New Vendor Sales Tax Basics Diane M. Werner, C.P.M. Ohio Department of Taxation Akron Service...

29

New Vendor Sales Tax Basics Diane M. Werner, C.P.M. Ohio Department of Taxation Akron Service Center

-

Upload

domenic-cannon -

Category

Documents

-

view

214 -

download

0

Transcript of New Vendor Sales Tax Basics Diane M. Werner, C.P.M. Ohio Department of Taxation Akron Service...

New Vendor Sales Tax Basics

Diane M. Werner, C.P.M.

Ohio Department of Taxation

Akron Service Center

The Basic Responsibilities of an Ohio Retailer (Vendor):

Obtain a vendor's license - ORC 5739.17 (A)

Collect sales tax - ORC 5739.29

Maintain complete records - ORC 5739.11 File tax returns with payment - ORC 5739.12

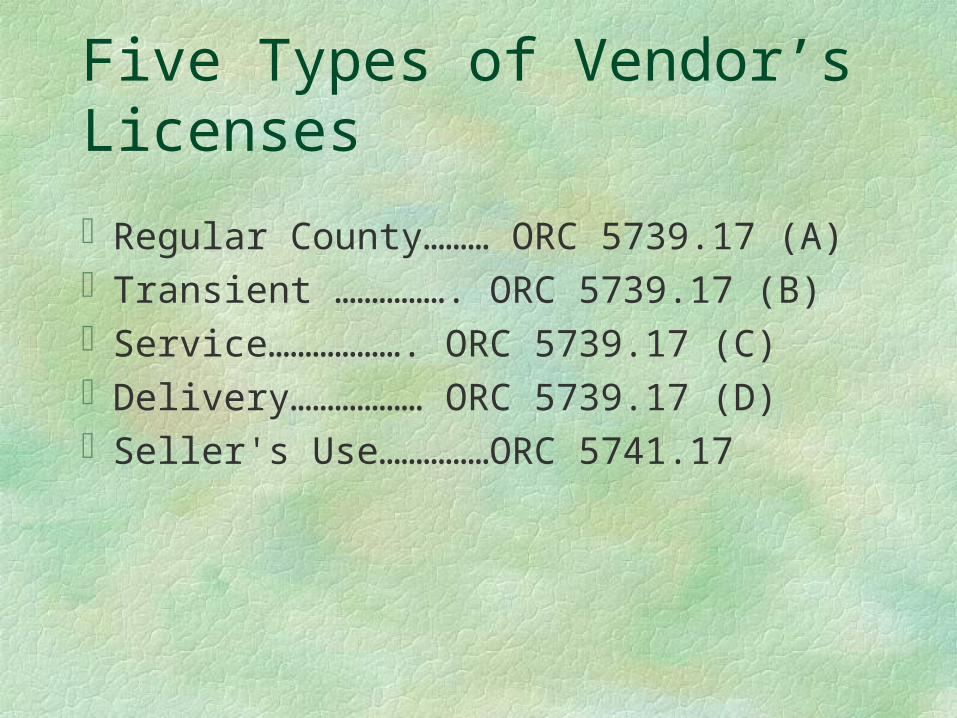

Five Types of Vendor’s Licenses

Regular County……… ORC 5739.17 (A) Transient ……………. ORC 5739.17 (B) Service………………. ORC 5739.17 (C) Delivery……………… ORC 5739.17 (D) Seller's Use……………ORC 5741.17

Obtain a Vendor’s License

Online at Ohio Business Gateway www.obg.ohio.gov

• All types including *Seller’s Use Permit/ Consumer’s Use*(license only, no returns)

ODT Service Center Akron Service Center 161 S. High St, Rm. 501

• All types including *Seller’s Use Permit/Consumer’s Use

*(license only, no returns)

County Auditor’s Office County where business is located

• Only their own county license

Is it Taxable?

Sales tax is applied to the retail sale, lease, and rental of tangible personal property (TTP) unless specifically exempted (ORC 5739.02).

Services listed in ORC chapter 5739.01 B(3).

www.tax.ohio.gov Contact Us:

Taxpayer Bares the Burden of Proof

The statute of limitations for tax reported for a registered taxpayer is 4 years.

No statute of limitation on tax collected and not remitted.

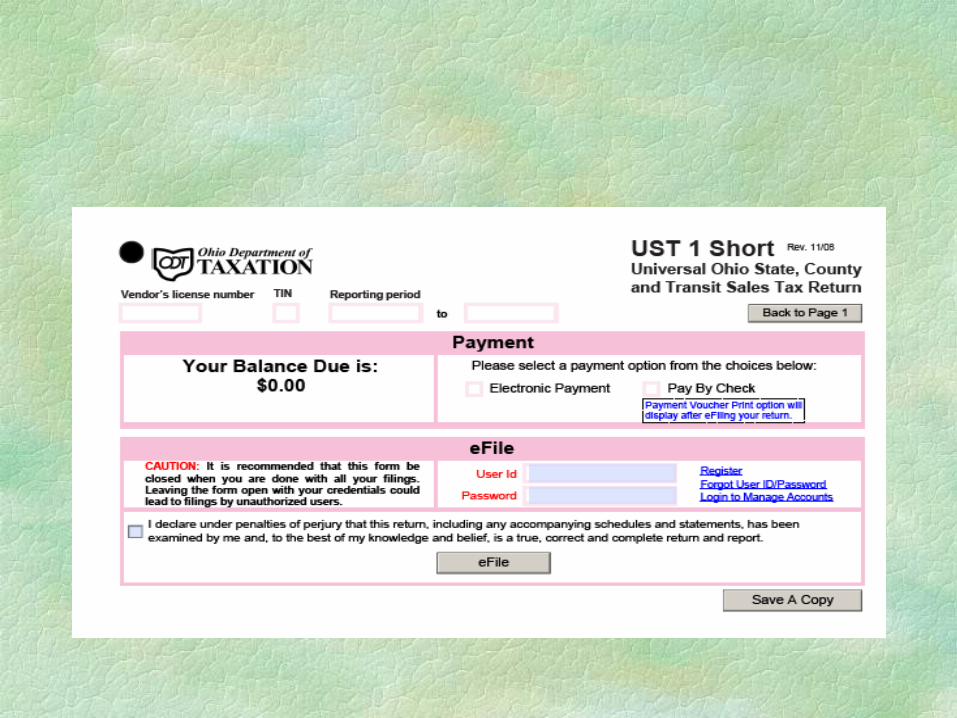

The way businesses file sales tax returns changed beginning with the first filing period in 2009. All vendors – regardless of sales volume – are required to file electronically rather than on paper.

Sales Tax Electronic Filing

Sales Tax Electronic Filing Options

www.tax.ohio.gov

Continued from prior page:

Complete form and click “next”

Review the information and click “register”

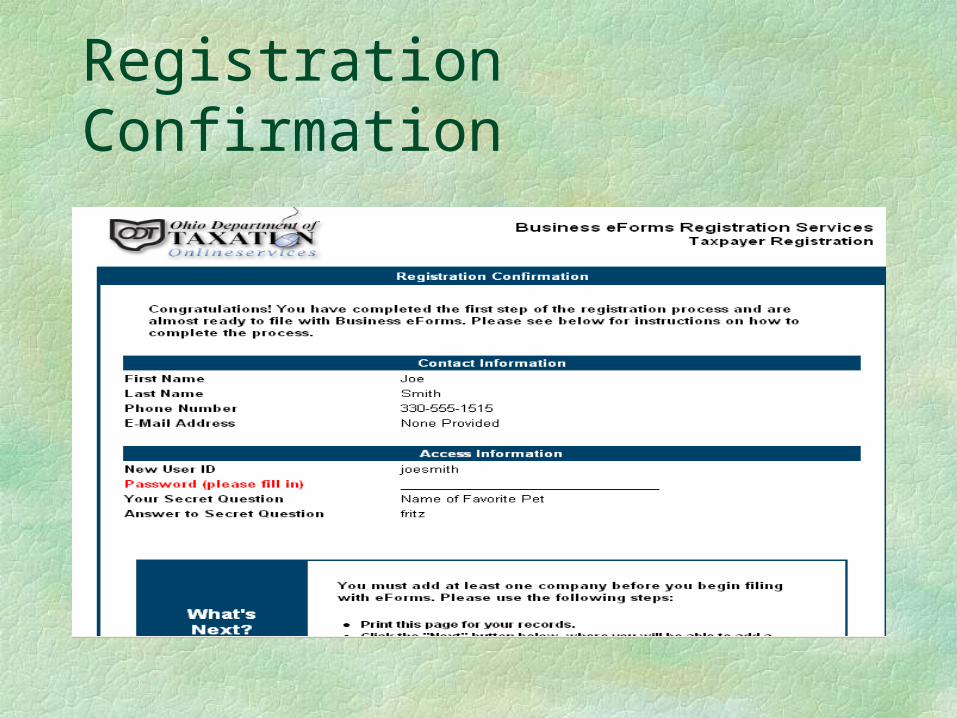

Registration Confirmation

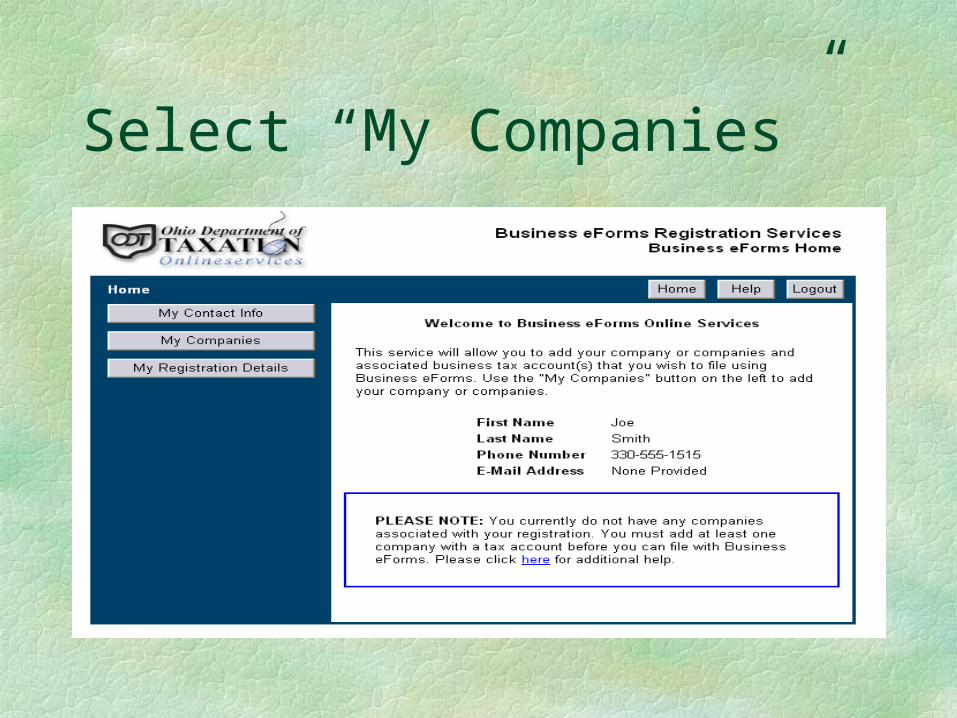

Select “My Companies”

Select “Add Companies”

Add company information, click “add”

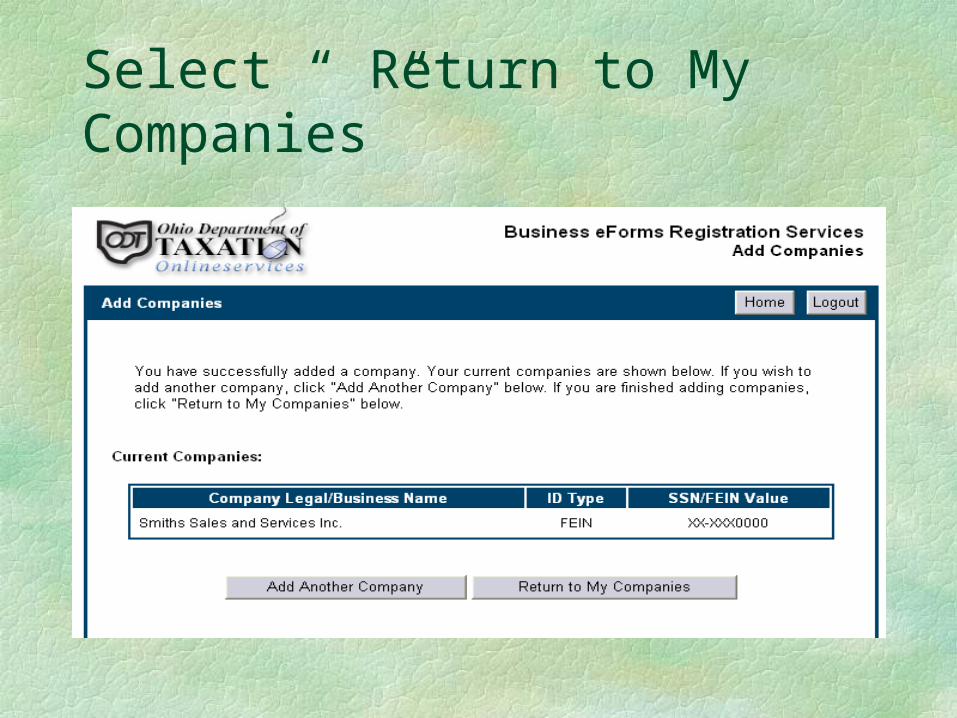

Select “ Return to My Companies”

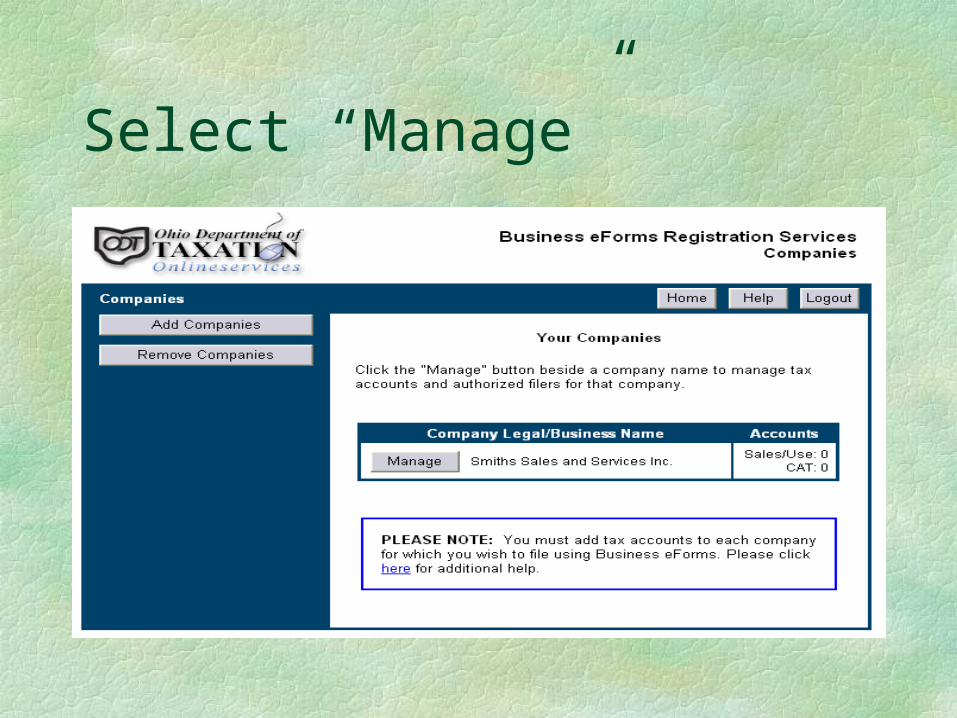

Select “Manage”

Choose “Add” sales tax account

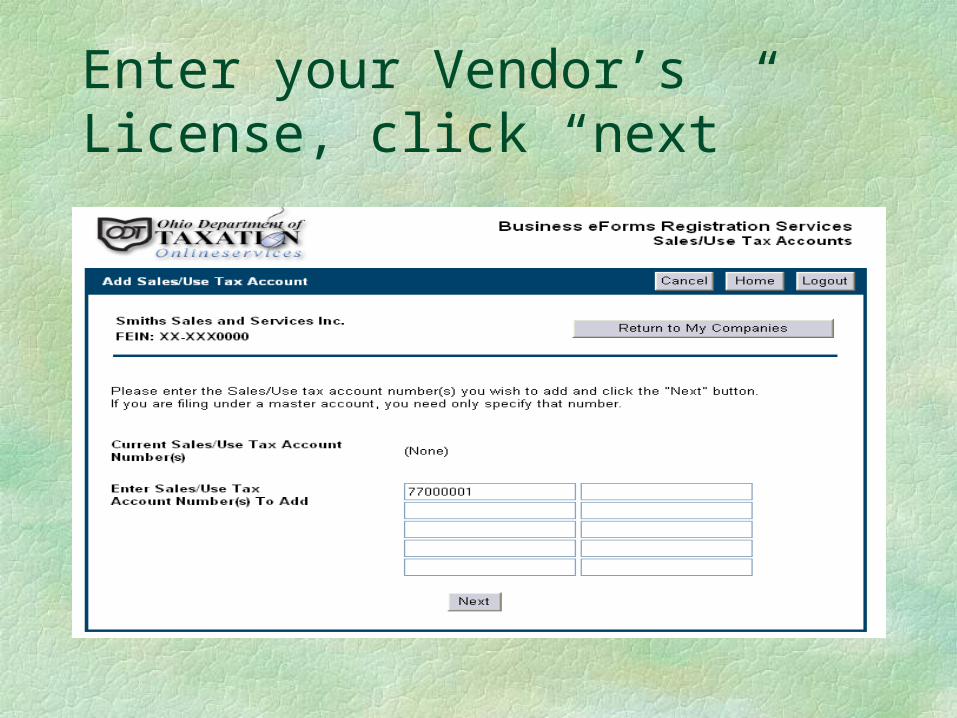

Enter your Vendor’s License, click “next”

Select “Add”

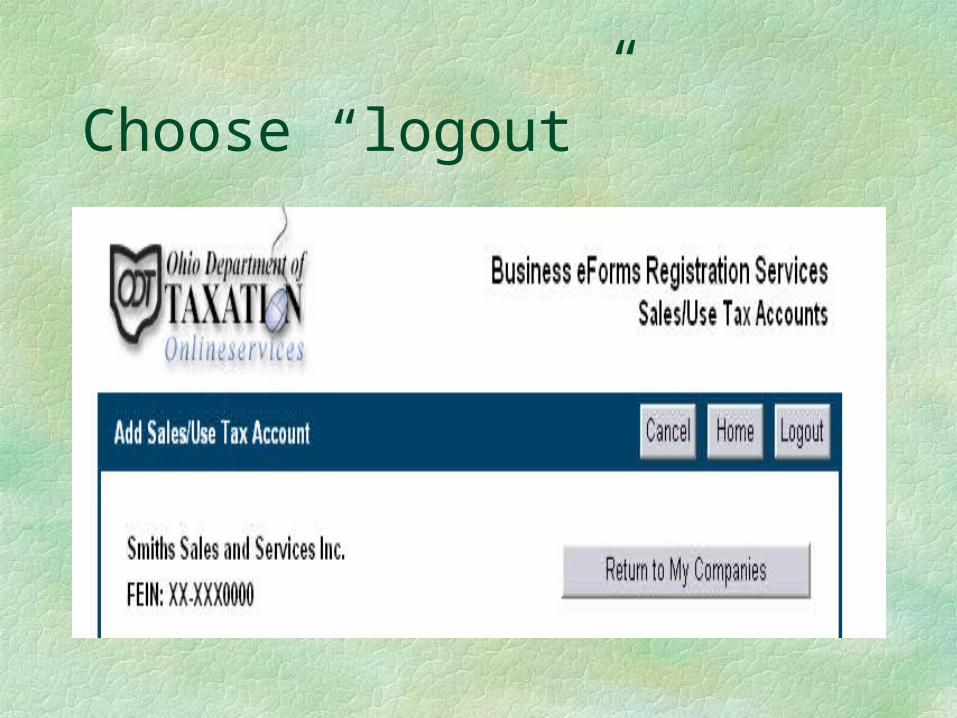

Choose “logout”

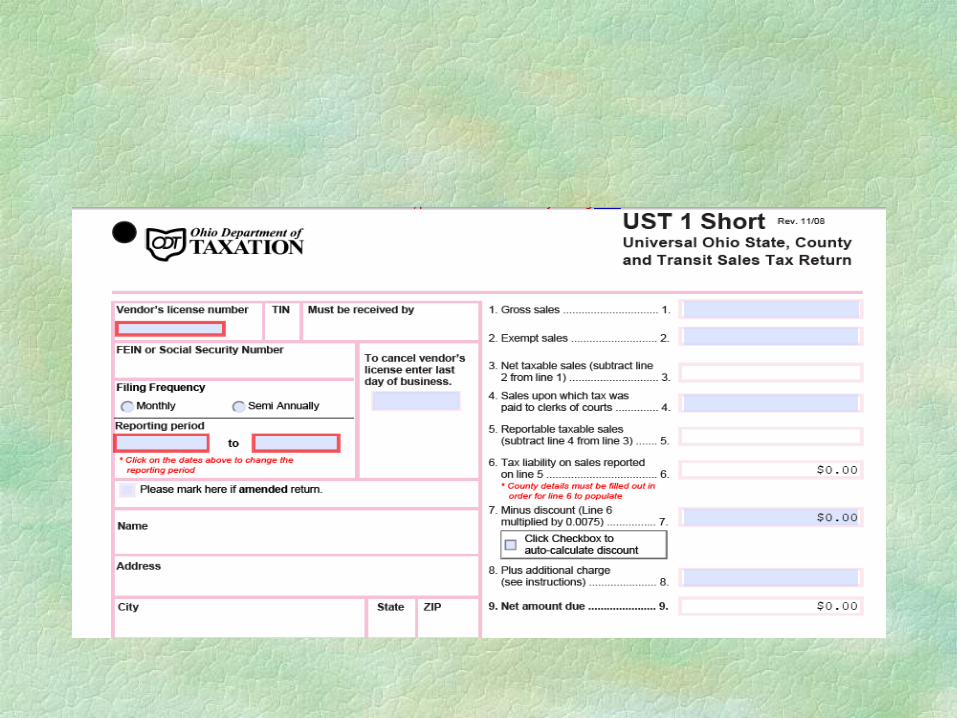

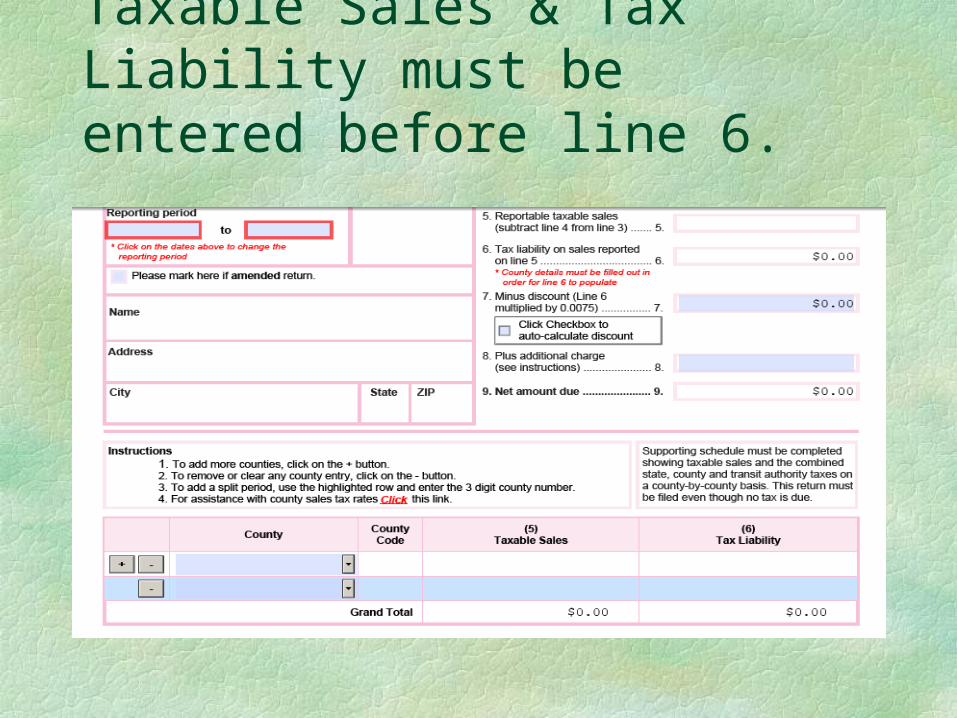

Taxable Sales & Tax Liability must be entered before line 6.

Sales Tax is a Trust Tax

.

Failure to remit tax collected is a fourth degree felony.

Be sure to cancel your license when you go out of business.