NIGERIA POWER & GAS SECTOR MARKETS;Post Policy Implementation Impediments

34

Name: Benjamin Ogbalor Position: CEO Company: EverlinkSourcing Ltd Country: Nigeria

-

Upload

benjamin-ogbalor -

Category

Documents

-

view

34 -

download

0

Transcript of NIGERIA POWER & GAS SECTOR MARKETS;Post Policy Implementation Impediments

Name: Benjamin Ogbalor

Position: CEO

Company: EverlinkSourcing Ltd

Country: Nigeria

NIGERIA GAS AND POWER SECTOR MARKET:

Post Policy Impediment Regime

Presentation Outline

• Optimal Electricity Market

• Structure of the Power Sector

• State of the electricity market in Nigeria

• Gas to Power

• Barrier & Policy Impediments

• Policy thrust of the Power Sector

• Regulatory Solutions

• Expected Results of an Optimal Sector

• New Market Expected results

Optimal Electricity Market

• Consistent Policy Direction & Long Term Planning

• Independent & Insulated Regulator

• Cost efficiency & Recovery by Utilities/ Electricity Market.

• Private ownership of Generation, Transmission, Distribution & Stabilization of Energy Supply Source

• Accountability of Regulator,& Players

• Strong Civic engagement in Market Rules formulation, Effective Cost Evaluation & Tariff Setting.

• Commerciality & Adequate Supply of Electricity.

• Creative & innovative regulations for growth

• Partnership dominated sector and huge capital influx:some key players+ many small players

Optimal Electricity Market

• Increasing presence of clean technologies, smart

grids ,cogeneration & distributed generation

• Variable RE (Energy Mix) & Integration to the Grid

• Small producers & responsive consumers

• Energy Saving culture & Use of EE appliances

• Electricity commodity markets & trade

• Interconnected Grid Systems/No interconnections

• State Intervention on projects with weak economics.

• Open & Spot Markets for Players

• GENCOs & DISCOs compete for supply to large

energy users.

Optimal Electricity Market

• Discos service areas(no exclusive rights)

• Free entry, competition across the market

• State, Private & CSO participate in Generation

• captive PPP programmes.

• Market driven Prices(except for users <2MW)

• De-licensing & high level of unregulation

• High collection rate & low Transmission/Distr. losses

• Financial services in rural areas.

• Capital inflow from securitization & local bond market

financing.

• Energy integration with neighboring countries

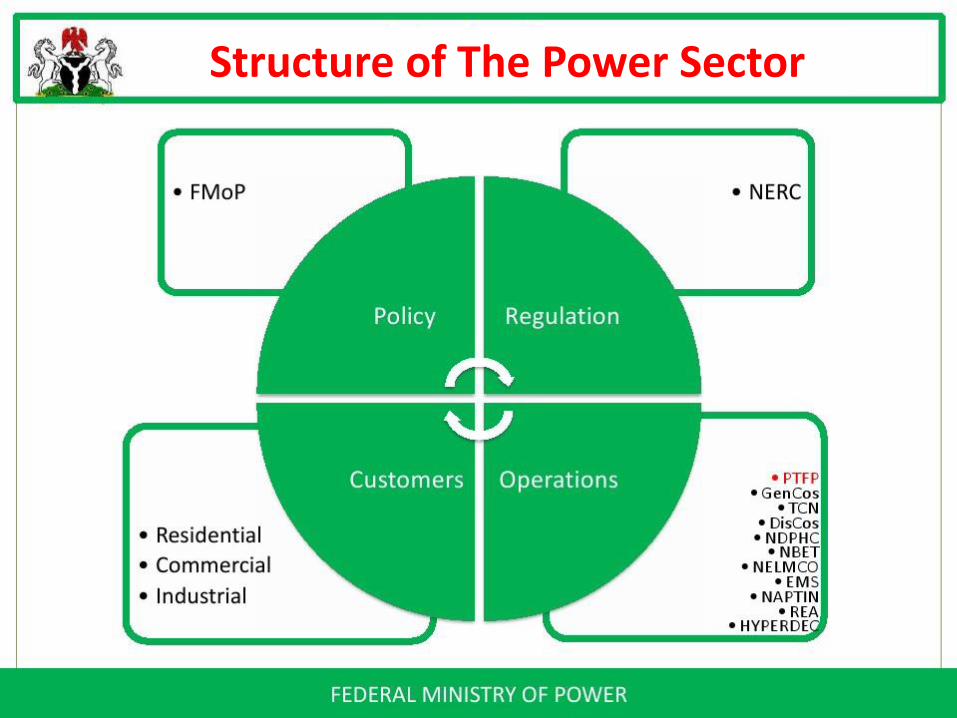

Structure of The Power Sector

Structure of The Power Sector: Ownership & Control

Pre- 2013 Configuration

State of Nigeria Electricity Market

• Strong Policy Framework: Weak Implementation

• Private sector owned :Generation/Distribution

• Govt. Owned Transmission: Poorly Funded

Generation:>85%:Gas (<15%:Hydro) : Poor Energy Mix

• Poor RE & EE. Traction & Demand Side Mgt

Weak Oversight /Unsynchronized & Poor Planning

Gas Shortage:Govt price Capping/fixing (DGSO & GMP)

• Poor Civic Engagement & Customer Service

• Access <50% & >50% (Rural pop):Fuel Wood: no

grid connection/use Agric. Waste & Biomass

Low Innovation(Gas storage,LNG, smart & clean

tech, Research, Diversification etc)

State of Nigeria Electricity Market (Energy Resources)

Status of Nigeria Electricity Market

• (2014 ) > 20GW licensed: 3.8GW ONLY delivered

• Evacuation Capacity : < 5GW & (2020):20GW

• Supply Deficit &Low per capita consumption(149 KWh).

• Monopolistic Operators: Cost recovery focused

• “Cost reflective” (& unrealistic ) tariff (2012)

• 50% of consumers (>2 million) without meters.

• Huge ATC&C losses + Debts as a result

• Low lending & Low investments (NO PPPs)

• Little Policy Creativity (mini grids, soft loans /consumer

programmes, RE & EE, ecofriendly cooking & rural

lighting programmes ,research & incentives)

• Exclusion of MSME operators

Nigeria Electricity Market(Economic Cost)

$40Bn Investment(1991-2011)=(<30GW) got 3GW only

• @$1.3million/1MW =27GW ($36Bn) unaccounted

• 2020 Generation Target of 40GW: $35Bn

• Supply Chain Investment (10yrs) :$10Bn/yr =$100Bn

• Tariff :2009-2014 (N11 -N24 kWh)

• Payment(poor): >N80/kWh (MAN :> N60/kWh)

• Others: N50-70/kWh (self-generation –fossil fuel).

• WHY NOT PAY MORE TO GET INVESTMENT?

• Annual Cost 2020(lost GDP):$130billion (PTFP).

Nigeria Electricity Market(Economic Cost)

• (2012 UNEP Survey) EE =Loss of 30% of Energy

(150 million incandescent bulbs)

• Annual Potential Savings/Loss:$84.9Million & 4TWh,

or 200MW Power Plants =($260Million @ $1.3/MW)

• Energy Saving Potentials: Other Appliances

• Locked-in 600tcf & $476.5Trillion(proven 187tcf)

• Locked-in Ancillary industries in fertilizer,

agriculture, petrochemicals & growth in banking and

finance etc.

• Locked-In $5Billion (2.0bcf/d flares) Gas Plants &

Pipeline network across Nigeria.

• Reduction in GNP & GDP capability

Status of Electricity Market(Social Cost)

>150 Million pop =>150GW (@1MW/1000 pop)

3.8GW (2010)=38Million pop Equiv. (Gap: >146GW)

• Reduction in Industrial production Capability

• Uncompetitiness/Capital flight/Shutdown

• Huge financial burden & Indebtedness of MAN

• Huge Unemployment & Untold hardship

• Youth restiveness, destitution, and prostitutions • Long Blackouts (17-22hrs/d) kill-off Semi Informal

Sector( Loss of Livelihood artisans ,youths and women) • Energy Loss-150Million Incandescent Bulbs:Co2

emissions(581 Kilotonne) & 1.7 Kg of Mercury Emission • Dependence of Fuel wood & Biomass( women and girls) • Risk of smoke ingestion and diseases and possible death.

.

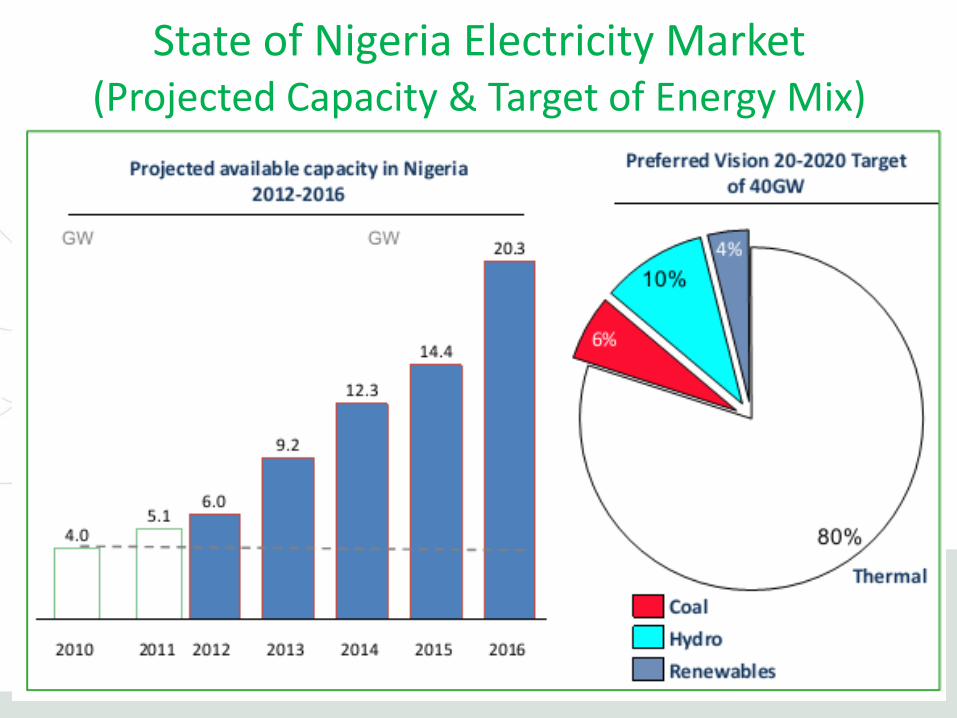

State of Nigeria Electricity Market (Projected Capacity & Target of Energy Mix)

Gas to Power

• Gas reserves:183.5 Tct (600tcf potential)

• Produces: 3.9 bct/d (Export: 2.5 bcf/d)

• Demand : 4 bcf/day (2013) .Flares 2.0bcf/d (AG)

• 2.7bcf/d Power Demand (Gets 1.4bcf/d)

• Domestic and Regional Market Undeveloped.

• Govt. fix prices & Control Market /DGSO

• Production(2016): 8.24 Bcf/d: DGSO (3 Bcf/d).

• <$1-$2 per mcf (mmbtu) till June 2014

• $2.5/mcf + ç80 for transport (June 2014)

• Export parity(2015)

(

19

COMPARISON OF NIGERIAN AND GLOBAL GAS PRICES Nigeria capped and has the lowest gas price <$ 1/mcf.

$1/mcf (June 2012) and $2.5mcf (June 2014) .

Suppliers reported payment recovery difficulties at above rate.

Gas to Power

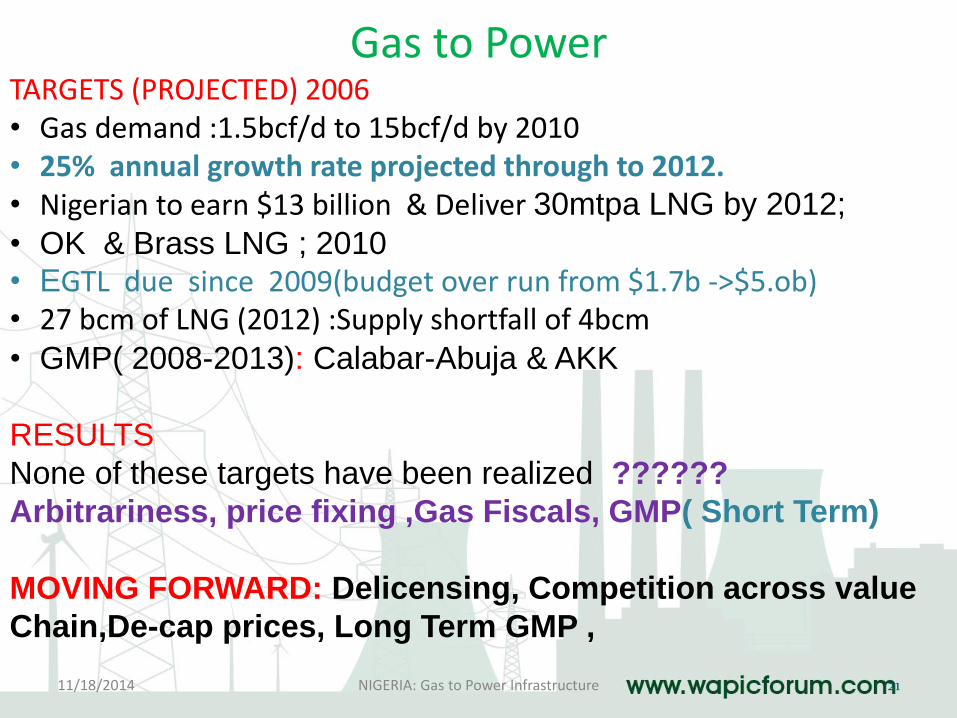

11/18/2014 NIGERIA: Gas to Power Infrastructure 21

TARGETS (PROJECTED) 2006 • Gas demand :1.5bcf/d to 15bcf/d by 2010 • 25% annual growth rate projected through to 2012. • Nigerian to earn $13 billion & Deliver 30mtpa LNG by 2012;

• OK & Brass LNG ; 2010 • EGTL due since 2009(budget over run from $1.7b ->$5.ob) • 27 bcm of LNG (2012) :Supply shortfall of 4bcm • GMP( 2008-2013): Calabar-Abuja & AKK

RESULTS

None of these targets have been realized ??????

Arbitrariness, price fixing ,Gas Fiscals, GMP( Short Term)

MOVING FORWARD: Delicensing, Competition across value

Chain,De-cap prices, Long Term GMP ,

Gas to Power: Demand & Supply

11/18/2014 NIGERIA: Gas to Power Infrastructure 22

Gas to Power Market:Govt. Intervention

Government’s Role in Gas to Power Market

11/18/2014

NIGERIA: Gas to Power Market Suppliers: Gas Producers Consumers: GENCOS

23

Gas to Power Market: Without Govt. Intervention

Suggested Government’s Role in Gas to Power Market

11/18/2014

NIGERIA: Gas to Power Market Supplies :Gas Producing Companies

Consumers: GENCOS

24

Barriers & Impediments

• Inappropriate Energy Mix & Policy Direction

• Investment imbalance on supply & demand side solutions

• Technical reasons (insufficient gas supply, poor maintenance culture, inappropriate use of chemicals, and programmable controllers or other key components)

• Licensing & Weak Due Diligence/Oversight

• Government Ownership of TCN: accountability & regulation

• Inadequate Competition & Micromanagement By NERC

• Weak policy & commercial framework for gas supply

• Arbitrariness (Price fixing, Cross Subsidies,DGSO)

• Weak Incentive Regime & Action on RE & EE Devt.

• Non realistic MYTO pricing regime

Policy Thrust of The Sector Hinged on the EPSR Act 2005

• Privatization & Concession: Improve Access & reduce cost

• Professionalise the management and operations

• Investment on supply side projects & demand side mgt.

• Emphasis gas and hydro generation systems

• Historical: Little attention to maint. & manpower devt.

• Willingness to attract Investments to finance the sector

• Commitment to promote Competitive Electricity Market.

• Intent & Tools Improve revenue: current N10bn to N17.6bn

• Intent and Action Increase and Diversify Energy Mix

• Plans to Increase RE share of generation and Improve

virtual generation/ EE culture

Regulatory Solutions

• Privatize & create competition in Transmission

• Enforce Financial and Technical Due diligence of

Market Operators to meet contract obligations

• Provide Fiscal and Financial Instruments to attract

funds & investments: Set Attractive Tarrifs

• Establish wiling buyer willing seller regime to ensure

cost recovery + impact invests and adequate supply.

• Civic engagement for accountability, ownership,

credibility of cost & pricing.

• Benchmarking & Initiatives to ensure cost efficiency

• Localization of technology and Professional services

• Eliminate subsidies(Promote very Efficient Technologies)

Regulatory Solutions

Incentivize RE & EE projects through

• Subsidize research & project development cost

• Low interest loans & Capital guarantee

• Institute National Debate on Energy Mix

Diversification & support private initiatives

• Main Transmission Tolls Exemptions (full exemptions

for plant producing <10MW & partial for <20MW))

• Establish quota of clean energy production & offtake

for GENCOS & DISCOS respectively

• Access to distribution networks & right to connect into

Grid & sell electricity at spot price.

• Tax breaks:water heating with thermal panels &

bldgs. outfitted with RE/EE systems

Regulations Solutions

• Low interest Loans and guarantees for projects.

• Solar over irrigation canal: harvesting solar energy & reduction of irrigation water loss by evaporation.

• Install pumped-storage hydroelectricity stations

• Long-term PPP concession-based agreements,BOT,BOO, BOOT, transfer of operating rights (TOR) & Contractor Financing

• Support State & Local Govt. to establish RE Parks :land, common services & permits, power evacuation, security etc to reduce cost & stimulate growth of RE

• Institute Consumer financing programmes to enhance affordability and access of the rural poor.

Regulatory Solutions

• Promote Partnerships and mergers to increase capacity of players in the Nigerian Electricity Supply Industry (NESI)

• High quality metering and enhanced audit information flow

• Introduce Availability Based Tariff (ABT) for transmission grid stability.

• Criminalize electricity theft & Collusion by staff & apply stringent penalties ,Special courts and speedy trials.

• Promote family biogas plants, microhydel units and million sq. metres of solar water heating capacity.

Expected Results of an Optimal Market

• Solvent and very profitable electricity sector with key

large and many small players

• Huge influx of investment capital in the various value

chain areas with smart project management

techniques and technology

• Electricity Supply Adequacy from a range of energy

mix and environmentally friendly technologies.

• Civic programmes for both the small scale producers

and the consumers and achievement of universal

access to electricity.

• Increased per capita total electricity consumption ,

National competitiveness and enhanced GDP..

Expected Results of an Optimal Market

• Establishment of allied industries in Gas Storage and

transportation systems such as railway

facilities,LNG Vehicles, Liquefaction and Gasification

Plants.

• Creative market practices: microcredit & innovative

technology for biomass usage & ecological stove

• Unlocking of USD467.5Trillion from the Gas Value Chain & massive growth Industries, Social & gas infrastructure, Financial Institutions.

• Affordable and adequate power act as a catalyst to

address poverty ,scale up productivity, health &

educational indices.

Summary & Conclusion • Huge & Viable Electricity Market Potential exist

• Policy Implementation stalled the ample growth of the

Electricity & Gas Sector and the general economy

• Govt should institute unfettered competitive electricity

and gas markets “willing buyer and willing seller”.

Engage Civic Society to eliminate unsustainable tariffs'

• Unlock revenue stream of $467Tn in the Gas Sector.

• Attract Investment & resources into Power sector.

• Improve GDP & well-being of Nigerians therefrom.

Thank You Q&A

11/18/2014 NIGERIA: Gas to Power Infrastructure 34