Newsflash: Share Buy-Back Rules Notified

4

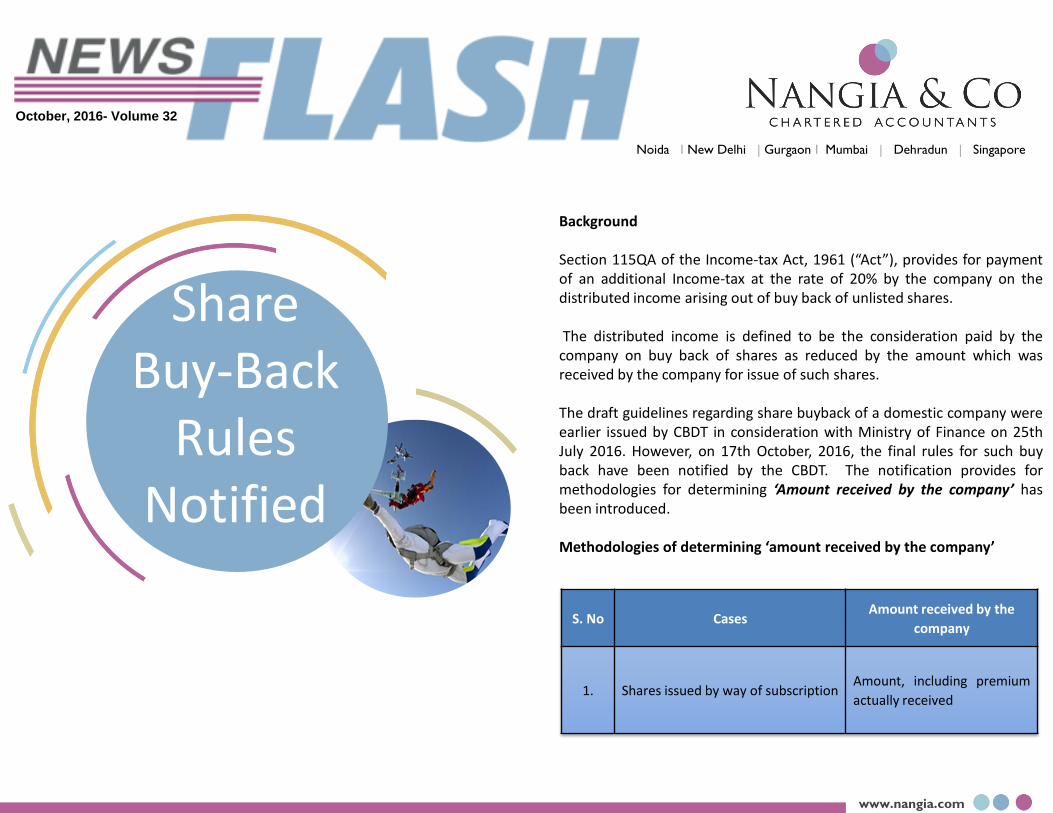

www.nangia.com Share Buy-Back Rules Notified Background Section 115QA of the Income-tax Act, 1961 (“Act”), provides for payment of an additional Income-tax at the rate of 20% by the company on the distributed income arising out of buy back of unlisted shares. The distributed income is defined to be the consideration paid by the company on buy back of shares as reduced by the amount which was received by the company for issue of such shares. The draft guidelines regarding share buyback of a domestic company were earlier issued by CBDT in consideration with Ministry of Finance on 25th July 2016. However, on 17th October, 2016, the final rules for such buy back have been notified by the CBDT. The notification provides for methodologies for determining ‘Amount received by the company’ has been introduced. Methodologies of determining ‘amount received by the company’ Noida I New Delhi | Gurgaon I Mumbai | Dehradun | Singapore October, 2016- Volume 32 S. No Cases Amount received by the company 1. Shares issued by way of subscription Amount, including premium actually received

-

Upload

nangia-co -

Category

Economy & Finance

-

view

181 -

download

0

Transcript of Newsflash: Share Buy-Back Rules Notified

www.nangia.com

Share Buy-Back

Rules Notified

Background Section 115QA of the Income-tax Act, 1961 (“Act”), provides for payment of an additional Income-tax at the rate of 20% by the company on the distributed income arising out of buy back of unlisted shares. The distributed income is defined to be the consideration paid by the company on buy back of shares as reduced by the amount which was received by the company for issue of such shares. The draft guidelines regarding share buyback of a domestic company were earlier issued by CBDT in consideration with Ministry of Finance on 25th July 2016. However, on 17th October, 2016, the final rules for such buy back have been notified by the CBDT. The notification provides for methodologies for determining ‘Amount received by the company’ has been introduced. Methodologies of determining ‘amount received by the company’

Noida I New Delhi | Gurgaon I Mumbai | Dehradun | Singapore

October, 2016- Volume 32

S. No Cases Amount received by the

company

1. Shares issued by way of subscription Amount, including premium

actually received

www.nangia.com

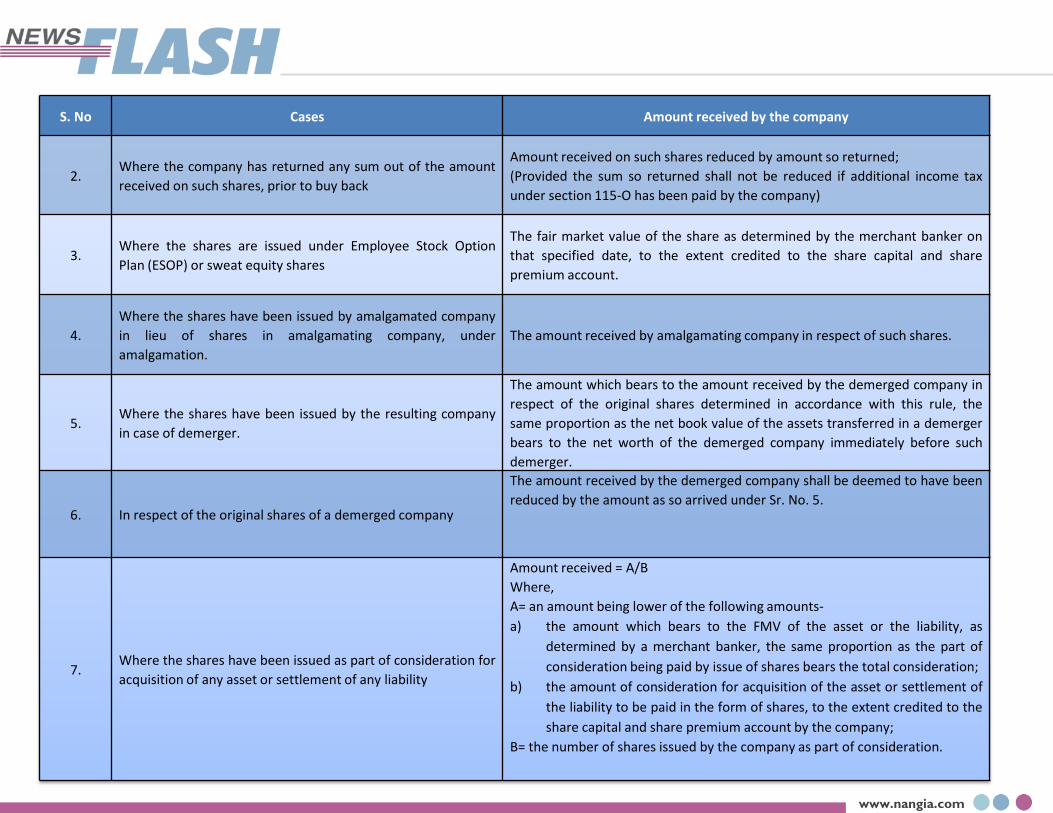

S. No Cases Amount received by the company

2. Where the company has returned any sum out of the amount

received on such shares, prior to buy back

Amount received on such shares reduced by amount so returned;

(Provided the sum so returned shall not be reduced if additional income tax

under section 115-O has been paid by the company)

3. Where the shares are issued under Employee Stock Option

Plan (ESOP) or sweat equity shares

The fair market value of the share as determined by the merchant banker on

that specified date, to the extent credited to the share capital and share

premium account.

4.

Where the shares have been issued by amalgamated company

in lieu of shares in amalgamating company, under

amalgamation.

The amount received by amalgamating company in respect of such shares.

5. Where the shares have been issued by the resulting company

in case of demerger.

The amount which bears to the amount received by the demerged company in

respect of the original shares determined in accordance with this rule, the

same proportion as the net book value of the assets transferred in a demerger

bears to the net worth of the demerged company immediately before such

demerger.

6. In respect of the original shares of a demerged company

The amount received by the demerged company shall be deemed to have been

reduced by the amount as so arrived under Sr. No. 5.

7. Where the shares have been issued as part of consideration for

acquisition of any asset or settlement of any liability

Amount received = A/B

Where,

A= an amount being lower of the following amounts-

a) the amount which bears to the FMV of the asset or the liability, as

determined by a merchant banker, the same proportion as the part of

consideration being paid by issue of shares bears the total consideration;

b) the amount of consideration for acquisition of the asset or settlement of

the liability to be paid in the form of shares, to the extent credited to the

share capital and share premium account by the company;

B= the number of shares issued by the company as part of consideration.

www.nangia.com

S. No Cases Amount received by the company

8.

Where the shares have been issued or allotted by a

company on succession or conversion of a firm into the

company or succession of sole proprietary concern by

the company

Amount received = A-B

C

A= book value of the assets in the balance sheet as reduced by any amount of

TDS/TCS/Advance tax as reduced by the amount of tax claimed as refund under the

Income-tax Act and any amount shown in the balance-sheet as asset including the

unamortized amount of deferred expenditure which does not represent the value of any

asset

B= book value of liabilities shown in the balance-sheet, but does not include the following

amounts, namely:-

a) capital, by whatever name called, of the proprietor or partners of the firm;

b) reserves and surpluses, by whatever name called, including balance in profit and loss

account;

c) any amount representing provision for taxation (Except TDS/TCS/advance tax

payment as reduced by the amount of tax claimed as refund under the Income-tax

Act, if any, to the extent of the excess over the tax payable with reference to the

book profits in accordance with the law applicable thereto);

d) any amount representing provisions made for meeting liabilities (except ascertained

liabilities) and;

e) any amount representing contingent liabilities,

C= number of shares issued on conversion or succession.

9. Where the shares have been issued without

consideration to existing shareholders Nil

10. Where the shares have been issued on conversion of

preference shares or bond or debenture, debenture-

stock or deposit certificate in any form or warrants or

any other security issued by the company

The amount received by the company in respect of such instrument so converted.

11. Where the shares are held in Dematerialized form and

the same cannot be distinctly identified The amount received by the company in respect of such share determined in accordance

with this rule on the basis of the first-in-first-out method (FIFO).

12. In any other case Face Value of shares

www.nangia.com

Our Comments The earlier provisions of the Act provided no

detailed methodology for determination of amount received by the company under buy back. The final rules in relation to determination of amount received by the company on issue of shares, being subject matter of tax on buy-back have now been notified by the CBDT. Determining the amount received by a company was a grey area and the final rules provide much needed clarity.

However, success of practical application of these rules can be assessed in due course of time from their applicability i.e. 1 June, 2016.

Another challenge that can be foreseen will be the taxability of buyback of shares executed between 1 June, 2016 upto the date of notification, and the same may be subject to litigations.

www.nangia.com [email protected]

DELHI

Suite - 4A, Plaza M-6, Jasola, New Delhi–110 025 Ph: +91-11-4737 1000, Fax: +91-11-4737 1010

GURGAON

Office No. 9, 14th Floor, Building No. 9B, DLF Cyber City, Phase III, Gurgaon - 122 002

MUMBAI

11th Floor, B Wing, Peninsula Business Park, Ganpatrao Kadam Marg,

Lower Parel, Mumbai–400 013, India

DEHRADUN

3rd Floor, NCR Plaza, New Cantt. Road, Dehradun–248 001

SINGAPORE 24 Raffles Place, #25-04A

Clifford Centre Singapore- 048621

NOIDA Nangia Tower, A - 109, Sector 136, Noida

Ph: +91-120-2598000, Fax: +91-120-2598010

OUR OFFICES