Nigeria Maize Value Chain Analysispdf.usaid.gov/pdf_docs/PA00N2C3.pdfThe factors that are inhibiting...

30

October 2012 This publication was produced for review by the United States Agency for International Development. It was prepared by Chemonics International Inc. Nigeria Maize Value Chain Analysis

Transcript of Nigeria Maize Value Chain Analysispdf.usaid.gov/pdf_docs/PA00N2C3.pdfThe factors that are inhibiting...

October 2012 This publication was produced for review by the United States Agency for International Development. It was prepared by Chemonics International Inc.

Nigeria Maize Value Chain Analysis

Nigeria Maize Value Chain Analysis - 2

Nigeria Maize Value Chain Analysis - 3

Nigeria Maize Value Chain Analysis

MARKETS II

Contract No. AID-620-C-12-00001

Submitted to USAID/Nigeria Mission

October 2012 This publication was produced for review by the United States Agency for International Development. It was prepared by Chemonics International Inc.

Nigeria Maize Value Chain Analysis - 4

Nigeria Maize Value Chain Analysis - 5

CONTENTS Executive summary ............................................................................................................ 6 Overview .............................................................................................................................. 7

Feeding Africa ................................................................................................................... 7 Nigeria’s Trade Patterns .................................................................................................... 8

Maize Profile ...................................................................................................................... 10 Supply and Demand ........................................................................................................ 10 Fish Feed Sector Demand .............................................................................................. 11 Value Chain Dynamics .................................................................................................... 12 Value Share .................................................................................................................... 14 Summary......................................................................................................................... 17

Maize Sector Survey ......................................................................................................... 18 Producers........................................................................................................................ 18 Summary......................................................................................................................... 22

Strategic Focus ................................................................................................................. 22 Annex I: Project Background ........................................................................................... 25 Annex II: Research Methodology ..................................................................................... 26 Annex III: References ........................................................................................................ 28 Annex IV: Source of Growth ............................................................................................. 29 Annex V: Voice from the Field ......................................................................................... 30

Nigeria Maize Value Chain Analysis - 6

Executive summary

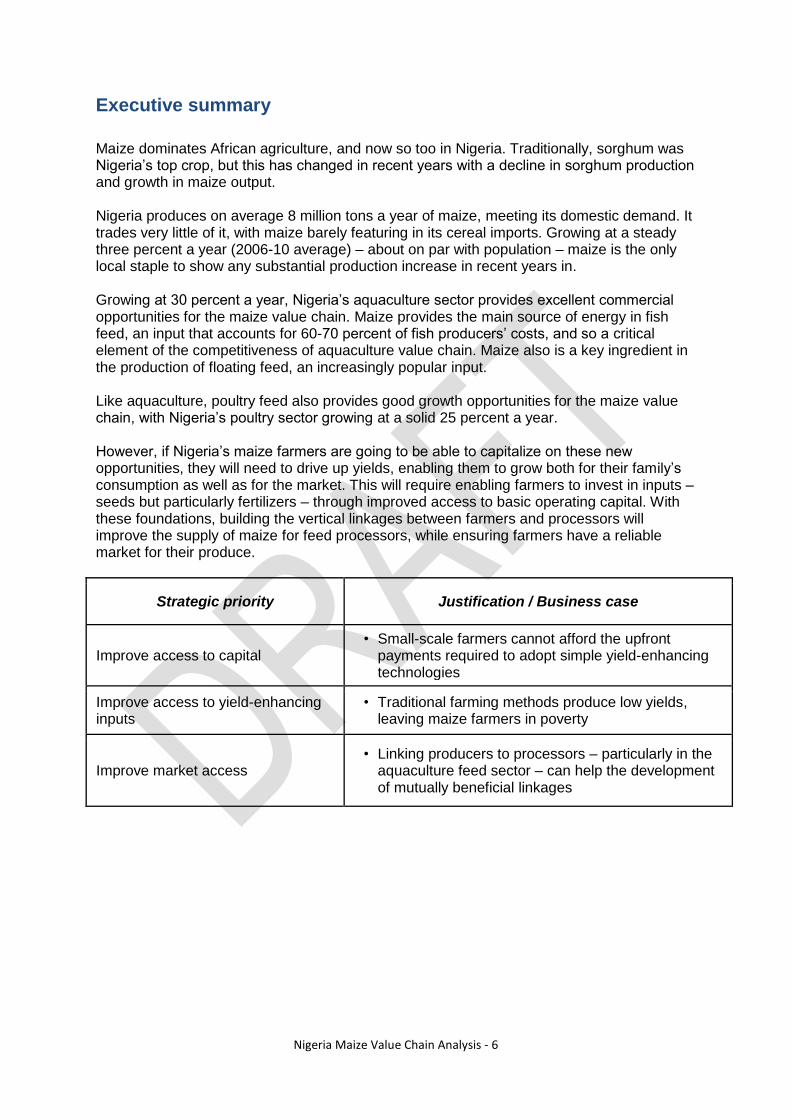

Maize dominates African agriculture, and now so too in Nigeria. Traditionally, sorghum was Nigeria’s top crop, but this has changed in recent years with a decline in sorghum production and growth in maize output. Nigeria produces on average 8 million tons a year of maize, meeting its domestic demand. It trades very little of it, with maize barely featuring in its cereal imports. Growing at a steady three percent a year (2006-10 average) – about on par with population – maize is the only local staple to show any substantial production increase in recent years in. Growing at 30 percent a year, Nigeria’s aquaculture sector provides excellent commercial opportunities for the maize value chain. Maize provides the main source of energy in fish feed, an input that accounts for 60-70 percent of fish producers’ costs, and so a critical element of the competitiveness of aquaculture value chain. Maize also is a key ingredient in the production of floating feed, an increasingly popular input. Like aquaculture, poultry feed also provides good growth opportunities for the maize value chain, with Nigeria’s poultry sector growing at a solid 25 percent a year. However, if Nigeria’s maize farmers are going to be able to capitalize on these new opportunities, they will need to drive up yields, enabling them to grow both for their family’s consumption as well as for the market. This will require enabling farmers to invest in inputs – seeds but particularly fertilizers – through improved access to basic operating capital. With these foundations, building the vertical linkages between farmers and processors will improve the supply of maize for feed processors, while ensuring farmers have a reliable market for their produce.

Strategic priority Justification / Business case

Improve access to capital • Small-scale farmers cannot afford the upfront

payments required to adopt simple yield-enhancing technologies

Improve access to yield-enhancing inputs

• Traditional farming methods produce low yields, leaving maize farmers in poverty

Improve market access • Linking producers to processors – particularly in the

aquaculture feed sector – can help the development of mutually beneficial linkages

Nigeria Maize Value Chain Analysis - 7

Overview

Feeding Africa The world food crisis in 2007-08, during which food prices experienced their sharpest rise in 30 years, leading to food riots in many parts of the world, focused global attention on the importance of agriculture. After decades of neglect, investment in agriculture is now on the rise. A notable example in Sub-Saharan Africa is Malawi, which spent as much as 4.2 percent of its GDP on a fertilizer subsidy scheme that moved the country from being a net importer of grain to an exporter to the region. Unfortunately, the amount of the subsidy was not one Malawi could sustain in the long run. While the situation has temporarily eased, fundamental issues have not gone away. At the heart of the developing world’s agricultural challenge is the basic issue that demand is rising faster than supply can keep up. Population growth, urbanization, and increasing incomes are leading to a shift in consumption from grains to meat in developing countries, requiring greater grain production for feed. In parallel, demand for biofuels is consuming more of the grain production from the large grain exporting countries. On the supply side, land under cultivation has increased but is nearing saturation, and yield growth in cereals is declining, from three to six percent a year levels during the Green Revolution in the 1960s to nearer one to two percent today. In some developing countries, yields are flat.

Not even flat Agricultural production per capita, 1964-2006

Source: The Economist; ―Whatever happened to the food crisis‖; June 2009

Since 1960, output in Africa has increased by 2.4%, while its population has grown at 2.6%, resulting in food aid requirements that are 4 times higher than other regions.

The Food and Agriculture Organization estimates that to keep pace with demand, developing countries will have to double food output by 2050. This amounts to a 70 percent rise in food production.

Nigeria Maize Value Chain Analysis - 8

Nigeria’s Trade Patterns Nigeria’s import base is expectedly diverse, as are its trading partners. While manufactured goods dominate its imports, food products – namely cereals and fish – also feature in its top 10 imports. Import substitution is therefore seen by policy makers as a driver toward achieving self-sufficiency in key agricultural commodities. Oil is king, dominating Nigeria’s exports, enabling the country to run a trade surplus. If one excludes oil, this picture changes dramatically, with imports dwarfing Nigeria’s non-oil exports. Non-oil exports are indeed growing fast, at a rate of 80 percent a year, albeit from a negligible base, as Nigeria diversifies its economy away from dependence on oil.

Top 10 imports Imports by value, US$

Source: International Trade Center data: http://www.trademap.org/; MARKETS II analysis. Note: Value share is 2006-10 average

In exports, oil is king, dominating Nigeria’s exports and enabling the country to formally run a trade surplus. However, excluding oil, this picture changes dramatically, with imports dwarfing Nigeria’s non-oil exports.

The Challenge According to Sachs Writing about the state of agriculture in Africa, economist Jeffery Sachs summarizes the challenge and solutions: ―...many poor countries’...farmers are producing far below what is technologically possible.‖ ―Traditional farming uses few inputs and gets poor yields. Poor peasants use their own seeds from the preceding season, lack fertilizer, depend on rain rather than irrigation, and have little if any mechanization beyond a traditional hoe. Their farms are small, perhaps one hectare (2.5 acres) or less. Under traditional agricultural conditions, the yields of grain – rice, wheat, maize, sorghum, or millet – are usually around one ton per hectare, for one planting season per year.‖ The key: ―There is nothing magic about [a] combination of high-yield seeds, fertilizer, and small-scale irrigation.‖

Import partners, share of value

Nigeria Maize Value Chain Analysis - 9

That said, non-oil exports have been on the rise, meaning that Nigeria is diversifying its economy away from its high oil dependence. It is early days yet, but the signs are very positive, with non-oil exports growing at 80 percent a year (albeit from a negligible base).1 A study that looked at the drivers of Nigeria’s growth compared with other African oil producers showed that oil accounted for only 35 percent of the country’s growth between 2002-07, compared to 86 percent for Angola. Agriculture accounted for an encouraging 27 percent of Nigeria’s growth, and services for 37 percent. However, manufacturing accounted for a paltry one percent of total growth, which is concerning for the agricultural processing sector. The factors that are inhibiting the growth of the manufacturing sector in Nigeria will similarly affect agricultural processors, from the erratic availability of power to the high costs of transportation.

Top 10 exports Exports by value, US$

Imports vs. exports, US$

Source: International Trade Center data: http://www.trademap.org/; MARKETS II analysis.

1 International Trade Center database: http://www.trademap.org/

Non-oil imports vs. exports, US$

Nigeria Maize Value Chain Analysis - 10

Maize Profile

Supply and Demand Maize is on the rise in Nigeria. With production growing steadily at three percent a year (2006-10 average), about on par with population growth, maize is the only locally produced staple that has exhibited any substantial production increase in recent years, supplanting sorghum as Nigeria’s top grain in terms of output. Nigeria produces on average 8 million tons a year of maize, which is largely what it consumes. It trades very little of it, with maize barely featuring in its cereal imports.

Preferred staples Share of acreage under cultivation across SSA

Source: HighQuest Partners, ―Market Potential of Sub-Saharan Africa: Prepared for the United States Soybean Export Council,‖ 2011; International Trade Center data: http://www.trademap.org/; MARKETS II analysis

The decline of sorghum production and the rise of maize are relatively recent, and have not as yet received much attention at a policy level. It is not as yet certain what is driving this change. Maize and sorghum sector stakeholders believe that part of the explanation is due to declining soil quality, which requires sorghum farmers to use fertilizer to achieve the yields that they are traditionally accustomed to. However, if they are to use fertilizer – which they are not accustomed to doing with sorghum – they believe that they may as well plant maize, which can give them higher returns. The increase in production may also be driven by the animal feed sector: the poultry sector, which is growing at 25 percent a year, but in particular the fish feed sector, which has been growing at 30 percent a year. It is on these prospects for the use of maize in Nigeria’s fish feed sector that MARKETS II is particularly focusing its attention.2

2 International Trade Center data: http://www.trademap.org/; United States Department of Agriculture, Foreign

Agricultural Service database: http://www.fas.usda.gov/psdonline/psdQuery.aspx; PIND, ―A Report on Aquaculture Value Chain Analysis in the Niger Delta,‖ 2011.

Nigeria’s grain imports, US$

Nigeria Maize Value Chain Analysis - 11

Quiet rise

Increased maize production in Nigeria, tons

Source: United States Department of Agriculture, Foreign Agricultural Service database: http://www.fas.usda.gov/psdonline/psdQuery.aspx

Fish Feed Sector Demand With its continued growth, Nigeria’s aquaculture sector provides excellent commercial opportunities for the maize value chain. Fish feed producers must balance cost with convertibility – the ratio of feed required to produce 1 kg of fish flesh. The overriding concern with feed composition is protein content, derived mainly from a mix of fish meal (and other animal protein sources) and oil seed-based proteins, most commonly from soybean meal. However, beyond protein, fish feed must respond to energy needs, derived mainly from maize. Maize also plays in important role in the floatability of feed. As a crucial ingredient in fish feed, the competitiveness of the aquaculture sector hinges on the maize sector, as fish feed accounts for 60-70 percent of all aquaculture production costs. In Nigeria, farmers and feed makers are also experimenting with cassava peel as a substitute carbohydrate source to maize. However, it has a much higher (and so worse) conversion ratio: 1 kg of fish flesh requires 10-20 kg of cassava peel, compared to 4-6 kg of maize. Though, maize prices are about 5 times higher than cassava peel. The fish feed sector therefore offers great commercial opportunities for maize producers. In addition to fish feed, there are also good opportunities in poultry feed, with Nigeria’s poultry sector growing at 25% or higher a year.3

3 Mississippi State University, ―Catfish nutrition: Feeds and feed formulation,‖ July 2006.

Nigeria Maize Value Chain Analysis - 12

Catfish feed formulations

(% share of feed)

Source: Mississippi State University, ―Catfish nutrition: Feeds and feed formulation,‖ July 2006; % indicates protein content’ MARKETS II field research and interviews.

Value Chain Dynamics Opportunities for improving the competitive profile of the maize value chain exist across the sector. However, as an established crop, there are few areas that are comparatively undeveloped, with the exception of the relatively recent fish feed sector and the business services related to it. However, support to access inputs for maize farming is required, from access to high-yielding seed varieties and agro-chemicals to increased mechanization. If these technologies are to be mobilized, access to finance at the farm-level will be necessary as well as technical assistance to support maize farmers in adopting new practices.

Key value chain actors

Nigeria Maize Value Chain Analysis - 13

Source: MARKETS II analysis; competitiveness rating is approximation.

Nigeria Maize Value Chain Analysis - 14

Value Share Fertilizers and herbicides form a substantial portion of production costs (after labor and transportation), which in part explains farmers’ reluctance or inability to take full advantage of them. Lack of fertilizers and herbicides has left maize yields stubbornly fixed around the 1.5 ton/ha average that Nigeria and much of Sub-Saharan Africa achieves.4

4 A. S. Olomola, ―Competitive commercial agriculture in Africa study (CCAA): Nigeria case study,‖ 2007.

Systems from the field: Credit and Inputs through Partnership Nigeria’s agricultural sector lacks adequate capital at every level: too little investment in processing, limited working capital for intermediaries, and few appropriate financial products, such as leasing and smallholder credit, to address farmers’ needs. At the same time, support to Nigeria’s financial institutions has been substantial, with loan guarantee funds and credit schemes from the Central Bank of Nigeria and donors. The biggest challenge that stakeholders face when trying to access credit is the inability of financial institutions to provide credit at the producer level. From the banks’ perspective, producers are unorganized and transaction costs are high. Even when adopting a value chain approach to finance, banks and processors face side selling by the farmers which can result in loan defaults. However, a new partnership has been formed to address these problems, between Plateau state’s farmers, Grand Cereals Limited (GCL), Agricultural Service & Training Centre (ASTC) – a private services company established in between Plateau state government in partnership with an Israeli firm, and Stanbic Bank. ASTC’s goal is to raise agricultural production levels, boost yields, and improve produce quality while improving farmers’ livelihoods in the state. ASTC provides mechanized agricultural services such as tillage, ridging, planting, spraying, weeding, harvesting, and shelling as well as fee-based input provision including hybrid seeds, high quality fertilizer and pesticides, extension services, and financial advisory services. Under this arrangement, Plateau’s framers, ASTC, GCL and Stanbic agree that:

The total cost of production per hectare is measured

Stanbic provides credit to farmers

ASTC provides all inputs and services to ensure optimal farmer yields

GCL provides a ready market for the farmers’ maize production at the end of the season

All stakeholders jointly value the farmers’ produce which is then delivered to GCL with help from ASTC

GCL then pays into the farmers bank accounts at Stanbic after the outstanding loan is deducted.

Though still its early stages, this system appears to be working well. Loans to farmers are approved quickly by the bank, giving farmers access to credit when they need it. ASTC is able to provide expertise and inputs to help boost yields. GCL receives high quality raw materials in the right quantity at the right time. Stanbic facilitates these transactions and begins to form relationships with farmers in the area – who, if they continue to succeed through this system, will be good future clients for the bank.

Nigeria Maize Value Chain Analysis - 15

Increasing yields and returns Value distribution, average across Nigeria in Naira

Source: A. S. Olomola, ―Competitive commercial agriculture in Africa study (CCAA): Nigeria case study,‖ 2007; Cost analysis data from NISER, 2001 in Olomola.

However, if Nigeria’s maize farmers are to break through the 1.5 tons/ha ceiling, they will have to spend more upfront on inputs. When modeling a typical maize farm in Nigeria, the MARKETS II field team developed two scenarios, based on common practices and data from two sets of informants from the field: a number of subsistence farmers and a number of mid-sized commercial farmers. The results confirmed that fertilizers in particular play a crucial role in driving up maize yields per hectare, and with it farmer margins. However, this requires a fertilizer outlay of more than double of that which a typical subsistence farmer spends. But without this expenditure, they are unable to generate enough surplus maize to buy sufficient quantities of yield-enhancing fertilizer for the next season. They are caught in a vicious cycle. Breaking out of it will require access to finance.

Increases in spending on inputs can yield good returns in end-margins

Stubbornly fixed, yields in tons/ha

Nigeria Maize Value Chain Analysis - 16

Production costs Farm-level costs/margins, Naira/ton

Source: MARKETS II data and analysis.

Nigeria Maize Value Chain Analysis - 17

Summary

Major growth in human maize consumption is not likely to occur in Nigeria beyond the rate of population growth.

However, demand from the animal feed industry will increase, particularly as Nigeria follows global trends of increased meat consumption with rising incomes.

There are signs that Nigeria’s farmers are responding to this, with maize production on the rise.

However, this response will be held back unless they are able to make the small, but critical investments required to increase yields. This will require greater access to agricultural credit at the farm level, for the purchase of higher yielding seed varieties and the use of fertilizers.

Voice from the Field: Cultivating the Adoption of Improved Practices Saminaka is a traditional farming community in Northern Nigeria. A leader in maize cultivation, the community also grows other crops like groundnut and soybeans. The Saminaka farmer is not different from other farmers across the country. He adopts a mixed variety of farming practices with an estimated 20% of farmers using only traditional methods, 40% utilizing a mix of traditional and improved methods, and another 40% more rigorously applying improved modern techniques. Years of farming in Saminaka has shown that maize farmers who employ traditional methods harvest between 0.5-1.5 tons per hectare, while those adopting improved practices can harvest between 4.5-5 tons per hectare. Hannatu Soni, a female maize farmer from Saminaka, has experienced the labor and yields of both agricultural methods. In 2005, Hannatu rented a 5 hectare piece of land for 5 years. After the first three years of cultivation, she was unimpressed with her output. She felt that she had gone into maize production without fully understanding the elements and techniques required. So she contacted an extension agent from her state’s agricultural development program who introduced her to modern farming techniques. Her yield per hectare jumped from 1.5 to 4.5 tons. Applying improved agronomic techniques requires a holistic approach. It involves other factors like access to finance for farmers to purchase quality inputs at the right time and the availability of extension services and agents to fill technical knowledge gaps and provide guidance. It also requires access to premium markets to motivate quality farmers. Hannatu sells her produce to Grand Cereals Limited, a feed producing company in Jos, which provides a guaranteed market. Improved farming techniques lie at the heart of driving productivity improvements at the farm level. Coupled with new market opportunities in the animal feed sector, the two present great opportunities for improving the livelihood of Nigerian maize farmers like Hannatu.

Nigeria Maize Value Chain Analysis - 18

Maize Sector Survey MARKETS II conducted a survey of Nigeria’s maize sector during August and September 2012, spending over 20 days in the field interviewing 64 sector participants involved in maize production, processing, input and other service supply, and policy formulation. The survey also included four focus group discussions with between seven to eight participants per session. The results of the field survey are reviewed below.

Producers Most survey respondents are in Kaduna and have mid-sized farms between one to five hectares. However, they are not exclusively maize farmers, with soybean – largely a cash crop – being commonly intercropped.

Overview

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Nigeria Maize Value Chain Analysis - 19

Soft capital

The respondents are quite well educated, with over a quarter having tertiary education. The majority belong to cooperatives, enjoying a wide range of benefits from marketing support, to input access, to general capacity building.

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Inputs

Hired labor is commonly used for land preparation. Hybrid seed usage is reasonably high, with most being privately supplied.

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Yields, sales, margins

Both yields and prices have increased, which should lead to farmers feeling better off. (Reported average yields from the survey respondents of between 3-3.5 ton/ha are generally higher than the subsistence farmer model of 1.5 tons/ha). However, when asked whether they feel that prices – of their inputs and outputs – have increased, decreased or stayed the same, the vast majority of the respondents feel that they had increased. While sales have increased, the general impression is that they have trailed the increase in costs. All of the surveyed farmers are feeling price inflation. Most sales are on the open market (40 percent) or directly to processors (33 percent).

Nigeria Maize Value Chain Analysis - 20

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Structural challenges

Access to capital comes from sources close to home, mainly cooperatives and friends and family. Respondents report that other sources are difficult to access. Climate change is felt mainly through drought and pests, though not to a high degree.

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Nigeria Maize Value Chain Analysis - 21

Constraints and suggested solutions

Farming constraints and respondents’ suggested solutions do not match up cleanly. However, a fairly clear demand for improved access to inputs – seeds and fertilizer – emerges. The maize farmers interviewed are fully aware that they are under performing, and are looking for support in access to basic yield enhancing technologies. However, marketing and market access remain ambiguous, with marketing featuring as a major constraint, but market access is not commonly cited as a key solution.

Source: Markets II maize VC survey, n=64 for whole maize survey set, 50 of which are producers.

Voice from the Field: The Need for Women’s Empowerment Women are essential to the economic development of any country or sector, yet despite their central role in Nigerian agriculture they experience discrimination in their access to key factors of production: land, finance, labor and knowledge. Restricted access to land limits a woman’s ability to access credit because of collateral requirements, while a lack of education puts women at a disadvantage in terms of their ability to adopt modern farming technologies. Ayisha, a maize farmer, says, ―I had to marry because my parents refused to send me to school, not because I did not want to be educated, but because our culture does not allow girls to go to school. It is believed that an educated girl will take the benefit of her education to her husband’s house. I am still interested in schooling but my husband has little money, so I have had to look for funding from other sources.‖ Ayisha is now planning to start going to school on a part-time basis, saying with a broad smile, ―I cannot wait to start school. If I am educated, I can interact with other women, and I can learn new things that will help me expand my farm. Even if I don’t inherit land I can buy more land, join associations and speak out. I will keep good records. My husband and my community will respect me.‖ Ayisha is one of many women in rural Nigeria who are striving to break through cultural limitations. To help them make up for lost opportunities, financial programs have to be targeted specifically towards women, ideally combined with literacy programs too. This will help to build the role of women in household and community decision-making, and bolster their control over the ever-vital factors of production.

Nigeria Maize Value Chain Analysis - 22

Summary

Maize is farmed along with other crops, prominently soybean.

Both prices and yields have moved upwards, but yields have moved more slowly.

Seeds are sourced from the market, but the market does not seem to be working well – seed access is a major constraint.

Commercial capital sources are not readily available, an area of concern in light of the high interest in improving producers’ access to inputs.

Focus Group Findings • Most maize farmers intercrop. • Small scale farmers join associations to share ideas and access inputs at bulk

purchase prices. • Fertilizer and seeds are big issues to small-scale farmers because of a lack of

resources, so access to capital is crucial. • Input dealers are generally reliable sources for timely inputs but expensive. • Interviewees feel it is easier to get seeds than fertilizer because: ―We can reuse our

old seed, but we cannot farm fertilizer.‖ • Storage facilities are essential to enabling farmers to hold their produce for when

prices are higher. • Participants do not feel that they have ready access to large markets. The open

market remains the most accessible, referred to as ―old reliable.‖ • Culture plays a key role in women’s participation in maize farming. Boys are initiated

into farming at a young age and are assigned a small portion of the farm. The same does not occur for girls, reducing their claim to the family farm and inhibiting their agricultural knowledge development.

Nigeria Maize Value Chain Analysis - 23

Strategic Focus

The preceding analysis was presented to maize sector stakeholders – producers, processors, input and service providers, and policy-makers – during a half-day workshop. The objective was to develop a common understanding of the current status of the maize sector in Nigeria and jointly develop a core set of strategic priorities around which MARKETS II could focus its efforts in support of the sector. These strategic priorities are presented below, and mapped to thematic focus areas against which MARKETS II has committed resources. These thematic areas are: inputs, finance, technology development and deployment, water and soil management, capacity building, climate change, information and communication technology (ICT), and women and youth. These strategic priorities and many of the actions listed for each will form the foundations for many of MARKETS II’s implementation activities.

Priority Justification / Business

case Suggested actions Thematic focus

• Improve access to capital

• Small-scale farmers cannot afford the upfront payment required to adopt simple yield-enhancing technologies

• Assess input access barriers and develop solutions

• Train banks on maize farmers’ finance needs, encouraging establishment of desk officers focused on agricultural finance

• Track progress

• Inputs • Finance • Capacity

building • Women and

youth

• Improve access to yield-enhancing inputs

• Traditional farming methods produce low yields

• This leaves maize farmers in poverty

• Support research institutes in production of breeder/foundation seeds

• Conduct soil survey in high-density maize areas and develop tailored fertilizer usage recommendations

• Develop means to improve distribution to the farm-level of seeds and fertilizers, tapping seed/fertilizer companies, input dealers, and processors

• Train farmers and dealers on usage

• Inputs • Technology • Water and soil

management • Capacity

building • Climate change • Women and

youth

Nigeria Maize Value Chain Analysis - 24

• Improve market access

• Linking producers to processors – particularly from the aquaculture feed sector – can help the development of mutually beneficial linkages

• Develop fora for linking producers to processors

• Support clustering of producers around key processors, particularly fish feed

• Develop systems for product aggregation and storage to reduce costs and post-harvest losses

• Develop systems to distribute up to date price information

• Capacity building

• ICT • Women and

youth

Nigeria Maize Value Chain Analysis - 25

Annex I: Project Background The MARKETS II project began in late April 2012 with the objective to increase the

competitiveness of selected agricultural commodity value chains by strengthening linkages

between value chain actors, improving access to inputs and finance, deploying and

disseminating technologies to new users, and by building the capacity of all value chain

actors through technical assistance.

MARKETS II builds off the success of the MARKETS (2005 – 2010) and Bridge to

MARKETS II (2011 – 2012) projects. It is designed to go deeper in fewer value chains (four

to five), and achieve greater impact. Furthermore, MARKETS II is expected to concentrate

its efforts in up to ten key states. By concentrating its resources on a reduced number of

value chains and states, USAID will be better able to assess its impact on targeted value

chains and beneficiaries.

In May 2012, a number of selection criteria were developed to select value chains for further

analysis. These criteria included low-entry threshold for women, youth, and vulnerable

groups; the geographical spread of the commodity; the importance of the commodity in the

GON Agricultural Transformation Agenda; the possibility of deploying new, low-cost

technologies; and whether the commodity falls within the MARKETS II smallholder farmer

mandate.

Based on this selection process, the following value chains were selected for further

analysis: cassava, sorghum, rice, cocoa, and aquaculture. Maize and soybean were also

selected as they are the main ingredients of fish feed, and the lack of quality fish feed is one

of the primary constraints of the aquaculture value chain.

Teams of MARKETS II staff and locally hired value chain experts conducted field research

using questionnaires with key informants and holding open ended focus group discussions

with a large number of stakeholders including producers, processors, traders, input

suppliers, service providers, and policy makers.5

A series of half day validation work shops were organized with participation of a cross-section of the stakeholders surveyed. The methodology is described in further detail in Annex II.

5 A detailed description of the survey methodology can be found in Annex I.

Nigeria Maize Value Chain Analysis - 26

Annex II: Survey Methodology

Timing

The Value Chain Analysis survey for seven commodities was carried out between August

14th and September 7th, 2012. The survey was preceded by a weeklong training on value

chain principles, MARKETS II intervention areas, and survey administration. During this

period survey questionnaires were developed. Data analysis began on September 10th and

continued through October 10th. Seven half day validation workshops were organized

between September 17th and 20th and included active participation by of a cross section of

the stakeholders interviewed during the survey.

The team

The entire MARKETS II technical team, including subcontractors, participated in the study.

Seven senior Nigerian consultants served as value chain team leaders. A total of 25 people

were involved in the survey work with administrative and management support from

MARKETS II. Two international consultants also assisted a key phases of the process—one

for training and start-up and one for data analysis, stakeholder validation and final document

preparation.

Value chain teams and states covered

Eleven teams were formed to cover the seven commodities across 20 states. Each team

contained at least one female staff member to make sure that gender-sensitive questions

could be addressed in mixed or all female focus groups without problems.

Commodity Number of teams States Cassava 1 Oyo, Ondo, Edo, Ogun

Cocoa 2 Cross River, Ondo, Oyo, Osun

Rice 2 Kano, Jigawa, Kebbi, Ebonyi, Anambra, Benue

Sorghum 2 Kano, Katsina, Kaduna

Aquaculture 1 Edo, Osun, Oyo, FCT, Lagos, Ogun

Maize 2 Kaduna, Plateau, Nassarawa

Soybean 1 Nassarawa, Kaduna, Niger, Benue

Target value chain stakeholders

The following stakeholders were targeted:

Producers (small and large scale)

Processors (small and large scale)

Service providers (mechanization, spraying, transporters, etc)

Policy makers (MARD, ADP)

Input dealers

Traders

Nigeria Maize Value Chain Analysis - 27

Survey tools

The teams used both structured key informant interviews and focus group discussions to

carry out the research. The table below presents the number of people interviewed through

both key informant interviews and focus group discussions.

Commodity Interviews

Maize 65 Rice 89 Soybean 40

Cocoa 85 Aquaculture 78 Sorghum 89 Cassava6 41

Service providers

All the MARKETS II service providers (5) were subcontracted to assist the value chain teams

with setting up meetings with key informants and focus groups and to help with translation

where necessary. They were specifically instructed to identify key informants among crop

association members, non-associated farmers, marketers, processors, input dealers,

extension agents, grain purchasers, women and youth groups, technology and service

providers, financial institutions and wholesalers and retailers and to assemble focus groups

consisting of male and female farmers, youth, extension agents, small processors,

cooperative groups, traders etc. Due to time constraints, it is possible that the selection of

producers was skewed towards producers that worked with MARKETS and BtM2 before.

The service providers played a key role in the survey process and made rapid progress

possible.

Data input and analysis

Data input was done by a team of three people and supervised by a data analyst. Value

chain teams sent completed questionnaires on a weekly basis to Abuja so that data input

was a continuous process during the survey. However, template development and data input

took longer than expected and, in some cases, delayed data analysis.

6 The number of actual interviews for cassava is disappointing but can be explained by the fact that it was a

single team covering a large area. The same is true for the soybean value chain team.

Nigeria Maize Value Chain Analysis - 28

Annex III: References The core source of data and insight that drives this value chain analysis is a aquaculture field survey conducted during August and September 2012, during which 62 sector participants were interviewed, and 4 focus group discussions held (with between 7-8 participants per session). In addition, detailed input from sector stakeholders was solicited during a half-day workshop at which the initial findings were discussed and the strategic priorities jointly developed. Finally, the following reports and research were also drawn upon:

The Economist, ―Whatever happened to the food crisis,‖ June 2009

The Economist, ―If food were words, nobody would go hungry,‖ Nov. 2009

The Economist, ―How to feed the world, ‖Nov. 2009

HighQuest Partners, ―Market Potential of Sub-Saharan Africa: Prepared for the United States Soybean Export Council,‖ 2011

International Trade Center database: http://www.trademap.org/

McKinsey Global Institute, ―Lions on the move: The progress and potential of African economies,‖ June 2010

Mississippi State University, ―Catfish nutrition: Feeds and feed formulation,‖ July 2006

A. S. Olomola, ―Competitive commercial agriculture in Africa study (CCAA): Nigeria case study,‖ 2007

PIND, ―A Report on Aquaculture Value Chain Analysis in the Niger Delta,‖ 2011

J. Sachs, ―A new deal for poor farmers,‖ Project Syndicate, June 2008

United States Department of Agriculture, Foreign Agricultural Service database: http://www.fas.usda.gov/psdonline/psdQuery.aspx

Value Chain Development Wiki: http://apps.develebridge.net/amap/index.php/Value_Chain_Development

Nigeria Maize Value Chain Analysis - 29

Annex IV: Source of Growth

Analysis by the McKinsey Global Institute of GDP growth by industry sector found that

Nigeria was more diversified than other oil exporting countries in Africa. While oil accounted

for 31 percent of all growth, agriculture accounted for 27 percent of GDP growth. However,

manufacturing accounted for only 1 percent of all growth, which does not bode well for the

development of the agricultural processing sector. The factors that are inhibiting the growth

of the manufacturing sector in Nigeria will similarly affect agricultural processors, from the

sporadic availability of power to the high cost of transportation.

Source of growth (Real GDP growth, 2002-07)

Source: McKinsey Global Institute, ―Lions on the move: The progress and potential of African economies,‖ June 2010.

While agriculturals have done well, the weak response of manufacturing does not bode well for agricultural processing in Nigeria

Nigeria Maize Value Chain Analysis - 30

Annex V: Voice from the Field Women are essential to the economic development of any country or sector, yet despite their central role in Nigerian agriculture they experience discrimination in their access to key factors of production: land, finance, labor and knowledge. Restricted access to land limits a woman’s ability to access credit because of collateral requirements, while a lack of education puts women at a disadvantage in terms of their ability to adopt modern farming technologies. Ayisha, a maize farmer, says, ―I had to marry because my parents refused to send me to school, not because I did not want to be educated, but because our culture does not allow girls to go to school. It is believed that an educated girl will take the benefit of her education to her husband’s house. I am still interested in schooling but my husband has little money, so I have had to look for funding from other sources.‖ Ayisha is now planning to start going to school on a part-time basis, saying with a broad smile, ―I cannot wait to start school. If I am educated, I can interact with other women, and I can learn new things that will help me expand my farm. Even if I don’t inherit land I can buy more land, join associations and speak out. I will keep good records. My husband and my community will respect me.‖ Ayisha is one of many women in rural Nigeria who are striving to break through cultural limitations. To help them make up for lost opportunities, financial programs have to be targeted specifically towards women, ideally combined with literacy programs too. This will help to build the role of women in household and community decision-making, and bolster their control over the ever-vital factors of production.