New Jersey Division of Taxation TAX OPIC Part … · New Jersey Division of Taxation Bulletin GIT-6...

33

AX OPIC New Jersey Division of Taxation Bulletin GIT-6 Rev. 12/07 T Part-Year Residents Introduction Part-year residents are subject to tax on income received from all sources (both inside and out- side New Jersey) during the portion of the year that they were residents of the State. Likewise, part-year nonresidents are subject to tax on any income received from New Jersey sources while they were nonresidents. This bulletin explains: • Who is a part-year resident/part-year non- resident for New Jersey income tax purposes, as well as who is a full-year resident or nonresident; • What your New Jersey income tax respon- sibilities are as a part-year resident/part-year nonresident; • How to complete a part-year New Jersey income tax return; and • When a part-year resident must file both resi- dent and nonresident income tax returns with New Jersey in the same tax year. NOTE: This bulletin covers filing requirements for individual residents and nonresidents only. The examples illustrate how to pre- pare part-year returns for tax year 2007. Thus, the forms and amounts (tax rates, income exclusions, etc.) shown in the text and examples may not reflect cur- rent information in subsequent tax years. For information on estates and trusts, see the in- structions for the New Jersey Gross Income Tax Fiduciary Return (Form NJ-1041). Contents Introduction .............................................. 1 Definitions ................................................ 2 Filing Requirements .................................. 3 Filing Status Considerations .................... 6 How Residents and Nonresidents Are Taxed ........................ 7 Completing a Part-Year Resident Return ..................................... 9 Completing a Part-Year Nonresident Return ............................... 18 Example: Part-Year Resident/Part-Year Nonresident Return Completion ........... 24 Important Changes • Eligibility for the New Jersey Earned In- come Tax Credit (NJEITC) has been ex- panded so that for 2007 taxpayers who are eligible and file for a Federal earned in- come credit can also receive a New Jersey credit in the amount equal to 20% of their Federal benefit. The percentage used to cal- culate the NJEITC will increase to 22.5% for tax year 2008 and to 25% of the Federal benefit for tax years 2009 and thereafter. • Any reference in this bulletin to a spouse also refers to a partner to a civil union (CU) recognized under New Jersey law.

Transcript of New Jersey Division of Taxation TAX OPIC Part … · New Jersey Division of Taxation Bulletin GIT-6...

AXOPIC

New Jersey Division of Taxation

Bulletin GIT-6

Rev. 12/07

T Part-Year Residents

IntroductionPart-year residents are subject to tax on incomereceived from all sources (both inside and out-side New Jersey) during the portion of the yearthat they were residents of the State. Likewise,part-year nonresidents are subject to tax on anyincome received from New Jersey sources whilethey were nonresidents. This bulletin explains:

• Who is a part-year resident/part-year non-resident for New Jersey income tax purposes,as well as who is a full-year resident ornonresident;

• What your New Jersey income tax respon-sibilities are as a part-year resident/part-yearnonresident;

• How to complete a part-year New Jerseyincome tax return; and

• When a part-year resident must file both resi-dent and nonresident income tax returns withNew Jersey in the same tax year.

NOTE: This bulletin covers filing requirementsfor individual residents and nonresidentsonly. The examples illustrate how to pre-pare part-year returns for tax year 2007.Thus, the forms and amounts (tax rates,income exclusions, etc.) shown in thetext and examples may not reflect cur-rent information in subsequent tax years.

For information on estates and trusts, see the in-structions for the New Jersey Gross Income TaxFiduciary Return (Form NJ-1041).

Contents

Introduction .............................................. 1

Definitions ................................................ 2

Filing Requirements .................................. 3

Filing Status Considerations .................... 6

How Residents and Nonresidents Are Taxed ........................ 7

Completing a Part-YearResident Return..................................... 9

Completing a Part-YearNonresident Return ...............................18

Example: Part-Year Resident/Part-YearNonresident Return Completion ...........24

Important Changes

• Eligibility for the New Jersey Earned In-come Tax Credit (NJEITC) has been ex-panded so that for 2007 taxpayers who areeligible and file for a Federal earned in-come credit can also receive a New Jerseycredit in the amount equal to 20% of theirFederal benefit. The percentage used to cal-culate the NJEITC will increase to 22.5%for tax year 2008 and to 25% of the Federalbenefit for tax years 2009 and thereafter.

• Any reference in this bulletin to a spousealso refers to a partner to a civil union(CU) recognized under New Jersey law.

Rev. 12/072

Bulletin GIT-6

DefinitionsFor New Jersey income tax purposes, yourresidency status depends on where you weredomiciled and where you maintained a permanentplace of abode during the tax year. In general,when you change your domicile to (or from) thisState during the year, you are a resident of NewJersey for part of the year (part-year resident) anda nonresident of New Jersey for part of the year(part-year nonresident). Your move is generallyconsidered a change of residency status (residentto nonresident or vice versa) if at the time youmoved, you intended to permanently leave onehome and establish a new, fixed, and permanenthome somewhere else.

Full-Year ResidentYou were a full-year New Jersey resident if:

• New Jersey was your domicile for the entireyear, and you did not satisfy all three condi-tions for nonresident status (below); or

• New Jersey was not your domicile, but youmaintained a permanent place of abode inNew Jersey for the entire year and you spentmore than 183 days in New Jersey. (Membersof the U.S. Armed Forces stationed in NewJersey who are not domiciled here are notresidents under this definition.)

Full-Year NonresidentYou were a full-year New Jersey nonresident if:

• New Jersey was not your domicile, and youspent 183 days or less here; or

• New Jersey was not your domicile, you spentmore than 183 days here, but you did notmaintain a permanent home here; or

• New Jersey was your domicile and you metall three of the following conditions for theentire year:

1. You did not maintain a permanent placeof abode in New Jersey; and

2. You did maintain a permanent place ofabode outside of New Jersey; and

3. You did not spend more than 30 days inNew Jersey.

Part-Year Resident/Part-Year NonresidentIf, as a result of a change of your domicile, youmet the definition of New Jersey resident ornonresident for only part of the year, you are aresident for part of the year (part-year resident)and a nonresident for the remainder of that year(part-year nonresident).

Domicile is any place you regard as your per-manent home—the place to which you intend toreturn after a period of absence (e.g., vacationabroad, business assignment, educational leave,etc.). You have only one domicile, although youmay have more than one place to live. Onceestablished, your domicile continues until youmove to a new location with the intent to estab-lish a fixed and permanent home there. Movingto a new location, even for a long time, does notchange your domicile if you intend to remainonly for a limited time.

Domicile is based on many factors, includingyour intent, where you register to vote, maintaina driver’s license and vehicle registration, havefamily ties, etc. You can have only one domicileat a time. The burden of proof is upon the per-son asserting a change of domicile to show thatthe necessary intention existed to abandon his orher domicile in one location and to establish afixed and permanent home in another.

Part-Year Residents

Rev. 12/07 3

Permanent place of abode is a residence (abuilding or structure where a person can live)that you maintain permanently as your household,whether you own it or not. It usually includes aresidence your spouse/civil union partner ownsor leases.

A residence, whether inside or outside of NewJersey, is not permanent if you maintain it onlyduring a temporary or limited period of time, nomatter how long, for the accomplishment of aparticular purpose (e.g., temporary job assign-ment). Likewise, a home used only for vacationsis not a permanent place of abode.

If New Jersey is your domicile, you will beconsidered a resident for New Jersey tax pur-poses unless you meet all three conditions fornonresident status. See Full-Year Nonresidenton page 2. Likewise, if New Jersey is not yourdomicile, you will be considered a New Jerseyresident only if you maintain a permanent placeof abode in New Jersey and spend more than183 days here.

Filing RequirementsYour filing status and gross income determinewhether you have to file a New Jersey incometax return. Age is not a factor in determiningwhether a person must file. Even minors (in-cluding students) and senior citizens must file ifthey meet the income filing requirements.

To find out whether or not you are required tofile a New Jersey income tax return, use the“Who Must File” chart in either the resident(NJ-1040) or nonresident (NJ-1040NR) returnbooklet.

Time Period Covered by Return(Full-Year or Part-Year)The period covered by your return will be twelvemonths (full-year return), or less than twelvemonths (part-year return). Most taxpayers use acalendar year (January 1–December 31) to recordtheir income. Fiscal year filers use a different pe-riod (e.g., July–June). This bulletin assumes thatyou are a calendar year filer.

New Jersey has two personal income tax returnsfor individuals: Form NJ-1040 for residents andForm NJ-1040NR for nonresidents. New Jerseydoes not have separate tax returns for part-yearresidents or part-year nonresidents. You mustuse either Form NJ-1040 or Form NJ-1040NR(or both) depending on your residency statusduring the year, and show the income you re-ceived during the period of time covered by thereturn. Part-year residents use the same form asfull-year residents (Form NJ-1040) and indicatethe period of their New Jersey residency aboveLine 1. The return should show only the incomereceived during that period. Likewise, part-yearnonresidents use the same form as full-year non-residents (Form NJ-1040NR), and indicateabove Line 1 the period of time they were NewJersey residents.

If you file a part-year nonresident return, youwill also file a part-year resident return, unlessyou had no income during the part of the yearyou were a resident. You must allocate your in-come between the resident and nonresident re-turns as appropriate. That is, report the incomeyou received during the time you were a residenton your part-year resident return, and report theincome you received during the part of the yearyou were a nonresident on your part-year non-resident return.

Rev. 12/074

Bulletin GIT-6

Examples1. Mary Smith was a New Jersey resident from

January 1 through December 31. She files a“full-year” resident return which showsincome received during the twelve-monthperiod January–December.

2. Harry and Louise Evans were New Jerseyresidents from May 1 to December 31. Theymust file a “part-year” resident return andreport the income they received during theirperiod of residency (May–December).

NOTE: If they had income from New Jerseysources between January 1 andApril 30, the period when their resi-dency status was “nonresident,” theymust file a New Jersey part-year non-resident return too. See Part-YearNonresidents on page 6.

3. Jane Henderson was a full-year resident ofNew York who worked in New Jersey fromJuly through November. She files a “full-year” nonresident return because she was anonresident for the entire year. Her NewJersey nonresident return will show theincome she received during the period shewas a nonresident i.e., January–December.

4. Adam Crenshaw worked in New Jersey forthe entire year. For three months of the yearhe was a New Jersey resident and for the re-maining nine months, a Delaware resident.Adam must file two New Jersey income taxreturns: (1) a “part-year” resident returnwhich shows the income he received duringthe three months he was a New Jersey resi-dent and (2) a “part-year” nonresident returnwhich shows his income during the periodhe was a nonresident of New Jersey.

Residency Status and IncomeFull-Year Residents—• You must file a full-year New Jersey resident

income tax return if you were a New Jerseyresident for the entire year and your grossincome for the entire year was more than$20,000 ($10,000 if filing status is single ormarried/CU partner, filing separate return.

• You are not required to file a full-year NewJersey resident income tax return if you werea New Jersey resident for the entire year andyour gross income for the entire year was$20,000 or less ($10,000 or less if filingstatus is single or married/CU partner, filingseparate return).

NOTE: If you are a full-year resident and yourincome is below the amount at whichyou would be required to file a tax re-turn, you must file Form NJ-1040 (or fileelectronically using NJ WebFile or ap-proved vendor software) to claim a re-fund of income tax withheld or estimatedpayments made. You must also file a re-turn to receive a New Jersey earned in-come tax credit even if you have no taxliability to New Jersey.

Part-Year Residents—• You must file a part-year New Jersey resident

income tax return if you were a New Jerseyresident for part of the year and your gross in-come from all sources for the entire year wasmore than $20,000 ($10,000 if filing status issingle or married/CU partner, filing separatereturn) and you received any income (whetherfrom New Jersey sources or not) during thepart of the year you were a New Jerseyresident.

Part-Year Residents

Rev. 12/07 5

You are subject to tax on the income shownon your part-year resident return if your grossincome for the entire year was more than$20,000 ($10,000 if filing status is single ormarried/CU partner, filing separate return),even if the income you reported on your part-year return for the period of New Jersey resi-dency was $20,000 or less ($10,000 or less iffiling status is single or married/CU partner,filing separate return).

No New Jersey income tax is due if the in-come you received during the entire year was$20,000 or less ($10,000 or less if filingstatus is single or married/CU partner, filingseparate return). If your gross income was$20,000 or less ($10,000 or less if filing sta-tus is single or married/CU partner, filingseparate return), enclose a copy of your Fed-eral income tax return when you file yourpart-year New Jersey return. If you did notfile a Federal return, enclose a statement withyour New Jersey return certifying that yourincome for the entire year was $20,000 or less($10,000 or less if filing status is single ormarried/CU partner, filing separate return).

NOTE: When you are a part-year New Jerseyresident, you are a nonresident for theremainder of that year. See the filingrequirements for Part-Year Nonresidentson page 6.

Examples1. During 2007, Jane Hanson, single, was a

resident of California for ten months and aNew Jersey resident for two months. Herincome as a California resident totaled$23,000, and the income she received duringthe two months she was a New Jersey resi-dent was $2,900. Jane is subject to tax on

the $2,900 she received as a part-year NewJersey resident because her income for theentire year was more than $10,000.

2. Martha Gibson, single, was a New Jerseyresident from January through September2007, when she moved to Florida and be-came a resident there. Her income as a NewJersey resident totaled $5,800 and her in-come while a Florida resident was $600.Martha is not required to file a New Jerseypart-year resident return, and she owes noNew Jersey income tax on the $5,800 she re-ceived as a part-year New Jersey resident be-cause her income for the entire year was$10,000 or less. However, Martha must filea return to claim any refund of New Jerseyincome tax that was either withheld or re-mitted through estimated payments. Whenshe files her 2007 New Jersey return, Marthamust enclose a copy of her Federal incometax return or, if no Federal return is filed, astatement certifying that her income for theyear was $10,000 or less.

Full-Year Nonresidents—• You must file a full-year New Jersey nonresi-

dent income tax return if you were not a NewJersey resident for any part of the year andyour gross income for the entire year from allsources (both inside and outside New Jersey)was more than $20,000 ($10,000 if filing sta-tus is single or married/CU partner, filingseparate return) and you received any amountof income from New Jersey sources duringthe year.

• You are not required to file a full-year non-resident return if you were a nonresident forthe entire year and your gross income from allsources (both inside and outside New Jersey)

Rev. 12/076

Bulletin GIT-6

was $20,000 or less ($10,000 or less if filingstatus is single or married/CU partner, filingseparate return).

NOTE: If you are a full-year nonresident andyour income is below the amount atwhich you would be required to file a taxreturn, you must file Form NJ-1040NRto claim a refund of income tax withheldor estimated payments made.

Part-Year Nonresidents—If you were a New Jersey resident for part of theyear, you were a nonresident for the remainderof that year. File part-year resident and/or non-resident returns as follows:

• You must file both a part-year resident returnand a part-year nonresident return if yourgross income from all sources for the entireyear was more than $20,000 ($10,000 if filingstatus is single or married/CU partner, filingseparate return) and you received income(whether from New Jersey sources or not)during the part of the year you were a residentand you received any amount of income fromNew Jersey sources during the part of the yearyou were a nonresident.

File only a part-year resident return if youreceived income (whether from New Jerseysources or not) during the part of the year youwere a resident, but you had no income fromNew Jersey sources during the part of the yearyou were a nonresident. See Part-Year Resi-dents on page 4.

• You must file only a part-year nonresidentincome tax return if your gross income fromall sources for the entire year was more than$20,000 ($10,000 if filing status is single ormarried/CU partner, filing separate return)

and you had income from New Jersey sourcesduring the part of the year you were a non-resident and you had no income during thepart of the year you were a resident.

No New Jersey income tax is due if the in-come you received from all sources duringthe entire year was $20,000 or less ($10,000or less if filing status is single or married/CUpartner, filing separate return). If your grossincome was $20,000 or less ($10,000 or lessif filing status is single or married/CU part-ner, filing separate return), enclose a copy ofyour Federal income tax return when you fileyour part-year New Jersey return. If you didnot file a Federal return, enclose a statementwith your New Jersey return certifying thatyour income for the entire year was $20,000or less ($10,000 or less if filing status issingle or married/CU partner, filing separatereturn).

• You need not file either a resident or a non-resident return if you received no incomeduring the part of the year you were a resi-dent, and no income from New Jersey sourcesduring the part of the year you were anonresident.

Filing Status ConsiderationsSpouse/Civil Union Partner WithDifferent Residency StatusIn general, you must use the same filing status onyour New Jersey return as you do for Federalincome tax purposes. If you do not file a Federalreturn, but you are filing a New Jersey return, usethe same filing status that you would have used ifyou had filed a Federal return, unless you are apartner in a civil union. For more informationrequest Tax Topic Bulletin GIT-4, Filing Status.

Part-Year Residents

Rev. 12/07 7

If a married couple files a joint Federal incometax return, they must also file a joint New Jerseyincome tax return. If spouses file separateFederal returns, separate State returns must alsobe filed. However, if you are a civil unioncouple, your filing status for New Jersey willnot match your Federal filing status for the year.

• One spouse/civil union partner New Jerseyresident, other spouse/civil union partnernonresident for entire year. If during the en-tire taxable year one spouse/civil union part-ner was a resident and the other a nonresident,separate New Jersey returns may be filed (theresident files a resident return and the non-resident files a nonresident return), even if thecouple files a joint Federal return. The resi-dent computes income and exemptions as if aFederal married, filing separate return hadbeen filed. The spouses/civil union partnershave the option of filing a joint return as resi-dents, in which case their joint income (fromboth inside and outside New Jersey) would betaxed as if both were residents.

• Married/civil union couples, both nonresi-dents; only one has income from New Jerseysources. If both spouses/civil union partnerswere nonresidents of New Jersey during theentire taxable year and only one earned, re-ceived, or acquired income from New Jerseysources, the one who had income from NewJersey sources may file a separate New Jerseyreturn, even if a joint Federal return was filed.The one with income from New Jerseysources computes income and exemptions asif a Federal married, filing separate return hadbeen filed. The married/civil union couple hasthe option of filing a joint return, in whichcase, their joint income must be shown on the

nonresident return. For more information oncompleting the nonresident return, see in-structions for Form NJ-1040NR.

Remember: A nonresident return must be filedif you received any amount of income from NewJersey sources as a nonresident, and your in-come from all sources (both inside and outsideNew Jersey) for the entire year was more than$20,000 ($10,000 if filing status is single ormarried/CU partner, filing separate return).

How Residents andNonresidents Are TaxedResidents. New Jersey residents are subject totax on their income from all sources, whetherthe income is from inside or outside of NewJersey. As a part-year New Jersey resident youmust report on your resident return all the in-come you received during the period of time youwere a New Jersey resident, whether in the formof money, goods, property, benefits, or services,unless specifically excluded by law. Married/civil union couples filing jointly must report theincome of both spouses/civil union partners.

The following are some examples of incomeyou must report if earned or received while youwere a resident of New Jersey: wages, fees, orcommissions earned in New Jersey or elsewhere(including a foreign country); interest receivedon a bank account whether located in or out ofNew Jersey; gain from the sale of property bothin and out of New Jersey; lottery winnings fromany state other than New Jersey; net profits frombusiness, regardless of where the business islocated; etc.

Rev. 12/078

Bulletin GIT-6

Remember: When completing your part-yearresident return, report only the income youreceived during the time period covered by yourresident return.

Part-year residents must prorate all exemptions,deductions, and credits, as well as the pensionand other retirement income exclusions, to re-flect the period covered by their return. For ex-ample, a full-year New Jersey resident is entitledto a $1,000 personal exemption; whereas a resi-dent for six months is entitled to a personal ex-emption of only $500. See Completing aPart-Year Resident Return on page 9.

For more information on completing the residentreturn, see the instructions for Form NJ-1040.

Nonresidents. For nonresidents, New Jersey in-come tax liability is based on the percentage oftheir total income that comes from New Jersey.

The income section of the New Jersey nonresi-dent return has two columns—Column A, in-come from everywhere and Column B, incomefrom New Jersey sources. In the first column,report your income from all sources (both insideand outside New Jersey) as if you were a resi-dent, and in the second column, list only incomethat was derived from New Jersey sources.Pennsylvania residents see page 19.

In accordance with Federal legislation (Service-members Civil Relief Act, P.L. No. 108-189)nonresident servicepersons are not required toinclude their military pay in either their “incomefrom everywhere” (Column A) or “income fromNew Jersey Sources” (Column B) on the NewJersey nonresident income tax return. For moreinformation, request Tax Topic Bulletin GIT-7,Military Personnel.

Remember: When completing your part-yearnonresident return, report in each column onlythe income you received during the time periodcovered by your nonresident return.

As a nonresident, your tax is computed on yourincome from all sources as if you were a NewJersey resident, and then prorated according tothe ratio that your New Jersey income bears toyour income from both inside and outside NewJersey. In other words, your final New Jerseyincome tax liability is based on the percentageof your income that comes from New Jersey.

For more information on completing the non-resident return, see the instructions for FormNJ-1040NR.

Part-Year Residents

Rev. 12/07 9

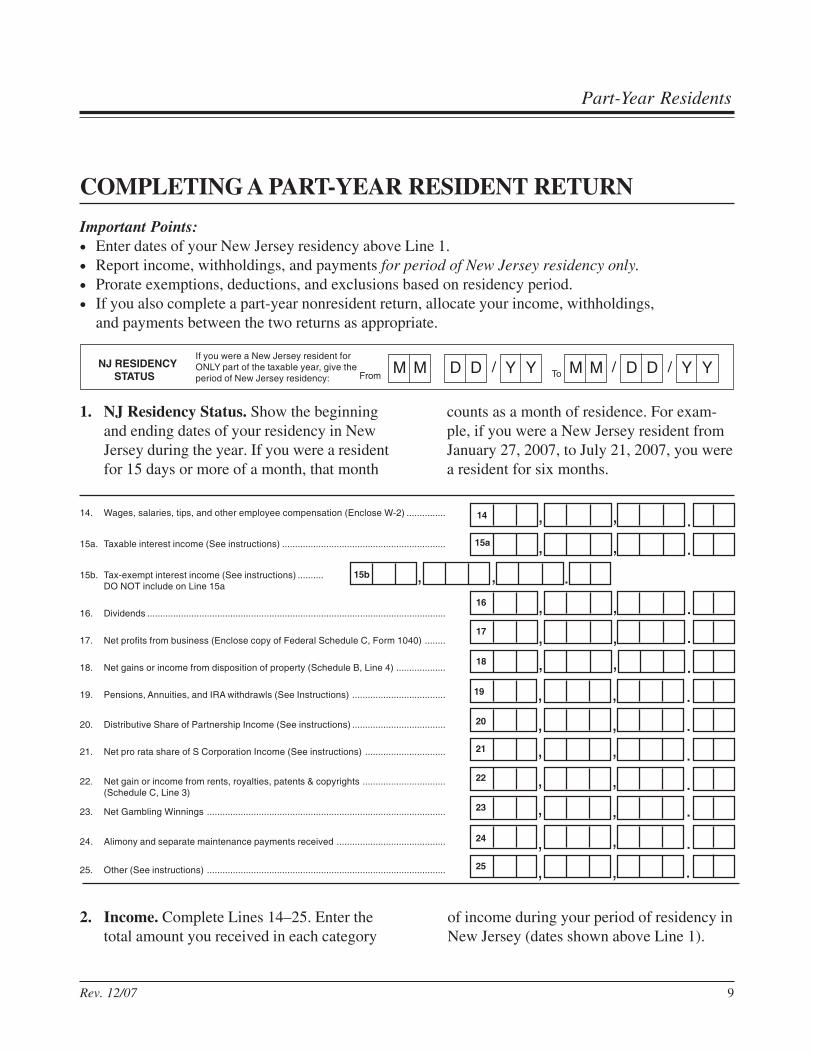

COMPLETING A PART-YEAR RESIDENT RETURN

Important Points:• Enter dates of your New Jersey residency above Line 1.• Report income, withholdings, and payments for period of New Jersey residency only.• Prorate exemptions, deductions, and exclusions based on residency period.• If you also complete a part-year nonresident return, allocate your income, withholdings,

and payments between the two returns as appropriate.

1. NJ Residency Status. Show the beginningand ending dates of your residency in NewJersey during the year. If you were a residentfor 15 days or more of a month, that month

NJ RESIDENCYSTATUS

If you were a New Jersey resident forONLY part of the taxable year, give theperiod of New Jersey residency: From ToY YD DM M Y YD DM M ///

counts as a month of residence. For exam-ple, if you were a New Jersey resident fromJanuary 27, 2007, to July 21, 2007, you werea resident for six months.

14. Wages, salaries, tips, and other employee compensation (Enclose W-2) ...............

15a. Taxable interest income (See instructions) ...............................................................

15b. Tax-exempt interest income (See instructions) ..........DO NOT include on Line 15a

16. Dividends ...................................................................................................................

17. Net profits from business (Enclose copy of Federal Schedule C, Form 1040) ........

18. Net gains or income from disposition of property (Schedule B, Line 4) ...................

19. Pensions, Annuities, and IRA withdrawls (See Instructions) ....................................

20. Distributive Share of Partnership Income (See instructions) ....................................

21. Net pro rata share of S Corporation Income (See instructions) ...............................

22. Net gain or income from rents, royalties, patents & copyrights ................................(Schedule C, Line 3)

23. Net Gambling Winnings ............................................................................................

24. Alimony and separate maintenance payments received ..........................................

25. Other (See instructions) ............................................................................................

, ,

, , .

14 , , .15a , , .

16 , , .17 .18 , , .

15b

, ,

19 , , .20 , , .21 , , .22 , , .23 , , .24 , , .25 .

2. Income. Complete Lines 14–25. Enter thetotal amount you received in each category

of income during your period of residency inNew Jersey (dates shown above Line 1).

Rev. 12/0710

Bulletin GIT-6

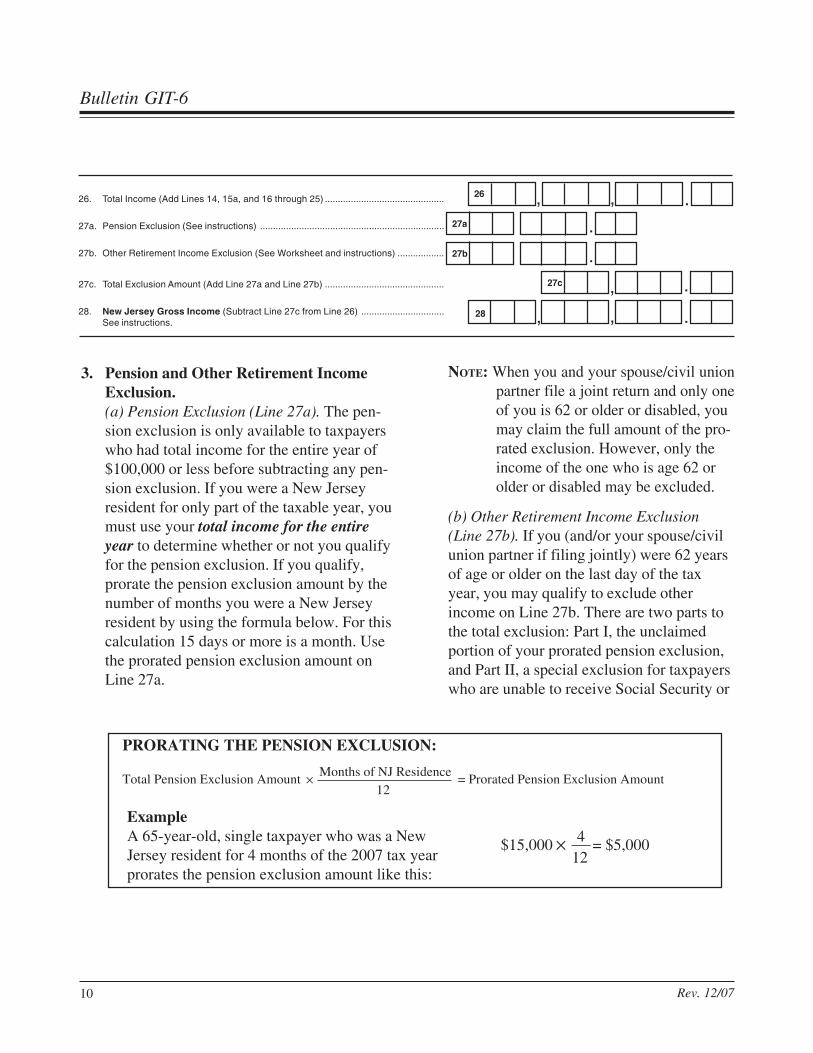

3. Pension and Other Retirement IncomeExclusion.(a) Pension Exclusion (Line 27a). The pen-sion exclusion is only available to taxpayerswho had total income for the entire year of$100,000 or less before subtracting any pen-sion exclusion. If you were a New Jerseyresident for only part of the taxable year, youmust use your total income for the entireyear to determine whether or not you qualifyfor the pension exclusion. If you qualify,prorate the pension exclusion amount by thenumber of months you were a New Jerseyresident by using the formula below. For thiscalculation 15 days or more is a month. Usethe prorated pension exclusion amount onLine 27a.

NOTE: When you and your spouse/civil unionpartner file a joint return and only oneof you is 62 or older or disabled, youmay claim the full amount of the pro-rated exclusion. However, only theincome of the one who is age 62 orolder or disabled may be excluded.

(b) Other Retirement Income Exclusion(Line 27b). If you (and/or your spouse/civilunion partner if filing jointly) were 62 yearsof age or older on the last day of the taxyear, you may qualify to exclude otherincome on Line 27b. There are two parts tothe total exclusion: Part I, the unclaimedportion of your prorated pension exclusion,and Part II, a special exclusion for taxpayerswho are unable to receive Social Security or

ExampleA 65-year-old, single taxpayer who was a NewJersey resident for 4 months of the 2007 tax yearprorates the pension exclusion amount like this:

4$15,000 12

= $5,000

PRORATING THE PENSION EXCLUSION:

Total Pension Exclusion Amount Months of NJ Residence

= Prorated Pension Exclusion Amount12

26. Total Income (Add Lines 14, 15a, and 16 through 25) ..............................................

27a. Pension Exclusion (See instructions) .......................................................................

27b. Other Retirement Income Exclusion (See Worksheet and instructions) ..................

27c. Total Exclusion Amount (Add Line 27a and Line 27b) ..............................................

28. New Jersey Gross Income (Subtract Line 27c from Line 26) ................................See instructions.

26 , , .

.27a

, , .28

, .27c

.27b

Part-Year Residents

Rev. 12/07 11

Railroad Retirement benefits. Do not com-plete Worksheet D in the NJ-1040 instruc-tion booklet to calculate the total exclusionamount you are eligible to claim. Instead,calculate your total exclusion as follows:

Part I. Total the earned income (wages, netprofits from business, partnership income,and S corporation income) you received forthe entire year. If your earned income for theentire year was $3,000 or less and you didnot use your entire prorated pension exclu-sion at Line 27a, you may be able to use theunclaimed pension exclusion at Line 27bprovided total income for the entire yearbefore subtracting any pension exclusionwas $100,000 or less.

Part II. If you are unable to receive SocialSecurity or Railroad Retirement benefits, butwould have been eligible for benefits hadyou fully participated in either program, youmay also be eligible for an additional exclu-sion, whether or not you used all of yourprorated pension exclusion on Line 27a.

NOTE: When you and your spouse/civil unionpartner file a joint return and only oneof you is 62 or older or disabled, youmay claim the full amount of the pro-rated exclusion. However, only theincome of the one who is age 62 orolder or disabled may be excluded.

More Information. For more detailedinformation on pension, annuity, and IRAwithdrawal income and the New Jerseyincome exclusions, request Tax Topic Bulle-tins GIT-1, Pensions and Annuities, andGIT-2, IRA Withdrawals. For information onRoth IRAs, request Technical BulletinTB-44, Roth IRAs. For information on calcu-lating your partnership and S corporation in-come, request Tax Topic Bulletin GIT-9P,Income From Partnerships, and GIT-9S, In-come From S Corporations.

Rev. 12/0712

Bulletin GIT-6

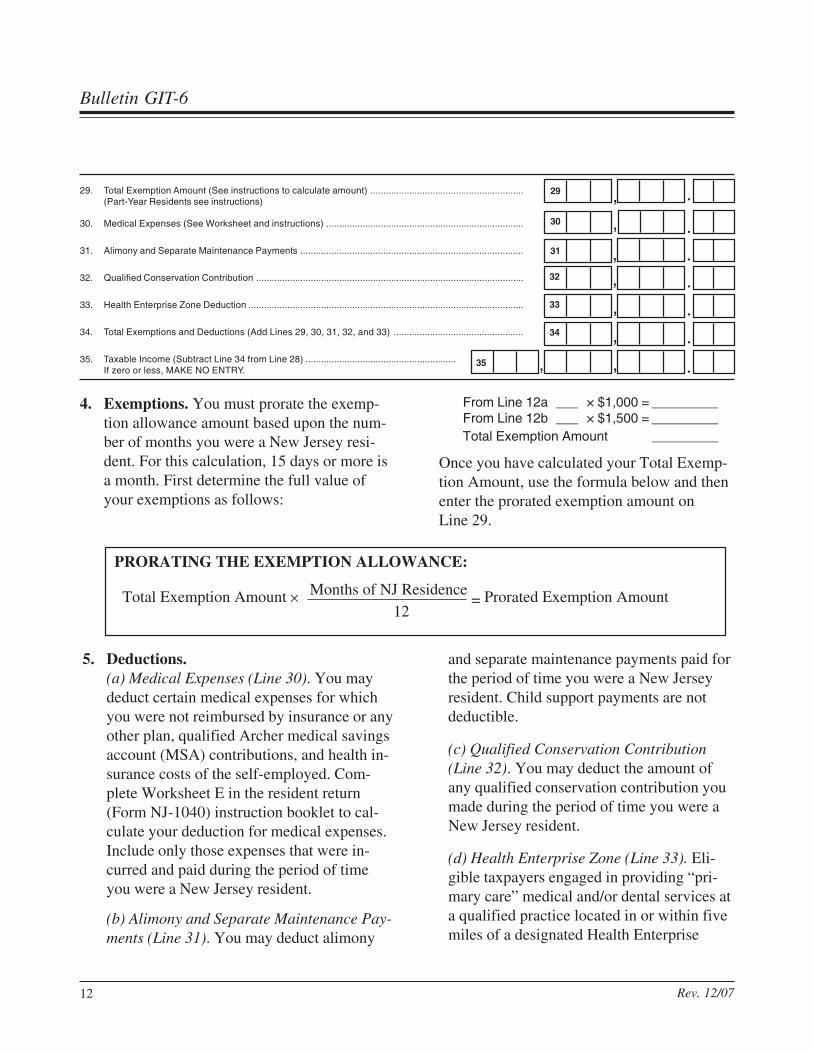

29. Total Exemption Amount (See instructions to calculate amount) ...........................................................(Part-Year Residents see instructions)

30. Medical Expenses (See Worksheet and instructions) ............................................................................

31. Alimony and Separate Maintenance Payments ......................................................................................

32. Qualified Conservation Contribution .......................................................................................................

33. Health Enterprise Zone Deduction ..........................................................................................................

34. Total Exemptions and Deductions (Add Lines 29, 30, 31, 32, and 33) ..................................................

35. Taxable Income (Subtract Line 34 from Line 28) ..........................................................If zero or less, MAKE NO ENTRY.

4. Exemptions. You must prorate the exemp-tion allowance amount based upon the num-ber of months you were a New Jersey resi-dent. For this calculation, 15 days or more isa month. First determine the full value ofyour exemptions as follows:

From Line 12a ___ × $1,000 = _________From Line 12b ___ × $1,500 = _________Total Exemption Amount _________

Once you have calculated your Total Exemp-tion Amount, use the formula below and thenenter the prorated exemption amount onLine 29.

5. Deductions.(a) Medical Expenses (Line 30). You maydeduct certain medical expenses for whichyou were not reimbursed by insurance or anyother plan, qualified Archer medical savingsaccount (MSA) contributions, and health in-surance costs of the self-employed. Com-plete Worksheet E in the resident return(Form NJ-1040) instruction booklet to cal-culate your deduction for medical expenses.Include only those expenses that were in-curred and paid during the period of timeyou were a New Jersey resident.

(b) Alimony and Separate Maintenance Pay-ments (Line 31). You may deduct alimony

and separate maintenance payments paid forthe period of time you were a New Jerseyresident. Child support payments are notdeductible.

(c) Qualified Conservation Contribution(Line 32). You may deduct the amount ofany qualified conservation contribution youmade during the period of time you were aNew Jersey resident.

(d) Health Enterprise Zone (Line 33). Eli-gible taxpayers engaged in providing “pri-mary care” medical and/or dental services ata qualified practice located in or within fivemiles of a designated Health Enterprise

PRORATING THE EXEMPTION ALLOWANCE:

Total Exemption Amount Months of NJ Residence = Prorated Exemption Amount12

,

, .29

, .30

31 .,32 .33 .34 .

35 , , .

,

,

Part-Year Residents

Rev. 12/07 13

Zone (HEZ) may qualify for a deduction.For information on eligibility requirementsand how to calculate the HEZ deduction, seeTechnical Bulletin TB-56, Health EnterpriseZones.

NOTE: New Jersey does not allow deduc-tions for adjustments taken on theFederal return such as employeebusiness expenses or IRA and KeoghPlan contributions.

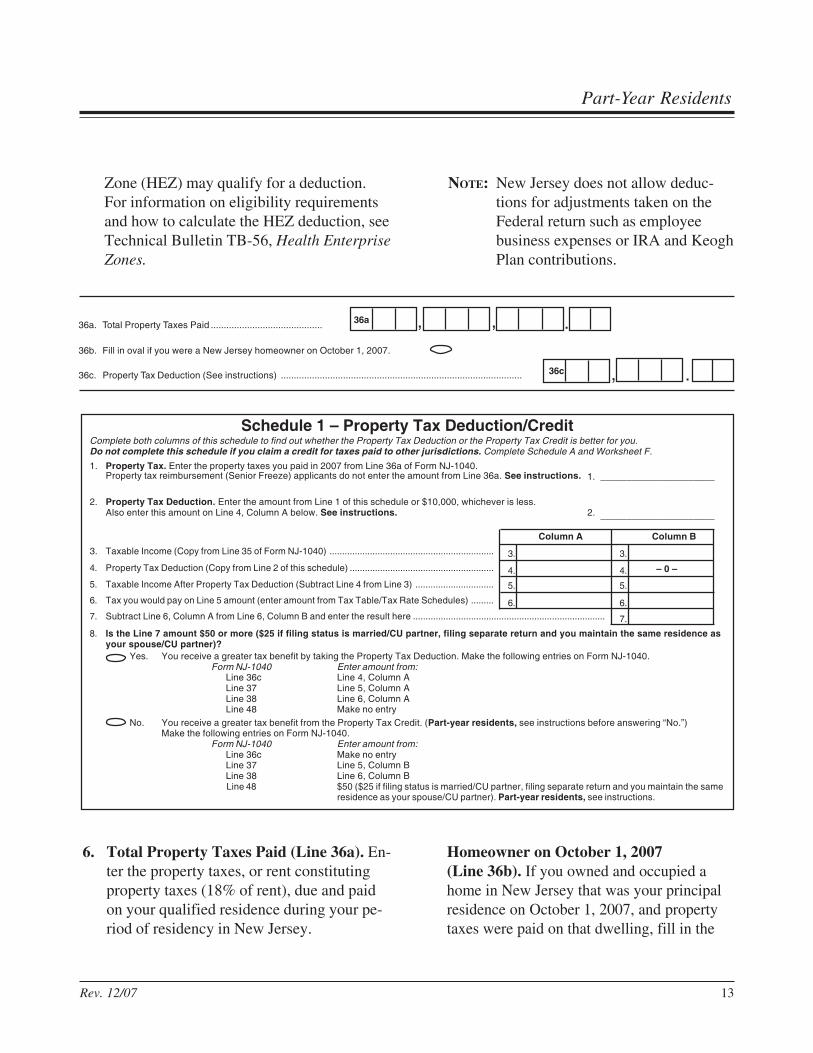

6. Total Property Taxes Paid (Line 36a). En-ter the property taxes, or rent constitutingproperty taxes (18% of rent), due and paidon your qualified residence during your pe-riod of residency in New Jersey.

Homeowner on October 1, 2007(Line 36b). If you owned and occupied ahome in New Jersey that was your principalresidence on October 1, 2007, and propertytaxes were paid on that dwelling, fill in the

36a. Total Property Taxes Paid ...........................................

36b. Fill in oval if you were a New Jersey homeowner on October 1, 2007.

36c. Property Tax Deduction (See instructions) ............................................................................................. 36c .,

, , .36a

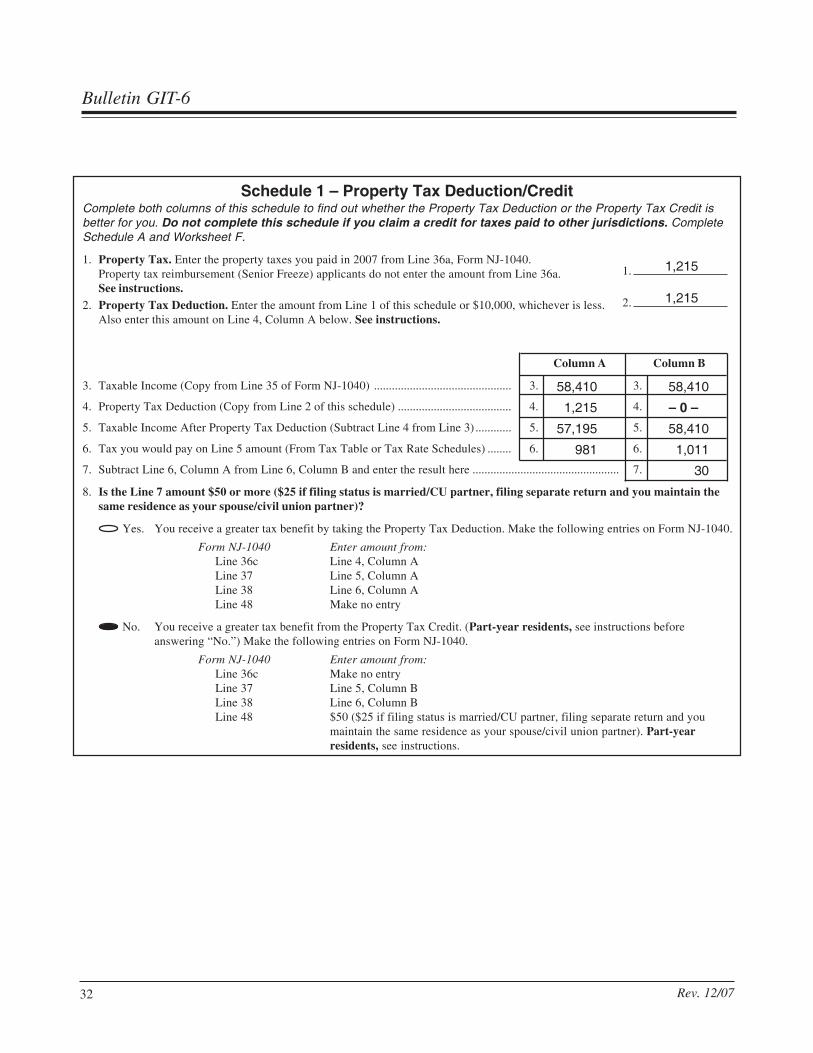

Schedule 1 – Property Tax Deduction/CreditComplete both columns of this schedule to find out whether the Property Tax Deduction or the Property Tax Credit is better for you.Do not complete this schedule if you claim a credit for taxes paid to other jurisdictions. Complete Schedule A and Worksheet F.

1. Property Tax. Enter the property taxes you paid in 2007 from Line 36a of Form NJ-1040.Property tax reimbursement (Senior Freeze) applicants do not enter the amount from Line 36a. See instructions. 1. ______________________

2. Property Tax Deduction. Enter the amount from Line 1 of this schedule or $10,000, whichever is less.Also enter this amount on Line 4, Column A below. See instructions. 2. ______________________

Column A Column B

3. Taxable Income (Copy from Line 35 of Form NJ-1040) ................................................................. 3. 3.

4. Property Tax Deduction (Copy from Line 2 of this schedule) ......................................................... 4. 4. – 0 –

5. Taxable Income After Property Tax Deduction (Subtract Line 4 from Line 3) ............................... 5. 5.

6. Tax you would pay on Line 5 amount (enter amount from Tax Table/Tax Rate Schedules) ......... 6. 6.7. Subtract Line 6, Column A from Line 6, Column B and enter the result here ............................................................................ 7.

8. Is the Line 7 amount $50 or more ($25 if filing status is married/CU partner, filing separate return and you maintain the same residence asyour spouse/CU partner)?

Yes. You receive a greater tax benefit by taking the Property Tax Deduction. Make the following entries on Form NJ-1040.Form NJ-1040 Enter amount from:

Line 36c Line 4, Column ALine 37 Line 5, Column ALine 38 Line 6, Column ALine 48 Make no entry

No. You receive a greater tax benefit from the Property Tax Credit. (Part-year residents, see instructions before answering “No.”)Make the following entries on Form NJ-1040.

Form NJ-1040 Enter amount from:Line 36c Make no entryLine 37 Line 5, Column BLine 38 Line 6, Column BLine 48 $50 ($25 if filing status is married/CU partner, filing separate return and you maintain the same

residence as your spouse/CU partner). Part-year residents, see instructions.

Rev. 12/0714

Bulletin GIT-6

oval on this line. Do not fill in the oval if, onOctober 1, 2007, you were a tenant or youwere not a homeowner.

Property Tax Deduction/Credit (Line 36c/Line 48). A part-year resident may be eli-gible to claim a deduction or credit for prop-erty taxes, or rent constituting property taxes(18% of rent), due and paid during their pe-riod of residency. If you do not claim creditfor taxes paid to another jurisdiction, com-plete Schedule 1 to determine the amount ofyour property tax deduction and whether youshould elect to take the property tax deduc-tion on Line 36c, Form NJ-1040 or the prop-erty tax credit on Line 48. If you claim creditfor taxes paid to another jurisdiction, com-plete Schedule A and Worksheet F to makethis determination. Enter on Line 1 ofSchedule 1 the amount of property taxes or18% of rent due and paid during your periodof residency from Line 36a, Form NJ-1040.Complete the balance of the schedule ac-cording to the instructions. The minimumbenefit for a full-year resident is $50. You

must prorate this minimum benefit based onthe number of months you were a New Jer-sey resident. For this calculation, 15 days ormore is a month. You must also prorate ifyour filing status is married/CU partner, fil-ing separate return. After prorating the $50minimum benefit, answer the question atLine 8 of Schedule 1 based on this proratedamount rather than the $50 amount. You willthen be able to determine whether you willreceive a greater tax benefit by taking theproperty tax deduction or claiming the pro-rated credit.

More Information. For information onclaiming credit for taxes paid to another ju-risdiction, request Tax Topic BulletinGIT-3W, Credit for Taxes Paid to OtherJurisdictions (Wage Income), and GIT-3B,Credit for Taxes Paid to Other Jurisdictions(Business/Nonwage Income). For more de-tailed information on the property tax deduc-tion/credit, see the instructions contained inthe resident return (Form NJ-1040) instruc-tion booklet.

41. Balance of Tax (From Line 40, Page 2) ...................................................................................

42. Sheltered Workshop Tax Credit ...............................................................................................

43. Balance of Tax after Credit (Subtract Line 42 from Line 41) ...................................................

, , .41

, , .42

, , .43

7. Sheltered Workshop Tax Credit. Enter theamount of your Sheltered Workshop TaxCredit from Part IV, line 12 of Form

GIT-317. Allocate the total amount of thecredit between your part-year resident andpart-year nonresident returns if appropriate.

Part-Year Residents

Rev. 12/07 15

8. Tax Withheld/Property Tax Credit/Estimated Payments.(a) Line 47. Enter the amount of New Jerseyincome tax withheld from wages you earnedor other payments you received while youwere a New Jersey resident. If your em-ployer combined wages you earned as a resi-dent and wages you earned as a nonresidenton the same W-2, and you earned some ofthose wages from New Jersey while a non-resident, include here only tax withheld dur-ing the period you were a resident. Allocatethe New Jersey income tax withheld be-tween your part-year resident and part-yearnonresident returns. If you did not earn anyof the wages on the W-2 while a nonresi-dent, report the total New Jersey tax with-held on the W-2.

(b) Line 48. If you are claiming a propertytax credit rather than a property tax deduc-tion, enter the amount of your proratedcredit.

(c) Line 49. Enter the amount of estimatedpayments to New Jersey for the period oftime you were a resident. If you made esti-mated payments both as a resident and as anonresident, enter on your part-year residentreturn the payment(s) made to meet the taxliability for your period of New Jersey resi-dency. Enter on the part-year nonresident re-turn the payment(s) made to satisfy your taxliability during the part of the year you werea nonresident. Also enter amounts, if any,paid to qualify for an extension of time tofile.

47. Total New Jersey Income Tax Withheld (Enclose Forms W-2 and 1099) .........................

48. Property Tax Credit (See instructions) ..................................................................................

49. New Jersey Estimated Tax Payments/Credit from 2006 tax return ......................................

50. New Jersey Earned Income Tax Credit (See instructions) ...................................................

51. EXCESS New Jersey UI/WF/SWF Withheld (See instructions) (Enclose Form NJ-2450) ......

52. EXCESS New Jersey Disability Insurance Withheld (See instructions)(Enclose Form NJ-2450) .......................................................................................................

53. Total Payments/Credits (Add Lines 47 through 52) ............................................................ , ,53 .

, .51

, .50

, ,49 .

.48

, .52

47 , , .

Fill in oval if you had the IRS figure your Federal Earned Income CreditFill in oval if you are a CU couple claiming the NJ Earned Income Tax Credit

Fill inonly one

Rev. 12/0716

Bulletin GIT-6

9. New Jersey Earned Income Tax Credit(Line 50). If you are eligible and file for aFederal earned income credit, you can alsoreceive a New Jersey credit in the amountequal to 20% of your Federal benefit. Com-plete the Earned Income Tax Credit Sched-ule to calculate the amount for Line 50,Form NJ-1040. However, you must prorateyour credit based on the number of monthsyou were a New Jersey resident. For this cal-culation 15 days or more is a month.

You must file Form NJ-1040 to receive aNew Jersey earned income tax credit, even ifyou are not required to file a return becauseyour gross income is below the minimumincome threshold (see Part-Year Residentson page 4).

NOTE: If your filing status is married/CUpartner, filing separate return, youmay not claim a New Jersey earnedincome tax credit.

If you asked the Internal Revenue Service tocalculate your Federal earned income credit,be sure to fill in the first oval below Line 50,

Form NJ-1040. (Civil union couples shouldnot fill in this oval even if one or both of youare eligible for a Federal credit and asked theIRS to calculate the amount. See the instruc-tions for Civil Union Couples below.) TheIRS will provide information to the Divisionof Taxation in October 2008. Please allow atleast 4–6 weeks for the Division to processthe information and issue a check for yourNew Jersey earned income tax credit.

Civil Union Couples. If you file a joint NewJersey return and wish to determine if youare eligible for the NJEITC, prepare a Fed-eral return as if you were married, filingjointly and calculate the amount of the Fed-eral earned income credit, if any, you wouldhave been eligible to receive on a joint Fed-eral return. Once you have determined theamount of the Federal credit you would havereceived as joint filers, you must use thatamount on the Earned Income Tax CreditWorksheet to calculate your New Jerseycredit. Be sure to fill in only the second ovalbelow Line 50 indicating you are a civilunion couple.

PRORATING THE NEW JERSEY EARNED INCOME TAX CREDIT:

Total New Jersey EITC Amount Months of NJ Residence

= Prorated New Jersey EITC Amount12

Earned Income Tax Credit Schedule(Keep for your records)

1. Enter the amount of your Federal earned income credit from your 2007 Federal Form 1040 or Form 1040A ............................. 1. _____________Fill in the first oval below Line 50 if you asked the IRSto calculate your Federal earned income credit.Civil union couples, see instructions.

2. Enter 20% of amount on line 1 here and on Line 50, Form NJ-1040. Part-year residents, see instructions ........................... 2. _____________

Part-Year Residents

Rev. 12/07 17

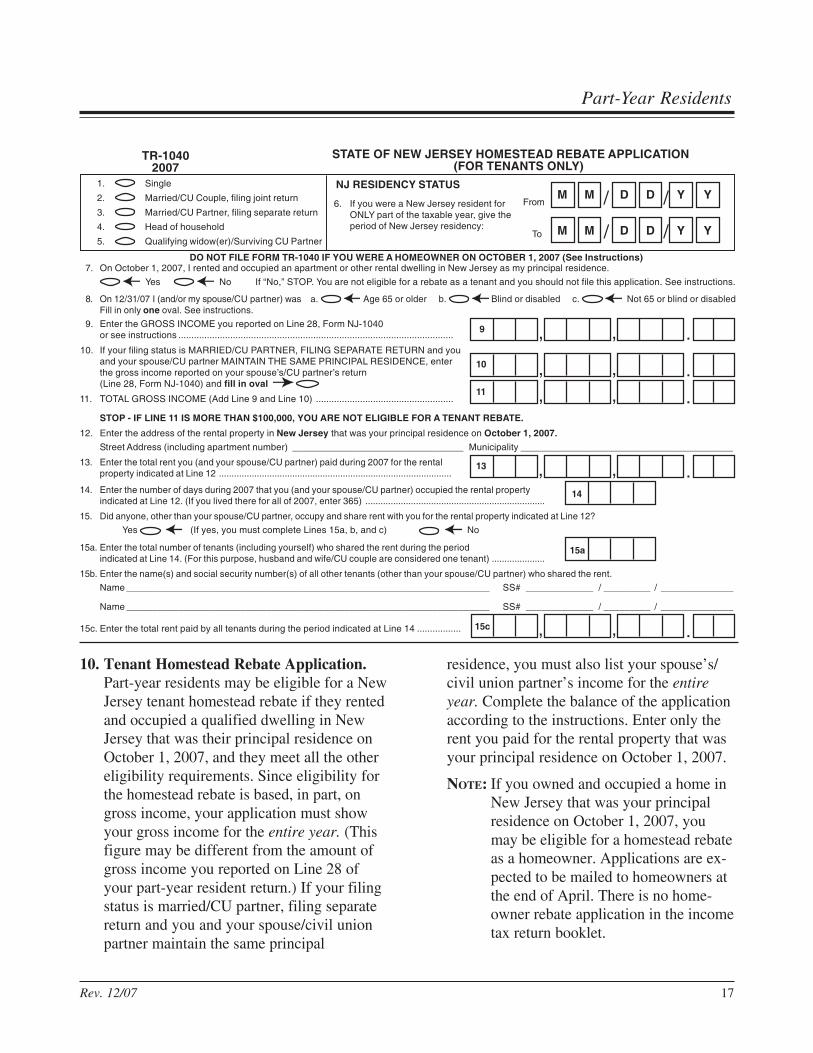

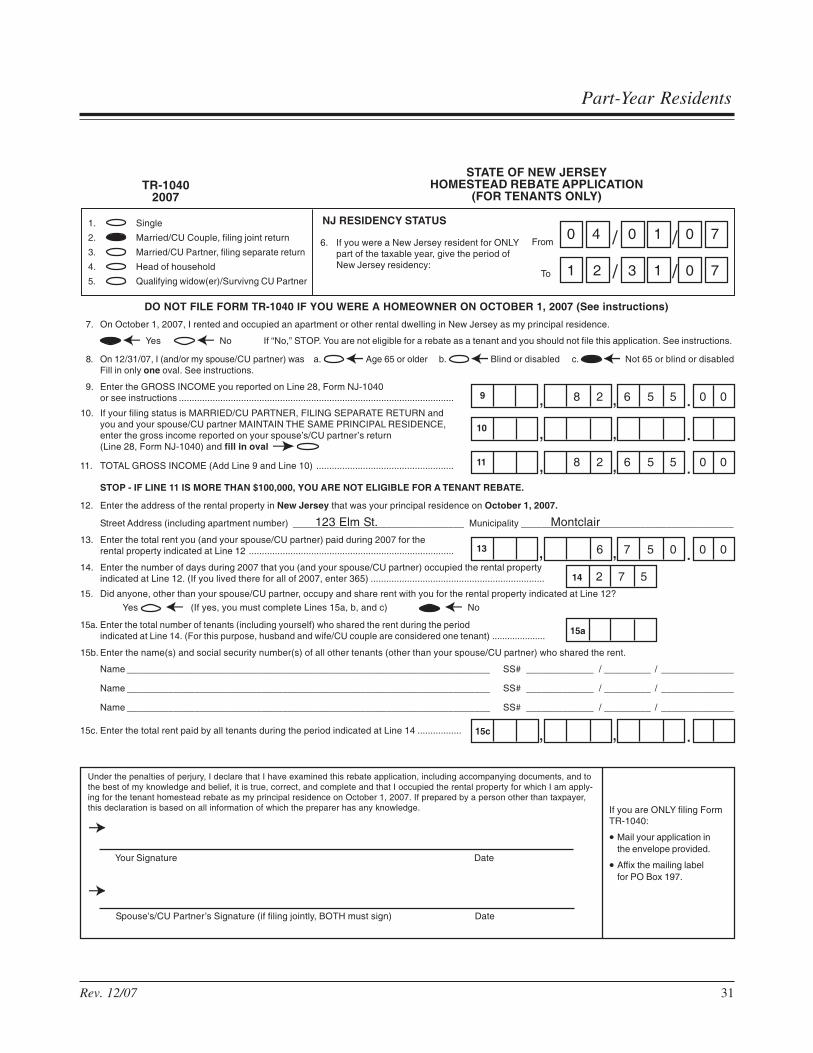

10. Tenant Homestead Rebate Application.Part-year residents may be eligible for a NewJersey tenant homestead rebate if they rentedand occupied a qualified dwelling in NewJersey that was their principal residence onOctober 1, 2007, and they meet all the othereligibility requirements. Since eligibility forthe homestead rebate is based, in part, ongross income, your application must showyour gross income for the entire year. (Thisfigure may be different from the amount ofgross income you reported on Line 28 ofyour part-year resident return.) If your filingstatus is married/CU partner, filing separatereturn and you and your spouse/civil unionpartner maintain the same principal

residence, you must also list your spouse’s/civil union partner’s income for the entireyear. Complete the balance of the applicationaccording to the instructions. Enter only therent you paid for the rental property that wasyour principal residence on October 1, 2007.

NOTE: If you owned and occupied a home inNew Jersey that was your principalresidence on October 1, 2007, youmay be eligible for a homestead rebateas a homeowner. Applications are ex-pected to be mailed to homeowners atthe end of April. There is no home-owner rebate application in the incometax return booklet.

TR-10402007

STATE OF NEW JERSEY HOMESTEAD REBATE APPLICATION(FOR TENANTS ONLY)

1. Single

2. Married/CU Couple, filing joint return

3. Married/CU Partner, filing separate return

4. Head of household

5. Qualifying widow(er)/Surviving CU Partner

6. If you were a New Jersey resident forONLY part of the taxable year, give theperiod of New Jersey residency:

NJ RESIDENCY STATUS

To

From //

/ /

M M

MM

D D

D D

Y Y

Y Y

7. On October 1, 2007, I rented and occupied an apartment or other rental dwelling in New Jersey as my principal residence.

Yes No If “No,” STOP. You are not eligible for a rebate as a tenant and you should not file this application. See instructions.

8. On 12/31/07 I (and/or my spouse/CU partner) was a. Age 65 or older b. Blind or disabled c. Not 65 or blind or disabledFill in only one oval. See instructions.

9. Enter the GROSS INCOME you reported on Line 28, Form NJ-1040or see instructions ..........................................................................................................

10. If your filing status is MARRIED/CU PARTNER, FILING SEPARATE RETURN and youand your spouse/CU partner MAINTAIN THE SAME PRINCIPAL RESIDENCE, enterthe gross income reported on your spouse’s/CU partner’s return(Line 28, Form NJ-1040) and fill in oval

11. TOTAL GROSS INCOME (Add Line 9 and Line 10) .....................................................

STOP - IF LINE 11 IS MORE THAN $100,000, YOU ARE NOT ELIGIBLE FOR A TENANT REBATE.

12. Enter the address of the rental property in New Jersey that was your principal residence on October 1, 2007.

Street Address (including apartment number) _________________________________ Municipality _________________________________________

13. Enter the total rent you (and your spouse/CU partner) paid during 2007 for the rentalproperty indicated at Line 12 ............................................................................................

14. Enter the number of days during 2007 that you (and your spouse/CU partner) occupied the rental propertyindicated at Line 12. (If you lived there for all of 2007, enter 365) .......................................................................

15. Did anyone, other than your spouse/CU partner, occupy and share rent with you for the rental property indicated at Line 12?

Yes (If yes, you must complete Lines 15a, b, and c) No

15a. Enter the total number of tenants (including yourself) who shared the rent during the periodindicated at Line 14. (For this purpose, husband and wife/CU couple are considered one tenant) .....................

15b. Enter the name(s) and social security number(s) of all other tenants (other than your spouse/CU partner) who shared the rent.

Name ______________________________________________________________________ SS# _____________ / _________ / ______________

Name ______________________________________________________________________ SS# _____________ / _________ / ______________

15c. Enter the total rent paid by all tenants during the period indicated at Line 14 .................

DO NOT FILE FORM TR-1040 IF YOU WERE A HOMEOWNER ON OCTOBER 1, 2007 (See Instructions)

, , .9

.11 , ,, , .10

.13 , ,14

15a

.15c , ,

Rev. 12/0718

Bulletin GIT-6

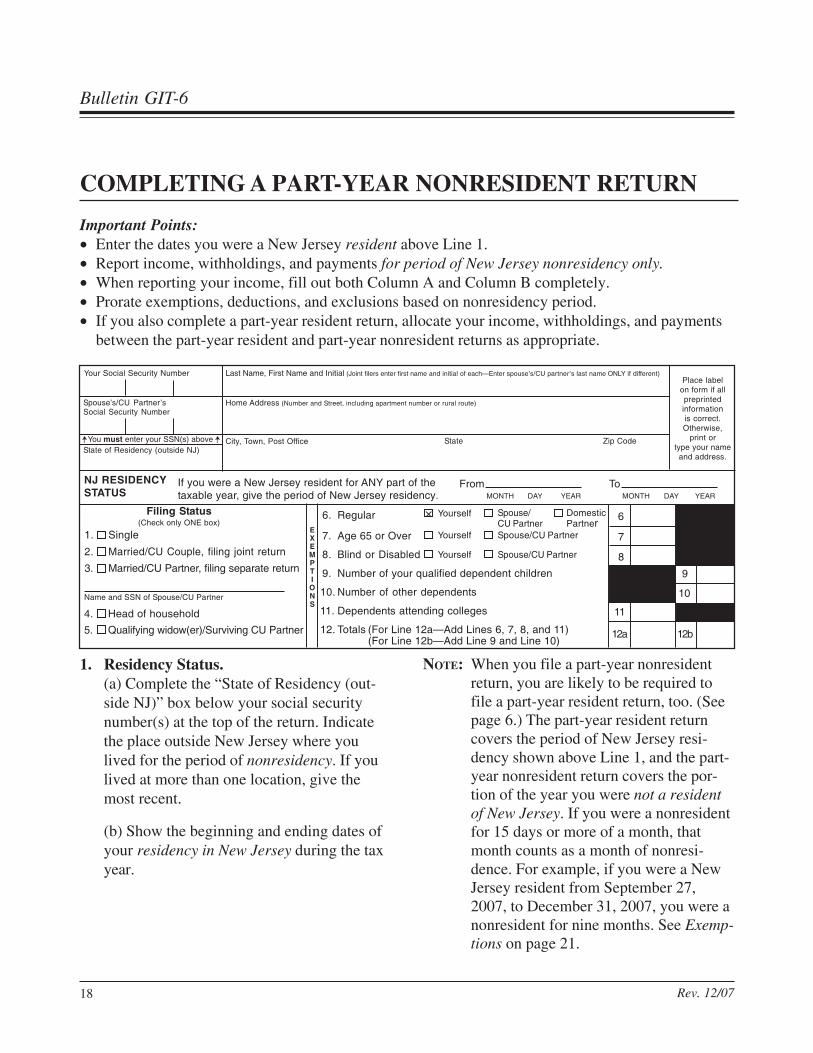

COMPLETING A PART-YEAR NONRESIDENT RETURN

Important Points:• Enter the dates you were a New Jersey resident above Line 1.• Report income, withholdings, and payments for period of New Jersey nonresidency only.• When reporting your income, fill out both Column A and Column B completely.• Prorate exemptions, deductions, and exclusions based on nonresidency period.• If you also complete a part-year resident return, allocate your income, withholdings, and payments

between the part-year resident and part-year nonresident returns as appropriate.

1. Residency Status.(a) Complete the “State of Residency (out-side NJ)” box below your social securitynumber(s) at the top of the return. Indicatethe place outside New Jersey where youlived for the period of nonresidency. If youlived at more than one location, give themost recent.

(b) Show the beginning and ending dates ofyour residency in New Jersey during the taxyear.

NOTE: When you file a part-year nonresidentreturn, you are likely to be required tofile a part-year resident return, too. (Seepage 6.) The part-year resident returncovers the period of New Jersey resi-dency shown above Line 1, and the part-year nonresident return covers the por-tion of the year you were not a residentof New Jersey. If you were a nonresidentfor 15 days or more of a month, thatmonth counts as a month of nonresi-dence. For example, if you were a NewJersey resident from September 27,2007, to December 31, 2007, you were anonresident for nine months. See Exemp-tions on page 21.

6. Regular

7. Age 65 or Over

8. Blind or Disabled

9. Number of your qualified dependent children

10. Number of other dependents

11. Dependents attending colleges

12. Totals (For Line 12a—Add Lines 6, 7, 8, and 11)(For Line 12b—Add Line 9 and Line 10)

Place labelon form if allpreprintedinformationis correct.Otherwise,

print ortype your name

and address.

Your Social Security Number

Spouse’s/CU Partner’sSocial Security Number

Last Name, First Name and Initial (Joint filers enter first name and initial of each—Enter spouse’s/CU partner’s last name ONLY if different)

Home Address (Number and Street, including apartment number or rural route)

City, Town, Post Office State Zip CodeYou must enter your SSN(s) aboveState of Residency (outside NJ)

NJ RESIDENCYSTATUS

If you were a New Jersey resident for ANY part of thetaxable year, give the period of New Jersey residency.

From ToMONTH DAY YEAR MONTH DAY YEAR

Filing Status(Check only ONE box)

1. Single

2. Married/CU Couple, filing joint return

3. Married/CU Partner, filing separate return

EXEMPTIONS

6

7

8

9

10

114. Head of household

5. Qualifying widow(er)/Surviving CU Partner

Name and SSN of Spouse/CU Partner

12a 12b

Yourself

Yourself

Yourself

Spouse/CU PartnerSpouse/CU Partner

Spouse/CU Partner

DomesticPartner

×

Part-Year Residents

Rev. 12/07 19

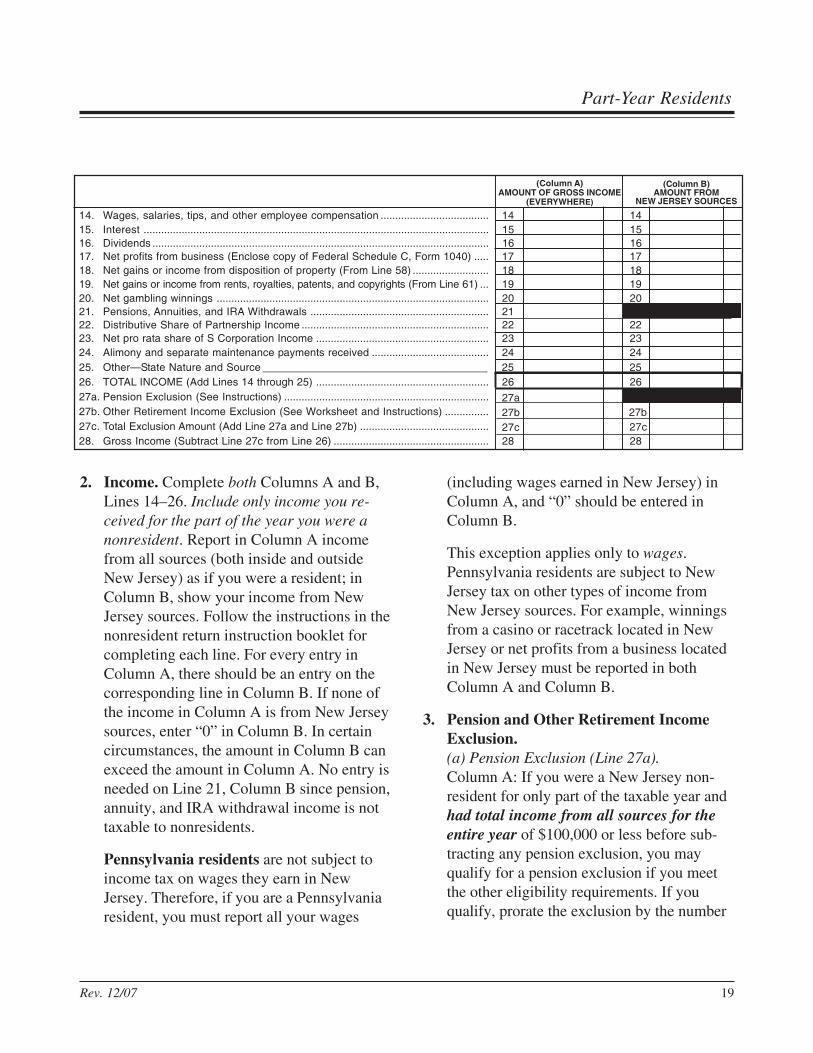

2. Income. Complete both Columns A and B,Lines 14–26. Include only income you re-ceived for the part of the year you were anonresident. Report in Column A incomefrom all sources (both inside and outsideNew Jersey) as if you were a resident; inColumn B, show your income from NewJersey sources. Follow the instructions in thenonresident return instruction booklet forcompleting each line. For every entry inColumn A, there should be an entry on thecorresponding line in Column B. If none ofthe income in Column A is from New Jerseysources, enter “0” in Column B. In certaincircumstances, the amount in Column B canexceed the amount in Column A. No entry isneeded on Line 21, Column B since pension,annuity, and IRA withdrawal income is nottaxable to nonresidents.

Pennsylvania residents are not subject toincome tax on wages they earn in NewJersey. Therefore, if you are a Pennsylvaniaresident, you must report all your wages

(including wages earned in New Jersey) inColumn A, and “0” should be entered inColumn B.

This exception applies only to wages.Pennsylvania residents are subject to NewJersey tax on other types of income fromNew Jersey sources. For example, winningsfrom a casino or racetrack located in NewJersey or net profits from a business locatedin New Jersey must be reported in bothColumn A and Column B.

3. Pension and Other Retirement IncomeExclusion.(a) Pension Exclusion (Line 27a).Column A: If you were a New Jersey non-resident for only part of the taxable year andhad total income from all sources for theentire year of $100,000 or less before sub-tracting any pension exclusion, you mayqualify for a pension exclusion if you meetthe other eligibility requirements. If youqualify, prorate the exclusion by the number

14. Wages, salaries, tips, and other employee compensation ..................................... 14 1415. Interest ...................................................................................................................... 15 1516. Dividends ................................................................................................................... 16 1617. Net profits from business (Enclose copy of Federal Schedule C, Form 1040) ..... 17 1718. Net gains or income from disposition of property (From Line 58) .......................... 18 1819. Net gains or income from rents, royalties, patents, and copyrights (From Line 61) ... 19 1920. Net gambling winnings ............................................................................................. 20 2021. Pensions, Annuities, and IRA Withdrawals ............................................................. 2122. Distributive Share of Partnership Income ................................................................ 22 2223. Net pro rata share of S Corporation Income ........................................................... 23 2324. Alimony and separate maintenance payments received ........................................ 24 2425. Other—State Nature and Source ______________________________________ 25 2526. TOTAL INCOME (Add Lines 14 through 25) ........................................................... 26 2627a. Pension Exclusion (See Instructions) ...................................................................... 27a 27a27b. Other Retirement Income Exclusion (See Worksheet and Instructions) ............... 27b 27b27c. Total Exclusion Amount (Add Line 27a and Line 27b) ............................................ 27c 27c28. Gross Income (Subtract Line 27c from Line 26) ..................................................... 28 28

(Column A)AMOUNT OF GROSS INCOME

(EVERYWHERE)

(Column B)AMOUNT FROM

NEW JERSEY SOURCES

Rev. 12/0720

Bulletin GIT-6

of months you were a New Jersey nonresi-dent. For this calculation 15 days or more isa month. See page 10 for a description ofhow to prorate the pension exclusion amount.

NOTE: When you and your spouse/civil unionpartner file a joint return and only oneof you is 62 or older or disabled, youmay claim the full amount of the pro-rated exclusion. However, only theincome of the one who is age 62 orolder or disabled may be excluded.

Column B: No entry is necessary inColumn B since pension, annuity, and IRAwithdrawal income is not taxable tononresidents.

(b) Other Retirement Income Exclusion(Line 27b, Columns A and B). If you (and/oryour spouse/civil union partner if filingjointly) were 62 years of age or older on thelast day of the tax year, you may qualify toexclude other income on Line 27b. There aretwo parts to the total exclusion: Part I, theunclaimed portion of your prorated pensionexclusion, and Part II, a special exclusion fortaxpayers who are unable to receive SocialSecurity or Railroad Retirement benefits. Donot complete Worksheet D in the NJ-1040NRinstruction booklet to calculate the total ex-clusion amount you are eligible to claim.Instead, calculate your total exclusion asfollows:

Part I. Total the earned income (wages, netprofits from business, partnership income,and S corporation income) you receivedfrom all sources for the entire year. If yourearned income for the entire year was $3,000or less and you did not use your entire pro-rated pension exclusion at Line 27a, youmay be able to use the unclaimed pensionexclusion at Line 27b provided total incomefrom all sources for the entire year beforesubtracting any pension exclusion was$100,000 or less.

Part II. If you are unable to receive SocialSecurity or Railroad Retirement benefits, butwould have been eligible for benefits hadyou fully participated in either program, youmay also be eligible for an additional exclu-sion, whether or not you used all of yourprorated pension exclusion at Line 27a.

NOTE: When you and your spouse/civil unionpartner file a joint return and only oneof you is 62 or older or disabled, youmay claim the full amount of the pro-rated exclusion. However, only theincome of the one who is age 62 orolder or disabled may be excluded.

More Information. For information on cal-culating your partnership and S corporationincome, request Tax Topic Bulletin GIT-9P,Income From Partnerships, and GIT-9S, In-come From S Corporations. For more infor-mation on pension, annuity, and IRAwithdrawal income and the New Jersey in-come exclusions, request Tax Topic Bulle-tins GIT-1, Pensions and Annuities, andGIT-2, IRA Withdrawals.

Part-Year Residents

Rev. 12/07 21

5. Deductions.(a) Medical Expenses (Line 31). You may de-duct certain medical expenses for which youwere not reimbursed by insurance or anyother plan, qualified Archer medical savingsaccount (MSA) contributions, and healthinsurance costs of the self-employed. Com-plete Worksheet E in the nonresident returninstruction booklet (Form NJ-1040NR) tocalculate your deduction for medical ex-penses. Include only those expenses that wereincurred and paid during the period of timeyou were a New Jersey nonresident.

(b) Alimony and Separate MaintenancePayments (Line 32). You may deduct ali-mony and separate maintenance paymentspaid for the period of time you were a NewJersey nonresident. Child support paymentsare not deductible.

4. Exemptions. You must prorate the exemp-tion allowance amount based upon thenumber of months you were a New Jerseynonresident. For this calculation 15 days ormore is a month. First determine the fullvalue of your exemptions as follows:

From Line 12a ____ × $1,000 = _________

From Line 12b ____ × $1,500 = _________

Total Exemption Amount _______________

Once you have calculated your Total Ex-emption Amount, use the formula belowand then enter the prorated exemptionamount on Line 30.

(c) Qualified Conservation Contribution(Line 33). You may deduct the amount ofany qualified conservation contribution youmade during the period of time you were aNew Jersey nonresident.

(d) Health Enterprise Zone (Line 34). Eli-gible taxpayers engaged in providing “pri-mary care” medical and/or dental services ata qualified practice located in or within fivemiles of a designated Health Enterprise Zone(HEZ) may qualify for a deduction. For infor-mation on eligibility requirements and how tocalculate the HEZ deduction, see TechnicalBulletin TB-56, Health Enterprise Zones.

NOTE: New Jersey does not allow deduc-tions for adjustments taken on theFederal return such as employeebusiness expenses or IRA and KeoghPlan contributions.

30. Total Exemption Amount (See instructions) .................................................. 30

31. Medical Expenses (See Worksheet and Instructions) .................................. 31

32. Alimony and separate maintenance payments ............................................. 32

33. Qualified Conservation Contribution .............................................................. 33

34. Health Enterprise Zone Deduction ................................................................. 34

35. Total Exemptions and Deductions (Add Lines 30, 31, 32, 33, and 34) ........ 35

36. TAXABLE INCOME (Subtract Line 35 from Line 29, Column A) ................. 36

PRORATING THE EXEMPTION ALLOWANCE:

Total Exemption Amount Months of NJ Nonresidence = Prorated Exemption Amount12

Rev. 12/0722

Bulletin GIT-6

39. NEW JERSEY TAX(Multiply amount from Line 37 x % on Line 38) .................. 39

40. Sheltered Workshop Tax Credit ..................................................................... 40

41. Balance of Tax after Credit (Subtract Line 40 from Line 39) ........................ 41

6. Sheltered Workshop Tax Credit. Enter theamount of your Sheltered Workshop TaxCredit from Part IV, line 12 of Form

GIT-317. Allocate the total amount of thecredit between your part-year resident andpart-year nonresident returns if appropriate.

7. Tax Withheld/Estimated Payments.(a) Line 44. Enter the amount of New Jerseyincome tax withheld from wages you earnedor other payments you received while youwere a New Jersey nonresident. If your em-ployer combined wages you earned as a resi-dent and wages you earned as a nonresidenton the same W-2, and you earned some ofthose wages from New Jersey while a non-resident, include here only tax withheld dur-ing the period you were a nonresident.Allocate the New Jersey income tax with-held between your part-year resident andpart-year nonresident returns if you earnedwages from New Jersey as a resident and asa nonresident.

44. Total New Jersey Income Tax Withheld (Enclose Forms W-2 and 1099) ..... 44

45. New Jersey Estimated Tax Payments/Credit from 2006 tax return ............... 4546. Tax paid on your behalf by Partnership(s) ...................................................... 4647. EXCESS NJ UI/WF/SWF Withheld (Enclose Form NJ-2450.

See instructions) .............................................................................................. 4748. EXCESS NJ Disability Insurance Withheld (Enclose Form NJ-2450.

See instructions) .............................................................................................. 4849. Total Payments/Credits (Add Lines 44 through 48) ................................................ ENTER TOTAL 49

(b) Line 45. Enter the amount of estimatedpayments to New Jersey for the period oftime you were a nonresident. If you madeestimated payments both as a resident and asa nonresident, enter on your part-year resi-dent return the payment(s) made to meet thetax liability for your period of New Jerseyresidency. Enter on the part-year nonresidentreturn the payment(s) made to satisfy yourtax liability during the part of the year youwere a nonresident. Also enter amounts, ifany, paid to qualify for an extension of timeto file.

Part-Year Residents

Rev. 12/07 23

8. Allocation of Wage and Salary IncomeEarned Partly Inside and Outside NewJersey. Complete this section only whenyou have wage/salary income earned partlyinside and partly outside New Jersey and youcannot readily determine the amount of wage/

salary income derived from New Jersey. Forpurposes of completing this section, “totaldays” on Line 63 means the number of dayscovered by your part-year return. CompleteLines 62–68 accordingly.

62. Amount reported on Line 14 in Column A required to be allocated .......................................................... 62

63. Total days in taxable year ............................................................................................................................ 63

64. Deduct nonworking days (Sundays, Saturdays, holidays, sick leave, vacation, etc.) ............................. 64

65. Total days worked in taxable year (Subtract Line 64 from Line 63) .......................................................... 65

66. Deduct days worked outside New Jersey ................................................................................................... 66

67. Days worked in New Jersey (Subtract Line 66 from Line 65) ................................................................... 67

68. ALLOCATION FORMULA

(See instructions if compensation depends entirely on volume of businesstransacted or if other basis of allocation is used.)

ALLOCATION OF WAGE AND SALARYINCOME EARNED PARTLY INSIDEAND OUTSIDE NEW JERSEY

PART III

(Salary earned inside N.J.)

= (Include this amounton Line 14, Col. B)

(Line 67)

(Line 65) (Enter amount from Line 62)×

Rev. 12/0724

Bulletin GIT-6

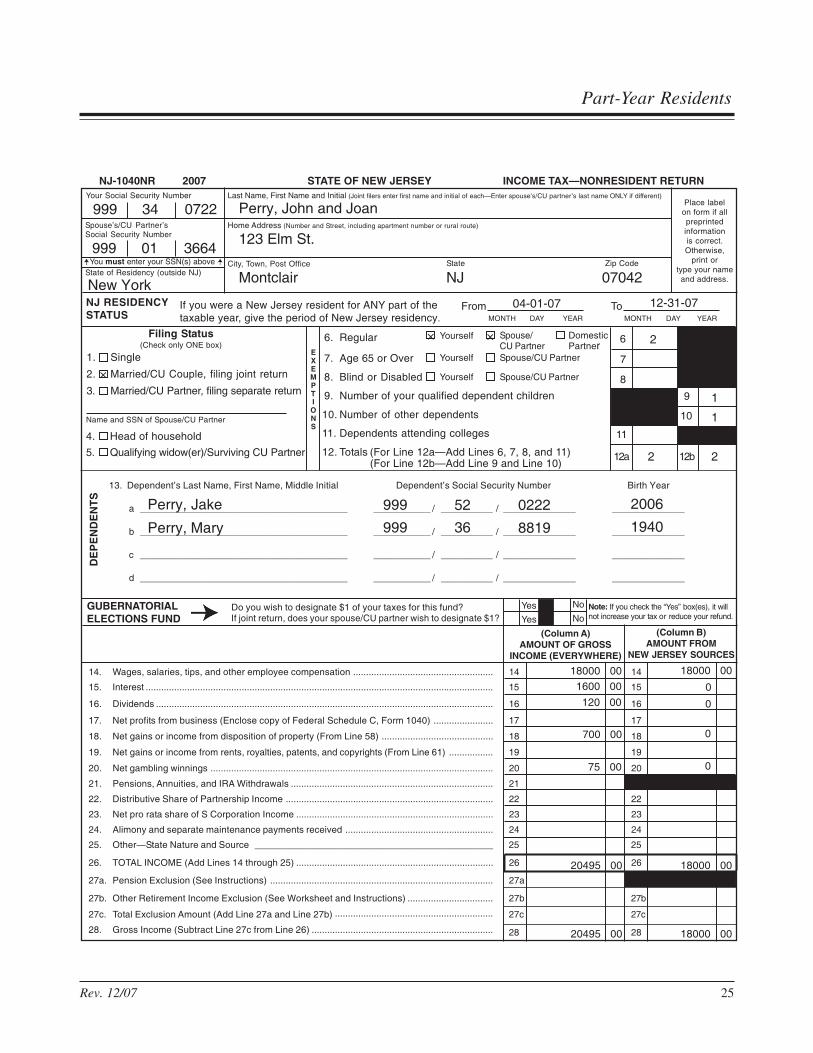

Example APart-Year Resident/Part-Year Nonresident• John Perry, age 35, and Joan Perry, age 32,

are married and file a joint Federal return.They have two dependents: their one-year-oldson and Mr. Perry’s 67-year-old mother.

• The family moved to New Jersey from NewYork City on April 1. They rented an apart-ment at 123 Elm St., Montclair, NJ 07042from April 1 to December 31 for $750 amonth.

• Husband worked for the same employer inNew Jersey all year; wages for the year,$72,000.

• Wife’s wages for part-time job fromSeptember to December, $3,000.

• Couple received $6,400 in interest on theirjoint accounts and $480 in dividends for theyear.

• On March 1, they sold 200 shares of jointlyheld stock in ABC Corp. for $3,500, pur-chased the previous year for $2,800.

• They won $75 in the New York Lottery onFebruary 3 and $62 in the New Jersey Lotteryon July 29.

• New Jersey income tax withheld: $1,983 forMr. Perry and $52 for Mrs. Perry.

• Four estimated tax payments of $50 eachmade to New Jersey on April 15, June 15,September 15, and January 15 of thefollowing year.

Part-Year Residents

Rev. 12/07 25

(Column A)AMOUNT OF GROSS

INCOME (EVERYWHERE)

NJ-1040NR 2007 STATE OF NEW JERSEY INCOME TAX—NONRESIDENT RETURN

13. Dependent’s Last Name, First Name, Middle Initial Dependent’s Social Security Number Birth Year

a ________________________________________ ___________ / __________ / ______________ ______________

b ________________________________________ ___________ / __________ / ______________ ______________

c ________________________________________ ___________ / __________ / ______________ ______________

d ________________________________________ ___________ / __________ / ______________ ______________

GUBERNATORIALELECTIONS FUND

Do you wish to designate $1 of your taxes for this fund?If joint return, does your spouse/CU partner wish to designate $1? Yes No

Note: If you check the “Yes” box(es), it willnot increase your tax or reduce your refund.

(Column B)AMOUNT FROM

NEW JERSEY SOURCES

14. Wages, salaries, tips, and other employee compensation ...................................................... 14 14

15. Interest ...................................................................................................................................... 15 15

16. Dividends .................................................................................................................................. 16 16

17. Net profits from business (Enclose copy of Federal Schedule C, Form 1040) ....................... 17 17

18. Net gains or income from disposition of property (From Line 58) ........................................... 18 18

19. Net gains or income from rents, royalties, patents, and copyrights (From Line 61) ................. 19 19

20. Net gambling winnings ............................................................................................................. 20 20

21. Pensions, Annuities, and IRA Withdrawals .............................................................................. 21 0

22. Distributive Share of Partnership Income ................................................................................ 22 22

23. Net pro rata share of S Corporation Income ............................................................................ 23 23

24. Alimony and separate maintenance payments received ......................................................... 24 24

25. Other—State Nature and Source ______________________________________________ 25 25

26. TOTAL INCOME (Add Lines 14 through 25) ............................................................................ 26 26

27a. Pension Exclusion (See Instructions) ...................................................................................... 27a 27a

27b. Other Retirement Income Exclusion (See Worksheet and Instructions) ................................. 27b 27b

27c. Total Exclusion Amount (Add Line 27a and Line 27b) ............................................................. 27c 27c

28. Gross Income (Subtract Line 27c from Line 26) ...................................................................... 28 28

18000 0018000 00

1600 00 0

0

0

0

120 00

700 00

75 00

20495 00 18000 00

18000 0020495 00

Yes No

DE

PE

ND

EN

TS

Perry, Jake

Perry, Mary

999

999

52 0222

36 8819

2006

1940

2

22

1

1

999 34 0722 Perry, John and Joan

123 Elm St.999 01 3664

Montclair NJ 07042New York04-01-07 12-31-07

6. Regular

7. Age 65 or Over

8. Blind or Disabled

9. Number of your qualified dependent children

10. Number of other dependents

11. Dependents attending colleges

12. Totals (For Line 12a—Add Lines 6, 7, 8, and 11)(For Line 12b—Add Line 9 and Line 10)

Place labelon form if allpreprintedinformationis correct.Otherwise,

print ortype your nameand address.

Your Social Security Number

Spouse’s/CU Partner’sSocial Security Number

Last Name, First Name and Initial (Joint filers enter first name and initial of each—Enter spouse’s/CU partner’s last name ONLY if different)

Home Address (Number and Street, including apartment number or rural route)

City, Town, Post Office State Zip CodeYou must enter your SSN(s) aboveState of Residency (outside NJ)

NJ RESIDENCYSTATUS

If you were a New Jersey resident for ANY part of thetaxable year, give the period of New Jersey residency.

From ToMONTH DAY YEAR MONTH DAY YEAR

Filing Status(Check only ONE box)

1. Single

2. Married/CU Couple, filing joint return

3. Married/CU Partner, filing separate return

EXEMPTIONS

6

7

8

9

10

114. Head of household

5. Qualifying widow(er)/Surviving CU Partner

Name and SSN of Spouse/CU Partner

12a 12b

Yourself

Yourself

Yourself

Spouse/CU PartnerSpouse/CU Partner

Spouse/CU Partner

DomesticPartner

×

×

×

Bulletin GIT-6

Rev. 12/0726

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements,and to the best of my knowledge and belief, it is true, correct, and complete. If prepared by a person other than taxpayer,this declaration is based on all information of which the preparer has any knowledge.

Pay amount on Line 50 in full.Write social security number(s)on check or money order andmake payable to:

STATE OF NEW JERSEY-TGIDivision of TaxationRevenue Processing CenterPO Box 244Trenton, NJ 08646-0244

You may also pay by e-checkor credit card.

Your signature Date Spouse’s/CU Partner’s Signature (if filing jointly, BOTH must sign.)

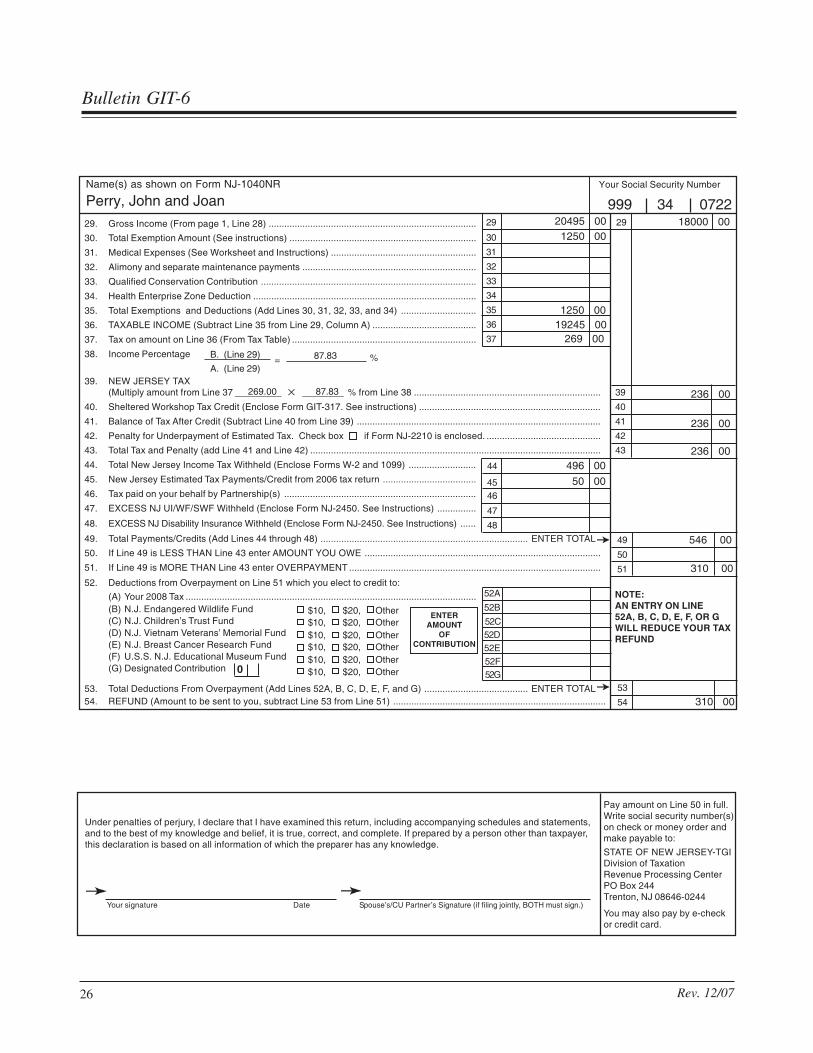

29. Gross Income (From page 1, Line 28) ................................................................................

30. Total Exemption Amount (See instructions) ........................................................................

31. Medical Expenses (See Worksheet and Instructions) ........................................................

32. Alimony and separate maintenance payments ...................................................................

33. Qualified Conservation Contribution ...................................................................................

34. Health Enterprise Zone Deduction ......................................................................................

35. Total Exemptions and Deductions (Add Lines 30, 31, 32, 33, and 34) .............................

36. TAXABLE INCOME (Subtract Line 35 from Line 29, Column A) ........................................

37. Tax on amount on Line 36 (From Tax Table) .......................................................................

38. Income Percentage

39. NEW JERSEY TAX(Multiply amount from Line 37 _________ ________ % from Line 38 ........................................................................ 39

40. Sheltered Workshop Tax Credit (Enclose Form GIT-317. See instructions) ...................................................................... 40

41. Balance of Tax After Credit (Subtract Line 40 from Line 39) .............................................................................................. 41

42. Penalty for Underpayment of Estimated Tax. Check box if Form NJ-2210 is enclosed. ............................................ 42

43. Total Tax and Penalty (add Line 41 and Line 42) ................................................................................................................ 43

44. Total New Jersey Income Tax Withheld (Enclose Forms W-2 and 1099) ..........................

45. New Jersey Estimated Tax Payments/Credit from 2006 tax return ....................................

46. Tax paid on your behalf by Partnership(s) ..........................................................................

47. EXCESS NJ UI/WF/SWF Withheld (Enclose Form NJ-2450. See Instructions) ...............

48. EXCESS NJ Disability Insurance Withheld (Enclose Form NJ-2450. See Instructions) ......

49. Total Payments/Credits (Add Lines 44 through 48) ................................................................................ ENTER TOTAL

50. If Line 49 is LESS THAN Line 43 enter AMOUNT YOU OWE ...........................................................................................

51. If Line 49 is MORE THAN Line 43 enter OVERPAYMENT .................................................................................................

52. Deductions from Overpayment on Line 51 which you elect to credit to:

(A) Your 2008 Tax ................................................................................................................(B) N.J. Endangered Wildlife Fund(C) N.J. Children’s Trust Fund(D) N.J. Vietnam Veterans’ Memorial Fund(E) N.J. Breast Cancer Research Fund(F) U.S.S. N.J. Educational Museum Fund(G) Designated Contribution

53. Total Deductions From Overpayment (Add Lines 52A, B, C, D, E, F, and G) ........................................ ENTER TOTAL54. REFUND (Amount to be sent to you, subtract Line 53 from Line 51) ..................................................................................

Name(s) as shown on Form NJ-1040NR Your Social Security Number

87.83269.00

Perry, John and Joan 999 34 0722

B. (Line 29)

A. (Line 29)= %87.83

ENTERAMOUNT

OFCONTRIBUTION