Notes - Le · PDF fileWell services Rigs Rotating equipment Subsea services ......

48

2015 Strategy & Outlook Focus on 4 key domains September 2015

Transcript of Notes - Le · PDF fileWell services Rigs Rotating equipment Subsea services ......

2015 Strategy & Outlook

Notes Focus on 4 key domains

September 2015

UPSTREAM Focus on cost discipline and

operational excellence

Arnaud BREUILLAC President, Exploration & Production

2015 Strategy & Outlook 3

Safety as a cornerstone of our strategy

Improving Upstream HSE performance

Reducing flaring** Mm3/d

Achieved target of 50% reduction on flaring Safety and operational efficiency go together

Reducing TRIR*

while increasing activity levels

* TRIR: Total Recordable Injury Rate ** Operated assets, excl. start-ups

0

1

2

0

100

200

300

2009 2014

200

1.3

1.9

Million

man-hours

TRIR

0

5

10

15

20

-50%

2005 2014

15

2015 Strategy & Outlook 4

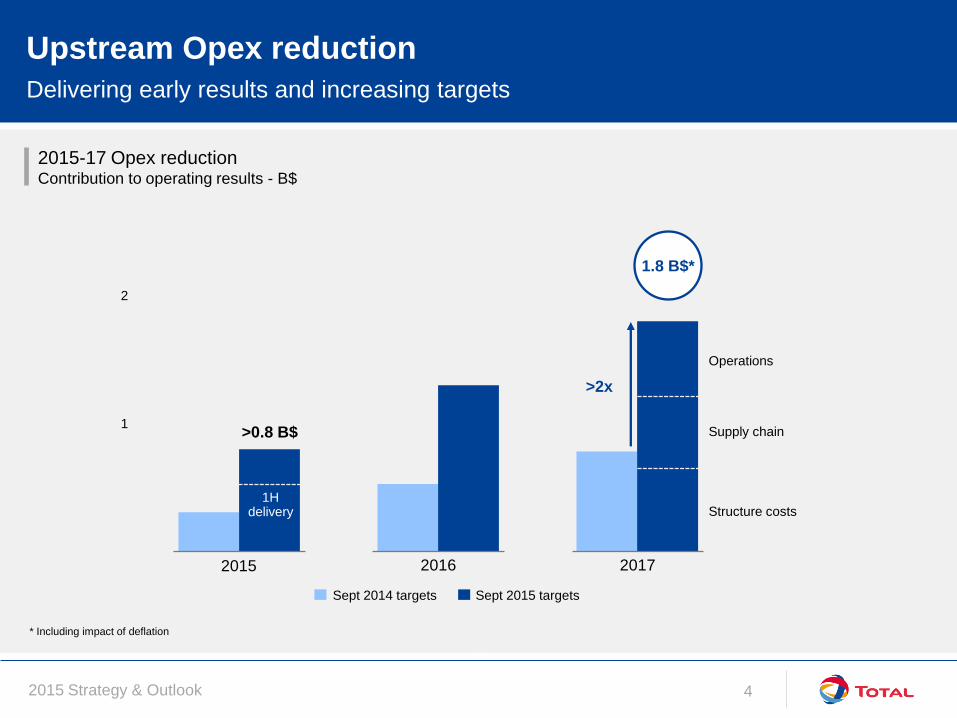

Upstream Opex reduction

Delivering early results and increasing targets

2015-17 Opex reduction Contribution to operating results - B$

Sept 2014 targets Sept 2015 targets

1.8 B$*

0

1

2

2015 2016 2017

1H delivery

Operations

Supply chain

Structure costs

>0.8 B$

>2x

* Including impact of deflation

2015 Strategy & Outlook 5

Systematic internal benchmarking

Measuring performance across all categories and assets

Identifying performance gaps

Encouraging best practice exchanges

between affiliates

Increasing cost awareness of all staff

Implementing performance-based

incentives

Maintenance benchmark Deep offshore - $/MCI*

Logistics benchmark

Helicopters - $/pax/h

Middle 50% Major assets

IT benchmark Workstations - $/unit

Top quartile Bottom quartile

* Maintenance complexity index based on number, type and complexity of equipment

Lower cost Higher cost

Lower cost Higher cost

Lower cost Higher cost

2015 Strategy & Outlook 6

Operations: revisiting operating models and logistics

Focusing on improving efficiency

Executing logistics action plan Nigeria - 100% operated savings - M$

Increasing passenger transport by sea

Reducing supply vessels

Improved utilization and fuel efficiency

Benefiting from synergies between FPSOs

Preparing onshore, implementing offshore

Developing multi-competence operators

New operating model Angola Block 17 - headcount

0

20

40

Fewer

vessels

Fuel

consumption

Synergies

2015 2017 0

500

-30%

2014 2017

Campaign teams

& smart rooms

Girassol

Dalia

Pazflor

CLOV

2015 Strategy & Outlook 7

Supply chain: reducing costs through contract renegotiations

Already achieving savings of up to 30%

Negotiated rate and fee reduction examples

Marine logistics

Seismic acquisition

Well services

Rigs

Rotating equipment

Subsea services

Tubulars

Operations & maintenance

Engineering

-40% -30% -20% -10% 0%

2015 Strategy & Outlook 8

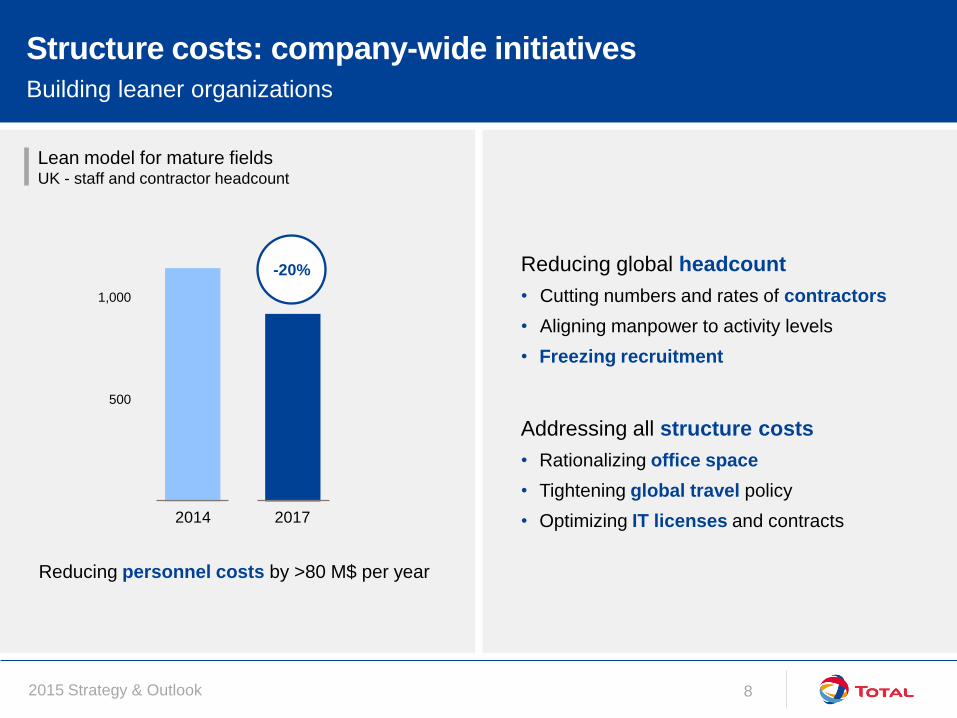

Reducing global headcount

• Cutting numbers and rates of contractors

• Aligning manpower to activity levels

• Freezing recruitment

Addressing all structure costs

• Rationalizing office space

• Tightening global travel policy

• Optimizing IT licenses and contracts

Lean model for mature fields UK - staff and contractor headcount

Reducing personnel costs by >80 M$ per year

-20%

0

500

1,000

2014 2017

Structure costs: company-wide initiatives

Building leaner organizations

2015 Strategy & Outlook 9

Tackling drilling costs

Optimizing rig fleet and drilling operations

Improving well execution Dalia, Angola - drilling time per well

Simplifying and standardizing well design Adapting rig count to activity levels

Terminating and renegotiating rig contracts

Managing rig count Operated rigs

0

10

20

30

40

50

60

Committed

Actions since

Jan 2015

0

20

40

60

80

100

120

100%

-35%

Lower NPT*

Rig sequence

Optimizing operations

2015 2017 2014 average

2015 2014

25

50

* NPT: non-productive time

2015 Strategy & Outlook 10

Production delivery: increasing operational efficiency

Launching dedicated program to improve performance

Remote monitoring of rotating equipment

Reducing unplanned production losses

Optimizing preventative maintenance

+75 kboe/d production in 2017

Production efficiency Operated assets - %

85%

90%

95%

2016 2014 2017

>3%

2015 Strategy & Outlook 11

Project delivery: excellence in deep offshore developments

Delivering the next generation of giant, competitive projects

Nigeria: Egina

• Adding 200 kb/d

• 36% progress, starting up in 2018

• Robust PSC terms driving resilience

Congo: Moho Nord & Ph 1b

• Adding 140 kb/d by 2016

• 49% overall progress, Ph 1b start-up in 2015

• Negotiated new fiscal terms ahead of FID

Leading deep offshore operator among peers Operated production* - Mboe/d

Deep offshore: strong cash flows 2019 contribution from deep offshore, at 60 $/b

0.0

0.8

Total XoM BP CVX Shell

* Wood Mackenzie, 2015 deep offshore FPSOs; peers: BP, Chevron, ExxonMobil, Shell

1/3 of Upstream

cash flow

15% of

production

2015 Strategy & Outlook 12

Project delivery: lessons learned from Laggan experience

Focused on delivering start-up late-2015

Offshore executed on time

and on budget

• Wells ready for start-up

• Subsea systems and pipelines

ready since 2014

Lessons from specific onshore

challenges

• Better anticipation of site-specific issues

• Better control of contractors/supply chain

• Adapt standards for onshore environment

An innovative subsea to shore project Total 60%, operator

Shetland onshore gas plant Hot work complete, commissioning ongoing

2015 Strategy & Outlook 13

Building a more resilient and profitable Upstream

Global cost reduction program targeting sustainable change

Back to basics

• Investing with discipline

through “good enough” design

• Revising operating models

and increasing efficiency

Changing culture sustainably

• Imperative to reduce costs at all levels

• Systematic cost benchmarking

linked to compensation

• Focusing on value creation

Reducing Opex per barrel $/boe

7 $/b

0

10

2017 2015 2014

EXPLORATION Revised strategy and organization

Kevin MCLACHLAN SVP Exploration

2015 Strategy & Outlook 15

Strong acreage position with opportunities

Maximizing potential from a large and diversified portfolio

Acreage for Total and peers* Net thousands km2

* Peers: BP, Chevron, Conoco, ENI, ExxonMobil, Shell, Statoil. Source IHS, Feb 2015, excl. USA and Canada onshore

0

500

STATOIL XOM CVX COP ENI TOTAL BP RDS

Rifts and grabens

Carbonates

Deltas

Abrupt margins

Unconventional Foothills

2015 Strategy & Outlook 16

High-graded exploration potential

>3 Bboe from 150 top ranked prospects

Global ranking and selectivity based on

risk, resource and value creation

Priority on high-impact wells

Improved process for prospect

assessment

Maintaining ~3 Bboe* of high-graded

exploration potential

High-graded conventional exploration potential

by play thematics and regions*

* Risked mean net resources

Foothills

Deltas

Abrupt

margins

Pre-salt

carbonates

Rifts and

grabens

Africa

Americas

Asia Pacific

Europe

Middle East

North Africa

2015 Strategy & Outlook 17

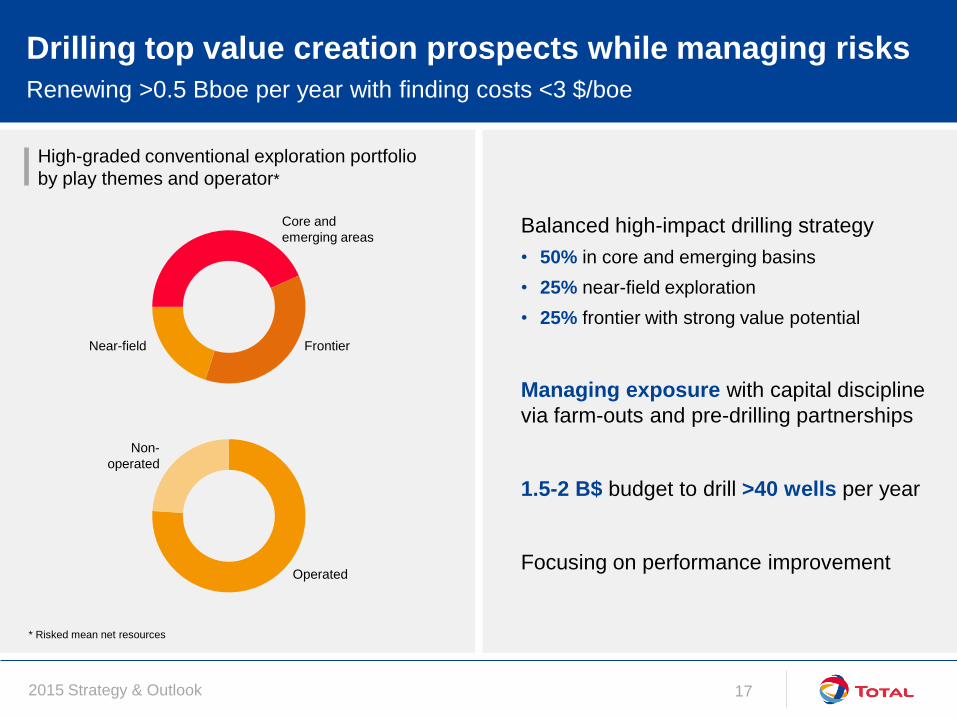

Drilling top value creation prospects while managing risks

Renewing >0.5 Bboe per year with finding costs <3 $/boe

Balanced high-impact drilling strategy

• 50% in core and emerging basins

• 25% near-field exploration

• 25% frontier with strong value potential

Managing exposure with capital discipline

via farm-outs and pre-drilling partnerships

1.5-2 B$ budget to drill >40 wells per year

Focusing on performance improvement

High-graded conventional exploration portfolio

by play themes and operator*

* Risked mean net resources

Core and

emerging areas

Near-field Frontier

Operated

Non-

operated

2015 Strategy & Outlook 18

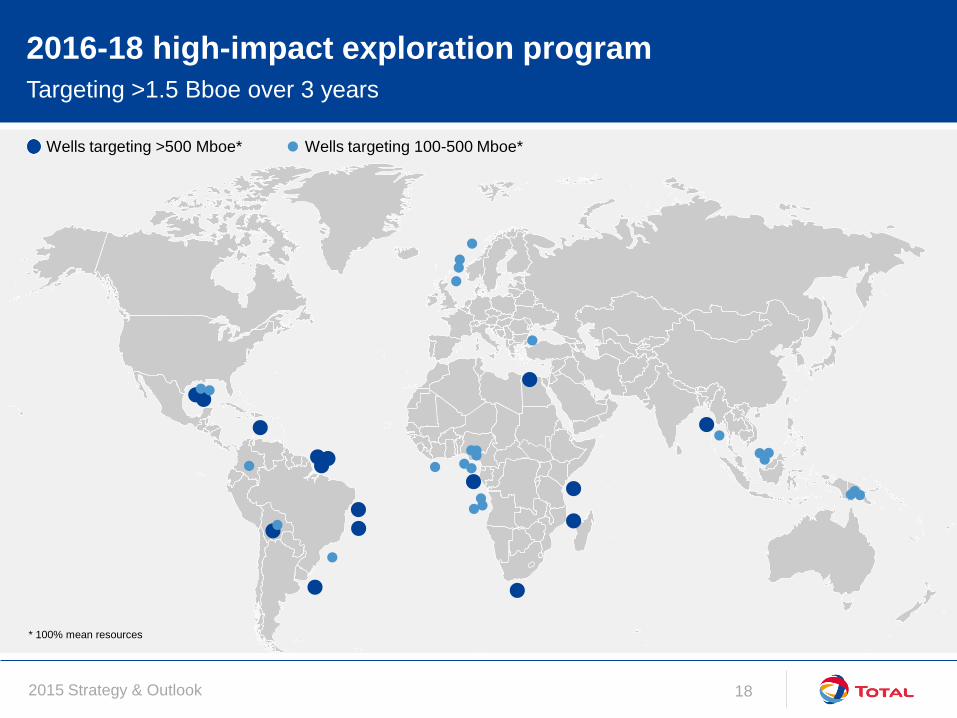

2016-18 high-impact exploration program

Targeting >1.5 Bboe over 3 years

* 100% mean resources

Wells targeting >500 Mboe* Wells targeting 100-500 Mboe*

2015 Strategy & Outlook 19

Focusing on core and emerging areas

US Gulf of Mexico, proving a new core area with North Platte discovery

North Platte lower tertiary discovery

• Total 40%

• >400 Mboe contingent and prospective

resources*

• North Platte 3 appraisal well ongoing

Goodfellow exploration

• Total 27.5%

• >400 Mboe prospective resources

• Exploration well in 2016

Other high value prospects to follow

236 blocks in Cobalt alliance Key prospects Discoveries

Fraser

Lewis Updip

Yeti

Rum

Ramsey

South

Platte

Williams Fork

North

Platte

Goodfellow

Baffin Bay

Houston

* Operator estimate

2015 Strategy & Outlook 20

Near-field exploration

Papua New Guinea, pursuing new prospects while appraising Elk-Antelope discovery

Total 40.1%, operator on PRL15

High potential play emerging in

onshore foothills environment

Proven play with significant potential

• Elk-Antelope discovery

• Antelope South well in 2016

• Further prospectivity under maturation for

future exploration drilling

2D PRL 15 composite seismic section

NNW SSE

Antelope Field Antelope South-1

Fields Prospects

PNG

Antelope

Elk

Antelope

South-1

2015 Strategy & Outlook 21

Frontier exploration with strong value creation potential

Uruguay Atlantic Margin, Block 14

Total 65%, operator

Successful farm-out completed

High-potential frontier prospects

de-risked with 3D and DHIs*

Raya, a giant ultra-deep offshore prospect

• Exploration well in 2016

• Success to de-risk several other targets

Raya-1

* DHI: direct hydrocarbon indication

Raya seismic section

Uruguay Raya-1

2km

SW NE

Flat Spot

2015 Strategy & Outlook 22

Transforming our exploration business with a new approach

New exploration teams organized around fully accountable regions

Focusing on value creation and

performance improvement

Emphasizing regions accountability

Strengthening regional knowledge

Revising processes for better quality

control and technical support

Rejuvenated exploration team

Opening regional hubs

Houston

Paris

Pau

Dubai Singapore

EXPLORATION

Americas Europe &

Central Asia Africa

Middle East &

North Africa Asia Pacific

Strategy, Planning

& Portfolio

Exploration

Excellence Geo-technology

Solutions

2015 Strategy & Outlook 23

Exploration key takeaways

New leadership team focused on

delivering top quartile performance

>3 Bboe high-graded exploration potential

Revised exploration drilling strategy

• 50% in core and emerging basins

• 25% near-field exploration

• 25% frontier with strong value potential

1.5-2 B$ budget, targeting

finding cost <$3/boe

Drilling >40 wells and >0.5 Bboe of

risked exploration potential per year

LNG Building on a profitable and integrated portfolio

Laurent VIVIER President, Gas

2015 Strategy & Outlook 25

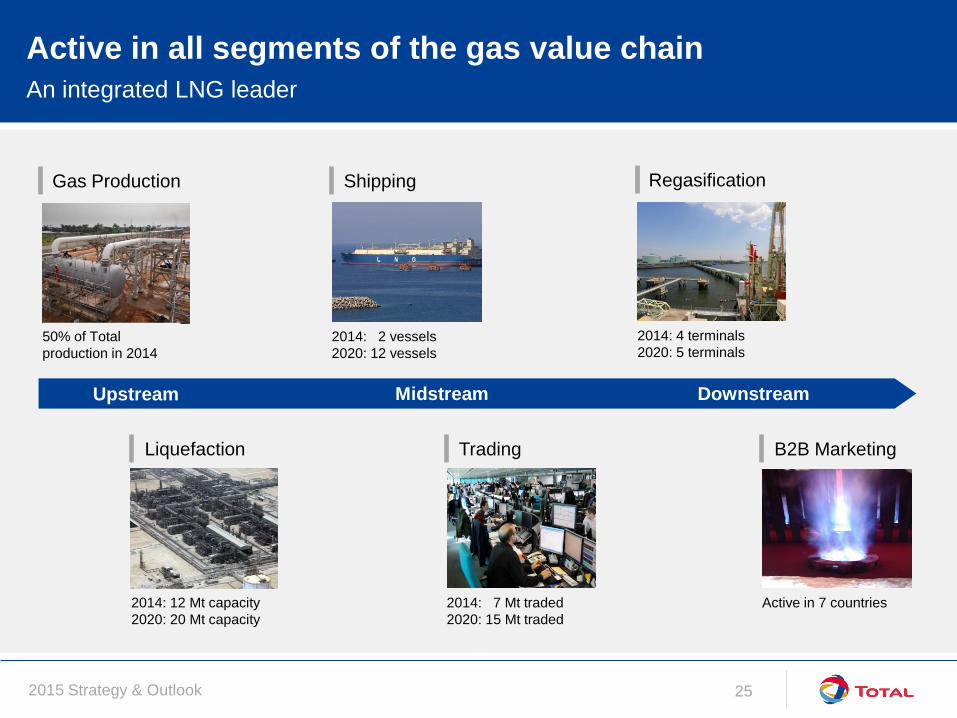

Active in all segments of the gas value chain

An integrated LNG leader

Liquefaction

2014: 12 Mt capacity

2020: 20 Mt capacity

Shipping

2014: 2 vessels

2020: 12 vessels

Trading

2014: 7 Mt traded

2020: 15 Mt traded

Regasification

2014: 4 terminals

2020: 5 terminals

B2B Marketing

Active in 7 countries

Midstream Upstream Downstream

Gas Production

50% of Total

production in 2014

2015 Strategy & Outlook 26

A global LNG player active in all markets

US exports

Altamira

South Hook

Fosmax

Dunkirk

Snøhvit Yamal

Angola

Nigeria

Yemen

Qatargas 1 & 2

Adgas

Qalhat

Oman

Ichthys GLNG

Bontang

Papua

project

Hazira

Liquefaction

Regasification

Long term purchase

Long term sale

2015 Strategy & Outlook 27

2014 2020

Profitable and growing business

Maximizing value from integration of upstream and trading

Total #3 in LNG* Mt/y

One of the Group’s growth drivers

Increasing LNG production capacity by 50%

More than doubling Trading portfolio

LNG contribution to Upstream in 2020

30% of net

operating income

20% of

production

Trading from Upstream

production

LNG plant direct sales

Trading from third party purchases

15

* Based on public data for BP, Chevron, Exxonmobil, Shell/BG (pro-forma)

2015 Strategy & Outlook 28

Starting up long plateau projects

Adding 8 Mt/y capacity

GLNG 7.2 Mt/y capacity

Total 27.5%

Train 1 gas-in Aug 2015

Upstream operational, LNG

plant being commissioned

Oil-indexed contracts to

Korea and Malaysia

Ichthys 8.9 Mt/y capacity + 100 kb/d liquids

Total 30%

Overall progress >75%

First LNG in 2017

Oil-indexed contracts to

Japan and Taiwan

Yamal 16.5 Mt/y capacity

Total 20%

Overall progress 30%

First LNG end-2017

Oil & gas-indexed contracts,

50% in Europe, 50% in Asia

2015 Strategy & Outlook 29

0

1

2

3

4

5

6

7

8

9

10

11

12

13

Maximizing value of Upstream production

Resilient contracts through the oil cycle

2014 Upstream LNG sales by area Mt/y

Low exposure to price reviews before 2020

S-curves and constants supporting prices

1/3 of Upstream contracts redirected in 2014

LNG contract price reviews

Contractual

destination

Realized

destination

Asia

Europe

North America

2015-19

After 2020

No price review

Rest of world 12

2015 Strategy & Outlook 30

Well positioned to seize new opportunities

Leveraging size and flexibility to capture margins

Trading arbitrage $/Mbtu

Enhancing supply optionalities

Well balanced long term and spot exposure

Global market with regional disparities

Arbitrage between three main areas

Trading portfolio evolution Mt/y

Flexible

destination

Long term

sales

Regas

capacity

Spot

2014

supply

2014

sales

2020

supply

2020

sales

15

Global arbitrage options

>2x

Fixed

destination

JKM 2014: 14

1H15: 8

NBP 2014: 8

1H15: 7 HH

2014: 4

1H15: 3

2015 Strategy & Outlook 31

Two competitive projects for production after 2020

Papua LNG Total 40.1%, operator

8.5 Mt/y capacity

Brownfield development taking advantage of

existing infrastructure

Positive resource appraisal ongoing

Greenfield development benefiting from

favorable location

Nigeria LNG Train 7 Total 15%

2015 Strategy & Outlook 32

Leveraging a core competency

Capturing the full value chain

Adding long plateau production

Global, well balanced and integrated

position

Growing trading portfolio with increasing

flexibility

Competitive new projects

Guy MAURICE SVP Africa,

Exploration & Production

Momar NGUER SVP Africa Middle-East,

Marketing & Services

AFRICA The leading integrated major

2015 Strategy & Outlook 34

Leading integrated major in Africa

Long history across the continent

Core region for Total

• 1/3 of Group cash flow from operations

• 1/3 of Group organic Capex

• 1/3 of Group production

Key resource base for Upstream

• Producing >650 kboe/d from six countries

• Exploration in a further 10 countries

Present in 44 countries

Downstream only

Upstream & Downstream

Upstream projects

Upstream only

2015 Strategy & Outlook 35

Successfully managing African context

Sustainable core competencies

Promoting local partnerships

Highly skilled local teams and

mobile international staff

Applying international best practice

More than 80 years in Africa

1934 Year of entry

Nigeria

1962

Angola

1953

Congo

1968

Gabon

1934

2015 Strategy & Outlook 36

Consistent operational delivery

Leveraging local expertise and operational excellence to create value

Implementing international

safety standards

Reducing flaring and monetizing gas

Reliably producing >1 Mboe/d since 2007

Improving HSE performance* in Africa

while growing operated production

* Operated assets, flaring excl. start-ups, TRIR: Total Recordable Injury Rate

0%

20%

40%

60%

80%

100%

120%

140%

160%

1H15 2010

100

2005

+38%

-56%

-53%

Base 100

in 2005

Production Flaring TRIR

2015 Strategy & Outlook 37

Deep offshore in Africa

Culture of continuous innovation

2001 2009 2006 2011 2007 2014 2008 2015 1997

ROSA Angola

CLOV Angola

AKPO Nigeria

PAZFLOR Angola

DALIA Angola

MOHO BILONDO Congo

MOHO Ph 1b Congo

BLOCK 17 Angola

GIRASSOL Angola

First giant deep offshore

FPSO, innovative

riser towers

20 km tie-back to

Girassol FPSO

Subsea multi-phase

pumps, variable speed

drive technology

First all-electric FPSO,

four-stage separation

First subsea

gas/liquid separation

and pumping modules

Flexible risers, integrated

production bundles and

pipe-in-pipe flow lines

Subsea seawater

treatment & injection

program

Deep offshore Girassol

discovery - a pioneer

explo well

Most powerful subsea

multi-phase pumps ever

installed

2015 Strategy & Outlook 38

Angola

Growing operated production to >700 kboe/d

Deep offshore Block 17 (Total 40%, operator) Cumulative production >2 Bb, 2 Bb reserves remaining

CLOV producing up to 180 kb/d and

generating 900 M$ cash in 2015 for Total

Kaombo (Total 30%, operator) progress

at 31%, adding 230 kb/d by 2018

Reducing costs prior to FID on Zinia 2

satellite and Acacia infill projects

3 high-impact exploration wells

Angola

ALNG

Kaombo

Girassol

Dalia

Pazflor

Zinia 2

Dalia 2A

CLOV Block 32

Block 17

Block 14

Block 0

Development Under study Producing

Acacia

2015 Strategy & Outlook 39

Nigeria

Adding to a strong and balanced portfolio

Diverse asset base Offshore, deep offshore, onshore and LNG

Ofon 2 flare-out and gas

monetization since 1Q15

Egina (Total 24%, operator) progress

at 36%, adding 200 kb/d by 2018

Evaluating developments on

Bonga SW, Ikike and NLNG T7

Continuing to explore

high-potential acreage

Bonga

Bonga SW

Usan

Ofon 2

Egina

Akpo

Ikike

NLNG

OML 58

NLNG T7

Nigeria

Amenam

Development Under study Producing

2015 Strategy & Outlook 40

Growth opportunities in Africa

New developments and exploration

Targeting new exploration provinces High-impact wells 2016-18

Frontier well in South Africa

High-potential deep offshore Kenya

Improved fiscal terms, progressing

development plan and pipeline route

Potential FID in 2017

Opening new frontier basin in Uganda >1 Bb resources

Uganda

EA-1A

EA-2

EA-2

Kingfisher

Total 33% Total 33%, operator

Lake

Albert

EA-1

Wells targeting >500 Mboe*

Wells targeting 100-500 Mboe*

* 100% mean resources

2015 Strategy & Outlook 41

0

100

200

300

400

500

600

700

800

E&P in Africa: continuing to deliver value

Securing the future through operational excellence and project delivery

Africa E&P cash flow from operations B$, at 60 $/b

Reducing costs in each affiliate

Growing production and cash flow

Producing safely and reliably

Delivering Moho Nord, Kaombo and Egina

Africa SEC production kboe/d

20%

2015 2017 2019 0

1

2

3

4

5

6

7

8

9 >40%

2015 2017 2019

800 8

2015 Strategy & Outlook 42

Unmatched M&S position in Africa

Leading Downstream operator leveraging critical mass

M&S presence in Africa Top 5 retailers in Africa 2014 number of service stations

M&S presence

Lubricant blendings

Equity refinery

Main fuels terminals

Leader with 17% market share in 43 countries

40% of M&S net operating income

and 35% of M&S investments in 2014

Competitive supply chain taking advantage of

extensive logistics network

4,000

2015 Strategy & Outlook 43

Recognized player bringing international standards

Building on a strong foundation by engaging local stakeholders

Leveraging local talent

• Targeting 60% nationals in management

• 29 university partnerships and

Young Graduates program in place

Increasing ties with local partners and

promoting local suppliers

Implementing highest standards

• Road safety

• Operational excellence in all facilities

African affiliates management

Enhancing local partnerships

280

managers Nationals

Other Africans

Non-Africans

Local minority shareholding

Presence through distributors

Main university partnerships

Fully owned affiliates

2015 Strategy & Outlook 44

Meeting increasing retail customer expectations in Africa

Delivering the brand promise

Offering premium quality retail

Modern stations with strong non-fuel services

High technology fuel and lubricants

Electronic payments and money transfers

African market growing at 2.5% per year

Increasing market share to 20%

M&S retail sales outpacing African market growth Base 100 in 2014

>4% per year

2014 2017 2019

market

2015 Strategy & Outlook 45

Meeting increasing B2B customer expectations in Africa

Rapidly expanding commercial activity

Leveraging global presence to offer most reliable

services in addition to fuel

Premium quality at a premium price Attracting and retaining high-value customers

M&S B2B sales

Base 100 in 2014

5% per year

2014 2017 2019

Mining &

construction

Aviation

Industry

Bulk

2015 Strategy & Outlook 46

Implementing an ambitious strategy

Generating higher returns from growing sales

Strong net operating income growth

Robust results, leveraging leadership

across all segments, in 43 countries

Maintaining 18% ROACE through

500 M$ per year investment phase

M&S net operating income in Africa B$

+30%

0.5

2014 2019 2017

2015 Strategy & Outlook 47

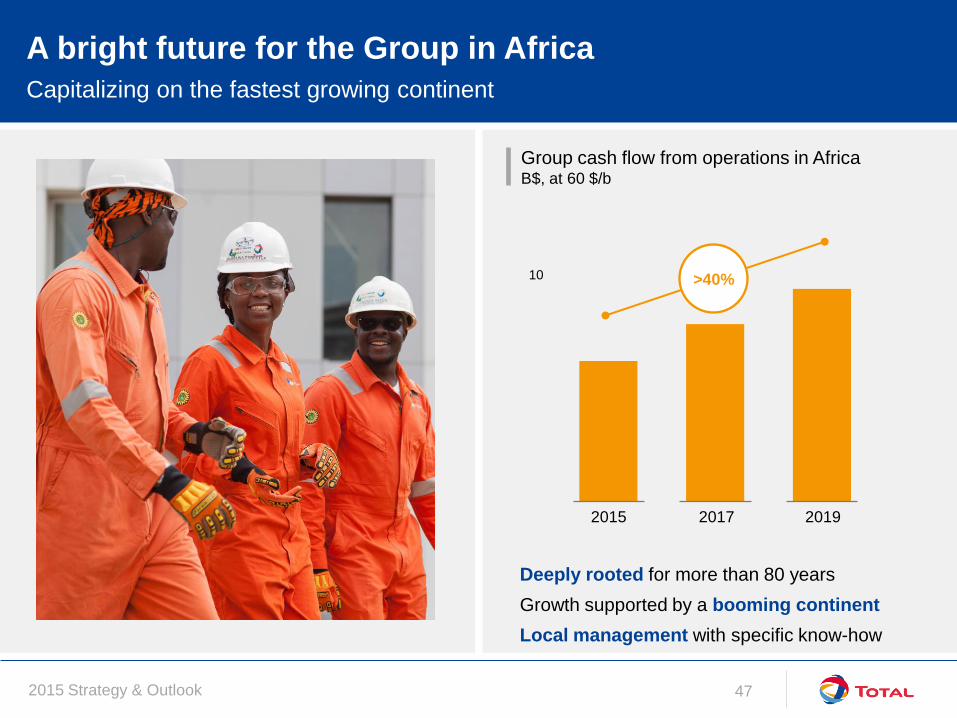

A bright future for the Group in Africa

Capitalizing on the fastest growing continent

Group cash flow from operations in Africa B$, at 60 $/b

Deeply rooted for more than 80 years

Growth supported by a booming continent

Local management with specific know-how

0

10

2017 2015 2019

>40%

2015 Strategy & Outlook 48

Disclaimer

This document may contain forward-looking information on the Group (including objectives

and trends), as well as forward-looking statements within the meaning of the Private

Securities Litigation Reform Act of 1995, notably with respect to the financial condition,

results of operations, business, strategy and plans of TOTAL. These data do not represent

forecasts within the meaning of European Regulation No. 809/2004.

Such forward-looking information and statements included in this document are based on a

number of economic data and assumptions made in a given economic, competitive and

regulatory environment. They may prove to be inaccurate in the future, and are subject to a

number of risk factors that could lead to a significant difference between actual results and

those anticipated, including currency fluctuations, the price of petroleum products, the ability

to realize cost reductions and operating efficiencies without unduly disrupting business

operations, environmental regulatory considerations and general economic and business

conditions. Certain financial information is based on estimates particularly in the assessment

of the recoverable value of assets and potential impairments of assets relating thereto.

Neither TOTAL nor any of its subsidiaries assumes any obligation to update publicly any

forward-looking information or statement, objectives or trends contained in this document

whether as a result of new information, future events or otherwise. Further information on

factors, risks and uncertainties that could affect the Company’s financial results or the

Group’s activities is provided in the most recent Registration Document filed by the

Company with the French Autorité des Marchés Financiers and annual report on Form 20-F

filed with the United States Securities and Exchange Commission (“SEC”).

Financial information by business segment is reported in accordance with the internal

reporting system and shows internal segment information that is used to manage and

measure the performance of TOTAL. Performance indicators excluding the adjustment

items, such as adjusted operating income, adjusted net operating income, and adjusted net

income are meant to facilitate the analysis of the financial performance and the comparison

of income between periods. These adjustment items include:

(i) Special items

Due to their unusual nature or particular significance, certain transactions qualified as

"special items" are excluded from the business segment figures. In general, special items

relate to transactions that are significant, infrequent or unusual. However, in certain

instances, transactions such as restructuring costs or asset disposals, which are not

considered to be representative of the normal course of business, may be qualified as

special items although they may have occurred within prior years or are likely to occur again

within the coming years.

(ii) Inventory valuation effect

The adjusted results of the Refining & Chemicals and Marketing & Services segments

are presented according to the replacement cost method. This method is used to assess

the segments’ performance and facilitate the comparability of the segments’ performance

with those of its competitors.

In the replacement cost method, which approximates the LIFO (Last-In, First-Out) method,

the variation of inventory values in the statement of income is, depending on the nature of

the inventory, determined using either the month-end price differentials between one period

and another or the average prices of the period rather than the historical value. The

inventory valuation effect is the difference between the results according to the FIFO (First-

In, First-Out) and the replacement cost.

(iii) Effect of changes in fair value

The effect of changes in fair value presented as an adjustment item reflects for some

transactions differences between internal measures of performance used by TOTAL’s

management and the accounting for these transactions under IFRS.

IFRS requires that trading inventories be recorded at their fair value using period-end spot

prices. In order to best reflect the management of economic exposure through derivative

transactions, internal indicators used to measure performance include valuations of trading

inventories based on forward prices.

Furthermore, TOTAL, in its trading activities, enters into storage contracts, which future

effects are recorded at fair value in Group’s internal economic performance. IFRS precludes

recognition of this fair value effect.

The adjusted results (adjusted operating income, adjusted net operating income, adjusted

net income) are defined as replacement cost results, adjusted for special items, excluding

the effect of changes in fair value.

Cautionary Note to U.S. Investors – The SEC permits oil and gas companies, in their filings

with the SEC, to separately disclose proved, probable and possible reserves that a company

has determined in accordance with SEC rules. We may use certain terms in this

presentation, such as resources, that the SEC’s guidelines strictly prohibit us from including

in filings with the SEC. U.S. investors are urged to consider closely the disclosure in our

Form 20-F, File N° 1-10888, available from us at 2, Place Jean Millier – Arche Nord

Coupole/Regnault - 92078 Paris-La Défense Cedex, France, or at our website: total.com.

You can also obtain this form from the SEC by calling 1-800-SEC-0330 or on the SEC’s

website: sec.gov.

![· @e] fid\ XelXc](https://static.fdocuments.in/doc/165x107/5c04b62e09d3f2183a8c24fe/-e-fid-xelxc-.jpg)