Nielsen Consumer Post Recession Report Sept09

17

Consumers in a Post-Recession World: A Nielsen Report September 2009

-

Upload

marketingfacts -

Category

Self Improvement

-

view

2.181 -

download

2

Transcript of Nielsen Consumer Post Recession Report Sept09

Consumers in a Post-RecessionWorld: A Nielsen Report

September 2009

2

How has the deepest global recession since the Great Depression of the 20th Century affected consumers globally?

Global banks have returned to profit, restoring confidence in a new financial structure. Stimulus plans put into action by governments are starting to take effect and the IMF has revised a more positive forecast for economic growth and recovery in the next year. But how has the deepest global recession since the Great Depression affected consumers globally? In this report, Nielsen uncovers how consumers in different regions will embrace the post-recession world and how recessionary habits may prove harder to break for consumers in the US and Europe – compared to consumers in BRIC markets (Brazil, Russia, India, China) and Asia - who are preparing to spend their way into prosperous times again.

3

Consumers in a Post Recession World

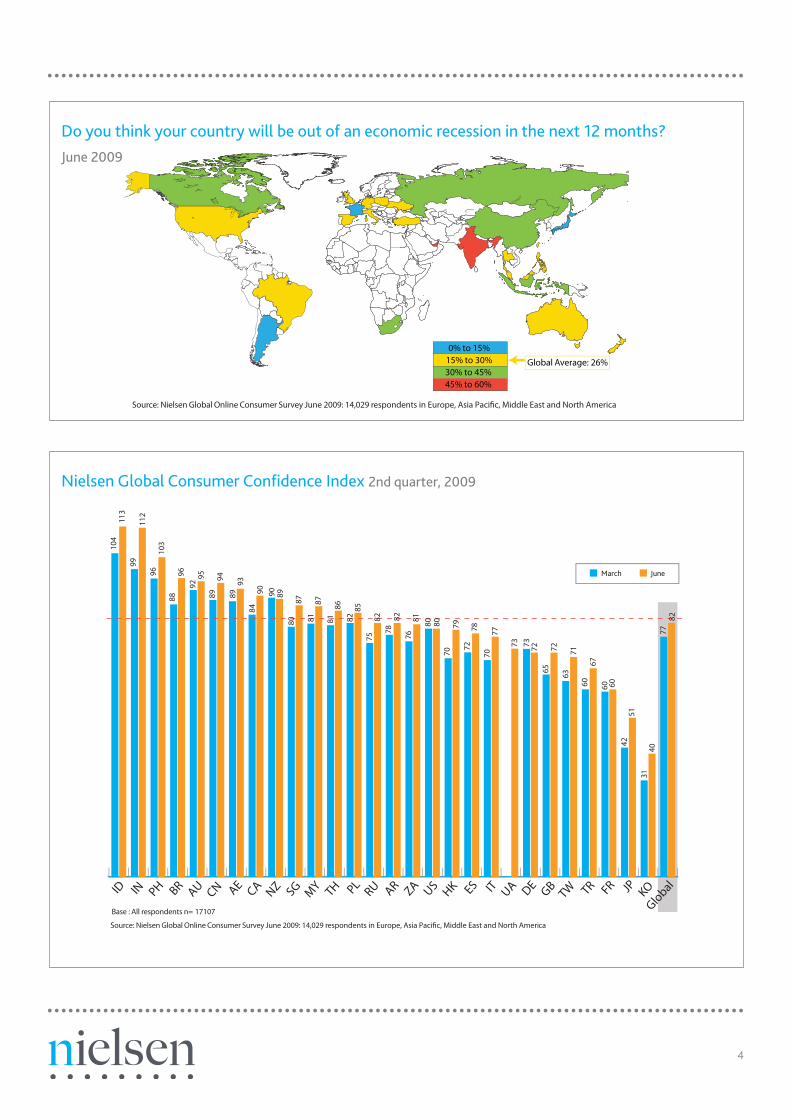

Hopes for a full economic recovery accelerated in 26 out of 28 major global markets in the 2nd Quarter of 2009 according to the latest Nielsen Global Consumer Confidence Index conducted in late June 2009. Driven by renewed consumer optimism and stock market gains in BRIC and key Asian markets, the Nielsen Global Consumer Confidence Index rose five Index points to 82 from 77. In addition, the number of consumers and countries who believe their economy is currently in recession declined six Index points in the last three months, with the most positive feelings of recovery emanating from the BRIC and Asian markets. In the last few months, consumers and market sentiment has switched from recession to recovery – signaling a major turning point for the Global Financial Crisis.

4

Global

KOJPFRTR

TWGBDEUAITESHKUSZAARRUPLTHMYSGNZCAAE

CNAUBRPHINID10

411

399

112

9610

388

9692

9589

9489

9384

90 90 8980

8781

8781

8682

8575

8278

8276

81 80 8070

7972

7870

77

73 73 7265

7263

7160

6760 60

4251

3140

7782

Base : All respondents n= 17107

March June

Source: Nielsen Global Online Consumer Survey June 2009: 14,029 respondents in Europe, Asia Paci�c, Middle East and North America

Nielsen Global Consumer Confidence Index 2nd quarter, 2009

Global Average: 26%

0% to 15%15% to 30%30% to 45%45% to 60%

Source: Nielsen Global Online Consumer Survey June 2009: 14,029 respondents in Europe, Asia Paci�c, Middle East and North America

Do you think your country will be out of an economic recession in the next 12 months?June 2009

5

Cautious Consumers

And while talk of a global recession may be receding, many consumers plan to hold on to their thrifty recessionary habits, according to a Nielsen study on consumers in the post-recession world.

The severity of this recession has brought about a change in consumer values, spending habits and lifestyle choices in many parts of the world, with some indication that consumers in the West will continue to refrain from excessive or unnecessary spending across all aspects of their lifestyles - at least in the short term.

Many consumers who cut back on new clothes, out-of-home entertainment and take-away meals and switched to cheaper grocery brands to make ends meet plan to stick to these new habits even when economic conditions improve, according to a recent Nielsen survey of 52 global markets. Even though consumer confidence is returning in most countries, the tactics and cutbacks that consumers adopted for the recession may be here to stay for many Europeans, Pacific and American consumers. Forty eight percent of Americans say they will continue to save on gas/electricity bills, 22 percent of Australians will continue to cut down on take-away meals and 23 percent of French say they will continue to use their car less.

3 2 2 24 3

2927

23

38

28 29

49 48

55

40

4547

17

21 20 1920

19

0

20

40

60

80

100

AP EU MEAP LA NA Global Average

Excellent Good Not so good BadBase : All respondents n = 17107

Source: Nielsen Global Online Consumer Omnibus June 2009: 14,029 respondents in Europe, Asia Paci�c, Middle East and North America

Perceptions of now being a good or bad time for people to buy the things they want and need

6

According to the Nielsen survey, nearly one in three (29%) global consumers will continue to economise on gas and electricity, while one in six will continue to cut down on take-away meals. One in six global consumers will continue to purchase cheaper grocery products, spend less on new clothes, cut down on out-of-home entertainment and one in seven will reduce telephone expenses.

Saving on gas and electricity, cutting down on take-away meals and spending less on new clothes (and switching to cheaper groceries) are key global trends today that may stick in the post recession world. On a regional basis, Pacific, North American and Western European consumers will continue to switch to cheaper grocery products, while consumers in the

emerging markets of South Africa, Turkey and Latin America will try to reduce telephone expenses in the post-recession era. Of all regions, Europeans will still be watching their expenditure on out-of-home entertainment most closely.

Not surprisingly, consumers in the US and Europe -- hardest hit by the global recession -- are most determined to cling to future cost saving measures in the post-recession world. Consumers in the BRIC markets, on the other hand, are generally looking forward to putting recent recessionary behaviours behind them and returning to their previous spending patterns, especially Chinese and Russian consumers.

5349

46 4541

3634 34 34 33

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RU CN UA PH BR PL DE FR AR IN

Source: Nielsen Global Online Consumer Survey June 2009: 14,029 respondents in Europe, Asia Pacific, Middle East and North America

Russian and Chinese consumers are utilizing spare cash to keep up with latest fashion trendsTop 10 countries who spend spare cash on purchasing new clothes

7

In the latest Nielsen Consumer Confidence Survey, BRIC and Asian markets scored the greatest increases in Consumer Confidence Indices in the past three months. The Confidence Index climbed 13 points in India and rose eight points in Russia and Brazil.

While the BRIC markets did not escape the ravages of the global recession, the downturn is unlikely to have a marked long-term impact on consumer behaviour. Unlike their Western counterparts, resilient and adaptable BRIC consumers simply tightened their belts temporarily and will soon return to their previous spending habits and lifestyle. The experience of previous economic crises in Latin America in particular has produced a very adaptable consumer who had learnt to act quickly and make necessary lifestyle cuts during downturns. Among the BRIC nations and perhaps all nations globally, the Chinese today remain the most confident of an economic rebound in the near future. In the Nielsen Global Confidence

Survey conducted in March 2009, China recorded just a seven point drop in consumer confidence in the past six months compared to double-digit declines in Russia, Brazil and India. In the latest Nielsen Consumer Confidence Index in late June, consumer confidence in China increased six Index points.

Despite the global recession hitting hard in 2008, China still managed to achieve moderate GDP growth. The Chinese government’s immediate response to the turndown with a domestic stimulus package - equal to 13 percent of the country’s GDP - played a significant factor in reassuring the Chinese that they would not be headed for a protracted economic slowdown. According to Nielsen, advertising spend in China still grew by 17 percent in 2008, driven by ad increases in pharmaceutical/health, toiletries, beverages, business/industry/agriculture and food products. Sales of FMCG products remained robust and rose by 21 percent last year compared to 2007.

47

28

31

25

21

22

18

13

10

2

48

34

31

30

27

25

25

22

13

11

2

31

0 10 20 30 40 50 60

Putting into savings

Holidays / vacations

New clothes

Paying off debts / credit cards / loans

Out of home entertainment

New technology products

Home improvements / decorating

Investing in shares of stock / mutual funds

I have no spare cash

Retirement fund

Don' t know/undecided

%Source: Nielsen Global Online Consumer Survey March 2009: 26, 719 respondents in 53 markets globallyAnd Nielsen Global Online Consumer Survey June 2009: 14, 029 respondents in Europe, Asia Pacific, Middle East and North America

Mar-09 Jun-09

After covering essential living costs, consumers are putting their spare cash away for the future

Q: Once youhave covered essential living expenses, which of the following statements best desribes what you do with your spare cash.

8

The World Bank’s revised forecast for China’s economic growth rate to 7.2 percent this year from their previous 6.5 percent is a global indication for China’s recovery. After the World Bank revision, the Chinese stock hit a 10 month high in mid-June fuelled by increasing consumer confidence and optimism.

Urban unemployment remains below five percent and personal investment in the stock market has rebounded in early 2009, with an 18 percent increase compared to the same time last year, according to the latest Nielsen Personal Finance Monitor conducted from December 2008 to February 2009.

Nielsen’s China Travel Monitor (conducted in January, 2009) also reported that over 50 percent of Chinese respondents planned to travel in China domestically in the next 12 months, and 16 percent planned to travel overseas. Among domestic travellers, nearly four in 10 said the financial crisis had no impact whatsoever on their travel plans and only four percent said they would cancel their travel plans altogether.

Consumer confidence in Russia has also been spurred by recent stock market gains. Russia’s two main stock exchanges are up over 70 percent in the first half of 2009 – and the stabilization of the rouble and rally in oil prices significantly increased consumer confidence. Nielsen’s Consumer Confidence Index in Russia rose seven points between March and May this year – the first increase recorded since the second half of 2007 and the highest single increase since the survey started in 2005.

While Russians are still well aware of inflation and unemployment, they’re starting to see beyond the crisis and are hoping for a quick return to previous spending patterns with one in six Russians saying they won’t retain any of their recessionary habits once the economy improves – and they are looking to open their wallets again to spend on their favourite pastime – clothes shopping.

This is a significant turnaround in Russian consumer sentiment and as confidence in the economy is restored, consumers’ desire for branded products and luxury goods will be reignited, bolstering Russia’s reputation as a purchasing powerhouse for high end consumer products.

Like Russians, Chinese consumers say they’ll be willing to take the time to hunt around for the best price on a bank loan or insurance but they not prepared to cut back on their fashion spend or out-of-home entertainment in the post-recession era.

Growth slowed in China but positive signs have emerged

FMCG consumer sales and media ad spend in China stalled in the first Quarter, but towards the end of the second Quarter positive signs emerged, with many indices bouncing back sharply in May and June. Second tier cities and modern trade outlets in general were most affected with consumer confidence low and consumers reigning in the purse strings. Lower tier cities and rural areas felt little impact, with some experiencing double digit sales growth and high consumer confidence throughout the first half of the year – and since the global economic crisis hit in the fourth Quarter 2008. China experienced volume and value declines in the modern trade for many FMCG categories, especially food. Falling commodity prices, retailer stimulated price cuts and government food pricing controls, further pressured end-consumer prices. This converges on a tight squeeze on value growth for FMCG and some other key consumer segments.

During the second quarter sales growth has started to recover and as this continues and conditions gradually stabilize globally, MNCs are returning to their investments in China, despite it being a more challenging local environment today than it was a few months ago.

9

Global Trends

On a global scale, continuing to save on gas and electricity bills has become a lifestyle habit. Among those 69 percent who have already taken action to reduce these bills since the onset of the recession, over 50 percent of Australians, Kiwis, South Africans, Filipinos, UK, Irish and US consumers say they will continue to take further action to reduce household utility bills.

As economic recovery gathers pace, consumption and spending will increase – but the post recession consumer is likely to consume very differently. The post-recession consumer will think twice and sometimes thrice about making purchases, big or small. The recession affected all social classes and has fundamentally changed how consumers consume – and particularly in the West where it’s now fashionable to be frugal; and trendy to be thrifty.

50

54

46

43

34

38

37

28

34

23

24

22

18

13

12

40

22

20

24

21

21

14

11

17

10

15

7

8

8

9

16

55

0 10 20 30 40 50 60

Try to save on gas and electricity

Spend less on new clothes

Cut down on out-of-home entertainment

Cut down on take-away meals

Switch to cheaper grocery brands

Cut down on telephone expenses

Delay upgrading technology, eg. PC, Mobile, etc

Cut down on holidays / short breaks

Use my car less often

Delay the replacement of major household items

Look for better deals on home loans,insurance, credit cards, etc

Cut out annual vacation

Cut down on at-home entertainment

Cut down on or buy cheaper brands of alcohol

Cut down on smoking

I have taken other actions not listed above

%Source: Nielsen Global Online Consumer Survey March and June 2009Base : All Respondents those who said yes at Q10 (code 1) n=9947

Actions taken in June 09 Actions predicted in March 09

Consumers cost-cutting actions in June were more dramatic than they anticipated in March Global Average

10

Organic Living This new mind-set has been directly impacted by consumers’ growing concerns about the world we live in, and the world that will exist for future generations.

Consumers, especially in the West, are realizing that sustainability, recycling, organic food, bottled water, waste and the global environment as a whole are all related to the actions they choose to take today.

Organic food and bottled water may prove to be among the first victims of the recession as the new consumer mind-set gathers momentum. At the onset of the recession, consumers cut back on spending on organic products and bottled water for economic reasons. Having done without them for several months or over a year, consumers may question if they really need these products in their lives again, especially with an ongoing controversial debate on the real “goodness” of organic products and the recycling and waste issues created by plastic, bottled water.

In the US, Australia and many Western European nations, sales of bottled water have been in decline for the past two years. Under current circumstances in the West, it’s unlikely that bottled water will rebound to its previously high-growth levels of five years ago.

In the USA, sales growth of organic products nosedived as the economy worsened. For the 4-week period ending in mid-May 2009, dollar sales of UPC-coded products with an organic label claim grew by just two percent compared to 24 percent in the previous year. Between 2005 and 2006, many organic products posted growth rates of 30 percent according to Nielsen. Manufacturers and producers of organic products are being challenged to prove that their product is truly “better for you, and better for the planet”. Consumers need good economic – and now, scientifically or medically proven -- reasons to justify paying extra for organic products, especially as it’s becoming known that carbon emissions are often lower from the non-organic alternative.

For US consumers, the top recessionary habits households have made part of their lifestyle are saving on gas/electricity

+0%

+5%

+10%

+15%

+20%

+25%

+30%

+35%

4 W/E

02/25/0

6

4 W/E

05/20/0

6

4 W/E

08/12/0

6

4 W/E

11/0

4/06

4 W/E

01/27/0

7

4 W/E

04/21/0

7

4 W/E

07/14/0

7

4 W/E

10/0

6/07

4 W/E

12/2

9/07

4 W/E

03/22/0

8

4 W/E

06/14/0

8

4 W/E

09/06/0

8

4 W/E

11/2

9/08

4 W/E

02/21/0

9

4 W/E

05/16/0

9

UPC-Coded OrganicsSource: Scantrack & LabelTrends, services of The Nielsen Company; (FDM ex-Walmart) % Change in 4-Week Dollar Sales vs. YAGO

Monthly sales growth of organicsbelow 4% in last five periods

USA: The economy takes it toll on organics

11

(48%), cutting down on take-away meals (28%) and continuing to switch to cheaper grocery products (28%). But while they’ll cut back in these areas, other parts of their lifestyle will see some rebound. Over 40 percent of US consumers said they’ll be spending on travel and holidays, dining out and out-of-home entertainment according to recent survey of 10,000 Nielsen HomescanTM households in the USA, a clear indication that while consumers are preparing to loosen their purse-strings in coming months, restraint will be key.

In many ways, the recession served to accelerate and intensify many of the trends that were emerging before the economic downturn. There has been a decreasing trend for take-away meals, mainly due to growing health and wellness trends, but the cost of take-away meals in developed markets has accelerated this considerably. Among those saying “no” to take-away meals are Australians, New Zealanders, Japanese, Irish, South Africans, Brazilians and USA consumers.

The winners in the take-away meal sector have been those companies that have changed their offering to become family-friendly eateries with an accent on value and healthy food options. Designer-look and family-friendly McCafes from McDonalds in Europe have been extremely popular during the downturn as families have embraced a low-cost family eating option in a modern, family-friendly environment.

66 65

60 61

45

54

26

19 1916

19 20

0

10

20

30

40

50

60

70

80

90

100

NA MEAP EU LA AP Global Average

%

Actions taken in June 09 Actions predicted in March 09Source: Nielsen Global Online Consumer Survey March and June 2009Base : All Respondents those who said yes at Q10 (code 1) n=9947

Consumers cut down on out-of-home entertainment significantly more than they predicted

The only two Dow Jones companies to grow in 2008 were Walmart and McDonalds. And recently Starbucks announced plans to lower prices on basic offerings, but raise prices on others. Segmentation is the key to success in this environment.

12

Staying in will continue to be the new ‘going out’, especially for around one in five Turkish and US consumers. As consumers decreased their out-of-home entertainment budgets there has been a welcome return to traditional social values with an emphasis on family and friends.

Some FMCG manufacturers have been quick to capitalize on consumers’ need for reassurance and security in these days, with the return of retro-style ads evoking carefree, secure times of childhood. Even when economic conditions improve, more consumers globally say they will continue to cut back on out-of-home entertainment while only six percent will cut back on at-home entertainment.

Many Europeans, Americans and Pacific consumers said they will continue to switch to cheaper priced grocery products – another trend which accelerated during the recession in certain markets and grocery categories -- and looks set to continue in the post-recession world. Around one in three Kiwi and US consumers, along with over 20 percent of German, French, UK, Australians, Malaysians and Singaporeans say they will continue to switch to cheaper grocery brands even when economic conditions improve.

When it comes to grocery shopping, what people say and what they do isn’t necessarily the same thing. It is true to say that Retail Brands have benefited from the ‘credit crunch’ brought about by the recession. Countries such as the UK, Switzerland and Germany had highly developed Retail Brand propositions prior to the recession, where the growth of Retail Brands had more to do with the consolidation of retail ownership. This gave more Head Office buyers the critical mass required in their categories to make a Retail Brand financially viable.

The recession may well have stimulated a lot more trial – and then conversion – to Retail

Brands, as consumers experience the range and quality on offer. In these markets, and for these ‘newly trialled’ Retail Brand categories, consumers may not see reason to switch back again. In previous downturns, consumers switched to cheaper products faster and it took a while for them to switch back to branded products. In this environment, leading brand manufacturers need to focus on regaining customer loyalty and ensuring growth of their brand equity.

A key driver of Retail Brand growth is the amount of innovation and commitment that Retailers are putting behind them, and the range of products available. FMCG manufacturers have also responded to consumers’ changing needs for extra-value, introducing products focusing on convenience, functionality and innovation. For the average shopper, there’s never been such a range of choice in terms of products and price as there is now. Similarly, with shopping habits largely defined by the retail landscape, there has been greater acceptance and popularity for shoppers to frequent the predominantly Retail Brand supermarkets of Aldi and Lidl. In Europe 1500 Aldi and Lidl stores opened between 2006 and 2008 and their expansion continues.

31.3%32.1%

33.3%

34.7%35.6%

36.7%37.2%

37.9%

31.4%30.6%30.1%

29.3%28.7%

28.0%27.4%27.0%

2001 2002 2003 2004 2005 2006 2007 2008

Value Share Volume ShareSource: The Nielsen Company

Retail Brand share in Europe: 8 years, 7 countries and 1944 categories

13

Valu

e sh

are

of R

etai

l Bra

nds

Retailer Concentration

10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

Den Swe

NZFinNor

Aus

Rus

Pol

Tur

USA

Cze

Ita Hun

Gre

Por

SloNed Spa

Fra

Ger

Can

BelAut

CH

UK

Source: The Nielsen Company

Retail Brands and retailer concentration

14

Average

46%44%

26%26%27%28%29%

32%

14%14%

17% 17%17%18% 18%19%

21% 21%22%22%24%

12% 11%

8%

Switz

erla

nd UK

Ger

man

y

Spai

n

Belg

ium

Can

ada

Aus

tria

Fran

ce

Net

herla

nds

Port

ugal

Slov

akia

Swed

en

Den

mar

k

Finl

and

New

Zea

land

Cze

ch R

ep.

USA

Hun

gary

Nor

way

Ital

y

Aus

tral

ia

Pola

nd

Gre

ece

Turk

ey

Source: The Nielsen Company

Retail Brand value share in Europe

8%

7%

5%

6%32%

1% 1%1% 1%

2%2% 2%

3%

2%

5%

22%

5%

Arg

entin

a

Chi

le

Col

umbi

a

Mex

ico

Braz

il

Hon

g Ko

ng

Ven

ezue

la

Sing

apor

e

Mal

aysi

a

Sout

h Ko

rea

Taiw

an

Indo

nesi

a

Thai

land

Chi

na

Phill

ippi

nes

Source: The Nielsen Company

Retail Brand value share - a global snapshot

15

In the Nielsen Global Online survey, fifteen percent of global consumers said they will spend less on new clothes even when the economy recovers, compared to 37 percent who have cut back on clothes spending during the recession. While the Chinese, Russians, UAE and Indians will be among the first to update their wardrobes in the post-recession world, those pledging to spend considerably less on fashion are Singaporeans, Malaysians, Italians, Turkish, Brazilians and Australians.

The Challenge for Marketers in the

Post-Recession WorldMajor international FMCG and fashion manufacturers face the same dilemma in the post-recession world – how to convince consumers to switch back to their ‘old’ brands or try new brands when they have experienced and been satisfied with the quality of a lower-priced option they’ve switched to during the recession. This question has played on manufacturers’ minds throughout the recession resulting in an increased focus on product innovation. Nielsen BASES information indicates that over 50 percent of tested products have succeeded with consumers and among forty new products that Nielsen tracked in the USA last year; none were adversely affected by the recession. The economic downturn sowed some ripe seeds for product innovation – marketers know they’re going to need a particularly innovative product that hits all the right spots with consumers to pry them away from their usual brand. Success in the post-recession era is based on achieving the right combination of value, product innovation and competitive differentiation.

In addition to product innovation, manufacturers now have to consider the impact of brand values and corporate responsibility on sales. Brand values used to be the domain of the marketer but these days, it has become a purchasing factor. The post-recession consumer has reassessed their lifestyle and has become a more socially aware and ethically-minded buyer. They expect the same values to resonate in the brands they buy and companies they buy from. The successful, post-recession FMCG company will have to be ethically and socially accountable in the way their products are sourced and manufactured, environmentally aware and good corporate citizens in every way.

16

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PH CN BR ID RU IN TR IT UA DE

Base : Source: Nielsen Global Online Consumer Survey June 2009All respondents n = 14029

4543

40

34 34 32

28 27 27 26

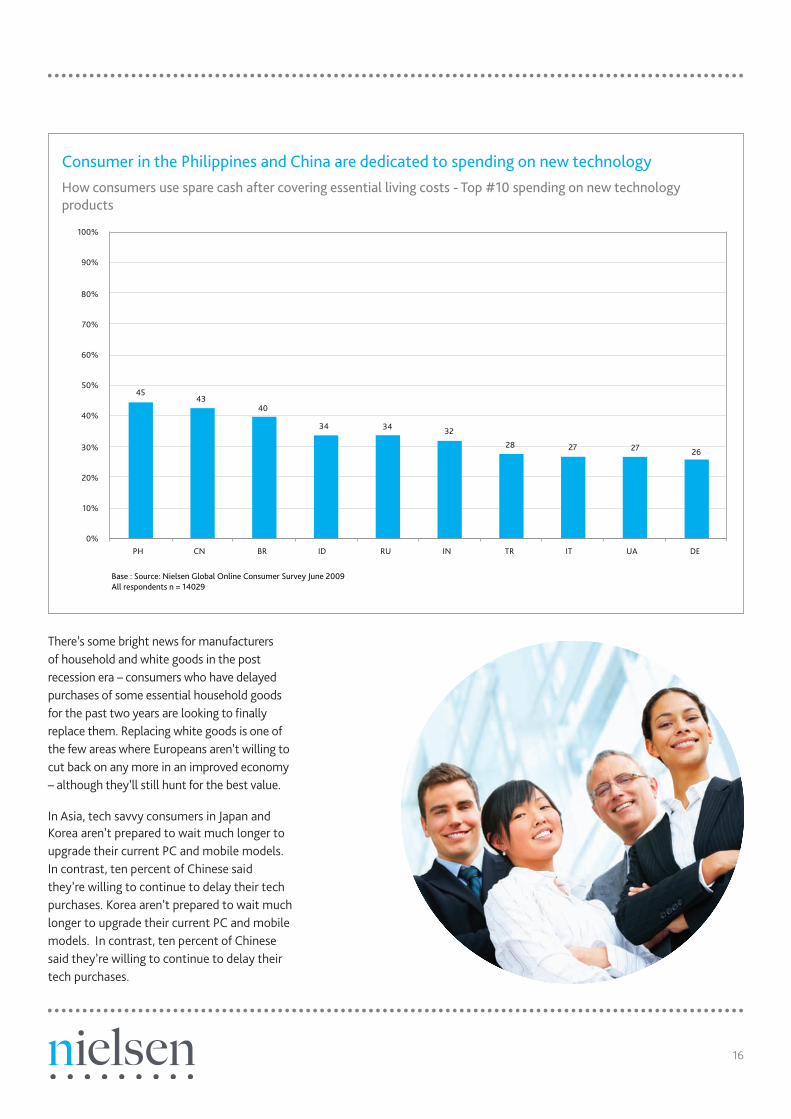

Consumer in the Philippines and China are dedicated to spending on new technology How consumers use spare cash after covering essential living costs - Top #10 spending on new technology products

There’s some bright news for manufacturers of household and white goods in the post recession era – consumers who have delayed purchases of some essential household goods for the past two years are looking to finally replace them. Replacing white goods is one of the few areas where Europeans aren’t willing to cut back on any more in an improved economy – although they’ll still hunt for the best value.

In Asia, tech savvy consumers in Japan and Korea aren’t prepared to wait much longer to upgrade their current PC and mobile models. In contrast, ten percent of Chinese said they’re willing to continue to delay their tech purchases. Korea aren’t prepared to wait much longer to upgrade their current PC and mobile models. In contrast, ten percent of Chinese said they’re willing to continue to delay their tech purchases.

17

11

The Nielsen Global Online Consumer Survey

A twice-yearly online study, the Nielsen Online Global Consumer Confidence survey polled 26, 719 consumers in 53 markets in

Europe, Asia Pacific, North America and the Middle East from March 19 to April 2, 2009 about their confidence levels and economic

outlook. The Nielsen Consumer Confidence Index is developed based on consumers’ confidence in the job market, status of their

personal finances and readiness to spend.

The Nielsen Company

The Nielsen Company is a global information and media company with leading market positions in marketing and consumer

information, television and other media measurement, online intelligence, mobile measurement, trade shows and business

publications (Billboard, The Hollywood Reporter, Adweek). The privately held company is active in more than 100 countries, with

headquarters in New York, USA. For more information, please visit, www.nielsen.com

AE United Arab EmiratesAR ArgentinaAT AustriaAU AustraliaBE BelgiumBR BrazilCA CanadaCH SwitzerlandCL ChileCN ChinaCO ColombiaCZ Czech RepublicDE GermanyDK DenmarkEE EstoniaEG EgyptES SpainFI FinlandFR FranceGB United KingdomGR GreeceHK Hong KongHU HungaryID IndonesiaIE IrelandIL IsraelIN India

IT ItalyJP JapanKO South KoreaLT LithuaniaLV LatviaMX MexicoMY MalaysiaNL NetherlandsNO NorwayNZ New ZealandPH PhilippinesPK PakistanPL PolandPT PortugalRO RomaniaRU RussiaSA Saudi ArabiaSE SwedenSG SingaporeTH ThailandTR TurkeyTW TaiwanUS United StatesVE VenezuelaVN VietnamZA South Africa

Country Abbreviations

Nielsen’s Quarterly Global Online Consumer Survey polled 26, 719 consumers in 53 markets in Europe, Asia Pacific, North America and the Middle East from March 19 to April 2, 2009 and polled 14, 029 respondents in 28 markets in Europe, Asia Pacific, Middle East and North America from June 15 to June 29, 2009 about their confidence levels and economic outlook. The Nielsen Consumer Confidence Index is developed based on consumers’ confidence in the job market, status of their personal finances and readiness to spend.

The Nielsen Company is a global information and media company with leading market positions in marketing and consumer information, television and other media measurement, online intelligence, mobile measurement, trade shows and business publications (Billboard, The Hollywood Reporter, Adweek). The privately held company is active in more than 100 counties,

Nielsen Global Online Consumer Survey

with headquarters in New York, USA. For more information, please visit, www.nielsen.com

The Nielsen Company