NISM Mutual Fund Distributors Certification Exam PDF/NISM_MFD_ch1n2.pdf · NISM Mutual Fund...

33

CENTRE FOR INVESTMENT EDUCATION AND LEARNING NISM Mutual Fund Distributors Certification Exam Module 1 Chapters 1 and 2

Transcript of NISM Mutual Fund Distributors Certification Exam PDF/NISM_MFD_ch1n2.pdf · NISM Mutual Fund...

Do not put content on the brand

CENTRE FOR INVESTMENT EDUCATION AND LEARNING

NISM Mutual Fund Distributors Certification Exam

Module 1

Chapters 1 and 2

Concept and Role of a Mutual Fund

Chapter 1

Basic Mutual Fund Concepts

3

Collective Investment Vehicle

‘Mutuality’ in contribution and benefit

Benefits accrue in the proportion to the share in the pool

Product is described by its ‘Investment Objective’

Investors match their objectives with the funds’ investment objectives

Investment objective defines the risk return profile of the fund

Mutual funds are first offered to an investor in NFO (New Fund Offer)

Unit Capital is the corpus of the fund

Number of Units * Face Value

Changes depending upon the nature of the fund

Net Assets

Assets Under Management (AUM) = Total Assets + Current Assets

Mutual Fund does not hold any long term liabilities

Net Assets = Total assets + Accrued income – Current liabilities – Accrued expenses

Net Asset Value = Net assets divided by units outstanding

Value per unit at current market prices

The net assets of a mutual fund may go up/down due to the following reasons:

Entry /exit of investors

Income from dividends or interest/ Expenses

Realised gains/losses

Unrealised gains/losses

4

Investment Portfolio

Portfolio is a collection of securities

Mutual funds can invest only in marketable securities

Value of the investment portfolio changes with a change in market price of the

securities

‘Marking to market’ - Process of using market price to value investment portfolio

Unrealised gains or Unrealised losses

Total Assets - Market Value of all the securities held in the portfolio

5

Advantages and Limitations of a Mutual Fund

Advantages

Portfolio diversification

Low transaction cost

Professional fund management

Higher flexibility

Protection of investor interest

Tax advantages

Liquidity

Limitations

Not customised portfolios

Offer several product variants

6

Mutual Fund Products - Structure

Open-ended Funds

No fixed maturity date

Accept continuous sale and re-purchase requests at fund offices and ISCs

Transactions are NAV-based

Unit capital is not fixed

Closed-ended Funds

Run for a specific period

Offered in an NFO but are closed for further purchases after the NFO

Compulsorily listed on a stock exchange to provide liquidity

Unit capital is kept constant

Interval Funds

Variant of closed-ended funds

Primarily closed-ended but become open-ended at specific intervals

7

Fund Classification

Based on investment objective

Debt funds investing in short and long term debt instruments for regular income

Equity funds investing in equity securities for capital appreciation

Hybrid funds investing in a combination of equity and debt for both income and capital

appreciation

Based on investment risk

Equity funds have a greater degree of risk as compared to a debt funds

Liquid funds are the least risky, as they invest in very short-term securities

Based on investment style

Active funds

Passive funds

8

Fund Classification-2

Based on investment horizon

Equity funds are recommended for the long term (five years and above)

Balanced funds are recommended for three years and above

Income funds are recommended for medium term (one year and above)

Short term debt funds are recommended for the short term (up to one year)

Liquid funds are recommended for ultra-short periods (up to a month)

Based on investment categories

Equity funds invest in equity shares; Debt funds invest in debt securities;

Money market funds invest in money market securities; Commodity funds invest in

commodity-linked securities;

Real estate funds invest in property-linked securities; Gold funds invest in gold-linked

securities

9

Funds Based on Investment Style

Passive Funds

Replicate a market index

Invest in the same securities and in the same proportion

No active stock or sector selection

Expenses are lower

Portfolio is modified everytime the index composition changes

Active Funds

Seek to invest in securities and sectors that may offer a better return than the index

Actively manage the allocation to market securities and cash

May perform better or worse than the market index

Incurs a higher cost than passive funds

10

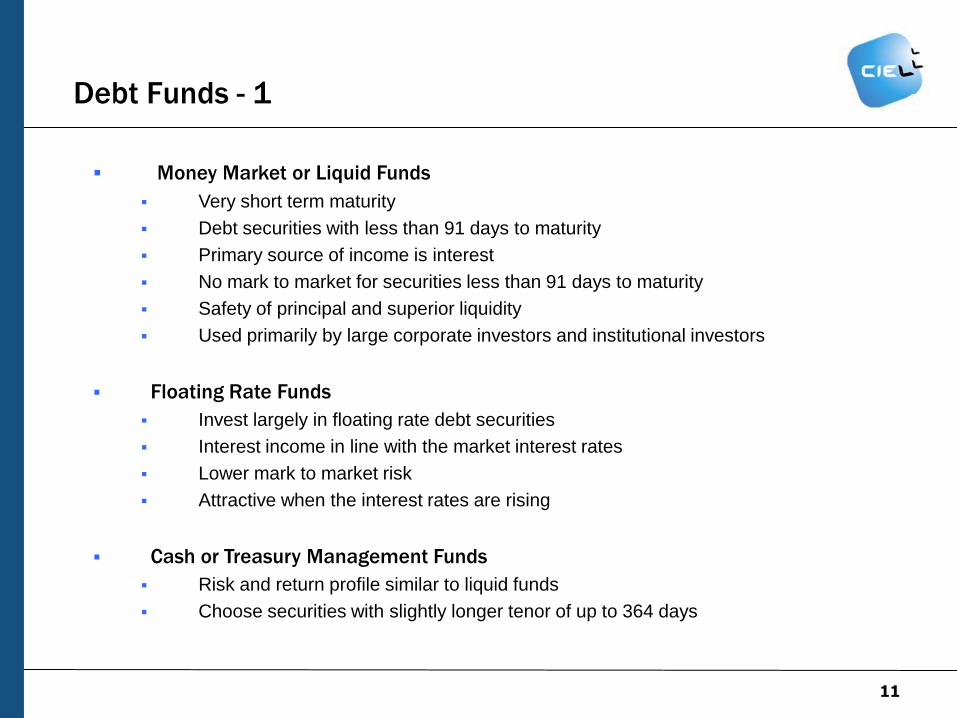

Debt Funds - 1

11

Money Market or Liquid Funds

Very short term maturity

Debt securities with less than 91 days to maturity

Primary source of income is interest

No mark to market for securities less than 91 days to maturity

Safety of principal and superior liquidity

Used primarily by large corporate investors and institutional investors

Floating Rate Funds

Invest largely in floating rate debt securities

Interest income in line with the market interest rates

Lower mark to market risk

Attractive when the interest rates are rising

Cash or Treasury Management Funds

Risk and return profile similar to liquid funds

Choose securities with slightly longer tenor of up to 364 days

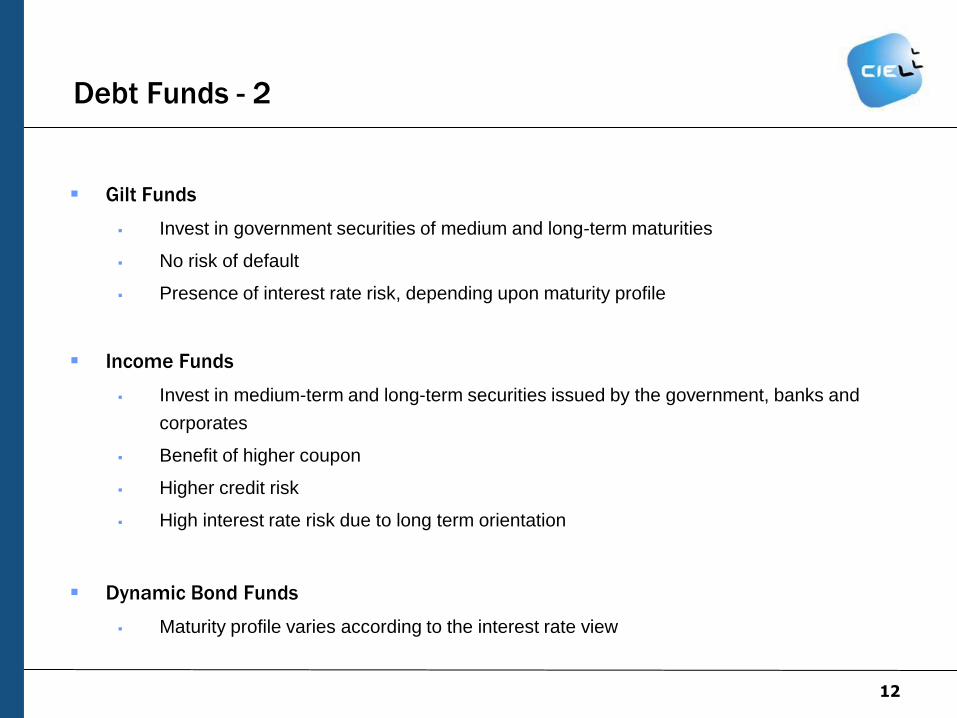

Debt Funds - 2

Gilt Funds

Invest in government securities of medium and long-term maturities

No risk of default

Presence of interest rate risk, depending upon maturity profile

Income Funds

Invest in medium-term and long-term securities issued by the government, banks and

corporates

Benefit of higher coupon

Higher credit risk

High interest rate risk due to long term orientation

Dynamic Bond Funds

Maturity profile varies according to the interest rate view

12

Debt Funds - 3

High-yield Debt Funds

Seek higher interest income by investing in debt instruments that have lower credit ratings

Also known as ‘junk bond funds’

Not permitted in India

Fixed Maturity Plans

Closed-end funds that invest in debt instruments with maturities that match the term of the

scheme

Debt securities are redeemed on maturity and paid to investors

No interest rate risk

Short Term Plan

Combine long and short term debt securities

Earn interest from short term securities

Capital gains from long term securities

13

Equity Funds

Diversified Equity Funds

Invest in equity shares across various sectors, sizes and industries

Less risky

Thematic Equity Funds

Multiple sectors and stocks falling within a theme

Less diversified than a diversified equity fund

Sector Equity Funds

Invest in a given sector

Concentrated funds and feature high risk

Sector performances tend to be cyclical

14

Strategy-Based Equity Funds

Growth Funds

Invest in companies whose earnings are expected to grow at an above-average rate

Value Funds

Identify stocks of good quality companies whose real worth has not been realised yet

Mid-cap and Small-cap funds

Focus on smaller and emerging companies for their higher growth potential

Dividend Yield Funds/Equity Income Funds

Invest in companies that have a high dividend yield

Attractive in bear and over-valued markets due to less volatility and regular dividend

income

Index Funds

Passive funds based on equity indices

15

Equity-Linked Savings Scheme

16

Some equity schemes are designated as ELSS at the time of launch

Offer tax benefits u/s 80C

Investment up to Rs. 100,000 in a year in such funds can be deducted from taxable income

of individual investors

ELSS must hold atleast 80% of the portfolio in equity securities

Lock-in period of 3 years from the date of investment

Hybrid Funds

Monthly Income Plans

• Smaller allocation to equity (5% to 25%) , Debt-oriented

• Periodic distribution of dividends, though there is no assurance

• Balanced Funds

• Equity-oriented hybrids that invest up to 65% in equity

• For investors who seek growth from equity but want protection from volatility

• Asset Allocation Funds

• Dynamic Funds that can change proportion between debt and equity depending upon market

outlook

• Capital Protection-Oriented Funds

• Debt securities with a derivative instrument or equity shares

• Structured portfolio such that ‘Amount invested + Interest = Investor’s principal’

17

Other Types of Funds-1

Fund of Funds (FoF)

Invests in funds of same fund house or various fund houses (Multi-manager)

Choice of funds according to investment objective

Two levels of expenses- underlying level and FoF level

International Funds

Invests in foreign securities or foreign funds

‘Feeder‘ fund ties up with the ‘Host’ fund in an FoF structure

Arbitrage Funds

Take equal and opposite exposure in different markets

Earn a return due to difference in price in the two markets

Low risk, return similar to the debt funds

18

Other Types of Funds - 2

Exchange Traded Funds (ETF)

Open-ended funds that track a market index

Units are listed like shares on the stock exchange

Sale and re-purchase transactions are executed on stock exchange

Demat accounts are used

Transactions at market prices, which may be different from the NAV

Commodity Funds

In India, direct investment in commodity futures is not allowed

Indian commodity funds usually invest in stocks of commodity companies or commodity ETFs

Gold Funds are structured as ETFs

19

Role of Mutual Funds

To the investor

they offer products that enable access to various markets

a diversified investment opportunity at a low cost

To the issuers of various securities,

they are institutional investors seeking better return, lower risk

Industry competitive and well-regulated

Mutual funds have grown from a single player (UTI) in 1964 to 40 players in 2010

There are about 850 mutual products in the market

Public sector mutual funds came in 1980s and the private/foreign funds came in 1990s

60% of assets are in short term debt funds, favoured by institutional investors

Measures by regulators and the industry to increase retail participation

20

Summary

Investment objective defines the risk-return profile of the mutual fund

Unit Capital = No. of units * Face value

Value of the investment portfolio changes with a change in market price of the securities

Assets Under Management (AUM) = Total Assets + Current Assets

Net Assets = Total assets + Accrued income – Current liabilities – Accrued expenses

Net Asset Value = Net assets/total outstanding units

Mutual funds offer benefits of diversification, professional management, low costs and liquidity

Choice overload and non-customization are limitations of investing in mutual funds

Open-ended funds accept continuous transactions while closed-ended funds are listed on stock

exchange. Interval funds are closed-ended but become open-ended at specific intervals

Active funds seek to better the return on the benchmark

21

Summary

Liquid funds have the lowest risk of NAV volatility

Floating rate funds offer low mark to market risk

Gilt funds have no credit risk

Income funds have a higher credit risk and provide benefit of higher coupon

High yield bond funds invest in debt instruments that have lower credit ratings

FMPs have no market/portfolio risk

Diversified equity funds are less riskier than thematic funds. Sector funds are riskiest.

ELSS have 3 year lock-in and provide tax benefits upto Rs.1lakh u/s 80C

MIP is debt-oriented while Balanced fund is equity-oriented

Balanced fund may have fixed or flexible asset allocation

International funds may invest in foreign securities or foreign funds

ETF transactions are executed on stock exchange

Indian commodity funds invest in stocks of commodity companies or commodity ETFs

22

Fund Structure and Constituents

Chapter 2

Structure of a Mutual Fund

The structure of a mutual fund in India is governed by the Sebi (Mutual Fund )

Regulations, 1996.

A mutual fund is set up as a trust

It raises money through sale of units of various schemes

Money raised is invested in securities

Investors in the fund are the beneficiaries of the trust

The three key entities in the structure of a mutual fund are:

The sponsor who sets up the fund

The trustees who supervise the fund on behalf of the investors

The asset management company which carries out the activities of the fund

24

Sponsor

Sponsor is the main business entity that sets up the mutual fund.

There can be more than one sponsor for a fund

Role of the sponsor

Is the promoter of the mutual fund

Sets up the trust and the AMC

Appoints the Board of Trustees and Board of Directors of the AMC

Seeks regulatory approval for the fund from Sebi

Eligibility criteria

At least 5 years experience in the financial services industry

Positive net worth over the last 5 financial years

Profits over the last 3 out of 5 years

At least 40% contribution to the capital of the AMC

25

Trust and Trustees

The mutual fund is the trust, and is managed by trustees

Trustees can be individuals or a trustee company with a board of trustees

Investors in the mutual fund are beneficiaries of the trust

Trustees must act on behalf of the investors

Trustees are appointed by the Sponsor with Sebi approval

Trust deed is executed by the Sponsor in favour of the trustees

Trustees oversee the working of the AMC and management of the mutual fund

Points to note

Sponsor must appoint at least 4 trustees

Key decisions of the AMC require trustee approval

Trustees must meet at least 6 times in a year

At least 2/3rds of the trustees/members of the board of trustees have to be independent

26

Asset Management Company (AMC)

AMC is the investment manager of the mutual fund

They manage the day to day affairs of a mutual fund

The compliance officer of the AMC reports regularly to the trustees of the fund

AMC is appointed by the trustees, with Sebi approval

Trustees appoint AMCs through an investment management agreement

Appointment to the board of an AMC has to be approved by trustees

AMC should have a net worth of at least Rs10 crore at all times

At least 50% of members of the board of an AMC board have to be independent.

The AMC of one mutual fund cannot be an AMC or trustee of another fund.

AMCs cannot engage in any business other than that of financial advisory and investment

management

27

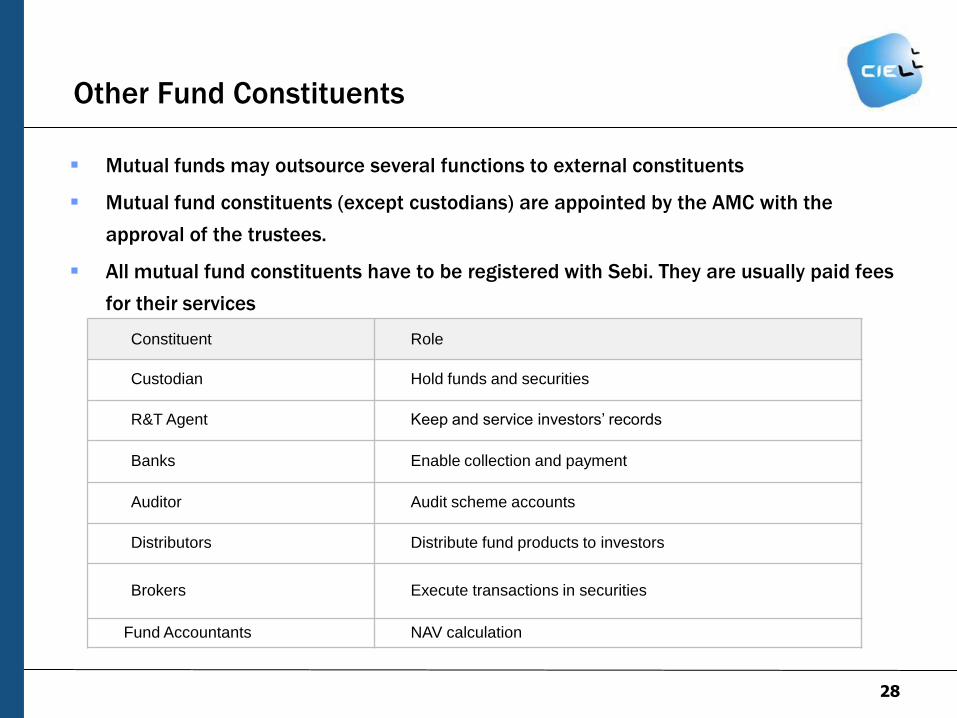

Other Fund Constituents

Mutual funds may outsource several functions to external constituents

Mutual fund constituents (except custodians) are appointed by the AMC with the

approval of the trustees.

All mutual fund constituents have to be registered with Sebi. They are usually paid fees

for their services

28

Constituent Role

Custodian Hold funds and securities

R&T Agent Keep and service investors’ records

Banks Enable collection and payment

Auditor Audit scheme accounts

Distributors Distribute fund products to investors

Brokers Execute transactions in securities

Fund Accountants NAV calculation

Custodian

Banks usually function as custodians

Custodians hold the custody of the assets of a mutual fund

They hold cash and securities of the mutual fund

Are appointed by the Sponsor

Only constituent NOT directly appointed by the AMC

Must be independent of the Sponsor and its associates

Sponsor cannot hold 50% or more of the capital of the custodian

Independence of custodian critical for investor protection

Functions of the Custodian

Delivering and accepting securities and cash for transactions in the investment portfolio

29

Registrars and Transfer Agents

R&T agents maintain investor records. They

Operate investor service centres for mutual funds

Accept and process investor transactions such as purchase, redemption and switches.

Create, maintain and update investor records.

30

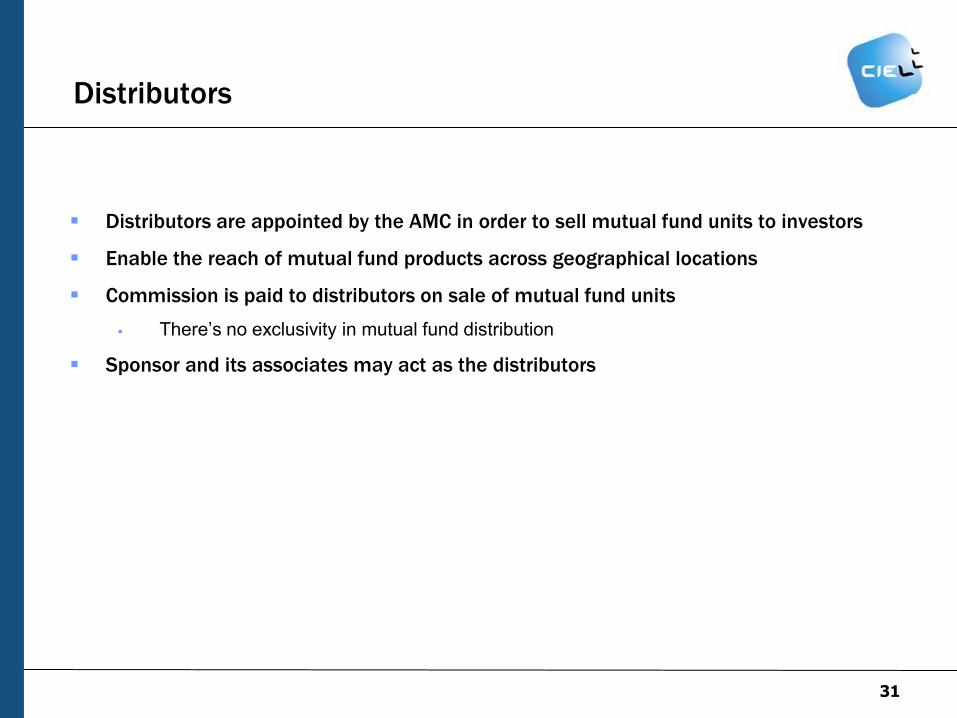

Distributors

Distributors are appointed by the AMC in order to sell mutual fund units to investors

Enable the reach of mutual fund products across geographical locations

Commission is paid to distributors on sale of mutual fund units

There’s no exclusivity in mutual fund distribution

Sponsor and its associates may act as the distributors

31

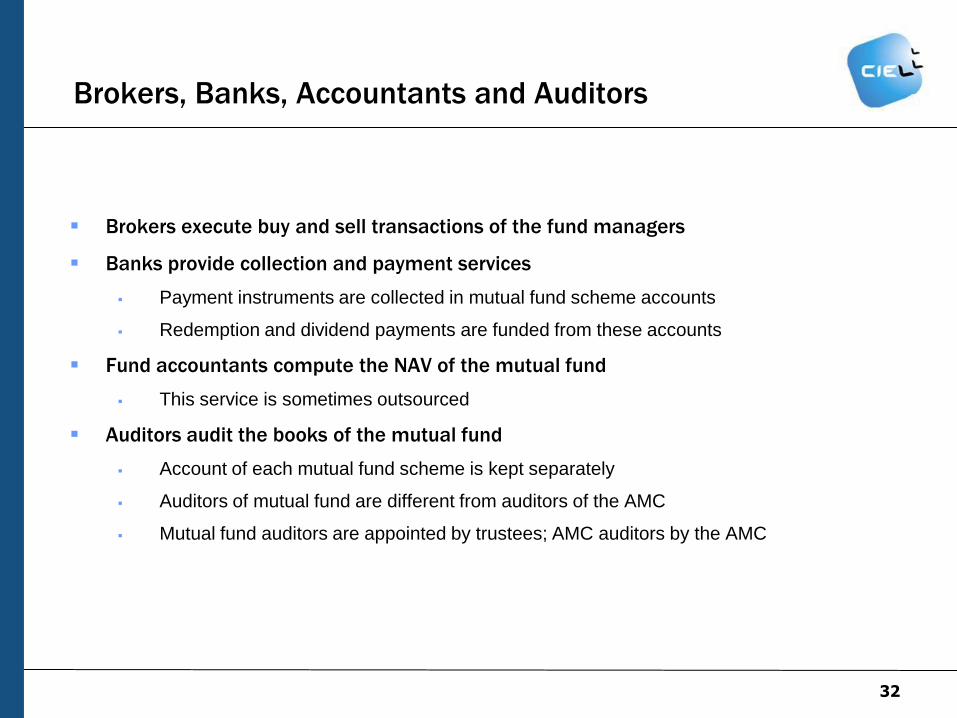

Brokers, Banks, Accountants and Auditors

Brokers execute buy and sell transactions of the fund managers

Banks provide collection and payment services

Payment instruments are collected in mutual fund scheme accounts

Redemption and dividend payments are funded from these accounts

Fund accountants compute the NAV of the mutual fund

This service is sometimes outsourced

Auditors audit the books of the mutual fund

Account of each mutual fund scheme is kept separately

Auditors of mutual fund are different from auditors of the AMC

Mutual fund auditors are appointed by trustees; AMC auditors by the AMC

32

Summary

Three-tier structure of Sponsor-Trust-AMC

Sponsor is the promoter who creates the trust and AMC

Investors in the mutual fund are beneficiaries of the trust

Board of trustees oversee the working of the mutual fund

AMC is the investment manager of the mutual fund

AMC should have a net worth of at least Rs10 crore at all times

Custodian holds assets of the fund and is independent of the Sponsor

R&T agent runs ISCs and maintains investor records

Distributors enable the reach of mutual fund products across geographical locations

Fund accountant calculates NAV

Auditors of the AMC must be different from the auditors of the mutual fund schemes

Mutual fund constituents (except custodians) are appointed by the AMC with the approval of

the trustees.

All mutual fund constituents have to be registered with Sebi

33

![NISM-Series-Mutual Fund Distributors Work Book[1]](https://static.fdocuments.in/doc/165x107/577d2a521a28ab4e1ea8fc62/nism-series-mutual-fund-distributors-work-book1.jpg)