Newcrest Research Report

6

Junaid EQUITY RESEARCH Newcrest Mining limited (ASX NCM) - Australia Current Price $10.85 Junaid Farooq– Research + (61) 405 154 351 [email protected]

-

Upload

junaid-farooq -

Category

Documents

-

view

31 -

download

4

Transcript of Newcrest Research Report

Junaid EQUITY RESEARCHNewcrest Mining limited (ASX NCM) - AustraliaCurrent Price $10.85

Junaid Farooq– Research+ (61) 405 154 [email protected]

Simon RESEARCH 2/06

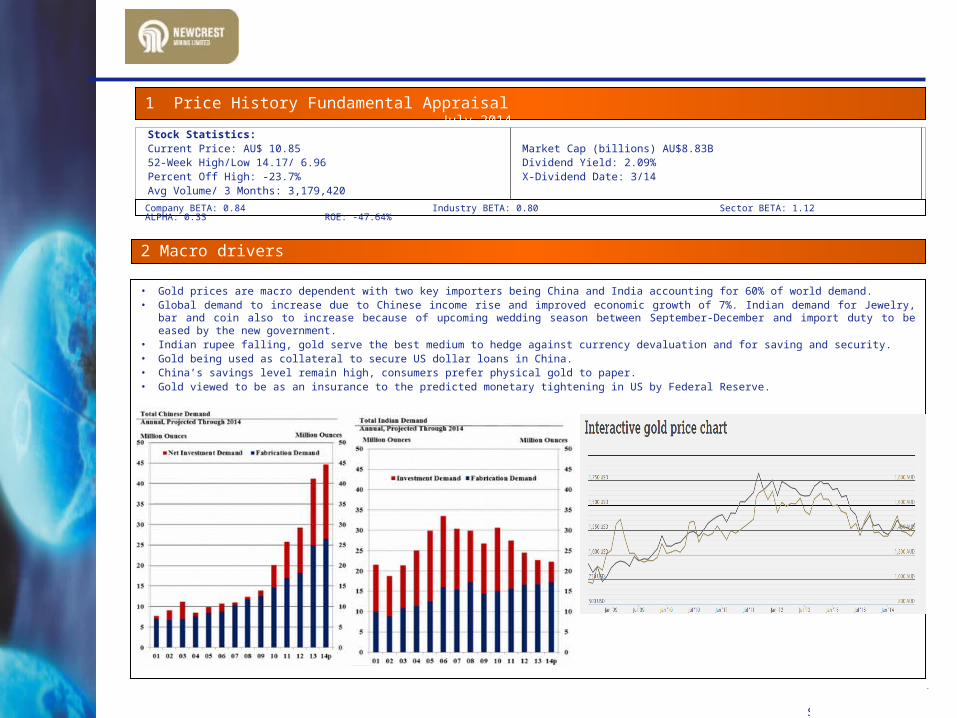

1 Price History Fundamental Appraisal July 2014Stock Statistics:Current Price: AU$ 10.8552-Week High/Low 14.17/ 6.96 Percent Off High: -23.7% Avg Volume/ 3 Months: 3,179,420

Market Cap (billions) AU$8.83BDividend Yield: 2.09%X-Dividend Date: 3/14

Company BETA: 0.84 Industry BETA: 0.80 Sector BETA: 1.12 ALPHA: 0.33 ROE: -47.64%

• Gold prices are macro dependent with two key importers being China and India accounting for 60% of world demand. • Global demand to increase due to Chinese income rise and improved economic growth of 7%. Indian demand for Jewelry, bar and coin also

to increase because of upcoming wedding season between September-December and import duty to be eased by the new government.• Indian rupee falling, gold serve the best medium to hedge against currency devaluation and for saving and security.• Gold being used as collateral to secure US dollar loans in China.• China’s savings level remain high, consumers prefer physical gold to paper.• Gold viewed to be as an insurance to the predicted monetary tightening in US by Federal Reserve.

1

2 Macro drivers

Simon RESEARCH 2/06

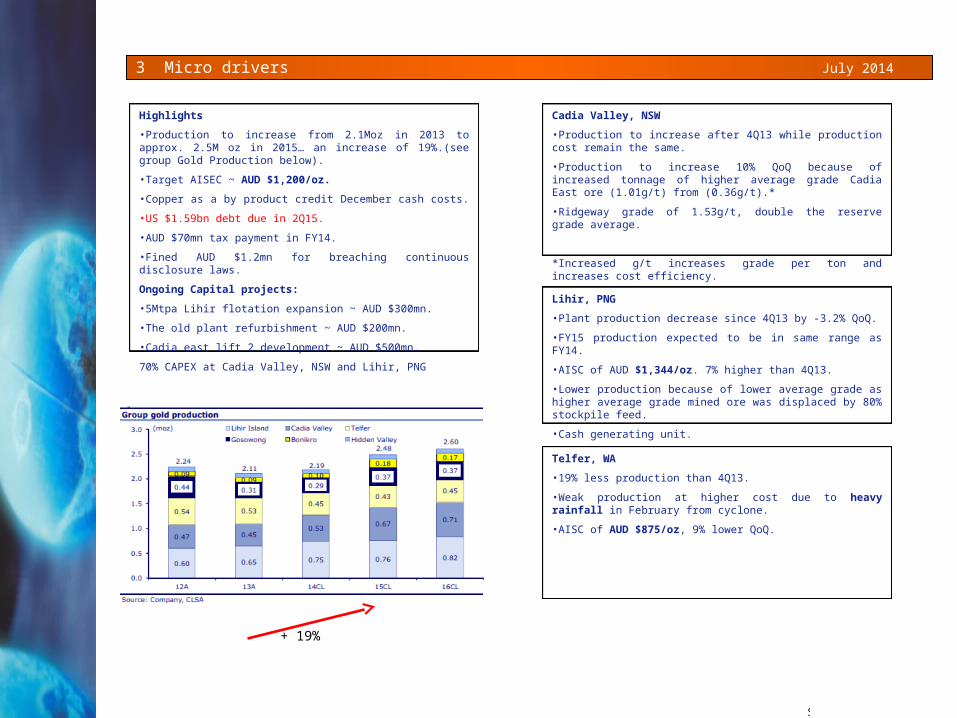

3 Micro drivers July 2014

Highlights

•Production to increase from 2.1Moz in 2013 to approx. 2.5M oz in 2015… an increase of 19%.(see group Gold Production below).

•Target AISEC ~ AUD $1,200/oz.

•Copper as a by product credit December cash costs.

•US $1.59bn debt due in 2Q15.

•AUD $70mn tax payment in FY14.

•Fined AUD $1.2mn for breaching continuous disclosure laws.

Ongoing Capital projects:

•5Mtpa Lihir flotation expansion ~ AUD $300mn.

•The old plant refurbishment ~ AUD $200mn.

•Cadia east lift 2 development ~ AUD $500mn.

70% CAPEX at Cadia Valley, NSW and Lihir, PNG

Cadia Valley, NSW

•Production to increase after 4Q13 while production cost remain the same.

•Production to increase 10% QoQ because of increased tonnage of higher average grade Cadia East ore (1.01g/t) from (0.36g/t).*

•Ridgeway grade of 1.53g/t, double the reserve grade average.

*Increased g/t increases grade per ton and increases cost efficiency.

Lihir, PNG

•Plant production decrease since 4Q13 by -3.2% QoQ.

•FY15 production expected to be in same range as FY14.

•AISC of AUD $1,344/oz. 7% higher than 4Q13.

•Lower production because of lower average grade as higher average grade mined ore was displaced by 80% stockpile feed.

•Cash generating unit.

Telfer, WA

•19% less production than 4Q13.

•Weak production at higher cost due to heavy rainfall in February from cyclone.

•AISC of AUD $875/oz, 9% lower QoQ.

+ 19%

Simon RESEARCH 2/06

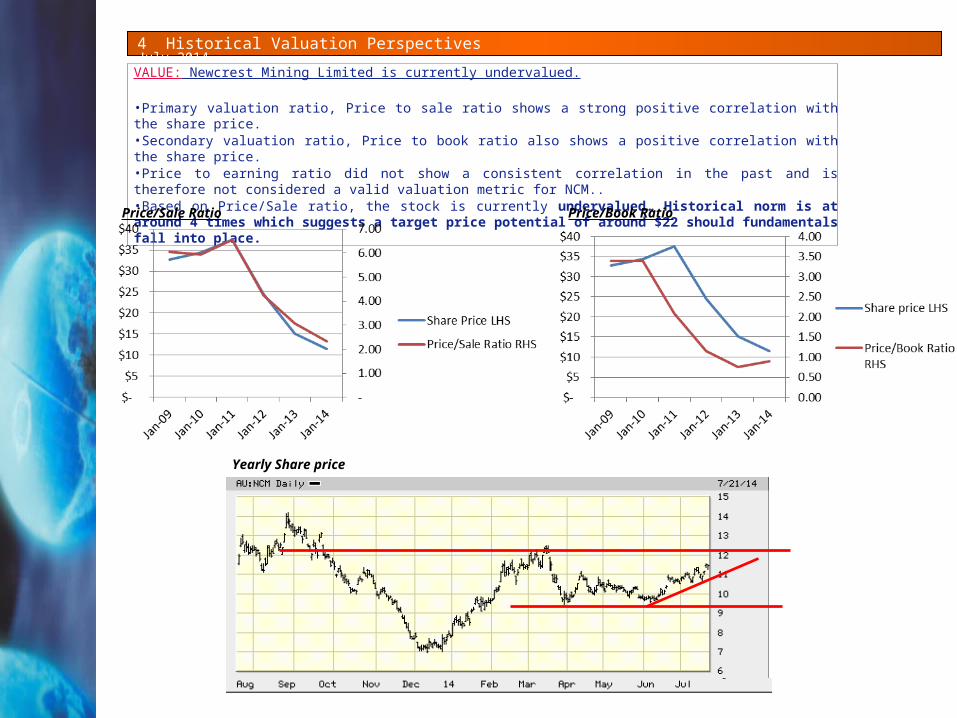

4 Historical Valuation Perspectives July 2014

VALUE: Newcrest Mining Limited is currently undervalued.

•Primary valuation ratio, Price to sale ratio shows a strong positive correlation with the share price.•Secondary valuation ratio, Price to book ratio also shows a positive correlation with the share price.•Price to earning ratio did not show a consistent correlation in the past and is therefore not considered a valid valuation metric for NCM..•Based on Price/Sale ratio, the stock is currently undervalued… Historical norm is at around 4 times which suggests a target price potential of around $22 should fundamentals fall into place.

Price/Book Ratio

Price/Sale Ratio

Yearly Share price

Simon RESEARCH 2/06

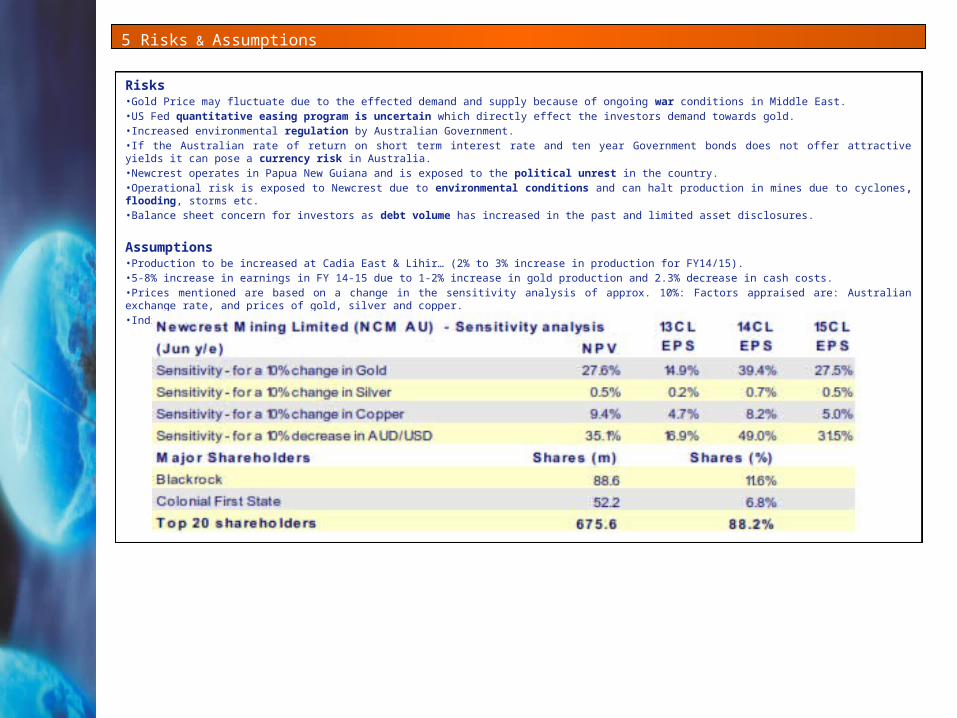

5 Risks & Assumptions July 2014

Risks•Gold Price may fluctuate due to the effected demand and supply because of ongoing war conditions in Middle East.•US Fed quantitative easing program is uncertain which directly effect the investors demand towards gold.•Increased environmental regulation by Australian Government.•If the Australian rate of return on short term interest rate and ten year Government bonds does not offer attractive yields it can pose a currency risk in Australia.•Newcrest operates in Papua New Guiana and is exposed to the political unrest in the country.•Operational risk is exposed to Newcrest due to environmental conditions and can halt production in mines due to cyclones, flooding, storms etc.•Balance sheet concern for investors as debt volume has increased in the past and limited asset disclosures.

Assumptions•Production to be increased at Cadia East & Lihir… (2% to 3% increase in production for FY14/15).•5-8% increase in earnings in FY 14-15 due to 1-2% increase in gold production and 2.3% decrease in cash costs.•Prices mentioned are based on a change in the sensitivity analysis of approx. 10%: Factors appraised are: Australian exchange rate, and prices of gold, silver and copper.•Indian demand for gold is dependent on duty and import tax cuts by Federal Government.

Simon RESEARCH 2/06

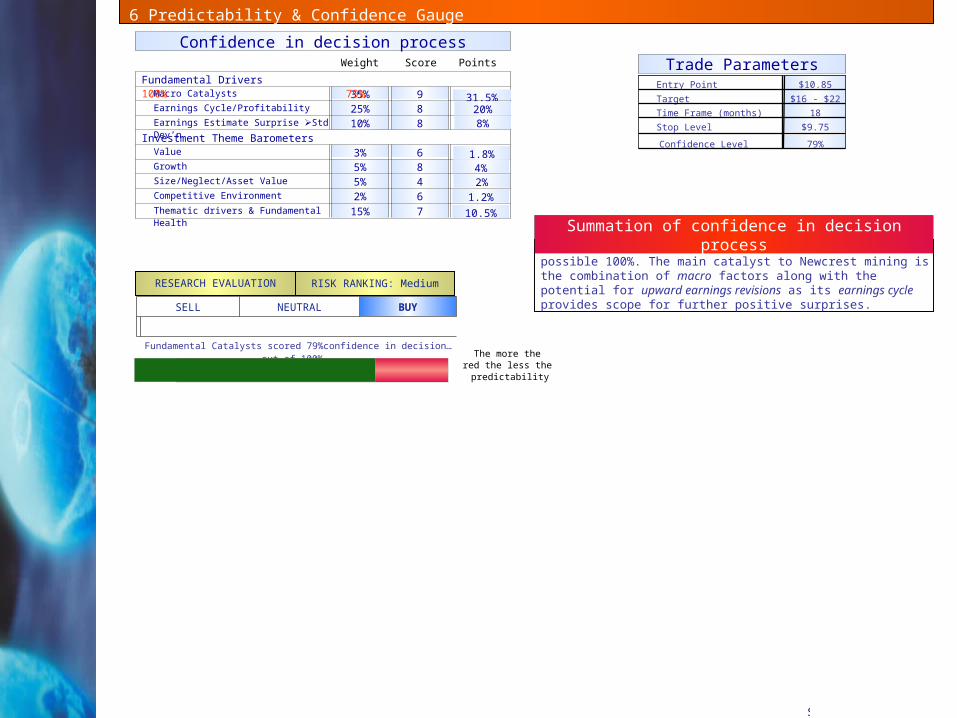

715%Thematic drivers & Fundamental Health

62%Competitive Environment45%Size/Neglect/Asset Value85%Growth63%Value

Investment Theme Barometers810%Earnings Estimate Surprise Std

Dev’n

825%Earnings Cycle/Profitability935%Macro Catalysts

Fundamental Drivers 100% 79%

Confidence in decision processWeight Score Points

79%Confidence Level

$9.75Stop Level

18Time Frame (months)

$16 - $22Target

$10.85Entry Point

Trade Parameters

The fundamental drivers scored well at 79% out of a possible 100%. The main catalyst to Newcrest mining is the combination of macro factors along with the potential for upward earnings revisions as its earnings cycle provides scope for further positive surprises.

Summation of confidence in decision process

6 Predictability & Confidence Gauge July 2014

SELL NEUTRAL BUY

Fundamental Catalysts scored 79%confidence in decision…out of 100%.

RESEARCH EVALUATION RISK RANKING: Medium

The more the red the less the

predictability

31.5%20%8%

1.8%4%2%

1.2%

10.5%