Nellie Byers Training Center Inc.FILE/...Supplies - 3,126 3,126 - 3,126 Utilities 10,461 3,939...

13

NELLIE BYERS TRAINING CENTER, INC. Financial Statements as of June 30, 2014 and 2013 and for the Years Then Ended and Independent Auditors' Report

Transcript of Nellie Byers Training Center Inc.FILE/...Supplies - 3,126 3,126 - 3,126 Utilities 10,461 3,939...

NELLIE BYERS TRAINING CENTER, INC.

Financial Statements as of June 30, 2014 and 2013 and for the Years Then Ended

and Independent Auditors' Report

NELLIE BYERS TRAINING CENTER, INC.

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS' REPORT 1

EINANCIAL STATEMENTS

Statements of Einancial Position 3

Statements of Activities and Changes in Net Assets 4

Statements of Eunctional Expenses 5

Statements of Cash Elows 7

Notes to Einancial Statements 8

=-G, Z Ab urtiier Zjuniga /\biiey Certified Public Accountants & Consultants

INDEPENDENT AUDITORS' REPORT

To the Board of Directors of Nellie Byers Training Center, Inc. Bogalusa, Louisiana

We have audited the accompanying financial statements of Nellie Byers Training Center, Inc. (a Louisiana not-for-profit corporation) (the Center), which comprise the statements of financial position as of June 30, 2014 and 2013, and the related statements of activities and changes in net assets, functional expenses, and cash flows for the years then ended, and the related notes to financial statements.

Management's Responsibility for the Einancial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors' judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

4330 Dumaine Street New Orleans, LA 70119

504-833-2436(0) • 504-484-0807(F)

200-B Greenleaves Blvd. Mandeville, LA 70448

985-626-8299(0) • 985-626-9767(F)

Limited Liability Company www.gzacpa.com

900 Village Lane P. O. Box 50, Pass Christian, MS 39571 985-626-8299(0) • 985-626-9767(F)

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Nellie Byers Training Center, Inc. as of June 30, 2014 and 2013, and the changes in its net assets and its cash flows for the years then ended in accordance with accounting principles generally accepted in the United States of America.

QwiXfyX/i LLC

Mandeville, Louisiana December 17, 2014

NELLIE BYERS TRAINING CENTER, INC. STATEMENTS OF FINANCIAL POSITION

AS OF JUNE 30, 2014 AND 2013

ASSETS CURRENT ASSETS

Cash and cash equivalents Certificate of deposit Investment Accounts receivable Medicaid receivable Prepaid insurance

Total current assets

PROPERTY AND EQUIPMENT Leasehold improvements Vehicles Furniture and equipment Building

Total property and equipment Less: accumulated depreciation

Total property and equipment, net

TOTAL ASSETS

LIABILITIES AND NET ASSETS CURRENT EIABIEITIES

Accounts payable and accrued liabilities

NET ASSETS Unrestricted

TOTAL LIABILITIES AND NET ASSETS

2014 2013

$ 213,387 $ 145,105 101,285 101,285

2,093 2,093 8,190 5,273

42,923 116,203 28,182 32,941

396,060 402,900

153,854 153,854 80,427 73,227 55,765 49,798

623,038 623,038 913,084 899,917

(392,763) (353,075)

520,321 546,842

$ 916,381 $ 949,742

$ 1,252 $ 7,861

915,129 941,881

$ 916,381 $ 949,742

See independent auditors' report and accompanying notes to financial statements. 3

NELLIE BYERS TRAINING CENTER, INC. STATEMENTS OF ACTIVITIES AND CHANGES IN NET ASSETS

FOR THE YEARS ENDED JUNE 30, 2014 AND 2013

2014 2013 REVENUES AND OTHER SUPPORT

Program services $ 41,300 $ 49,000 Sales of services 55,203 68,181 Medicaid 309,889 363,780 Donations 837 1,175 United Way designation 283 434 Other 806 5.432

Total revenues and other support 408,318 488,002

EXPENSES Program services 403,870 432,858 Support services 31,200 28,790

Total expenses 435,070 461,648

CHANGE IN NET ASSETS (26,752) 26,354

NET ASSETS-Beginning of year 941,881 915,527

NET ASSETS-End of year $ 915,129 $ 941,881

See independent auditors' report and accompanying notes to financial statements. 4

NELLIE BYERS TRAINING CENTER, INC. STATEMENT OF FUNCTIONAL EXPENSES

FOR THE YEAR ENDED JUNE 30, 2014

Program Services Support Services

Adult Habilitation

Work Activity Total

General and Administrative Total

Salaries $ 102,828 $ 54,920 $ 157,748 $ 12,863 $ 170,611 Payroll tax expense 7,971 4,257 12,228 996 13,224 Workers' compensation insurance 5,828 10,290 16,118 646 16,764

Contract labor - 39,843 39,843 - 39,843 Depreciation 31,750 7,938 39,688 - 39,688 Transportation 2,540 22,861 25,401 - 25,401 Ground maintenance - 2,619 2,619 - 2,619 Insurance 48,701 2,563 51,264 - 51,264 Lunch program - 547 547 - 547 Maintenance 3,129 20,862 23,991 2,241 26,232 Miscellaneous 1,393 10,283 11,676 - 11,676 Office expenses 566 4,176 4,742 - 4,742 Professional fees - - - 10,255 10,255 Seminars - - - 436 436 Supplies - 2,472 2,472 - 2,472 Utilities 11,284 4,249 15,533 3,763 19,296

$ 215,990 $ 187,880 $ 403,870 $ 31,200 $ 435,070

See independent auditors' report and accompanying notes to financial 5

statements.

NELLIE BYERS TRAINING CENTER, INC. STATEMENT OF FUNCTIONAL EXPENSES

FOR THE YEAR ENDED JUNE 30, 2013

Program Services Support Services

Adult Habilitation

Work Activity Total

General and Administrative Total

Salaries $ 103,095 $ 55,063 $ 158,158 $ 12,897 $ 171,055 Payroll tax expense 8,901 4,754 13,655 1,113 14,768 insurance 6,714 11,855 18,569 745 19,314 Contract labor - 52,847 52,847 - 52,847 Depreciation 28,825 7,206 36,031 - 36,031 Transportation 2,651 23,858 26,509 - 26,509 Ground maintenance - 3,190 3,190 - 3,190 Insurance 24,631 1,250 25,881 - 25,881 Lunch program - 6,195 6,195 - 6,195 Maintenance 4,368 30,796 35,164 1,451 36,615 Miscellaneous 4,357 32,163 36,520 - 36,520 Office expenses 312 2,301 2,613 - 2,613 Professional fees - - - 8,100 8,100 Seminars - - - 996 996 Supplies - 3,126 3,126 - 3,126 Utilities 10,461 3,939 14,400 3,488 17,888

$ 194,315 $ 238,543 $ 432,858 $ 28,790 $ 461,648

See independent auditors' report and accompanying notes to financial 6

statements.

NELLIE BYERS TRAINING CENTER, INC. STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED JUNE 30, 2014 AND 2013

2014 2013 CASH FLOWS FROM OPERATING ACTIVITIES

Change in net assets $ (26,752) $ 26,354 Adjustments to reconcile change in net assets to

net cash provided by (used in) operating activities: Depreciation 39,688 36,031 Changes in operating assets:

Certificates of deposit - (9) Accounts receivable (2,917) 2,427 Medicaid receivable 73,280 (86,399)

Prepaid insurance 4,759 (4,589) Changes in operating liabilities:

Accounts payable and accrued liabilities (6,609) 4,540

Net cash provided by (used in) operating activities 81,449 (21,645)

CASH FLOWS FROM INVESTING ACTIVITIES Purchases of property and equipment (13,167) (

Net cash used in investing activities (13,167) (

NET CHANGE IN CASH AND CASH EQUIVALENTS 68,282 (30,545)

CASH AND CASH EQUIVALENTS - Beginning of year 145,105 175,650

CASH AND CASH EQUIVALENTS-End of year $ 213,387 $ 145,105

See independent auditors' report and accompanying notes to financial statements. 7

NELLIE BYERS TRAINING CENTER, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Organization - Nellie Byers Training Center, Inc. (the Center) was incorporated on July 1, 1975. The Center was organized to promote the general welfare of the mentally retarded, to advise and aid parents in the solution of mentally retarded problems, and to provide work-training services for the retarded citizens of Bogalusa, Louisiana.

Basis of Accounting - The Center's financial statements are presented on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America. All income is recorded when earned and all expenses are recorded when incurred.

Financial Statement Presentation - The Center presents its financial statements in accordance with guidelines of the Financial Accounting Standards Board related to not-for-profit organizations. Under these guidelines, the Center is required to report information regarding its financial position and activities according to three classes of net assets as follows:

• Unrestricted net assets represent the portion of net assets that are not subject to donor restrictions. • Temporarily restricted net assets arise from contributions that are restricted by donors for specific

purposes or time periods. There were no temporary restricted net assets as of June 30, 2014 and 2013.

• Permanently restricted net assets are donor-imposed assets that stipulate that the donation be maintained permanently but permits the use of all or part of the income derived. There were no permanently restricted net assets as of June 30, 2014 and 2013.

Donated Assets and Services - The Center records noncash donations as contributions at its estimated fair value at the date of donation. The Center recognizes donated services, if significant in amount, that create or enhance non-financial assets or that require specialized skills, that are provided by individuals possessing those skills, and that would typically need to be purchased if not provided by donation. There were no donated assets or services for the years ending June 30, 2014 and 2013.

Fair Value Measurements - FASB Codification 820-10, Fair Value Measurements, adopts a hierarchy approach for ranking the quality and reliability of the information used to determine fair values in one of three categories to increase consistency and comparability in fair value measurements and disclosures. The highest priority (tier 1) is given to quoted prices in active markets for identical assets. Tier 2 assets are valued based on inputs other than quoted prices that are "observable." For example, quoted prices for similar securities or quoted prices in inactive markets would both be observable. In tier 3, the inputs used for valuation are not observable or transparent and assumptions have to be made about how market participants would price the underlying assets. Investments are classified based on the lowest level of input that is significant to the fair value measurement.

Use of Estimates - The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenditures during the reporting period. Actual results could differ from those estimates.

NELLIE BYERS TRAINING CENTER, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

Cash and Cash Equivalents - For purposes of the statements of cash flows, the Center's management considers all unrestricted highly liquid debt instruments purchased with an initial maturity of three months or less to be cash equivalents.

Investment - Investments are recorded at fair market value based on market quotations and consist of mutual funds.

Property and Equipment - Property and equipment are recorded at cost, except for donated items, which are stated at fair market value at the date of donation. Maintenance and repairs are charged as expenses when incurred. Purchases or donated items of $500 or more and a useful life of more than three years are capitalized. Acquisitions of property and equipment are made with unrestricted assets. The Center uses straight line depreciation method provided over the estimated useful lives of the respective assets as follows:

• Leasehold improvements 10-15 years • Vehicles 5-7 years • Furniture and equipment 5-7 years • Building 39 years

Impairment of Long-lived assets - The Center reviews long-lived assets, consisting of property and equipment and cost in excess of net income acquired, for impairment and determines whether an event or change in facts and circumstances indicates that their carrying amount may not be recoverable. The Center determines recoverability of the assets by comparing the carrying value of the asset to net future undiscounted cash flows that the asset is expected to generate. The impairment recognized is the amount by which the carrying amount exceeds the fair market value of the asset. There were no asset impairments recorded during 2014.

Accounts and Medicaid Receivables - Accounts and Medicaid receivables are stated at the amounts management expects to collect from outstanding balances. Management provides for probable uncollectible amounts through a provision for bad debt expense and an adjustment to a valuation allowance based on its assessment of the current status of individual receivables from grants, contracts. Medicaid and others. Balances that are still outstanding after management has used reasonable collection efforts are written off through a charge to the valuation allowance and a credit to the applicable accounts receivable. Management believes that all receivables are collectible and, as such, has not recorded a valuation allowance as of June 30, 2014 and 2013.

Medicaid Reimbursement Programs - The Center is paid by Medicaid for services provided to Medicaid beneficiaries and is paid a predetermined per-diem for these services based, for the most part, on the Plan of Care assigned to each client.

Restricted and Unrestricted Revenue and Support - Contributions received are recorded as unrestricted, temporarily restricted, or permanently restricted support, depending on the existence and/or nature of any donor restrictions. Support that is restricted by the donor is reported as an increase in unrestricted net assets if the restrictions expire in the reporting period in which the support is recognized. All other donor-restricted support is reported as an increase in temporarily or permanently restricted net assets, depending on the nature of the restriction. When a restriction expires (that is, when a stipulated time

NELLIE BYERS TRAINING CENTER, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

restriction ends or the purpose of the restriction is accomplished), temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statements of activities and changes in net assets. No revenues were restricted at June 30, 2014 and 2013.

Dividends - Dividends received related to investments are recorded when received. For the years ended June 30, 2014 and 2013, dividends totaled $140 and $241 and were recorded in other revenues in the statements of activities and changes in net assets.

Functional Expense Allocation - Functional expenses are allocated among various program services and general and administrative categories based on actual use or management's best estimate.

Income Taxes - Under the provisions of the Internal Revenue Code, Section 501(c)(3), and the applicable income tax regulations of Louisiana, the Center is exempt from taxes on income other than unrelated business income. The Center has also been classified as an entity that is not a private foundation in Section 170 (b)(l)(A)(vi). Since the Center had no net unrelated business income during the years ended June 30, 2014 and 2013, no provision for income tax was made. Management does not believe there are any uncertainties included in the first statement. As of June 30, 2014, the following tax years were open for review by the Internal Revenue Service: fiscal years ended June 30, 2013 and June 30, 2012. The June 30, 2014 fiscal year end tax return has not yet been submitted.

NOTE B - CONCENTRATIONS OF CREDIT RISK

The Center maintains cash balances at several financial institutions located in Bogalusa, Louisiana. Accounts at each of these institutions are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000. The Center's cash was not in excess of the FDIC limit at June 30, 2014 and 2013.

The Center has investment accounts that contain cash and securities. Balances are insured up to $500,000 with a limit of $100,000 for cash, by the Securities Investors Protection Corporation (SIPC). The Center's securities were not in excess of the SIPC limit at June 30, 2014 and 2013. The Center has no policy requiring collateral or other security to support its deposits.

NOTE C - FAIR VALUES OF FINANCIAL INSTRUMENTS

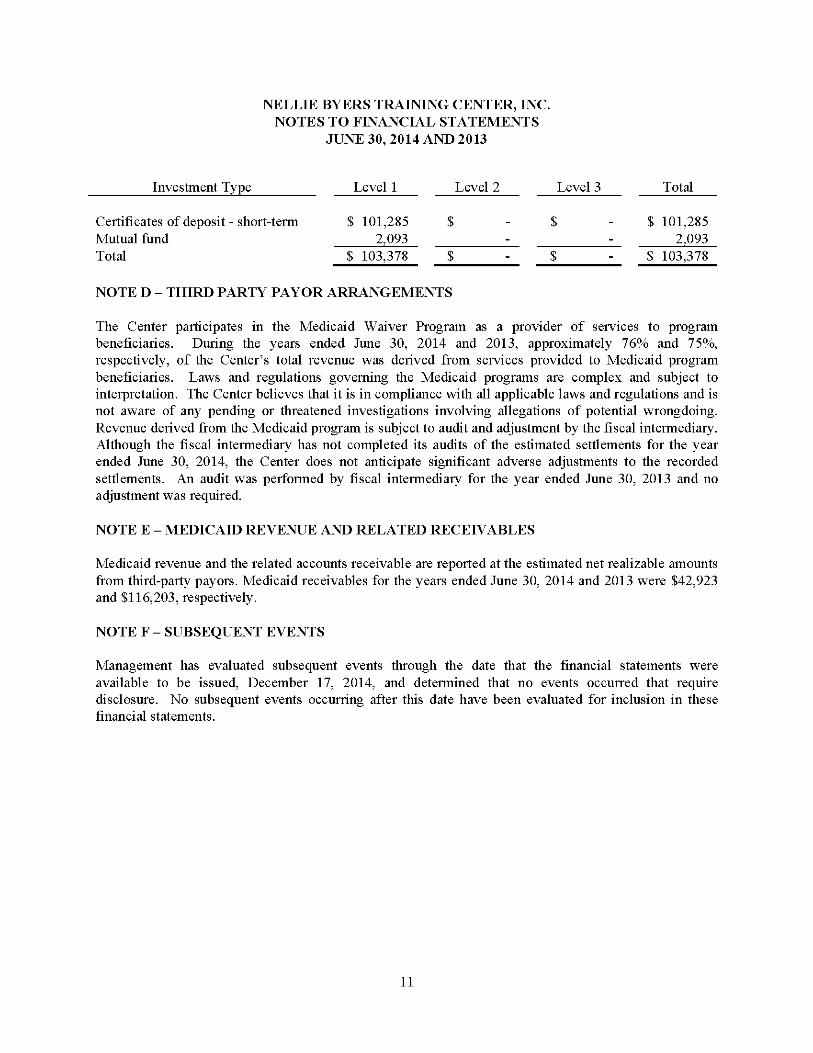

The investment portfolio as of June 30, 2014, summarized using Level 1, 2, and 3, as defined in Note A is as follows:

Investment Type Level 1 Level 2 Level 3 Total

Certificates of deposit - short-term $ 101,285 $ - $ - $ 101,285 Mutual fund 2,093 ^ ^ 2,093 Total $ 103,378 $ - $ - $ 103,378

The investment portfolio as of June 30, 2013, summarized using Level 1, 2, and 3, is as follows:

10

NELLIE BYERS TRAINING CENTER, INC. NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2014 AND 2013

Investment Type Level 1 Level 2 Level 3 Total

Certificates of deposit - short-term $ 101,285 $ - $ - $ 101,285 Mutual fund 2,093 ^ ^ 2,093 Total $ 103,378 $ - $ - $ 103,378

NOTE D - THIRD PARTY PAYOR ARRANGEMENTS

The Center participates in the Medicaid Waiver Program as a provider of services to program beneficiaries. During the years ended June 30, 2014 and 2013, approximately 76% and 75%, respectively, of the Center's total revenue was derived from services provided to Medicaid program beneficiaries. Laws and regulations governing the Medicaid programs are complex and subject to interpretation. The Center believes that it is in compliance with all applicable laws and regulations and is not aware of any pending or threatened investigations involving allegations of potential wrongdoing. Revenue derived from the Medicaid program is subject to audit and adjustment by the fiscal intermediary. Although the fiscal intermediary has not completed its audits of the estimated settlements for the year ended June 30, 2014, the Center does not anticipate significant adverse adjustments to the recorded settlements. An audit was performed by fiscal intermediary for the year ended June 30, 2013 and no adjustment was required.

NOTE E - MEDICAID REVENUE AND RELATED RECEIVABLES

Medicaid revenue and the related accounts receivable are reported at the estimated net realizable amounts from third-party payors. Medicaid receivables for the years ended June 30, 2014 and 2013 were $42,923 and $116,203, respectively.

NOTE F - SUBSEQUENT EVENTS

Management has evaluated subsequent events through the date that the financial statements were available to be issued, December 17, 2014, and determined that no events occurred that require disclosure. No subsequent events occurring after this date have been evaluated for inclusion in these financial statements.

11