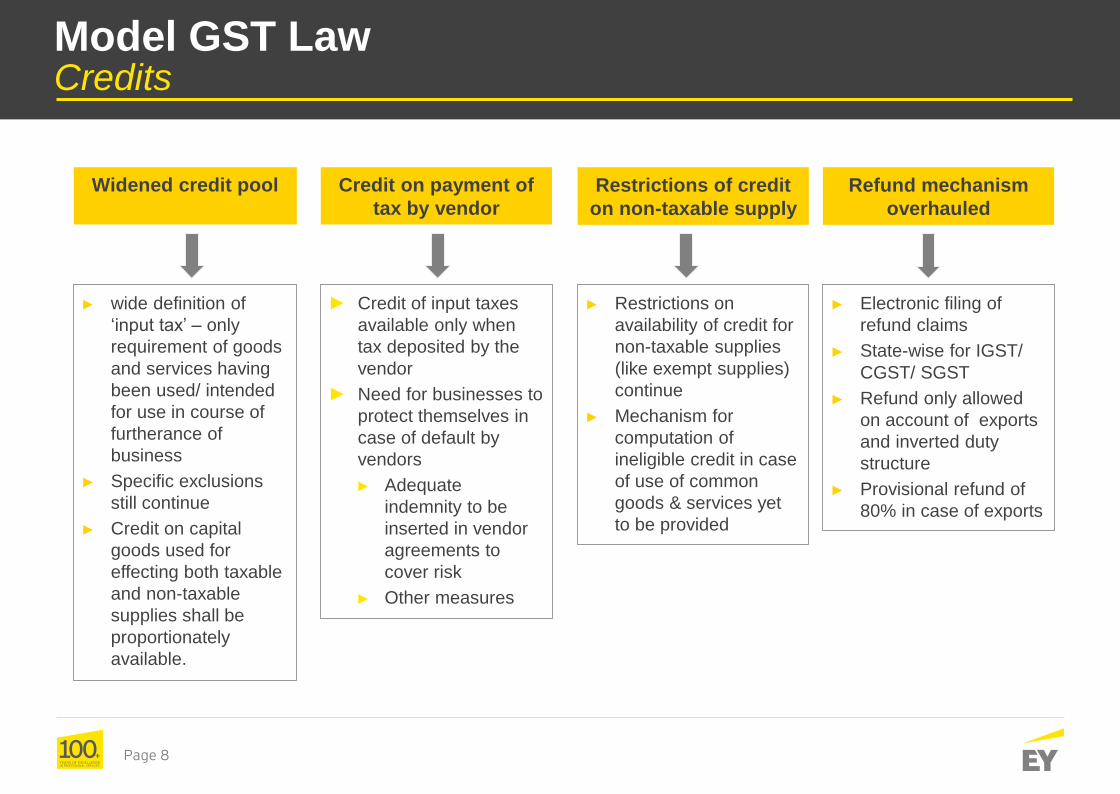

Model GST LawCredits

► wide definition of

‘input tax’ – only

requirement of goods

and services having

been used/ intended

for use in course of

furtherance of

business

► Specific exclusions

still continue

► Credit on capital

goods used for

effecting both taxable

and non-taxable

supplies shall be

proportionately

available.

Widened credit pool

► Restrictions on

availability of credit for

non-taxable supplies

(like exempt supplies)

continue

► Mechanism for

computation of

ineligible credit in case

of use of common

goods & services yet

to be provided

Credit on payment of

tax by vendor

► Credit of input taxes

available only when

tax deposited by the

vendor

► Need for businesses to

protect themselves in

case of default by

vendors

► Adequate

indemnity to be

inserted in vendor

agreements to

cover risk

► Other measures

► Electronic filing of

refund claims

► State-wise for IGST/

CGST/ SGST

► Refund only allowed

on account of exports

and inverted duty

structure

► Provisional refund of

80% in case of exports

Restrictions of credit

on non-taxable supply

Refund mechanism

overhauled

Page 9

Model GST LawValue of Supply

Supplier and recipient are not related

Price is the sole consideration

Transaction Value

Valuation Rules

Transaction at arm’s length price

Comparative Value – Goods/ services of like kind and quality supplied at same time to

other customer

Adjusted for difference in date of supply, quality, quantity and freight/ insurance

depending on place of supply

Computed value method – Cost + charges for design or brand + profit and general

expenses

Residual method – Value determined using reasonable means

Page 10

Model GST LawTransitional Provision

Provisional certificate of registration valid for 6 months issued to all

persons registered under the previous law

Every person to furnish prescribed information for issue of certificate

of registration

Carry forward of CENVAT credit/ input tax credit as disclosed in the

last return furnished

Transfer of credit permissible only when same is eligible under earlier

law as well as new law

Unavailed CENVAT credit on capital goods, not carried forward in a return to be allowed in certain situations

Credit of eligible duties and taxes in respect of inputs held in stock allowed in certain situations

Pending proceeding of appeal, revision, review initiated before the appointed day to be disposed of in accordance with the

provisions of the earlier law

Page 11

Paradigm Shift in Compliance- As per draft Rules

Return In relation to To be filed by

GSTR 1 Outward supplies

(sale, stock transfer,

export)

10 of next month

GSTR 2 Inward supplies

(purchases, import)

15th of next month

GSTR 3 Final Monthly return 20th of next month

GSTR 7 Tax deducted at

source

10th of next month

GSTR 9 Annual return 31st December of

next FY

ITC ledger Continuous

Cash ledger Continuous

Tax ledger Continuous

Return Time period To be filed by

Excise

ER 1 Monthly return 10th of next month

ER 4 Annual return 30th November of next FY

VAT return in each State

Monthly / Quarterly return As prescribed

Annual return As prescribed

Audit reports As prescribed

Service Tax

ST 3 (Half yearly)25 days from half year

end

Annual return 30th November of next FY

Present Compliance Regime GST Compliance Regime

Page 12

Tax Payer

GSTN

Uploading of supply details by 10th of

succeeding month

To file GSTR 1 by 10th

of succeeding month

Inward supply details in GSTR 2 to be auto

populated on basis of GSTR1 filed by supplier

Modifications in details and filing of GSTR 2 by

15th of succeeding month

Reconciliation to be done by 20th of

succeeding month

Pay tax

GSTR 3 to be filed by 20th of succeeding

month

Multiple inter-dependent return filing steps

Page 13

Transitional provisions

► Provisional certificate of

registration valid for six months

issued to all persons registered

under the previous law

► Input tax credit available under the

existing indirect tax law to

continue under the new GST

regime

Tax incentives

► Exemption on purchases for

export incentive zones (Export

Oriented Units, Software

Technology Parks of India Units)

may be discontinued

► Special Economic Zone benefit

likely to continue

► Area based exemption ~ Net

Refund

GST rate band

► Standard rate: 18% to 20% (GST

Council ~ 6% to 26%)

► Lower rate: 12% [essential goods

and services (pharma,

health/education services, etc.]

► Zero rate: Exports (exceptions

may include marketing support,

testing, cloud-based services,

etc.)

Some tax minutiae

► Place of supply / Time of supply ~

Specifics

► Transition stock ~ Inbuilt taxes

► Inter-unit transfers - Taxable

► Valuation principle for transfer –

Related party

► Input credit ~ Matching concept

► Sales return ~ reverse supply

ERP infrastructure & Change

management

► Requirement for GST compliant

ERP systems (invoicing, tax rates,

accounting/capturing taxes and

credits)

► Process mapping

► Employee related claim

documents, policies

► Contracts ~ GST clause

Compliance

► Transaction level details to be

reported

► Compliance to increase

significantly. Estimated 39

returns/statements in a year for

each state

► Reconciliation between supplier

and customer returns

Impact areas under GST

Page 14

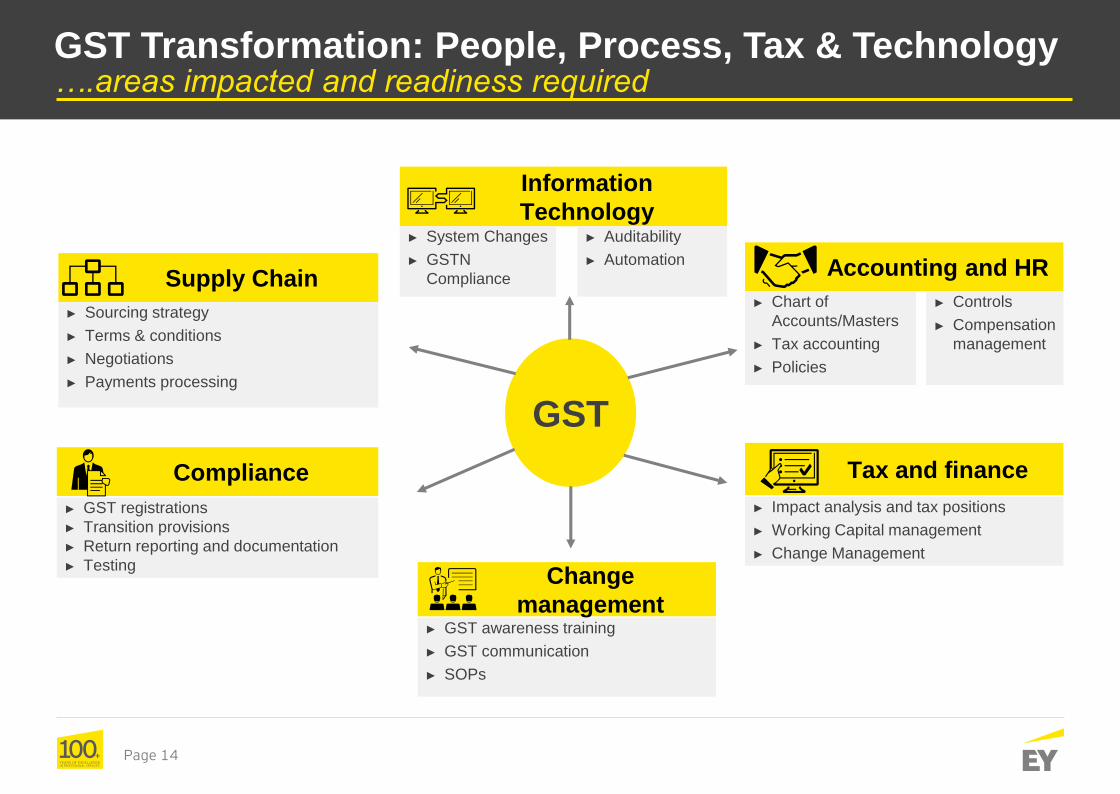

GST Transformation: People, Process, Tax & Technology….areas impacted and readiness required

► Sourcing strategy

► Terms & conditions

► Negotiations

► Payments processing

Supply Chain Accounting and HR

Tax and finance

Information

Technology

Compliance

Change

management

► Impact analysis and tax positions

► Working Capital management

► Change Management

► GST awareness training

► GST communication

► SOPs

► GST registrations

► Transition provisions

► Return reporting and documentation

► Testing

► System Changes

► GSTN

Compliance

► Auditability

► Automation

GST

► Chart of

Accounts/Masters

► Tax accounting

► Policies

► Controls

► Compensation

management

Page 15

Goal

2. 100% Compliance

3. Business value

creation

1. No business

disruptionTimely manage

risks and

opportunities

Start early:

Several months in

advance for readiness

and implementation

Significant impact

on policies,

procedures and

controls

IT implementation

takes time and

requires testing

Comprehensivene

ss: Mapping of all

possible scenarios

for flow of goods

and services

Governance

GST Steering

Committee, PMO

and Change

management are

critical

GST Insights

Learnings from GST implementation across the globe

Page 16

August/ Sept

2016

April 2017

and looking

ahead

On-boarding and kick off

Go – live and post implementation

Impact assessment

Business process design

Considerations

IT Implementation and testing

30- 50 days action plan:

► Mapping of scenarios and process heat maps

► IT landscape mapping and impact assessment

► Awakening the organization – GST workshops

Risk/opportunity

assessment

Steering

Committee /

PMO

Change

Management plan Technology

enablement

50-100 days implementation plan

► Policy/ SOP changes

► Transition/ Cut – over plan

► IT implementation and testing

► Go live and compliance testing

Transition plan/

cut over

GST Implementation Roadmap

Thank you

“This Presentation provides certain general information existing as at the time of production. This Presentation does not purport to identify all the issues or developments pursuant to the transaction. Accordingly, this presentation should neither be regarded as comprehensive nor sufficient for the purposes of decision-making. Ernst & Young does not undertake any legal liability for any of the contents in this presentation. The information provided is not, nor is it intended to be an advice on any matter and should not be relied on as such. Professional advice should be sought before taking action on any of the information contained in it. Without prior permission of Ernst & Young, this document may not be quoted in whole or in part or otherwise referred to in any documents.”