Nomura Initiaties Gold(1)

105

A new era for gold producers Initiating coverage of the European gold sector with a Bullish rating In this Anchor Report, we undertake a detailed analysis of gold market supply/demand fundamentals. We conclude that the gold price should stay elevated with significant upside risks through 2015, translating into a new era for gold producers. A cash build in the producers should drive growth, spur M&A and push dividends higher. This improving outlook has yet to be priced into gold equities, which are trading at historical lows in terms of valuation, offering an attractive entry point given current market instability. We see light at the end of the tunnel for gold equity investors. We initiate coverage of six European gold equities. Our top picks are Randgold Resources, African Barrick Gold and Avocet Mining. Key analysis in this report includes: Proprietary scenario analysis on central bank demand for gold. A review of shifts in the aggregate global gold producer income statement and balance sheet. How this new era translates into stock-specific opportunities within the European gold sector. EQUITY RESEARCH ANCHOR REPORT January 18, 2012 Research analysts European Metals & Mining Tyler Broda, CFA – NIplc [email protected] +44 20 7102 4770 Jonathan Wright – NIplc j[email protected] +44 20 7102 7326 David Radclyffe – NIplc [email protected] +44 20 7102 8434 Juho Lahdenpera, CFA – NIplc j[email protected] +44 20 7102 7450 Patrick Jones – NIplc [email protected] +44 20 7102 5486 Neil Sampat – NIplc [email protected] +44 20 7102 1871 Ashraf Khan [email protected] +91 22 3053 3231 Industry specialist Matthew Kates [email protected] +44 20 7103 1402 See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

-

Upload

sovereign01 -

Category

Documents

-

view

203 -

download

8

Transcript of Nomura Initiaties Gold(1)

A new era for gold producers

Initiating coverage of the European gold sector with a Bullish rating

In this Anchor Report, we undertake a detailed analysis of gold market supply/demand fundamentals. We conclude that the gold price should stay elevated with significant upside risks through 2015, translating into a new era for gold producers. A cash build in the producers should drive growth, spur M&A and push dividends higher. This improving outlook has yet to be priced into gold equities, which are trading at historical lows in terms of valuation, offering an attractive entry point given current market instability. We see light at the end of the tunnel for gold equity investors. We initiate coverage of six European gold equities. Our top picks are Randgold Resources, African Barrick Gold and Avocet Mining.

Key analysis in this report includes:

Proprietary scenario analysis on central bank demand for gold.

A review of shifts in the aggregate global gold producer income statement and balance sheet.

How this new era translates into stock-specific opportunities within the European gold sector.

EQUITY RESEARCH

AN

CH

OR

RE

PO

RT

January 18, 2012

Research analysts

European Metals & Mining

Tyler Broda, CFA – NIplc [email protected] +44 20 7102 4770

Jonathan Wright – NIplc [email protected] +44 20 7102 7326

David Radclyffe – NIplc [email protected] +44 20 7102 8434

Juho Lahdenpera, CFA – NIplc [email protected] +44 20 7102 7450

Patrick Jones – NIplc [email protected] +44 20 7102 5486

Neil Sampat – NIplc [email protected] +44 20 7102 1871

Ashraf Khan [email protected] +91 22 3053 3231

Industry specialist

Matthew Kates [email protected] +44 20 7103 1402

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

European Gold Sector Initiation

EUROPEAN METALS & MINING

EQ U I T Y R E S E A RC H

ANCHOR REPORT: A new era for gold producers

Cash build to usher in a new era for gold equities

January 18, 2012

Sector view Remains Bullish

Gold prices to stay elevated for longer Gold prices have risen substantially over the past 10 years. Market expectations of future price movements are extremely varied at the moment as multiple uncertainties in the global financial system provide the potential for large swings in demand. Our analysis suggests that gold prices are well supported at current levels as paradigm shifts in central bank and investment demand alongside constrained supply are likely to provide elevated prices beyond 2014.

High profitability to persist for gold equities Importantly for gold equities, high levels of profitability are likely to be sustained. The resultant cash build within the global gold equity balance sheet is likely to usher in a new era for the gold equities as increased dividends, higher valuations for growth potential and valuation tension from an expected pickup in M&A provide the basis for a rally in the gold mining sector.

Gold equities look attractive in current equity market Gold equities have underperformed gold bullion over the past five years. Sector P/E and EV/EBITDA ratios are near 20-year lows. We believe this is about to change. Increasing market expectations of higher longer-term gold price forecasts, cash margins above USD 1,300/oz and a 15% average 2013 free cash flow yield for the companies analysed herein should increase investor interest in the sector. This new era of elevated profitability and cash flow should see gold equities outperform gold bullion once again.

Top picks: Randgold Resources, African Barrick Gold & Avocet Mining Our recommendations are built around these emerging themes. The European gold equity sector consists of generally smaller companies and is an eclectic group from a global perspective; however, we believe there are some intriguing opportunities. Our top picks included in this report are: • Randgold Resources (RRS, Buy, 9,850p TP), in our view, offers the best

exposure to diversified growth and the purest exposure to the gold price of the companies included in this report.

• African Barrick Gold (ABG, Buy, 750p TP) is likely to see its very significant cash build continue, and we believe the shares possess an as-yet-unpriced strategic optionality within its strong balance sheet.

• Avocet Mining (AVM, Buy, 310p TP) has a significant medium-term growth profile and catalysts, and could benefit from increasing M&A activity in the sector.

Research analysts

European Metals & Mining

Tyler Broda, CFA - NIplc [email protected] +44 20 7102 4770

Jonathan Wright - NIplc [email protected] +44 20 7102 7326

David Radclyffe - NIplc [email protected] +61 2 8062 8434

Juho Lahdenpera, CFA - NIplc [email protected] +44 20 7102 7450

Patrick Jones - NIplc [email protected] +44 20 7102 5486

Neil Sampat - NIplc [email protected] +44 20 7102 1808

Industry specialist

Matthew Kates - NIplc [email protected] +44 20 7103 1402

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Nomura | European Gold Sector Initiation January 18, 2012

2

Contents

3 Executive summary

5 Company summaries

8 A longer-term perspective on gold

11 Forecast gold prices

12 Supply

17 Demand

25 A new era for gold equities

30 European sector review

34 RRS – Randgold Resources (Buy, 9,850p TP)

44 AVM – Avocet Mining (Buy, 310p TP)

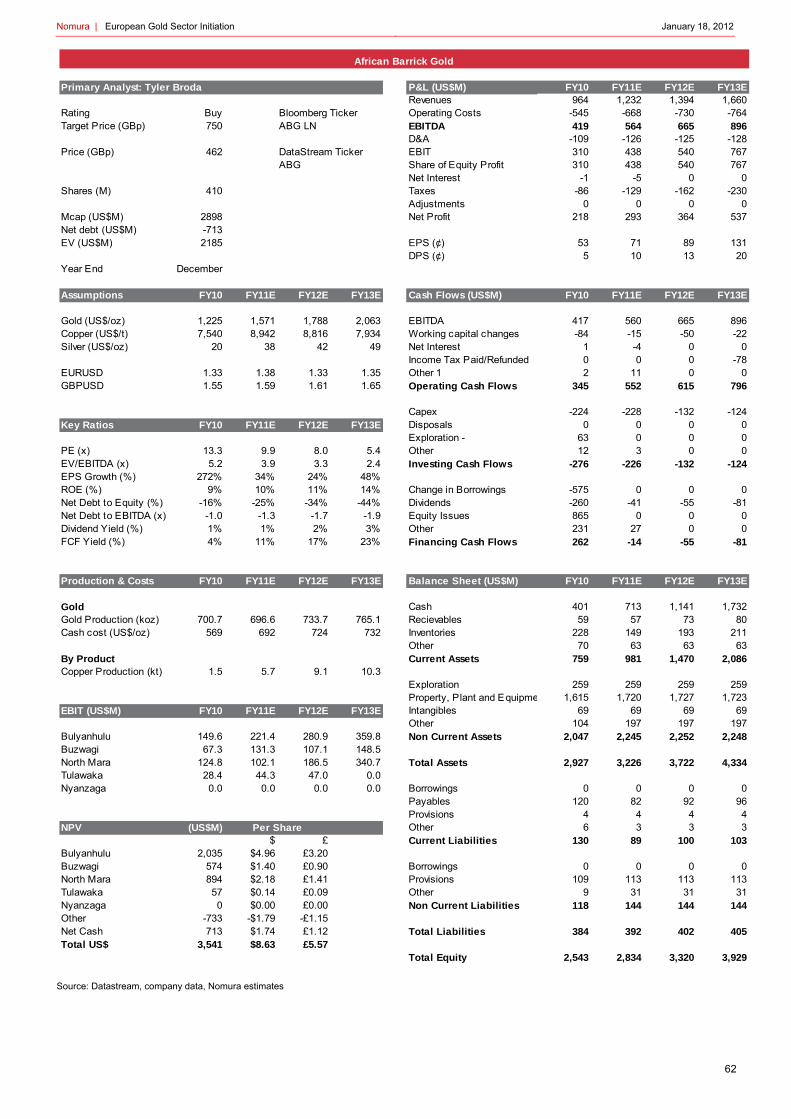

52 ABG – African Barrick Gold (Buy, 750p TP)

64 CEY – Centamin (Neutral, 120p TP)

72 POG – Petropavlovsk (Reduce, 860p TP)

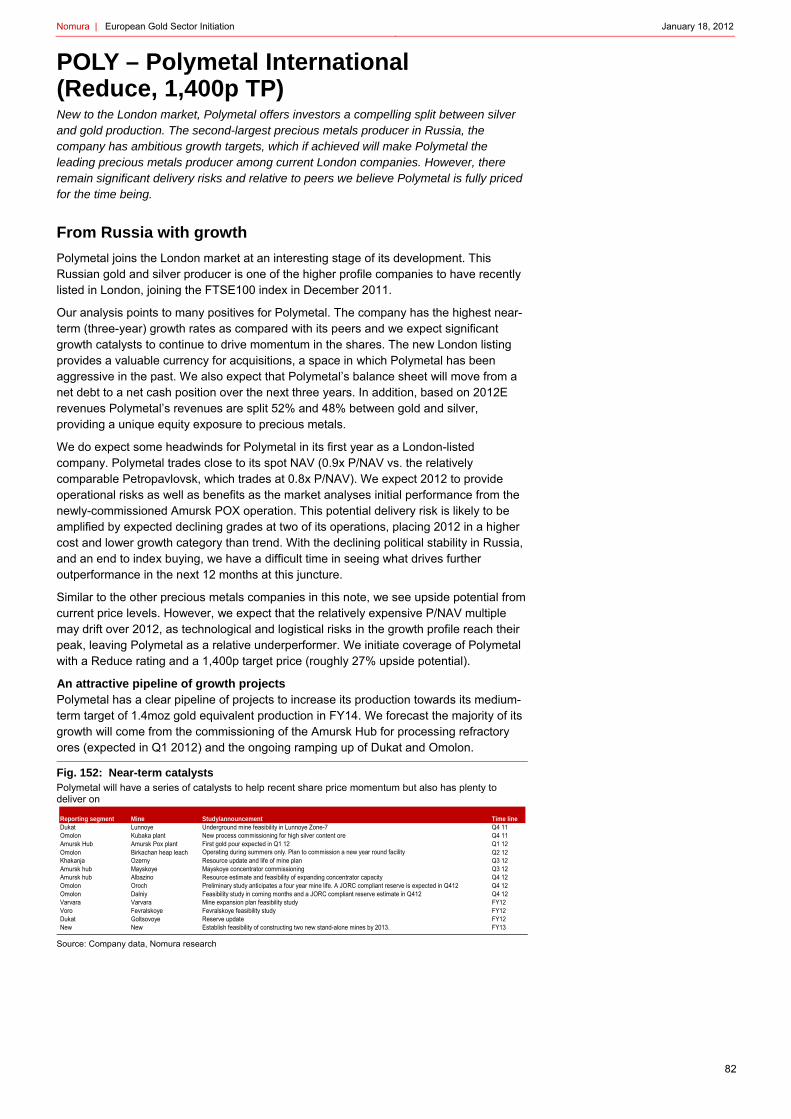

82 POLY – Polymetal International (Reduce, 1,400p TP)

92 SA US – Seabridge Gold (Buy, USD 31.80 TP)

101 Appendix A-1

Research analysts

European Metals & Mining

Tyler Broda, CFA - NIplc [email protected] +44 20 7102 4770

Jonathan Wright - NIplc [email protected] +44 20 7102 7326

David Radclyffe - NIplc [email protected] +61 2 8062 8434

Juho Lahdenpera, CFA - NIplc [email protected] +44 20 7102 7450

Patrick Jones - NIplc [email protected] +44 20 7102 5486

Neil Sampat - NIplc [email protected] +44 20 7102 1808

Industry specialist

Matthew Kates - NIplc [email protected] +44 20 7103 1402

Nomura | European Gold Sector Initiation January 18, 2012

3

Executive summary Our Bullish sector view is built on three key premises.

The current gold price is well supported and should continue to rise in the medium term

Secular Asian demand growth, low and/or negative real interest rates, increasing central bank demand and potential increases in investment sentiment indicate that demand levels will grow. On the supply side, a lack of flexibility in near-term mine supply and a levelling off of scrap gold supply is likely to continue to put upward pressure on the spot gold price.

Our proprietary analysis suggests that central bank demand has the potential to grow from virtually nothing to nearly half of the level currently seen by jewellery (which accounts for 40% of the market). This, in conjunction with a potential wider shift in asset allocation to gold, could see gold prices de-anchoring from current levels. We have used relatively conservative gold demand forecasts in our overall estimates, leaving the gold price with significant upside risk, in our view.

Our gold price forecasts remain near 2012 consensus at USD 1,788/oz, and slightly above 2013 consensus at USD 2,063/oz. Importantly for the gold equities, we expect the gold price to stay above 2010 levels through 2015 and expect long-term equilibrium prices of USD 1,200/oz.

The strong gold price will likely result in a period of rapid EBITDA growth and cash build for the miners

The aggregate industry EBITDA (based on the DS World Gold Mining Index) is set to reach USD 60bn by 2013 compared with the roughly USD 10bn generated in each of the years between 2006 and 2009. This should translate into increasing cash balances for producers. We expect dividends to grow, new expansion projects to progress and M&A activity to also increase sharply. Net debt levels are already low (only two of the seven companies in our coverage universe have net debt positions).

Cash heavy balance sheets have important implications for the sector. As seen in the case of Eldorado Gold Corporation’s recent bid for European Goldfields, M&A activity, especially for growth ounces, is likely to increase, in our view. All of the companies in this report are in a position to benefit from this trend either as acquirers, acquirees or both.

Gold equity valuations are at historical lows

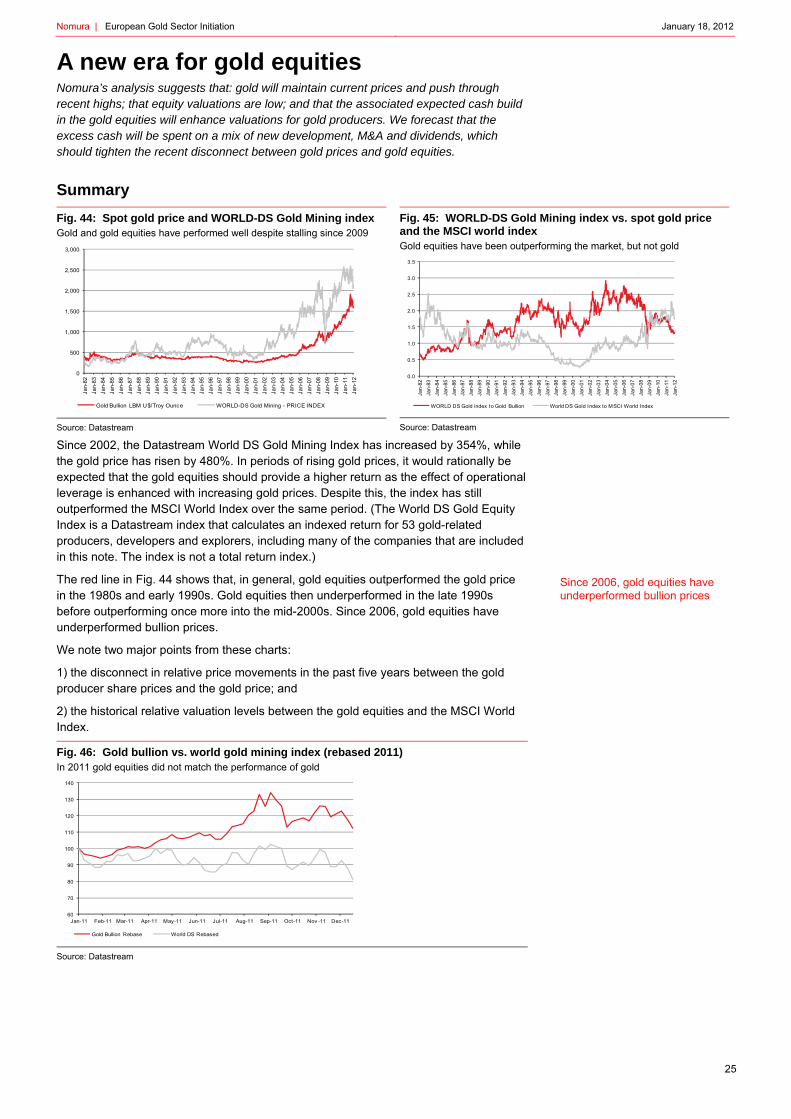

Despite increased profitability and improved balance sheets, gold equities have underperformed gold bullion since 2006 and are trading near 20-year lows in terms of P/E and EV/EBITDA multiples. Even without recovery in sector multiples, the rapid EBITDA growth to c. USD 60bn a year by 2013E (2011: c. USD 30bn), would imply a significant increase in the enterprise value of gold equities over the next two years.

The producers have failed to participate in the recent gold price rally, with gold increasing by 9% in 2011 as global gold equities fell by c.20%. The global gold P/Es have averaged 23x since 2000, whereas the stocks now trade below a 2012E P/E of 15x, providing space for valuation uplift.

The current sector dividend yield is 1.0% and in recent years a number of companies have announced new dividend policies. Assuming yields remain at current levels, FY13E consensus dividends imply a global market capitalisation approaching USD 500bn or nearly 50% upside potential.

On a P/NAV basis, all of our stocks, with the exception of Randgold, trade at below 1.0x (at spot gold prices). We calculate an average implied price of USD 1,488/oz. This implies that investors are not yet pricing in the full potential for gold prices to stay stronger for longer.

We forecast gold producers to achieve record levels of EBITDA and net cash

Cash balances are likely to translate into greater M&A activity and higher dividends, increasing equity valuations

Valuations remain low, despite the high gold price and the related earnings uplift

P/NAV multiples imply value at current spot prices

We expect diversified demand drivers to support the gold price

Nomura | European Gold Sector Initiation January 18, 2012

4

Fig. 1: Forecast gold price Consensus gold expectations are varied

Source: Bloomberg, Nomura research

Fig. 2: Historical and consensus EBITDA and net debt Gold producers are set for a period of rising EBITDA and rising cash levels

Source: Datastream

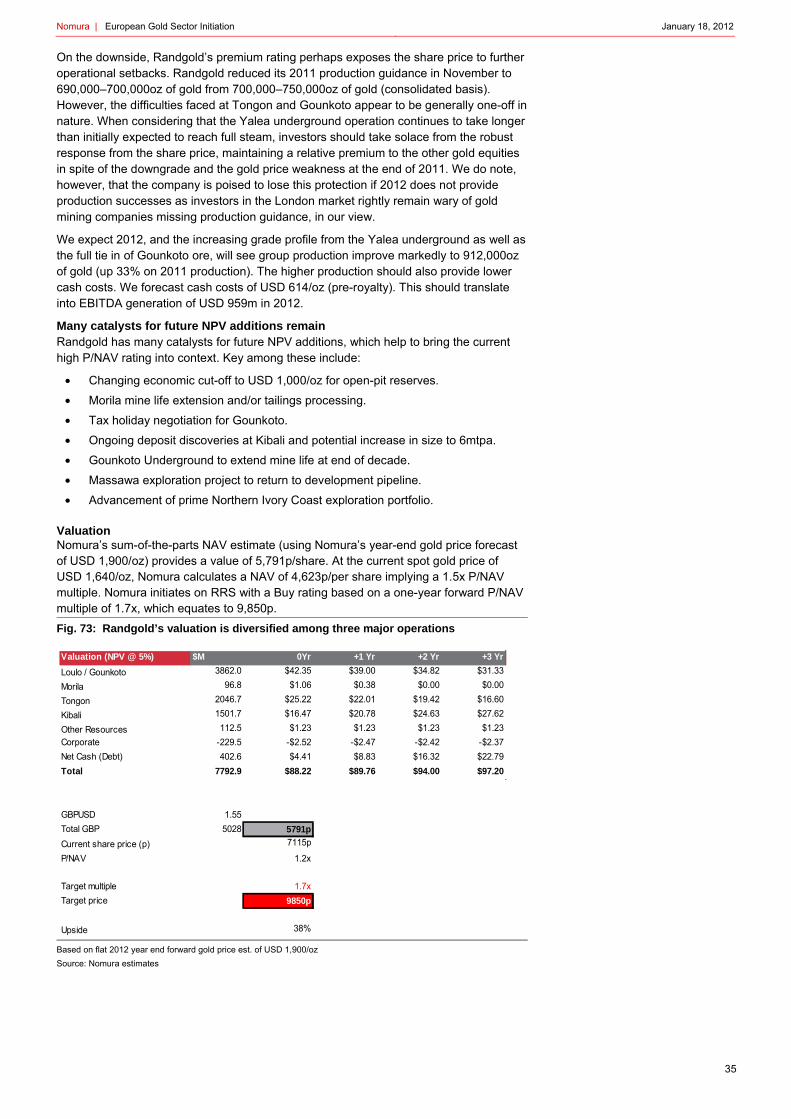

Fig. 3: Price to NAV On average, the equities are trading at 0.8x based on the spot gold price and all except Randgold trade below 1.0x

Source: Nomura estimates, using a 5% discount rate and spot gold prices of USD 1,640/oz

500

1,000

1,500

2,000

2,500

3,000

3,500

2012e 2013e 2014e 2015e

Nomura High Mean Low

Gol

dpr

ice

(USD

/oz)

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q1

2000

Q3

2000

Q1

2001

Q3

2001

Q1

2002

Q3

2002

Q1

2003

Q3

2003

Q1

2004

Q3

2004

Q1

2005

Q3

2005

Q1

2006

Q3

2006

Q1

2007

Q3

2007

Q1

2008

Q3

2008

Q1

2009

Q3

2009

Q1

2010

Q3

2010

Q1

2011

Q3

2011

Q1

2012

Q3

2012

Q1

2013

Q3

2013

Net debt EBITDA ($m)

$m

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

1.6x

1.8x

Centamin Af rican Barrick Gold

Avocet Mining Petropavlovsk Polymetal Randgold Resources

P/NAV

Nomura gold price forecasts are roughly in line with consensus in each of the next four years

Forecast gold prices would push global sector EBITDA to USD 60bn by FY13E, with a related build in net cash

Even given the recent fall in the price of gold, the London-based producers (with the exception of Randgold) are still trading at a discount to NAV; given the potential upside to the current gold price, the miners provide excellent value, in our view

Nomura | European Gold Sector Initiation January 18, 2012

5

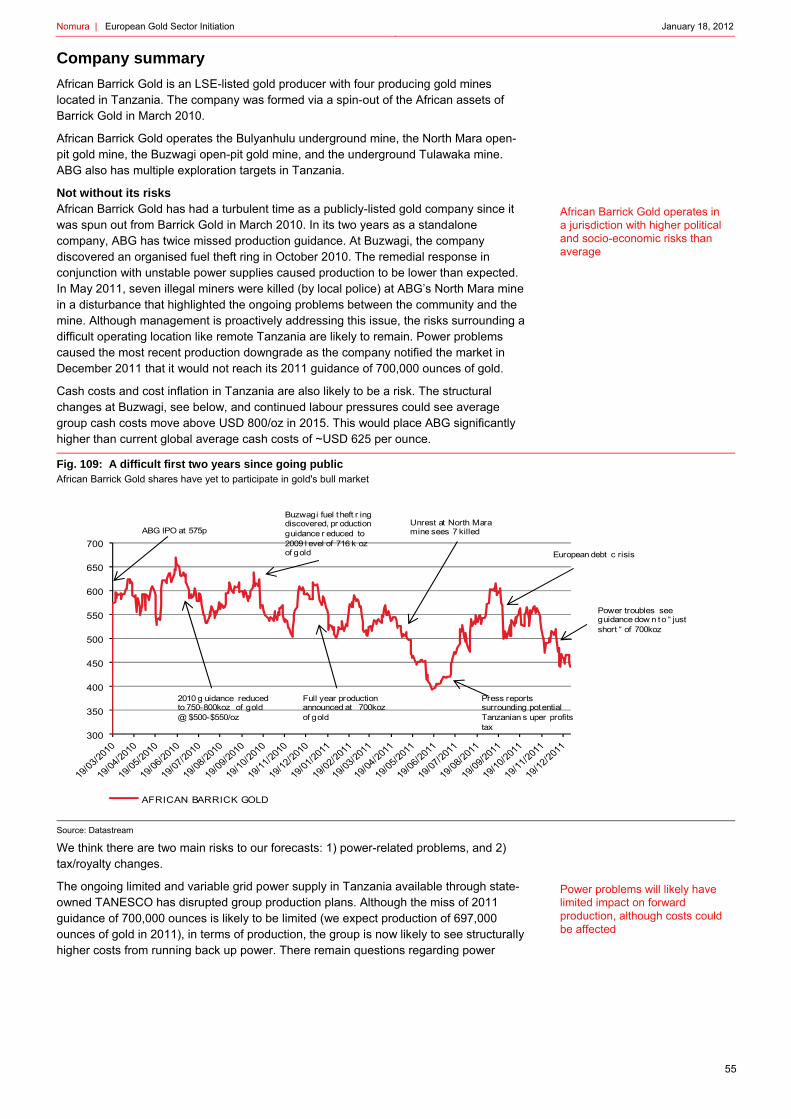

Company summaries We see upside potential from current levels for all of the gold companies included in this report. In our view, the increasingly compelling macro outlook for gold should provide outperformance for gold equities as compared with the wider market. We see average upside potential of 42% in our universe. Nomura uses a relative rating system, therefore we have attempted to balance our ratings between those with higher upside potential and those with lower upside potential or higher risks. Our top European recommendations include Randgold Resources, African Barrick Gold and Avocet Mining.

Fig. 4: Company summary

Current prices as at close of 16 January 2012. Source: Datastream, Nomura estimates

African Barrick Gold PLC (ABG LN, Buy, TP 750p) Spun out of parent Barrick Gold in 2010, African Barrick Gold is an intermediate gold producer with four gold mines in Tanzania. We estimate that the group produced 697,000oz of gold in 2011 at a cash cost of USD 692/oz. ABG trades at 0.6x our spot gold P/NAV estimates, a valuation which, in our view, is hampered by the continued production disappointments since its IPO.

ABG has an exceptionally strong balance sheet and the group’s strategic optionality does not appear to have been priced into the current share price. We see 2012 as a potentially transformational year for the group as high profitability and further cash generation (we expect a free cash flow yield (FCFY) of 24% for the group by 2013) should increase tension on a current slack market valuation. Nomura initiates on ABG with a Buy rating and a 750p target price, which is equivalent to a P/NAV of 0.8x based on our 2012 exit gold price forecast of USD 1,900/oz.

Avocet Mining PLC (AVM LN, Buy, TP 310p) Now a pure-play West African junior producer, Avocet Mining is turning its full attention to growth both at its current Inata operations in Burkina Faso and its Guinean exploration asset. We expect 2012 to provide continued positive catalysts as the group better defines its growth potential, for which we believe there is significant upside potential.

We forecast that Avocet produced 164,000oz of gold in 2011 at a cash cost of USD 706/oz. The shares underperformed the wider gold equity market in 2011. We believe that the market has yet to price in Avocet’s new exposure to the gold price (following its renegotiation of hedge deliveries) or the potential, as disclosed in the 2011 interim results, to expand Inata once again. Nomura initiates on AVM with a Buy rating and a 310p target price, which is equivalent to a P/NAV of 0.9x based on our 2012 exit gold price forecast of USD 1,900/oz.

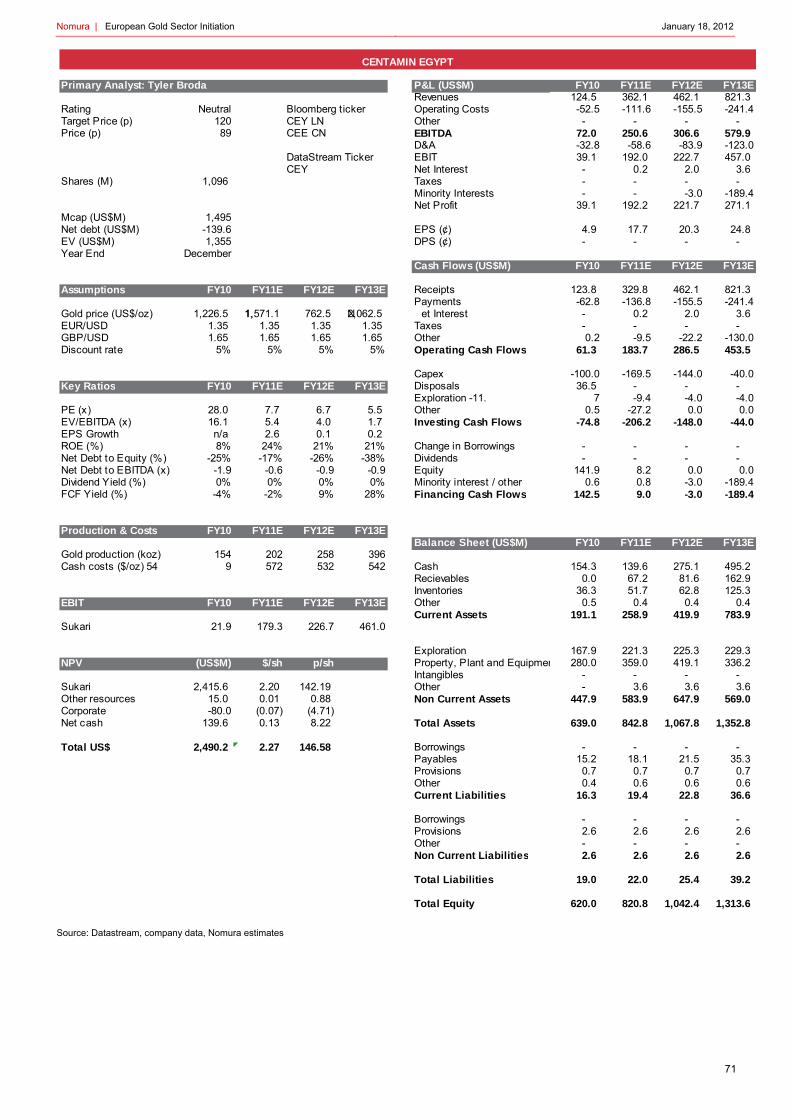

Centamin PLC (CEY LN, Neutral, TP 120p) Centamin is a growing junior-intermediate gold producer. It operates the 9.1moz Sukari open-pit and underground mine in southern Egypt. It produced 202,000oz of gold at a forecast cash cost of USD 572/oz in 2011 and our forecasts suggest higher production will result from further plant and mining expansions in 2012.

Centamin’s shares fell by c.50% in 2011 both owing to missed production guidance and to the uncertainty generated by the Egyptian revolution. In addition, the company will begin to see half of the cash flows accrue to the Egyptian government as per the extraction licence, eroding forward EPS growth. The 35% upside potential to the target price reflects the fact that the shares appear to be underpriced and oversold. However, we believe that CEY will maintain higher-than-average risks through the Egyptian election period and as such Nomura initiates on CEY with a Neutral rating. Our 120p 12-month target price is equivalent to 0.5x our 2012 exit gold price forecast of USD 1,900/oz.

Company Ticker Market cap Current price Rating Target price2012e EBITDA

Nomura estimate2012e EBITDA

Consensus median2012e EBITDA

Consensus high/low

Randgold Resources RRS 9,988 7115p Buy 9850p 959 1019 946 - 1344Polymetal P OLY 6,448 1100p Reduce 1400p 1,208 1195 933 - 1472African Barrick Gold ABG 2,904 462p Buy 750p 665 713 613 - 1,066Petropavlovsk P OG 1,952 685p Reduce 860p 570 608 372 - 971Centamin C EY 1,498 89p Neutral 120p 307 310 148 - 362Avocet Mining AVM 654 214p Buy 310p 109 104 75 - 126

Seabridge Gold SA 817 $19.23 Buy $31.80 n/a n/a n/a

In our view, ABG’s valuation is overly hampered by previous production misses

Our analysis indicates that high profitability and significant strategic optionality is not being captured in the current valuation

AVM has an aggressive growth programme

Avocet shareholders have not as yet benefitted from strategic changes in 2011

CEY’s main Sukari asset continues to expand

Egyptian risk and low EPS growth mitigate upside potential from attractive valuation

Nomura | European Gold Sector Initiation January 18, 2012

6

Petropavlovsk PLC (POG, Reduce, TP 860p) Petropavlovsk, a Russian intermediate gold producer, operates four open-pit hard rock gold mines in Russia’s Amur region supported by a promising growth profile. We forecast that POG produced 624,000oz of gold at a cash cost of USD 762/oz in 2011. The main production growth is likely to come from the POX Hub being built at Pokrovskiy. This hub will process refractory ore and should open up a further avenue of growth for POG.

In our view, Petropavlovsk continues to have an attractive valuation and, although the company has made significant progress in rationalising its targets, there remain roadblocks in achieving a full re-rating in 2012, in our view. The relatively high net-debt position, persisting Russian risk discount, the non-precious metal IRC stake and general declining mined grades should continue to place pressure on the P/NAV multiples as the company moves toward commissioning of the POX hub in 2013. Nomura initiates on POG with a Reduce rating and an 860p target price, which is equivalent to 0.7x our 2012 exit gold price forecast of USD 1,900/oz.

Polymetal International (POLY LN, Reduce, TP, 1,400p) New to the FTSE 100 Index, Polymetal is a leading Russian intermediate gold and silver producer. It operates six mining complexes in Russia using a hub approach to rationalise capital costs. Polymetal has one of the leading growth profiles of the London gold equities and provides an interesting split to investors in context of its roughly 50-50 gold/silver exposure. We forecast that it will produce 1,006,000oz of gold equivalent in 2012 at an average cost of USD 752/oz.

Polymetal appears fully priced at the moment, in our view. It has outperformed the sector since its London IPO and now trades on our spot P/NAV estimate of 0.9x. Although there are many positives, including the attractive growth profile, there are many delivery risks that could put this premium rating under pressure in 2012. Nomura initiates on POLY with a Reduce rating and a 1,400p target price, which is equivalent to a P/NAV of 0.9x based on our 2012 exit gold price forecast of USD 1,900/oz.

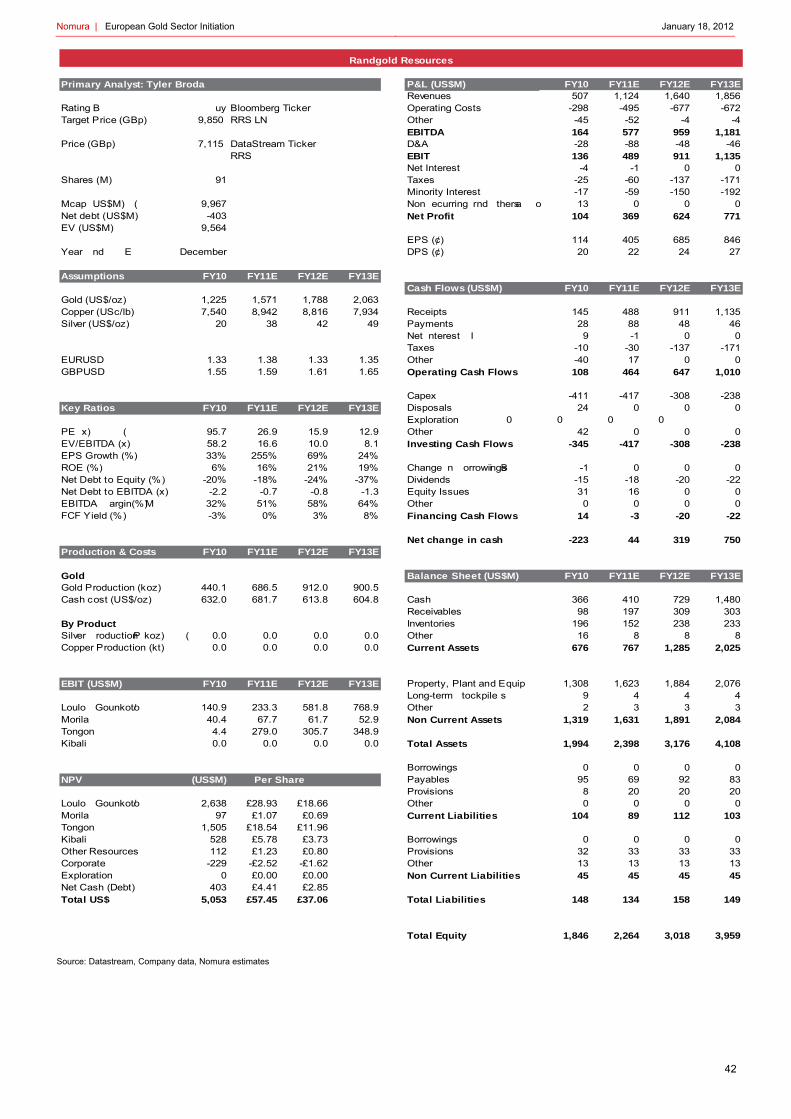

Randgold Resources (RRS LN, Buy, TP 9,850p) Randgold Resources’ African growth story continues as production at the Loulo/Gounkoto complex increases and the large Kibali open-pit and underground mine in the DRC is built. We forecast that this intermediate gold producer produced 686,000oz at a cash cost of USD 682/oz (excluding royalties) in 2011.

Randgold shares remain the most expensive in the London sector, as the company rates highly on almost all categories including production growth, costs, diversification of risks (both political and operational) and potential, as yet unpriced, NAV growth. Although the shares are relatively expensive, Randgold’s quality means that it is likely to give investors the cleanest exposure to positive sector trends and maintain its multiple. Nomura initiates on RRS with a Buy rating and a 9,850p target price, which is equivalent to 1.7x our 2012 exit gold price forecast of USD 1,900/oz.

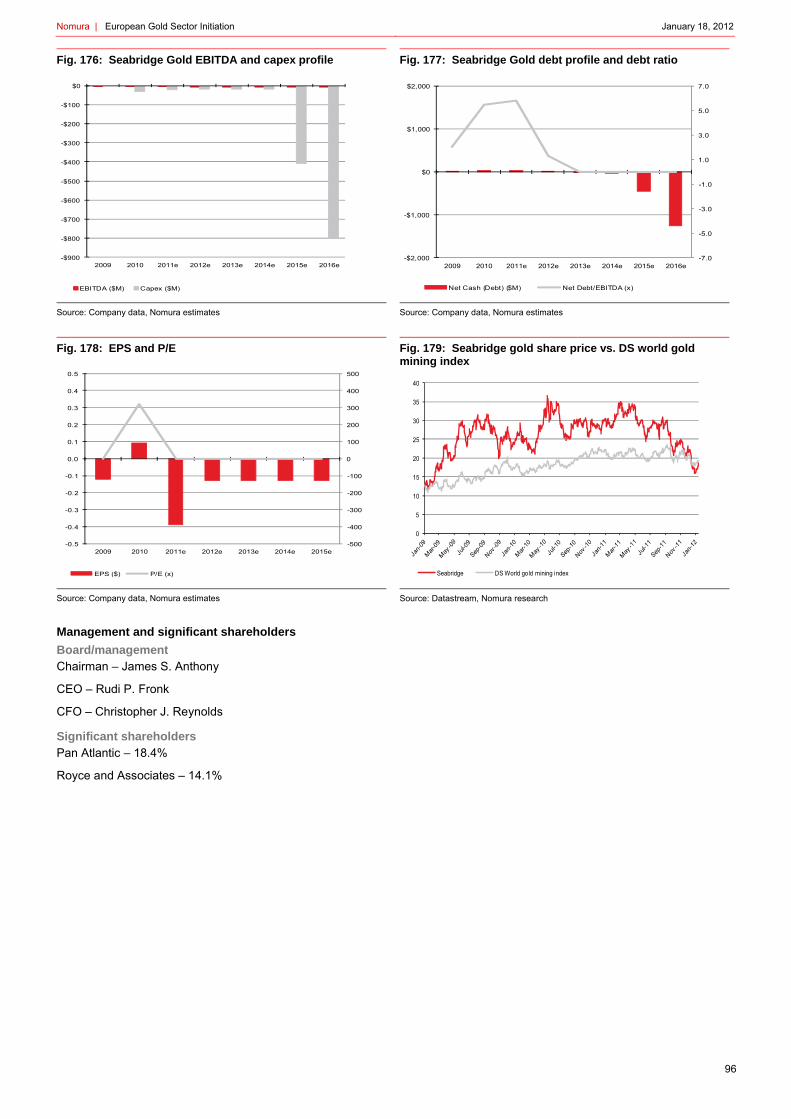

Seabridge Gold (SEA CN, Buy, TP USD 31.80) Included in this report is a transfer of coverage update for Seabridge Gold. We maintain the Buy rating and set a USD 31.80, 12-month target price (previously USD 51.00). Seabridge Gold owns and is progressing the massive KSM gold-silver-copper-molybdenum project and the Courageous Lake gold project in Canada.

Seabridge Gold provides perhaps the greatest relative exposure to higher gold prices, in our view. The high expected capex levels for its main projects and its need for a partner to progress these projects see the shares trade on a significant discount to its underlying potential value. As gold prices increase, the probability of these assets being partnered, financed and progressed should increase, reducing the discount in the P/NAV multiple. We anticipate that KSM and Courageous Lake are unlikely to be in production until the end of the decade (at earliest), and there remains significant uncertainty around permitting, financing and development. A discount is, therefore, warranted.

However, investors will be able to gain long-term exposure to our new era for gold equities theme as the Seabridge development story takes place. Our target is based on a 0.4x P/NAV target price using our long-term gold price estimates and we note our valuation is heavily risked for development and financing risks.

The POX hub at Pokrovskiy will account for the main growth from 2013

The attractive valuation will continue to face headwinds, in our view, in 2012

We expect Randgold’s growth to continue

A top-quality company that provides the cleanest exposure for growth-oriented gold equity investors

Although not currently producing, we believe that Seabridge offers substantial upside potential under our forecast gold price

Polymetal is a solid company with strong growth prospects but, in our view, is fully priced

Nom

ura | European G

old Sector Initiation

January 18, 20127

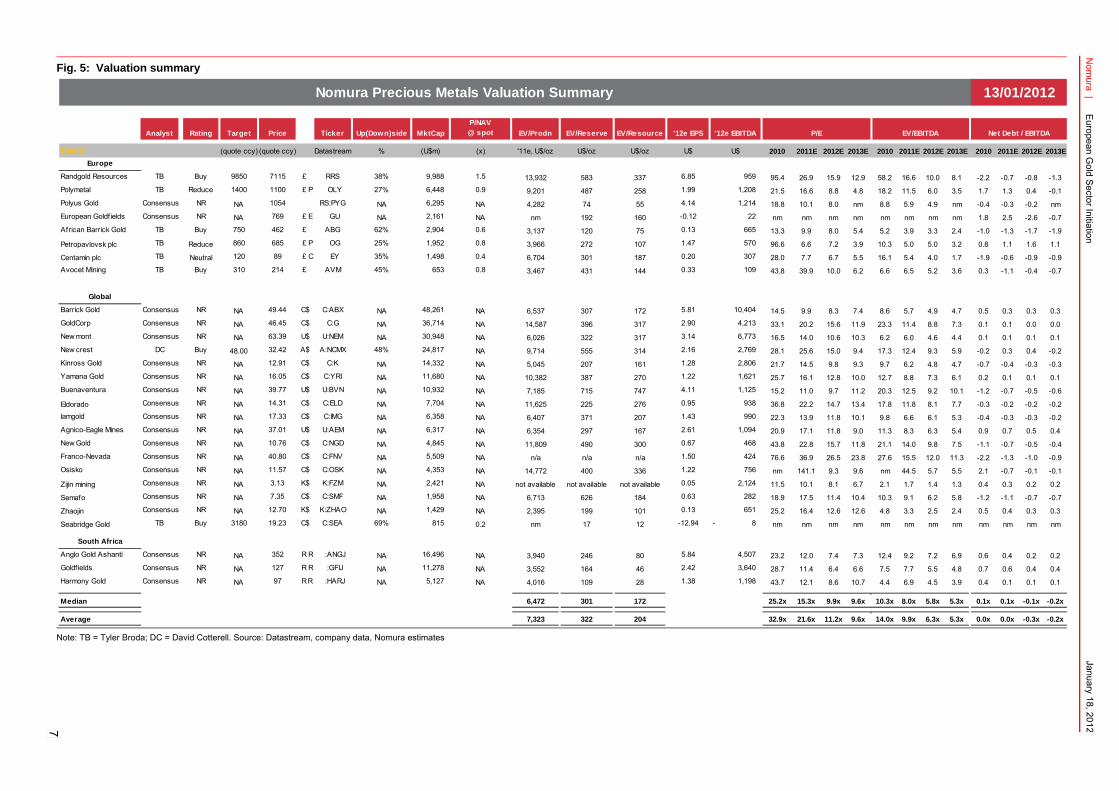

Fig. 5: Valuation summary

Note: TB = Tyler Broda; DC = David Cotterell. Source: Datastream, company data, Nomura estimates

Analyst Rating Target Price Ticker Up(Down)side MktCap

P/NAV@ spot EV/Prodn EV/Reserve EV/Resource '12e EPS '12e EBITDA

Gold (quote ccy) (quote ccy) Datastream % (U$m) (x) '11e, U$/oz U$/oz U$/oz U$ U$ 2010 2011E 2012E 2013E 2010 2011E 2012E 2013E 2010 2011E 2012E 2013E

Europe

Randgold Resources TB Buy 9850 7115 £ RRS 38% 9,988 1.5 13,932 583 337 6.85 959 95.4 26.9 15.9 12.9 58.2 16.6 10.0 8.1 -2.2 -0.7 -0.8 -1.3Polymetal TB Reduce 1400 1100 £ P OLY 27% 6,448 0.9 9,201 487 258 1.99 1,208 21.5 16.6 8.8 4.8 18.2 11.5 6.0 3.5 1.7 1.3 0.4 -0.1Polyus Gold Consensus NR NA 1054 RS:PYG NA 6,295 NA 4,282 74 55 4.14 1,214 18.8 10.1 8.0 nm 8.8 5.9 4.9 nm -0.4 -0.3 -0.2 nmEuropean Goldfields Consensus NR NA 769 £ E GU NA 2,161 NA nm 192 160 -0.12 22 nm nm nm nm nm nm nm nm 1.8 2.5 -2.6 -0.7African Barrick Gold TB Buy 750 462 £ ABG 62% 2,904 0.6 3,137 120 75 0.13 665 13.3 9.9 8.0 5.4 5.2 3.9 3.3 2.4 -1.0 -1.3 -1.7 -1.9

Petropavlovsk plc TB Reduce 860 685 £ P OG 25% 1,952 0.8 3,966 272 107 1.47 570 96.6 6.6 7.2 3.9 10.3 5.0 5.0 3.2 0.8 1.1 1.6 1.1

Centamin plc TB Neutral 120 89 £ C EY 35% 1,498 0.4 6,704 301 187 0.20 307 28.0 7.7 6.7 5.5 16.1 5.4 4.0 1.7 -1.9 -0.6 -0.9 -0.9Avocet Mining TB Buy 310 214 £ AVM 45% 653 0.8 3,467 431 144 0.33 109 43.8 39.9 10.0 6.2 6.6 6.5 5.2 3.6 0.3 -1.1 -0.4 -0.7

Global

Barrick Gold Consensus NR NA 49.44 C$ C:ABX NA 48,261 NA 6,537 307 172 5.81 10,404 14.5 9.9 8.3 7.4 8.6 5.7 4.9 4.7 0.5 0.3 0.3 0.3GoldCorp Consensus NR NA 46.45 C$ C:G NA 36,714 NA 14,587 396 317 2.90 4,213 33.1 20.2 15.6 11.9 23.3 11.4 8.8 7.3 0.1 0.1 0.0 0.0New mont Consensus NR NA 63.39 U$ U:NEM NA 30,948 NA 6,026 322 317 3.14 6,773 16.5 14.0 10.6 10.3 6.2 6.0 4.6 4.4 0.1 0.1 0.1 0.1New crest DC Buy 48.00 32.42 A$ A:NCMX 48% 24,817 NA 9,714 555 314 2.16 2,769 28.1 25.6 15.0 9.4 17.3 12.4 9.3 5.9 -0.2 0.3 0.4 -0.2Kinross Gold Consensus NR NA 12.91 C$ C:K NA 14,332 NA 5,045 207 161 1.28 2,806 21.7 14.5 9.8 9.3 9.7 6.2 4.8 4.7 -0.7 -0.4 -0.3 -0.3Yamana Gold Consensus NR NA 16.05 C$ C:YRI NA 11,680 NA 10,382 387 270 1.22 1,621 25.7 16.1 12.8 10.0 12.7 8.8 7.3 6.1 0.2 0.1 0.1 0.1Buenaventura Consensus NR NA 39.77 U$ U:BVN NA 10,932 NA 7,185 715 747 4.11 1,125 15.2 11.0 9.7 11.2 20.3 12.5 9.2 10.1 -1.2 -0.7 -0.5 -0.6

Eldorado Consensus NR NA 14.31 C$ C:ELD NA 7,704 NA 11,625 225 276 0.95 938 36.8 22.2 14.7 13.4 17.8 11.8 8.1 7.7 -0.3 -0.2 -0.2 -0.2Iamgold Consensus NR NA 17.33 C$ C:IMG NA 6,358 NA 6,407 371 207 1.43 990 22.3 13.9 11.8 10.1 9.8 6.6 6.1 5.3 -0.4 -0.3 -0.3 -0.2Agnico-Eagle Mines Consensus NR NA 37.01 U$ U:AEM NA 6,317 NA 6,354 297 167 2.61 1,094 20.9 17.1 11.8 9.0 11.3 8.3 6.3 5.4 0.9 0.7 0.5 0.4New Gold Consensus NR NA 10.76 C$ C:NGD NA 4,845 NA 11,809 490 300 0.67 468 43.8 22.8 15.7 11.8 21.1 14.0 9.8 7.5 -1.1 -0.7 -0.5 -0.4Franco-Nevada Consensus NR NA 40.80 C$ C:FNV NA 5,509 NA n/a n/a n/a 1.50 424 76.6 36.9 26.5 23.8 27.6 15.5 12.0 11.3 -2.2 -1.3 -1.0 -0.9Osisko Consensus NR NA 11.57 C$ C:OSK NA 4,353 NA 14,772 400 336 1.22 756 nm 141.1 9.3 9.6 nm 44.5 5.7 5.5 2.1 -0.7 -0.1 -0.1

Zijin mining Consensus NR NA 3.13 K$ K:FZM NA 2,421 NA not available not available not available 0.05 2,124 11.5 10.1 8.1 6.7 2.1 1.7 1.4 1.3 0.4 0.3 0.2 0.2

Semafo Consensus NR NA 7.35 C$ C:SMF NA 1,958 NA 6,713 626 184 0.63 282 18.9 17.5 11.4 10.4 10.3 9.1 6.2 5.8 -1.2 -1.1 -0.7 -0.7

Zhaojin Consensus NR NA 12.70 K$ K:ZHAO NA 1,429 NA 2,395 199 101 0.13 651 25.2 16.4 12.6 12.6 4.8 3.3 2.5 2.4 0.5 0.4 0.3 0.3

Seabridge Gold TB Buy 3180 19.23 C$ C:SEA 69% 815 0.2 nm 17 12 -12.94 8- nm nm nm nm nm nm nm nm nm nm nm nm

South Africa

Anglo Gold Ashanti Consensus NR NA 352 R R :ANGJ NA 16,496 NA 3,940 246 80 5.84 4,507 23.2 12.0 7.4 7.3 12.4 9.2 7.2 6.9 0.6 0.4 0.2 0.2Goldfields Consensus NR NA 127 R R :GFIJ NA 11,278 NA 3,552 164 46 2.42 3,640 28.7 11.4 6.4 6.6 7.5 7.7 5.5 4.8 0.7 0.6 0.4 0.4Harmony Gold Consensus NR NA 97 R R :HARJ NA 5,127 NA 4,016 109 28 1.38 1,198 43.7 12.1 8.6 10.7 4.4 6.9 4.5 3.9 0.4 0.1 0.1 0.1

Median 6,472 301 172 25.2x 15.3x 9.9x 9.6x 10.3x 8.0x 5.8x 5.3x 0.1x 0.1x -0.1x -0.2x

Average 7,323 322 204 32.9x 21.6x 11.2x 9.6x 14.0x 9.9x 6.3x 5.3x 0.0x 0.0x -0.3x -0.2x

Nomura Precious Metals Valuation Summary 13/01/2012

P/E EV/EBITDA Net Debt / EBITDA

Nomura | European Gold Sector Initiation January 18, 2012

8

A longer-term perspective on gold Ineffective global governmental and central bank responses to the financial crisis of 2008 and the related sovereign debt crisis are causing investors to rethink some of the fundamental tenets of fiat currency systems. Associated with this, gold’s historical position of importance has the potential to re-emerge, with many important consequences for gold demand.

Gold has occupied a significant, yet constantly evolving place in the history of financial markets. Gold coins were first minted in ancient times, beginning gold’s tradition as the ultimate store of value. The use of gold coins as a mainstream currency persisted until the 16th century when significant discoveries of silver in Latin America saw a dual system develop; with gold and silver competing for use in international and domestic trade. By the early 18th century gold had re-emerged as the de facto monetary standard when Britain set a gold/silver ratio that eventually relegated silver from significant use. By the end of the 19th century most industrial countries adhered to a gold standard.

World War I and its associated pressures on government expenditures saw the gold standard end when major European countries halted the convertibility of their currencies into gold. The gold standard was generally restored in the post-war years; however, this return was short-lived, as leading economies once again suspended convertibility in order to devalue their currencies in response to the Great Depression. The US remained on a gold standard, although the 1934 Gold Reserve Act nationalised private gold holdings and devalued the gold dollar.

The end of World War II saw the implementation of what came to be known as the Bretton Woods system, a two-tiered gold-exchange system where the US dollar was backed by gold and all other currencies were pegged to the dollar. This lasted until 1971 when a combination of short-term pressures alongside the rise of German and Japanese economic power caused US president Richard Nixon to end the gold standard.

Fig. 6: 40-year gold price chart – nominal USD A bull market rally that started almost 10 years ago

Source: Datastream, Nomura research

Fig. 7: US M1 money stock and rate of change The current pace of monetary expansion in the US is near all-time highs

Source: Federal Reserve Bank of St. Louis, Nomura research

It has only been since 1971 that the world has shifted to a sustained, full-faith, fiat currency system. Between 1980 and 2000 the gold price fell as economic prosperity and contained inflation expectations led private investors, institutional investors and central banks away from gold. The 2000s saw gold demand rebound as lower interest rates and strong growth from Asian economies started a bull market that is ongoing today.

Nomura’s Quantitative Research report, Why gold is cheap in Asia, dated 16 August 2011, on why Asian nominal income growth and not US CPI has been the driver of the gold bull market. It provides a crucial perspective shift in understanding that gold has become a global commodity with global demand drivers and has been heavily influenced by Asian economic growth.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Jan-71 Jan-76 Jan-81 Jan-86 Jan-91 Jan-96 Jan-01 Jan-06 Jan-11

Go

ld p

ric

e (U

S$/o

z)

Gold Bullion LBM U$/Troy Ounce

-0.2%

-0.1%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0

500

1,000

1,500

2,000

2,500

Jan-75 Jan-80 Jan-85 Jan-90 Jan-95 Jan-00 Jan-05 Jan-10

US

M1

mon

ey s

uppl

y (U

S$bn

)

M1 Money Stock 52 wk rolling % weekly increase

The end of the Bretton Wood system in 1971 saw gold-backed currency replaced with a full faith, fiat currency system

The past 40 years have seen a fundamental shift in the nature and location of gold demand

Nomura | European Gold Sector Initiation January 18, 2012

9

Gold has moved in and out of vogue many times over the past 100 years. Figure 6 provides perspective to the drop in gold prices that occurred at the end of 2011. A price correction was arguably overdue, especially in the context of the cyclicality of certain demand segments and the above-trend price increases in mid-2011. That said, our analysis suggests that the forces that have pushed gold up by 480% in the past 10 years are still in force and could well be exacerbated over the medium term.

Gold price appreciation has increased exponentially since the market stabilisation following the initial impact of the 2008 financial crisis. Concerns around the stability of fiat monetary systems in conjunction with exceedingly high sovereign debt levels are leading investors to review alternative stores of value, increasing gold investment demand.

Gold certainly has a long and well-established pedigree when placed in the context of its historical role in financial markets. We expect this re-emergence of gold as an asset class to persist over the medium term even as the world emerges from the sovereign debt crisis and continued shifts in the global economic landscape will see further shifts in reserve currency systems.

This is likely to have important implications for the gold producers. Figure 8 shows global P/E multiples for gold equities remain remarkably constrained despite the shift in gold prices seen over the past 10 years.

Fig. 8: Global P/E for gold equities Gold equities have not followed the gold price in valuation terms

Source: Datastream

The practical constraints of re-implementing a gold standard system after the financial innovations of the past 40 years make a return to a Bretton Woods type system unrealistic, especially when we consider the gold standard’s lack of flexibility in implementing Keynesian or monetarist economic policies. However, it is important in the light of the current fragility of the world’s financial system and the ongoing paradigm shift with regard to the value of fiat currencies, to analyse gold from a broader historical perspective. This time might not be different.

In addition to the paradigm shift questioning faith in fiat currencies and longer-term shifts in world reserve currency systems; from a fundamental perspective, various longer-term trends are supportive of the gold price including:

– secular demand growth from Asia,

– a lack of flexibility in medium-term mine supply growth potential; and

– a shift in emerging market central bank attitudes toward gold as part of reserves.

0

5

10

15

20

25

30

35

40

45

Jan-92 Jul-93 Jan-95 Jul-96 Jan-98 Jul-99 Jan-01 Jul-02 Jan-04 Jul-05 Jan-07 Jul-08 Jan-10 Jul-11

12mth forward PE

We expect that the increase in the gold price since 2008 will persist

Although a return to the gold standard is unrealistic, fiat currencies are under greater scrutiny than ever before

Nomura | European Gold Sector Initiation January 18, 2012

10

Short-term volatility drivers The exogenous risks are likely to favour gold prices, as well, in the context of a limited response from near-term new mine supply. There are a number of factors that could cause gold to trade above our estimates in the short term. These include:

– the perceived threat from elevated inflation expectations from potential further quantitative easing,

– the potential for a lack of alternatives to the eurozone crisis, other than monetisation of debt European Rates Insight: A multiplicity of risk factors into 2012, and

– an increase in investor activity in an era with expected near-zero real interest rates.

The speed of the changing fundamentals within various sub-segment demand categories will no doubt add volatility to the gold price. Current weakness in the Indian rupee has seen Indian gold imports fall sharply. Financial system deleveraging can place pressure on investment demand for gold, which tends to be a larger proportion of demand than for other commodities.

Overall, our analysis suggests that the gold price remains well supported over the medium term, albeit with potentially high volatility from the demand perspective causing wide potential swings.

The gold price could see further, and more profound, spikes in the short term

Nomura | European Gold Sector Initiation January 18, 2012

11

Forecast gold prices We continue to expect increasing gold prices into 2013 as the expected supply response to the higher prices of the past few years underwhelms as compared with the positive structural changes in demand.

Nomura’s gold price forecasts remain near the upper end of the 2012 and 2013 estimate ranges. However, as we have noted above, the supply side is relatively unprepared for future unexpected demand shocks, and this could push the price much further along trend and much higher than we are forecasting in our base-case estimates.

In 2012, we expect the gold price to stabilise following the year-end 2011 sell off as gold continues to attract increased central bank demand, persisting demand growth from Asia (in value terms) and below trend scrap supply growth.

Fig. 9: Nomura long-term gold price forecasts We expect prices above 2010 levels over the longer term

Source: Bloomberg, Nomura estimates

Fig. 10: Consensus gold price forecasts There remain considerable upside risks to our forecast

Source: Bloomberg, Nomura estimates

Fig. 11: Forecast supply and demand model We expect the market to increase in size alongside the higher gold prices, but supply becomes constrained above forecast levels

Source: GFMS, Nomura estimates

0

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E

Historical Nomura forecast

Gol

d p

rice

(US$

/oz)

500

1,000

1,500

2,000

2,500

3,000

3,500

2012e 2013e 2014e 2015e

Nomura High Mean Low

Go

ldpr

ice

(US

D/o

z)

2006 2007 2008 2009 2010 2011E 2012E 2013E

Supply

Mine production 2,481 2,472 2,408 2,581 2,688 2,794 2,988 3,005Net central bank and IMF sales 365 484 235 34 0 0 0 0Scrap gold 1,133 982 1,316 1,695 1,651 1,679 1,949 2,105Hedging 0 0 0 0 0 32 0 0Implied disinvestment 0 0 58 0 0 0 0 0Total supply 3,979 3,938 4,017 4,310 4,339 4,505 4,937 5,111

Demand

Jewellery 2,300 2,423 2,304 1,814 2,035 1,969 2,049 2,037Industrial and other 657 679 718 697 767 809 817 811Net central bank and IMF demand 0 0 0 0 77 336 750 800Physical bar investment 237 244 645 531 859 1,065 953 823Hedging 434 440 350 236 180 0 25 0Implied investment 351 152 0 1,032 421 326 343 639Total Demand 3,979 3,938 4,017 4,310 4,339 4,505 4,937 5,111

The current gold price is supported by Asian secular demand, a shift in central bank attitudes to holding gold and relatively inelastic supply

Nomura | European Gold Sector Initiation January 18, 2012

12

Supply Gold is different from most commodities in the sense that the metal is not normally ‘consumed’ as it is used. Unlike a barrel of oil used in a vehicle or the wheat used to make a loaf of bread, the precious nature of gold, its durability and its store of value characteristics allow significant above ground stocks to exist. According to the World Gold Council, over 165,000 tonnes have been mined in recorded history. The vast majority of this gold is accounted for. This means that supply comes from not only from new mine production and scrap gold, but also from shifts in net demand within multiple categories of ‘consumption’.

The nature of annual global gold supplies has changed over the past decade. Net investment (new investment demand vs. previous investment sold back onto the market), was persistently positive except for a brief period following the initial onset of the financial crisis. Gold exhibits positive tail risk protection as discussed in this note from Nomura FX research Why gold is cheap in Asia.

In 2009, central banks became net buyers of gold for the first time in years, removing traditional sources of gold from the market. Central banks moving from supplying the market to buying gold is a main paradigm shift that is revisited in the demand section below. The end of the most recent IMF gold sales programme of 403 tonnes announced in 2009 has only solidified this trend.

Our analysis suggests these trends will persist over the coming years.

This leaves two main sources of gold supply in the current environment: new mine production and recycled scrap gold (gold that has been returned to the market from selling old jewellery and industrial products).

Mine production has stayed consistent over this period, accounting for 62% of total supply in 2010 as compared with 67% in 2001. Higher prices have seen scrap gold’s contribution to supply increase from 19% of total supply in 2001 to 38% of total supply in 2010 (Fig. 12).

Fig. 12: Gold supply Net central bank selling has stopped, leaving mine production and recycled scrap gold as main sources of supply

Source: GFMS, Nomura research

The ability for gold supply to meet a further demand shock appears limited.

Mine production, after falling for most of the past decade, is increasing once again. However, a lack of new, large-scale mines and the time frame required to find and develop such projects are likely to place a cap on potential new mine supply in the medium term. Higher prices are likely to drive unanticipated extensions to mine lives and this will make certain currently uneconomic resources mineable, but this on the margin, will not shift mine supply substantially in the near term, in our view.

0

1,000

2,000

3,000

4,000

5,000

6,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Mine production Scrap gold Net central bank and IMF sales Implied disinvestment Hedging

Gol

d (t)

Because it is not normally ‘consumed’, the supply of gold comes from mining, recycling and changes in net demand

Central banks are now net buyers for the first time in years

Although increasing, mining and recycling supply is unlikely to meet additional spikes in demand

Nomura | European Gold Sector Initiation January 18, 2012

13

Scrap gold supply has increased sharply on the back of the higher prices seen at the end of the last decade. However, scrap supply figures in 2010 and 2011 have been lower than expected, weakening a previously strong positive correlation between scrap supply and gold prices. This suggests a potential exhaustion of available stocks or a change in the relative utility of scrap gold from an investment perspective.

Despite the contained nature of the main supply increases, we forecast record aggregate supply levels as higher prices elicit both higher levels of mine supply and scrap material. In our view, however, the supply side from these two main categories is stretched and a supply response would be limited were one of the various demand categories to exceed projections.

Mine production Gold mine production fell steadily last decade. Excluding a late decade surge in production in 2009, production fell by an average of 1% per year during the 2000s. This lost decade was driven by the low prices at the end of the 1990s, which saw structural underinvestment in production capacity and exploration.

Fig. 13: Global new mine supply Peak gold? Production is rising again, but for how long?

Source: Brook Hunt, a Wood Mackenzie company, Nomura research

Fig. 14: Expansion capital expenditure Capital expenditure for expansions has not kept pace with the gold price

Source: Brook Hunt, a Wood Mackenzie company, Nomura research

The gold bull market starting in 2002, which has now seen prices increase by 480%, has shifted the underlying dynamics for new mine supply. The persisting higher gold prices have provided, what Brook Hunt expects to be, a new wave of production.

We have modified the costed Brook Hunt global mine supply forecasts (Fig. 13) to reflect an estimate for global production to 2018. Fig. 13 shows production peaking in 2014 at our adjusted estimate of 3,159 tonnes. It should be noted that this includes all lower probability projects and could be viewed as a best-case estimate.

Brook Hunt notes that capital expenditure for new gold mine production hit a peak of USD 8.5bn in 2008 and has since fallen (Fig. 14). We expect expansion capex to level off at USD 5bn, although we would expect this to increase in conjunction with the stronger balance sheets that are likely to build into 2012. The lack of recent near-term capex begins to feed through after 2014, when production is expected to decline back towards 2011 levels (Brook Hunt), suggesting that a structural medium-term shift in gold demand cannot be met by new gold supply alone.

There is likely to be a response to the higher gold prices that is not captured in the above estimates, and this could be significant in the longer term. High gold prices are likely to increase the economics of previously discovered, but uneconomic deposits, and the expected high margins will make smaller and less scalable operations, like the heap or dump leaching of oxide material, more economic. The other expected outcome is likely to be longer mine lives as current infrastructure is used to process previously uneconomic near-mine deposits. These trends, in conjunction with a potential boom in exploration and higher industry capital expenditure rates could potentially fill future supply gaps. However, this would be a longer-term phenomenon and is dependent on gold prices maintaining or exceeding current prices.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e

2013

e

2014

e

2015

e

2016

e

2017

e

2018

e

adj possible adj probable adj base case adj operating mines

New

Gol

d m

ine

supp

ly (t

)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Capital expenditure Gold price

Glo

bal n

ew m

ine

capi

tal e

xpen

ditu

re

Gold

price USD

/oz

Peak production is 13% higher than current levels

Capital expenditure for growth is falling despite higher gold prices

Longer-term production rates may be better than expected, but this will not alleviate expected medium-term tightness

Gold mine production is increasing after falling for most of the past decade

Nomura | European Gold Sector Initiation January 18, 2012

14

Fig. 15: Global mine production by country, 2000 Africa and North America were leaders a decade ago

Source: GFMS, Nomura research

Fig. 16: Global mine production by country, 2010 Asia and Latin America have seen the most growth

Source: GFMS, Nomura research

Geographical distribution of global gold production has stayed relatively similar on a regional basis over the past decade (Fig. 15, 16), remaining one of the most diversified commodities by production on a geographic basis. Thematically, Asia, Latin America, Russia and Africa (ex-South Africa) have seen increasing production while South Africa, the US and Australia and other developed countries have seen decreasing production (Fig. 17).

Should gold prices remain high, we would expect this trend to persist. Average cash margins for new projects are likely to provide a positive risk/reward outcome despite higher political risks. This is particularly important for the European equity market where African and CIS-based assets constitute a significant part of the assets of the London-listed gold companies.

Fig. 17: Key geographical shifts in gold production 2000-2010 Gold production is slowly shifting away from traditional producer countries.

Source: GFMS, Nomura research

Scrap gold Recycled gold (from consumer consumption, mainly jewellery) accounts for 39% of our 2012 supply expectations. Scrap gold supply has increased markedly since the onset of the 2008 crisis, and this has delivered scrap gold levels ahead of historical averages when compared with gold price changes. However, data from 2010 and 2011 has seen this relationship falter. Fig. 19 shows the relationship between annual gold price changes and aggregate levels of scrap supply. We expect these forecasts to remain below trend in the coming years.

1%

19%

14%

18%

25%

12%

11%

Europe North America Latin America Asia Africa Oceania Former Soviet Union

1%12%

20%

25%

20%

10%

12%

Europe North America Latin America Asia Africa Oceania Former Soviet Union

0

100

200

300

400

500

600

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Africa ex-South Africa South Africa ChinaUnited States Russia Latin AmericaAustralia

Gol

d pr

oduc

tion

(t)

The European gold mining equity market is skewed towards African and CIS-based assets

Nomura | European Gold Sector Initiation January 18, 2012

15

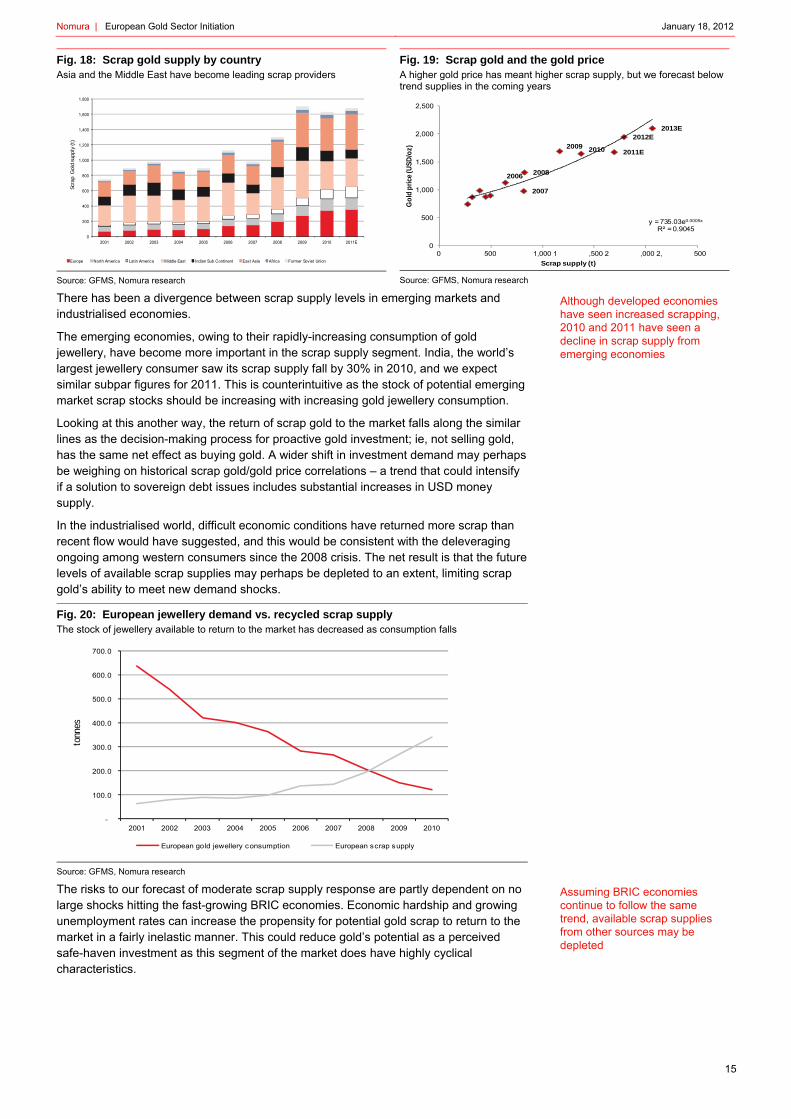

Fig. 18: Scrap gold supply by country Asia and the Middle East have become leading scrap providers

Source: GFMS, Nomura research

Fig. 19: Scrap gold and the gold price A higher gold price has meant higher scrap supply, but we forecast below trend supplies in the coming years

Source: GFMS, Nomura research

There has been a divergence between scrap supply levels in emerging markets and industrialised economies.

The emerging economies, owing to their rapidly-increasing consumption of gold jewellery, have become more important in the scrap supply segment. India, the world’s largest jewellery consumer saw its scrap supply fall by 30% in 2010, and we expect similar subpar figures for 2011. This is counterintuitive as the stock of potential emerging market scrap stocks should be increasing with increasing gold jewellery consumption.

Looking at this another way, the return of scrap gold to the market falls along the similar lines as the decision-making process for proactive gold investment; ie, not selling gold, has the same net effect as buying gold. A wider shift in investment demand may perhaps be weighing on historical scrap gold/gold price correlations – a trend that could intensify if a solution to sovereign debt issues includes substantial increases in USD money supply.

In the industrialised world, difficult economic conditions have returned more scrap than recent flow would have suggested, and this would be consistent with the deleveraging ongoing among western consumers since the 2008 crisis. The net result is that the future levels of available scrap supplies may perhaps be depleted to an extent, limiting scrap gold’s ability to meet new demand shocks.

Fig. 20: European jewellery demand vs. recycled scrap supply The stock of jewellery available to return to the market has decreased as consumption falls

Source: GFMS, Nomura research

The risks to our forecast of moderate scrap supply response are partly dependent on no large shocks hitting the fast-growing BRIC economies. Economic hardship and growing unemployment rates can increase the propensity for potential gold scrap to return to the market in a fairly inelastic manner. This could reduce gold’s potential as a perceived safe-haven investment as this segment of the market does have highly cyclical characteristics.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E

Europe North America Latin America Middle East Indian Sub Continent East Asia Africa Former Soviet Union

Scra

p G

old

supp

ly(t

)

2006

2007

2008

2009 2010 2011E

2012E2013E

y = 735.03e0.0005x

R² = 0.9045

0

500

1,000

1,500

2,000

2,500

0 500 1,000 1 ,500 2 ,000 2, 500

Go

ld p

rice

(US

D/o

z)

Scrap supply (t)

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

European gold jewellery consumption European scrap supply

tonn

es

Although developed economies have seen increased scrapping, 2010 and 2011 have seen a decline in scrap supply from emerging economies

Assuming BRIC economies continue to follow the same trend, available scrap supplies from other sources may be depleted

Nomura | European Gold Sector Initiation January 18, 2012

16

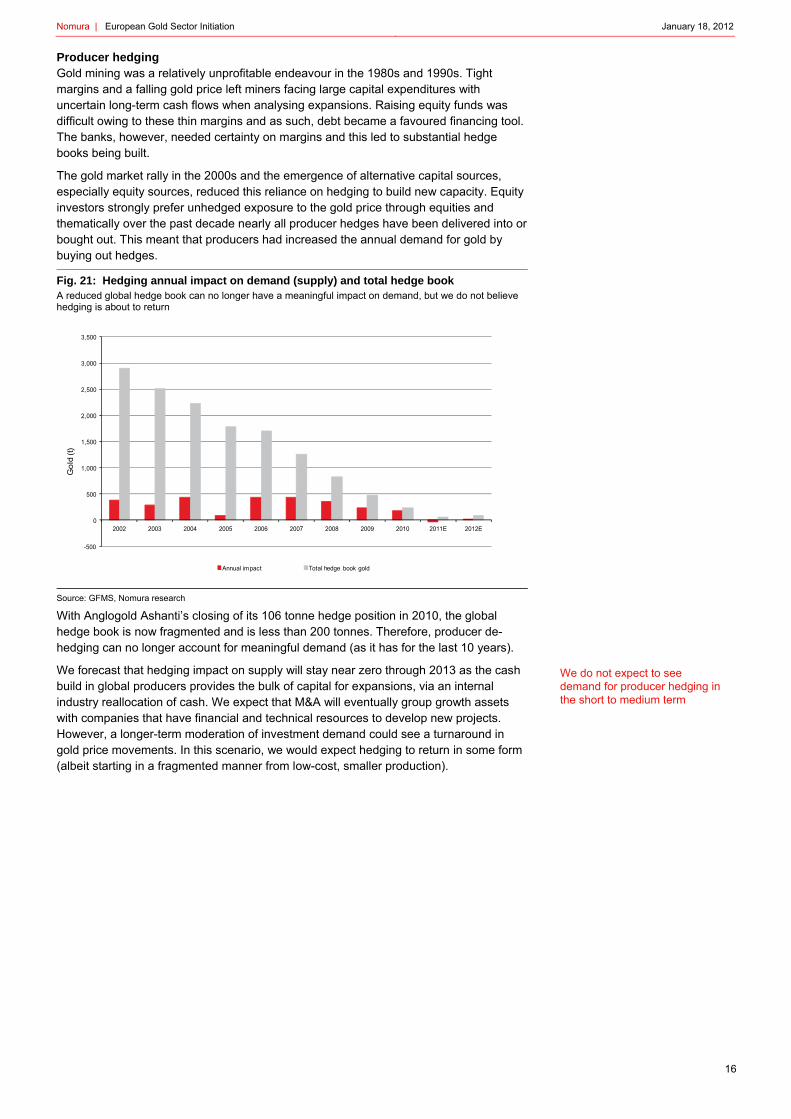

Producer hedging Gold mining was a relatively unprofitable endeavour in the 1980s and 1990s. Tight margins and a falling gold price left miners facing large capital expenditures with uncertain long-term cash flows when analysing expansions. Raising equity funds was difficult owing to these thin margins and as such, debt became a favoured financing tool. The banks, however, needed certainty on margins and this led to substantial hedge books being built.

The gold market rally in the 2000s and the emergence of alternative capital sources, especially equity sources, reduced this reliance on hedging to build new capacity. Equity investors strongly prefer unhedged exposure to the gold price through equities and thematically over the past decade nearly all producer hedges have been delivered into or bought out. This meant that producers had increased the annual demand for gold by buying out hedges.

Fig. 21: Hedging annual impact on demand (supply) and total hedge book A reduced global hedge book can no longer have a meaningful impact on demand, but we do not believe hedging is about to return

Source: GFMS, Nomura research

With Anglogold Ashanti’s closing of its 106 tonne hedge position in 2010, the global hedge book is now fragmented and is less than 200 tonnes. Therefore, producer de-hedging can no longer account for meaningful demand (as it has for the last 10 years).

We forecast that hedging impact on supply will stay near zero through 2013 as the cash build in global producers provides the bulk of capital for expansions, via an internal industry reallocation of cash. We expect that M&A will eventually group growth assets with companies that have financial and technical resources to develop new projects. However, a longer-term moderation of investment demand could see a turnaround in gold price movements. In this scenario, we would expect hedging to return in some form (albeit starting in a fragmented manner from low-cost, smaller production).

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E

Annual impact Total hedge book gold

Gol

d(t)

We do not expect to see demand for producer hedging in the short to medium term

Nomura | European Gold Sector Initiation January 18, 2012

17

Demand Gold demand has increased considerably over the past 10 years in value terms. The market has grown from USD 34bn in 2001 to an estimated USD 240bn in 2011. In total tonnes, however, this growth has been less pronounced; annual gold demand by volume had actually stayed flat until 2009.

Our analysis suggests that demand in total volume terms will meet higher supply resulting from higher prices. Although we forecast there will be more material on the market, on balance, the main demand drivers and their exposure to further exogenous shocks, should leave the price well supported, in our view.

Traditional sources of demand are jewellery, industrial demand (electronics, dental, among others), and physical bar investment. A key change to the market has been the emergence of net central bank buying. Emerging market central banks have been net purchasers of gold since 2008, and the lack of desire to further erode the capital base of central banks have seen sales through the CBGA agreement (Europe) come to an end for the time being. This, in conjunction with a stronger implied investment category, may well push the demand side out of balance with the supply side, resulting in higher prices.

Fig. 22: Segmental gold demand in volume terms The aggregate level of gold demand has stayed constant, but has seen shifts towards investment demand

Source: GFMS, Nomura estimates

Fig. 23: Segmental gold demand in value terms A weaker USD has contributed to the value uplift

Source: GFMS, Nomura estimates

As gold is priced in US dollar terms, a weaker US dollar (as seen at the start of last the decade) helped to kick-start the gold rally. Since 2008, however, this relationship has broken down somewhat. Although there are insufficient data points for true statistical evidence, the charts below show that this relationship has directionally weakened as the R² in the past 16 quarters is lower than the negative correlation between 2000 and 2008. Notably, in recent periods, only two quarters in the past 10 quarters in which the dollar has strengthened, has the gold price declined (this includes Q4 2011 when the gold price saw its most recent correction).

Fig. 24: Gold vs. DXY 1980-2011

Source: Bloomberg

Fig. 25: Gold vs. DXY 2000-2008

Source: Bloomberg

Fig. 26: Gold vs. DXY 2008-2011

Source: Bloomberg

0

1,000

2,000

3,000

4,000

5,000

6,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Jewellery Industrial and otherPhysical bar investment Net central bank and IMF demandHedging Implied investment

70

75

80

85

90

95

100

105

110

115

1200

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Jewellery Industrial and otherPhysical bar investment Net central bank and IMF demandHedging Implied investment

Gol

dde

man

d (U

SD

bn) D

XY (inverted)

y = -0.6363x + 0.0106R² = 0.1848

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0%

Go

ld p

rice c

hn

ag

e

DXY (USD/oz)

y = -0.6852x + 0.0299R² = 0.227

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0%

Go

ld p

rice c

hn

ag

e

DXY (USD/oz)

y = -0.2227x + 0.0421R² = 0.0529

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-10.0% -5.0% 0.0% 5.0% 10.0% 15.0%Go

ld p

rice c

hn

ag

e

DXY (USD/oz)

We believe that the current gold price is well supported by demand

Nomura | European Gold Sector Initiation January 18, 2012

18

Perhaps more importantly for gold demand (especially for gold demand for investment purposes), is that real interest rates are expected by Nomura to stay low over the next two years. Fig. 27 presents Nomura’s main interest rate forecasts to 2014. A traditional drawback to gold as an investment is the lack of yield that it provides. In times of higher interest rates (but stabilised inflation expectations) gold performs poorly owing to its lack of yield. In the near term, the dovish monetary policy stance of most global central banks and below-trend growth expectations should allow the general investment climate for gold to stay relatively positive over the next two years.

Fig. 27: Real interest rates in major economies With the exception of China, real interest rates are forecast by Nomura to stay negative through 2013

Source: Datastream, Nomura research

Jewellery The gold jewellery market is perhaps the most sensitive demand subsector to higher gold prices. In volume terms, we expect demand from India and East Asia to stay relatively level over the next three years as higher prices erode total volume demand (Fig. 28). In dollar value terms, however, we expect both regions to continue along the path of structural growth (India has averaged 26% annual increases since 2003, China 31%), with the caveat that the uncertain economic environment may provide short-term volatility in the growth rates.

Fig. 28: Gold jewellery demand in total tonnage terms Higher prices are reducing gold demand on a volume basis

Source: GFMS, Nomura research

Fig. 29: Gold jewellery demand in USD billion Gold jewellery demand in dollar terms continues to be driven by India and China

Source: GFMS, Nomura research

Our gold jewellery forecasts are based on an extrapolation of demand trends over the past 10 years and then modified to account for Nomura estimates for individual country GDP growth rates. What this does not allow for, however, is for our model to capture significant shifts in sub-segment specific demand trends. Gold imports into China from Hong Kong in recent months have risen well past trend levels according to the Census and Statistics department of Hong Kong. Media reports suggest that this is attributable to a diversion of funds from the volatile property market or perhaps even PBOC buying. The jewellery purchase decision can be tilted towards investment in an emerging middle class and this could help to keep demand well supported if a wider positive shift in investment demand is to occur owing to other global factors.

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2006 2007 2008 2009 2010 2011 2012E 2013E

US UK ECB China India

0

100

200

300

400

500

600

700

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Go

ld je

wellery

dem

an

d (t)

Europe North America Latin America Middle East Indian Sub Continent China

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Jew

ellery

dem

an

d (U

S$ b

n)

Europe North America Latin America Middle East Indian Sub Continent China

Low real interest rates will likely support the attractiveness of gold as an investment

Gold jewellery demand is largely driven by India and China

Nomura | European Gold Sector Initiation January 18, 2012

19

Fig. 30: China imports of gold from Hong Kong There has been a recent spike in the import of gold from Hong Kong into China

Source: Census and statistics department of Hong Kong, Nomura research

We do expect there to be volatility along this structural demand growth path. The Bombay Bullion Association has reported that Q4 2011 gold imports into India fell by 125 tonnes or 56% y-o-y. The strong Indian Rupee has caused record gold prices in local terms. The slowing Indian economy, falling inflation and the resultant increase in real interest rates is likely to have contributed to this shift in imports. These trends could continue into 2012 (and could perhaps extend through other emerging economies). However, the total of 878 tonnes of gold imported in 2011, although down 9% y-o-y, is still much higher than the 559 tonnes in 2009, especially when factoring in the 61% increase in average gold prices. It should also be noted that shifts in fundamental demand sub-categories, especially the cyclically exposed jewellery and industrial categories, can cause the various investment categories to experience volatility. This can cause near-term expectations on price to vary; however, in our view, despite the softer Q4 imports, the longer-term global wealth transfer towards emerging markets, like India, is likely to continue.

Central bank buying Gold has traditionally held an important place within the balance sheets of central banks. In the late 1990s, however, as gold prices reached their lows, many of the industrialised world’s central banks were reducing their gold holdings. Following a group of unannounced sales by various central banks, and then the announcement by the UK that it would sell the majority of its gold reserves, The Washington Agreement on Gold was signed in 1999 between the US, the IMF, the eurozone, Switzerland and Sweden (CBGA).

Fig. 31: Top central bank gold holdings The gold held in the central banks is mainly held by US and Europe

Source: World Gold Council

800

1000

1200

1400

1600

1800

2000

0

20

40

60

80

100

120Se

p-09

Oct-0

9

Nov-

09

Dec-

09

Jan-

10

Feb-

10

Mar

-10

Apr-1

0

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct-1

0

Nov-

10

Dec-

10

Jan-

11

Feb-

11

Mar

-11

Apr-1

1

May

-11

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Oct-1

1

Nov-

11

Imports (000 kg) Gold price ($/oz)

000

kg

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Top 10 holders of gold

tonn

es

Central banks are now net buyers of gold for the first time in years

Nomura | European Gold Sector Initiation January 18, 2012

20

The CBGA was agreed to manage the sales of gold from central banks to mitigate the risk of large price impacts on remaining gold reserves, hence ensuring greater stability in the international financial system. The agreement set out the total tonnage that was allowed to be sold by signatories over a set period, initially 400 tonnes per year for five years. The agreement stated that gold “will remain an important element of global monetary reserves”. Notably, this took the form of a “gentlemen’s agreement” and is not subject to international treaties. Through the past 10 years, and via a second and now a third Washington agreement, a steady level of signatory selling occurred. The price impact on gold was generally limited as was borne out by increasing prices in the 2000s.

Net central bank selling has now become net central bank buying. This shift is important and its impact on the overall market dynamic should not be overlooked, in our view.

European sales under the CBGA 3 (mid-September 2009-2011) have amounted to 12 tonnes as the eurozone sovereign debt crisis has hamstrung central banks from eroding their balance sheets further. The end of the IMF’s sale of 400 tonnes of gold in November 2010 has also removed a source of supply, further shifting the aggregate central banks category towards demand.

Fig. 32: Net central bank selling Our forecasts suggest that central banks will become key buyers of gold in the coming years

Source: World Gold Council, Nomura estimates

There is a general divergence between the levels of gold held by central banks in developed and emerging markets. Developed countries’ central banks tend to hold gold from an era where reserves were held both in US dollar and in gold (prior to the end of the gold standard). Emerging economies by contrast have largely generated their reserves over the past 40 years in the modern US dollar reserve currency system (and notably post gold standard). EM central banks have far lower gold holdings as a percentage of total US dollar reserves (c.5%).

Recent data suggest that emerging market economies are increasing their asset allocation of reserves to gold. Fig. 33 provides the notable net changes in 2011 led by Mexico, Russia and Thailand.

Fig. 33: 2011 changes in gold holdings Multiple emerging market central banks have been buying significant amounts of gold

Source: World Gold Council Nov. estimates

-1,000

-800

-600

-400

-200

0

200

400

600

800

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Net central bank selling

Gol

d(t)

-40

-20

0

20

40

60

80

100

120

Mex

ico

Rus

sia

Thai

land

Kore

a

Boliv

ia

Oth

er

Tajik

ista

n

Col

umbi

a

Sri L

anka

Philip

pine

s

Net purchases (tonnes)

Emerging market economies are increasingly looking to diversify their reserves by buying gold

Nomura | European Gold Sector Initiation January 18, 2012

21

The recent bilateral currency agreement between China and Japan, which will promote direct yuan-yen trade and will see Japan hold yuan in its foreign currency reserves for the first time highlights the emergence of potential alternatives to the US dollar in regards to its status as a global reserve currency. In our view, the longer-term uncertainty in regards to how this will develop as emerging markets continue to grow (according to The Economist, China is likely to eclipse US GDP by 2018), will see gold’s re-emergence as an international reserve persist.

To illustrate the potential impact of this shift in sentiment on the gold market, we have run a scenario analysis that shows total demand for gold would be approximately 3,400 tonnes (total demand in FY11E is 4,505), if the 18 largest non-US/EU US dollar reserve holders moved their allocation of gold to 10% of total reserves (note this is ex-China).

Fig. 34: Scenario analysis to increase gold holdings to 10% allocation Significant purchases could come from multiple buyers

Source: World Gold Council

Notably, we have not included China in this scenario analysis. China is relatively unlikely to shift from its current 1.7% gold allocation in a straightforward manner as this would signal a lack of faith in its remaining USD 3.3trn in US dollar reserves. Were China to merely maintain its 1.7% allocation in future years, based on the recent growth rates of its reserves, China would need to purchase approximately 160 tonnes of gold a year. Were China to increase its gold holdings to 10%, it would be required to purchase 5,146 tonnes of gold, or 113% of total global estimated annual demand.

The non-China, 3,400 tonnes of gold to be purchased amounts to 75% of a year’s demand (based on 2011E demand levels). Should a potential shift in gold asset allocation levels occur in a rapid and unstructured manner, (ie, in the form of a shock to the US dollar as a reserve, for instance), the buying would likely come from multiple countries all looking to protect the value of its existing reserve position. In such a scenario, the gold price would respond considerably, in our view. This aspect enhances the tail risk protection of gold to counter potential US dollar stability concerns.

We are including under 25% of the above demand estimates (ex-China) for our global net demand estimates for 2012 and 2013, and hence the risks to this demand category, in our view, remains to the upside. The timing or rapidity of these changes is unknowable at present, especially given the instability in the current market environment.

Net investment demand The remaining gold demand consists of investment in physical bars and a range of alternative products, including exchange traded funds (ETFs), medals and imitation coins, and other financial products.

In the 40 years since the dissolution of the Bretton Woods system and its fixed price, the geographical spread of gold demand has undergone a profound shift. In 1970, North America and Europe accounted for 47% of the overall market (rising to 68% in 1980), this has now fallen to 27%, with the Indian subcontinent and East Asia picking up the majority of the balance (58% in 2010 vs. 35% in 1970).

0

100

200

300

400

500

600

700

800

900

Current holdings Implied increase

Gold demand has shifted east over the past 40 years and is now weighted towards the Indian subcontinent and East Asia

Nomura | European Gold Sector Initiation January 18, 2012

22

Fig. 35: Total gold demand is geographically diverse (2010) Western investment demand is now below 50% of total

Source: World Gold Council, Nomura research

Fig. 36: Demand for physical investment in gold (2010) India and China constitute 52% of demand for physical investment in gold

Source: World Gold Council, Nomura research

Physical investment Rising income levels in emerging markets – in particular in India and East Asia – have fuelled growth in demand for physical investment in gold (jewellery, bars, coins and medals). In two of the fast-growing economies, India and China, gold is regarded as a sign of prosperity and an integral part of religious ceremony, weddings and other holidays (for example, the WGC has identified the Chinese New Year, the onset of Diwali in October and weddings as typical occasions for gold purchasing). In the charts below, we attempt to quantify this cultural affinity with gold in some developing markets, by showing how a number of these countries have exhibited much higher gold consumption than their GDP per capita would suggest. In 2009, for instance, demand for gold per capita in China and India was roughly comparable with much more prosperous nations, such as the UK.

Despite rising gold prices, this trend has actually accentuated in recent years with Indian gold demand per capita rising from 0.49gm in 2009 to 0.82gm in 2010 to now account for 32% of the physical investment market (although this trend began to stall somewhat in Q4 11). And in Q3 11, with global physical investment demand in tonnes stalling (overall dollar demand continued to grow), two of the three markets that bucked this trend and continued to grow were developing markets: China and Russia.

Fig. 37: 2009: GDP per capita (USD) vs. demand per capita (mg) Demand for gold per capita in China and India was roughly comparable with much more prosperous nations, such as the UK

Source: World Gold Council, World Bank

Fig. 38: 2010: GDP per capita (USD) vs. demand per capita (mg) Indian demand per capita almost doubled in 2010. Demand in China and Russia also increased

Source: World Gold Council, World Bank

Note: Demand includes all physical investment (including jewellery, but excluding the actions of central banks).

The regional dispersion of physical investment demand, its relative reweighting towards ‘gold-friendly’ emerging markets and growth despite rising prices support our assumption that gold demand from physical investment will remain at or slightly below recent historical levels despite continuing price pressure. Ongoing demand from developing markets would constitute upside to this forecast; for instance, if Chinese consumption continued to trend upwards and increase to the 0.82gm seen in India, this would imply additional gold demand of 500 tonnes per annum.

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

Invest Jewellery Tech

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

India Greater China

Other Europe ex CIS

US Middle East

Turkey Vietnam Russia Thailand

IndiaChinaThailand

Indonesia

Russia

United Kingdom Italy

US

South Korea

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

-0.10 - 0.10 0 .20 0. 30 0.40 0. 50 0.60 0. 70 0.80 0. 90 1. 00

IndiaChina Thailand

Indonesia

Russia

United KingdomItaly

US

South Korea

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

- 0.10 0.20 0 .30 0. 40 0.50 0 .60 0. 70 0.80 0 .90

Many of the countries with the fastest-growing economies have a strong cultural affinity with gold

We believe that physical investment demand will fall slightly from recent yearly highs. Ongoing demand from developing nations is a source of potential upside to this forecast

Recent years have also seen a rise in the purchase of gold for investment purposes in these markets; in 2010, annual bar and coin demand increased by 60% in India and 72% in China

Nomura | European Gold Sector Initiation January 18, 2012

23

Alternative investment The vast majority of alternative investments relate to ETFs (c. 350 tonnes in 2010). Launched in 2003, the number of available funds and their holdings has increased rapidly as investors have sought exposure to fluctuations in the gold price through these equity vehicles.