No Slide Titlelibrary.corporate-ir.net/library/93/938/93866/items/147732/CHRT_1Q... · 22 April...

21

Investor Update April 22, 2005 Singapore

Transcript of No Slide Titlelibrary.corporate-ir.net/library/93/938/93866/items/147732/CHRT_1Q... · 22 April...

Investor Update

April 22, 2005Singapore

22 April 2005

Safe Harbor StatementThis presentation contains forward-looking statements, as defined in the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements, including without limitation, statements relating to our growth and profitability strategy; our ability to win first source business; revitalization of our manufacturing base to reduce the cost structure; the doubling of our 0.13 micron and below capacity with 300 mm commencing production in mid-2005; the implementation of a “borderless fab”; our plans to improve cost structure and reduce breakeven utilization to 75% by end 2005; our position with respect to advanced technology, acceleration of our technology migration and closing of our technology gap; the Chartered-IBM technology platform becoming the preferred solution at 90-nm and beyond; Fab 7's production schedule, our process roadmap; our open EDA/IP approach; our plans on utilization of mature capacity and plans for establishment of a manufacturing presence in China; the increase in our advanced capacity; our guidance on revenue (including the our share of SMP), net loss, ASP and utilization for second quarter of 2005; our projected 2005 financial and liquidity position, the cash flow from operations, available credit facilities, capital expenditures and target cash balance at the end of December 2005 and the projected 2005 depreciation and amortization reflect our current views with respect to future events and financial performance and are subject to certain risks and uncertainties, which could cause actual results to differ materially from historical results or those anticipated. Among the factors that could cause actual results to differ materially are: changes in market outlook and trends, specifically in the foundry services and communications and computer markets; demands from our major customers, excess inventory and life cycles of specific products; competition from other foundries; unforeseen delays or interruptions in our plans for our fabrication facilities; the performance level of and technology mix in our fabrication facilities; our progress on leading edge products; the successful implementation of our partnership, technology and supply alliances; the timing and rate of the semiconductor market recovery; economic conditions in the United States as well as globally and the growth rate of fabless companies and the outsourcing strategy of integrated device manufacturers. Although we believe the expectations reflected in such forward-looking statements are based upon reasonable assumptions, we can give no assurance that our expectations will be attained. In addition to the foregoing factors, a description of certain other risks and uncertainties which could cause actual results to differ materially can be found in the section captioned "Risk Factors" in our Annual Report on Form 20-F filed with the U.S. Securities and Exchange Commission. You are cautioned not to place undue reliance on these forward-looking statements, which are based on the current view of management on future events. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

22 April 2005

CharteredFocused on Growth and Profitability

Leveraging recent gains in advanced technology; partnering with IBM to place Chartered at forefront of technology

Creating opportunity for major “first source” wins

Higher growth; enhanced margins; better diversification

Revitalizing manufacturing base; reducing cost structure

Targeting to double 0.13-micron and below capacity from 2004 to 2005, with 300mm commencing production in mid 2005

Implementing “borderless fab” approach

Intensifying actions to improve cost structure and reduce break-even utilization to 75% by end 2005

Capture advanced technology market opportunity; reduce cost; increase flexibility

22 April 2005

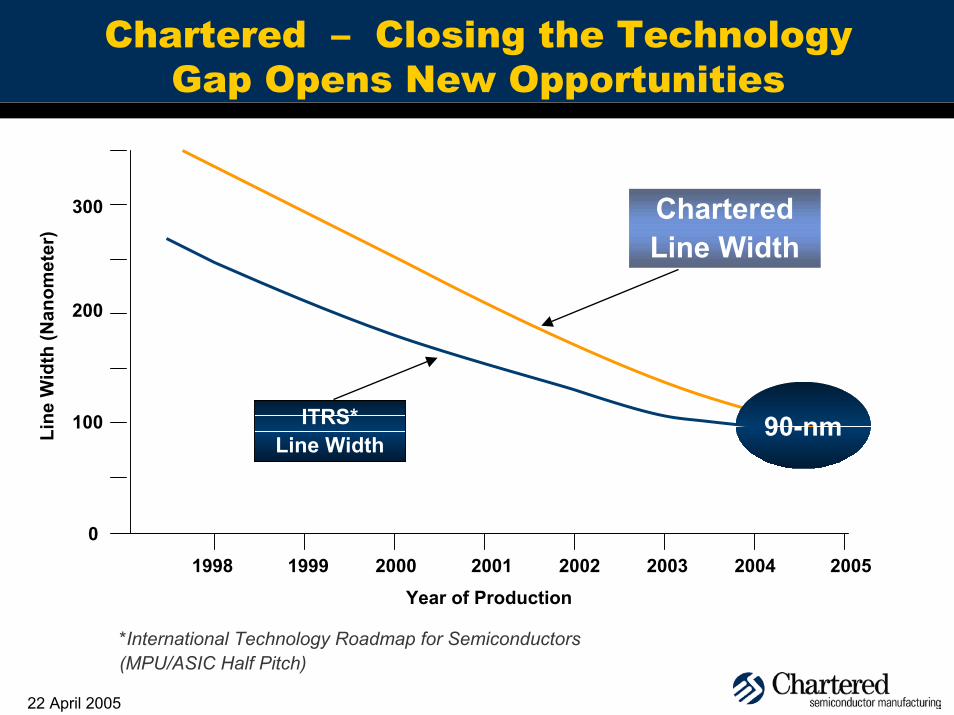

Chartered – Closing the Technology Gap Opens New Opportunities

90-nm

Chartered Line Width

300

Line

Wid

th (N

anom

eter

)

200

ITRS* Line Width

100

01998 1999 2000 2001 2002 2003 2004 2005

Year of Production

*International Technology Roadmap for Semiconductors(MPU/ASIC Half Pitch)

22 April 2005

Accelerating Technology Migration

Technology accelerationAdvancing at the most rapid pace in our history- 2 to 3 quarters at 0.13um vs 10 quarters at 0.25um

CHRT-IBM technology platform is now the preferred alternative industry platform at 90-nm node and beyond- Infineon and Samsung joined development team at 65-nm- Recently announced cross-foundry design enablement is an

industry firstLogic, mixed-signal, RF CMOS, BiCMOS, SiGe, embedded memory

Expanding market reachNew customers, new end markets, better diversification

300mm Fab 7 underwayEntered into pilot production at end-2004Starting commercial shipment in July 2005

22 April 2005

Rapidly Increasing Leading-edge ShipmentsRevenue by Technology

17%

22%

16%

20%

13%

12%

11%

24%

19%

21%

8%

17%

13%

28%

20%

18%

5%

16%

18%

26%

11%

17%

3%

25%

3%11%

21%

11%

18%

4%

32%

1Q04 2Q04 3Q04 4Q04 1Q05

Up to 0.25um

Up to 0.35um

Above 0.35um

Note: Includes Chartered’s share of minority-owned joint-venture SMP (Fab 5)

*Includes revenues from services related to generation of customers’ mask sets

Up to 0.18um

32% 0.13um

$63M$34M

Other*

Up to 0.15um

0.13-micron revenues up 1.8X

22 April 2005

CHRT-IBM Technology PlatformMomentum Building Rapidly

Industry’s first cross-foundry design enablement announced – Artisan and Virage join as partners

First customer announcement – 90nm SOI

4Q02

3Q034Q03

1Q042Q04

Cadence,Magma,Mentor & Synopsys join design enablement platform

CHRT-IBM extend joint development to 45nmcovering 3 generations of advanced process tech

CHRT-IBM-IFX-Samsung jointly developed 65nm design manual and SPICE models available for both base and low-power processes

1Q05

4Q04

3Q04Samsung joins joint development at 65-nm

Infineon joins joint development at 65-nm Fab 7 – begin equipment move-in

Customer discussions begin CHRT-AMD sourcing and

manufacturing technology agreements announced2Q03

1Q03

CHRT-IBM joint development (90 & 65nm) and reciprocal mfg agreement announced

Customer-focused approach is setting a new standard for foundry compatibility, design portability and sourcing flexibility

22 April 2005

AMD / Chartered Sourcing Agreement

AMD and Chartered sign sourcing and manufacturing technology agreements

Chartered to manufacture AMD64 microprocessors beginning 2006

AMD chooses Chartered for leading-edge manufacturingcapabilities

Chartered adopts AMD’s Automated Precision Manufacturing

Chartered has adopted portions of AMD’s yield-enhancement technology for implementation in Fab 7

Chartered is the only independent foundry to be offering90nm SOI production

22 April 2005

Chartered Process Roadmap

90nm

65nm

Low-K 300mm

Low-K 300mm

90nm

65nm

Low-K 300mm

Low-K 300mm

90nm

65nmLow-K

300mmLow-K 300mm

90nm Low-K

300mm

0.18um 20V

Core Logic

High Speed

Low Power

Mixed Signal/ RF CMOS

HV CMOS

2004

Note: Center of circle indicates pilot production

2005 2006

22 April 2005

Chartered Open EDA/IP Approach

Industry backgroundStarting at 0.18-um node and including 0.13-um and 90-nm, many foundries have design rule compatible baseline logic processes

Customers prefer open EDA/IP approachDesign portability – choice and flexibility in bringing design to foundry of choice; flexibility to move or second source

Chartered solutionProvide easy access to robust third-party network of pre-qualified EDA, IP and design services solutionsTake leadership role in advocating an open, standards-based approach with industry organizations and commercial consortiums

22 April 2005

Access to Complete Design Solutions

Chartered

Design Tools

LibrarySolutions

IPSolutions

Design Services

22 April 2005

Utilization of Mature Capacity

Targeting niche technology markets, leveraging Chartered’s mixed signal and RF CMOS strength

Example end products:SmartCards RFID TagsDisplay driversPower Mgt for Mobile Products

Targeting strategic partnerships for volume production

Working toward establishing manufacturing presence in China

22 April 2005

Revitalizing Capacity BaseIncreasing Advanced Capacity

Note: Includes Chartered’s share of minority-owned joint-venture SMP (Fab 5)

K 8” Equivalent Wafers 2003 2004 2005E

0.13um

90nm

170

3571250 1289

1475

2003 2004 2005E

Total Capacity

71

Up 110%

Advanced CapacityUp 5.0X from 2003 to 2005

22 April 2005

Woodlands Campus

Fab 6Chartered Silicon

Partners (CSP)

Fab 6Chartered Silicon

Partners (CSP)

Fab 2

Fab 7Fab 7

CharteredReserved Land

Fab 2

CharteredReserved Land

Fab 5Silicon Manufacturing

Partners (SMP)

Fab 5Silicon Manufacturing

Partners (SMP)

Fab 3Fab 3

22 April 2005

Quarterly Financials(US$M)

Revenue Net Income / Cash FlowTotal Business Base*

5549

14

229256 257 191 181

15

52

1.9 15.3 16.2

(85)

(27)

87829793

60

Net Income Cash Flow from Operations

284

*Includes Chartered’s share of minority-owned joint-venture SMP (Fab 5)

1Q04 2Q04 3Q04 4Q04 1Q05

306308

205

1Q04 2Q04 3Q04 4Q04 1Q05

196

SMPChartered

22 April 2005

2Q05 Outlook

*Includes Chartered’s share of minority-owned joint-venture SMP (Fab 5)**Includes loss impact due to CSP accounting treatment $17.2M in 1Q05 and projected to be $21.5M in 2Q05

-$(6.0)M, +/- $4M$(9.7)MGross profit (loss)

$(0.33), +/- $0.02

$(83.0)M, +/- $5M

65%, +/- 2%

$943, +/- $25

$915, +/- $20

$215.0M, +/- $5M

$193.0M, +/- $4M

22 Apr GuidanceMidpoint and Range

-

-

-

Down 5% to 10%

Down 6% to 10%

Up 7% to 12%

Up 4% to 9%

SequentialChange

$(84.5)MNet income (loss)**

$(0.34) Earnings (loss) per ADS

59%Utilization

$1,019ASP including Chartered’s share of SMP*

$996ASP

$196.1MRevenues including Chartered’s share of SMP*

$181.4MRevenues

1Q 2005Actual

2Q 2005

22 April 2005

Liquidity PositionSources & Uses – 2Q05 to 4Q05

Sources: (US$M) Uses: (US$M)

Opening Cash Balance $656(April 1, 2005)

Net Capacity Deposits 35and Other

Credit Facilities* 452

Derived Cash Flow 200from Operations**

Total $1,343

Cap Ex $546

Debt Repayments 297

Target Cash Balance 500(Dec 31, 2005)

Total $1,343

* Additional US$329M available and planned for use beyond 2005, bringing total credit facilities to US$781M

** Depreciation and Amortization for 2Q05 to 4Q05 expected to be US$409M

22 April 2005

CharteredFocused on Growth and Profitability

Leveraging recent gains in advanced technology; partnering with IBM to place Chartered at forefront of technology

Creating opportunity for major “first source” wins

Higher growth; enhanced margins; better diversification

Revitalizing manufacturing base; reducing cost structure

Targeting to double 0.13-micron and below capacity from 2004 to 2005, with 300mm commencing production in mid 2005

Implementing “borderless fab” approach

Intensifying actions to improve cost structure and reduce the break-even utilization to 75% by end 2005

Capture advanced technology market opportunity; reduce cost; increase flexibility

22 April 2005

Reconciliation Table

In order to provide investors additional information regarding the company’s financial results as determined in accordance with US GAAP, Chartered also provides information on its total business base revenues, which include the Company’s share of Silicon Manufacturing Partners (“Revenues including Chartered’s share of SMP”). SMP is a minority-owned joint-venture company and under US GAAP reporting, SMP revenues are not consolidated into Chartered’s revenues (“Revenues”). References to revenues including Chartered’s share of SMP are therefore not in accordance with US GAAP. To ensure clarity, the tables below provide a reconciliation.

(US$M) 1Q04 2Q04 3Q04 4Q04 1Q05Revenue 228.4 255.8 257.3 190.6 181.4CHRT share of SMP Revenue 55.3 52.3 49.2 14.1 14.7Revenue with CHRT share of SMP 283.7 308.1 306.5 204.7 196.1

22 April 2005

US GAAP Reconciliation TableBreakdown by Technology (micron)

Revenues (US GAAP) Percentage of Total 1Q 2004 2Q 2004 3Q 2004 4Q 2004 1Q 2005 0.13 and below 15% 18% 17% 27% 33% Up to 0.15 0% 0% 0% 0% 0% Up to 0.18 17% 18% 13% 15% 17% Up to 0.25 20% 21% 21% 11% 12% Up to 0.35 27% 30% 33% 28% 22% Above 0.35 21% 13% 16% 19% 13% Other* - - - - 3% Total 100% 100% 100% 100% 100% Chartered’s share of SMP Revenues Percentage of Total 1Q 2004 2Q 2004 3Q 2004 4Q 2004 1Q 2005 0.13 and below 2% 8% 9% 3% 10% Up to 0.15 67% 48% 34% 39% 53% Up to 0.18 30% 35% 42% 56% 37% Up to 0.25 1% 9% 15% 2% 0% Up to 0.35 0% 0% 0% 0% 0% Above 0.35 0% 0% 0% 0% 0% Total 100% 100% 100% 100% 100% Revenues including Chartered’s share of SMP Percentage of Total 1Q 2004 2Q 2004 3Q 2004 4Q 2004 1Q 2005 0.13 and below 12% 17% 16% 25% 32% Up to 0.15 13% 8% 5% 3% 4% Up to 0.18 20% 21% 18% 17% 18% Up to 0.25 16% 19% 20% 11% 11% Up to 0.35 22% 24% 28% 26% 21% Above 0.35 17% 11% 13% 18% 11% Other* - - - - 3% Total 100% 100% 100% 100% 100% * Includes revenues from services related to generation of customers’ mask sets