OCTOBER 2015 - PuneICAIpuneicai.org/wp-content/uploads/Newsletter_October_15.compressed.pdfSonesh...

8

2015 OCTOBER Pune VOL - IV - Issue No. 10

Transcript of OCTOBER 2015 - PuneICAIpuneicai.org/wp-content/uploads/Newsletter_October_15.compressed.pdfSonesh...

2015

OCTOBER

Pune VOL - IV - Issue No. 10

Success is a tasty dish. Patience, intelligence, knowledge and experience are its ingredients but hard work is that little salt that makes it delicious.

2News Letter Pune Branch of WIRC of ICAI/October 2015

CA. Shekhar SaneSpeaker - Seminar for CA students

on Amendment to Service Tax

CA. Chetan DagaSpeaker - Seminar on Clause by Clause

Analysis of Form 3CD

CA. Sanket ShahSpeaker - Seminar for CA students on the topic Accounting Standards

CA. Riddhi ChandakSpeaker - Study Circle Meet for

CPT Students on the Topic Law for CPT

WORKSHOP ON EMPLOYMENT AND CAREER GUIDANCE HELD AT ABEDA INAMDAR NIGHT COLLEGE, PUNE

Participants CA. Dashrath BaccheSpeaker

CA. Sonesh SanchetiSpeaker

CA Tushar PatelSpeaker

Participants

WORKSHOP ON EMPLOYMENT AND CAREER GUIDANCE HELD AT MMCC COLLEGE, PUNE

WORKSHOP ON EMPLOYMENT AND CAREER GUIDANCE HELD AT VISHWAKARMA COLLEGE, PUNE

WORKSHOP ON EMPLOYMENT AND CAREER GUIDANCE HELD AT

SARSWATI COLLEGE, BAJIRAO ROAD, PUNE

Ms. BucheSpeaker

Participants

Dear Members,

Greetings of the Season!

Finally September-2015 is over and the slogging & tiring work schedules are put to rest. The hustle & bustle of last month to catch-up with the deadlines for Tax Audit, Statutory Audit & Income Tax Returns filing was quite challenging.

October started with the grateful tribute to father of nation Mahatma Gandhiji and the stalwart leader and past prime minister of India Shri LalBahadur Shastri.

On the backdrop of the professional workloads during September at Branch level there was least activities for members, still a seminar on Clause by Clause Analysis of Form 3CD that was very useful and time specific for members as well the articled staff of members was conducted.

At Pune Branch topic-wise five study groups have been formed for preparation of the research papers, on topics:-

Integrated Reporting;

A study on the Impact of implementation of Ind AS 115 Revenue from Contract with Customers on different industries e.g., software, telecom, real estate etc.;

Issues in adoption of Accrual System of Accounting in government;

Accounting arising in not-for-profit sector in the context of Accounting Standards;

Impact of implementation of Ind AS;

The last date for completion of the assignment is 15th November, 2015. The members interested to join the study groups are welcome.

For students, from November-2015 exam preparation point various seminars on topics like Amendment to Service Tax, How to solve Audit paper of CA Final exam, Law paper for CPT, Accounting Standards, How to face CA examination, and motivation speech �Live, Don't Just Exist� were organized. The series of Career Counseling programmes in association with the Department of Commerce, Savitribai Phule Pune University continue in various schools and colleges.

Now the Branch is gearing up for the forthcoming period and planning

various CPE and other events, the details of which are published elsewhere in the Newsletter.

As usual my perennial request to please keep visiting our website www.puneicai.org from time to time and also, please make maximum use of the dedicated email id [email protected] where you can send email for any of your query/enquiry.

While concluding this message I take the opportunity to extend my best wishes for Dusserha and Deepawali. May these festivities bring in fresh ray of hope and confidence & refreshing breeze of happiness, health, peace and prosperity to you, your family members and friends.

Thanking you. With best regards�..!

Life is an echo, all comes back. The good, the bad, the false, the true; so give the world the best you have and the best will come back to you.

Plot No. 8, Parshwanath Nagar, CTS No. 333, Sr. No. 573, Munjeri, Opp. Kale hospital, Near Mahavir Electronics, Bibwewadi, Pune 411 037

Tel: (020) 24212251 / 52Web: www.puneicai.orgEmail: [email protected]

PUNE BRANCH OF WIRC OF ICAI

Chairman Communiqué

3News Letter Pune Branch of WIRC of ICAI/October 2015

Queries? Enquires? Problems? Dif�culties?

Mail us to [email protected]

Looking for Article Vacancy?

Visit to http://puneicai.org/articles-vacancy/

Download Pune ICAI Mobile App

for latest information on programme/updates

Anger is the false show of strength by a weak person while politeness and a cool mind reflect dignity and strength of a strong person.

NA

4News Letter Pune Branch of WIRC of ICAI/October 2015

5th Oct To 10th Oct, 2015

Series of seminar for Students on income tax & transfer pricing

ICAI Bhawan Bibvewadi, Pune-378 AM

To10 AM

NA

8th Oct To 15th Oct, 2015

Mock Test for Final & IIPC Students

Sinhgad Technical Education Society's - Smt. Kashibai Navale

College of Commerce, Erandwane, Karve Road, Pune -411004

2 PMTo

5 PMRs. 100/-

10th Oct, 2015Seminar on Preparation of Vat Audit & Way to GST ICAI Bhawan Bibvewadi, Pune-37

10 AMTo

1 PM

Rs. 300(For Members)

Rs. 100 (For Students)

10th & 11th Oct, 2015

Workshop on Advanced Power Point

IIFA Campus917/15 A, Vikas A, Ganeshwadi, Behind British Library, FC Road, Shivajinagar, Pune-411004

9:30 AMTo

5:30 PMRs. 2100/-

12th To 14th Oct, 2015

Lecture series on Companies Act ICAI Bhawan Bibvewadi, Pune-37

8 AMTo

10 AMRs. 200/-

15th Oct, 2015Seminar on Significant Accounting Policies ICAI Bhawan Bibvewadi, Pune-37

8 AMTo

10 AMRs. 200/-

16th Oct, 2015 Seminar on Transfer Pricing ICAI Bhawan Bibvewadi, Pune-375 PM

To8 PM

Rs. 300/-

16th & 17th Oct, 2015

Lecture Series on Audit under Maharashtra Co-operative Act

ICAI Bhawan Bibvewadi, Pune-378 AM

To10 AM

Rs. 200/-

17th Oct, 2015Young Members' Empowerment Programme ICAI Bhawan Bibvewadi, Pune-37

5 PMTo

8 PM

Fees Rs. 300/-(For Members

born on or after1/1/1985)

& Fees Rs. 500/-

(For other members)

17th Oct, 2015Seminar for Students How to Do financial Planning ICAI Bhawan Bibvewadi, Pune-37

8:30 AM To

10:30 AMNA

17th Oct to 1st Nov, 2015

Certificate Course on Concurrent Audit of Banks

CORONET Hotel 1205/4,Apte Road, Deccan Gymkhana, Pune-04

9:30 AMTo

5:30 PMRs. 12,500/-

18th Oct, 2015Seminar for Students-How to get Maximum out of your Articleship

ICAI Bhawan Bibvewadi, Pune-379 AM

To11 AM

NA

31st Oct, 2015Seminar on Challenges of Recent Recession ICAI Bhawan Bibvewadi, Pune-37

2 PMTo

5 PM

Rs. 300/- (For Members)

Rs. 100/- (For Students)

NA

3 Hrs

12 Hrs

2 Hrs

2 Hrs

3 Hrs

2 Hrs

3 Hrs

NA

36 Hrs

NA

3 Hrs

We do not always have to defend our self with words sometimes our silence gives people a clue that we have better thoughts and a better mind.

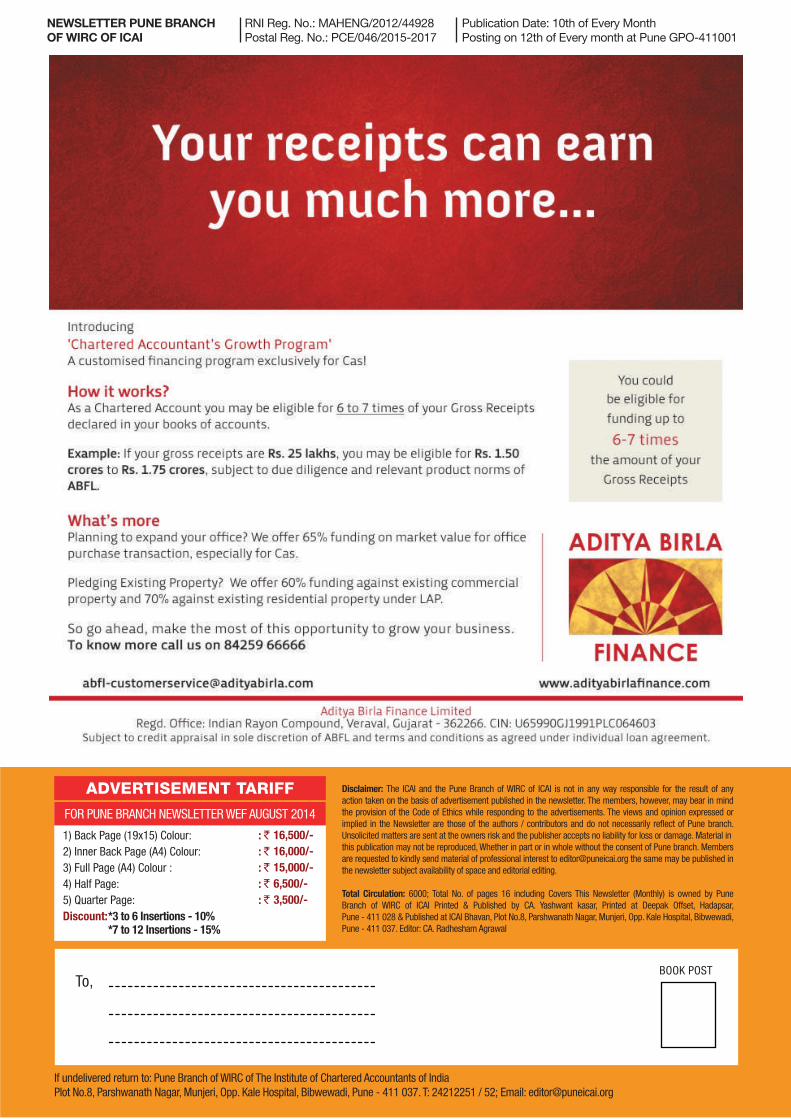

COMPLIANCE CALENDAR FOR OCTOBER - NOVEMBER, 2015

15th October, 2015 TDS return for quarter ended September, 2015 - Non Govt. deductorsTCS return for quarter ended September, 2015 - ALL deductorsForms 24Q,26Q,27Q,27EQ

PF epayment of September, 2015

21stOctober, 2015 ESI payment of September, 2015

MVAT and CST return for month/quarter/half year ended September, 2015 -Form 231-235, CST 1

MVAT and WCT TDS payment of September, 2015

22nd October, 2015 Issue TDS certificate u/s 194-IA for September, 2015 TDS deducted - Form 16B

25th October,2015 Service tax half year ended September, 2015 return - Return ST- 3

30th October, 2015 TDS certificates issue for quarter ended September, 2015 - Non Govt. deductorsTCS certificates issue for quarter ended September, 2015 - ALL deductors - Forms 16A/27D

31st October, 2015 TDS return for quarter ended September, 2015 - Govt. Deductors Forms 24Q,26Q,27Q,27EQ

Balance sheet in XBRL/non XBRL format - Form AOC 4

Banks return for quarter ended September, 2015 for interest upto Rs. 10,000/- - Form 26QAA

Profession Tax and return for September, 2015 - MTR-6, FORM IIIB

6th November, 2015 Service tax epayment of October,2015 - GAR-7

7th November, 2015 TDS/TCS payment of October, 2015 - ITNS 281

Submitting Forms 15G, 15H, 27C received in October, 2015 to IT Commissioner

10th November, 2015 Excise return for October, 2015- ER-1/2/6

STPI MPR Performance report for October, 2015

15th November, 2015 TDS certificates issue for quarter ended September, 2015 - Govt. deductors - Forms 16A/27D

PF epayment of October, 2015

Compiled by CA. Amruta Saswadkar, Pune. [email protected]

DATE PARTICULARS

5 STEPS TO BE GST READY CA. Pritam Mahure [email protected]

Though, the Government was able to pass the 122nd Constitutional Amendment Bill, 2014 (GST Bill)in LokSabha, which will eventually pave the way for Goods and Services Tax (GST) in India, currently the GST Bill is awaiting passage in RajyaSabha. Even the attempts made by the Government to pass the GST Bill in RajyaSabha turned out to be futile and the entire Monsoon Session was a wash out. However, the Governments determination to introduce GST is palpable from the fact that the State Finance Ministers met on 15 September 2015 to finalise GST draft legislations. Further, Infosys Systems was awarded contract to build GST Network which will be technology backbone for GST.

Given the aforesaid, its imperative for the business organisations to gear up (well in advance!) for this biggest tax reform since independence. In the following paras, the author discusses on possible steps which an organisation should take to be on GST Ready.

1. Sensitise the business eco-systemIt is an accepted fact that GST is not merely a tax change but a business change as it will impact all functions of an organisation such as finance, product pricing, supply chain, information technology, contracts, commercials etc. Thus, its imperative that all these functional teams should be aware about the GST. But the underlying question is what should these team members read/ refer for GST?

In this regard, its pertinent to note that most of the key aspects of the proposed GST regime are already in public domain through various reports such as 122nd Constitutional Amendment Bill, 2014 ('GST Bill'), RajyaSabha Select Committee Report on GST Bill, First Discussion Paper (issued by the Empowered Committee), Task Force Report on GST (issued by the 13th Finance Commission)etc. Thus, based on this knowledge available in public domain the organisation may consider sensitising its

employees.

The organisation can also consider sensitising its entire business eco-system i.e. not only the employees but also vendors(such as Tier-1, Tier-2 vendors etc) and key customers of the organisation. An early initiation of training will give the concerned employees, vendors and customers a sense of involvement in discussion much before GST legislation it is put in public domain.

2. Understand GST Impact on operationsGST may provide opportunities but at the same time it could bring threats. Given this, an organisation may consider carrying out an exercise to identify how its operations will get impacted because of GST. For GST Impact Analysis exercise, the respective department heads such as finance, supply chain, product pricing, human resource etc should also be involved to ensure that they provide their inputs and suggestions.

Going one step forward, organisations can also identify possible cost savings which key suppliers / vendors could be entitled to in the proposed GST regime. Based on the possible cost savings to suppliers / vendors, the organisations can have discussion with its vendors for passing of benefits by way of cost reduction in the coming years (i.e. after GST is introduced). Early discussion and engaging with vendors for GST will ensure maximum possible benefit to be passed on to the organisation.

3. Gear up for transition of Information Technology (IT) systemsIT is a key area as irrespective of the fact whether the organisation is ready or not, on the very first day GST is introduced, the information technology system of an organisation has to be ready and running else it will bring the entire business to standstill.

5News Letter Pune Branch of WIRC of ICAI/October 2015

Only those who have the patience to do simple things perfectly will acquire the skill to do difficult things easily.

6News Letter Pune Branch of WIRC of ICAI/October 2015

Given this, to avoid the threat of disruption of business, it is advisable that early study should be carried out to understand how the systems migration for GST could be done.

4. Design Alternate Business StrategiesTo gear up for GST regime, the organisation may also identify alternate efficient business strategies to ensure smooth transition to GST. Even, supply chain strategies is expected to undergo a major change as entire India will become one market and there may not be any tax cost involved for intra-State vis-à-vis inter-State procurement of goods. An organisation will also have to revisit their pricing strategies as business competitors may well reduce prices of their product to pass on the GST benefits.

However, while forming alternate business strategies, it goes without saying that the

organisation should take into consideration the commercial feasibility of alternate business strategies before these strategies are recommended.

5. Make representation before the GovernmentIntroduction of GST regime could affect negatively (than positively!) to few industries/ sectors. Thus, efforts should be made by the organisation to identify the possible issues for which appropriate representation could be made before the Government though various trade chambers and forums.

While current economic situation is characterised by volatile economic conditions, introduction of GST remains a ray of hope, thus early initiation of aforesaid steps can surely help the organisations gain most of the proposed GST regime.

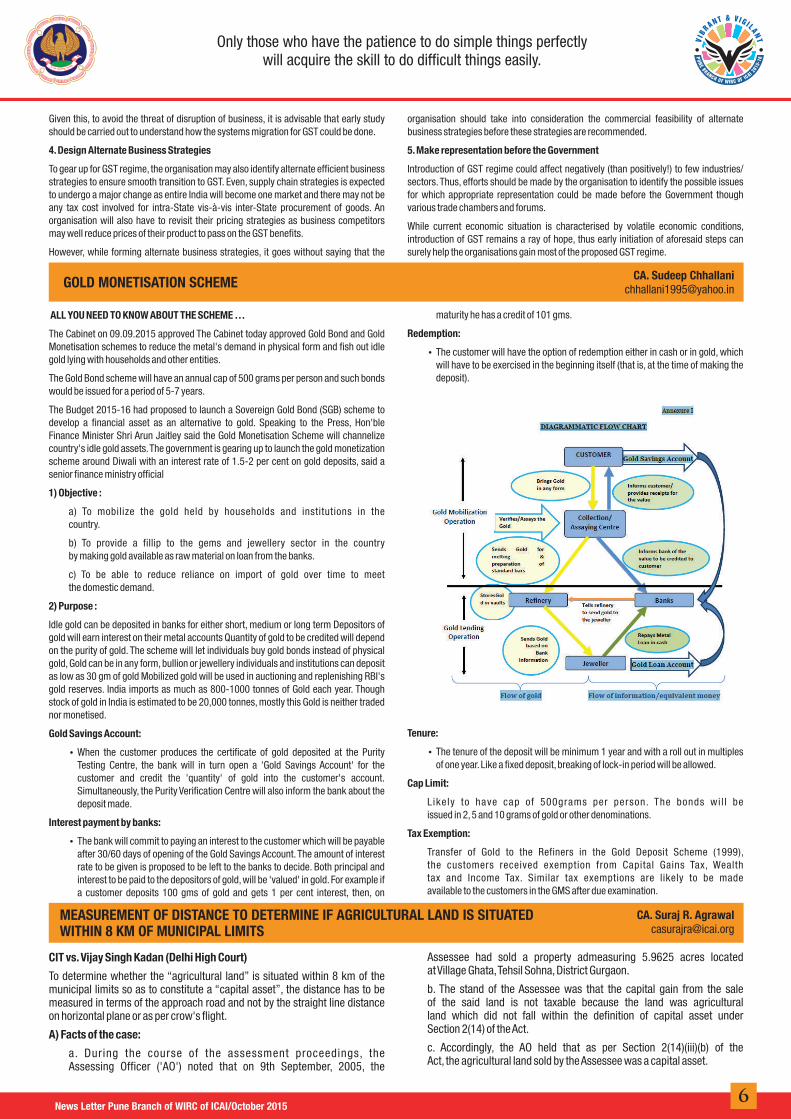

GOLD MONETISATION SCHEME CA. Sudeep [email protected]

ALL YOU NEED TO KNOW ABOUT THE SCHEME � The Cabinet on 09.09.2015 approved The Cabinet today approved Gold Bond and Gold Monetisation schemes to reduce the metal's demand in physical form and fish out idle gold lying with households and other entities.

The Gold Bond scheme will have an annual cap of 500 grams per person and such bonds would be issued for a period of 5-7 years.

The Budget 2015-16 had proposed to launch a Sovereign Gold Bond (SGB) scheme to develop a financial asset as an alternative to gold. Speaking to the Press, Hon'ble Finance Minister Shri Arun Jaitley said the Gold Monetisation Scheme will channelize country's idle gold assets. The government is gearing up to launch the gold monetization scheme around Diwali with an interest rate of 1.5-2 per cent on gold deposits, said a senior finance ministry official

1) Objective : a) To mobilize the gold held by households and institutions in the country.

b) To provide a fillip to the gems and jewellery sector in the country by making gold available as raw material on loan from the banks.

c) To be able to reduce reliance on import of gold over time to meet the domestic demand.

2) Purpose : Idle gold can be deposited in banks for either short, medium or long term Depositors of gold will earn interest on their metal accounts Quantity of gold to be credited will depend on the purity of gold. The scheme will let individuals buy gold bonds instead of physical gold, Gold can be in any form, bullion or jewellery individuals and institutions can deposit as low as 30 gm of gold Mobilized gold will be used in auctioning and replenishing RBI's gold reserves. India imports as much as 800-1000 tonnes of Gold each year. Though stock of gold in India is estimated to be 20,000 tonnes, mostly this Gold is neither traded nor monetised.

Gold Savings Account: When the customer produces the certificate of gold deposited at the Purity

Testing Centre, the bank will in turn open a 'Gold Savings Account' for the customer and credit the 'quantity' of gold into the customer's account. Simultaneously, the Purity Verification Centre will also inform the bank about the deposit made.

Interest payment by banks: The bank will commit to paying an interest to the customer which will be payable

after 30/60 days of opening of the Gold Savings Account. The amount of interest rate to be given is proposed to be left to the banks to decide. Both principal and interest to be paid to the depositors of gold, will be 'valued' in gold. For example if a customer deposits 100 gms of gold and gets 1 per cent interest, then, on

maturity he has a credit of 101 gms.

Redemption: The customer will have the option of redemption either in cash or in gold, which

will have to be exercised in the beginning itself (that is, at the time of making the deposit).

Tenure: The tenure of the deposit will be minimum 1 year and with a roll out in multiples

of one year. Like a fixed deposit, breaking of lock-in period will be allowed.

Cap Limit: L ikely to have cap of 500grams per person. The bonds wi l l be issued in 2, 5 and 10 grams of gold or other denominations.

Tax Exemption: Transfer of Gold to the Refiners in the Gold Deposit Scheme (1999), the customers received exemption from Capital Gains Tax, Wealth tax and Income Tax. Similar tax exemptions are likely to be made available to the customers in the GMS after due examination.

MEASUREMENT OF DISTANCE TO DETERMINE IF AGRICULTURAL LAND IS SITUATED WITHIN 8 KM OF MUNICIPAL LIMITS

CA. Suraj R. [email protected]

CIT vs. Vijay Singh Kadan (Delhi High Court)To determine whether the �agricultural land� is situated within 8 km of the municipal limits so as to constitute a �capital asset�, the distance has to be measured in terms of the approach road and not by the straight line distance on horizontal plane or as per crow's flight.

A) Facts of the case: a. During the course of the assessment proceedings, the Assessing Officer ('AO') noted that on 9th September, 2005, the

Assessee had sold a property admeasuring 5.9625 acres located at Village Ghata, Tehsil Sohna, District Gurgaon.

b. The stand of the Assessee was that the capital gain from the sale of the said land is not taxable because the land was agricultural land which did not fall within the definition of capital asset under Section 2(14) of the Act.

c. Accordingly, the AO held that as per Section 2(14)(iii)(b) of the Act, the agricultural land sold by the Assessee was a capital asset.

Never respond to rudeness. When people are rude to you, they reveal who they are, not who you are. Do not take it personally, be silent.

7News Letter Pune Branch of WIRC of ICAI/October 2015

d. AO accordingly made an addit ion of Rs 7,75,12,500/- to the income of the Assessee as long term capital gains.

B) Issue put before Delhi High Court:"Whether distance up to the land should be considered or up to the village within which such land is situated?"

C) Contentions of Appellant: a. According to the Assessee, the land did not fall within a distance of 8 km from the outer limit of the Gurgaon Municipality

b. The Assessee produced a certificate of the patwari in terms of which "in the year 2006 Ghata Village was approximately 9 Kms. away from Gurgaon Municipal Committee."

c. The Assessee also produced the certificates of two architects to the effect that the distance between the land and the outer limits of Gurgaon municipality was 9.645 Kms.

D) Contention by Revenue: a . The AO, however, re jec ted the cer t i f ica tes produced by the Assessee since the "scientif ic mode of determining the distance by a straight l ine method has not been employed" by the said architects.

b. The AO preferred the certificate of the Tehsildar, Sohna District and of the Engineer of the Gurgaon Municipal Corporation which stated that the distance was 6.6 Kms.

c. The CIT (A) rejected the certificates relied upon by the AO and the Assessee. He concluded that "the distance of agricultural land, in terms of Section 2(14)(i i i )(b) has to be measured along the road and not as per crow's flight/ aerial distance."

d. However, the CIT (A) observed that "the distance is to be taken from the local limits from the Municipal Corporation to the 'area' in which the land is situated and not up to the land as mentioned in the report of the Patwari."

e. The CIT (A) rejected the certificate furnished by the AO from the Directorate of Survey (AIR) and the DGDC Data Centre, New Delhi and concluded that the "shortest distance along the road from

IFFCO Junction on the Municipal boundary up to Northern outer limit of Ghata, the Village in which the land is situated is 7.17 Kms. along the road."

E) Ruling of Honorable Delhi High Court: a. The presumption of the Assessing Officer as well as CIT(A) that the 'area' means the v i l lage in which such land is s i tuated is without any basis.

b. the correct interpretation of the word 'in any area within such distance not being more than 8 Kms. from the local limits of any munic ipal i ty ' would mean the land should be with in such area w h i c h i s n o t m o r e t h a n 8 K m s . f r o m t h e l o c a l l i m i t o f t h e municipality

c. The ITAT concluded that the land had to be within the distance of 8 Kms. from the outer limit of the Gurgaon municipality and not from the outer l imit of the vi l lage Ghata in which the land was located.

d. On the strength of the certificate produced by the Assessee from the former Additional Director General, CPWD that the distance of the land from the outer limit of the Gurgaon Municipality was 10.4 Kms, the ITAT held that the land owned by the Assessee did not fall within Clauses (a) or (b) of Section 2 (14) (iii).

e. No substantial question of law arises. The appeal is dismissed.

F) Key Take Away a. The Court is of the view that for the purposes of Section 2 (14) (iii) ( b ) o f t h e A c t , t h e d i s t a n c e h a d t o b e m e a s u r e d f r o m t h e agricultural land in question to the outer limit of the municipality by road and not by the straight line or the aerial route.

b. The distance has to be measured from the land in question itself and not from the village in which the land is situated.

The Institute of Chartered Accountants of India Pune Branch wants to recruit following staff immediately

BRANCH-INCHARGE: One Post

Post Graduate from University recognized by University Grants

Commission with minimum 5 years' full time experience or Graduate from University recognized by

University Grants Commission with minimum 10 years' full time experience in any equivalent

Organization or Corporate. Fluent English both in writing and speaking and Knowledge of

computer is essential.

ACCOUNTANT: One Post

M.Com / MBA (with commerce background) / CA. Inter

levelprofessional/ Accounting Technician with 5 years'

experience in any equivalent organization or Corporate. Good

English andKnowledge of computer is essential.

SENIOR SUPERVISORS: Two Posts

Graduate from University recognized by University Grants Commission with minimum 6

years' full time experience in any equivalent organization or

Corporate. Reasonable Communication in English and

Knowledge of computer is essential.

PEONS: Three Posts

Higher Secondary Education or equivalent(i.e. 10+2) with 5 years full time experience in equivalent

organization or Corporate. Reasonable understanding of

English and working Knowledge of computer is preferred.

Please apply with detailed profile giving Qualifications & Work Experience to: The Chairman, Pune Branch of WIRC of ICAI

'ICAI Bhavan', Plot No. 8, Parshwanath Nagar, Munjeri, Bibwewadi, PUNE - 411 037. Email: [email protected] with CC to : [email protected]