New opportunities for your retirement strategy€¦ · the plan, consider opening a TIAA Brokerage...

20

New opportunities for your retirement strategy Announcing updates to the Bowling Green State University Alternative Retirement Plan (ARP) and 403(b) Plan

Transcript of New opportunities for your retirement strategy€¦ · the plan, consider opening a TIAA Brokerage...

New opportunities for your retirement strategy Announcing updates to the Bowling Green State University Alternative Retirement Plan (ARP) and 403(b) Plan

Table of contentsA new chapter is about to start ���������������������������������������������������������������������������������������������������������������������������������������������������������������1

Action plan for the updates ���������������������������������������������������������������������������������������������������������������������������������������������������������������������2

Understanding retirement plan fees ������������������������������������������������������������������������������������������������������������������������������������������������� 2-3

Your new options ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������ 4-6

For TIAA participants ������������������������������������������������������������������������������������������������������������������������������������������������������������������������������7-8

Retirement plan investment advice ������������������������������������������������������������������������������������������������������������������������������������������������������9

Choose your investment path ��������������������������������������������������������������������������������������������������������������������������������������������������������������� 10

New TIAA Brokerage option ������������������������������������������������������������������������������������������������������������������������������������������������������������������� 11

On-site events ���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� 12

About TIAA �����������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������13

Q&A �������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������14-16

We’re here to help �������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������� 17

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 1

A new chapter is about to startHelping you plan and save for the future is important to us at Bowling Green State University (BGSU). That’s why we’re pleased to announce updates to the BGSU Alternative Retirement Plan (ARP) and 403(b) Plan (the “Plans”).

What you need to know W New investment options. The new investments,

carefully selected by BGSU for its employees, may give you the ability to create a diversified retirement portfolio.

W New TIAA contracts will be issued called Retirement Choice (RC) and Retirement Choice Plus (RCP) contracts. Any balance in existing TIAA contracts will remain there, although no new contributions may be added to them.

W Lower fees. BGSU and Cammack Retirement Group have selected investment options with a lower overall cost to you.

W Increased transparency on fees. A new fee structure will make it easier to see the cost of each investment option, as well as fees paid for plan administration.

W You can receive personalized advice on the investment options from a TIAA financial consultant. This service is available as part of your retirement Plans at no additional cost to you. Investment advice is available online, by phone or through a one-on-one advice session.

W New TIAA Brokerage option. If you would like to have access to more investment choices, BGSU is adding a brokerage option. Please note: BGSU will not monitor the performance of the funds in your personal brokerage account, and TIAA does not offer investment advice for brokerage balances.

W Retirement@Work™. A new online portal will be available to enroll in the Plans, select your preferred vendor(s), and view your plan balances. This portal will be available in January 2020 for future changes to your Plans.

No longer employed by BGSU? You are receiving this guide because you have investments in one or more of the BGSU retirement plans. Even though you are not actively contributing and actions may not be required, you should review this information carefully to learn how your account could be affected.

Retirement plan updates start the week of October 7, 2019

Key dates (2019 – 2020) EventsWeek of September 30 You will be enrolled in a TIAA account and receive a confirmation kit with

important information on making the most of your participation with TIAA.

Beginning the week of October 7

On-site group seminars begin.

October 7 Open investment election period starts.

Beginning the week of October 14

One-on-one financial counseling sessions begin.

Beginning with the first payroll in January

Changes take effect. All contributions will be directed to your new account.

2 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

Action plan for the updatesInvestment election period All plan participants will have the opportunity to select investment options from the new menu during an investment election period starting October 7, 2019.

While you can make changes to your investment elections at any time, the investment election period allows you to select from the new investment options prior to the first payroll in January 2020, when the changes go into effect.

Starting October 7 W Access your new account and review investment

options online at TIAA.org/bgsu. You can identify the new accounts by looking for contract types “RC” and “RCP”.

W Update your investment allocations for future contributions.

W Review your beneficiary designation and update if needed.

Have questions? W Attend a seminar to get a guided tour of the plan

changes (page 12).

W Use the online Retirement Advisor tool. It provides investment advice based on your goals and risk tolerance. Visit TIAA.org/retirementadvisor and log in to your account.

W Schedule an advice session with a financial consultant to get personalized retirement plan advice (page 9).

Understanding retirement plan feesWhen making decisions about your BGSU account, it’s important to know there are fees associated with many of the plan’s services and investments. Some fees may be paid by your employer; others may be paid by you based on the services and investments you choose. A recent change impacts how your plan administration costs will be assessed.

Plan servicing fees have always been a part of the BGSU Retirement Plans. The fees pay for TIAA plan management and also cover the costs of reporting, communications, investment consulting and legal advice to operate the Plan.

Previously, the investment expenses of some, but not all, of the funds offered in the Plans covered plan servicing activities. This methodology resulted in participants paying different fee levels, and some paying no fee at all depending on where each participant allocated their assets.

In the past, these fees were included as part of the net expense ratio you pay per investment and were not detailed on your quarterly statements. You will see the details of the new fee structure on the March 31, 2020, quarterly statement for the quarter that begins January 1, 2020.

There are two key points to note about the new fee structure:

W Overall plan expenses are going down.

W The amount each participant pays will be more transparent. It will be clearly labeled on your quarterly statement.

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 3

1 Plan servicing fees can be deducted from investment options in Retirement Choice (RC) and Retirement Choice Plus (RCP) contracts. However, plan servicing fees cannot be deducted from Retirement Annuity (RA), Group Retirement Annuity (GRA), Supplemental Retirement Annuity (SRA) and Group Supplemental Retirement Annuity (GSRA) contracts.

General administrative services Your plan charges an annual administrative fee to cover services such as recordkeeping, legal, accounting, investment advisory, and other plan and participant services.1

Effective January 1, 2020, an annual plan servicing fee of up to 0.125% ($1.25 per $1,000 invested) will be deducted proportionally from each of your investments on a quarterly basis. This amount will be realized by assessing a fee or credit to each investment you choose within the plan. Each fee or credit will be applied to your account on the last business day of each quarter and is identified as a “TIAA Plan Servicing Fee” or a “Plan Servicing Credit” on your quarterly statements (see the “Investment-specific services” section for more detail).

Investment-specific services Each of the plan’s investment options has a fee for investment management and associated services. Plan participants generally pay for these costs through what is called an expense ratio. Expense ratios are displayed as a percentage of assets. For example, an expense ratio of 0.50% means a plan participant pays $5 annually for every $1,000 in assets. Taking the expense ratio into consideration helps you to compare investment fees.

In some cases, investment providers share in the cost of plan administration. This practice is called “revenue sharing.” An investment manager, distribution company or transfer agent may pay a portion of a mutual fund’s expense ratio from their revenues to a plan recordkeeper, such as TIAA, for keeping track of the ownership of the mutual fund’s shares and other shareholder services. Any revenue shared by an investment provider is included as part of each investment’s expense ratio (it is not in addition to the published expense ratios).

Please note that TIAA Traditional, TIAA Real Estate Account and all CREF Annuity accounts do not have revenue sharing. Rather, TIAA may apply a “plan services expense offset” to the plan’s administrative and recordkeeping costs for these investment options.

If the revenue sharing or offset amount of the investment option you select exceeds the total administration cost, a credit is applied to the investment option. If the revenue sharing amount is less than the total administration cost, then a fee is applied. These fee and credit assessments will be shown on your March 31, 2020, quarterly statement.

For information on investment-specific expenses and fees, please refer to the investment table(s) provided. You can also find the expense ratios and other fees and expenses at TIAA.org/bgsu or in the prospectuses at TIAA.org/performance.

Brokerage fee TIAA Brokerage customers are charged a commission on all transactions and other account-related fees in accordance with the TIAA Commission and Fee Schedule. Please visit TIAA.org/SDA_CAA for a complete list of commissions and fees. Other fees and expenses apply to a continued investment in the funds and are described in the fund’s current prospectuses.

All things considered Fees are important, but they are just one factor in how you make your decisions. In addition to fees and expenses, you should be sure your investment choices reflect your personal risk tolerance, the time frame until your retirement, and the appropriate asset allocation to suit your investment needs.

4 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

Your new optionsChanges to the retirement plan’s investment lineup BGSU is taking this opportunity to change the investment options available through the plan. The new investments, carefully selected by BGSU for its employees, may give you the ability to create a diversified retirement portfolio that matches your investment goals and preferences. In addition, should you prefer to avoid making individual fund selections, BGSU has identified a default investment plan option. The new default option is a TIAA-CREF Lifecycle Index Fund. Each lifecycle fund provides a diversified retirement portfolio in a single fund.

The new investments have been organized into three tiers, as reflected in the chart on the following page.

Tier 1 – Lifecycle or target-date fundsA lifecycle or target-date fund is a “fund of funds,” primarily invested in shares of other mutual funds.1 The fund’s investments are automatically adjusted from more aggressive to more conservative over time as the target retirement date approaches. The principal value of a lifecycle fund isn’t guaranteed at any time and will fluctuate with market changes. The target date represents an approximate date when investors may plan to begin withdrawing from the fund. However, you are not required to withdraw the funds at the target date. Also, please note that the lifecycle fund is selected for you based on your projected retirement date (assuming a retirement age of 65). After the target date has been reached, some of your money may be merged into a fund with a more stable asset allocation.

Tier 2 – Core investment lineupComprised of both active and passive investment options, this tier allows you to create your own investment mix, using funds carefully selected for the Plan. Tier 2 will offer mutual fund choices across all major asset classes and will include many recognized major mutual fund providers.

Tier 3 – TIAA Brokerage If you have specialized investing needs and want access to a wider range of options beyond those offered in the plan, consider opening a TIAA Brokerage account. Together with your retirement plan investments, the brokerage account can offer you more options to help meet your investing needs.

With your brokerage account, you can independently research and select from thousands of mutual funds, including from some well-known fund families.2

Please note: BGSU will not monitor the performance of the funds offered through the brokerage account, and TIAA does not offer investment advice for brokerage assets. You will bear the risk of investing through the brokerage account. BGSU recommends that you exercise caution and consider seeking professional guidance when investing through a brokerage account.

Before investing in a brokerage account,3 you can contact TIAA to learn more at 800-927-3059, weekdays, 8 a.m. to 7 p.m. (ET).

1 Lifecycle funds share the risks associated with the types of securities held by each of the underlying funds in which they invest. In addition to the fees and expenses associated with the lifecycle funds, there is exposure to the fees and expenses associated with the underlying mutual funds.

2 The brokerage account option is available to participants who maintain both a legitimate U.S. residential address and a legitimate U.S. mailing address. Certain securities may not be suitable for all investors. Securities are subject to investment risk, including possible loss of the principal amount invested.

3 By opening a brokerage account, you will be charged a commission on all transactions and other account-related fees in accordance with the TIAA Commission and Fee Schedule. Please visit TIAA.org/SDA_CAA. Other fees and expenses apply to a continued investment in the funds and are described in the fund’s current prospectus.

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 5

Annual Fund Operating Expenses

Plan Servicing Fee Calculations (A + B = C)

Account or Fund/Share Class Ticker

Gross Expense Ratio2 %

Net Expense Ratio2 %

A. Revenue Sharing3 %

B. Plan Servicing Fee/

(Credit) %

C. Total Administrative

Fee %

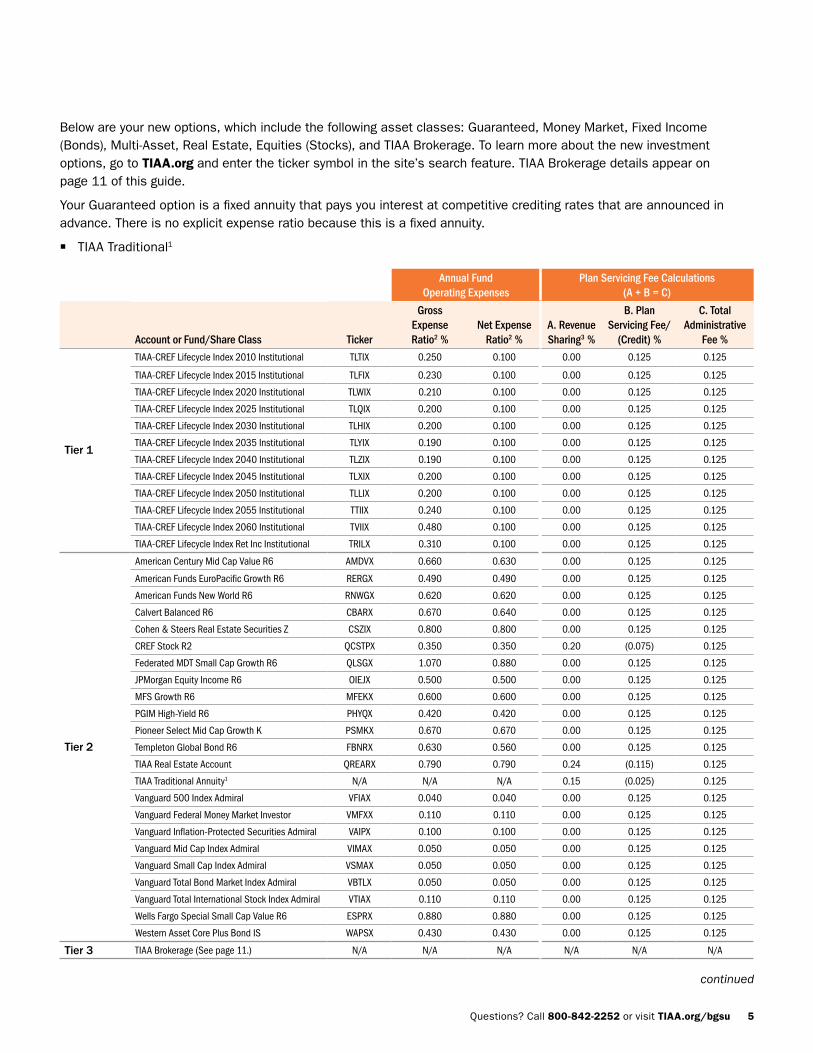

Tier 1

TIAA-CREF Lifecycle Index 2010 Institutional TLTIX 0.250 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2015 Institutional TLFIX 0.230 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2020 Institutional TLWIX 0.210 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2025 Institutional TLQIX 0.200 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2030 Institutional TLHIX 0.200 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2035 Institutional TLYIX 0.190 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2040 Institutional TLZIX 0.190 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2045 Institutional TLXIX 0.200 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2050 Institutional TLLIX 0.200 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2055 Institutional TTIIX 0.240 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index 2060 Institutional TVIIX 0.480 0.100 0.00 0.125 0.125

TIAA-CREF Lifecycle Index Ret Inc Institutional TRILX 0.310 0.100 0.00 0.125 0.125

Tier 2

American Century Mid Cap Value R6 AMDVX 0.660 0.630 0.00 0.125 0.125

American Funds EuroPacific Growth R6 RERGX 0.490 0.490 0.00 0.125 0.125

American Funds New World R6 RNWGX 0.620 0.620 0.00 0.125 0.125

Calvert Balanced R6 CBARX 0.670 0.640 0.00 0.125 0.125

Cohen & Steers Real Estate Securities Z CSZIX 0.800 0.800 0.00 0.125 0.125

CREF Stock R2 QCSTPX 0.350 0.350 0.20 (0.075) 0.125

Federated MDT Small Cap Growth R6 QLSGX 1.070 0.880 0.00 0.125 0.125

JPMorgan Equity Income R6 OIEJX 0.500 0.500 0.00 0.125 0.125

MFS Growth R6 MFEKX 0.600 0.600 0.00 0.125 0.125

PGIM High-Yield R6 PHYQX 0.420 0.420 0.00 0.125 0.125

Pioneer Select Mid Cap Growth K PSMKX 0.670 0.670 0.00 0.125 0.125

Templeton Global Bond R6 FBNRX 0.630 0.560 0.00 0.125 0.125

TIAA Real Estate Account QREARX 0.790 0.790 0.24 (0.115) 0.125

TIAA Traditional Annuity1 N/A N/A N/A 0.15 (0.025) 0.125

Vanguard 500 Index Admiral VFIAX 0.040 0.040 0.00 0.125 0.125

Vanguard Federal Money Market Investor VMFXX 0.110 0.110 0.00 0.125 0.125

Vanguard Inflation-Protected Securities Admiral VAIPX 0.100 0.100 0.00 0.125 0.125

Vanguard Mid Cap Index Admiral VIMAX 0.050 0.050 0.00 0.125 0.125

Vanguard Small Cap Index Admiral VSMAX 0.050 0.050 0.00 0.125 0.125

Vanguard Total Bond Market Index Admiral VBTLX 0.050 0.050 0.00 0.125 0.125

Vanguard Total International Stock Index Admiral VTIAX 0.110 0.110 0.00 0.125 0.125

Wells Fargo Special Small Cap Value R6 ESPRX 0.880 0.880 0.00 0.125 0.125

Western Asset Core Plus Bond IS WAPSX 0.430 0.430 0.00 0.125 0.125

Tier 3 TIAA Brokerage (See page 11.) N/A N/A N/A N/A N/A N/A

Below are your new options, which include the following asset classes: Guaranteed, Money Market, Fixed Income (Bonds), Multi-Asset, Real Estate, Equities (Stocks), and TIAA Brokerage. To learn more about the new investment options, go to TIAA.org and enter the ticker symbol in the site’s search feature. TIAA Brokerage details appear on page 11 of this guide.

Your Guaranteed option is a fixed annuity that pays you interest at competitive crediting rates that are announced in advance. There is no explicit expense ratio because this is a fixed annuity.

W TIAA Traditional1

continued

6 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

1 TIAA Traditional Annuity is a guaranteed insurance contract and not an investment for federal securities law purposes. Any guarantees under annuities issued by Teachers Insurance and Annuity Association of America (TIAA) are subject to its claims-paying ability. Interest credited includes a guaranteed rate plus additional amounts as may be established by the TIAA Board of Trustees. Such additional amounts, when declared, remain in effect for the “declaration year,” which begins each March 1 for accumulating annuities and January 1 for payout annuities. Additional amounts are not guaranteed for periods other than the period for which they were declared.

2 Gross expense ratio includes all of an investment’s expenses. Net expense ratio takes into account any investment fee waivers and expense reductions, giving an indication of what is currently being charged.

3 “Revenue Sharing” describes the practice when investment providers share in the cost of plan administration. Please note that TIAA Traditional, TIAA Real Estate, TIAA Stable Value and all CREF Annuity accounts do not have an explicit revenue share. Rather, they have a “plan services offset” that is applied to your plan’s administrative and recordkeeping costs.

Investment products may be subject to market and other risk factors. See the applicable product literature, or visit TIAA.org and enter a ticker symbol in the site’s search feature for details. Annuity account options are available through annuity contracts issued by TIAA or CREF. These contracts are designed for retirement or other long-term goals and offer a variety of income options, including lifetime income. Payments from the variable annuity accounts are not guaranteed and will rise or fall based on investment performance. A redemption fee may apply. See the fund’s prospectus for details.

BGSU’s restricted annuities and creditsThe following table includes retirement plan annuities in the Retirement Annuity (RA), Group Retirement Annuity (GRA) and Group Supplemental Retirement Annuity (GSRA) contracts that are restricted, which means new contributions are no longer accepted. These annuities will, however, continue to rebate plan offsets.

Annual Fund Operating Expenses

Plan Servicing Fee Calculations (A + B = C)

Account or Fund/Share Class Ticker

Gross Expense Ratio2 %

Net Expense Ratio2 %

A. Revenue Sharing3 %

B. Plan Servicing Fee/

(Credit) %

C. Total Administrative

Fee %

CREF Bond Market R2 (variable annuity) QCBMPX 0.320 0.320 0.20 (0.075) 0.125

CREF Equity Index R2 (variable annuity) QCEQPX 0.265 0.265 0.20 (0.075) 0.125

CREF Global Equities R2 (variable annuity) QCGLPX 0.320 0.320 0.20 (0.075) 0.125

CREF Growth R2 (variable annuity) QCGRPX 0.285 0.285 0.20 (0.075) 0.125

CREF Inflation-Linked Bond R2 (variable annuity) QCILPX 0.270 0.270 0.20 (0.075) 0.125

CREF Money Market R2 (variable annuity) QCMMPX 0.275 0.275 0.20 (0.075) 0.125

CREF Social Choice R2 (variable annuity) QCSCPX 0.290 0.290 0.20 (0.075) 0.125

CREF Stock R2 (variable annuity) QCSTPX 0.350 0.350 0.20 (0.075) 0.125

TIAA Real Estate Account (variable annuity) QREARX 0.790 0.790 0.24 (0.115) 0.125

TIAA Traditional Annuity1 (guaranteed annuity) N/A N/A N/A 0.15 (0.025) 0.125

Your new options (continued)

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 7

For TIAA participantsNew accounts will be issuedDuring the week of September 30, 2019, Retirement Choice (RC) and Retirement Choice Plus (RCP) contracts will be issued for any participant who has contributed within the last ninety days, as follows:

Plan name Current contract New contractBowling Green State University Alternative Retirement Plan (ARP)

Group Retirement Annuity (GRA) Retirement Choice (RC)

Bowling Green State University Tax-Deferred Annuity Plan (403(b))

Supplemental Retirement Annuity (SRA) Group Supplemental Retirement Annuity (GSRA) Retirement Annuity (RA)

Retirement Choice Plus (RCP)

Once the new contract(s) is issued, you will receive an enrollment confirmation from TIAA that will provide additional information about your new account(s). You will receive one confirmation for each contract in which you are enrolled. Your current beneficiary designation(s) will be applied to your new account(s).

How your future contributions and current account balances will be affected Starting with the first payroll in 2020, your future contributions will be directed to your new account(s) and invested in the lifecycle fund that corresponds to the year you turn 65, as shown in the chart below. For example, if you will turn 65 in 2044, contributions will be directed to the TIAA-CREF Lifecycle Index 2045 Fund. If you wish to make your own fund selections from those in Tier 2, you may do so.

Any balance(s) you have with TIAA will remain in your existing account(s), although no new contributions, rollovers or transfers may be made to these accounts. You will only be permitted to transfer balances among CREF Money Market Account, CREF Stock Account, TIAA Real Estate and TIAA Traditional Annuity. If you would like to transfer balance(s) to the new investment options, contact a TIAA financial consultant for more information.

Birth year chart

Investment option Ticker Birth yearTIAA-CREF Lifecycle Index 2010 Fund – Institutional Class TLTIX Prior to 1948

TIAA-CREF Lifecycle Index 2015 Fund – Institutional Class TLFIX 1948 – 1953

TIAA-CREF Lifecycle Index 2020 Fund – Institutional Class TLWIX 1954 – 1958

TIAA-CREF Lifecycle Index 2025 Fund – Institutional Class TLQIX 1959 – 1963

TIAA-CREF Lifecycle Index 2030 Fund – Institutional Class TLHIX 1964 – 1968

TIAA-CREF Lifecycle Index 2035 Fund – Institutional Class TLYIX 1969 – 1973

TIAA-CREF Lifecycle Index 2040 Fund – Institutional Class TLZIX 1974 – 1978

TIAA-CREF Lifecycle Index 2045 Fund – Institutional Class TLXIX 1979 – 1983

TIAA-CREF Lifecycle Index 2050 Fund – Institutional Class TLLIX 1984 – 1988

TIAA-CREF Lifecycle Index 2055 Fund – Institutional Class TTIIX 1989 – 1993

TIAA-CREF Lifecycle Index 2060 Fund – Institutional Class TVIIX 1994 and after

continued

8 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

Understanding your new account(s) There are a number of differences between your current contracts and the new Retirement Choice (RC) and Retirement Choice Plus (RCP) contracts. Most of the differences apply to the TIAA Traditional Annuity and are highlighted below. If you’re thinking about transferring some or all of your account balances to your new contract, make sure you understand the differences before you initiate a transfer.

W Under the RC and RCP contracts, TIAA Traditional has a rate guarantee that is between 1% and 3%, determined annually, which may be lower than the guaranteed rate in your current contract.1 The adjustable rate guarantee in the new contracts allows TIAA to be more responsive to the prevailing interest rate environment, and provides the potential for higher credited rates through the crediting of additional amounts.2

W If TIAA Traditional balances are transferred out of an existing contract, you risk giving up a favorable crediting rate(s) on older contributions.

W TIAA Traditional balances in the Retirement Choice contract can be liquidated within a shorter time frame than under the existing contracts.

W Moving money from an existing contract to a new contract is a permanent decision. Money cannot be moved back into a legacy contract.

For details, see the contract comparison chart located at TIAA.org/comparison. If you have questions, call 800-842-2252.

If you have any recurring transfers or rollovers in your current contracts, you will need to provide updated investment instructions. You will receive a separate communication if your account is affected. If you do not provide instructions upon receiving the letter, future transfers or rollovers may be automatically redirected to your new contracts and the default investment option for the plan.

Choosing different investmentsBeginning October 7, 2019, you may change the way future contributions are directed before the new investment menu takes effect with the first January payroll in 2020. If you do not provide investment instructions

prior to the first payroll contribution in 2020, you can always make changes after the new menu is in effect. If you do not make a selection prior to the first payroll in 2020, your future contributions will be directed to your new account(s) and invested in the TIAA-CREF Lifecycle Index Fund that corresponds to the year you turn 65.

Action steps Select investments. Beginning October 7, you can update your investment choices for future contributions to begin with the first payroll in January 2020.

Name your beneficiary. Your beneficiary designation will be carried over from your existing contract(s). Naming a beneficiary is an important aspect of managing your retirement account. Please take this opportunity to confirm your choices.

Attend a seminar. Find out about the retirement program changes and steps you may wish to take. See page 12.

Get advice. Has it been awhile since you reviewed your investment mix? You’re eligible to receive retirement plan investment advice at no additional cost. It’s all about helping you retire on your terms. Schedule your session at TIAA.org/schedulenow.

Retirement plan online portal coming in early 2020—Retirement@Work™ The new retirement plan online portal was designed to give you greater access to your retirement account. Currently, the enrollment and account management processes are paper-based, so this will enhance your access and experience.

Use the new Retirement@Work online portal to:

W Enroll in the retirement plans

W View all BGSU 403(b) and ARP retirement plan balances regardless of vendor

W Start or change voluntary contributions

W Update vendors

W Select new investment options via links to each vendor’s website

W Access Brokerage

W Manage your account on an ongoing basis

You will hear more about Retirement@Work as the live date approaches, including how to access and use the system.

1 Guarantees are subject to TIAA’s claims-paying ability. 2 TIAA’s Board of Trustees declares whether additional amounts will be paid in March of each year. Additional amounts are not guaranteed. Such

additional amounts, when declared, remain in effect for the “declaration year” which begins each March 1 for accumulating annuities and January 1 for payout annuities. Additional amounts are not guaranteed for periods other than the period for which they were declared.

For TIAA participants (continued)

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 9

Retirement plan investment adviceAs a participant in the BGSU retirement plans, you have access to personalized retirement plan advice on the Plans’ investment options from a TIAA financial consultant. This service is available as part of your retirement program at no additional cost to you.

TIAA’s advice is designed to help you answer important questions, including:1. Am I on track to reach my retirement savings goals?

We’ll help you analyze how your investments are performing and determine if you’re saving enough to help address your needs.

2. Which combination of retirement plan investments is right for me? Get assistance picking the right investments based on your Plans’ investment options, diversifying properly and allocating contributions to balance your need for growth potential with your tolerance for risk.

3. How can I meet my income needs in retirement? Get help determining the amount you’ll need to meet your retirement income goals.

IMPORTANT: The projections or other information generated by the Retirement Advisor tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Results may vary with each use and over time.

How to access TIAA’s advice

Online Get quick, convenient answers using the Retirement Advisor online tool. Visit TIAA.org/retirementadvisor and log in to your account.

By phone or in person Receive personalized retirement plan investment advice either over the phone or in person.

Schedule your advice session by calling 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET).

You can also schedule online at TIAA.org/schedulenow.

10 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

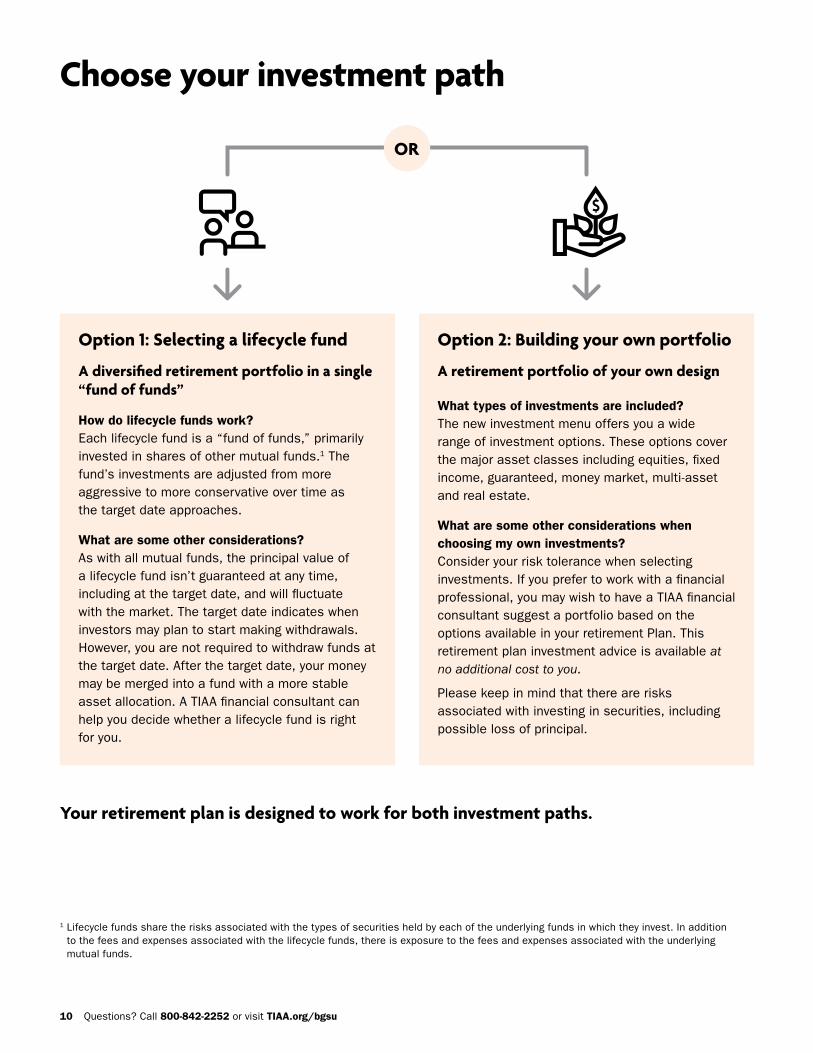

Option 1: Selecting a lifecycle fund

A diversified retirement portfolio in a single “fund of funds”

How do lifecycle funds work? Each lifecycle fund is a “fund of funds,” primarily invested in shares of other mutual funds.1 The fund’s investments are adjusted from more aggressive to more conservative over time as the target date approaches.

What are some other considerations? As with all mutual funds, the principal value of a lifecycle fund isn’t guaranteed at any time, including at the target date, and will fluctuate with the market. The target date indicates when investors may plan to start making withdrawals. However, you are not required to withdraw funds at the target date. After the target date, your money may be merged into a fund with a more stable asset allocation. A TIAA financial consultant can help you decide whether a lifecycle fund is right for you.

Choose your investment path

Option 2: Building your own portfolio

A retirement portfolio of your own design

What types of investments are included? The new investment menu offers you a wide range of investment options. These options cover the major asset classes including equities, fixed income, guaranteed, money market, multi-asset and real estate.

What are some other considerations when choosing my own investments? Consider your risk tolerance when selecting investments. If you prefer to work with a financial professional, you may wish to have a TIAA financial consultant suggest a portfolio based on the options available in your retirement Plan. This retirement plan investment advice is available at no additional cost to you.

Please keep in mind that there are risks associated with investing in securities, including possible loss of principal.

Your retirement plan is designed to work for both investment paths.

1 Lifecycle funds share the risks associated with the types of securities held by each of the underlying funds in which they invest. In addition to the fees and expenses associated with the lifecycle funds, there is exposure to the fees and expenses associated with the underlying mutual funds.

OR

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 11

New TIAA Brokerage option

1 The brokerage account option is available to participants who maintain both a legitimate U.S. residential address and a legitimate U.S. mailing address. Certain securities may not be suitable for all investors. Securities are subject to investment risk, including possible loss of the principal amount invested.

2 By opening a brokerage account, you will be charged a commission only on applicable transactions and other account-related fees in accordance with the TIAA Commission and Fee Schedule. Please visit TIAA.org/SDA_CAA. Other fees and expenses apply to a continued investment in the funds and are described in the fund’s current prospectuses.

Access thousands of mutual funds and many well-known fund families beyond the core investment options.1

For investors with specialized investing needs, more choice can mean more opportunity to direct retirement investments across markets and asset classes outside of your Plan’s core lineup.

With your brokerage account, you can independently research and select from thousands of mutual funds.

It’s important to understand that BGSU will not monitor the performance of the funds offered through the brokerage account, and TIAA does not offer investment advice for brokerage assets. Plan participants will bear the risk of investing through the brokerage account. BGSU recommends that you exercise caution and consider seeking professional guidance when investing through a TIAA Brokerage account.

Please note that you may only invest up to 95% of your BGSU Plan account balance in a TIAA Brokerage account.

Before investing in a brokerage account, consider contacting TIAA to learn more.

Learn more about a brokerage account2 by contacting us at 800-927-3059, weekdays, 8 a.m. to 7 p.m. (ET).

12 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

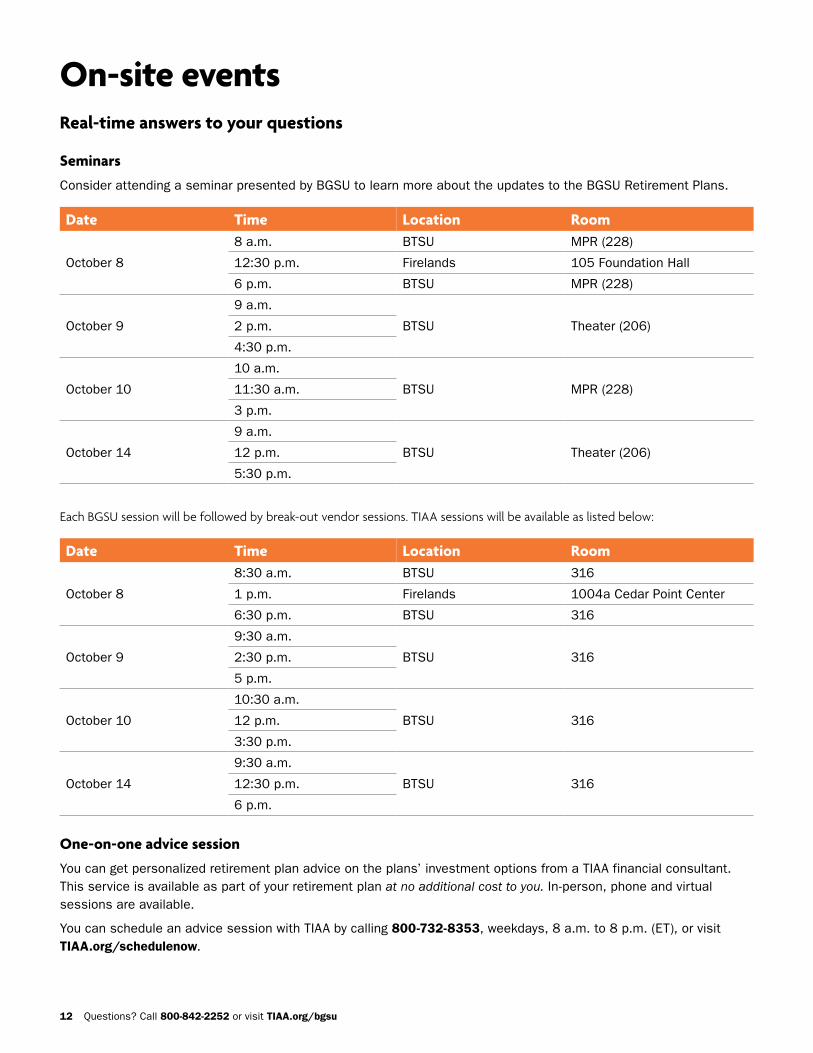

On-site eventsReal-time answers to your questions

SeminarsConsider attending a seminar presented by BGSU to learn more about the updates to the BGSU Retirement Plans.

Date Time Location Room

October 8

8 a.m. BTSU MPR (228)

12:30 p.m. Firelands 105 Foundation Hall

6 p.m. BTSU MPR (228)

October 9

9 a.m.

BTSU Theater (206)2 p.m.

4:30 p.m.

October 10

10 a.m.

BTSU MPR (228)11:30 a.m.

3 p.m.

October 14

9 a.m.

BTSU Theater (206)12 p.m.

5:30 p.m.

Each BGSU session will be followed by break-out vendor sessions. TIAA sessions will be available as listed below:

Date Time Location Room

October 8

8:30 a.m. BTSU 316

1 p.m. Firelands 1004a Cedar Point Center

6:30 p.m. BTSU 316

October 9

9:30 a.m.

BTSU 3162:30 p.m.

5 p.m.

October 10

10:30 a.m.

BTSU 31612 p.m.

3:30 p.m.

October 14

9:30 a.m.

BTSU 31612:30 p.m.

6 p.m.

One-on-one advice sessionYou can get personalized retirement plan advice on the plans’ investment options from a TIAA financial consultant. This service is available as part of your retirement plan at no additional cost to you. In-person, phone and virtual sessions are available.

You can schedule an advice session with TIAA by calling 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET), or visit TIAA.org/schedulenow.

1918 | TIAA Teachers Insurance and

Annuity Association of America created

About TIAAProviding strong support on the road to retirement no matter where you are todayTIAA’s purpose has remained constant since it was established 100 years ago: We’re here to help you save for—and generate income during—retirement. Over the years, we’ve regularly enhanced the ways we deliver on our purpose.

As an organization with deep roots among nonprofits—in higher education, government, hospital/medical, research, religious institutions and K-12—TIAA is committed to continuous learning. When we see opportunities to enhance our retirement plan services, we share them with the institutions we serve.

Not sure where to begin? You can meet with us to help you take the next step!Personalized retirement plan advice is available on the Plans’ investment options from a TIAA financial consultant. This service is available as part of your retirement program at no additional cost to you. You can schedule a session by calling 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET). You can also visit TIAA.org/schedulenow.

14 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

Q&A1. Why is BGSU updating the ARP and 403(b) Plans?

BGSU is committed to providing you with competitive retirement benefits and recently conducted a review of the retirement Plans. The resulting updates are intended to give you the investments, services and tools you need to pursue your retirement savings goals.

2. How can I learn about the new investment options?A list of the new investment options is included in this guide. You can visit the dedicated retirement Plan website at TIAA.org/bgsu for additional information.

3. What if I would like help making investment choices?You can get personalized advice on the Plans’ investment options from a TIAA financial consultant. This service is available as part of your retirement program at no additional cost to you.

To schedule an advice session, call TIAA at 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET). You can also schedule online at TIAA.org/schedulenow.

4. What should I expect from an advice session?You can expect a thorough review of your account and an action plan for moving forward. Bring all your investment account statements, including any retirement investments outside of the retirement plans and your most recent Social Security statement, if available. A TIAA financial consultant will use this information to understand your current financial situation and develop an action plan. You may bring anyone you like to your session with you.

5. What happens to my current outstanding systematic withdrawal, TPA (transfer payout annuity) or required minimum distribution? You will receive separate communications if you need to take any action.

6. How do lifecycle funds work?Each lifecycle fund consists of underlying mutual funds that invest in a broad range of asset classes. The allocations and risk level depend on how many years remain until the fund’s target date. To help reduce risk as the fund’s target date approaches, the fund’s mix of stocks, bonds and other types of investments is adjusted to a more conservative mix.

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 15

7. What else should I know about lifecycle funds?As with all mutual funds, the principal value of a lifecycle fund isn’t guaranteed at any time and will fluctuate with market changes. The target date indicates when investors may plan to start making withdrawals. However, you are not required to withdraw your money at the target date. A TIAA financial consultant can help you decide whether a lifecycle fund is right for you.

8. I am currently contributing to TIAA. What happens to my current account balances and future contributions?All balances will remain where they are. Starting October 7, 2019, you can direct future contributions to other options on the new investment menu. If no action is taken, BGSU has provided instructions to invest future contributions in the TIAA-CREF Lifecycle Index Fund closest to the year you turn 65, effective with the first payroll in January 2020.

9. Does it make sense to consolidate my retirement accounts?Some individuals might find it easier to manage their retirement money by working with only one provider. That said, transferring balances can sometimes trigger costs. Before consolidating outside retirement balances, check with your employee benefits office to see if you can transfer those balances directly to your TIAA retirement account. You should carefully consider all your options. For instance, you may be able to leave money with a prior provider, roll over money to an IRA, or cash out all or part of the account value. Weigh the advantages and disadvantages of each option carefully, including investment options and services, fees and expenses, withdrawal options, required minimum distributions, tax treatment and your particular financial needs. You should seek the guidance of your financial professional and tax advisor before consolidating balances.

continued

16 Questions? Call 800-842-2252 or visit TIAA.org/bgsu

Q&A (continued)

10. Can I move money from an existing TIAA account to a new one?Yes, but it’s a move you’ll want to weigh carefully. You may move money out of your existing TIAA contracts to the new contracts, subject to any restrictions that apply to the investments. However, any money that you move out of your existing contract(s) cannot be moved back into them. Money in the TIAA Traditional Annuity deserves special attention. For instance, money moved out of TIAA Traditional in the existing contracts will no longer receive the 3% minimum guaranteed rate. In short, the pros and cons are different for every participant. To learn more about TIAA Traditional, liquidity rules, and the differences between RC and RCP contracts, please see the contract comparison chart at TIAA.org/comparison or contact TIAA at 800-842-2252.

11. What are annuities?There are different types of annuities, but they are typically designed to give you the opportunity to help grow your money while you’re working and provide you with the option to receive income for life when you retire. In fact, annuities are the only retirement products that can guarantee to pay you (or you and a spouse or partner) income for life.

Guaranteed annuities (also known as fixed annuities): Earn a minimum guaranteed interest rate on your contributions, plus the potential for additional amounts of interest. In retirement, guaranteed annuities can offer you income for life that will never fall below a certain guaranteed level and provide income that is guaranteed to last for your lifetime.1

Variable annuities: Invest in a variety of asset classes, and account values will fluctuate based on the performance of the investments in the accounts. It is possible to lose money in variable annuities. In retirement, variable annuities can provide an income stream that is guaranteed to last for your lifetime, but the actual amount will rise or fall based on investment performance.

1 Guarantees are based on the claims-paying ability of the issuing company.

Questions? Call 800-842-2252 or visit TIAA.org/bgsu 17

We’re here to help

Not sure where to begin? Let us help you take the next step!

Manage your account online by going to TIAA.org/bgsu and selecting Log in.

If you’re new to TIAA, select Log in, then click Register for Online Access. Follow the on-screen directions to gain online access to your account.

If you have any questions or would like assistance selecting your new investment options, call TIAA at 800-842-2252, weekdays, 8 a.m. to 10 p.m., and Saturday, 9 a.m. to 6 p.m. (ET).

Schedule a one-on-one advice session by calling TIAA at 800-732-8353, weekdays, 8 a.m. to 8 p.m. (ET), or visit TIAA.org/schedulenow. There is no additional cost to you for this service.

In person Phone Online

Retirement planning on the goTake your planning with you with the TIAA mobile app.

Get a clear picture of your accounts anytime with the TIAA app:

W Check your balances

W Track investment/fund performance

W Contact a TIAA financial consultant

W Retrieve secure messages and notifications about account activity

Visit your favorite app store to download today.

MT 910136 910136 1248507-Guide (09/19)

This material is for informational or educational purposes only and does not constitute investment advice under ERISA. This material does not take into account any specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on the investor’s own objectives and circumstances.

Distributions from 403(b) plans before age 59½, severance from employment, death or disability may be prohibited, limited and/or subject to substantial tax penalties. Different restrictions may apply to other types of plans.

The TIAA group of companies does not provide legal or tax advice. Please consult your legal or tax advisor.

Investment, insurance, and annuity products are not FDIC insured, are not bank guaranteed, are not bank deposits, are not insured by any federal government agency, are not a condition to any banking service or activity, and may lose value.

You should consider the investment objectives, risks, charges, and expenses carefully before investing. Please call 877-518-9161 or go to TIAA.org/bgsu for current product and fund prospectuses that contain this and other information. Please read the prospectuses carefully before investing.TIAA-CREF Individual & Institutional Services, LLC, Member FINRA and SIPC, distributes securities products. After-tax annuities are issued by TIAA-CREF Life Insurance Company, New York, NY. Brokerage Services are provided by TIAA Brokerage, a division of TIAA-CREF Individual & Institutional Services, LLC. Member FINRA/SIPC. Each is solely responsible for its own financial condition and contractual obligations.

©2019 Teachers Insurance and Annuity Association of America-College Retirement Equities Fund, 730 Third Avenue, New York, NY 10017