Novartis Q4 and Annual Results 2016 - Media Presentation

67

Novartis AG Media Relations Q4 and Full Year 2016 Results Media presentation | January 25, 2017

Transcript of Novartis Q4 and Annual Results 2016 - Media Presentation

Novartis AG

Media Relations

Q4 and Full Year 2016

Results

Media presentation | January 25, 2017

Disclaimer

This presentation contains forward-looking statements that can be identified by terminology such as such as “potential,” “expected,” “will,” “planned,” or similar expressions, or by express or implied

discussions regarding potential new products, potential new indications for existing products, or regarding potential future revenues from any such products; potential shareholder returns or credit

ratings; or regarding the potential outcome of the announced review of options being undertaken to maximize shareholder value of the Alcon Division; or regarding the potential financial or other

impact on Novartis or any of our divisions of the significant reorganizations of recent years, including the creation of the Pharmaceuticals and Oncology business units to form the Innovative

Medicines Division, the creation of the Global Drug Development organization and Novartis Operations (including Novartis Technical Operations and Novartis Business Services), the transfer of the

Ophthalmic Pharmaceuticals products of our Alcon Division to the Innovative Medicines Division, the transfer of selected mature, non-promoted pharmaceutical products from the Innovative

Medicines Division to the Sandoz Division, and the transactions with GSK, Lilly and CSL; or regarding the potential impact of the share buyback plan; or regarding potential future sales or earnings

of the Novartis Group or any of its divisions; or by discussions of strategy, plans, expectations or intentions. You should not place undue reliance on these statements. Such forward looking

statements are based on the current beliefs and expectations of management regarding future events, and are subject to significant known and unknown risks and uncertainties. Should one or

more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those set forth in the forward looking statements. There

can be no guarantee that any new products will be approved for sale in any market, or that any new indications will be approved for any existing products in any market, or that any approvals which

are obtained will be obtained at any particular time, or that any such products will achieve any particular revenue levels. Nor can there be any guarantee that the review of options being undertaken

to maximize shareholder value of the Alcon Division will reach any particular results, or at any particular time. Neither can there be any guarantee that Novartis will be able to realize any of the

potential strategic benefits, synergies or opportunities as a result of the significant reorganizations of recent years, including the creation of the Pharmaceuticals and Oncology business units to

form the Innovative Medicines Division, the creation of the Global Drug Development organization and Novartis Operations (including Novartis Technical Operations and Novartis Business

Services), the transfer of the Ophthalmic Pharmaceuticals products of our Alcon Division to the Innovative Medicines Division, the transfer of selected mature, non-promoted pharmaceutical

products from the Innovative Medicines Division to the Sandoz Division, and the transactions with GSK, Lilly and CSL. Neither can there be any guarantee that shareholders will achieve any

particular level of shareholder returns. Nor can there be any guarantee that the Group, or any of its divisions, will be commercially successful in the future, or achieve any particular credit rating or

financial results. In particular, management’s expectations could be affected by, among other things: regulatory actions or delays or government regulation generally; the potential that the strategic

benefits, synergies or opportunities expected from the significant reorganizations of recent years, including the creation of the Pharmaceuticals and Oncology business units to form the Innovative

Medicines Division, the creation of the Global Drug Development organization and Novartis Operations (including Novartis Technical Operations and Novartis Business Services), the transfer of the

Ophthalmic Pharmaceuticals products of our Alcon Division to the Innovative Medicines Division, the transfer of selected mature, non-promoted pharmaceutical products from the Innovative

Medicines Division to the Sandoz Division, and the transactions with GSK, Lilly and CSL may not be realized or may take longer to realize than expected; the inherent uncertainties involved in

predicting shareholder returns or credit ratings; the uncertainties inherent in the research and development of new healthcare products, including clinical trial results and additional analysis of

existing clinical data; our ability to obtain or maintain proprietary intellectual property protection, including the ultimate extent of the impact on Novartis of the loss of patent protection and exclusivity

on key products which commenced in prior years and will continue this year; safety, quality or manufacturing issues; global trends toward health care cost containment, including ongoing pricing

and reimbursement pressures, such as from increased publicity on pharmaceuticals pricing, including in certain large markets; uncertainties regarding actual or potential legal proceedings,

including, among others, actual or potential product liability litigation, litigation and investigations regarding sales and marketing practices, intellectual property disputes and government

investigations generally; general economic and industry conditions, including uncertainties regarding the effects of the persistently weak economic and financial environment in many countries;

uncertainties regarding future global exchange rates; uncertainties regarding future demand for our products; and uncertainties regarding potential significant breaches of data security or data

privacy, or disruptions of our information technology systems; and other risks and factors referred to in Novartis AG’s current Form 20-F on file with the US Securities and Exchange Commission.

Novartis is providing the information in this presentation as of this date and does not undertake any obligation to update any forward-looking statements as a result of new information, future events

or otherwise.

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 2

1. Group review Joseph Jimenez, Chief Executive Officer

2. Financial review Harry Kirsch, Chief Financial Officer

3. R&D Jay Bradner, President NIBR & Vas Narasimhan, Global Head

Drug Development & CMO

4. Q&A All presenters

Agenda

3

1. Group review

2016 in review

Industry trends & our strategy to win

The next growth phase

Last year we established 5 objectives for 2016

Deliver strong

Financial Results

Strengthen

Innovation

Improve

Alcon Performance

Capture

Cross-Divisional Synergies

Build a

High-Performing Organization

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 5

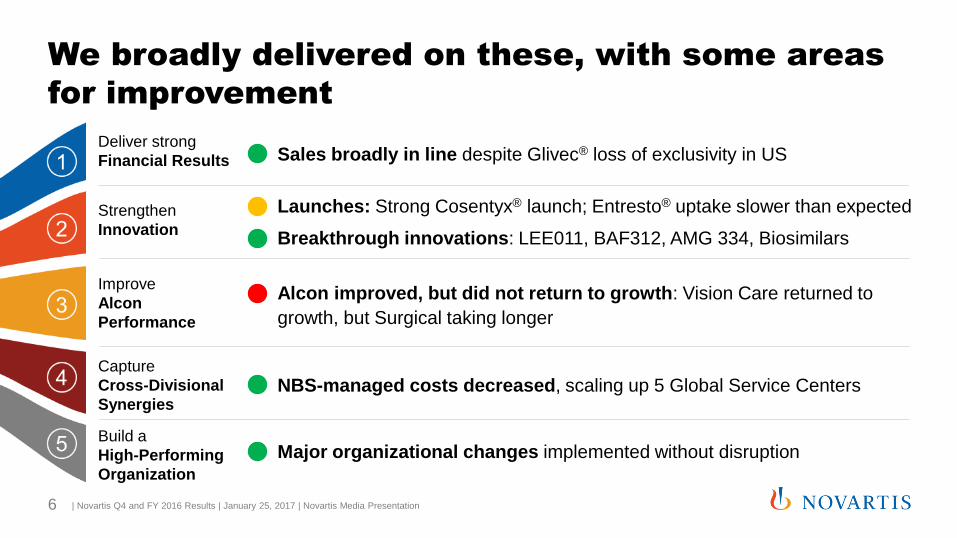

We broadly delivered on these, with some areas

for improvement

Deliver strong

Financial Results

Strengthen

Innovation

Improve

Alcon

Performance

Capture

Cross-Divisional

Synergies

Build a

High-Performing

Organization

Sales broadly in line despite Glivec® loss of exclusivity in US

Breakthrough innovations: LEE011, BAF312, AMG 334, Biosimilars

Alcon improved, but did not return to growth: Vision Care returned to

growth, but Surgical taking longer

Major organizational changes implemented without disruption

Launches: Strong Cosentyx® launch; Entresto® uptake slower than expected

NBS-managed costs decreased, scaling up 5 Global Service Centers

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 6

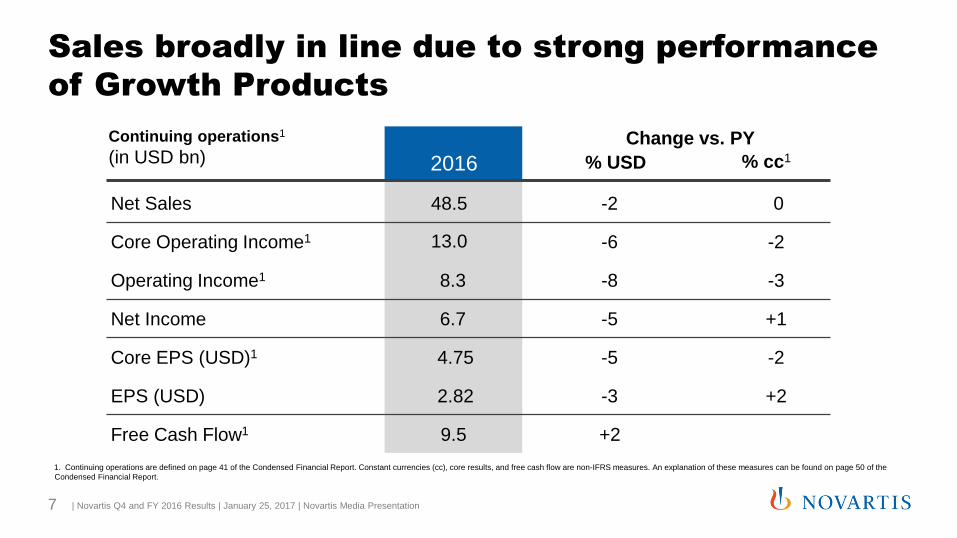

Sales broadly in line due to strong performance

of Growth Products

Continuing operations1

(in USD bn) 2016 % USD % cc1

Net Sales 48.5 -2 0

Core Operating Income1 13.0 -6 -2

Operating Income1 8.3 -8 -3

Net Income 6.7 -5 +1

Core EPS (USD)1 4.75 -5 -2

EPS (USD) 2.82 -3 +2

Free Cash Flow1 9.5 +2

Change vs. PY

1. Continuing operations are defined on page 41 of the Condensed Financial Report. Constant currencies (cc), core results, and free cash flow are non-IFRS measures. An explanation of these measures can be found on page 50 of the

Condensed Financial Report.

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 7

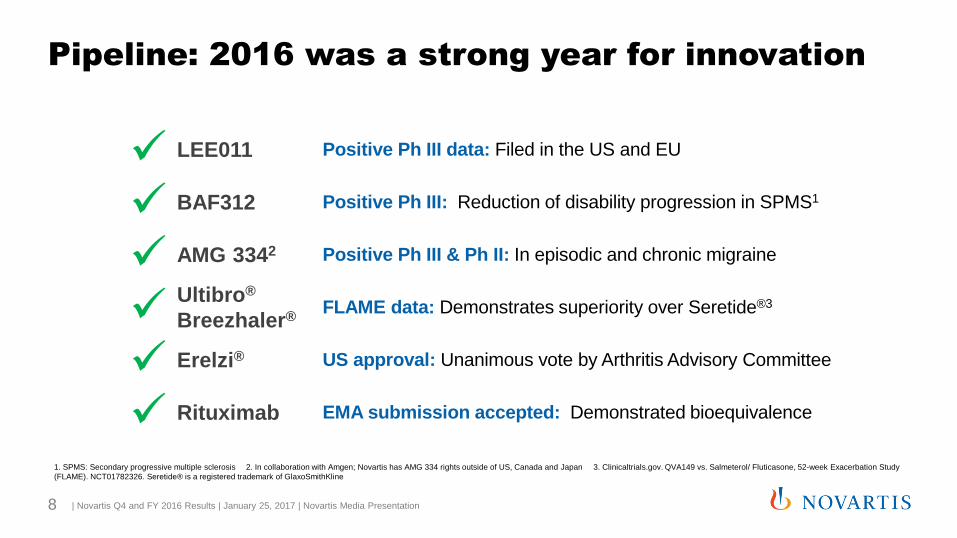

Pipeline: 2016 was a strong year for innovation

1. SPMS: Secondary progressive multiple sclerosis 2. In collaboration with Amgen; Novartis has AMG 334 rights outside of US, Canada and Japan 3. Clinicaltrials.gov. QVA149 vs. Salmeterol/ Fluticasone, 52-week Exacerbation Study

(FLAME). NCT01782326. Seretide® is a registered trademark of GlaxoSmithKline

BAF312 Positive Ph III: Reduction of disability progression in SPMS1

Ultibro®

Breezhaler® FLAME data: Demonstrates superiority over Seretide®3

LEE011 Positive Ph III data: Filed in the US and EU

AMG 3342 Positive Ph III & Ph II: In episodic and chronic migraine

Rituximab EMA submission accepted: Demonstrated bioequivalence

Erelzi® US approval: Unanimous vote by Arthritis Advisory Committee

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 8

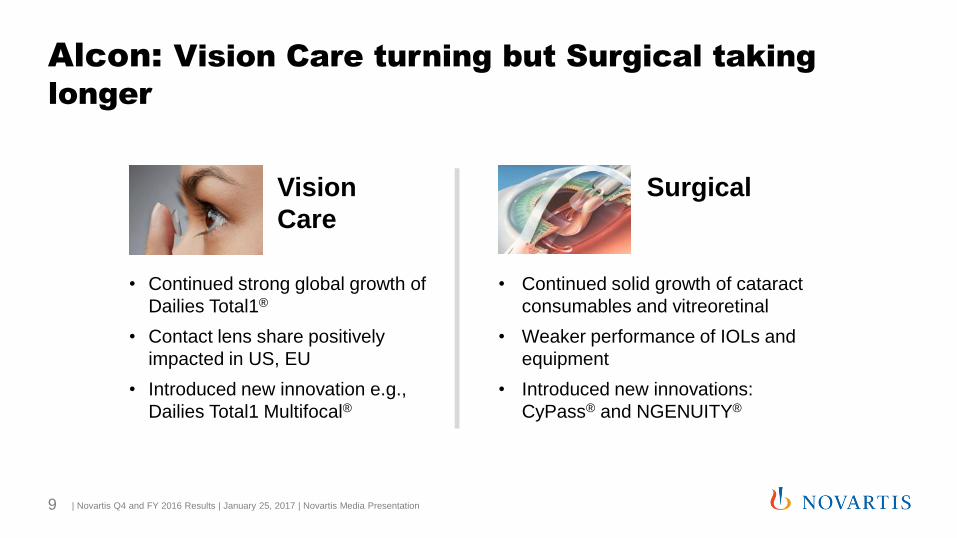

Alcon: Vision Care turning but Surgical taking

longer

Surgical Vision

Care

• Continued strong global growth of

Dailies Total1®

• Contact lens share positively

impacted in US, EU

• Introduced new innovation e.g.,

Dailies Total1 Multifocal®

• Continued solid growth of cataract

consumables and vitreoretinal

• Weaker performance of IOLs and

equipment

• Introduced new innovations:

CyPass® and NGENUITY®

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 9

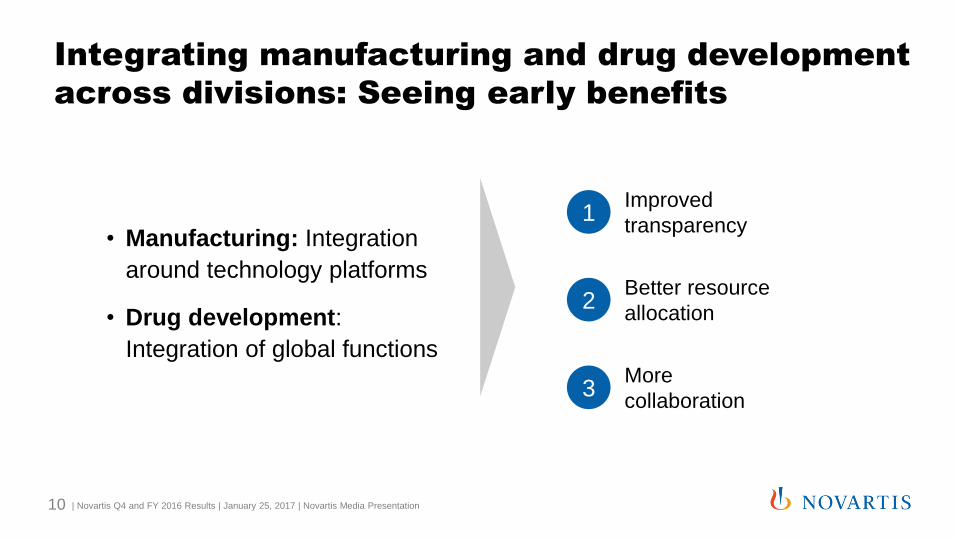

Integrating manufacturing and drug development

across divisions: Seeing early benefits

Improved

transparency 1

Better resource

allocation 2

More

collaboration 3

• Manufacturing: Integration

around technology platforms

• Drug development:

Integration of global functions

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 10

1. Group review

2016 in review

Industry trends & our strategy to win

The next growth phase

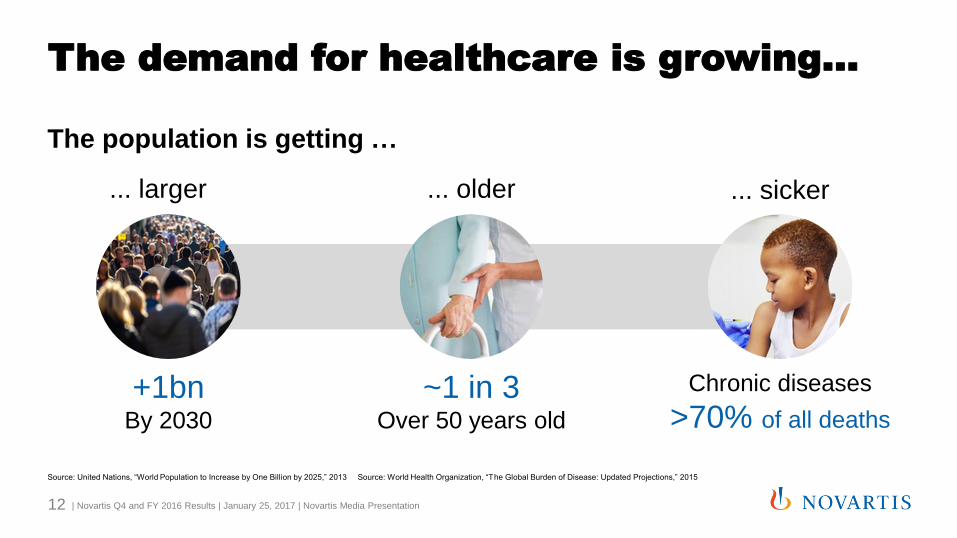

The demand for healthcare is growing...

... older

~1 in 3 Over 50 years old

... larger

+1bn By 2030

... sicker

Chronic diseases

>70% of all deaths

Source: United Nations, “World Population to Increase by One Billion by 2025,” 2013 Source: World Health Organization, “The Global Burden of Disease: Updated Projections,” 2015

The population is getting …

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 12

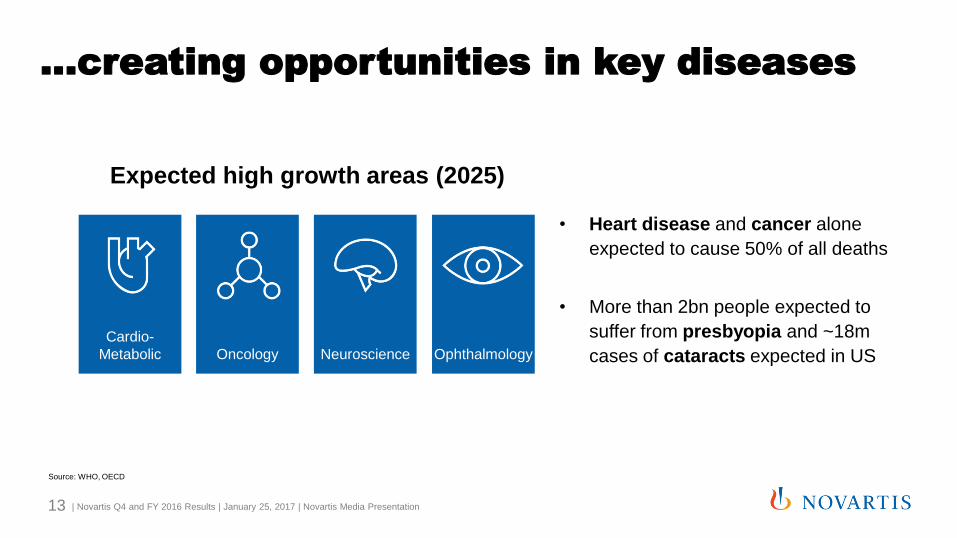

...creating opportunities in key diseases

Source: WHO, OECD

Expected high growth areas (2025)

Neuroscience Ophthalmology

Cardio-

Metabolic Oncology

• Heart disease and cancer alone

expected to cause 50% of all deaths

• More than 2bn people expected to

suffer from presbyopia and ~18m

cases of cataracts expected in US

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 13

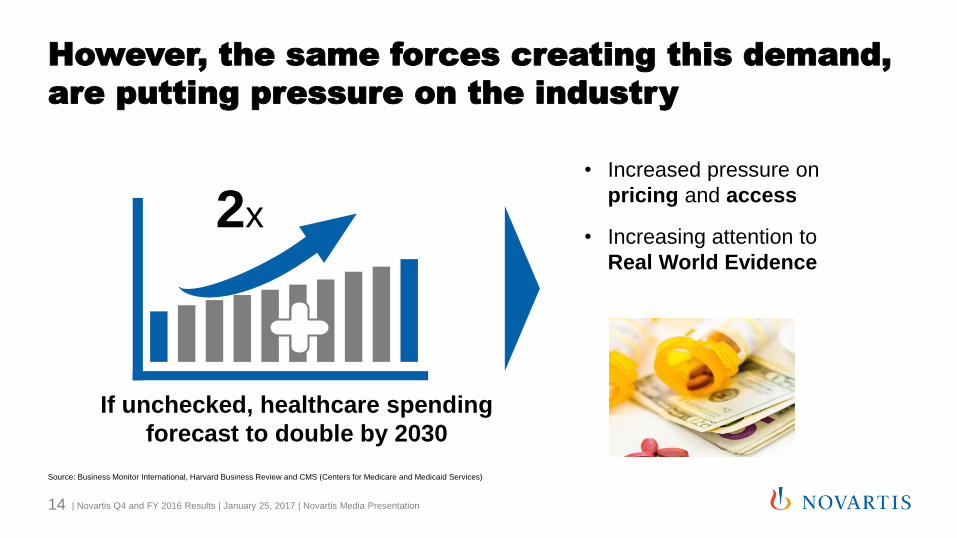

However, the same forces creating this demand,

are putting pressure on the industry

• Increased pressure on

pricing and access

• Increasing attention to

Real World Evidence

If unchecked, healthcare spending

forecast to double by 2030

2x

Source: Business Monitor International, Harvard Business Review and CMS (Centers for Medicare and Medicaid Services)

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 14

To win in this environment, we are rethinking all

aspects of our business

We are “Reimagining Medicine”

How we innovate 1 How we sell 2 How we operate 3

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 15

1. Group review

2016 in review

Industry trends & our strategy to win

The next growth phase

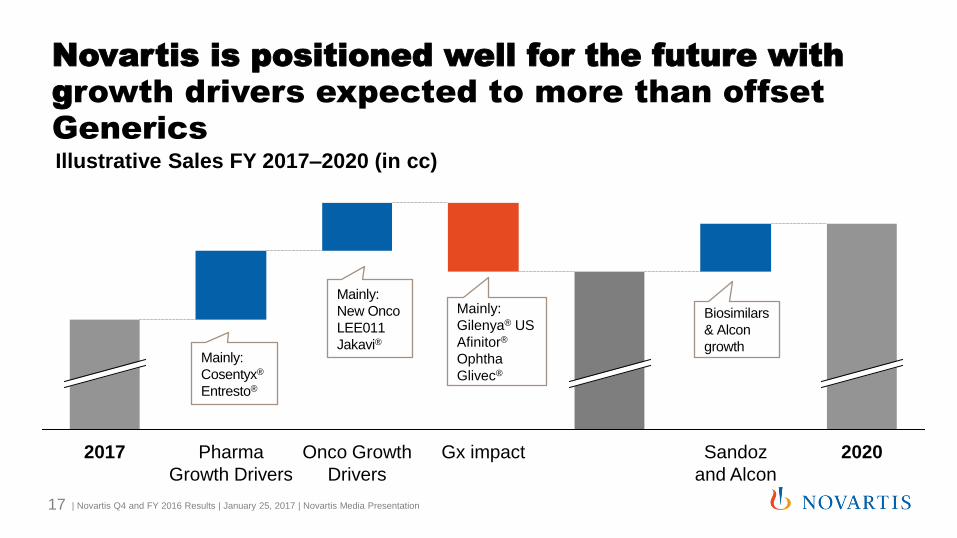

Novartis is positioned well for the future with

growth drivers expected to more than offset

Generics

2020 Sandoz

and Alcon

Gx impact Onco Growth

Drivers

Pharma

Growth Drivers

2017

Mainly:

New Onco

LEE011

Jakavi®

Mainly:

Cosentyx®

Entresto®

Biosimilars

& Alcon

growth

Mainly:

Gilenya® US

Afinitor®

Ophtha

Glivec®

Illustrative Sales FY 2017–2020 (in cc)

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 17

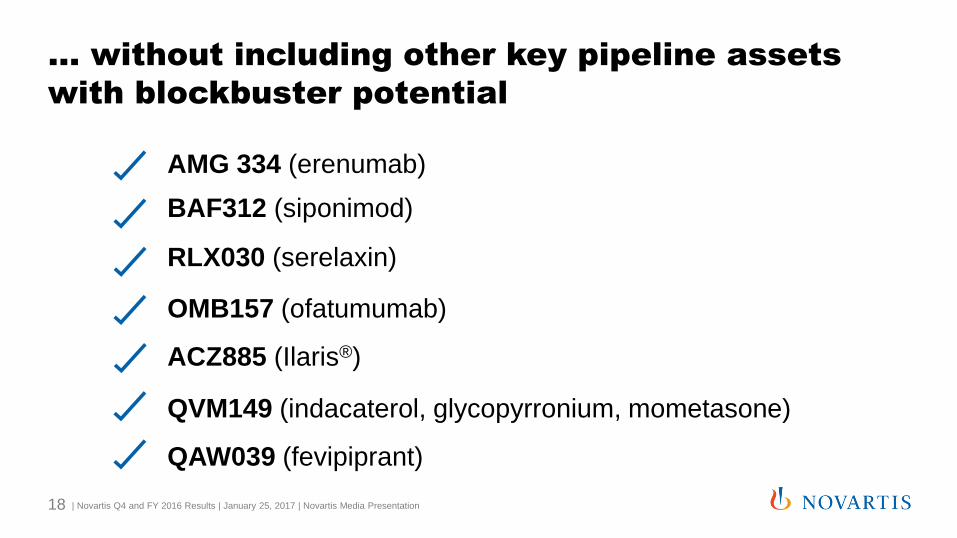

... without including other key pipeline assets

with blockbuster potential

AMG 334 (erenumab)

RLX030 (serelaxin)

ACZ885 (Ilaris®)

QVM149 (indacaterol, glycopyrronium, mometasone)

QAW039 (fevipiprant)

OMB157 (ofatumumab)

BAF312 (siponimod)

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 18

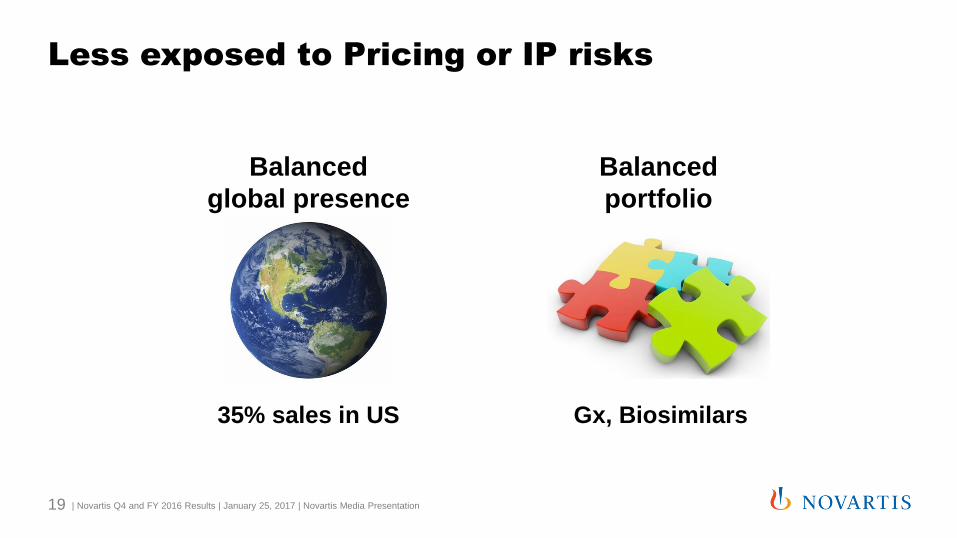

Less exposed to Pricing or IP risks

Balanced

global presence

35% sales in US Gx, Biosimilars

Balanced

portfolio

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 19

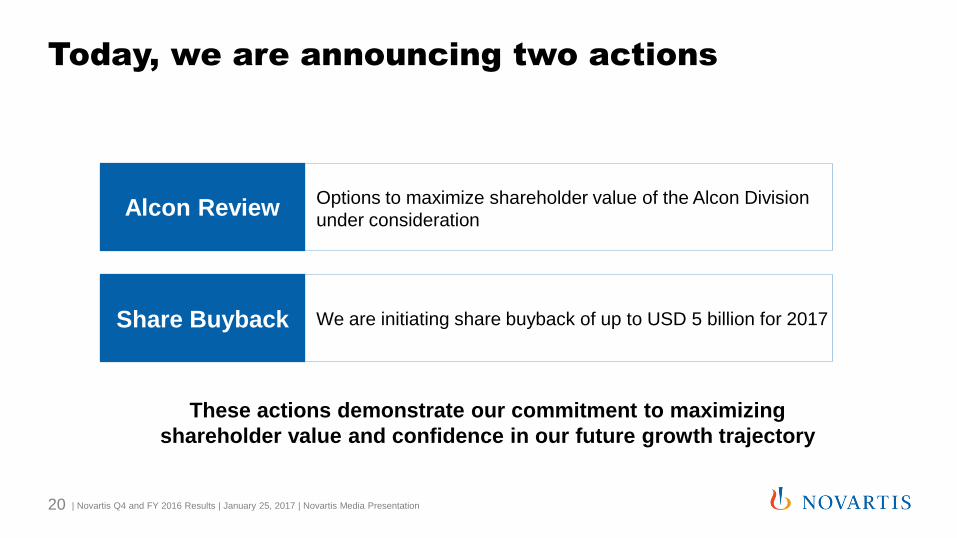

Today, we are announcing two actions

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 20

Alcon Review Options to maximize shareholder value of the Alcon Division

under consideration

Share Buyback We are initiating share buyback of up to USD 5 billion for 2017

These actions demonstrate our commitment to maximizing

shareholder value and confidence in our future growth trajectory

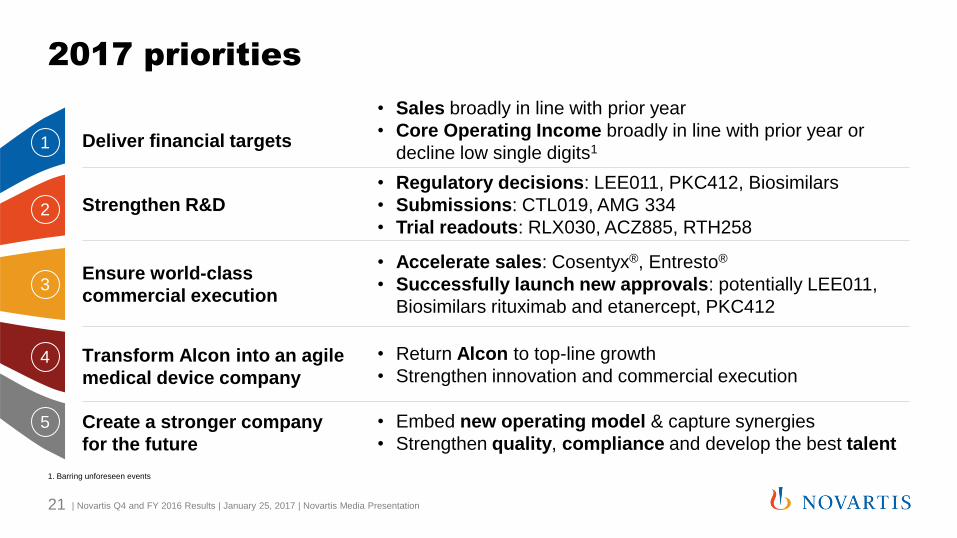

2017 priorities

Strengthen R&D

Ensure world-class

commercial execution

Transform Alcon into an agile

medical device company

Create a stronger company

for the future

Deliver financial targets

2

3

4

5

1

• Regulatory decisions: LEE011, PKC412, Biosimilars

• Submissions: CTL019, AMG 334

• Trial readouts: RLX030, ACZ885, RTH258

• Sales broadly in line with prior year

• Core Operating Income broadly in line with prior year or

decline low single digits1

• Accelerate sales: Cosentyx®, Entresto®

• Successfully launch new approvals: potentially LEE011,

Biosimilars rituximab and etanercept, PKC412

• Return Alcon to top-line growth

• Strengthen innovation and commercial execution

• Embed new operating model & capture synergies

• Strengthen quality, compliance and develop the best talent

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 21

1. Barring unforeseen events

1. Group review Joseph Jimenez, Chief Executive Officer

2. Financial review Harry Kirsch, Chief Financial Officer

3. R&D Jay Bradner, President NIBR & Vas Narasimhan, Global Head

Drug Development & CMO

4. Q&A All presenters

Agenda

22

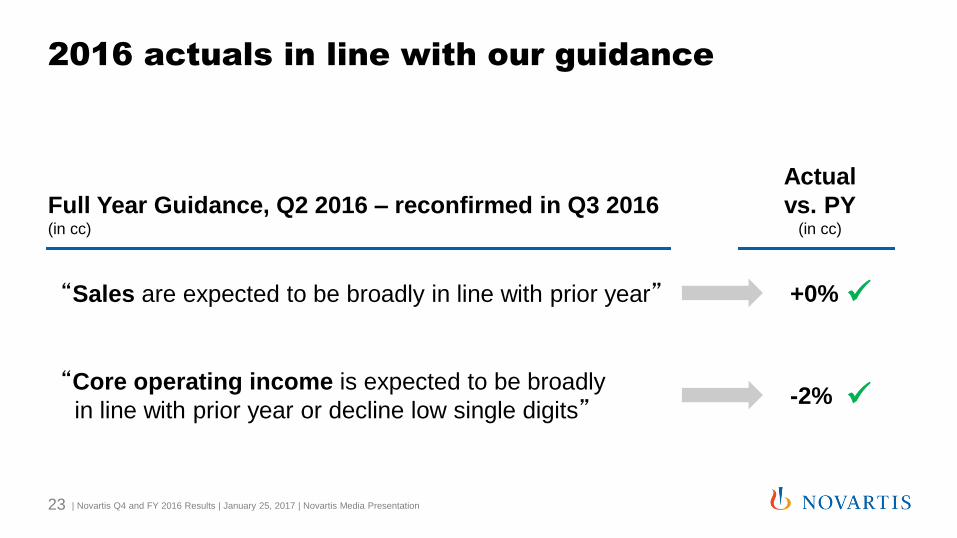

2016 actuals in line with our guidance

Actual

vs. PY (in cc)

Full Year Guidance, Q2 2016 – reconfirmed in Q3 2016 (in cc)

“Sales are expected to be broadly in line with prior year” +0%

-2% “Core operating income is expected to be broadly

in line with prior year or decline low single digits”

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 23

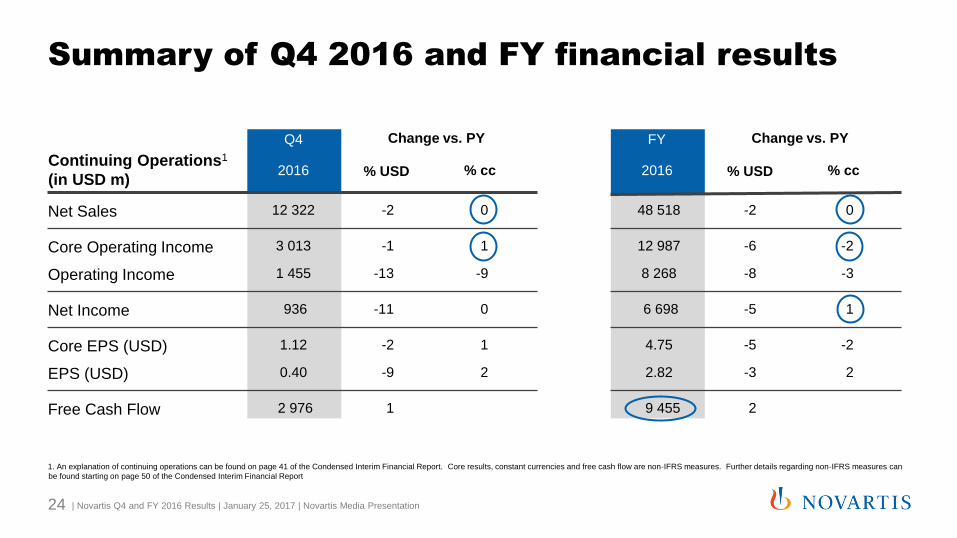

Summary of Q4 2016 and FY financial results

1. An explanation of continuing operations can be found on page 41 of the Condensed Interim Financial Report. Core results, constant currencies and free cash flow are non-IFRS measures. Further details regarding non-IFRS measures can

be found starting on page 50 of the Condensed Interim Financial Report

Q4

Continuing Operations1

(in USD m) 2016 % USD % cc

Net Sales 12 322 -2 0

Core Operating Income 3 013 -1 1

Operating Income 1 455 -13 -9

Net Income 936 -11 0

Core EPS (USD) 1.12 -2 1

EPS (USD) 0.40 -9 2

Free Cash Flow 2 976 1

Change vs. PY FY

2016 % USD % cc

48 518 -2 0

12 987 -6 -2

8 268 -8 -3

6 698 -5 1

4.75 -5 -2

2.82 -3 2

9 455 2

Change vs. PY

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 24

Q4 2016

Net sales

change vs. PY

Core operating

income

change vs. PY Core ROS

Core margin

change vs. PY

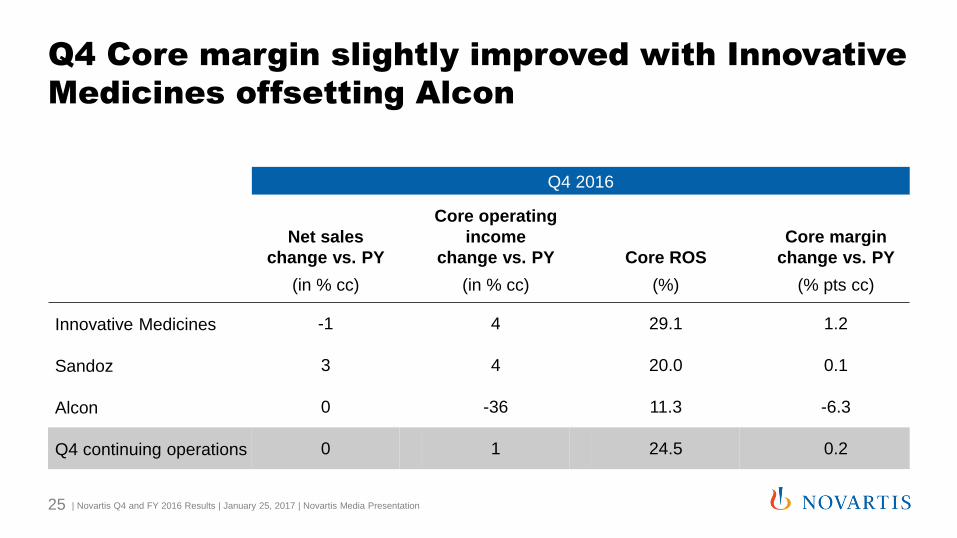

(in % cc) (in % cc) (%) (% pts cc)

Innovative Medicines -1 4 29.1 1.2

Sandoz 3 4 20.0 0.1

Alcon 0 -36 11.3 -6.3

Q4 continuing operations 0 1 24.5 0.2

Q4 Core margin slightly improved with Innovative

Medicines offsetting Alcon

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 25

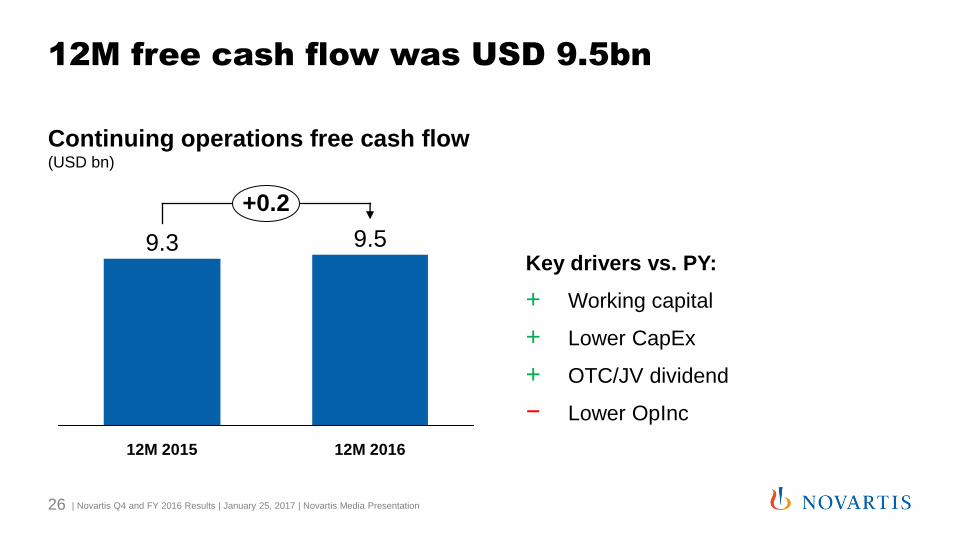

12M free cash flow was USD 9.5bn

Key drivers vs. PY:

+ Working capital

+ Lower CapEx

+ OTC/JV dividend

− Lower OpInc

+0.2

12M 2016

9.5

12M 2015

9.3

Continuing operations free cash flow (USD bn)

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 26

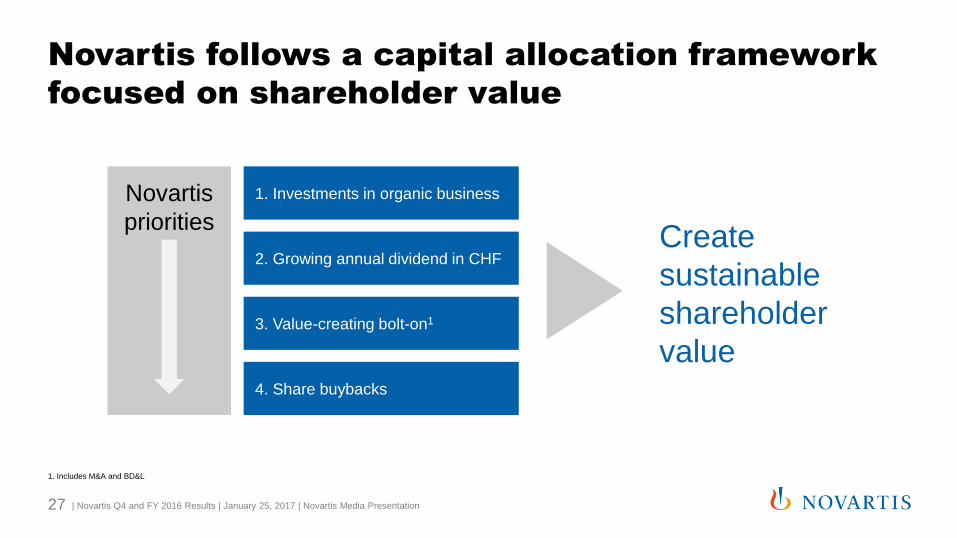

Novartis follows a capital allocation framework

focused on shareholder value

1. Investments in organic business

2. Growing annual dividend in CHF

3. Value-creating bolt-on1

4. Share buybacks

Create

sustainable

shareholder

value

Novartis

priorities

1. Includes M&A and BD&L

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 27

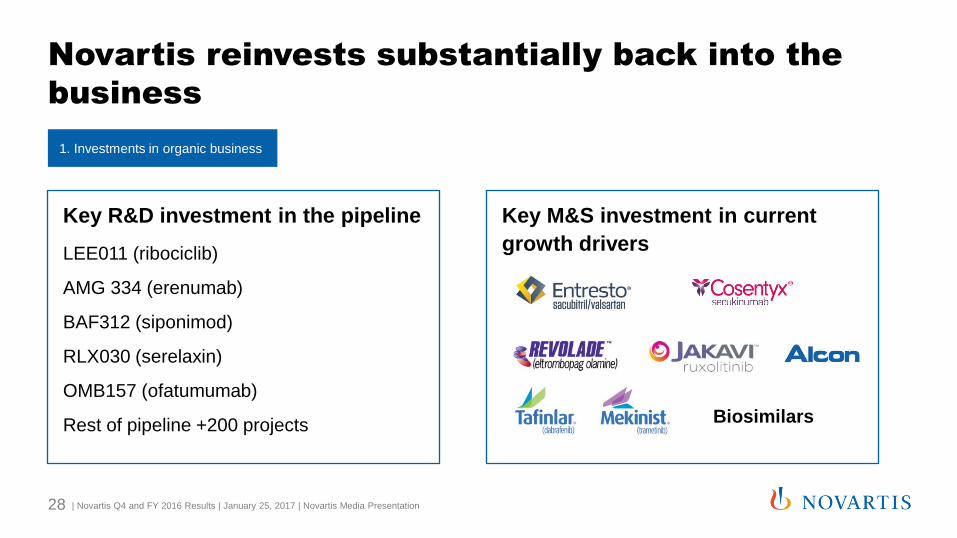

Novartis reinvests substantially back into the

business

Key M&S investment in current

growth drivers

Key R&D investment in the pipeline

LEE011 (ribociclib)

AMG 334 (erenumab)

BAF312 (siponimod)

RLX030 (serelaxin)

OMB157 (ofatumumab)

Rest of pipeline +200 projects

1. Investments in organic business

Biosimilars

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 28

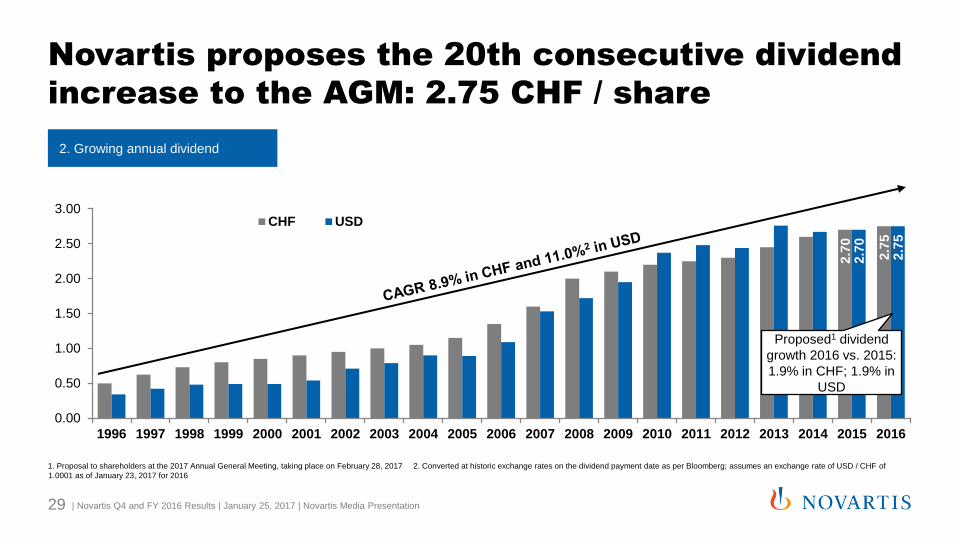

2.7

0

2.7

5

2.7

0

2.7

5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

CHF USD

Novartis proposes the 20th consecutive dividend

increase to the AGM: 2.75 CHF / share

1. Proposal to shareholders at the 2017 Annual General Meeting, taking place on February 28, 2017 2. Converted at historic exchange rates on the dividend payment date as per Bloomberg; assumes an exchange rate of USD / CHF of

1.0001 as of January 23, 2017 for 2016

Proposed1 dividend

growth 2016 vs. 2015:

1.9% in CHF; 1.9% in

USD

2. Growing annual dividend

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 29

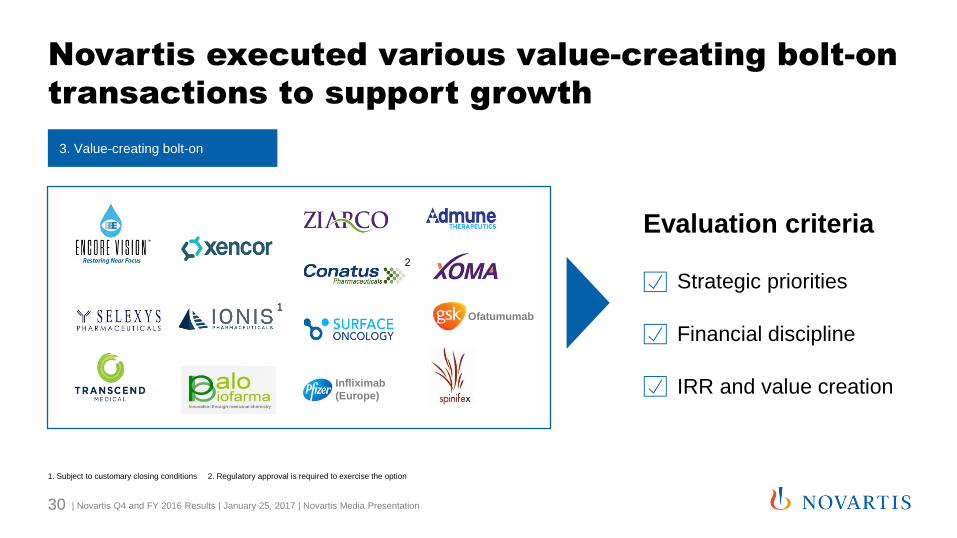

Novartis executed various value-creating bolt-on

transactions to support growth

1. Subject to customary closing conditions 2. Regulatory approval is required to exercise the option

Evaluation criteria

Strategic priorities

IRR and value creation

Financial discipline

3. Value-creating bolt-on

Infliximab

(Europe)

2

Ofatumumab 1

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 30

Initiating a share buyback of up to USD 5 bn in

2017 reinforcing confidence in growth prospects

• Initiating a share buyback1 of up to USD 5 billion, reinforcing confidence in growth

prospects

• Novartis aims to execute this buyback in 2017

• Novartis envisages to finance the buyback through new debt, actively using its

strong balance sheet

• Attractive funding rates reflecting historically low interest rates

1. Under the existing authority of the seventh share buyback program granted by the AGM in February 2016

4. Share buybacks

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 31

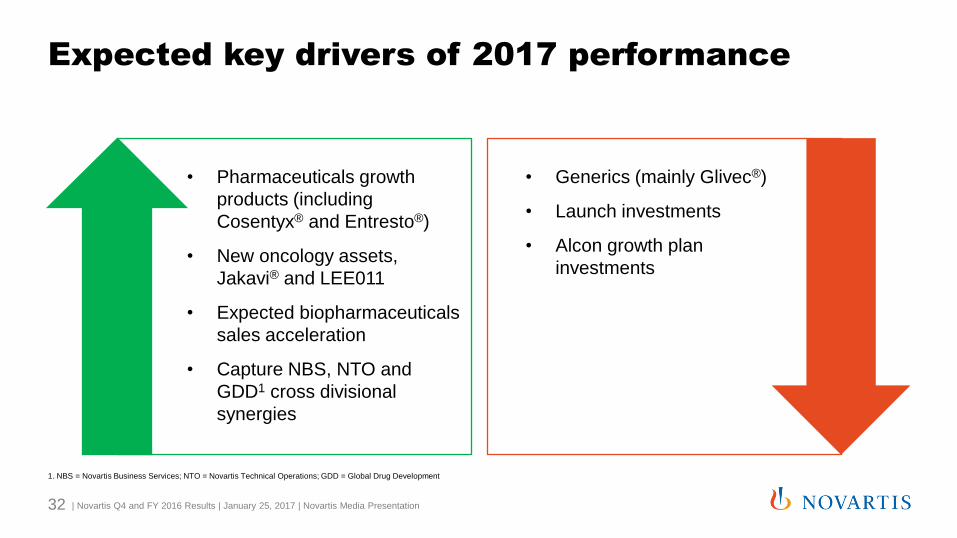

Expected key drivers of 2017 performance

1. NBS = Novartis Business Services; NTO = Novartis Technical Operations; GDD = Global Drug Development

• Pharmaceuticals growth

products (including

Cosentyx® and Entresto®)

• New oncology assets,

Jakavi® and LEE011

• Expected biopharmaceuticals

sales acceleration

• Capture NBS, NTO and

GDD1 cross divisional

synergies

• Generics (mainly Glivec®)

• Launch investments

• Alcon growth plan

investments

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 32

2017 Full Year Guidance

• In 2017, we expect continued genericization of Glivec® to impact results

• Group net sales expected to be broadly in line with PY

• IM Division broadly in line

• Sandoz low single digit growth

• Alcon broadly in line to low single digit growth

• Group core operating income expected to be broadly in line with PY to

low single digit decline

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 33

Barring unforeseen events (in cc)

1. Group review Joseph Jimenez, Chief Executive Officer

2. Financial review Harry Kirsch, Chief Financial Officer

3. R&D Jay Bradner, President NIBR & Vas Narasimhan, Global

Head Drug Development & CMO

4. Q&A All presenters

Agenda

34

A new era for R&D at Novartis

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 35

NIBR 2.0 - A Strategy for the Next Generation of Discovery

Innovate the New Science of

Therapeutics

Deliver Medicines First for

Those Who Need Them Most

Open our

Framework

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 36

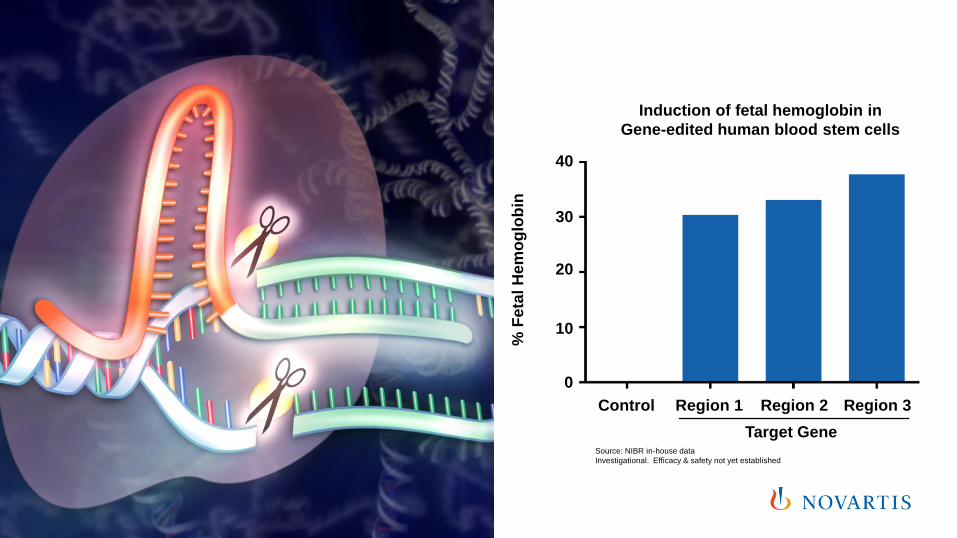

% F

eta

l H

em

og

lob

in

Induction of fetal hemoglobin in

Gene-edited human blood stem cells

0

10

20

30

40

Control

Target Gene

Region 2 Region 3 Region 1

Source: NIBR in-house data

Investigational. Efficacy & safety not yet established

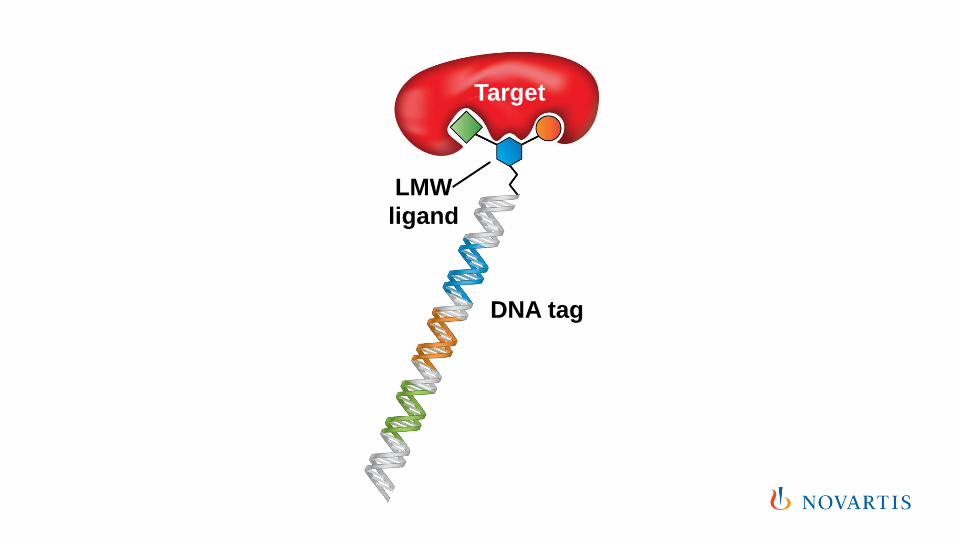

Target

LMW

ligand

DNA tag

Target

LMW

ligand

DNA tag

Target

LMW

ligand

DNA tag

Target

LMW

ligand

DNA tag

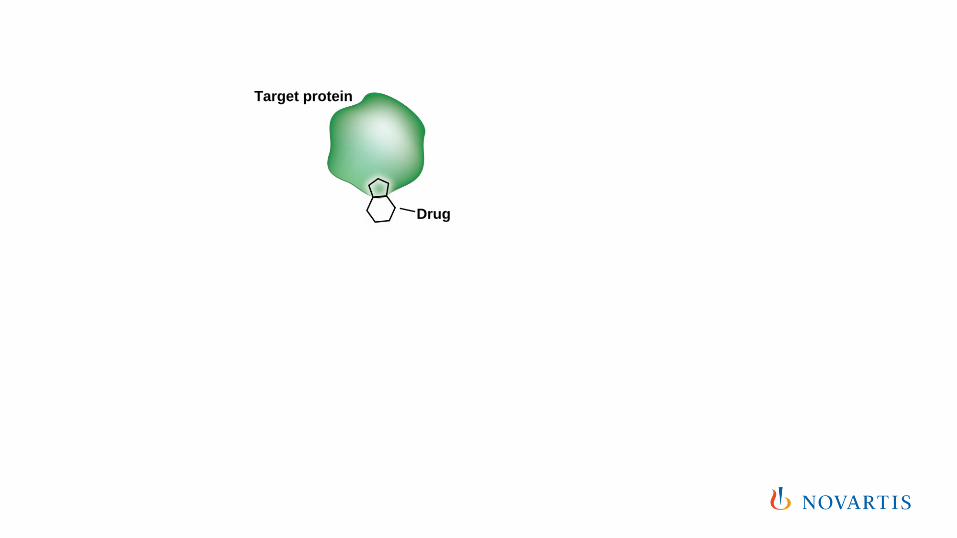

Target protein

Drug

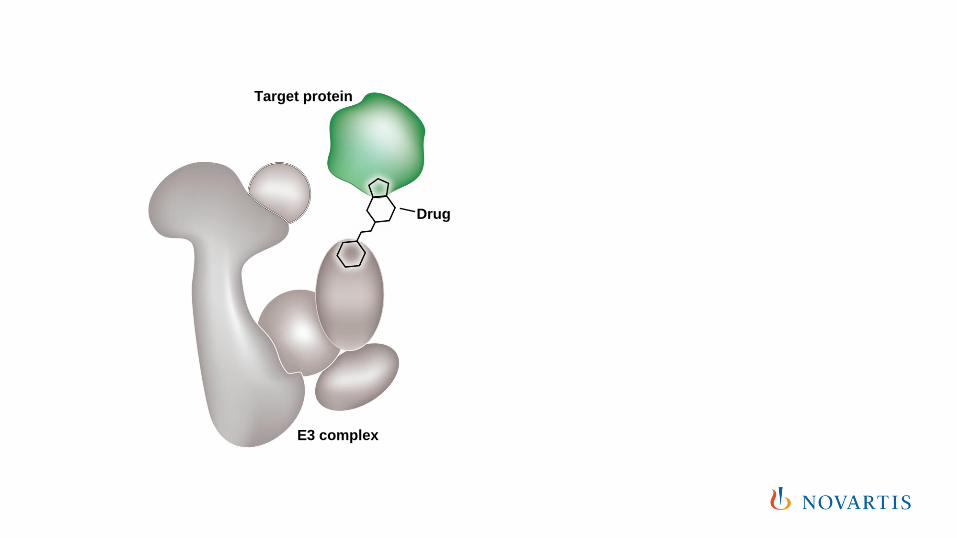

Target protein

E3 complex

Drug

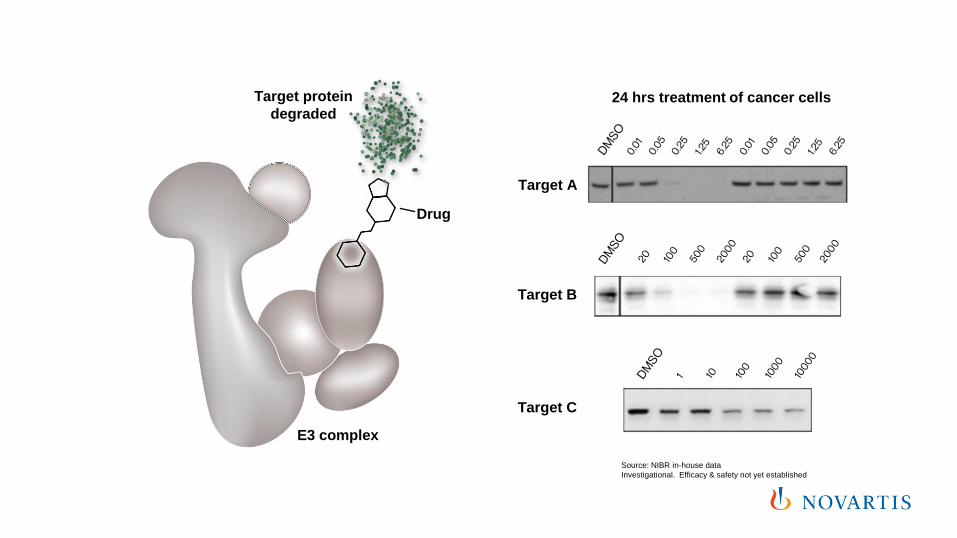

Target protein

degraded

E3 complex

Drug

Target A

24 hrs treatment of cancer cells

Target B

Target C

Source: NIBR in-house data

Investigational. Efficacy & safety not yet established

A relatively small number of patients currently

respond to immuno-oncology therapy options

Even among responders, a significant number

need to discontinue therapy due to adverse

events

Data emerging over the next 12-18 months

from Novartis and competitor trials will inform

the most impactful paths forward

We aim for a leadership position in oncology

by leveraging our broad immuno-oncology

and targeted therapy portfolios

Immuno-Oncology: Opportunities and Challenges

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 50

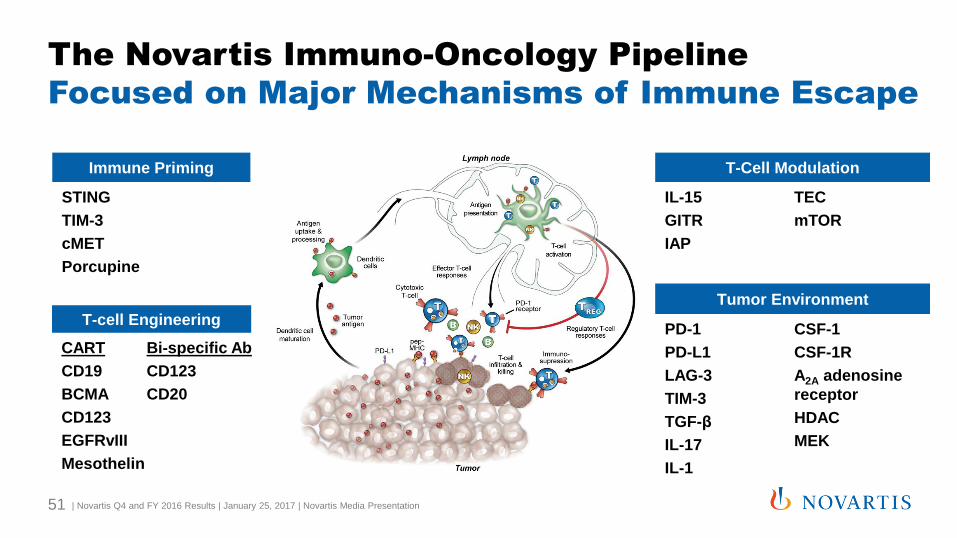

Immune Priming

STING

TIM-3

cMET

Porcupine

T-Cell Modulation

IL-15

GITR

IAP

TEC

mTOR

Tumor Environment

PD-1

PD-L1

LAG-3

TIM-3

TGF-β

IL-17

IL-1

CSF-1

CSF-1R

A2A adenosine

receptor

HDAC

MEK

T-cell Engineering

CART

CD19

BCMA

CD123

EGFRvIII

Mesothelin

Bi-specific Ab

CD123

CD20

The Novartis Immuno-Oncology Pipeline

Focused on Major Mechanisms of Immune Escape

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 51

Pediatric ALL filing on CTL019

expected in early 2017

DLBCL filing of CTL019 expected in H2

2017

Integration of the Cell & Gene Therapy

Unit into broader Novartis organization

Increased investment at NIBR in CART

manufacturing science

Cell-based Immunotherapy Anticipated to Reach

Regulatory Consideration in 2017

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 52

Strong pipeline focused on second

generation immuno-therapy

Rapidly progressing 18 checkpoint

and additional novel targets

20 exploratory immuno-oncology

studies expected by early 2017

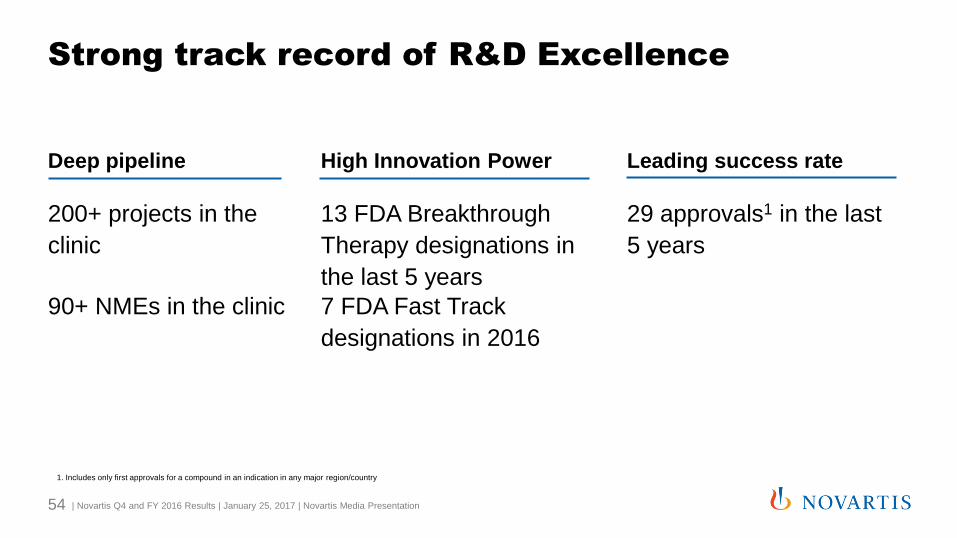

Strong track record of R&D Excellence

Deep pipeline

200+ projects in the

clinic

90+ NMEs in the clinic

High Innovation Power

7 FDA Fast Track

designations in 2016

13 FDA Breakthrough

Therapy designations in

the last 5 years

Leading success rate

29 approvals1 in the last

5 years

1. Includes only first approvals for a compound in an indication in any major region/country

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 54

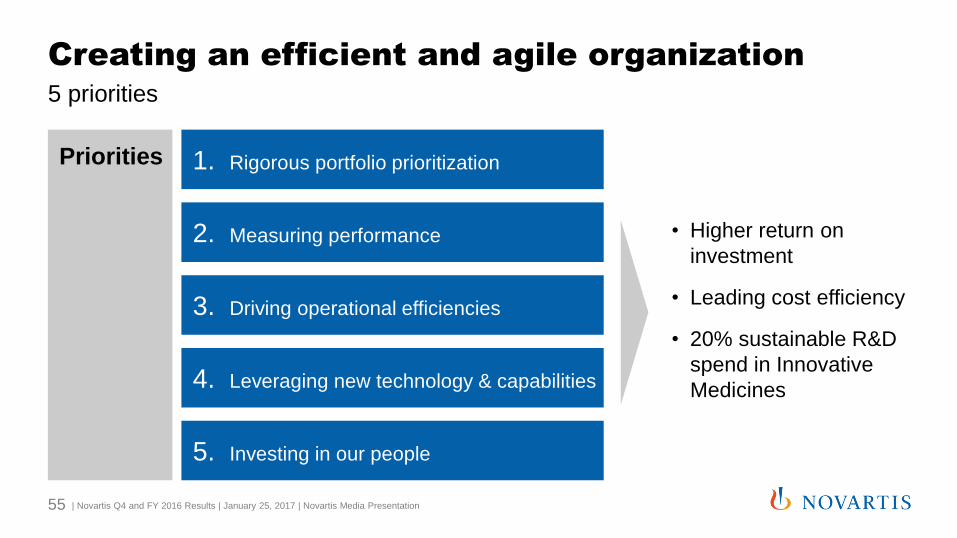

Creating an efficient and agile organization

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 55

1. Rigorous portfolio prioritization

2. Measuring performance

3. Driving operational efficiencies

4. Leveraging new technology & capabilities

5. Investing in our people

Priorities

5 priorities

• Higher return on

investment

• Leading cost efficiency

• 20% sustainable R&D

spend in Innovative

Medicines

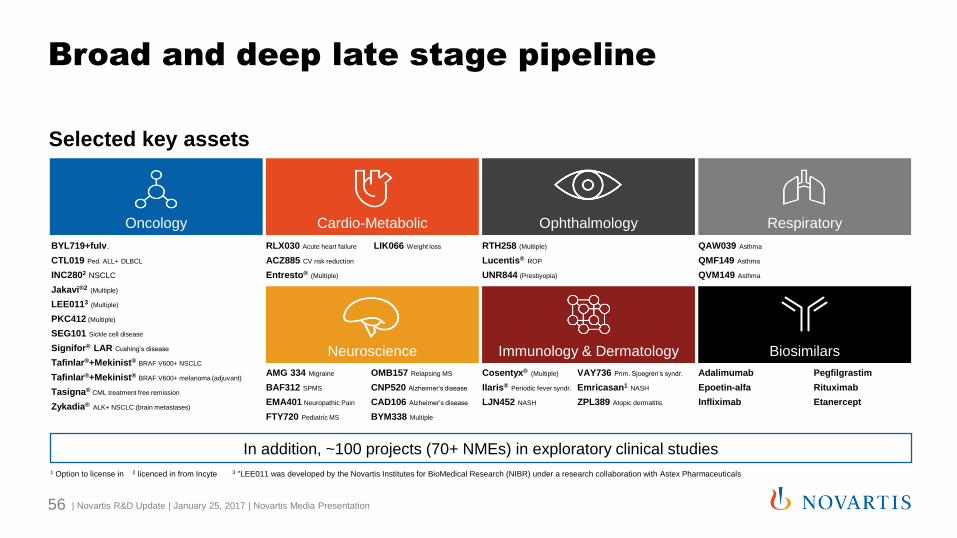

Oncology

Broad and deep late stage pipeline

| Novartis R&D Update | January 25, 2017 | Novartis Media Presentation 56

Cardio-Metabolic

BYL719+fulv.

CTL019 Ped. ALL+ DLBCL

INC2802 NSCLC

Jakavi®2 (Multiple)

LEE0113 (Multiple)

PKC412 (Multiple)

SEG101 Sickle cell disease

Signifor® LAR Cushing’s disease

Tafinlar®+Mekinist® BRAF V600+ NSCLC

Tafinlar®+Mekinist® BRAF V600+ melanoma (adjuvant)

Tasigna® CML treatment free remission

Zykadia® ALK+ NSCLC (brain metastases)

Ophthalmology

RTH258 (Multiple)

Lucentis® ROP

UNR844 (Presbyopia)

Respiratory

QAW039 Asthma

QMF149 Asthma

QVM149 Asthma

Biosimilars Neuroscience Immunology & Dermatology

Adalimumab

Epoetin-alfa

Infliximab

Pegfilgrastim

Rituximab

Etanercept

AMG 334 Migraine

BAF312 SPMS

EMA401 Neuropathic Pain

FTY720 Pediatric MS

OMB157 Relapsing MS

CNP520 Alzheimer’s disease

CAD106 Alzheimer’s disease

BYM338 Multiple

Cosentyx® (Multiple)

Ilaris® Periodic fever syndr.

LJN452 NASH

VAY736 Prim. Sjoegren’s syndr.

Emricasan1 NASH

ZPL389 Atopic dermatitis

RLX030 Acute heart failure

ACZ885 CV risk reduction

Entresto® (Multiple)

LIK066 Weight loss

In addition, ~100 projects (70+ NMEs) in exploratory clinical studies

1 Option to license in 2 licenced in from Incyte 3 "LEE011 was developed by the Novartis Institutes for BioMedical Research (NIBR) under a research collaboration with Astex Pharmaceuticals

Selected key assets

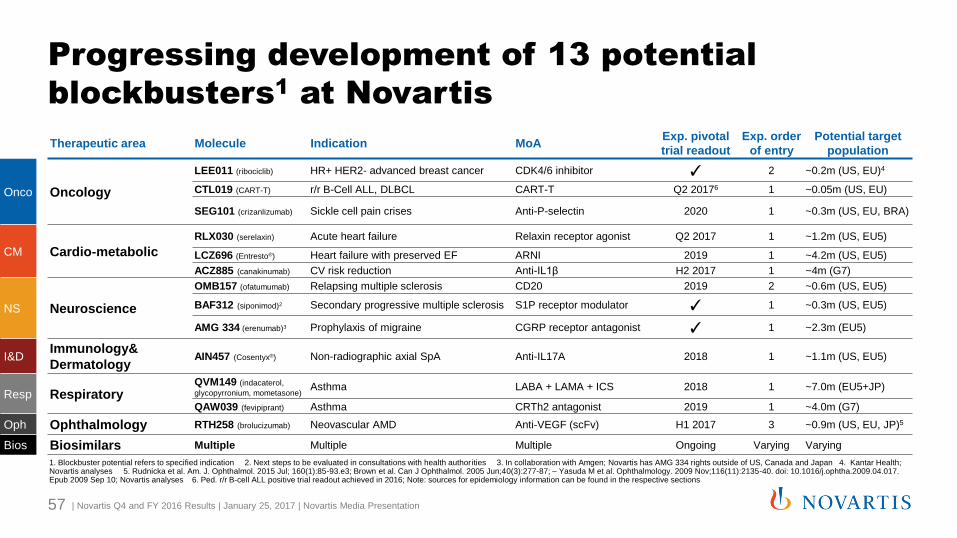

Progressing development of 13 potential

blockbusters1 at Novartis

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 57

Therapeutic area Molecule Indication MoA Exp. pivotal

trial readout

Exp. order

of entry

Potential target

population

Onco Oncology

LEE011 (ribociclib) HR+ HER2- advanced breast cancer CDK4/6 inhibitor ✓ 2 ~0.2m (US, EU)4

CTL019 (CART-T) r/r B-Cell ALL, DLBCL CART-T Q2 20176 1 ~0.05m (US, EU)

SEG101 (crizanlizumab) Sickle cell pain crises Anti-P-selectin 2020 1 ~0.3m (US, EU, BRA)

CM Cardio-metabolic

RLX030 (serelaxin) Acute heart failure Relaxin receptor agonist Q2 2017 1 ~1.2m (US, EU5)

LCZ696 (Entresto®) Heart failure with preserved EF ARNI 2019 1 ~4.2m (US, EU5)

ACZ885 (canakinumab) CV risk reduction Anti-IL1β H2 2017 1 ~4m (G7)

NS Neuroscience

OMB157 (ofatumumab) Relapsing multiple sclerosis CD20 2019 2 ~0.6m (US, EU5)

BAF312 (siponimod)2 Secondary progressive multiple sclerosis S1P receptor modulator ✓ 1 ~0.3m (US, EU5)

AMG 334 (erenumab)3 Prophylaxis of migraine CGRP receptor antagonist ✓ 1 ~2.3m (EU5)

I&D Immunology&

Dermatology AIN457 (Cosentyx®) Non-radiographic axial SpA Anti-IL17A 2018 1 ~1.1m (US, EU5)

Resp Respiratory QVM149 (indacaterol,

glycopyrronium, mometasone) Asthma LABA + LAMA + ICS 2018 1 ~7.0m (EU5+JP)

QAW039 (fevipiprant) Asthma CRTh2 antagonist 2019 1 ~4.0m (G7)

Oph Ophthalmology RTH258 (brolucizumab) Neovascular AMD Anti-VEGF (scFv) H1 2017 3 ~0.9m (US, EU, JP)5

Bios Biosimilars Multiple Multiple Multiple Ongoing Varying Varying

1. Blockbuster potential refers to specified indication 2. Next steps to be evaluated in consultations with health authorities 3. In collaboration with Amgen; Novartis has AMG 334 rights outside of US, Canada and Japan 4. Kantar Health; Novartis analyses 5. Rudnicka et al. Am. J. Ophthalmol. 2015 Jul; 160(1):85-93.e3; Brown et al. Can J Ophthalmol. 2005 Jun;40(3):277-87; – Yasuda M et al. Ophthalmology. 2009 Nov;116(11):2135-40. doi: 10.1016/j.ophtha.2009.04.017. Epub 2009 Sep 10; Novartis analyses 6. Ped. r/r B-cell ALL positive trial readout achieved in 2016; Note: sources for epidemiology information can be found in the respective sections

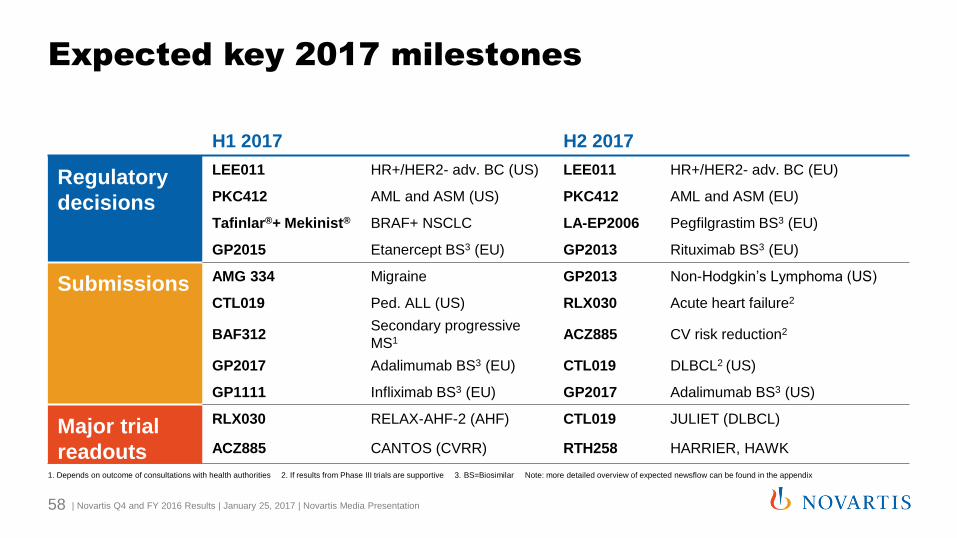

Expected key 2017 milestones

1. Depends on outcome of consultations with health authorities 2. If results from Phase III trials are supportive 3. BS=Biosimilar Note: more detailed overview of expected newsflow can be found in the appendix

H1 2017 H2 2017

Regulatory

decisions

LEE011 HR+/HER2- adv. BC (US) LEE011 HR+/HER2- adv. BC (EU)

PKC412 AML and ASM (US) PKC412 AML and ASM (EU)

Tafinlar®+ Mekinist® BRAF+ NSCLC LA-EP2006 Pegfilgrastim BS3 (EU)

GP2015 Etanercept BS3 (EU) GP2013 Rituximab BS3 (EU)

Submissions AMG 334 Migraine GP2013 Non-Hodgkin’s Lymphoma (US)

CTL019 Ped. ALL (US) RLX030 Acute heart failure2

BAF312 Secondary progressive

MS1 ACZ885 CV risk reduction2

GP2017 Adalimumab BS3 (EU) CTL019 DLBCL2 (US)

GP1111 Infliximab BS3 (EU) GP2017 Adalimumab BS3 (US)

Major trial

readouts

RLX030 RELAX-AHF-2 (AHF) CTL019 JULIET (DLBCL)

ACZ885 CANTOS (CVRR) RTH258 HARRIER, HAWK

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 58

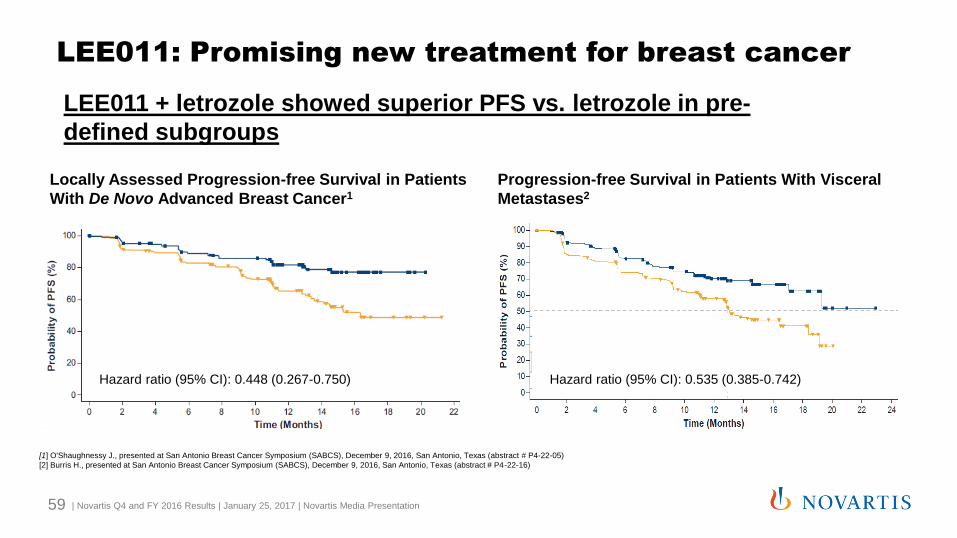

Locally Assessed Progression-free Survival in Patients

With De Novo Advanced Breast Cancer1

Progression-free Survival in Patients With Visceral

Metastases2

LEE011: Promising new treatment for breast cancer

[1] O'Shaughnessy J., presented at San Antonio Breast Cancer Symposium (SABCS), December 9, 2016, San Antonio, Texas (abstract # P4-22-05)

[2] Burris H., presented at San Antonio Breast Cancer Symposium (SABCS), December 9, 2016, San Antonio, Texas (abstract # P4-22-16)

Hazard ratio (95% CI): 0.448 (0.267-0.750) Hazard ratio (95% CI): 0.535 (0.385-0.742)

LEE011 + letrozole showed superior PFS vs. letrozole in pre-

defined subgroups

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 59

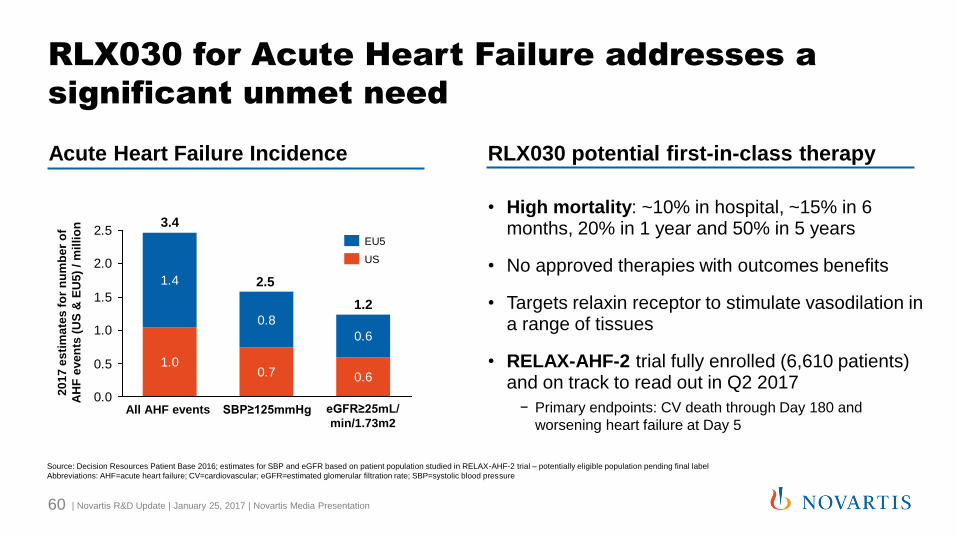

RLX030 for Acute Heart Failure addresses a

significant unmet need

| Novartis R&D Update | January 25, 2017 | Novartis Media Presentation 60

Acute Heart Failure Incidence

• High mortality: ~10% in hospital, ~15% in 6 months, 20% in 1 year and 50% in 5 years

• No approved therapies with outcomes benefits

• Targets relaxin receptor to stimulate vasodilation in a range of tissues

• RELAX-AHF-2 trial fully enrolled (6,610 patients) and on track to read out in Q2 2017

− Primary endpoints: CV death through Day 180 and

worsening heart failure at Day 5

20

17

es

tim

ate

s f

or

nu

mb

er

of

AH

F e

ve

nts

(U

S &

EU

5)

/ m

illi

on

1.00.7 0.6

1.4

0.8

0.6

0.0

0.5

1.0

1.5

2.0

2.5

1.2

SBP≥125mmHg All AHF events eGFR≥25mL/

min/1.73m2

EU5

US

Source: Decision Resources Patient Base 2016; estimates for SBP and eGFR based on patient population studied in RELAX-AHF-2 trial – potentially eligible population pending final label

Abbreviations: AHF=acute heart failure; CV=cardiovascular; eGFR=estimated glomerular filtration rate; SBP=systolic blood pressure

RLX030 potential first-in-class therapy

2.5

3.4

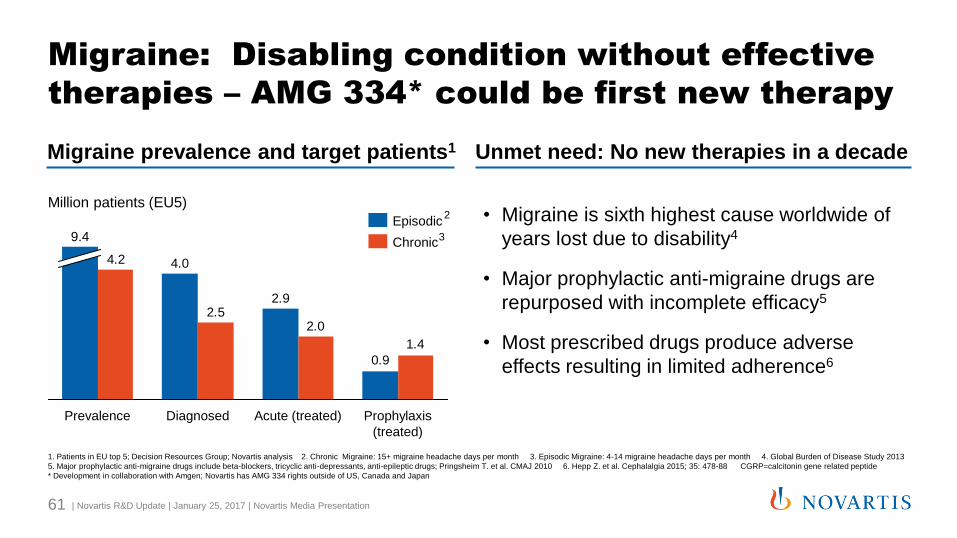

Migraine: Disabling condition without effective

therapies – AMG 334* could be first new therapy

| Novartis R&D Update | January 25, 2017 | Novartis Media Presentation 61

• Migraine is sixth highest cause worldwide of

years lost due to disability4

• Major prophylactic anti-migraine drugs are

repurposed with incomplete efficacy5

• Most prescribed drugs produce adverse

effects resulting in limited adherence6

1. Patients in EU top 5; Decision Resources Group; Novartis analysis 2. Chronic Migraine: 15+ migraine headache days per month 3. Episodic Migraine: 4-14 migraine headache days per month 4. Global Burden of Disease Study 2013

5. Major prophylactic anti-migraine drugs include beta-blockers, tricyclic anti-depressants, anti-epileptic drugs; Pringsheim T. et al. CMAJ 2010 6. Hepp Z. et al. Cephalalgia 2015; 35: 478-88 CGRP=calcitonin gene related peptide

* Development in collaboration with Amgen; Novartis has AMG 334 rights outside of US, Canada and Japan

Migraine prevalence and target patients1 Unmet need: No new therapies in a decade

2

3

Million patients (EU5)

0.9

2.9

4.0

1.4

2.02.5

4.2

Prevalence Diagnosed Acute (treated) Prophylaxis

(treated)

9.4 Chronic

Episodic

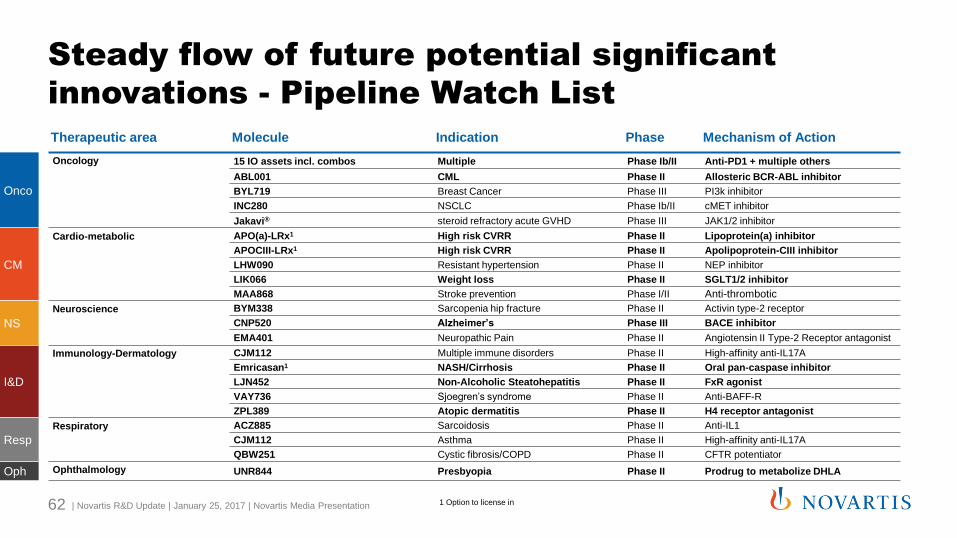

Steady flow of future potential significant

innovations - Pipeline Watch List

| Novartis R&D Update | January 25, 2017 | Novartis Media Presentation 62

Therapeutic area Molecule Indication Phase Mechanism of Action

Onco

Oncology 15 IO assets incl. combos Multiple Phase Ib/II Anti-PD1 + multiple others

ABL001 CML Phase II Allosteric BCR-ABL inhibitor

BYL719 Breast Cancer Phase III PI3k inhibitor

INC280 NSCLC Phase Ib/II cMET inhibitor

Jakavi® steroid refractory acute GVHD Phase III JAK1/2 inhibitor

CM

Cardio-metabolic APO(a)-LRx1 High risk CVRR Phase II Lipoprotein(a) inhibitor

APOCIII-LRx1 High risk CVRR Phase II Apolipoprotein-CIII inhibitor

LHW090 Resistant hypertension Phase II NEP inhibitor

LIK066 Weight loss Phase II SGLT1/2 inhibitor

MAA868 Stroke prevention Phase I/II Anti-thrombotic

NS

Neuroscience BYM338 Sarcopenia hip fracture Phase II Activin type-2 receptor

CNP520 Alzheimer’s Phase III BACE inhibitor

EMA401 Neuropathic Pain Phase II Angiotensin II Type-2 Receptor antagonist

I&D

Immunology-Dermatology CJM112 Multiple immune disorders Phase II High-affinity anti-IL17A

Emricasan1 NASH/Cirrhosis Phase II Oral pan-caspase inhibitor

LJN452 Non-Alcoholic Steatohepatitis Phase II FxR agonist

VAY736 Sjoegren’s syndrome Phase II Anti-BAFF-R

ZPL389 Atopic dermatitis Phase II H4 receptor antagonist

Resp

Respiratory ACZ885 Sarcoidosis Phase II Anti-IL1

CJM112 Asthma Phase II High-affinity anti-IL17A

QBW251 Cystic fibrosis/COPD Phase II CFTR potentiator

Oph Ophthalmology UNR844 Presbyopia Phase II Prodrug to metabolize DHLA

1 Option to license in

Pioneering breakthrough approaches in multiple

disease areas

Obesity Liver Disease Alzheimer’s

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 63

1. Secondary prevention of cardiovascular events

2. Tuberous sclerosis complex

3. Diffuse large B-cell lymphoma

4. Multiple sclerosis

5. Severe aplastic anemia

6. Chronic myeloid leukemia

7. Non-small cell lung cancer

8. Neovascular age-related macular degeneration

9. Non-Hodgkin’s lymphoma

10. Non-radiographic axial spondyloarthritis

11. Multi-drug resistant

12. Breast cancer

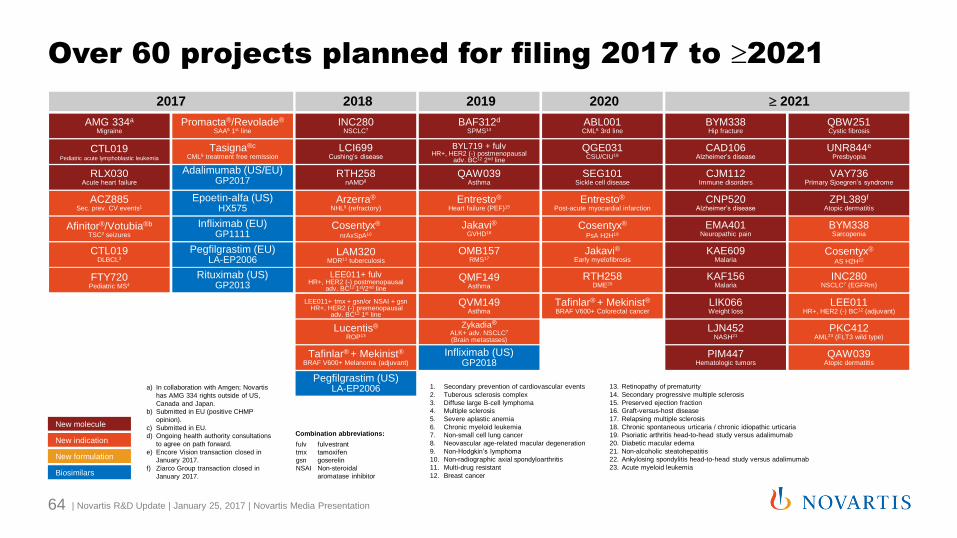

Over 60 projects planned for filing 2017 to 2021

| Novartis R&D Update | January 25, 2017 | Novartis Media Presentation 64

a) In collaboration with Amgen; Novartis

has AMG 334 rights outside of US,

Canada and Japan.

b) Submitted in EU (positive CHMP

opinion).

c) Submitted in EU.

d) Ongoing health authority consultations

to agree on path forward.

e) Encore Vision transaction closed in

January 2017.

f) Ziarco Group transaction closed in

January 2017.

New molecule

New indication

New formulation

Biosimilars

13. Retinopathy of prematurity

14. Secondary progressive multiple sclerosis

15. Preserved ejection fraction

16. Graft-versus-host disease

17. Relapsing multiple sclerosis

18. Chronic spontaneous urticaria / chronic idiopathic urticaria

19. Psoriatic arthritis head-to-head study versus adalimumab

20. Diabetic macular edema

21. Non-alcoholic steatohepatitis

22. Ankylosing spondylitis head-to-head study versus adalimumab

23. Acute myeloid leukemia

Combination abbreviations:

fulv fulvestrant

tmx tamoxifen

gsn goserelin

NSAI Non-steroidal

aromatase inhibitor

Pegfilgrastim (EU) LA-EP2006

KAE609 Malaria

CAD106 Alzheimer’s disease

LIK066 Weight loss

CJM112 Immune disorders

ABL001 CML6 3rd line

EMA401

Neuropathic pain

CNP520 Alzheimer’s disease

BYM338 Hip fracture

QGE031 CSU/CIU18

BYM338 Sarcopenia

PIM447 Hematologic tumors

VAY736 Primary Sjoegren’s syndrome

Entresto®

Post-acute myocardial infarction

QAW039 Atopic dermatitis

Tafinlar® + Mekinist®

BRAF V600+ Colorectal cancer

RTH258

DME20

Jakavi®

Early myelofibrosis

Afinitor®/Votubia®b TSC2 seizures

CTL019 Pediatric acute lymphoblastic leukemia

Tasigna®c CML6 treatment free remission

LCI699 Cushing’s disease

BAF312d SPMS14

QAW039 Asthma

Entresto®

Heart failure (PEF)15

Lucentis®

ROP13

INC280 NSCLC7

KAF156 Malaria

QVM149 Asthma

QMF149 Asthma

LEE011+ fulv HR+, HER2 (-) postmenopausal

adv. BC12 1st/2nd line

LEE011+ tmx + gsn/or NSAI + gsn HR+, HER2 (-) premenopausal

adv. BC12 1st line

Zykadia® ALK+ adv. NSCLC7

(Brain metastases)

Cosentyx®

nrAxSpA10

BYL719 + fulv HR+, HER2 (-) postmenopausal

adv. BC12 2nd line

OMB157

RMS17

ACZ885 Sec. prev. CV events1

RLX030 Acute heart failure

CTL019 DLBCL3

Arzerra®

NHL9 (refractory)

Tafinlar® + Mekinist® BRAF V600+ Melanoma (adjuvant)

RTH258 nAMD8

2021 2019 2018 2017 2020

Jakavi®

GVHD16

FTY720 Pediatric MS4

LJN452 NASH21

Adalimumab (US/EU) GP2017

Epoetin-alfa (US) HX575

Infliximab (EU) GP1111

Rituximab (US) GP2013

QBW251 Cystic fibrosis

AMG 334a

Migraine

LEE011 HR+, HER2 (-) BC12 (adjuvant)

Cosentyx®

PsA H2H19

Cosentyx®

AS H2H22

LAM320 MDR11 tuberculosis

Promacta®/Revolade® SAA5 1st line

ZPL389f

Atopic dermatitis

PKC412

AML23 (FLT3 wild type)

UNR844e

Presbyopia

SEG101 Sickle cell disease

Pegfilgrastim (US) LA-EP2006

Infliximab (US) GP2018

INC280 NSCLC7 (EGFRm)

We are poised to deliver the next wave of

breakthrough medicines for patients

Group-wide portfolio management World-class talent Cutting-edge Technology

No

vart

is s

tren

gth

Unmet need

| Novartis Q4 and FY 2016 Results | January 25, 2017 | Novartis Media Presentation 65

1. Group review Joseph Jimenez, Chief Executive Officer

2. Financial review Harry Kirsch, Chief Financial Officer

3. R&D Jay Bradner, President NIBR & Vas Narasimhan, Global Head

Drug Development & CMO

4. Q&A All presenters

Agenda

66

Questions