NN AAPL 130122 A For Apple

34

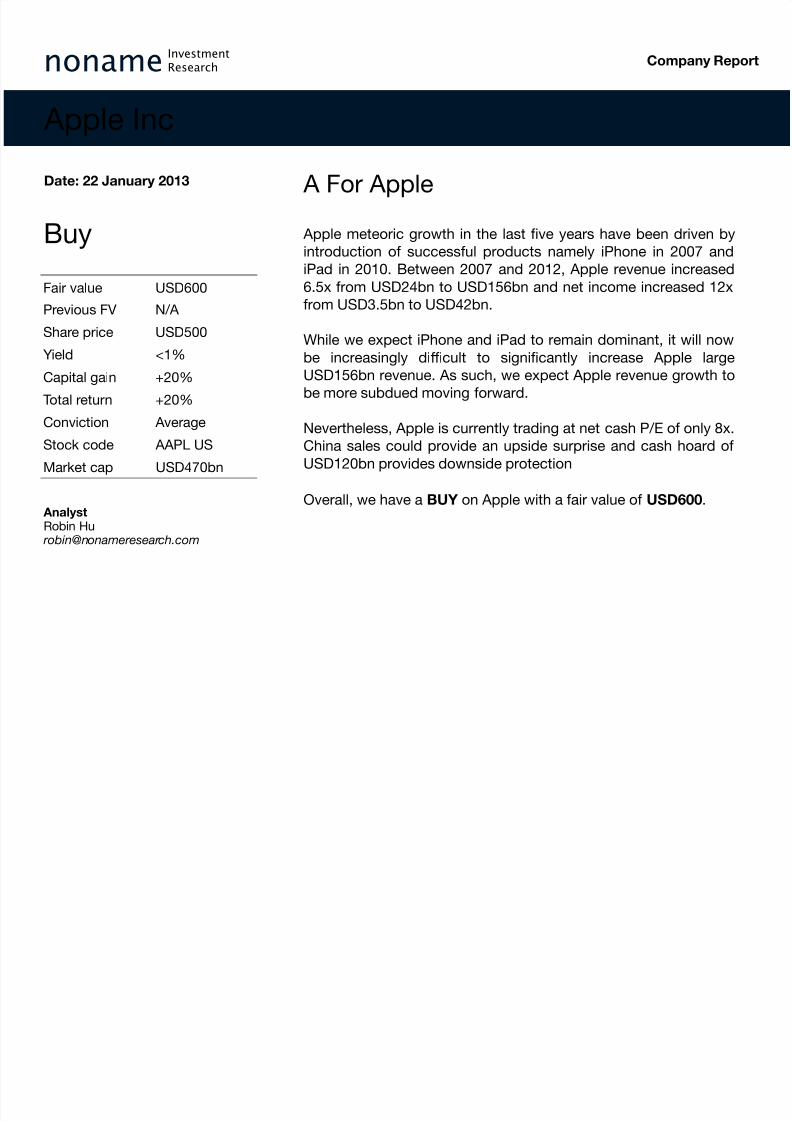

noname Investment Research Buy A For Apple Company Report Apple meteoric growth in the last five years have been driven by introduction of successful products namely iPhone in 2007 and iPad in 2010. Between 2007 and 2012, Apple revenue increased 6.5x from USD24bn to USD156bn and net income increased 12x from USD3.5bn to USD42bn. While we expect iPhone and iPad to remain dominant, it will now be increasingly di fficult to significantly increase Apple large USD156bn revenue. As such, we expect Apple revenue growth to be more subdued moving forward. Nevertheless, Apple is currently trading at net cash P/E of only 8x. China sales could provide an upside surprise and cash hoard of USD120bn provides downside protection Overall, we have a BUY on Apple with a fair value of USD600. Apple Inc Date: 22 January 2013 Fair value USD600 Previous FV N/A Share price USD500 Yield <1% Capital gain +20% T otal return +20% Conviction Average Stock code AAPL US Market cap USD470bn Analyst Robin Hu robin@n onameresear ch.com

-

Upload

nonameresearch -

Category

Documents

-

view

227 -

download

0

Transcript of NN AAPL 130122 A For Apple

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 1/34

nonameInvestment

Research

Buy

A For Apple

Company Report

Apple meteoric growth in the last five years have been driven by

introduction of successful products namely iPhone in 2007 and

iPad in 2010. Between 2007 and 2012, Apple revenue increased6.5x from USD24bn to USD156bn and net income increased 12x

from USD3.5bn to USD42bn.

While we expect iPhone and iPad to remain dominant, it will now

be increasingly difficult to significantly increase Apple large

USD156bn revenue. As such, we expect Apple revenue growth to

be more subdued moving forward.

Nevertheless, Apple is currently trading at net cash P/E of only 8x.

China sales could provide an upside surprise and cash hoard of

USD120bn provides downside protection

Overall, we have a BUY on Apple with a fair value of USD600.

Apple Inc

Date: 22 January 2013

Fair value USD600

Previous FV N/A

Share price USD500

Yield <1%

Capital gain +20%

Total return +20%

Conviction Average

Stock code AAPL US

Market cap USD470bn

AnalystRobin Hu

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 2/34

2

Quantitative Overview

Qualitative OverviewLooking Ahead

Valuation and Conclusion

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 3/34

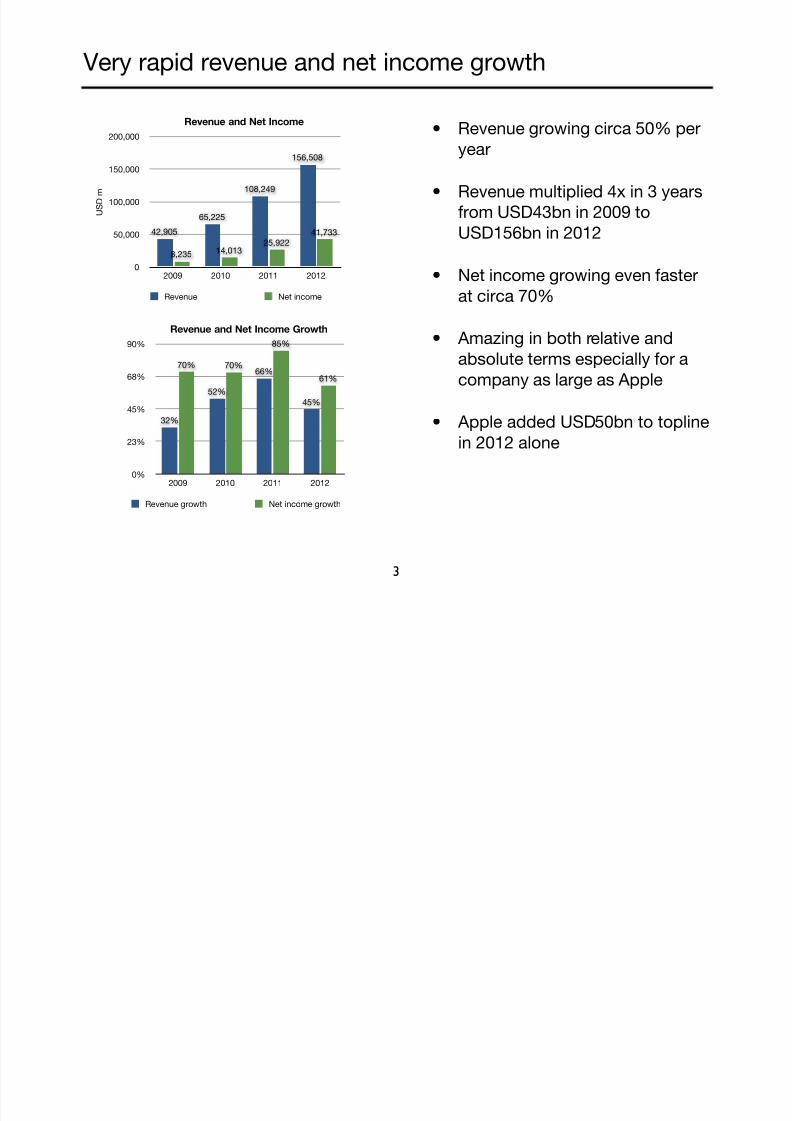

Very rapid revenue and net income growth

• Revenue growing circa 50% per

year

• Revenue multiplied 4x in 3 years

from USD43bn in 2009 to

USD156bn in 2012

• Net income growing even fasterat circa 70%

• Amazing in both relative and

absolute terms especially for a

company as large as Apple

• Apple added USD50bn to topline

in 2012 alone

3

0%

23%

45%

68%

90%

2009 2010 2011 2012

61%

85%

70%70%

45%

66%

52%

32%

Revenue and Net Income Growth

Revenue growth Net income growth

0

50,000

100,000

150,000

200,000

2009 2010 2011 2012

41,733

25,92214,0138,235

156,508

108,249

65,225

42,905

Revenue and Net Income

U S D m

Revenue Net income

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 4/34

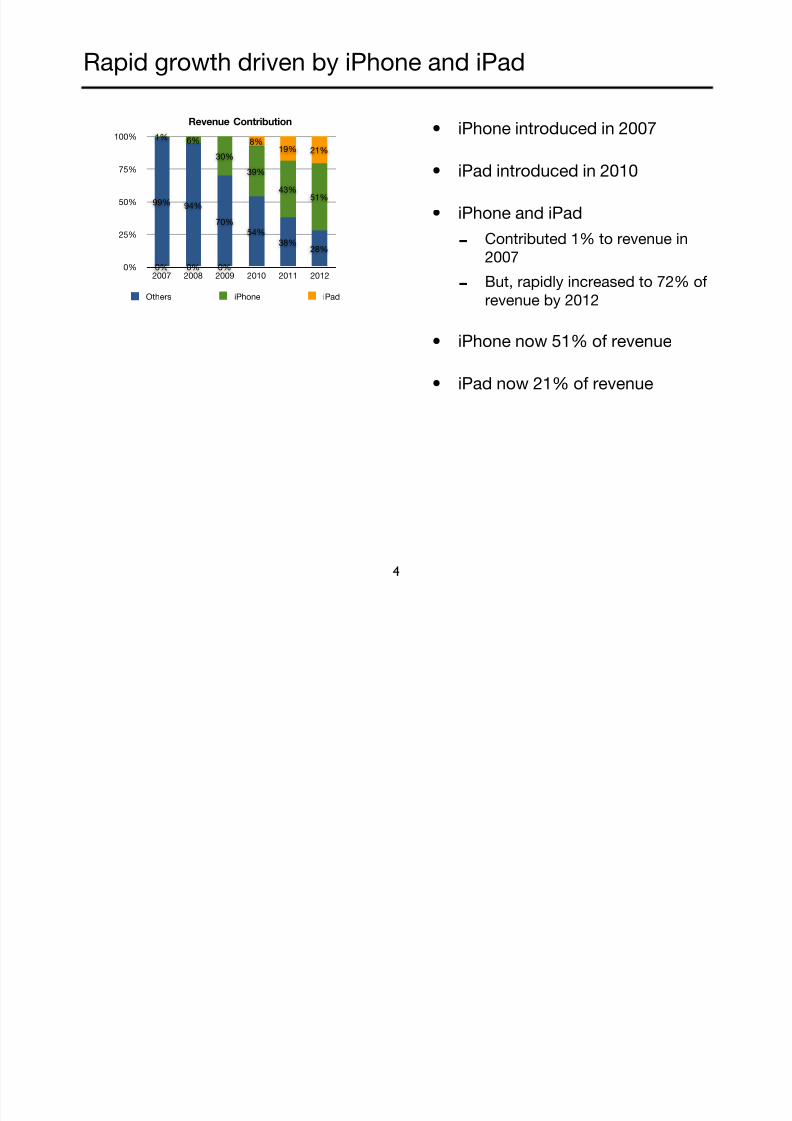

Rapid growth driven by iPhone and iPad

• iPhone introduced in 2007

• iPad introduced in 2010

• iPhone and iPad

-Contributed 1% to revenue in

2007

-

But, rapidly increased to 72% ofrevenue by 2012

• iPhone now 51% of revenue

• iPad now 21% of revenue

4

0%

25%

50%

75%

100%

2007 2008 2009 2010 2011 2012

21%19%8%

0%0%0%

51%43%

39%

30%

6%1%

28%38%

54%

70%

94%99%

Revenue Contribution

Others iPhone iPad

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 5/34

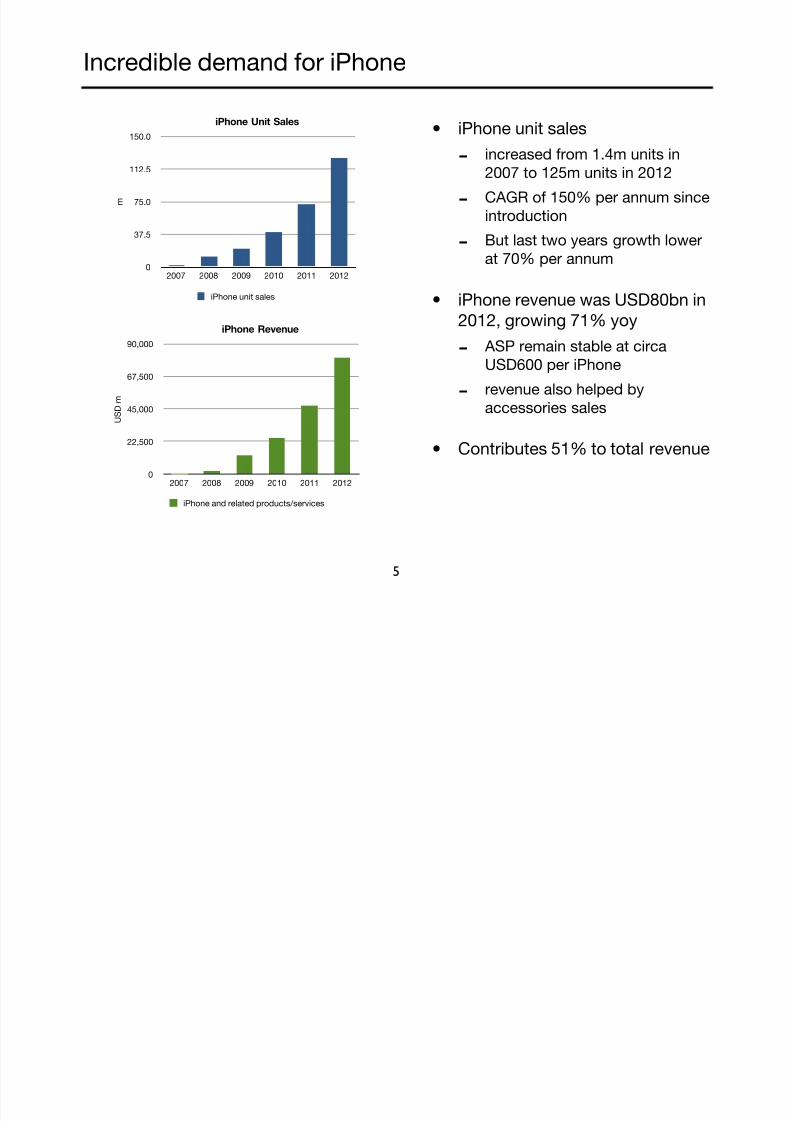

Incredible demand for iPhone

• iPhone unit sales

-increased from 1.4m units in

2007 to 125m units in 2012

-CAGR of 150% per annum since

introduction

-But last two years growth lower

at 70% per annum

• iPhone revenue was USD80bn in

2012, growing 71% yoy

- ASP remain stable at circa

USD600 per iPhone

-revenue also helped by

accessories sales

• Contributes 51% to total revenue

5

0

22,500

45,000

67,500

90,000

2007 2008 2009 2010 2011 2012

iPhone Revenue

U S

D m

iPhone and related products/services

0

37.5

75.0

112.5

150.0

2007 2008 2009 2010 2011 2012

iPhone Unit Sales

m

iPhone unit sales

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 6/34

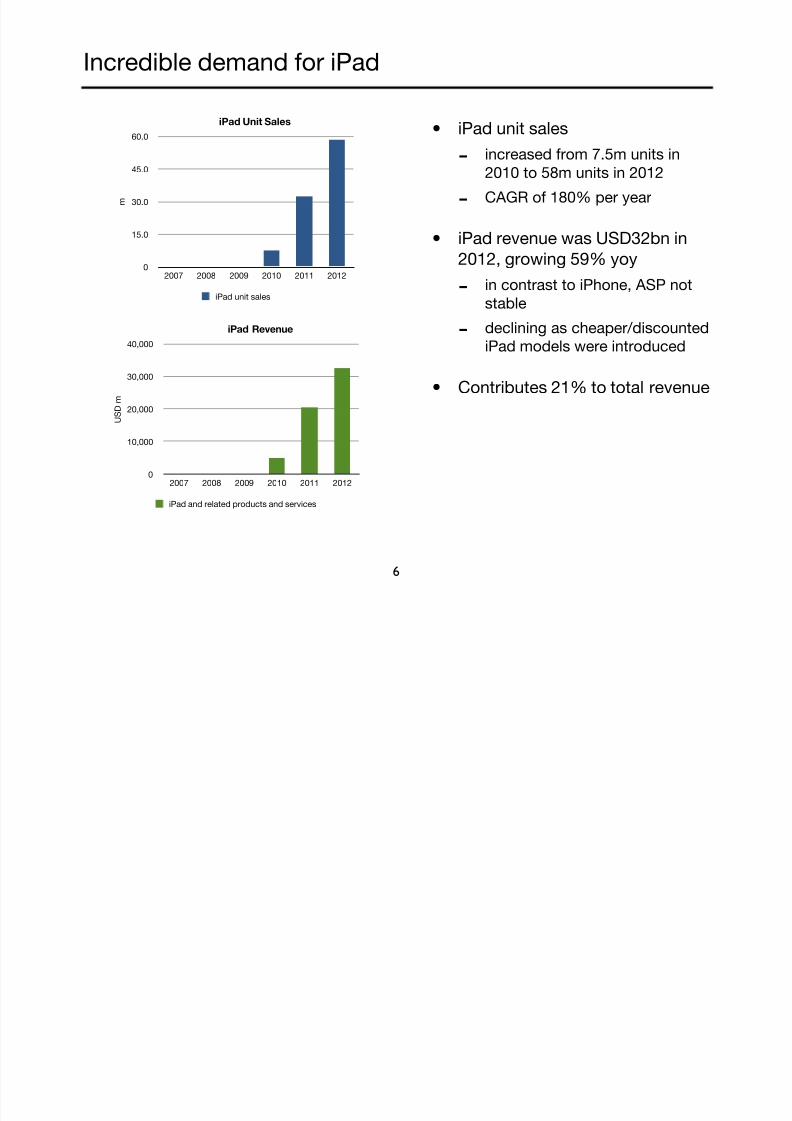

Incredible demand for iPad

• iPad unit sales

-increased from 7.5m units in

2010 to 58m units in 2012

-CAGR of 180% per year

• iPad revenue was USD32bn in

2012, growing 59% yoy

-

in contrast to iPhone, ASP not

stable

- declining as cheaper/discounted

iPad models were introduced

• Contributes 21% to total revenue

6

0

15.0

30.0

45.0

60.0

2007 2008 2009 2010 2011 2012

iPad Unit Sales

m

iPad unit sales

0

10,000

20,000

30,000

40,000

2007 2008 2009 2010 2011 2012

iPad Revenue

U S

D m

iPad and related products and services

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 7/34

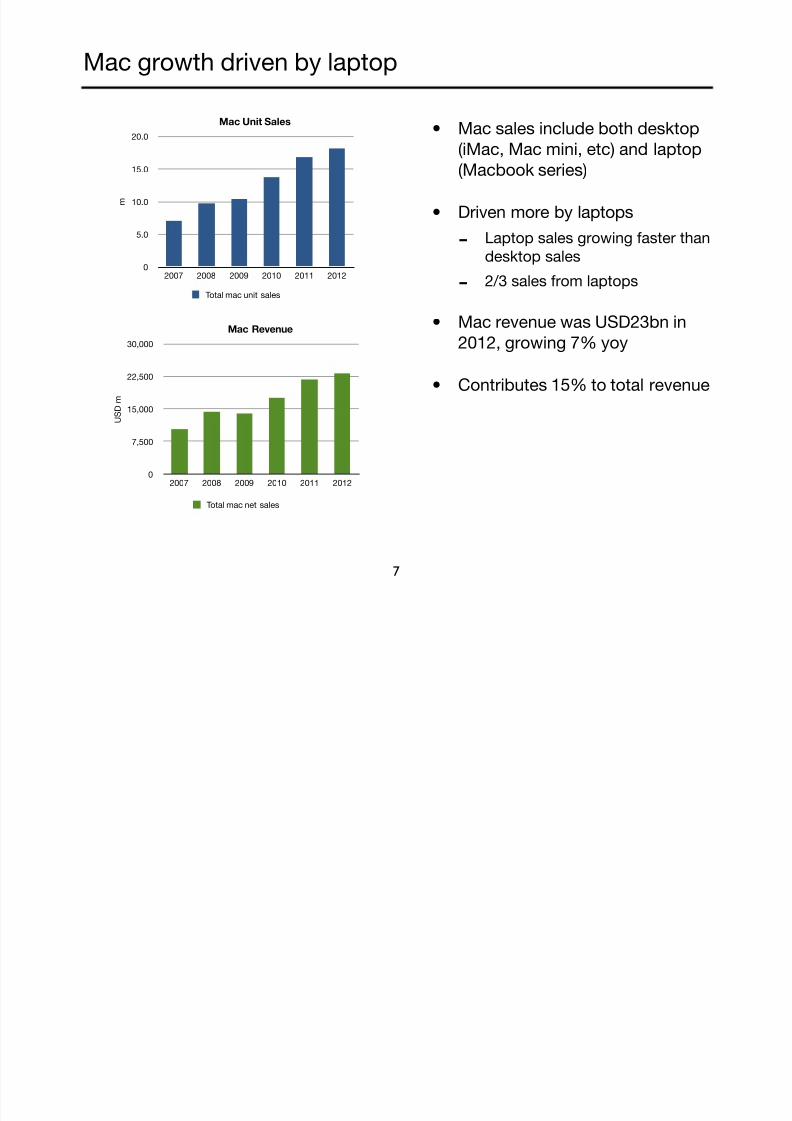

Mac growth driven by laptop

• Mac sales include both desktop

(iMac, Mac mini, etc) and laptop

(Macbook series)

• Driven more by laptops

-Laptop sales growing faster than

desktop sales

-

2/3 sales from laptops

• Mac revenue was USD23bn in

2012, growing 7% yoy

• Contributes 15% to total revenue

7

0

5.0

10.0

15.0

20.0

2007 2008 2009 2010 2011 2012

Mac Unit Sales

m

Total mac unit sales

0

7,500

15,000

22,500

30,000

2007 2008 2009 2010 2011 2012

Mac Revenue

U S

D m

Total mac net sales

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 8/34

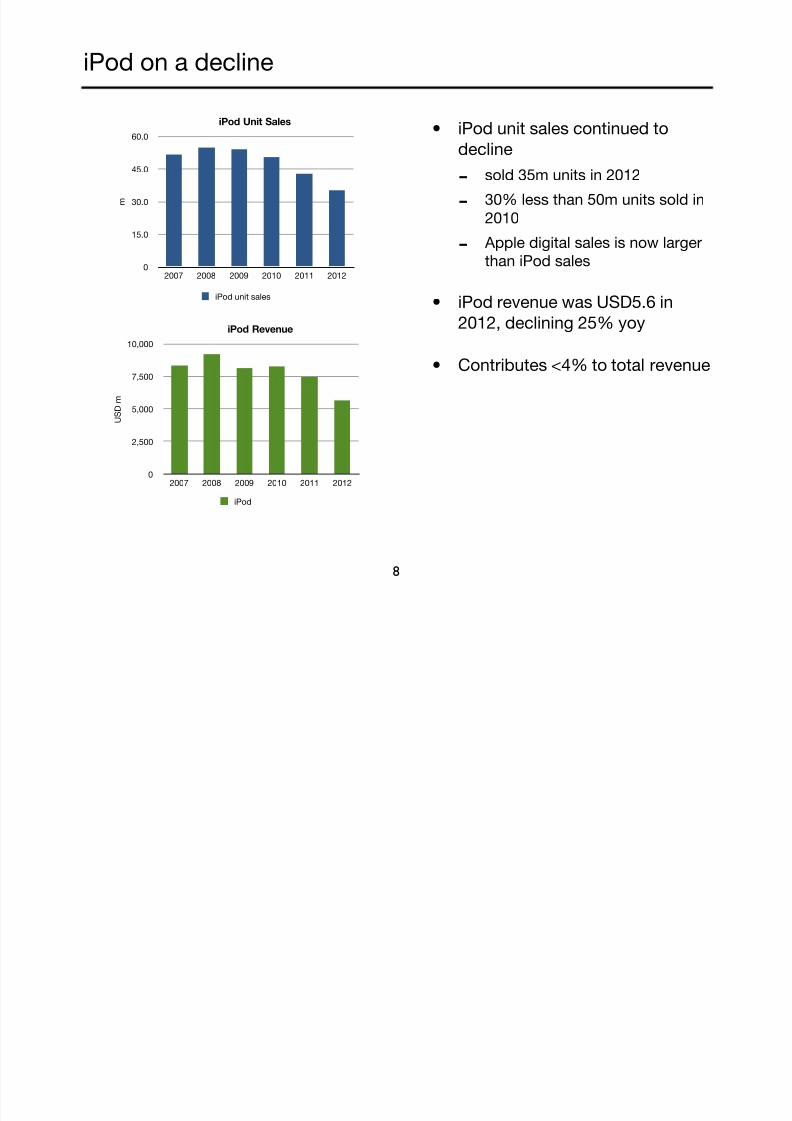

iPod on a decline

• iPod unit sales continued to

decline

-sold 35m units in 2012

-30% less than 50m units sold in

2010

- Apple digital sales is now larger

than iPod sales

• iPod revenue was USD5.6 in

2012, declining 25% yoy

• Contributes <4% to total revenue

8

0

15.0

30.0

45.0

60.0

2007 2008 2009 2010 2011 2012

iPod Unit Sales

m

iPod unit sales

0

2,500

5,000

7,500

10,000

2007 2008 2009 2010 2011 2012

iPod Revenue

U S

D m

iPod

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 9/34

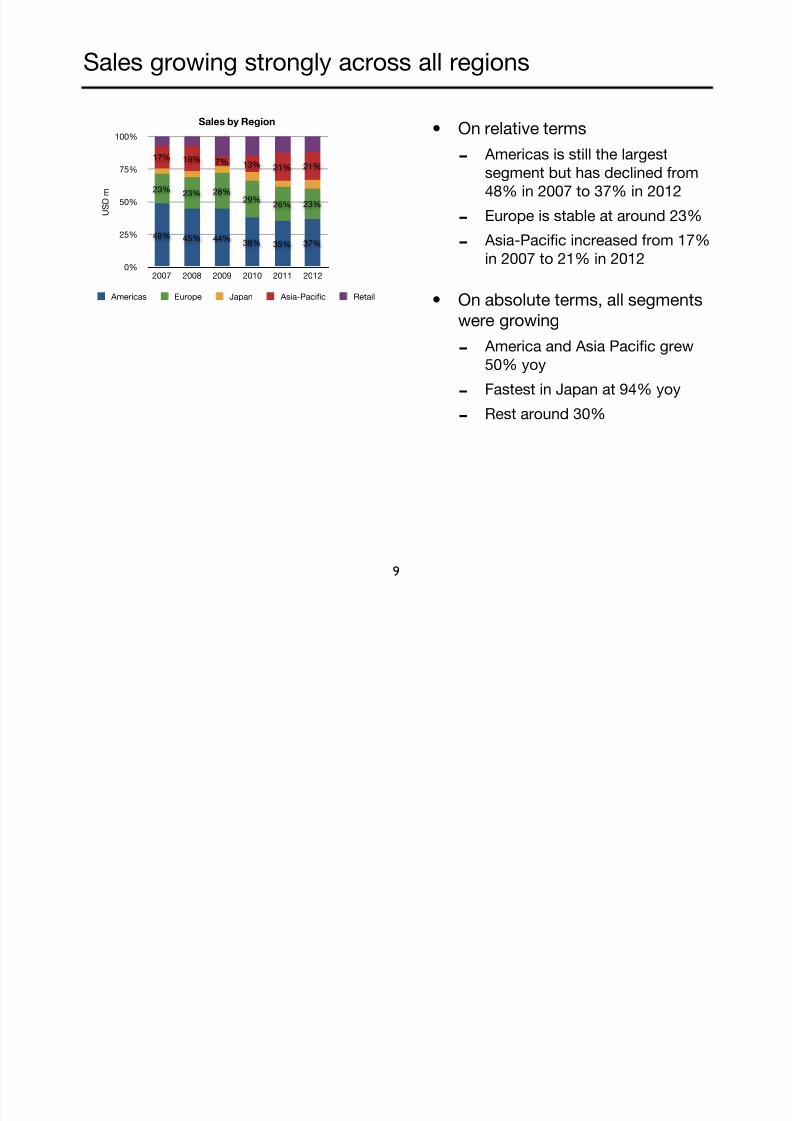

Sales growing strongly across all regions

• On relative terms

- Americas is still the largest

segment but has declined from

48% in 2007 to 37% in 2012

- Europe is stable at around 23%

- Asia-Pacific increased from 17%

in 2007 to 21% in 2012

• On absolute terms, all segments

were growing

- America and Asia Pacific grew

50% yoy

-Fastest in Japan at 94% yoy

-

Rest around 30%

9

0%

25%

50%

75%

100%

2007 2008 2009 2010 2011 2012

21%21%13%7%19%17%

23%26%29%

28%23%23%

37%35%38%44%45%48%

Sales by Region

U S D m

Americas Europe Japan Asia-Pacific Retail

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 10/34

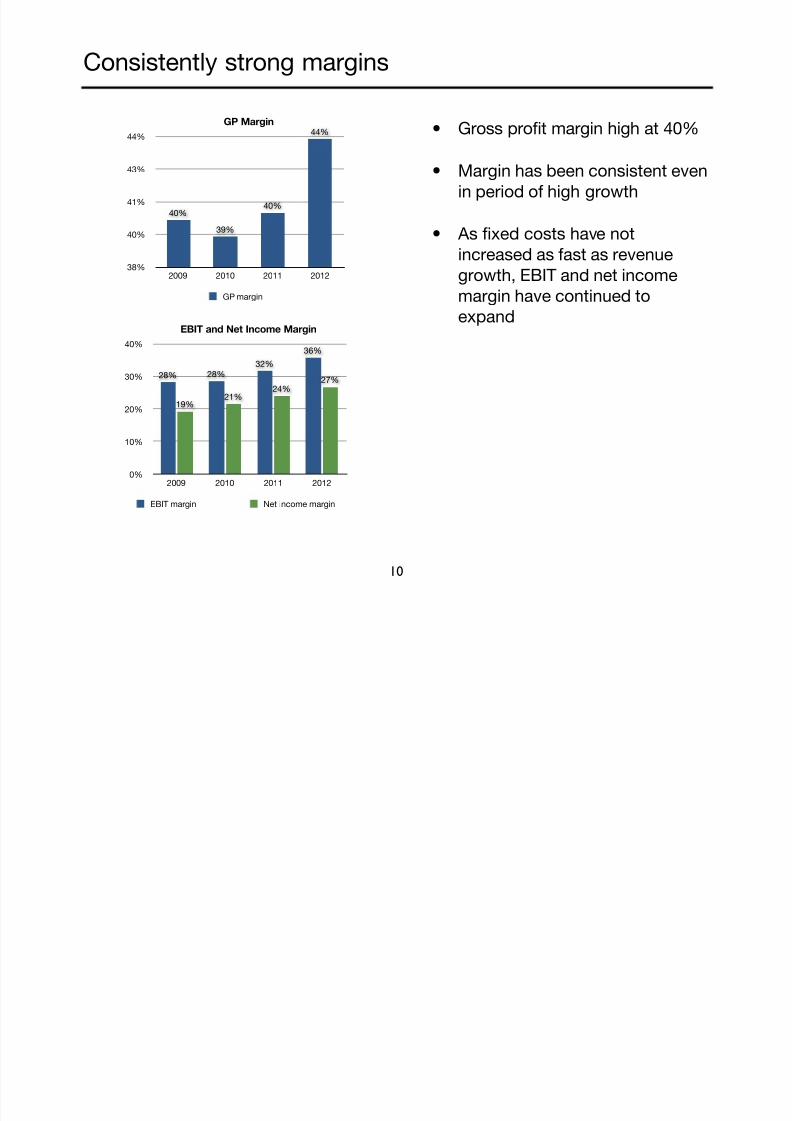

Consistently strong margins

• Gross profit margin high at 40%

• Margin has been consistent even

in period of high growth

• As fixed costs have not

increased as fast as revenue

growth, EBIT and net incomemargin have continued to

expand

10

38%

40%

41%

43%

44%

2009 2010 2011 2012

44%

40%

39%

40%

GP Margin

GP margin

0%

10%

20%

30%

40%

2009 2010 2011 2012

27%24%

21%19%

36%

32%

28%28%

EBIT and Net Income Margin

EBIT margin Net income margin

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 11/34

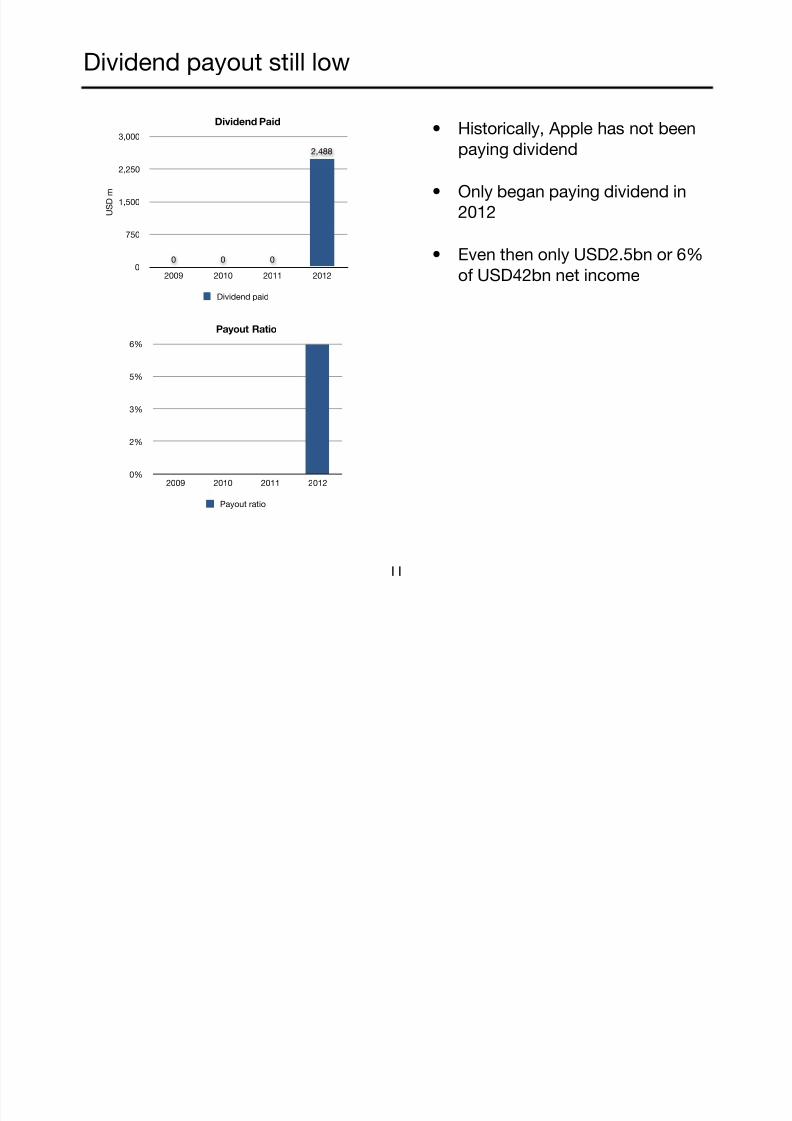

Dividend payout still low

• Historically, Apple has not been

paying dividend

• Only began paying dividend in

2012

• Even then only USD2.5bn or 6%

of USD42bn net income

11

0

750

1,500

2,250

3,000

2009 2010 2011 2012

2,488

000

Dividend Paid

U S D m

Dividend paid

0%

2%

3%

5%

6%

2009 2010 2011 2012

Payout Ratio

Payout ratio

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 12/34

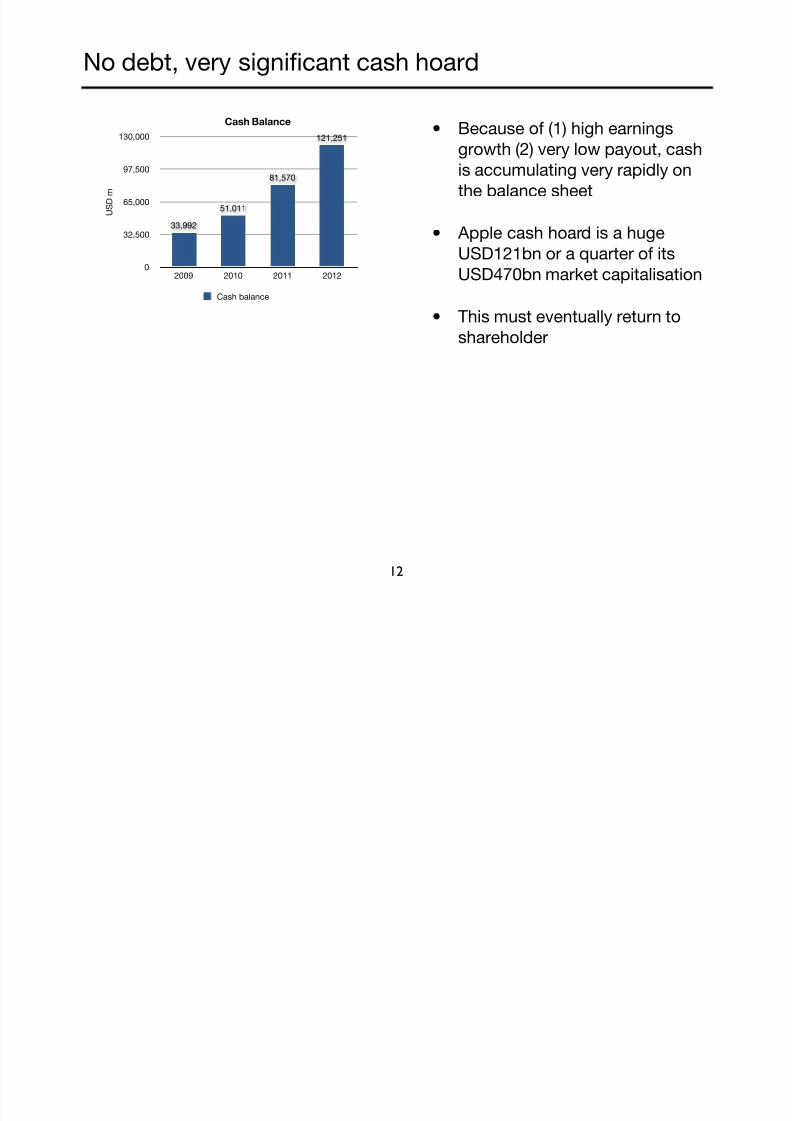

No debt, very significant cash hoard

• Because of (1) high earnings

growth (2) very low payout, cash

is accumulating very rapidly on

the balance sheet

• Apple cash hoard is a huge

USD121bn or a quarter of its

USD470bn market capitalisation

• This must eventually return to

shareholder

12

0

32,500

65,000

97,500

130,000

2009 2010 2011 2012

121,251

81,570

51,011

33,992

Cash Balance

U S D m

Cash balance

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 13/34

13

Quantitative Overview

Qualitative OverviewLooking Ahead

Valuation and Conclusion

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 14/34

Apple’s competitive advantages

Edge in innovation

Integrated business model

Financial strength

14

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 15/34

The real innovator

• In the mobility business

-Introduced iPhone in 2007, revolutionising the phone market

-Introduced App Store in 2008, popularising the concepts of apps for mobile

phones. The App Store is currently the largest at 700k apps

-Introduced iPad in 2010

• And going back further

-

Introduced iPod in 2001 and its subsequent iterations (Shuffle, Touch, Nano)

-Introduced iTunes in 2001 as a digital content manager

-Introduced iTunes Store in 2003 as online digital media store and introducing

the concept of aggressively priced (99 sen), volume based music sale

- Adopted retail presence model with Apple Retail Store in 2001. Though met

with skepticism initially, this has now proven to be the correct model

• And going back even further

-Invented personal computer with Apple II in 1970s

-Invented GUI and mouse

15

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 16/34

What were the competitors doing all this time?

• What has Apple competitors introduced in comparison?

• Why didn’t RIM or Nokia or Samsung launched a phone like iPhone in 2007?

These are players that are already in the phone business

• Why didn’t any of the competitors see the benefit of an App Store? Now,

only Google App Store is a viable competitor to Apple App Store

• Apple took the lead with iPhone in 2007 but why did the competitors allow

Apple to take the lead with iPad again in 2010?

• Why are the competitors always behind?

• Perhaps something wrong with their business model?

16

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 17/34

Apple’s business model

“[Apple] ...is committed to bringing the best user experience to its customers

through its innovative hardware, software, peripherals, and services.

[Apple]... business strategy leverages its unique ability to design and develop its

own operating systems, hardware, application software, and services to provide

its customers new products and solutions with superior ease-of-use, seamlessintegration, and innovative design”

Apple Annual Report

17

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 18/34

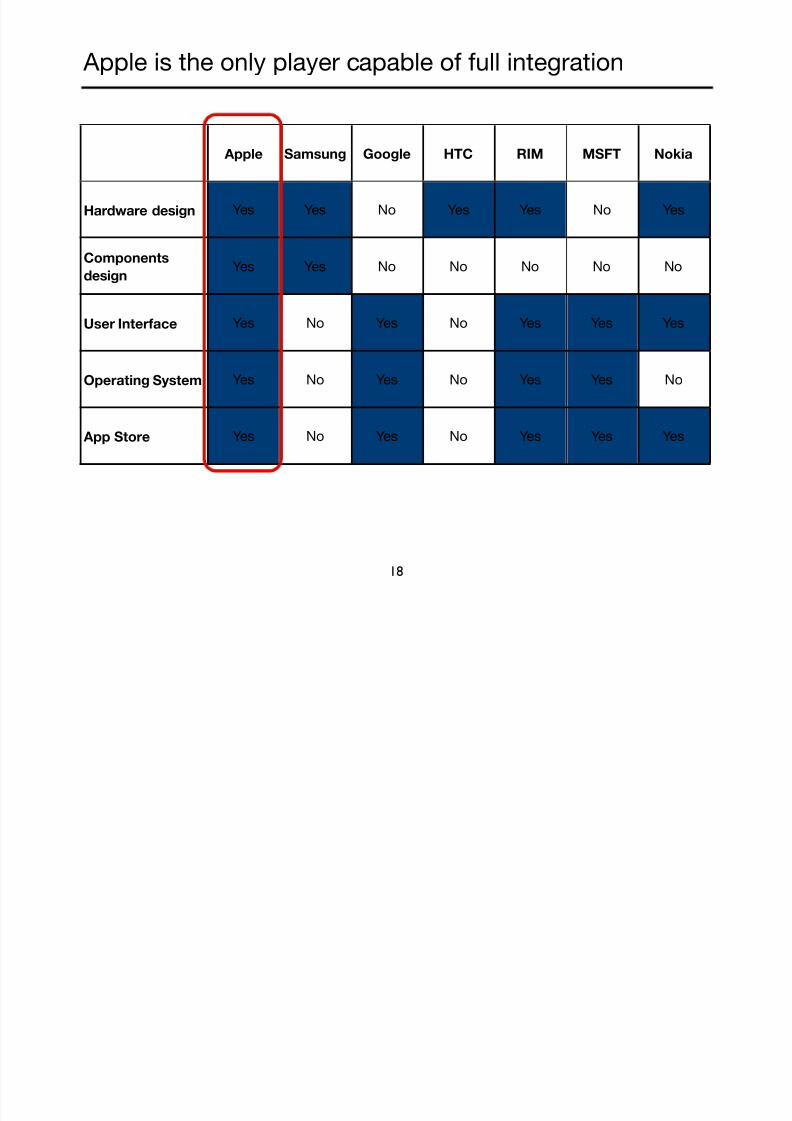

Apple is the only player capable of full integration

18

Apple Samsung Google HTC RIM MSFT Nokia

Hardware design Yes Yes No Yes Yes No Yes

Components

design

Yes Yes No No No No No

User Interface Yes No Yes No Yes Yes Yes

Operating System Yes No Yes No Yes Yes No

App Store Yes No Yes No Yes Yes Yes

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 19/34

Benefit of full integration

• Full control of user experience

- Apple controls Mac OS, iOS, App Store, iTunes, iBookstore

-This provides (1) integration (2) consistent user experience across Apple

products desktops, laptops, iPhones, iPads

-This help cross selling and “lock-in” users into Apple ecosystem

• Clear differentiation

-

If you like iOS, Mac OS or App Store, you must buy an Apple product

-In contrast, if you like Android, you can pick a device from Google, Motorola,

HTC, Samsung, Sony

- This creates clear differentiation for Apple that can not be replicated by

competitors

-Not only are Apple’s competitors fighting Apple, they must also fight amongst

themselves since they sell similar products

19

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 20/34

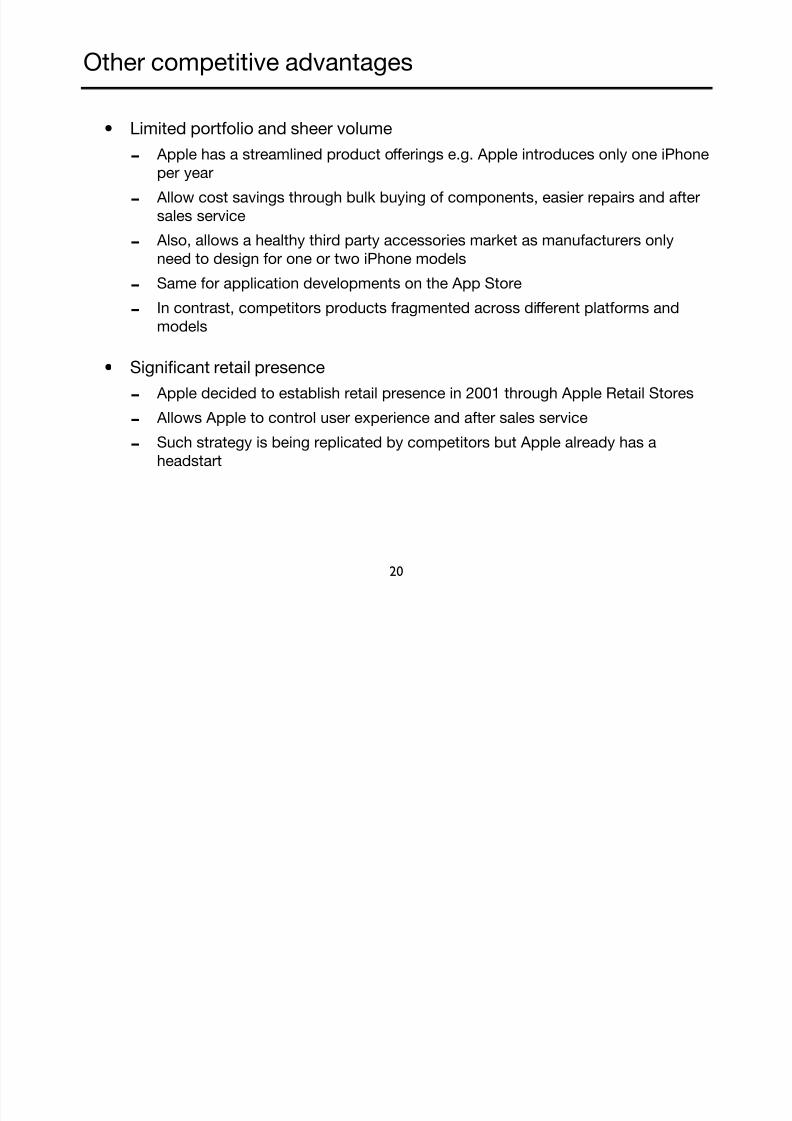

Other competitive advantages

• Limited portfolio and sheer volume

- Apple has a streamlined product offerings e.g. Apple introduces only one iPhone

per year

- Allow cost savings through bulk buying of components, easier repairs and after

sales service

- Also, allows a healthy third party accessories market as manufacturers only

need to design for one or two iPhone models

-

Same for application developments on the App Store

-In contrast, competitors products fragmented across different platforms and

models

• Significant retail presence

- Apple decided to establish retail presence in 2001 through Apple Retail Stores

-

Allows Apple to control user experience and after sales service

-Such strategy is being replicated by competitors but Apple already has a

headstart

20

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 21/34

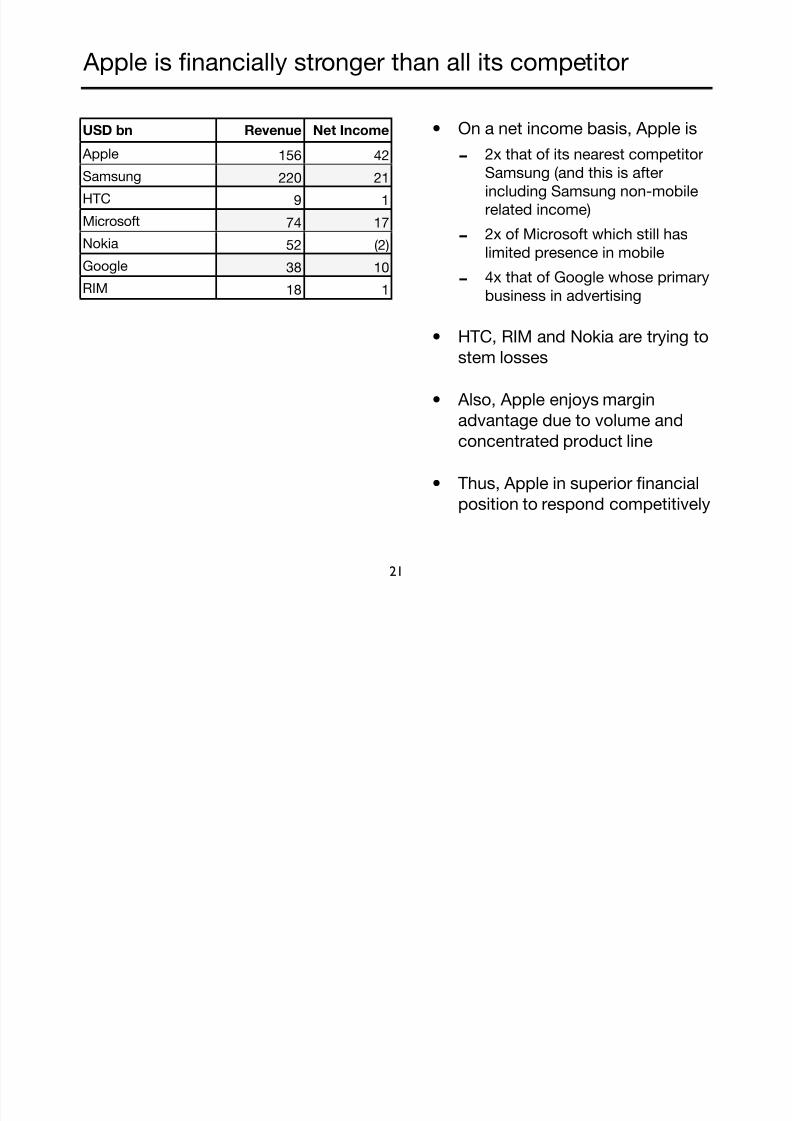

Apple is financially stronger than all its competitor

• On a net income basis, Apple is

-2x that of its nearest competitor

Samsung (and this is after

including Samsung non-mobile

related income)

-2x of Microsoft which still has

limited presence in mobile

-

4x that of Google whose primarybusiness in advertising

• HTC, RIM and Nokia are trying to

stem losses

• Also, Apple enjoys margin

advantage due to volume andconcentrated product line

• Thus, Apple in superior financial

position to respond competitively

21

USD bn Revenue Net Income

Apple

Samsung

HTC

Microsoft

Nokia

RIM

156 42

220 21

9 1

74 17

52 (2)

38 10

18 1

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 22/34

Apple’s competitive advantages

Edge in innovation

Integrated business model

Financial strength

22

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 23/34

23

Quantitative Overview

Qualitative OverviewLooking Ahead

Valuation and Conclusion

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 24/34

24

What would Apple look like in the short term?

• Revenue composition continues to be dominated by iPhone/iPad

-By virtue of size, iPhone and iPad will continue to dominate revenue

-New products rumored to include iPhone 5S, cheaper iPhones, Apple TV

-But unlikely to have any impact in 2013

• Revenue growth may be more subdued

-Two sources contribute to revenue (1) upgrade buyers (2) new buyers

-Upgrade buyers merely replace their existing Apple products hence serve to

maintain revenue

-Only new buyers capable of creating strong revenue growth

- Apple revenue is biased towards hardware hence need to introduce new product

to sustain growth

-But what else can Apple introduce after iPhone and iPad?

-Very little other than cheaper iPhones to drive volume in emerging market

- Also, it is hard to grow a USD156bn revenue meaningfully

-Therefore, we believe Apple revenue will now grow at markedly lower rate

compared to previous years

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 25/34

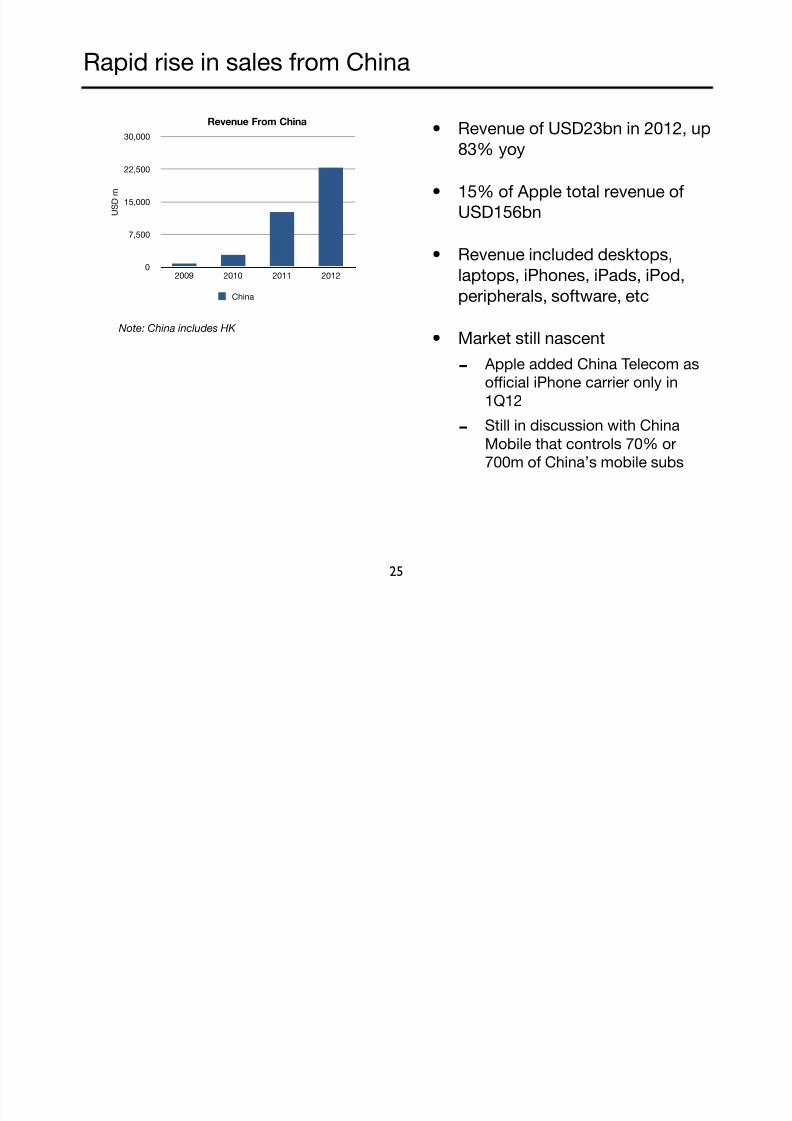

Rapid rise in sales from China

• Revenue of USD23bn in 2012, up

83% yoy

• 15% of Apple total revenue of

USD156bn

• Revenue included desktops,

laptops, iPhones, iPads, iPod,peripherals, software, etc

• Market still nascent

- Apple added China Telecom as

official iPhone carrier only in

1Q12

-

Still in discussion with China

Mobile that controls 70% or

700m of China’s mobile subs

25

0

7,500

15,000

22,500

30,000

2009 2010 2011 2012

Revenue From China

U S D m

China

Note: China includes HK

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 26/34

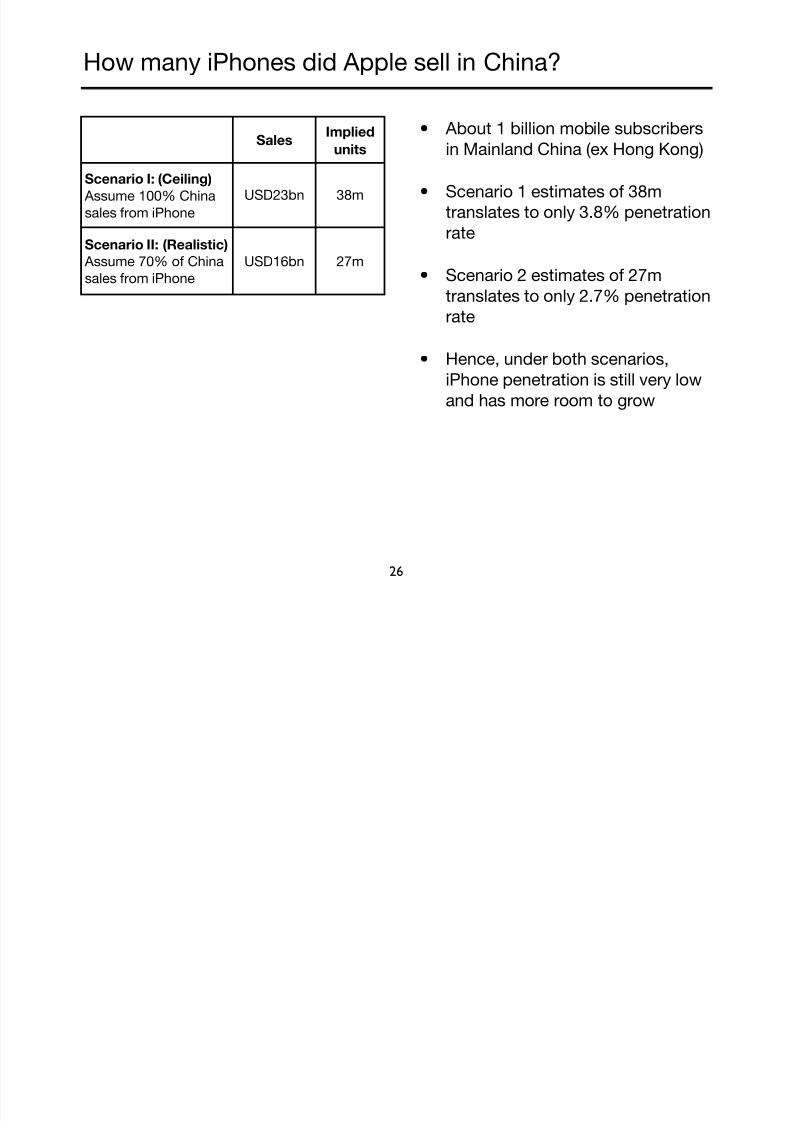

How many iPhones did Apple sell in China?

• About 1 billion mobile subscribers

in Mainland China (ex Hong Kong)

• Scenario 1 estimates of 38m

translates to only 3.8% penetration

rate

• Scenario 2 estimates of 27mtranslates to only 2.7% penetration

rate

• Hence, under both scenarios,

iPhone penetration is still very low

and has more room to grow

26

SalesImplied

units

Scenario I: (Ceiling)

Assume 100% China

sales from iPhone

USD23bn 38m

Scenario II: (Realistic)

Assume 70% of China

sales from iPhone

USD16bn 27m

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 27/34

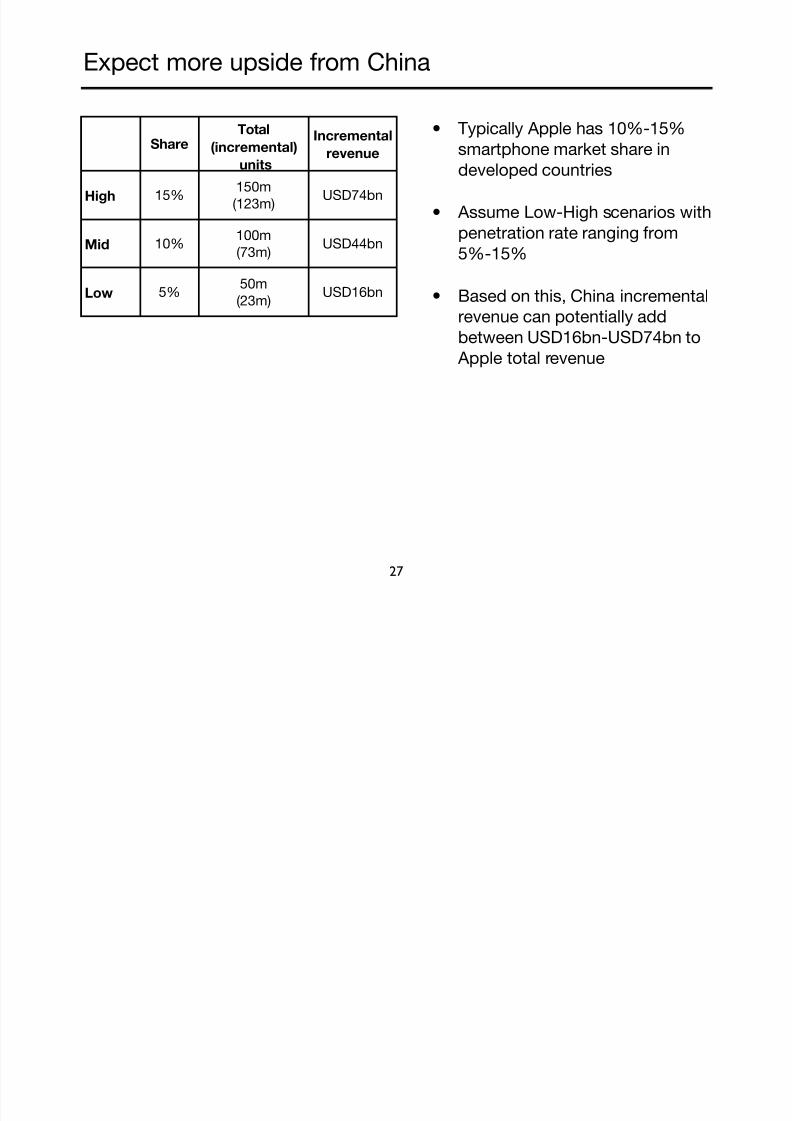

Expect more upside from China

• Typically Apple has 10%-15%

smartphone market share in

developed countries

• Assume Low-High scenarios with

penetration rate ranging from

5%-15%

• Based on this, China incremental

revenue can potentially add

between USD16bn-USD74bn to

Apple total revenue

27

Share

Total

(incremental)

units

Incrementalrevenue

High 15%150m

(123m)USD74bn

Mid 10%100m

(73m)USD44bn

Low 5% 50m(23m)

USD16bn

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 28/34

28

Quantitative Overview

Qualitative OverviewLooking Ahead

Valuation and Conclusion

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 29/34

Lets recap

29

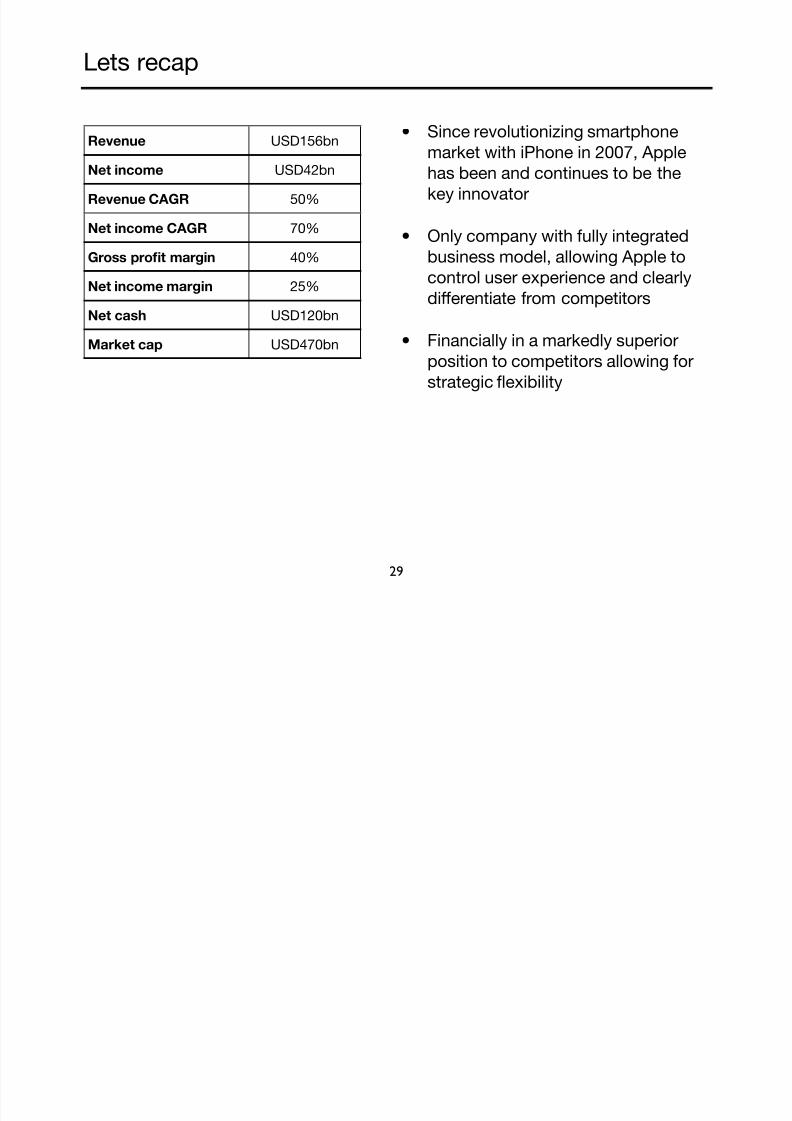

• Since revolutionizing smartphone

market with iPhone in 2007, Apple

has been and continues to be the

key innovator

• Only company with fully integrated

business model, allowing Apple to

control user experience and clearlydifferentiate from competitors

• Financially in a markedly superior

position to competitors allowing for

strategic flexibility

Revenue USD156bn

Net income USD42bn

Revenue CAGR 50%

Net income CAGR 70%

Gross profit margin 40%

Net income margin 25%

Net cash USD120bn

Market cap USD470bn

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 30/34

On the positive side

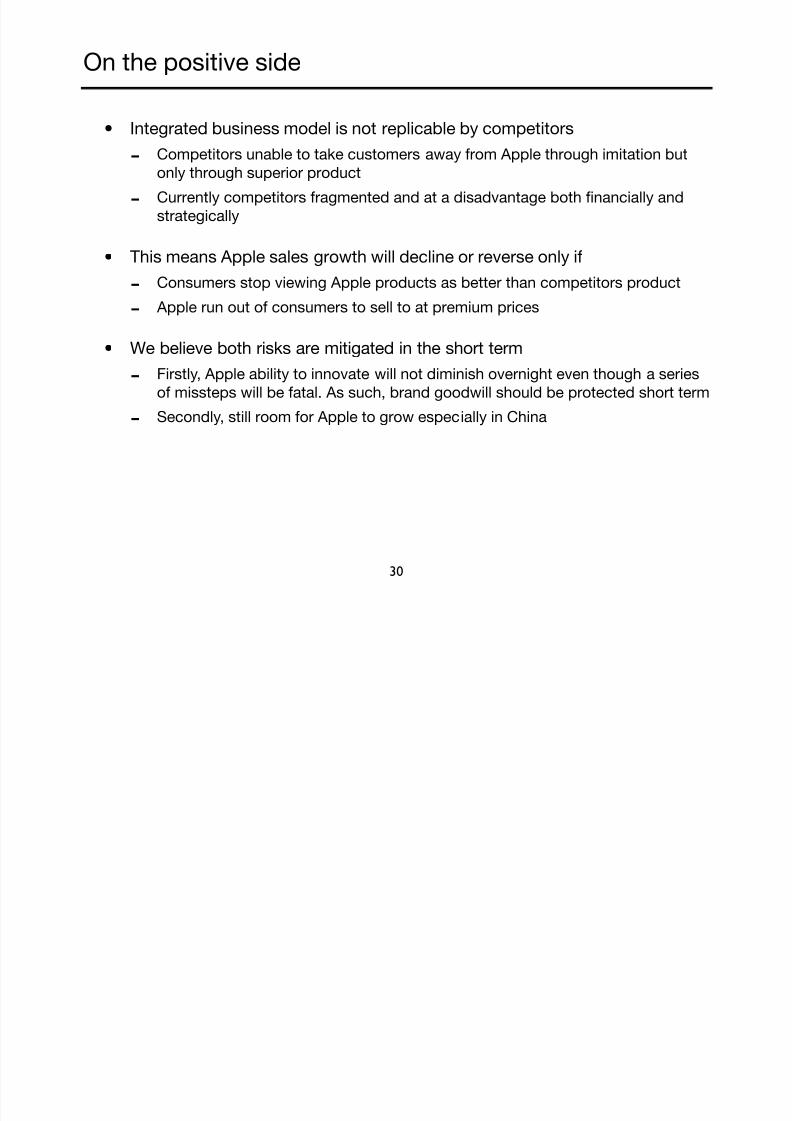

• Integrated business model is not replicable by competitors

-Competitors unable to take customers away from Apple through imitation but

only through superior product

-Currently competitors fragmented and at a disadvantage both financially and

strategically

• This means Apple sales growth will decline or reverse only if

-

Consumers stop viewing Apple products as better than competitors product

- Apple run out of consumers to sell to at premium prices

• We believe both risks are mitigated in the short term

-Firstly, Apple ability to innovate will not diminish overnight even though a series

of missteps will be fatal. As such, brand goodwill should be protected short term

-

Secondly, still room for Apple to grow especially in China

30

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 31/34

On the negative side

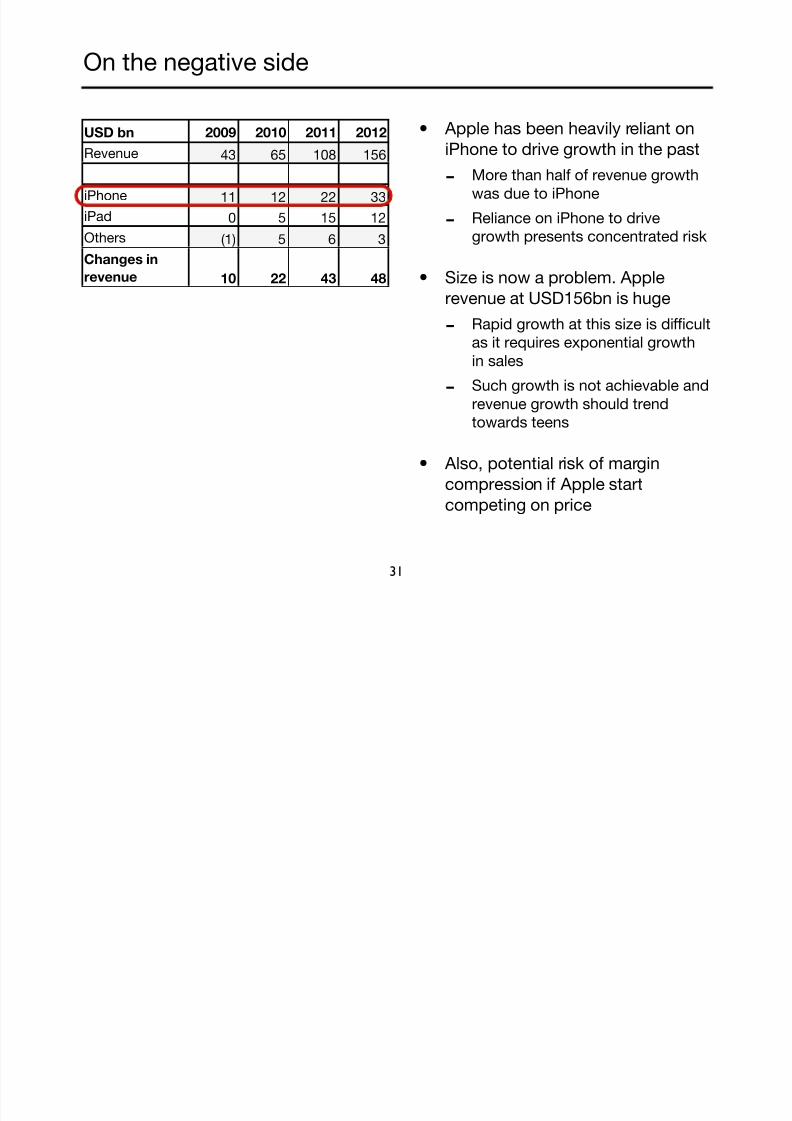

• Apple has been heavily reliant on

iPhone to drive growth in the past

-More than half of revenue growth

was due to iPhone

-Reliance on iPhone to drive

growth presents concentrated risk

• Size is now a problem. Applerevenue at USD156bn is huge

- Rapid growth at this size is difficult

as it requires exponential growth

in sales

-Such growth is not achievable and

revenue growth should trend

towards teens

• Also, potential risk of margin

compression if Apple start

competing on price

31

USD bn

Revenue

iPhone

iPad

Others

Changes in

revenue

2009 2010 2011 2012

43 65 108 156

11 12 22 33

0 5 15 12

(1) 5 6 3

10 22 43 48

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 32/34

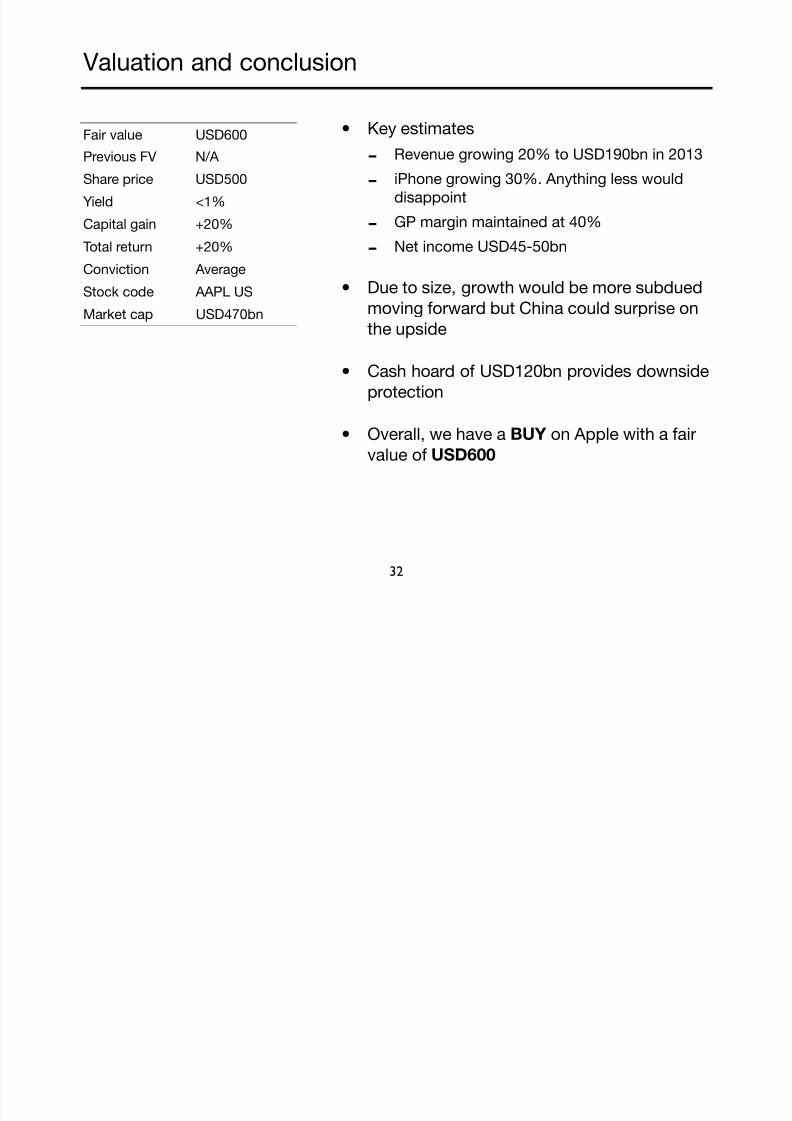

Valuation and conclusion

• Key estimates

-Revenue growing 20% to USD190bn in 2013

-iPhone growing 30%. Anything less would

disappoint

-GP margin maintained at 40%

-Net income USD45-50bn

• Due to size, growth would be more subdued

moving forward but China could surprise on

the upside

• Cash hoard of USD120bn provides downside

protection

• Overall, we have a BUY on Apple with a fair

value of USD600

32

Fair value USD600

Previous FV N/A

Share price USD500

Yield <1%

Capital gain +20%

Total return +20%

Conviction Average

Stock code AAPL US

Market cap USD470bn

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 33/34

Rating structure

The rating structure consists of two main elements; fair value and conviction rating. The fair value reflects the security intrinsic value and is derived based on fundamental analysis. The conviction rating reflects

uncertainty associated with the security fair value and is derived based on broad factors such as underlying

business risks, contingent events and other variables. Both the fair value and conviction rating are then used

to form a view of the security potential total return. A Buy call implies a potential total return of 10% or more,

a Sell call implies a potential total loss of 10% or more while all other circumstances result in a Neutral call.

Disclaimer

This report is for information purposes only and is prepared from data and sources believed to be correct

and reliable at the time of issue. The data and sources have not been independently verified and as such, no

representation, express or implied, is made with respect to the accuracy, completeness or reliability of the

information or opinions in this report. The information and opinions in this report are not and should not be

construed as an off er, recommendation or solicitation to buy or sell any securities referred to herein.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and

consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects

before participating in any transaction.

7/29/2019 NN AAPL 130122 A For Apple

http://slidepdf.com/reader/full/nn-aapl-130122-a-for-apple 34/34

www.nonameresearch.com