OCCASIONAL PAPER - IMF eLibrary...Cataloging-in-Publication Data Price: US$25.00 (US$22.00 to...

72

Transcript of OCCASIONAL PAPER - IMF eLibrary...Cataloging-in-Publication Data Price: US$25.00 (US$22.00 to...

O C C A S I O N A L PA P E R 224

Managing Systemic Banking Crises

By a Staff Team Led byDavid S. Hoelscher and Marc Quintyn

INTERNATIONAL MONETARY FUND

Washington DC

2003

©International Monetary Fund. Not for Redistribution

© 2003 International Monetary Fund

Production: IMF Multimedia Services DivisionFigures: Theodore F. Peters, Jr.

Typesetting: Alicia Etchebarne-Bourdin

Cataloging-in-Publication Data

Price: US$25.00(US$22.00 to full-time faculty members and

students at universities and colleges)

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel.: (202) 623-7430 Telefax: (202) 623-7201

E-mail: [email protected]: http://www.imf.org

recycled paper

Hoelscher, David S.Managing systemic banking crises / by a staff team led by David S.

Hoelscher and Marc Quintyn—Washington, D.C.: International MonetaryFund, 2003.

p. cm.—(Occasional paper, ISSN 0251-6365; 224)

Includes bibliographical references.ISBN 1-58906-224-8

1. Banks and banking. 2. Financial crises. I. Quintyn, Marc. II. InternationalMonetary Fund. III. Occasional paper (International Monetary Fund); no. 224.

HG1601.H53 2003

©International Monetary Fund. Not for Redistribution

Preface v

I Overview 1

II Systemic Crises: Causes, Cost, and Resolution 3

The Emergence of a Systemic Crisis 3The Cost of Banking Crises 3Macroeconomic Context for Bank Restructuring 5A Strategy for Managing a Systemic Banking Crisis 6Implementation of Restructuring Strategies 8

III Crisis Containment 11

Overview of Strategy 11Policies for Stabilization 11Burden Sharing and Depositor Protection 17

IV Bank Restructuring 19

Overview of Strategy 19Legal and Institutional Framework 19Burden Sharing and Loss Allocation 20Bank Restructuring Options 20Returning the Banking System to Normal 23

V Asset Management and Corporate Debt Restructuring 26

Overview of Strategy 26Managing Nonperforming Assets 26Corporate Debt Restructuring 29

VI Bank Restructuring and Macroeconomic Policies 32

Issues in Monetary and Exchange Rate Policies 32Systemic Crises and Economic Growth 33Postcrisis Reintermediation 36The Impact of Sovereign Debt Restructuring 36

Appendices

I Costs of Banking Crises 40

II Case Studies of Banking Crises 43

References 62

Boxes

1. Bank Resolution Terminology 2

Contents

iii

©International Monetary Fund. Not for Redistribution

CONTENTS

2. Typology of Banking Crises 43. Guiding Principles from Recent Systemic Banking Crises 94. Dealing with Bank Runs in Dollarized Economies 145. Indonesian Bank Closures—Doing It Wrong and Doing It Right 176. Deposit Freeze: The Case of Ecuador 187. Difficulties in the Identification of Bank Solvency 218. How to Assess the Financial Condition of Banks: The Case of Turkey 229. Elements of the Public Recapitalization Program in Turkey 24

10. Appropriate Design Features of a Centralized AssetManagement Company 28

11. Good Practices for Corporate Debt Restructuring 3012. Best Practices in Corporate Workouts 3113. Depositor Reactions to Contract Changes 39

Figures

1. Fiscal Costs of Selected Crisis Countries 52. Options for Asset Management 273. Estimated Output Losses in Selected Crisis Countries 344. Evolution of Bank Deposits and Loans in

Selected Crisis Countries 1990–2001 37

Text Tables

1. Liquidity Support During Selected Systemic Banking Crises 122. Blanket Guarantees: Overview of Their Implementation 16

Appendix Tables

AI.1. Fiscal Costs of Selected Banking Crises 41AI.2. Fiscal Costs of Selected Banking Crises: Sources and

Country-Specific Information 42AII.1. Description of the System Before and After the Crisis 43AII.2. Crisis Outbreak and Containment: Financial and Monetary Measures 45AII.3. The Restructuring Phase: Judicial and Institutional Measures 48AII.4. The Restructuring Phase: Financial and Corporate Measures 52AII.5. Management of Impaired Assets 56AII.6. Exit from the Crisis 60

iv

The following symbols have been used throughout this paper:

. . . to indicate that data are not available;

— to indicate that the figure is zero or less than half the final digit shown, or that the itemdoes not exist;

– between years or months (e.g., 2001–02 or January–June) to indicate the years ormonths covered, including the beginning and ending years or months;

/ between years (e.g., 2001/02) to indicate a fiscal (financial) year.

“n.a.” means not applicable.

“Billion” means a thousand million.

Minor discrepancies between constituent figures and totals are due to rounding.

The term “country,” as used in this paper, does not in all cases refer to a territorial entity thatis a state as understood by international law and practice; the term also covers some territorialentities that are not states, but for which statistical data are maintained and provided interna-tionally on a separate and independent basis.

©International Monetary Fund. Not for Redistribution

This paper updates the International Monetary Fund’s work on general principles,strategies, and techniques for managing systemic banking crises in light of the newchallenges faced in recent financial sector crises.

The project was carried out in the Monetary and Financial Systems Department(MFD) under the supervision of Stefan Ingves, Director of MFD, and Carl-JohanLindgren. Both gave intellectual direction and clarity to the department’s work, draw-ing from their significant experiences in the field.

The material in this paper was originally prepared in late 2002 for the IMF’s Exec-utive Board and was subsequently discussed by the Core Principles Liaison Group ofthe Basel Committee on Banking Supervision in April 2003. The final paper has fur-ther benefited from comments by Executive Directors and IMF staff.

The paper reflects in particular the contributions of the staff of MFD’s SystemicBanking Issues Division. The authoring team included Michael Andrews, Luis Cor-tavarría, Fernando Delgado, Olivier Frécaut, Dong He, Mats Josefsson, YuriKawakami, Marina Moretti, Alvaro Piris, Steven Seelig, and Michael Taylor. SilviaRamirez provided valuable research assistance, and the paper would not have beencompleted without the excellent secretarial assistance of Sandra Solares. Gail Berreof the External Relations Department edited the paper and coordinated production ofthe publication.

The views expressed in this paper, as well as any errors, are the sole responsibilityof the authors and do not necessarily represent the opinions of the IMF ExecutiveBoard or other members of the IMF staff.

Preface

v

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

This paper draws lessons on the general princi-ples, strategies and techniques for the effective

management of systemic banking crises.1 Lessonsoutlined in this paper derive from the accumulatedexperiences of IMF staff. Principles and practices ofcrisis management derived from earlier crises havealready been discussed by the IMF Executive Boardand subsequently published.2 Recent financial sectorcrises and their resolution have raised new issuesand provided additional experiences. Specifically,banking crises in Argentina, Ecuador, Russia,Turkey, and Uruguay have occurred within the con-text of highly dollarized economies, high levels ofsovereign debt, and/or severely limited fiscal re-sources. These factors have introduced new chal-lenges as the effectiveness of many of the typicaltools for bank resolution has been affected.

Banks’ unique features—their key role in interme-diation and growth, price stability, and the paymentsystem—makes the management of banking prob-lems markedly different from the management ofother corporate failures. This paper focuses, how-ever, on issues raised in systemic crises and not onthe resolution of individual bank problems. Resolu-tion of individual bank problems in normal times isthe subject of a recent report by the Working Groupof the Basel Committee on Banking Supervision.3This paper draws on the conclusions of that reportand should be seen as a complement to it. In thesame vein, in-depth discussions of legal issues arebeing addressed by a joint IMF/World Bank project.4

Managing a systemic banking crisis is a complex,multiyear process. Whereas defusing an initial li-

quidity crisis may be accomplished in a few weeks,resolving a systemic banking crisis and the relatedcorporate debt restructuring can take many years.While many of the initial measures are macroeco-nomic in nature—meant to restore confidence—themedium-term restructuring is largely a microeco-nomic exercise.

The key to successful banking crisis managementis coordination of the banking strategy with the over-all policy framework. Management of such crisesoften requires adjustments in most aspects of eco-nomic policy implementation. While this paper con-centrates on the specifics of bank restructuring, poli-cymakers need to be aware of the broader policycontext within which bank restructuring must takeplace. Banking resolution has to take place in a sup-portive macroeconomic environment. Over the fullcycle of a crisis, this often requires the authorities todeal with various combinations of monetary and ex-change policies (including the possible introductionof capital controls), and fiscal and debt managementpolicies. Macroeconomic constraints must be consis-tent with the framework for addressing banking sec-tor problems.

Banking crises are often costly to society. Thecosts of banking crises can be minimized if appropri-ate policies are followed. The banking strategy mustbe rapidly designed and efficiently implemented. Adelay in addressing the emerging crisis increases thecosts and prolongs the crisis. Modifications in thelegal framework may become necessary if bankshareholders and creditors have excessive powersthat allow them to pass eventual costs to the govern-ment. The process of bank diagnosis must be quicklyimplemented. The banking strategy, together with thepolicies concerning depositor protection, should bedesigned to avoid the presumption that banks cannotfail. Rather, the strategy should aim for an efficientbanking system that is viable over the medium term.

In an effort to limit the public costs of a crisis, pri-vate funds should be the first source for bank recapi-talization. To that end, it may be helpful to maximizeprivate sector participation in bank restructuring.This latter effort may involve reducing legal impedi-ments to foreign investment in the banking system.

I Overview

1

1There is some debate about the definition of a systemic crisis.Systemic crisis is generally considered one in which the stabilityof the banking system and, as a consequence, the payments sys-tem and real sector, are threatened.

2Lindgren, Garcia, and Saal (1996); IMF (1997); and Lindgrenand others (1999). See also Bank for International Settlements(1999) and Dziobek and Pazarbas,iglu (1997).

3Basel Committee on Banking Supervision (2002).4A joint IMF/World Bank project is developing guidelines for

the legal and institutional aspects of dealing with bank insolven-cies (forthcoming IMF/WB paper). On this topic, see also Asser(2001).

©International Monetary Fund. Not for Redistribution

I OVERVIEW

The provision of public resources, in turn, should besubject to clear and transparent rules. Moreover, thepolicy on the provision of public resources should bemade within the context of the medium-term sus-tainability of the public sector finances. Finally, theeventual costs of a banking crisis will be eased bythe adoption of appropriate techniques to maximizeasset recovery and reprivatization of intervenedbanks (see Box 1 for bank resolution terminology).

A full crisis-management cycle represents a se-quence of interdependent events. To present anddiscuss such a sequence poses a challenge, yet canlook deceptively orderly. It is important to keep inmind that no presentation represents a one-size-fits-all model for dealing with systemic bankingcrises. There are common threads and similaritiesamong countries but, in the end, all countries haveto deal with their own special economic, legal, in-

stitutional, and political conditions. The intentionhere is modest—to present and discuss tools thatare available and how they can be used.

The structure of the paper is as follows: Section IIprovides a brief discussion of causes of a systemicbanking crisis, its costs, and the crisis managementstrategy. Section III describes the initial crisis con-tainment stage. Section IV deals with the secondcomponent, bank restructuring, while Section Vcovers the third component, management of nonper-forming loans and corporate debt restructuring. Sec-tion VI discusses linkages between bank restructur-ing and macroeconomic policies. Appendix Idiscusses the methodology for measuring fiscalcosts associated with major systemic crises. Finally,Appendix II provides case studies of key systemicbanking crises that have emerged since the early1990s.

2

Box 1. Bank Resolution Terminology

Some terms related to bank resolution have a rangeof meanings. The following terminology is used in thispaper:

Intervention or takeover of insolvent or nonviableinstitutions by the authorities refers to the assumption ofcontrol of a bank, i.e., taking over the powers of man-agement and shareholders. The term “intervened bank”is used to indicate a bank where such actions have takenplace. Such a bank may be closed or may stay openunder the control of the authorities while its financialcondition is better defined and decisions are made on anappropriate resolution strategy. Such strategies includeliquidation, merger or sale, transfer to a bridge bank, re-capitalization by the government, and sales or transfersof blocks of assets or liabilities. A bank undergoing thisprocess is termed a “resolved bank.”

Closure means that the bank ceases to carry on thebusiness of banking as a legal entity. A closure may bepart of a legal process of achieving the orderly exit of aweak bank through a range of resolution options, in-cluding liquidation or a complete or partial transfer ofits assets and liabilities to other institutions. A bankmay be left with a rump of bad assets to be worked out.Withdrawal of the banking license typically accompa-nies a closure.

Liquidation is the legal process whereby the assetsof an institution are sold and its liabilities are settled tothe extent possible. Bank liquidation can be voluntaryor forced, within or outside general bankruptcy proce-dures, and with or without court involvement. In liqui-

dation, assets are sold to pay off the creditors in theorder prescribed by the law. In a systemic crisis withseveral institutions to be liquidated simultaneously andquickly, special procedures or institutions may beneeded for the liquidation because existing structurescannot carry out the job in a timely manner.

A merger (or sale) of an institution means that allthe assets and liabilities of the firm are transferred toand absorbed into another institution. Mergers can bevoluntary or government assisted. A key issue is toavoid mergers of weak banks that result in a muchlarger weak bank, or the weakening of an initiallystrong bank.

In a purchase and assumption operation, a solventbank purchases all or a portion of the assets of a failingbank, including its customer base and goodwill, to-gether with all or part of its liabilities. In such a sup-ported purchase and assumption operation, the govern-ment typically will pay with securities to the purchasingbank the difference between the value of the assets andliabilities. Purchase and assumption operations couldinclude some form of put option, entitling the acquiringbank to return certain assets within a specified time pe-riod, or a contractual profit or loss–sharing agreementrelated to some or all of the assets.

A bridge bank involves the use of a temporary finan-cial institution to receive and manage the good assets ofone or several failed institutions. A bridge bank may beallowed to undertake some banking business, such asproviding new credit and restructuring existing credits.

©International Monetary Fund. Not for Redistribution

The Emergence of a Systemic Crisis

A systemic crisis emerges when problems in oneor more banks are serious enough to have a signifi-cant adverse impact on the real economy. This im-pact is most often felt through the payment system,reductions in credit flows, or the destruction of assetvalues. A systemic crisis often is characterized byruns of creditors, including depositors, from bothsolvent and insolvent banks, thus threatening the sta-bility of the entire banking system. The run is fueledby fears that the means of payment will be unobtain-able at any price, and in a fractional reserve bankingsystem this leads to a scramble for high-poweredmoney and a withdrawal of external credit lines.

Loss of creditor confidence can result from therecognition of significant banking system weak-nesses. Such recognition may be triggered by eco-nomic or political events. The events in the Asiancountries in 1997 are among the more recent exam-ples of such a crisis.5 Creditors can also lose confi-dence in sound banking systems due to poor macro-economic policies, external shocks, or even impropersequencing of financial sector reforms. The resultingliquidity crisis, if mismanaged, can result in financialpanic and insolvency. International capital market in-tegration in the 1990s has added a new dimension tobanking crises. Perceptions by foreign investors ofmacroeconomic weaknesses, concerns about the fu-ture path of economic policies, political turmoil, orfear of contagion from other crises can lead to aquick deterioration in international creditor senti-ments (see Box 2 for a more in-depth discussion ofthe causes of banking crises).

Treatment of a systemic banking crisis contrastsin important ways with the treatment of individualbank failures in stable periods. Policies consideredappropriate in stable periods may aggravate uncer-tainties in a systemic crisis, worsening private sec-tor confidence and slowing recovery. In stable peri-ods, for example, deposits have only limitedprotection, emergency liquidity assistance is given

under very restricted conditions, and undercapital-ized or insolvent banks are immediately intervenedand resolved. In a systemic crisis, however, eventscan change rapidly, banking conditions may deteri-orate quickly, and information on the true conditionof banks tends to be limited and often outdated. Insuch an environment, policies should be aimed atlimiting the loss of depositor confidence, protectingthe payment system, restoring solvency to the bank-ing system, and preventing further macroeconomicdeterioration.

A successful restructuring requires decisive gov-ernment action from the onset of the crisis. Deter-mined actions to strengthen macroeconomic policiesand implement structural reforms can reduce themagnitude of the crisis. Often, such early determina-tion is lacking because the authorities (and marketparticipants) need time to recognize the severity ofthe situation, or worse, are in denial. Delays in imple-mentation may prevent or slow the return of both de-positor confidence and access to international capitalmarkets, deepening the crisis. Comparisons of recentcrises in Argentina (2002), Brazil (1999), Russia(1998), and Turkey (2000) point to the importance ofrapid and determined policy adjustments.

The Cost of Banking Crises

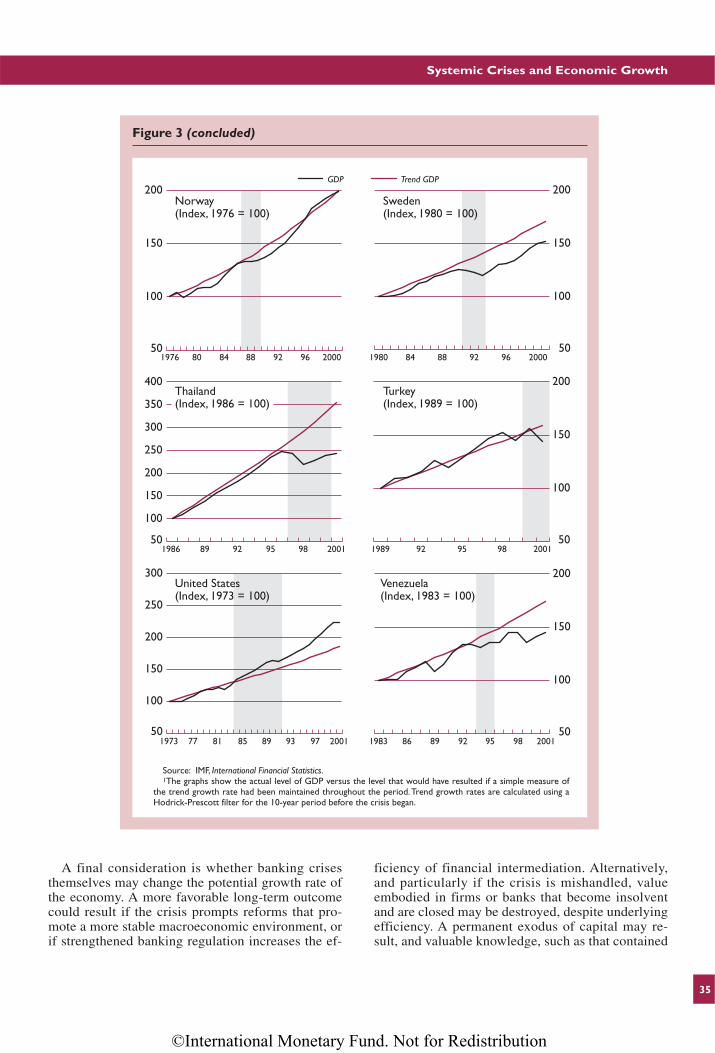

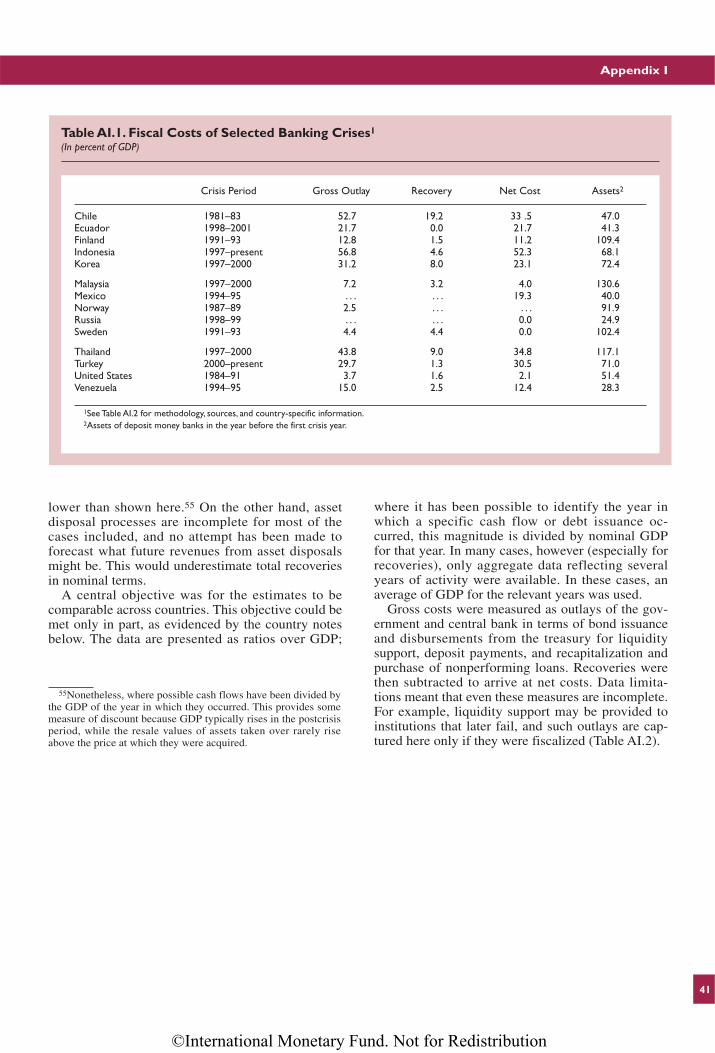

Measuring the cost of banking crises is a difficulttask.6 One needs to distinguish between the totalcost to the society, which is hard to measure, and thefiscal cost. The former concept is discussed in Sec-tion VI. Here we deal with the fiscal cost.

The costs of banking crises have varied sharply.Costs to the public sector have ranged from smallamounts (close to zero) in Russia and the UnitedStates to over 50 percent of GDP in Indonesia (Fig-ure 1 and Appendix I). Three main factors affectthe gross cost to the public sector: the initialmacroeconomic conditions and the financial sector,

II Systemic Crises: Causes, Cost, andResolution

3

5Lindgren and others (1999).

6See, among others, Frydl (1999) and Frydl and Quintyn(2000).

©International Monetary Fund. Not for Redistribution

II SYSTEMIC CRISES: CAUSES, COST, AND RESOLUTION

the authorities’ policy response (i.e., the specificmeasures taken), and the degree of success in re-covering the value of assets acquired during the cri-sis. Fiscal costs may not represent a complete lossto the economy, as some part of the expenditurerepresents a transfer to the domestic private sector.A banking crisis will also result in costs to theeconomy in terms of macroeconomic instabilityand foregone growth, which have proven complexto estimate.

Gross costs can be measured as outlays of thegovernment and central bank in terms of bond is-suance and disbursements from the treasury for li-quidity support, payout of guarantees on deposits,costs of recapitalization, and purchase of nonper-forming loans. Net costs to the public sector deductfrom gross costs recoveries from the sale of assetsand equity stakes and repayment of debt by recapi-talized entities.7

Gross costs have varied widely in recent crises.Initial macroeconomic and financial sector condi-tions are important determinants of the differences.For example, financial and corporate sector weak-nesses in the Asian crisis countries made financialinstitutions more vulnerable to declines in asset val-ues, devaluation, and reversal of capital flows. Thisvulnerability in turn helped foster speculative attacksand worsen capital flight, increasing losses and rais-ing the ultimate resolution costs.

The policy response of authorities has also beenkey. Russia, for example, did not offer a blanketguarantee and did not recapitalize banks with pub-lic funds. While the costs to the economy may havebeen lower had there been more active public inter-vention, the direct costs to the state were low. The quality of the policy response, in terms of ei-ther macroeconomic adjustment or the handling ofbank failure, affects the severity of the crisis. Lackof policy coordination or a clear, well-communi-cated strategy can raise costs to the economy by prolonging the crisis, undermining efforts to stem deposit runs and increasing uncertainty for borrowers, shareholders, and depositors. Late

4

Box 2.Typology of Banking Crises

A banking system crisis usually arises from multiplesources, each interacting with one another to aggravateand accelerate the crisis. For that reason, typologies areartificial and of only limited analytical use. At best,only broad categories can be identified that capture themost fundamental elements of a crisis.

Based on their causes, banking crises can be classi-fied broadly into one of two categories: predominantlymicroeconomic, or predominantly macroeconomic.Crises arising from microeconomic causes are largelyrelated to poor banking practices. Lax lending practicesmay fuel asset price bubbles or lead to excessive con-centration of banks’ portfolios. Weak risk-control sys-tems have been a major factor in the emergence of anumber of crises, leading to a variety of balance sheetdeficiencies—large and undetected mismatches (eithercurrency or maturity) on the balance sheets or poorasset quality, leading to large unrealized losses. Bankswith balance sheet deficiencies are vulnerable to anyshock, and even comparatively minor external eventsmay be sufficient to provoke a loss of confidence and ageneralized run.

Crises arising from macroeconomic causes are initi-ated by developments external to the banking system.Deterioration in the macroeconomic policy environmentmay cause banking crises in even well-managed bankingsystems. Well-run banking systems operating in a stronglegal and regulatory framework can be overwhelmed bythe effects of poor macroeconomic policies. While well-run banks may be able to absorb some macroeconomic

shocks, continued unsound monetary, exchange rate, orfiscal policies can produce financial strains that over-whelm banks’ defenses, affecting their solvency or forc-ing them into risky operations. The way in which thesepolicies might affect banks depends on balance sheetstructures. For example, large exposures to the govern-ment—often the result of high yields on public bonds—increase bank vulnerability to unsustainable fiscal poli-cies. Dollarization of financial contracts, whilecontributing to higher intermediation, makes banks vul-nerable to unsound exchange rate polices, as even in theabsence of currency mismatches banks are exposed tocredit risk from unhedged borrowers. Even with overallsound balance sheet structure, banks are vulnerable tounsustainable monetary policies, leading to high andvolatile interest rates. It goes without saying that theworst crises are those where macroeconomic shocks af-fect a weak banking system.

As long as the banks remain liquid, banking distresscan persist for a prolonged period until some triggerleads creditors to lose confidence in the banking sys-tem, leading to a generalized run. Many kinds of eventscan trigger a loss of confidence, including emergenceof illiquidity in an individual bank (local contagion), aloss of confidence in the government and its ability toimplement its macroeconomic framework, or the emer-gence of a systemic crisis in a country related throughfinancial and trade channels (international contagion).Lack of appropriate action or delays in addressing theemerging problems further fuels the bank run.

7Appendix Table AI.2 provides these data and a fuller discus-sion of methodology used, as well as data sources and importantcountry-specific information.

©International Monetary Fund. Not for Redistribution

Macroeconomic Context for Bank Restructuring

recognition of the systemic nature of the problemscan also increase the final costs. For example, boththese factors were important in Venezuela in themid-1990s.

A final difference affecting net costs is how suc-cessfully the state recovers the value of assets ac-quired during the crisis. Two components are partic-ularly important: sale of nonperforming loans andreprivatization (or sale of equity) of banks acquiredduring recapitalization. Recovery performance canvary considerably. While Sweden and Norway wereable to recover all the costs associated with the cri-sis and still retain stakes in banks taken over, in gen-eral recovery rates have been low. The market valueof nonperforming loans typically declines quiterapidly, while equity stakes in banks and enterprisesmight appreciate as they recover, or fall to zero.Also, in many cases, such as the United States,funds generated from asset disposals were recycledand used to recapitalize further institutions, thuslowering gross outlays.

Macroeconomic Context for Bank Restructuring

Coordination with the overall macroeconomicframework is a key factor in successful banking cri-sis management. Systemic financial crises affectmost sectors of the economy and require adjust-

ments in most aspects of economic policy imple-mentation. While this paper concentrates on bankingsystem restructuring, policymakers need to be awareof the broader policy context within which such re-structuring must take place. Bank restructuringneeds to be implemented in conjunction with sup-porting macroeconomic policies, taking into accountexisting macroeconomic constraints. Moreover,measures to contain the crisis and restructure banksmay have macroeconomic consequences that need tobe taken into account in the design of a bank resolu-tion strategy.

At the outset of a crisis, macroeconomic policiesmay need to be adjusted to restore confidence in thebanking system and the currency. The policy mixwill depend on the nature of the macroeconomic im-balances and the state of the banking system. A tem-porary tightening of policies may be inevitable, how-ever, when a creditor run from the banking systemoccurs with accompanying pressures on the pricelevel, net international reserves, and the exchangerate. Comprehensive macroeconomic policy adjust-ments will be needed to restore stability, lower inter-est rates after an initial hike, and allow for a return ofeconomic stability.

Authorities may consider capital controls whenfaced with runs not only on deposits but also on thecurrency. Capital controls must be tight enough to beeffective, and their design should address the likeli-hood that means for evasion will quickly emerge.

5

0 10 20 30 40 50 60

Indonesia 1997–present

Gross costNet cost

Chile 1981–83

Thailand 1997–2000

Turkey 2000–presentKorea 1997–2000

Ecuador 1998–2001

Venezuela 1994–95

Finland 1991–93Malaysia 1997–2000

Sweden 1991–93

United States 1984–91

Norway 1987–891

Sources: IMF, International Financial Statistics,World Economic Outlook, and national authorities.1Data on net cost unavailable.

Figure 1. Fiscal Costs of Selected Crisis Countries(In percentage of GDP)

©International Monetary Fund. Not for Redistribution

II SYSTEMIC CRISES: CAUSES, COST, AND RESOLUTION

Such careful design is critical to ensure an effectivesystem that minimizes the economic costs of thecontrols.8

Operations of the nonfinancial public sector oftenlie at the heart of a financial crisis. Persistent fiscaldeficits, financed through central bank credit expan-sion, often fuel inflation and asset price bubbles.Moreover, high levels of government debt can under-mine creditor and depositor confidence, making thebanking system more prone to runs. Tax reform,combined with expenditure prioritization, is thereforea key aspect of the broad policy response to systemicfinancial crises in many cases. Design of the fiscaladjustment path must be clearly embedded in thebroad strategic response to systemic financial crises.9When sovereign debt dynamics are unsustainable,however, measures to achieve sovereign debt sustain-ability may sometimes cause banking system insol-vency, thus increasing costs to the government andthe economy that could reduce or eliminate the gainsfrom debt reduction. Therefore, strategies for bothbank and debt restructuring must be closely coordi-nated and consistent with each other.

As the macroeconomic policy stance and mone-tary policy tools are adjusted, the authorities mayalso have to strengthen their sovereign debt manage-ment. Banking crisis resolution has fiscal implica-tions, and the techniques chosen will need to be con-sistent with the medium-term sustainability of publicdebt. The authorities should seek to ensure that thedebt growth is not excessive and is closely coordi-nated with monetary and fiscal policy objectives.The changes in maturity structure, exchange expo-sure, and contingent claims must be carefully con-sidered as part of the overall financial resolutionstrategy, as they can affect the costs of financing theresolution of the crisis.10

A Strategy for Managing a Systemic Banking Crisis

The strategy for managing a banking crisis must betailored to country-specific conditions. Country-specific factors include the cause of the crisis, themacroeconomic conditions and outlook of the coun-try, the financial position of the banking system, therisks of internal and external contagion, and the avail-ability of resolution tools.11 In recent years, two polar

examples have emerged. Banking crises have oc-curred in countries with weak banking systems domi-nated by local currency–denominated assets and lia-bilities, and where the governments had a relativelywide range of resolution tools. The Asian crisislargely reflected these conditions. In contrast, criseshave also emerged where the banking systems havebeen relatively strong, and highly dollarized, butwhere the governments had limited resolution tools.The recent crises in Latin American countries reflectthese conditions. While future crises may fall be-tween these two extremes, the differences in approachillustrated by these polar cases provide a guide toadapting banking strategies to local conditions.

Any strategy typically includes three intercon-nected components. The first and most urgent com-ponent deals with an acute liquidity crisis. The lia-bilities of the banking system must be stabilized anddeposit runs stopped. The second component seeksremoval of insolvent or nonviable banks from thesystem and restoration of financial soundness andprofitability. The third component of the strategy,which has a medium-term time horizon, focuses onthe financial restructuring of nonperforming loansand the operational restructuring of bank borrowers.

Crisis Containment

The most immediate component of managing abanking crisis is the stabilization of bank liabilities—stopping depositor and creditor runs. The centralbank, as the lender of last resort, should provide suffi-cient liquidity to the banking system to protect thepayment system and give the authorities time to iden-tify the causes of the crisis and design an appropriateresponse. In the face of sharp increases of liquidity,the central bank should use its monetary instrumentsto sterilize any resulting increase in the money supply.Moreover, such support should be limited to solventbanks. In the early stages of the crisis, however, it isdifficult to distinguish between insolvency and illi-quidity, and the government may have to recapitalizethe central bank once the crisis has been resolved. Inhighly dollarized economies, the central bank’s abilityto provide emergency liquidity is constrained by thelevel of international reserves, access to internationalcapital markets, and support from international finan-cial institutions. In such cases, the liquidity may notbe available, and more aggressive policies on bankresolution may be needed.

If credible, a blanket guarantee can restore investorconfidence and stabilize banks’ liabilities. A blanket

6

8See Ishii and others (2002).9See Daniel and Saal (1997).10See IMF and World Bank (2001) and World Bank (2001).11Country-specific factors also include ownership structures of

the banking system and the corporate sector; human resource con-straints; the legal, regulatory, judicial, and administrative frame-

works; traditions of transparency; as well as political cohesionand the quality of leadership. These factors will influence thepace and success of the resolution strategy.

©International Monetary Fund. Not for Redistribution

A Strategy for Managing a Systemic Banking Crisis

guarantee gives the government some breathingspace to develop a comprehensive restructuring strat-egy. It also makes resolution of weak banks easier, asbank interventions and closures are less likely toprompt depositor panic. A blanket guarantee alone,however, cannot contain a liquidity crisis; to be suc-cessful, it must be part of a credible stabilizationpackage. Moreover, the moral hazard risks in a blan-ket guarantee have to be balanced against the poten-tial benefits from such a guarantee. A blanket guaran-tee may not be credible in the face of unsustainablepublic debt dynamics or in a highly dollarized bank-ing system. If dollarization is moderate, a guaranteecould cover foreign currency liabilities in their do-mestic currency equivalent at market exchange rates.

If market-oriented stabilization measures do notcontain the crisis, the authorities may have to resortto administrative measures to avoid losing monetarycontrol. Such measures include securitization of de-posits, forced extension of maturities, or a depositfreeze. To varying degrees, these measures imposerestrictions on the depositors’ ability to withdrawtheir funds. Administrative measures can causemajor economic disruption and, therefore, must beviewed as a last resort to stop a run on banks if allother measures fail.

Bank Restructuring

The second component of the restructuring strat-egy is to restore the profitability and solvency of thebanking system. The first task is to identify the sizeand distribution of bank losses. Supervisory datamay be outdated, so a process for collecting databased on uniform valuation criteria should be initi-ated. The next task is to classify banks into one ofthree categories: viable and meeting regulatory re-quirements, nonviable and insolvent, or viable butundercapitalized. In the latter classification, an addi-tional assessment will be needed of the ability of theexisting shareholders to recapitalize their bankswithin an acceptable period.

The determination of a bank’s viability is a criticalaspect of managing the restructuring process. Finan-cial statements and asset values of a bank are oftendistorted during a crisis, making it difficult to deter-mine a bank’s financial position. Under such circum-stances, viability may be determined by examiningtwo factors. First, the bank must develop a medium-term business plan and cash flow projections, basedon realistic macroeconomic assumptions that showfuture profitability and medium-term strength. Sec-ond, shareholders must be committed and financiallysound. Any business plan can go wrong; the share-holders must stand ready to adopt corrective mea-sures. In addition, the authorities must develop aview as to the future volume of activity that the

economy can absorb and establish criteria for bankevaluation that aims at an appropriately dimensionedbanking system.12

Resolution techniques will depend on the banks’financial conditions and medium-term prospects. Allsolvent but undercapitalized banks should be re-quired to present acceptable restructuring plans.Bank recapitalization may be phased in if accompa-nied by an acceptable restructuring plan. An insol-vent bank should be intervened and transferred to theinstitution responsible for bank resolution, whichwill decide whether to close it or keep it open. If thebank is closed, decisions need to be made on how tomanage assets and liabilities, including nonperform-ing assets, performing assets, and deposits. If thebank is kept open, the restructuring institution mustdecide on a range of options, including whether torecapitalize the bank with public funds; to offer it forimmediate sale or as a merger partner to a private in-stitution; or to merge it with another solvent, govern-ment-owned bank.

Explicit decisions about burden sharing must bemade in the design of the restructuring strategy. Abanking crisis reflects losses of banks and their bor-rowers. The costs must be shared by some combina-tion of bank shareholders, depositors, other credi-tors, and taxpayers. How the costs are paid and thedistribution of the costs among different agents is apolitical as well as a technical decision, which re-quires explicit consideration in the design of thestrategy. This process is difficult because the deter-mination of losses is extremely difficult, nonper-forming loans have no clear market value, and thesize of losses is constantly changing in response tochanges in the business environment. Strong and co-hesive political leadership is required to addressthese issues.

Public capital support of private banks may be jus-tified in some situations. The authorities may helpprivate owners achieve a least-cost resolution. In thiscase, injection of new funds by the shareholderscould be supplemented with public funds. Publicparticipation in the recapitalization may be justifiedwhen the economy does not have sufficient capitaland foreign interest is limited. Public funds may alsobe justified when the banking problems are the di-rect result of public policy.

Once the banking system has stabilized and bothcorporate restructuring and asset resolution are

7

12The proposal is not to identify and protect a core banking sys-tem; in principle, market forces should determine the winners andlosers among financial institutions. Rather, the authorities shouldadopt uniform and transparent rules that apply to all banks. If faced with the need to consolidate the banking system, pruden-tial rules must be sufficiently strong to ensure continued financialintermediation.

©International Monetary Fund. Not for Redistribution

II SYSTEMIC CRISES: CAUSES, COST, AND RESOLUTION

under way, the authorities will need to turn tostrengthening the financial system and fosteringreintermediation. Tasks at this stage include deter-mining the role of both private and public financialinstitutions, reinforcing prudential and regulatoryoversight, and strengthening transparency. Marketdiscipline has to be strengthened, as the safeguardsput in place at the height of the crisis must be phasedout at a safe but meaningful pace. Exit rules for fail-ing banks will have to be enforced and legal, judi-cial, and institutional structures strengthened to pro-mote an effective and competitive banking system.

Difficult decisions must be made concerning thetreatment of any bank that was nationalized as a re-sult of the crisis. Reprivatization of banks and bankassets should take place according to a carefully de-veloped strategy. The government will have to deter-mine how to maximize the bank’s net value in lightof expected future economic growth, either throughrapid divestment of nationalized assets or a slowerapproach.13 Similarly, the government must deter-mine how best to increase market competition. Pri-vatization of small banks may increase competitionin the market, but it may be difficult to attract ade-quate buyers. A single large institution may be easierto sell at a cost of reduced competition in the market.The role of foreign investors must be defined. Thereis little experience to date on this stage of crisis reso-lution, and it remains a critical policy issue for thefuture.

Asset Management

The third component of crisis management is assetmanagement and corporate debt restructuring. Bankshave three options in dealing with nonperforming as-sets: they can restructure the loans, liquidate theloans, or sell the assets to a specialized institution forresolution. This process of asset management is inex-tricably intertwined with corporate restructuring.Poorly designed corporate debt restructuring can im-pede or even reverse progress in financial sector re-structuring. The objective of this phase of crisis man-agement is to seek arrangements that allow banks tomaintain positive cash flows, deepen business rela-tions with solvent borrowers, and encourage corpo-rate debt restructuring.

Banks and corporations must seek the timely andorderly restructuring of corporate debt in a way thatshares the burden equitably. Government action isoften required to ensure that banks are not at a disad-vantage in negotiating with borrowers. Formal insol-

vency rules often must be strengthened while, at thesame time, institutions and mechanisms are estab-lished to encourage out-of-court settlement. The fi-nancial restructuring of corporate debt should proceedin the context of a broader operational restructuring ofthe companies, which is a prerequisite for renewedcorporate profitability, new investment, access to bankcredit, and economic growth. If loans cannot be re-structured, they should be liquidated and any collat-eral foreclosed.

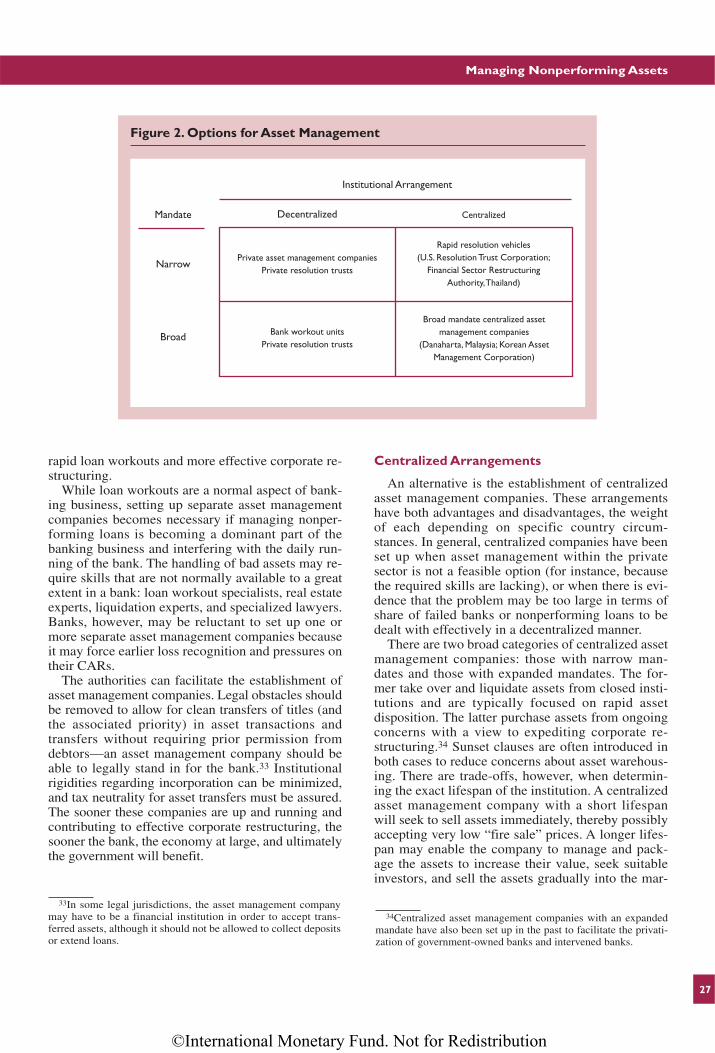

There are a number of institutional options formanaging impaired assets. Nonperforming loans canbe managed by the banks or sold to specialized assetmanagement companies, either privately or publiclyowned. While each setup has both advantages anddisadvantages, experience suggests that, in general,private financial institutions can respond morequickly and efficiently. Government-owned central-ized asset management companies may lack incen-tives for maximizing recovery values, and may besubject to political interference. On the other hand,such companies may be relatively more efficientwhen the size of the problem is large—hence, assetmanagement may involve economies of scale—orthe required skills are unavailable.

Implementation of RestructuringStrategies

Implementation of a wide-ranging restructuringagenda is difficult to coordinate. Crisis episodeshave evolved at varying paces and with different re-sults (see Appendix II). Such differences are causedby a variety of factors, including initial conditions,policy mix, international environment, and even un-expected exogenous events. Notwithstanding im-portant differences among crisis cases, some gen-eral lessons have emerged. While the followingpractices are not always required for the successfulimplementation of a strategy, they do appear tomake implementation relatively smoother and im-prove the probability of success (see Box 3 for anoverview of guiding principles).

Successful restructuring efforts have used thesense of urgency created by the outbreak of the crisisto initiate quickly the reform process. Experiencesuggests that political resistance to reform measuresis weakest early in the process when a broad consen-sus to address the causes of the crisis is highest. Asthe crisis continues, vested political or economic in-terests emerge or reemerge, and the reform processbecomes slower and more difficult.

A second practice is the establishment of a coordi-nating unit or committee early in the crisis to designand oversee crisis management. To be effective, thiscommittee should be composed of senior govern-

8

13Also, the government needs to factor in the possible pitfallsof prolonged government management of a bank, e.g., politicalinfluence, lack of managerial capacity, and so forth.

©International Monetary Fund. Not for Redistribution

Implementation of Restructuring Strategies

ment officials that have both the responsibility andthe authority to develop economic policy. Often sucha group is composed of cabinet-level officials andsenior staff of central banks and financial sectoroversight agencies. While this committee shouldhave responsibility for strategy design, it would nor-mally oversee, but not implement, the strategy.

A related practice is to avoid excessive centraliza-tion of policy implementation and give governmentagencies the authority and responsibility to imple-ment the restructuring strategy. Often, existing agen-cies with established credibility may be given such aresponsibility. Existing agencies—including the cen-

tral bank, the supervisory agency, the ministry of fi-nance, and the deposit insurance agency—often haveadequate staff, organization, and infrastructure.Given the need to act quickly, it may be cost effec-tive to rely on these existing institutions. On theother hand, establishing new bodies with specializedstaff may be necessary. Such new agencies may bestaffed with specialists not normally available ormay be given special responsibilities in the conductof the restructuring strategy. The decision to rely onthe existing institutional framework or establish newinstitutions will depend on the credibility and expe-rience of existing institutions, the need for special-

9

Box 3. Guiding Principles from Recent Systemic Banking Crises

• Political support is important for successful crisismanagement. Public disagreements or expressions ofdoubt among prominent government participants canundermine confidence in the containment and restruc-turing process.

• A single, accountable authority can facilitate crisismanagement. Strong leadership is needed to dealwith vested interests, determine issues affectingwealth and income distribution (burden sharing), andshepherd the restructuring program through the leg-islative process. This authority should clearly com-municate the strategy and decisions to the public.

• Speed of intervention is essential. Decisive stepsneed to be taken in the initial stages to stop creditorand depositor withdrawals. The best opportunity forsignificant progress is in the early stages when polit-ical support to resolve the crisis is normally at itshighest.

• A coherent and comprehensive package of mea-sures should be implemented. Such a package mayinclude credible macroeconomic adjustments, emer-gency liquidity support, a blanket guarantee wherecredible, and early closure of clearly insolvent banks.Should such measures not be effective, the authoritiesmay need to resort to administrative measures as alast alternative—securitization of deposits, lengthen-ing of deposit maturities, or a deposit freeze.

• Protection of depositors and other creditors willease the restructuring process. Where credible, ablanket guarantee can ease creditor fears and facilitatethe closure of weak banks. When a blanket guaranteeis not credible, the authorities may have to rely on ad-ministrative measures.

• Burden-sharing decisions should be explicit. Exist-ing shareholders should be the first to either inject ad-ditional capital or lose their investment. If capital con-tinues to be insufficient, other stakeholders need totake losses. With a blanket guarantee, the govern-ment—and thereby taxpayers—assume the losses ofdepositors and other creditors. Under administrative

measures, depositors and other creditors typicallymay have to take a share of the losses.

• The bank resolution strategy should include athorough diagnosis and bank resolution plan. Aprocess of bank triage should take place. Nonviableinstitutions should be liquidated or merged with vi-able banks, and adjustment periods could be providedfor viable but undercapitalized banks.

• Bank resolution should follow a principle of equityand fair treatment. Restructuring policies should beapplied to all banks on a uniform basis, that is indepen-dent of their ownership (public, domestic private, orforeign private) or type (wholesale, retail, or niche).

• The banking strategy should be designed to mini-mize the present value costs of the crisis. The likelycosts of different options should be identified, and thestrategy should be based on the lowest present valueof costs to the economy. Costs estimates should in-clude an estimate of the impact of each option on thebanking system, economic growth, and the sustain-ability of government debt.

• Recapitalization with government funds may bejustifiable in some circumstances. Private fundsshould be used first, and the terms for public assis-tance should be uniform and transparent.

• Asset resolution is an essential complement tobank restructuring. An early and active involvementin impaired asset management would prevent creditdiscipline from eroding. A variety of institutionalarrangements and techniques are available. Theyshould be chosen in order to achieve the desiredtrade-off between rapid resolution and recovering thevalue of the impaired assets.

• Corporate restructuring should go hand in handwith bank restructuring. Without corporate restruc-turing—both financial and operational—economicactivity will slow down further, and the banking sys-tem may not get out of, or fall back into, a state of dis-tress. Corporate debt restructuring should be based onmarket principles and reinforce payment discipline.

©International Monetary Fund. Not for Redistribution

II SYSTEMIC CRISES: CAUSES, COST, AND RESOLUTION

ized institutions, and the speed with which new insti-tutions can be created and staffed.

The fourth practice is communicating with thebroader public. An often-neglected aspect of crisismanagement is the importance of strengthening mar-ket confidence by informing the public about the di-rection of public policy. The authorities should useall forms of communication to explain their views onthe causes of the crisis, their understanding of howthe crisis will be resolved, and where the reformstrategy will lead. The announcements should beconsistent, regular, and ideally be given by a singleofficial spokesperson throughout the containmentand restructuring efforts. This communication strat-egy can be effective in forging and then maintainingsupport for the reform efforts and can help reducethe influence of entrenched special interest groups.

Finally, the authorities can benefit from thedemonstration effect of quick and successful wins.Restructuring can be a prolonged process, with diffi-cult adjustments and costs. Reform fatigue can be re-duced by taking advantage of opportunities forshort-term successes. The authorities should seek toidentify steps that produce some immediate resultsas an indication that the benefits from the reformprocess are not only to be achieved over the mediumterm, but also immediately. These steps, whenplaced in the context of the broader strategy, canhelp to mobilize support for the entire reformprocess.14

10

14This process is similar to what Hirschman (1963) has referredto as “reform mongering.”

©International Monetary Fund. Not for Redistribution

Overview of StrategyIrrespective of its origin, a systemic banking crisis

first emerges as a liquidity problem in some or all ofthe banks. Large creditors, both foreign and domes-tic, are generally the first to leave the banking sys-tem.15 As the outflow becomes known, smaller de-positors follow quickly. Very large amounts canmove in hours and, if not stopped, such runs maystall the operation of the payment system.

Liquidity and deposit withdrawals are symptoms ofunderlying problems but do not necessarily signal asystemic banking crisis. The authorities must form aquick judgment whether the deposit runs reflect con-cerns about the solvency of individual institutions, thestability of the banking system, or overall economicmanagement. This judgment is often difficult becausereliable data are scarce and quickly outdated. More-over, wishful thinking and denial may affect the au-thorities’ judgment. Available supervisory, centralbank, and market data will give some idea of the orderof magnitude of the total losses in the banking system.Such data will also indicate whether deposit with-drawals reflect flight to quality within the bankingsystem or a more general flight from the banking sys-tem. As a banking crisis becomes systemic, creditorsare no longer able to distinguish viable from nonvi-able banks, and confidence in the overall stability ofthe system is jeopardized.

A top priority in the early stages is to stabilizebanking system liabilities by stopping depositor andcreditor runs. Irrespective of the causes of the crisis,the first step should be to provide sufficient liquidityto the banking system to protect the payment systemand give the authorities time to determine the causesof the crisis and design an appropriate policy re-sponse. Options could include some combination ofprotection for creditors, particularly depositors; up-front closure of clearly insolvent banks; and adop-tion of a comprehensive macroeconomic stabiliza-tion package. If these measures are unsuccessful, orif emergency liquidity facilities are limited by a highdegree of dollarization or the inability to sterilize

liquidity injections, the authorities may be forced toconsider administrative measures to stop the depositruns, such as a reduction in deposit liquidity, a fulldeposit freeze, or capital controls. These administra-tive measures are likely to cause major economicdisruption and, therefore, must be viewed only as alast resort if all other measures fail.

While liquidity support is needed to protect thepayment system, the authorities must seek to limitthe impact of this support on prices and the ex-change rate. Liquidity support can cause seriouspressures on prices and the exchange rate. Accord-ingly, the central bank must use available monetaryinstruments to sterilize the growth in base money.The tightening of monetary policy is likely to resultin increases in domestic interest rates. These ratesmust be brought down as quickly as feasible becausehigh rates for protracted periods will severely dam-age bank borrowers and banks, and draw politicalcriticism, as discussed in Section VI.

An often-neglected aspect of crisis management isthe importance of strengthening market confidenceby announcing the authorities’ strategy. Notwith-standing the need to deal with an unfolding crisisand take a multitude of quick actions, attentionshould be given to making public announcements toexplain the authorities’ understanding of the crisisand actions the government is taking. Such an-nouncements should be consistent and authoritativeand ideally be given by a single official spokesmanthroughout the containment and restructuringphases. To the extent possible, a political consensusfor a crisis management strategy should be forged,and the working arrangement among different gov-ernment authorities and agencies defined. Clear andconsistent information will help contain rumors andmisinformation, avoid new panics, and prevent fur-ther erosion of private sector confidence.

Policies for Stabilization

Emergency Liquidity Support

Central bank support provides the first line of de-fense against liquidity shortages in banks. Illiquid

III Crisis Containment

11

15Creditors can refuse to roll over lines of credit, and depositorscan withdraw their funds.

©International Monetary Fund. Not for Redistribution

III CRISIS CONTAINMENT

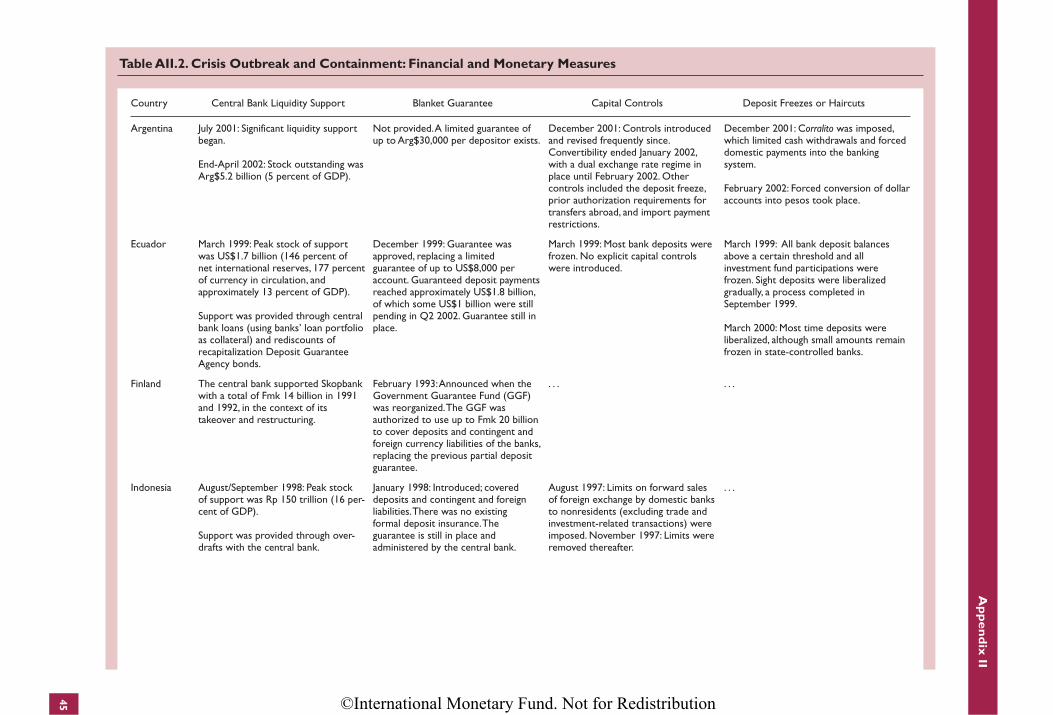

banks should be provided necessary resources, whilethe authorities identify the causes of the crisis, de-velop an appropriate response, and begin imple-menting actions to deal with insolvent banks. Sup-port can be given in a variety of ways, includinguniform reductions in reserve requirements, accessto overdraft facilities and discount windows, openmarket operations, and instruments such as reposand reverse repos (see Table 1 and Appendix II foran overview of measures taken during the contain-ment stage). The criteria for providing such supportmust be uniformly applied to all banks in the system,and the rules for providing such support should betransparent. Differentiating among banks will onlycause uncertainties and could worsen depositor con-fidence. In highly dollarized economies, the centralbank’s ability to provide liquidity support is con-strained by the level of international reserves, andaggressive measures may be needed on bank inter-vention and resolution.

Conditions for central bank liquidity support innormal times, such as collateral and penalty interestrates, may need to be eased. In a systemic crisis, thevalue and quality of collateral may not be known,while excessive penalty rates may add to banks’ dis-tress. At the same time, the central bank must main-tain its intervention rates at levels sufficiently high tomake it a source of last (rather than first) resort forliquidity. Absent traditional central bank safeguards,borrowing banks should be subject instead to restric-tions on their activities and heightened supervision.16

In principle, liquidity support should be providedonly to solvent banks, but the differentiation be-tween solvent and insolvent banks is often difficultin systemic crises because data are poor or outdated.Ideally, insolvent banks should be expeditiously in-tervened. Ceasing liquidity support to selected banksmay not be feasible if this interrupts the payment

12

Table 1. Liquidity Support During Selected Systemic Banking Crises

Country Stock of Support1 Form Notes

Ecuador 13 percent of GDP in 1998–99 Central Bank of Ecuador loans Most loans not repaid; the central and rediscounting of bonds bank forclosed on some fixed issued by the Deposit assets used as collateralGuarantee Agency (AGD)

Indonesia Rp 156 trillion (16 percent of GDP) Bank of Indonesia overdrafts . . .in August 1998

Korea W 11.3 trillion + US$23.3 billion Bank of Korea deposits and All loans repaid(2.5 percent of GDP) in December loans1997

Malaysia RM 35 billion (13 percent of GDP) Bank Negara deposits Most loans repaid by end-1998at end-January 1998

Mexico MEX$38 billion + US$3.9 billion Loans and capital injection from All outstanding foreign currency (2+1.3 percent of GDP) in April 1995 Banking Fund for the Protection loans repaid by early September

of Savings (FOBAPROA) 1995borrowed from the Bank of Mexico

Russia Rub 105–120 billion (4 percent of Central Bank of Russia loans to Rub 9.3 billion repaid by end-1998GDP) between August and October 13 banks for a term of up to 1998 one year

Thailand B 1,037 billion (22 percent of GDP) Loans and capital injection from FIDF claim on financial institutions in early 1999 the Financial Institutions declined to B 227 billion by

Development Fund (FIDF), a end-1999subentity of the Bank of Thailand

Turkey TL 6 quadrillion (3.3 percent of One-week repos by Savings One-week repos rolled over into GDP) in September 2001 Deposit Insurance Fund (SDIF) longer-term instruments

and state banks with the Central Bank of Turkey

1At peak.

16He (2002).

©International Monetary Fund. Not for Redistribution

Policies for Stabilization

system and risks triggering a wider crisis. Stoppingliquidity support to the entire system would be evenless feasible. Given these uncertainties, central banksupport in response to a systemic crisis should be ex-plicitly guaranteed by the government, in the under-standing that any losses accrued will ultimately becarried by the government.

Special factors must be considered in highly dollar-ized economies. The absence of a lender of last resortmay make dollarized systems more prone to runs andmake runs more difficult to stop. Policymakers havetried to tap dollar resources with a variety of means,including high liquidity requirements and prearrangedcredit lines, and from various sources, such as the for-eign bank sector. These measures may be beneficial inthe case of small banking sector problems, but insuffi-cient in the case of a systemic run.

In highly dollarized economies, the constraints onliquidity support and on depositor protection willmake administrative measures more likely. Thesemeasures include securitization of bank liabilities orrestrictions on deposit withdrawals, often precededby a short bank holiday to design and prepare imple-mentation of the measures. Nominal losses to depos-itors should be considered only as a last resort if allother options cannot be implemented or have failed,because nominal losses will make any reintermedia-tion in the financial system even more difficult toachieve (Box 4).

Blanket Guarantee

A blanket guarantee can help to stop runs onbanks caused by loss of depositor confidence in theoverall banking system. A blanket guarantee typi-cally consists of an announcement by the govern-ment that it will ensure that all bank liabilities exceptcapital and subordinated debt are honored. If a lim-ited deposit insurance system is in effect, it wouldhave to be suspended until the blanket guarantee isremoved. A blanket guarantee gives the governmentsome breathing space to develop and start imple-menting a comprehensive restructuring strategy.17

A blanket guarantee alone will not contain a li-quidity crisis. If implemented, it needs to be part of apackage of credible stabilization measures. Credibil-ity depends in the first place on the government’sperceived ability to honor the guarantee. While thegovernment need not have sufficient resources to re-deem the entire stock of bank liabilities, fiscal ca-pacity should be seen as sufficient to meet any ex-pected calls on the guarantee. A blanket guaranteealso requires strong political commitment. The gov-ernment must be perceived to stand fully behind theguarantee. Public disagreements or expressions of

doubt would undermine confidence in a guarantee.Legislation may be required to make it fully effec-tive. The details of the guarantee must be clearly ex-plained to the public. A guarantee will always betested. When depositors and creditors see that theirclaims are protected even when banks are inter-vened, they tend to stay in the system.

A blanket guarantee may not be credible in the faceof unsustainable public debt dynamics or in highlydollarized banking systems. If political uncertaintiesor the government’s financial capacity to deal with thecrisis is in doubt, a blanket guarantee will not be cred-ible.18 If dollarization is moderate, a guarantee couldcover foreign currency liabilities in their domesticcurrency equivalent at market exchange rates. If dol-larization is high, however, and creditors and deposi-tors are fleeing the currency and the banking system,the government will need to show both its capacity(access to foreign reserves and lines of external credit)and willingness to handle foreign exchange with-drawals for the guarantee to be credible.

The coverage of a blanket guarantee must be clearlyspelled out (see Table 2 and Appendix II for countryexperiences). While shareholders and subordinateddebt holders should not be covered, depositors andother creditors of locally incorporated banks (includ-ing branches of foreign banks) are typically includedregardless of residency criteria and currency denomi-nation.19 Off-balance-sheet items become coveredwhen they enter the balance sheet.20 Insider claims arenot typically covered.21 Important groups of near bankdeposit-taking institutions may also be included.

Any guarantee involves moral hazard, which canbe contained if the guarantee is properly designedand managed. A blanket guarantee is a temporary as-surance to stop runs. A guarantee does not imply thatbanks will not require intervention but rather pro-vides a necessary depositor and/or creditor protec-tion for undertaking far-reaching bank restructuringwithout disturbing market confidence. As long asshareholders understand that they will lose their in-vestments if the bank is improperly run, moral haz-ard can be contained. At the same time, various re-strictions may be used to limit reckless operations bybanks, such as eliminating coverage of deposits onwhich excessively high interest rates are paid, andimposing a fee for the guarantee.

13

17Garcia (2000b).

18The use of a blanket guarantee may also be constrained underdifferent private sector involvement scenarios, especially relatedto nonresident creditors.

19Dollar deposits, however, usually would be paid out in thelocal currency, converted at the market exchange rate.

20Derivatives and other off-balance-sheet contracts cannot beexcluded, if a bank continues operations, as derivatives convertinto plain on-balance-sheet liabilities in case of defaults.

21In Indonesia, such transactions were included if contracted at“arm’s length.”

©International Monetary Fund. Not for Redistribution

Blanket guarantees distort market discipline andshould be replaced with limited deposit insurance asconditions permit. The blanket guarantee should beremoved once the banking system is sound. Themarket should be given advance notice of the re-moval (possibly 6–12 months). The guarantee maybe phased out by lifting the guarantee of deposits ofthe more sophisticated creditors (e.g., interbankcreditors followed by large creditors) and, once thesystem has been shown to be stable, the guarantee onall depositors.

Bank Interventions or Closures

As part of the policies for immediate stabiliza-tion, clearly insolvent or nonviable banks should beintervened or closed at an early stage. If the marketsuspects the existence of insolvent banks, failure totake action could undermine efforts to stabilizemarket expectations. Up-front takeovers or closuresof insolvent banks are drastic actions that giveother banks notice that the situation is serious andthe authorities are taking appropriate measures. By

III CRISIS CONTAINMENT

14

Box 4. Dealing with Bank Runs in Dollarized Economies

A high degree of dollarization can have a significantimpact on the policy options available to address bankruns because it imposes limits on the authorities’ abilityto recognize and address emerging banking sectorproblems. This issue emerged forcefully during the re-cent Latin American crises but had also been a concernin earlier episodes of distress. Specific constraints im-posed by dollarization include the absence of an effec-tive lender of last resort or a blanket guarantee to re-spond to bank runs, which in turn can contribute to thesize of the problem by increasing the speed and depthof deposit withdrawals.

Policy Environment with Dollarization

Dollarization complicates the task of addressing de-posit runs, with partial dollarization creating the mostchallenges. For example, with dollarization there maybe considerably more uncertainty about the extent ofthe crisis. In particular, in a partially dollarized system,with currency mismatches on the asset and liabilitiesside of bank balance sheets, rapid changes in the ex-change rate may cause sudden changes in banks’ networth that are difficult to detect promptly. In addition,dollarization may have an impact on credit risk if com-panies or individuals that borrowed in dollars are un-able to generate dollar earnings.

More important, dollarization severely limits theavailability of policy tools. It imposes limits on thepossible extent of liquidity support—there is no unlim-ited lender-of-last-resort facility in foreign currency.The knowledge of rigid limits on possible support pay-ments may make bank runs in highly dollarizedeconomies more likely to occur and, once under way,more self-sustaining. Similarly, if the banking systemis sizeable, the government may well be unable to pro-vide a credible blanket guarantee for foreign currencydeposits. In partially dollarized economies, whilelender-of-last-resort facilities and a blanket guaranteemay be provided in domestic currency, the relativelysmaller domestic monetary base (compared to nondol-larized countries) might lead to a very fast and highdomestic liquidity expansion and/or an even faster col-lapse of the exchange rate. In addition, the nature ofthe guarantee is inconsistent with depositors’ currency

preferences, and it is likely to be less effective than aguarantee in foreign currency would have been.

Partially or fully dollarized economies also face im-portant constraints on supporting macroeconomic poli-cies. Dollarization makes monetary policy less effec-tive, and the need to maintain convertibility at parbetween local dollars and U.S. dollars removes the ex-change rate as an equilibrating mechanism. Dollariza-tion complicates fiscal support for the bank restructur-ing process because funds needed for any publicrecapitalization program may have to be committed inforeign currency to avoid asset/liability currency mis-matches, and may not be consistent with a sustainablepath of foreign debt.

Finally, it would appear that alternatives to lender oflast resort and other safeguards—for example, the pres-ence of foreign banks, prearranged credit lines, or size-able earmarked reserves—are beneficial mainly in thecase of smaller banking sector problems.1 In the case ofsystemic runs in dollarized economies, these safe-guards may not be enough: the presence of a significantshare of foreign institutions does not necessarily limitthe extent of bank runs (Uruguay 2002, Argentina2002). While the perceived support of the parent typi-cally isolates foreign subsidiaries from a systemic runat the outset of a crisis, such support may not alwaysmaterialize—particularly when the crisis proves deepand the authorities’ response slow, uncertain, or confis-catory. Under these circumstances, depositor runs arelikely to extend to foreign banks. Prearranged creditlines may become unavailable in the time of most ur-gent need due to strong built-in safeguards. Sizeableearmarked reserves can stabilize expectations, but un-less they extend to cover a significant portion of bank-ing sector liabilities, there will be residual uncertaintyand the perception of risk.

Modified Policies to Stop Bank Runs in Dollarized Economies

The additional constraints and limited role of safe-guards call for more attention to financial sector sound-ness in dollarized economies. Where, in spite of such added vigilance, bank runs do occur, theory and coun-try experiences suggest that a range of additional issues

©International Monetary Fund. Not for Redistribution

Policies for Stabilization

removing the worst banks, market distortions andexcess capacity are removed from the banking sys-tem to the benefit of remaining banks.

If a credible blanket guarantee is in place, suchearly closures should not affect confidence nega-tively. The operation might be successful evenlacking such a guarantee if the prevailing view of the market is that the targeted institutions are the only insolvent ones. If this is not the case, how-ever, upfront bank takeovers or closures with lossesimposed on creditors and uninsured depositors

could aggravate bank runs on the banking systemas a whole.22

Reflecting fears about these pitfalls, few countrieshave actually imposed losses on creditors and depos-itors in a systemic crisis when closing banks. While

15

needs to be taken into account when formulating an ap-propriate strategy.

Provision of Emergency Liquidity

Liquidity support was identified as a key element inaddressing systemic runs. In a dollarized economy,dollar liquidity support will be limited by the avail-ability of resources, and it might be necessary to havea more clearly defined strategy on liquidity provision.Dollar assistance can be provided as long as suffi-cient dollar resources are available. Sources of liquid-ity can include high international reserves prior to therun (e.g., Argentina 1995); contingent facilities(swaps, repos); international financial support or bailout (e.g., Mexico 1995); or liquidity from sharehold-ers (e.g., Uruguay 2002). Drawing down such re-sources can, however, have costs in terms of credibil-ity and limitations to macroeconomic policymaking.

With limited dollar assistance possible, a decisionneeds to be taken whether to shift assistance in partor fully to local currency (e.g., Bulgaria 1996, Rus-sia 1998, and Ecuador 1999). This option avoids theneed for other stop-gap measures (see also below) andcircumvents constraints on the lender of last resort asthe central bank can print local currency. The expan-sion in the money supply and the currency mismatch,however, are likely to result in a combination of lossof international reserves, exchange rate depreciation,and inflation.

Depositor Protection

Depositor protection, in particular through a blanketguarantee, has proved to be of key importance in ad-dressing systemic bank runs. In a dollarized economy,funding constraints emerge similar to those discussedabove in the case of liquidity support.

• A guarantee of deposits in foreign currency can beeffective as long as sufficient dollar backing isavailable. In some countries, most notably the tran-sition economies, banking systems tended to besmall enough that a full blanket guarantee of for-eign currency deposits might have been an option.In most others though, reserve and fiscal con-

straints would undermine the credibility of a blan-ket guarantee issued in foreign currency.

• A blanket guarantee in local currency is unlikely toinstill depositor confidence because depositorswill demand their original dollars rather than localcurrency counterpart. Moreover, the announce-ment of a local currency guarantee may aggravatethe crisis if depositors fear the banking systemdoes not have sufficient dollar resources and there-fore seek to buy dollars in the exchange market.Guaranteeing deposits in local currency at a fixedexchange rate (Russia 1998) implies a “haircut” todepositors when the exchange rate depreciates, anddepositors are therefore likely to withdraw theirfunds and convert them to foreign exchange assoon as possible.

• One option for depositor protection would be to transfer deposits in failed banks to a bank (pub-lic or private) that is perceived to be sound andwith significant foreign exchange holdings backedup by a corresponding amount of central bank securities to ensure liquidity. In conditions of asystemic run, such banks will only exist in rarecases.

Administrative Measures

Given the added constraints of dollarization for li-quidity support and depositor protection, administrativemeasures are more likely to be needed. Measures men-tioned in the text—securitization of deposits, the exten-sion of deposit maturities, or the imposition of bankholidays or other restrictions on deposit withdrawals—are also available in dollarized settings. Similarly, thegeneral principles stressed for general bank runs (e.g.,uniformity of policies applied to banks) to minimizethe fallout from such policies apply. These measures,while allowing some breathing space, may have a po-tential, however, to delay the success of longer-termreintermediation efforts.

1The issue is also relevant in economies with currencyboards, which face similar challenges.

22In República Bolivariana de Venezuela, the absence of aguarantee led to waves of bank failures in 1994. In the often-citedcase of Indonesia (see Box 5) a poorly managed closing decisioncontributed to a general run on banks and required the retroactiveintroduction of a blanket guarantee.

©International Monetary Fund. Not for Redistribution

III CRISIS CONTAINMENT

suspensions or closures of banks and other financialinstitutions were part of the initial measures to stabi-lize the banking systems in Indonesia, Korea, andThailand, only Thailand imposed losses on somecreditors of the first group of 16 suspended financecompanies (near-banks). In Indonesia, the creditorsand depositors of the 16 banks that were closed ini-tially were subsequently all compensated in full(Box 5).

Administrative Measures

If a package of market-oriented stabilization mea-sures is not feasible or fails to contain the crisis, theauthorities may have to adopt administrative mea-sures to avoid losing monetary control. Such mea-sures include securitization of deposits, forced exten-sion of maturities, or a deposit freeze. Administrativemeasures are extremely disruptive and should be usedwith caution. They can cause major economic andpolitical disruption, and therefore must be viewed asa final, desperate measure to stop a run on banks if all

other measures fail. Banks should be treated uni-formly when administrative measures are applied.Differential treatment could worsen the banking crisis and may impede restoration of financial ser-vices. The administrative measures may cover all de-posits or may allow for a small amount of funds to bewithdrawn.