NVAB Commissionaire Structure ucturing

33

Governance of commissionaire and LRD business models Rutger Hafkenscheid OCTOBER 29, 2010 VMW TAXAND

-

Upload

rutgerhafkenscheid -

Category

Documents

-

view

264 -

download

1

Transcript of NVAB Commissionaire Structure ucturing

Governance of commissionaire and LRD business models

Rutger Hafkenscheid

OCTOBER 29, 2010

VMWTAXAND

Some trends

• Since 1990, globalization and ERP software development allowed global & centralized business functions, such as

• r&d• marketing• sourcing & procurement• manufacturing• inventory management• distribution.

• Business restructuring helped to rationalize these functions and optimize their supply chain and the efficient use of business resources.

• These business restructurings also allowed companies to optimize their tax structure and transfer pricing systems by concentrating business risks and the expected profits attached to those risks in low tax juridisctions.

Example: before restructuring

Production plants

Production plants

Sales officesSales officesSupplierSupplier CustomerCustomer

Credit

Price

Inventory

Product apetite

Sourcing

Financing

Price

Capacity

Employment cost

Employment cost

$50 $250$150

Profit $100@30%

Profit $100@30%

Profit $200@30%

Example: after restructuring

Toll Manufact.

Toll Manufact. LRDLRD

SupplierSupplier CustomerCustomer

Credit

Price

Inventory

Product apetite

Sourcing

Financing

Price

Capacity

Employment cost

Employment cost

Central Enterprene

ur

Central Enterprene

ur $250$50

Profit $20@30%

Profit $20@30%

Profit $160@10%

Profit $200@14%

A typical US MNE structure

Toll Manufact.

Toll Manufact. LRDLRD

Central Enterprene

ur(Tax haven)

Central Enterprene

ur(Tax haven)

US ParentUS Parent

Profit $20@30%

Profit $20@30%

Profit $160@10%

Profit $200@14%

Profit $200 @35%Credit @14%

Conclusion

• The IRS sees tax revenu decline• Local authorities see tax revenu decline

Relation between profit allocation and ETR?

Source: Tax Notes Services, August 16, 2010

‘The amount of profit shifted to low-tax countries is not consistent with the measurable economic activity in those countries’

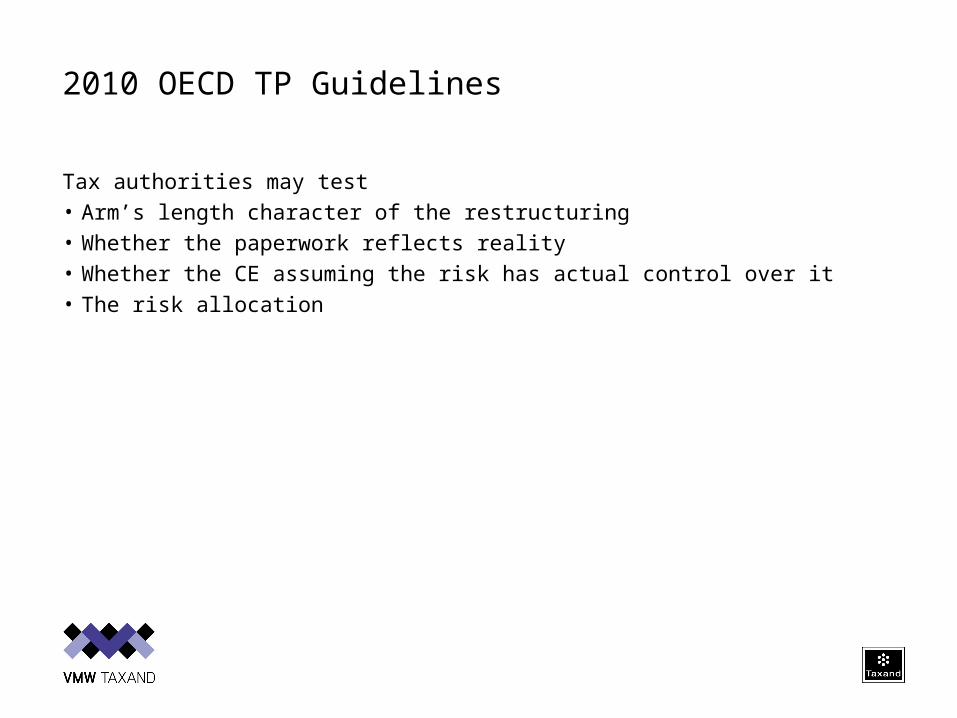

2010 OECD TP Guidelines

Tax authorities may test• Arm’s length character of the restructuring• Whether the paperwork reflects reality• Whether the CE assuming the risk has actual control over it• The risk allocation

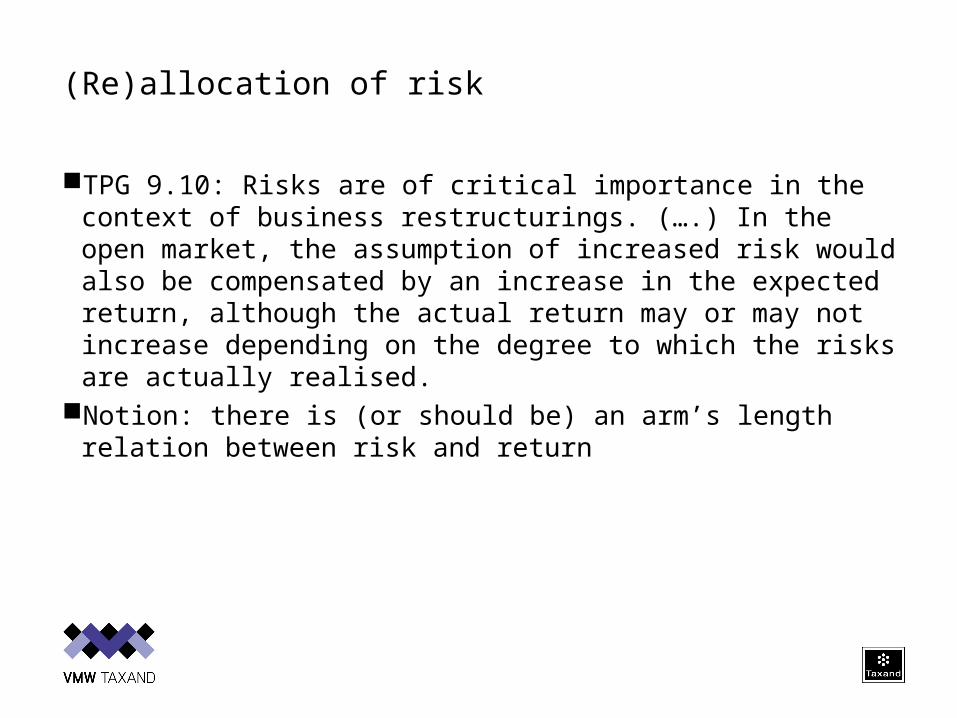

(Re)allocation of risk

TPG 9.10: Risks are of critical importance in the context of business restructurings. (….) In the open market, the assumption of increased risk would also be compensated by an increase in the expected return, although the actual return may or may not increase depending on the degree to which the risks are actually realised.

Notion: there is (or should be) an arm’s length relation between risk and return

Risk

• Inherent to risk is that one event may have two or more scenarios and thus two or more outcomes

• Economic theory uses three measurements to evaluate risk• Expected value• Variance• WACC

Expected value

• Definition: probability weighted average of all possible outcomes.• Example

• Allows to compare two investments with different returns and risk profiles.

Variance

• Definition: distance between expected value and possible outcomes

• Example

• Investment A: variance from $46,000 is -$56,000 and +$14,000

• Investment B: variance from $41,250 is -$46,250 and +$8,750.

• Allows to compare the relative risk profiles of two investments

• Often expressed in standard deviation

Risk-return relation

Expected return

Expected return

VarianceVariance

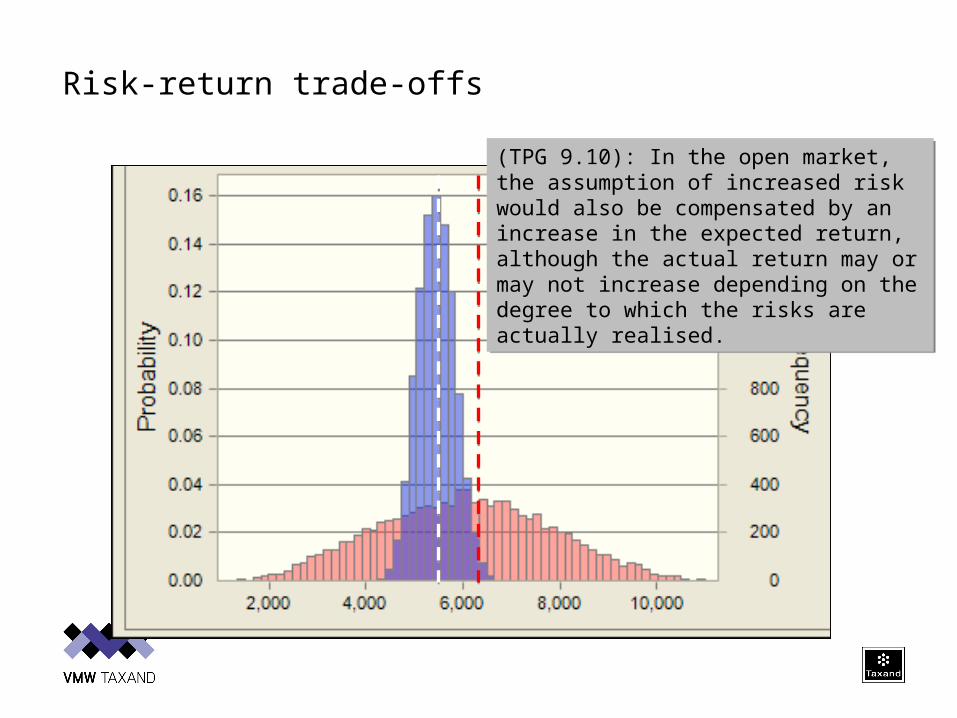

Risk-return trade-offs

Risk premiumRisk premium

Profit potential given up

Profit potential given up

Loss potential hedged

Loss potential hedged

Weighted average cost of capital (WACC)

WACCWACC

Average cost of equity

Average cost of equity

Average cost of debt

Average cost of debt

Capital structure

(D/E Ratio)

Capital structure

(D/E Ratio)

Cost of equityCost of equity

Average gross cost of

debt

Average gross cost of

debtTax shieldTax shield

Risk free rate

(3-4%)

Risk free rate

(3-4%)

Market risk premium(4-5%)

Market risk premium(4-5%)

Industry beta(0.68-2.4)

Industry beta(0.68-2.4)

Allows to compare the values of two investments with a different risk profile by discounting their cashflows at a risk adjusted discount rate

Example

Risk-return trade-offs

WACC 12%WACC 12%

WACC 7%WACC 7%

Risk-return trade-offs

(TPG 9.10): In the open market, the assumption of increased risk would also be compensated by an increase in the expected return, although the actual return may or may not increase depending on the degree to which the risks are actually realised.

(TPG 9.10): In the open market, the assumption of increased risk would also be compensated by an increase in the expected return, although the actual return may or may not increase depending on the degree to which the risks are actually realised.

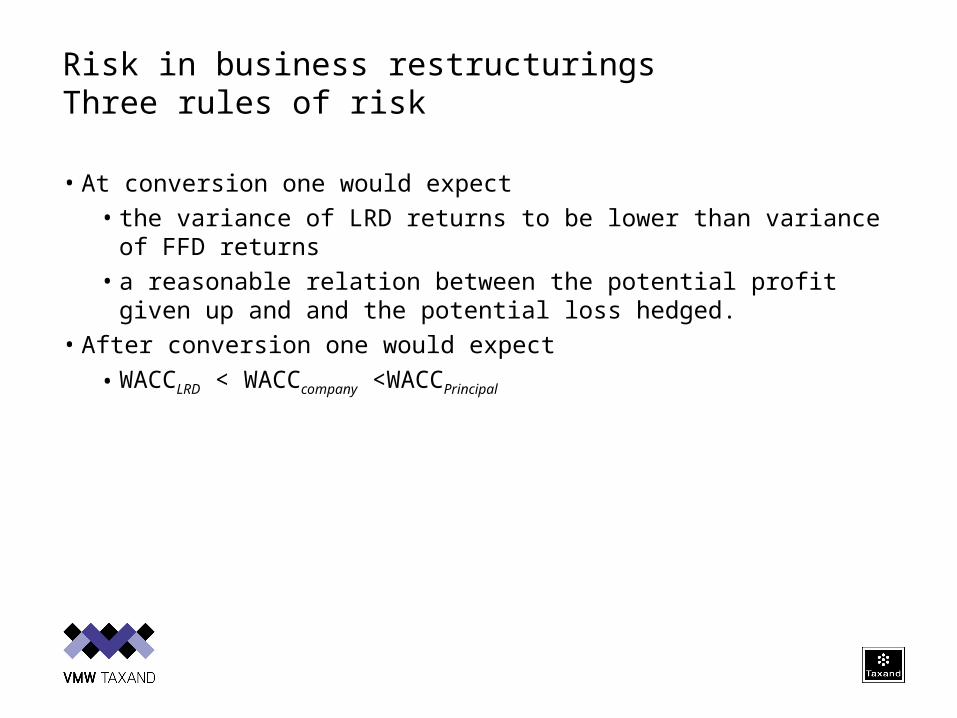

Risk in business restructuringsThree rules of risk

• At conversion one would expect

• the variance of LRD returns to be lower than variance of FFD returns

• a reasonable relation between the potential profit given up and and the potential loss hedged.

• After conversion one would expect

• WACCLRD < WACCcompany <WACCPrincipal

Case studyFFD Business Model

Operational profit

Operational profit

RevenuRevenu

SalesSales

ASP($47,50-$52,50)

ASP($47,50-$52,50)

Sales volume(850k—950k)

Sales volume(850k—950k)

Cost of sales

Cost of sales

ACP($37,50)

ACP($37,50)

Sales volume

(850k-950k)

Sales volume

(850k-950k)

OpexOpex

Fixed Opex($5.5m)

Fixed Opex($5.5m)

Variable Opex

Variable Opex

Cost ratio(10%)

Cost ratio(10%) SalesSales

ASP($47,50-$52,50)

ASP($47,50-$52,50)

Sales volume

(850k-950k)

Sales volume

(850k-950k)

Case study

Risk distribution FFD

Conversion FFD into commissionaireMidpoint commission rate: 2%Upper Quartile commission rate: 5%

Options realistically available:

Current situation:

Conversion FFD into commissionaireMidpoint commission rate: 2%Upper Quartile commission rate: 5%

5% commission rate2% commission rate

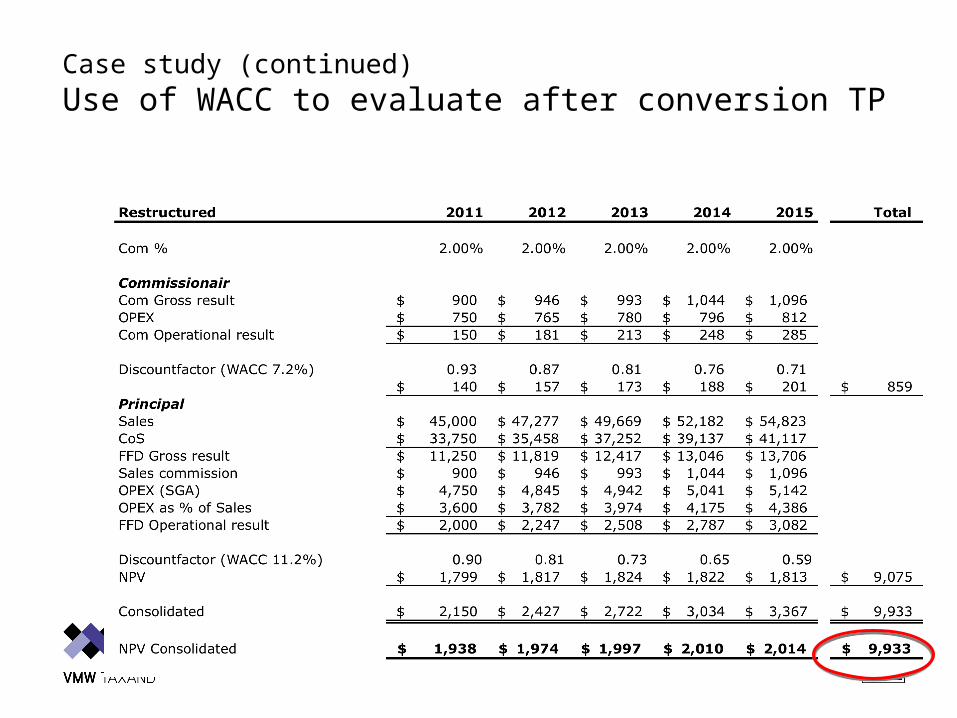

Case study (continued)Use of WACC to evaluate after conversion TP

Value Consolidated

Value Consolidated

Value LRDValue LRD Value PrincipalValue Principal

Forecast LRD profit

Forecast LRD profit LRD WACCLRD WACC Forecast

Principal profitForecast

Principal profit Principal WACCPrincipal WACC

Case study (continued)

Use of WACC to evaluate after conversion TP

Case study (continued)

Use of WACC to evaluate after conversion TP

Case study (continued)

Solved on commissionaire WACC

Case study (continued)

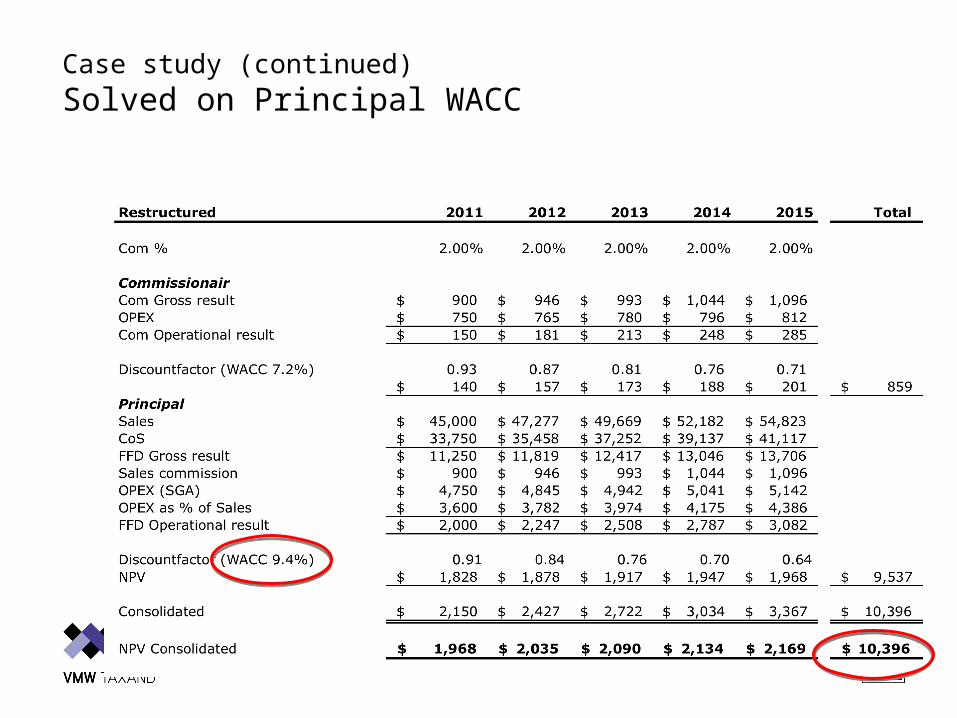

Solved on Principal WACC

Case study (continued)

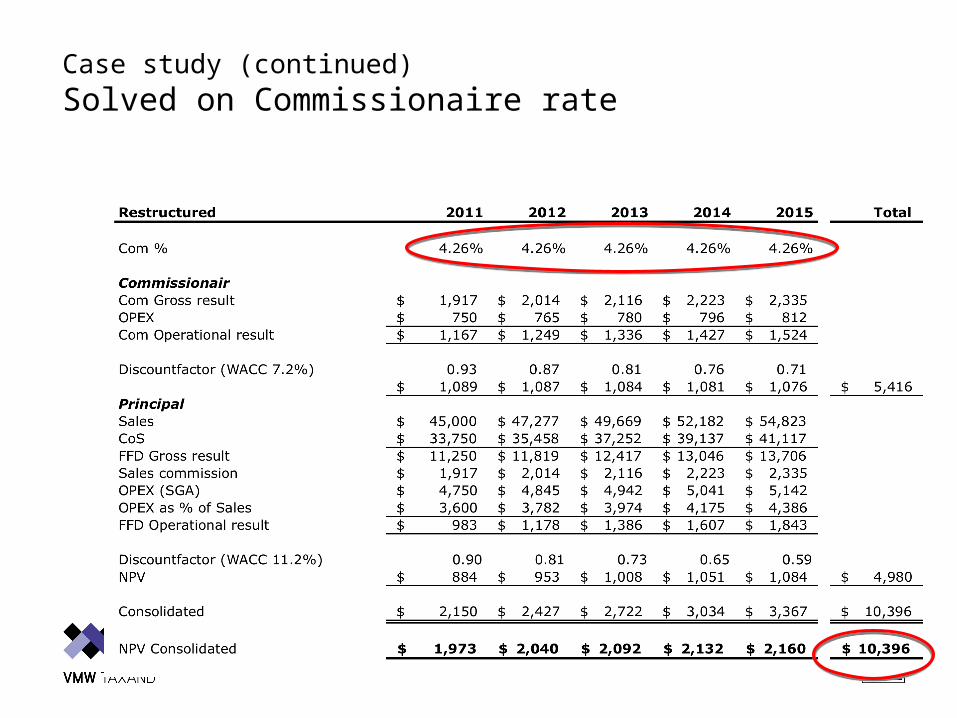

Solved on Commissionaire rate

… But how about the benchmark studies?

1 Tax authorities have become as good in manipulating databases as taxpayers.

2 Databases allow only a qualitative functional analysis, but no quantitative

3 >70% cross border transactions are intercompany, and the number is increasing. So how reliable is a database?

Morale of this story

1 Do an economic sanity check on the risk allocation of a business restructuring before the tax authorities do it for you…

2 Why interesting for lawyers? – Client privilege!