NEFS Market Wrap Up Week 8

26

NEFS Research Division Presents: The Weekly Market Wrap-Up

-

Upload

nottingham-economics-and-finance-society -

Category

Documents

-

view

221 -

download

6

description

Â

Transcript of NEFS Market Wrap Up Week 8

Week Ending 31st January 2016

1

NEFS Research Division Presents:

The Weekly Market

Wrap-Up

NEFS Market Wrap-Up

2

Contents Macro Review 3 United Kingdom

United States Eurozone

Japan Australia & New Zealand

Canada

Emerging Markets

10

China India

Russia and Eastern Europe Latin America

Africa South East Asia

Middle East

Equities

17

Financials Oil & Gas

Retail Technology

Pharmaceuticals

Commodities

Energy Precious Metals

Agriculturals

22

Currencies 25

EUR, USD, GBP AUD, JPY & Other Asian

Week Ending 31st January 2016

3

THE WEEK IN BRIEF

Global growth

remains an issue

Amid sustained slow growth in China, low

growth rates continue to persist among

economies across the globe. While China’s

growth rate was 6.9% for 2015 was roughly in

line with the targeted rate of “around 7%”, the

pace of the economy has showed a significant

slowing at the back end of last year and into the

start of 2016, and is impacting heavily on

growth rates across the board. Africa’s exports

of raw materials to China have fallen

significantly, hindering producers across the

continent, particularly those in the mining

industry. Meanwhile, falling demand from China

is affecting exports out of countries ranging

from India to Australia, dragging on their

economic growth performance. With the

outlook for China seeming gloomy, it seems

that growth figures of those countries that

depend on China for exports (of which there are

many) could be restrained for some time.

Oil price slump

worsens…

Before Christmas, the dramatic fall in oil prices

amazed many, and as the price of Brent Crude

Oil dipped below $40 per barrel, down from a

peak of $112 per barrel in 2014, it seemed as if

the price could go no lower. Yet since then,

price falls have showed no let up, and this

month we have seen prices plunge, even

dropping below the $30 per barrel price for a

short period. While the price recovered to some

extent later in the month, the World Bank has

cut average price forecasts by over a third for

2016 from $52 per barrel to $37 per barrel.

Given that current oil prices have remained so

low for what is becoming a long time, pressure

is increasing on OPEC to come to a deal with

Russia to reduce oil production, in order to

boost prices.

… Continuing to

restrain inflation

Such low oil prices are continuing hold down

prices across the board in a global economy

that is already experiencing a low level of

inflation. It seems that we could still be waiting

a while longer for any sign of an increase in the

interest rate by the UK’s Bank of England.

Across the pond, while Janet Yellen initially

indicated that there could be up to three or four

increases in the Federal Reserve’s interest rate

in the US this year, given that inflation seems to

be restrained, it appears that further rate hikes

may be somewhat later than many had

predicted at the end of the last year. Perhaps

most significantly, the Bank of Japan surprised

most of us on Friday, voting to cut interest rates

on reserves held by financial institutions with

the Bank to -0.1%, demonstrating the difficulty

that it is facing in guiding the economy to its

inflationary target of 2%. Unless oil prices begin

to return to more normal levels, it seems hard

to imagine Japan, or indeed many other

countries, including the UK, to achieve inflation

targets any time soon.

Jack Millar

NEFS Market Wrap-Up

4

MACRO REVIEW

United Kingdom

Since December, the Bank of England’s (BoE)

Monetary Policy Committee (MPC) held their

monthly meeting to make their decision on the

Bank Rate and money supply that should be set

for the UK. Predictably, interest rates were held

constant at 0.5% for the 82nd consecutive time

since March 2009.

The BoE’s monetary policy objective is to

deliver price stability, which is defined by the

Government’s inflation target of 2%. CPI

inflation, shown on the below chart, was just

0.2% in December 2015, improving slightly

from 0.1% in November. Oil prices have been

falling since mid-2014 due to global supply

exceeding global demand. The price of a barrel

of crude oil fell to under $30 last week, for the

first time in 12 years. Alongside China’s

slowdown in growth, this has meant that

inflation has been subdued in many countries,

in addition to the UK.

Mark Carney, the Governor of the BoE, stated

last week in his “The Turn of the Year” speech

that a rise in Bank Rate would be considered

when inflation, GDP, and average wage growth

rise to normal levels. He added that the MPC

aim for inflation to be on target in two years,

hinting that a rate rise would not be any time

soon. In response to his dovish speech, pound

sterling fell to $1.42, a seven year low.

One of Carney’s first moves as Governor of the

BoE in 2013 was to announce his Forward

Guidance policy, which was not to raise Bank

Rate from its current level of 0.5% at least until

the headline measure of the unemployment

rate reached the 7% threshold. Unemployment

fell more quickly than anticipated, as shown on

the second graph below, leading to revisions of

the policy and eventually rendering it

unsuccessful. Unemployment is currently at

5.1%, far below the 7% guideline the MPC were

hoping for. Yet wage growth has not

accompanied the employment increase, and

this is one of the factors holding back an interest

rate rise. The ONS released their Labour

Market Statistics report last week, stating that

average earnings is around half the rate it was

pre-crisis. This has been due to a combination

of factors: higher employment in low paid jobs;

low inflation - firms consider 2% growth in pay

a generous offer in a 0% inflation climate; slack

in the labour market, giving workers bargaining

power; and ongoing effects of the 2008 financial

crisis, as workers sacrifice their pay in order to

hold on to a job.

Shamima Manzoor

Week Ending 31st January 2016

5

United States

Following the encouraging economic signs and

the strengthening US jobs market as discussed

in the pre-Christmas market wrap-ups, in a

unanimous voting decision the US Federal

reserve raised the short-term interest rate for

the first time in nearly a decade since the

economy was struck by the worst financial

crash of modern times. The Fed announced a

quarter point increase in the target range for the

federal funds rate to 0.25% - 0.5%, a small but

mighty change. The initial Federal Open Market

Committee's forecast implied three or four more

increases through this year, to end at around

1.25%, however, if the inflation remains as

weak as it appears, rates could rise much more

slowly.

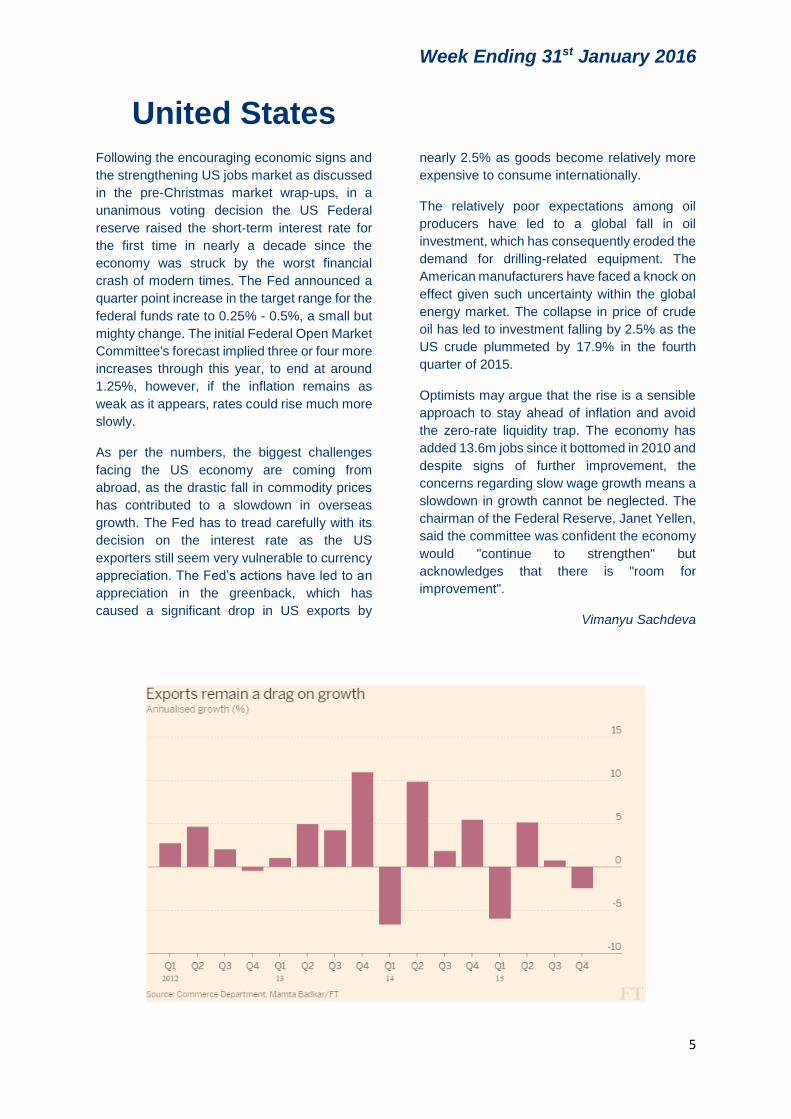

As per the numbers, the biggest challenges

facing the US economy are coming from

abroad, as the drastic fall in commodity prices

has contributed to a slowdown in overseas

growth. The Fed has to tread carefully with its

decision on the interest rate as the US

exporters still seem very vulnerable to currency

appreciation. The Fed’s actions have led to an

appreciation in the greenback, which has

caused a significant drop in US exports by

nearly 2.5% as goods become relatively more

expensive to consume internationally.

The relatively poor expectations among oil

producers have led to a global fall in oil

investment, which has consequently eroded the

demand for drilling-related equipment. The

American manufacturers have faced a knock on

effect given such uncertainty within the global

energy market. The collapse in price of crude

oil has led to investment falling by 2.5% as the

US crude plummeted by 17.9% in the fourth

quarter of 2015.

Optimists may argue that the rise is a sensible

approach to stay ahead of inflation and avoid

the zero-rate liquidity trap. The economy has

added 13.6m jobs since it bottomed in 2010 and

despite signs of further improvement, the

concerns regarding slow wage growth means a

slowdown in growth cannot be neglected. The

chairman of the Federal Reserve, Janet Yellen,

said the committee was confident the economy

would "continue to strengthen" but

acknowledges that there is "room for

improvement".

Vimanyu Sachdeva

NEFS Market Wrap-Up

6

Eurozone

European equities rebounded as the European

Central Bank said there were "no limits" to the

stimulus measures it might take to boost the

Eurozone economy.

After plunging by 3.5%, London, Frankfurt and

Paris were modestly higher in early afternoon

trading, ECB chief Mario Draghi said the bank

is "determined" to do what it takes to steer

Eurozone inflation back up towards its target of

2%.

"We have the power, willingness and

determination to act. There are no limits how far

we are willing to deploy our policy instruments,"

Draghi told a news conference after the

Eurozone’s central bank held its key interest

rates unchanged at its first policy meeting of the

year.

That stance was expected as inflation is stuck

at low levels in Europe and both the ECB and

the Bank of England will probably keep

borrowing costs at very low levels for a while

longer. "The ongoing decline in the price of

crude oil, weakening outlook for growth in

emerging economies and further softening of

inflation expectations have all increased

downside risks to the outlook for inflation in the

Eurozone," noted Lee Hardman, currency

analyst at Bank of Tokyo-Mitsubishi UFJ.

Last month council also cut the interest rate on

deposits at the central bank from commercial

banks by 0.10 percentage points to negative

0.30%. The idea is to make banks pay for

leaving money unused and push them to lend it

instead, thus increasing capital flow in the

market.

"With new downside risks to economic growth

and a significant drop in oil prices depressing

the near-term outlook for inflation, chances

have risen that the council may then agree to

an additional stimulus," Schmieding added.

Weak inflation is a sign of a sluggish economy,

and falling prices can hurt growth if they

become entrenched. The ECB focuses on

inflation because that's its legal mandate under

the European Union agreements that

established the euro.

Central bank stimulus can have far-reaching

effects on businesses, investors, savers and

consumers. The ECB stimulus has meant a

stronger dollar against the euro, adding a

headwind for US exporters to Europe. It has

also slashed returns on savings in conservative

investments such as bonds, insurance policies

and bank accounts for people looking ahead to

retirement.

With the Eurozone bogged down by the refugee

crisis and stagnant growth, it is hopeful that

quantitative easing would drive an increase of

capital and spending in the market.

Erwin Low

Week Ending 31st January 2016

7

Japan

The Bank of Japan (BoJ) voted on Friday to

reduce interest rates on excess reserves held

by financial institutions with the BoJ to -0.1%.

This move, which follows in the footsteps of the

ECB and others, comes as a surprise to many

as the governor of the BoJ Haruhiko Kuroda

had previously denied that the central bank was

considering negative interest rates. This is a

bold step by the BoJ, which demonstrates its

willingness to do what it takes to achieve their

inflationary target of 2%, and the cut comes

after the expected time frame for reaching this

target was pushed back for the third time in less

than a year. As a result of this news the Yen

plunged 1% against the euro and yields on

Japanese government bonds fell. The bank claims that it is moving because of the

recent slowdown in China and the fall in energy

prices rather than because of weakness in the

domestic economy, however many will point to

the fact that the growth in household spending,

at -4.4%, was much lower than expected.

Although unemployment remained low at

around 3%, companies have opted not to

increase wages, which is good news for

investors but may add to the deflationary

pressure. Indeed, a slew of other weak data for

December may also have spurred the BoJ into

making this announcement; retail sales at -

1.1% were lower than expected, industrial

production at -1.4% also failed to meet

forecasts, and both imports and exports fell. Mr

Kuroda did, however, claim that underlying

inflation was strong and pointed to a price index

that excludes energy prices, which reports

inflation as 1.3%, as evidence of this.

By instigating negative interest rates the BoJ

hopes that borrowing cost for companies and

households will fall and that this will increase

the demand for loans and encourage

investment in higher yielding assets. Critics

argue, however, that this will only promote “tit

for tat” currency devaluations, deprive

commercial lenders and their customers and

encourage fiscal indiscipline by the

government.

In other news, Akira Amari, one of the key

players in the ‘Abenomics’ programme, a

strategy designed to end the age of stagnant

prices (see diagram) in Japan, resigned over

corruption allegations. This will be a blow for

Prime Minister Shinzo Abe as it may make it

more difficult for him to implement some of his

key economic policies and could therefore

jeopardise the aforementioned move by the

BoJ.

Daniel Nash

NEFS Market Wrap-Up

8

Australia & New

Zealand

A combination of economic events arose during

the festive period in Australia. Westpac’s

consumer sentiment measurement declined

from 3.9% to -0.8% in December, with a further

depreciation by 3.5% towards the end of

December, driven by family finances and

international factors including spill over effects

on financial markets. Australia’s seasonally

adjusted unemployment rate remained

unchanged at 5.8%. This was slightly below

market consensus with 1000 jobs were lost, the

smallest decline since May 2010. But local

newspapers advocate that young Australians

are pessimistic about finding jobs and are

reluctant to take entrepreneurial risks. Flat

exports and a 1% rise in imports resulted in a

further decline in the trade deficit from -2.40

billion to -3.31 billion, stumping forecasters who

made a -2.61 billion prediction. The main drag

on trade was an unexpected reduction in

exports of metal, along with non-monetary gold.

JP Morgan analyst, Tom Kennedy, stated that it

was merely “temporary” factors which resulted

in a lower Australian trade deficit.

This week Australia awaited for the CPI inflation

figures to be released. There was a marginal

decrease by 0.1%, presenting itself at 0.4% in

the three months through December, with the

annual rate at 1.7%. Tobacco along with

domestic and international vacation travel were

the main contributors to the rise in consumer

prices, although slightly offset by falling prices

of motor fuels and telecommunications

services.

In New Zealand, the reserve bank lowered the

official cash rate from 2.75% to 2.50%, as

expected by forecasters in December. CPI

inflation was below the 1-3% target (a result of

the strengthening of the New Zealand dollar

and a 65% fall in world oil prices in 2014) and

so the country’s monetary policy needs to be

accommodative to this.

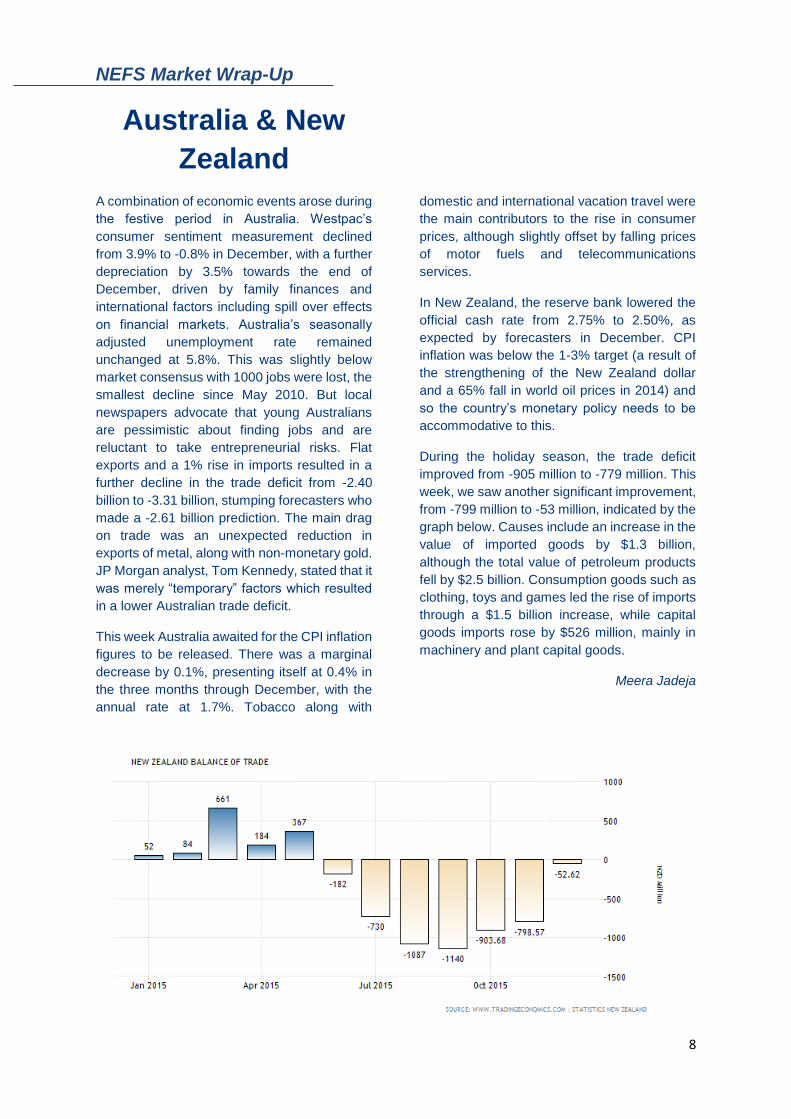

During the holiday season, the trade deficit

improved from -905 million to -779 million. This

week, we saw another significant improvement,

from -799 million to -53 million, indicated by the

graph below. Causes include an increase in the

value of imported goods by $1.3 billion,

although the total value of petroleum products

fell by $2.5 billion. Consumption goods such as

clothing, toys and games led the rise of imports

through a $1.5 billion increase, while capital

goods imports rose by $526 million, mainly in

machinery and plant capital goods.

Meera Jadeja

Week Ending 31st January 2016

9

Canada

The forecast for GDP growth in Canada has

been reduced for the second time in the last

month, from 1.7% to 1.3% for 2016, by one of

the largest banks in Canada, CIBC Markets.

One of the major contributions to the reduction

in the prediction of GDP growth is the fall in the

price of oil. In 2014, oil exports out of Canada

were valued at $128.6 billion and accounted for

27.2% of Canada’s total exports. This indicates

that oil exports are a significant contribution to

GDP values in Canada. In the year to

December 2015, oil prices declined by 40%

which was one of the main reasons cited by

CIBC for their first reduction in the prediction for

GDP growth.

It has also been announced that Canadian GDP

growth increased to 0.3% in November, this is

in comparison to zero GDP growth in October

and a decline of 0.5% in September 2015. This

comes as good news after Canada performed

weakly last year, entering a recession at the

beginning of 2015, after GDP growth declined

for two consecutive months.

The Federal agency states this increase in GDP

growth was mainly accounted for by

improvements in the performance of retail and

wholesale trade, manufacturing and energy

extraction. Wholesale trade increased by 1.3%

in November after decreasing for four

consecutive months. Retail trade growth rose

by 1.2% and manufacturing by 0.4%. Natural

resource extraction increased by 0.6% and gas

extraction by 2.1% in November 2015.

However, despite this improvement in the

Canadian economy, GDP growth for the final

quarter of 2015 may have only increased by a

fractional amount. The senior rates strategist at

T D Securities, Andrew Kelvin, stated that the

increase of GDP growth in Canada puts GDP

growth for the final quarter of 2015 at zero. This

is exactly what the Canadian central bank had

predicted previously. For the Bank of Canada,

"it doesn't change anything there," Kelvin said.

Consequently, whilst the slight improvement in

GDP growth is a reason for some hope, the

Canadian economy is still performing weakly

and there still a long way to go to recover from

the technical recession of early 2015.

Kelly Wiles

NEFS Market Wrap-Up

10

EMERGING MARKETS

China

The global market selloff over the last month

can be largely attributed to the sentiment

present within and around the Chinese

economy. Locally, major equity indices in China

are down by approximately 20-25% since the

start of the New Year.

The Caixin manufacturing purchasing

managers index (PMI) for December was

released at the start of the new business year

with a dismal reading of 48.2. This was below a

forecast of 48.9, representing yet another

month of declines in manufacturing. A survey

figure below 50 indicates a contraction in the

sector, and is a leading indicator of economic

health. The release of this data preceded the

triggers of the newly implemented circuit

breakers. Trading was halted for 15 minutes on

the first trading day after the CSI 300 fell by 5%

before closing early for the day after it fell

further to -7%. The circuit breakers were

activated once again later in the week after just

30 minutes of trading. Designed to limit market

swings, the ineffectiveness of the mechanism

led to its suspension.

China recorded gross domestic product of

about $10 trillion in 2015. Inflation-adjusted

fourth quarter GDP figures came in at 6.8%,

representing a full-year growth rate of 6.9%, the

slowest rate since 1990, but this was roughly in

line with China’s target of ‘around 7%’. The

services sector, comprising sectors such as

finance and healthcare, accounted for

approximately 50% of GDP. Consumption

contributed to 60% of growth. The target growth

rate for 2016 has been set at 6.5%. There is a

consensus that China’s maximum potential

growth is slowing as an aging population

shrinks the labour force and growth from a

shifting labour force to the modern economy is

exhausted. President Xi Jinping has

established that policy in 2016 will focus on

supply-side reforms. However, demand-side

stimulus from the central bank will still take

place, evident in the recent devaluations in the

Yuan.

The recent devaluations in the Yuan have also

rocked global markets. It is worth remembering

that the Chinese have kept the Yuan relatively

strong in recent years to facilitate the

economy’s transition from a manufacturing and

investment-based one to one that is driven by

services and consumption. Credibility of its

growth figures still remains an issue.

Improvements in transparency of the economy

and less market intervention can help turn

China into a country the world can trust.

Sai Ming Liew

Week Ending 31st January 2016

11

India

Aside from the optimistic growth rate reported

in November, the rest of the holidays were

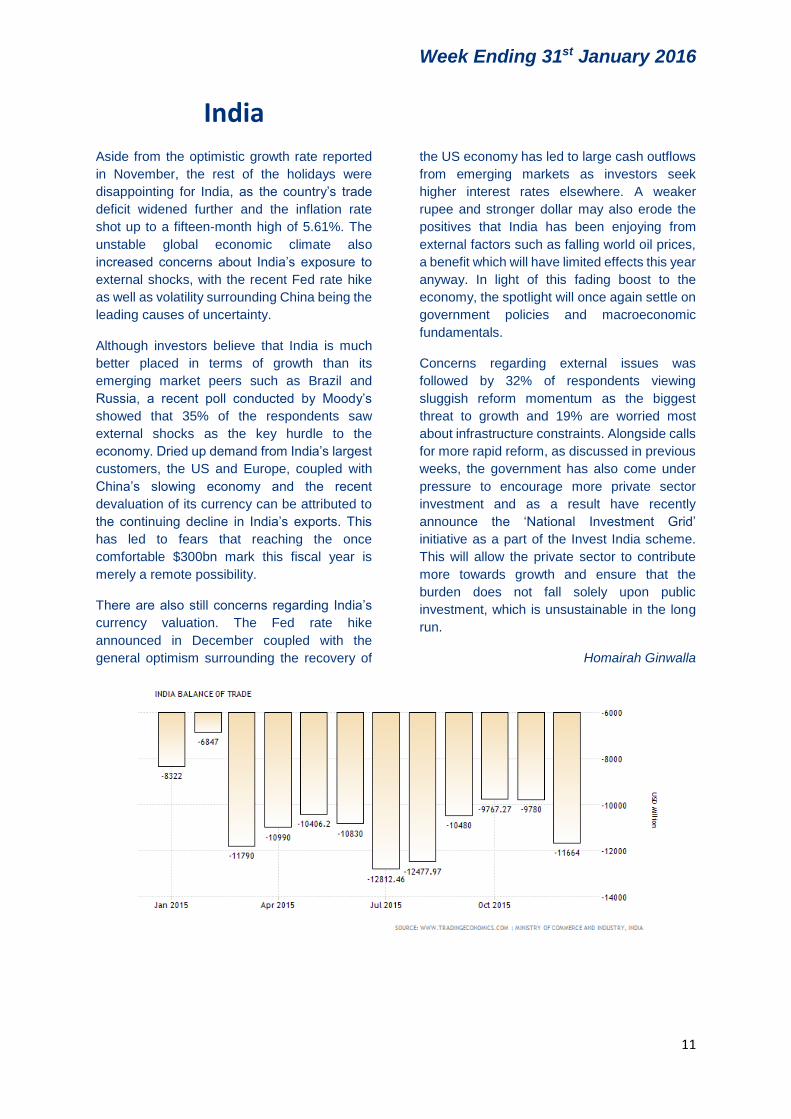

disappointing for India, as the country’s trade

deficit widened further and the inflation rate

shot up to a fifteen-month high of 5.61%. The

unstable global economic climate also

increased concerns about India’s exposure to

external shocks, with the recent Fed rate hike

as well as volatility surrounding China being the

leading causes of uncertainty.

Although investors believe that India is much

better placed in terms of growth than its

emerging market peers such as Brazil and

Russia, a recent poll conducted by Moody’s

showed that 35% of the respondents saw

external shocks as the key hurdle to the

economy. Dried up demand from India’s largest

customers, the US and Europe, coupled with

China’s slowing economy and the recent

devaluation of its currency can be attributed to

the continuing decline in India’s exports. This

has led to fears that reaching the once

comfortable $300bn mark this fiscal year is

merely a remote possibility.

There are also still concerns regarding India’s

currency valuation. The Fed rate hike

announced in December coupled with the

general optimism surrounding the recovery of

the US economy has led to large cash outflows

from emerging markets as investors seek

higher interest rates elsewhere. A weaker

rupee and stronger dollar may also erode the

positives that India has been enjoying from

external factors such as falling world oil prices,

a benefit which will have limited effects this year

anyway. In light of this fading boost to the

economy, the spotlight will once again settle on

government policies and macroeconomic

fundamentals.

Concerns regarding external issues was

followed by 32% of respondents viewing

sluggish reform momentum as the biggest

threat to growth and 19% are worried most

about infrastructure constraints. Alongside calls

for more rapid reform, as discussed in previous

weeks, the government has also come under

pressure to encourage more private sector

investment and as a result have recently

announce the ‘National Investment Grid’

initiative as a part of the Invest India scheme.

This will allow the private sector to contribute

more towards growth and ensure that the

burden does not fall solely upon public

investment, which is unsustainable in the long

run.

Homairah Ginwalla

NEFS Market Wrap-Up

12

Russia and Eastern

Europe

With reports published over the Christmas

period confirming last year’s economic growth

rates throughout Eastern Europe, it is a fair

conclusion to draw that 2015 has seen a very

mixed bag of results.

Russia’s financial situation has continued to

worsen, with GDP shrinking by 3.8%

throughout the year (as shown on the graph

below). The Ruble has lost more than half its

value in the past 18 months, leading to very

expensive imports and high inflation rates.

Wage growth is at a new low, and as

consumers adjust to lower real disposable

incomes, Russian retail consumption has fallen

by 8.9%. Investment rates have fallen

throughout the year, with a drop of 8.7% in

December. With increasing unemployment and

government unable to take economic action

against falling oil prices, social discontent is

rising rapidly.

Unfortunately the Belarusian economy is not

much better. After 20 years of positive growth,

2015 saw Belarus fall into recession (3.9% drop

in GDP). Whilst some argue it is due to Belarus’

loss of a strong trading partner (Russia), others

suggest that Belarus faces a structurally

unsound economy that will require large

economic reforms to amend. Ukraine is also in

a difficult position, despite its EU free-trade

agreement. Tax evasion and corruption

amongst the elites has prevented economic

meltdown, however Ukraine still faces

particularly low GDP growth rates (1% in 2015),

and increasing inflation rates.

On a more positive note, Bulgaria did extremely

well in 2015. It greatly surpassed expectations

by reaching growth levels of 3%, and it is hoped

that growth will reach 4.5% in 2016. The Czech

Republic has also been successful, with

unemployment at a low level in comparison with

other European countries (at 10.5%). 2016

looks positive for Slovakia and Romania, with

continued high levels of growth predicted. In

Hungary, the government introduced growth-

enhancing measures, which should ensure

GDP growth levels of 2%. Unfortunately

however, some fear that these measures are

unaffordable, and will worsen the economic

divide between the dynamic centres of western

and central Hungary and the struggling Eastern

regions. Finally, Poland has continued to do

well, with 2015 growth reaching a four-year high

of 3.6%. This should be sustained throughout

2016, with increasing trade and rising private

consumption levels.

Consequently, whilst the coming year will be

turbulent for Eastern Europe, particularly in

Ukraine and Russia, many economists predict

that various states will see a successful year of

economic growth and reform.

Charlotte Alder

Week Ending 31st January 2016

13

Latin America

The Christmas break has seen some

interesting developments within emerging

markets, particularly in Latin America, where

we have seen the likes of Mauricio Macri take

power in Argentina. Meanwhile, with Brazil

facing its highest levels of inflation since 2002,

the country’s central bank has been left with

some challenging decisions, as policymakers

struggle to curb rising inflation amid a deep

contraction. Considering this, Brazil’s central

bank left its benchmark interest rate unchanged

at 14.25% at its January 20th meeting; the Selic

rate was left on hold at a 9-year high for the

fourth straight meeting.

Argentina’s new centre-right government has

been busy with a 30% devaluation of the

Argentine peso, shortly after Mr Macri took

power, alongside the removal of stringent

capital controls put in place by Ms Fernández

de Kirchner in 2011. However this move fuelled

inflation fears even though economists at

Barclays described the move as “perfectly

orchestrated”.

Yet, although the new market-friendly

administration has made a “strong start”,

including a well-received devaluation, many

serious challenges lie ahead. These include

tackling inflation of about 30%, a fiscal deficit of

almost 8% and a decade-long legal dispute with

creditors in the US that are blocking Argentina’s

access to international capital markets.

However, progress is being made: in an effort

to end the debt saga, Argentina will make a

proposal to the group of hedge funds led by

Paul Singer, a US billionaire, by next week, say

government officials. The approach is sooner

than many analysts had expected and could

open the door to economic normality for

Argentina. ”. Further deals are being negotiated

and the government is expected soon to

announce a $5bn loan from a group of

international banks, led by JPMorgan and

HSBC, to boost central bank reserves which

had been depleted by the previous leftist

administration.

The future is looking more promising for

Argentina, as last week the new finance

minister announced plans to reduce the primary

fiscal deficit by 1% and bring inflation down to

between 20 and 25%. The opposite could be

said for Brazil, and it could be in for a very

painful year even with the Olympics set to take

place over the summer.

Max Brewer

NEFS Market Wrap-Up

14

Africa

Years of rapid economic growth across sub-

Saharan Africa fuelled hopes of a prosperous

new era where economies no longer depended

on the fickle global demand for Africa’s raw

resources. However the recent slowdown of the

Chinese economy and as its once seemingly

insatiable hunger for Africa’s commodities

wanes, many African economies are tumbling

quickly.

The outlook across the continent has grown

grimmer, especially in its two biggest

economies, Nigeria and South Africa.

The International Monetary Fund, on

Tuesday, has sharply cut its projections for the

continent. They also predicted an increase in

the unemployment rate of 0.8% in the 1st

quarter of 2016. As Africa’s biggest exporter of

iron ore to China, South Africa is suffering from

a slump in mining as well as in other sectors like

manufacturing and agriculture. The economy

of South Africa is expected to slide into a

recession this year.

South African Reserve Bank governor

announced on Thursday a 50 basis-point

increase in the repo rate to 6.75%, in line with

the consensus and therefore the prime lending

rate will be 10.25%. Lending rates have

increasing continuously since 2015 owing to

expectations of higher inflation. Inflation is still

expected to breach the upper end of the target

set by the central bank.

Nigeria, Africa’s biggest oil producer, is reeling

from the further fall in crude prices this week.

With oil accounting for 80% of government

revenue, the government may also lack the

resources to quell potential unrest in the Niger

Delta, the source of the country’s oil. In addition,

weakening currencies make it harder for

Nigeria and many other African governments to

repay China for loans used to build large

infrastructure projects.

But experts also see bright spots on the map.

While previously high-flying commodity

exporters, like Angola and Zambia have been

hit hardest by China’s slowdown, other

countries are showing greater resilience.

The International Monetary Fund has urged

Kenya to diversify its economy to take

advantage of new promising sectors with huge

opportunities for growth in the face of gloomy

projections for world growth. IMF Kenya

representative cited the need to enhance

productivity in the country's agricultural sector

which will lead to new business opportunities in

other sectors. Eventually this would translate

into deeper insertion of Kenyan products in

global markets, especially when the ongoing

investment in infrastructure upgrades start to

pay off.

Sreya Ram

Week Ending 31st January 2016

15

South East Asia

Indonesia, Southeast Asia’s largest economy,

continues their ongoing struggle to promote

economic growth and enhance living standards.

It comes after the central bank of Indonesia cut

its 2016 forecast GDP growth for the second

time this year and now expects yearly growth of

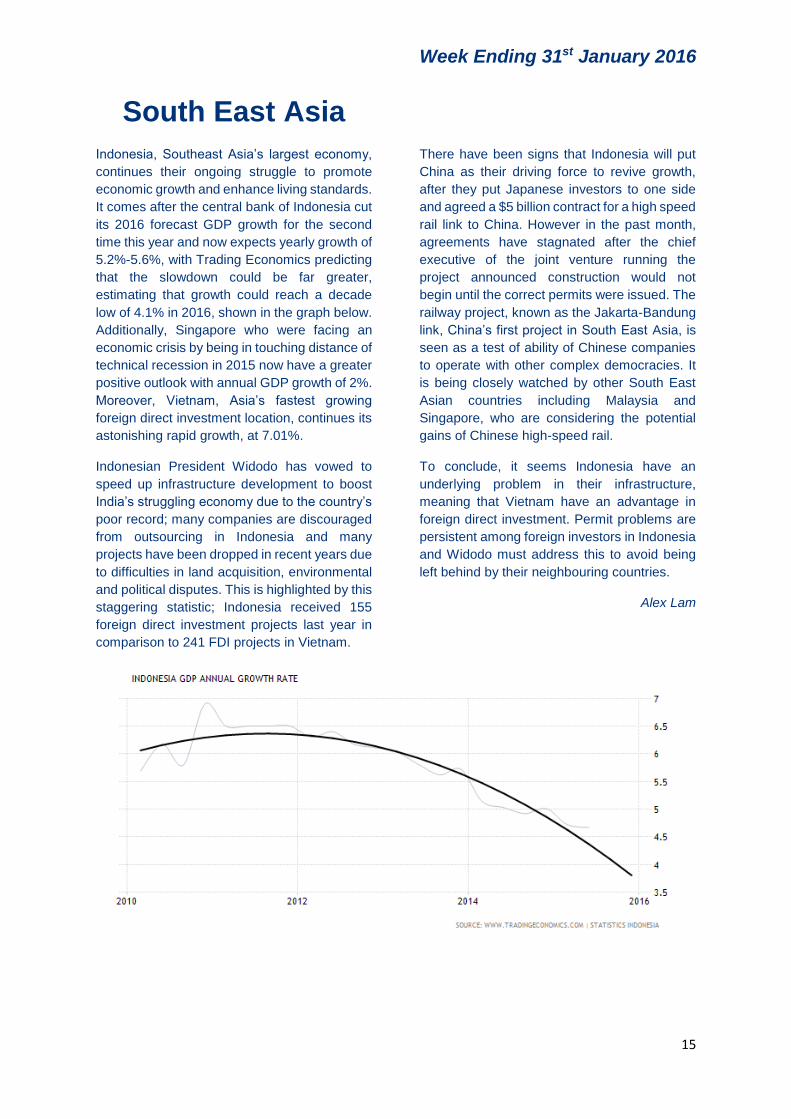

5.2%-5.6%, with Trading Economics predicting

that the slowdown could be far greater,

estimating that growth could reach a decade

low of 4.1% in 2016, shown in the graph below.

Additionally, Singapore who were facing an

economic crisis by being in touching distance of

technical recession in 2015 now have a greater

positive outlook with annual GDP growth of 2%.

Moreover, Vietnam, Asia’s fastest growing

foreign direct investment location, continues its

astonishing rapid growth, at 7.01%.

Indonesian President Widodo has vowed to

speed up infrastructure development to boost

India’s struggling economy due to the country’s

poor record; many companies are discouraged

from outsourcing in Indonesia and many

projects have been dropped in recent years due

to difficulties in land acquisition, environmental

and political disputes. This is highlighted by this

staggering statistic; Indonesia received 155

foreign direct investment projects last year in

comparison to 241 FDI projects in Vietnam.

There have been signs that Indonesia will put

China as their driving force to revive growth,

after they put Japanese investors to one side

and agreed a $5 billion contract for a high speed

rail link to China. However in the past month,

agreements have stagnated after the chief

executive of the joint venture running the

project announced construction would not

begin until the correct permits were issued. The

railway project, known as the Jakarta-Bandung

link, China’s first project in South East Asia, is

seen as a test of ability of Chinese companies

to operate with other complex democracies. It

is being closely watched by other South East

Asian countries including Malaysia and

Singapore, who are considering the potential

gains of Chinese high-speed rail.

To conclude, it seems Indonesia have an

underlying problem in their infrastructure,

meaning that Vietnam have an advantage in

foreign direct investment. Permit problems are

persistent among foreign investors in Indonesia

and Widodo must address this to avoid being

left behind by their neighbouring countries.

Alex Lam

NEFS Market Wrap-Up

16

Middle East

Generating economic growth in the Middle East

is crucial to defeating extremism, Iranian

President Hassan Rouhani said on Tuesday,

putting forward his country as a regional trade

hub and pillar of stability. This comes as

Rouhani makes a four-day trip to Italy and

France, looking to rebuild Iranian relations with

the West some two weeks after financial

sanctions on Tehran were rolled back following

the implementation of its nuclear deal with

world powers.

Italy announced some 17 billion euros of

business deals with Iran on Monday. Sizeable

contracts are also in the offing in France,

reflecting EU countries' keenness to cash in on

the diplomatic thaw with the Islamic Republic.

One particular highlight is the ongoing

negotiations with European aircraft maker

Airbus to buy 114 planes, in what would

represent an upgrade for a fleet that has an

average age of 25 years and includes some

aircraft that predate the 1979 Islamic revolution.

Underscoring the growing warmth, Rouhani

said he expected Italian Prime Minister Matteo

Renzi to visit Iran in the coming months to help

boost bilateral economic alliances. "We are

ready to welcome investment, welcome

technology and create a new export market,"

Rouhani told a business forum, saying Iran had

ambitions to develop its own economy after

years of curbs and hardship. As the graph

below shows, Iran has struggled with a wide

scale deterioration of its economy for the past 4

years, directly as a result of Western sanctions

to its past nuclear ambitions. With Iran’s GDP

per capita having fallen 10.7% since 2011,

Rouhani is hopeful that these new deals will

begin a much needed revival of the domestic

economy amid the strife of Islamic State in the

region.

"If we want to combat extremism in the world, if

we want to fight terror, one of the roads before

us is providing growth and jobs. Lack of growth

creates forces for terrorism. Unemployment

creates soldiers for terrorists," Rouhani said.

However problems have arisen with Iran's

emergence from the diplomatic cold. Sunni

arch-rival Saudi Arabia – alarmed at these new

deals with the Western Powers – has sought to

deflate hopes that Tehran would be a bonanza

for foreign investors. The two powerhouses of

the gulf have ended all diplomatic and

economic relations in response to the recent

execution of Sheik Nimr al-Nimr, a popular

cleric and activist against the Saudi elite.

Harry Butterworth

Week Ending 31st January 2016

17

EQUITIES

Financials

On January the 29th, Tullet Prebon announced

it is to cut 7.5% (70 people) of staff within

Europe and North America. The move,

combined with a higher profit margin forecast,

pushed the company’s shares up by 8% over

the following day, establishing a solid start to

the year with a positive prospective forming for

shareholders. This future outlook sees share

prices forecasted at an annual median of 383p

on the London Stock Exchange, representing

an impressive 14% rise of the current value.

Furthermore, dividends of 17p are expected

over the following fiscal year, representing a

rise of 0.9%. This positive potential for this

company intrigues investors, who are holding

onto shares in the meantime. But the low

returns offer a reasonable excuse for not

buying.

Earlier this week, the Bank of Japan shocked

investors with a surprising announcement of

adopting a negative interest rate, with rates

being cut to minus 0.1%. This ended what was

a month of volatility surrounding the central

bank and as a result have seen equity

benchmarks jumping, alongside a plummet in

the yield of 10-year Japanese government

bonds with a drop of over half to 0.10%, settling

a record low return.

The monetary attempt to encourage economic

spending saw Bank of Japan’s shares tumble,

with their shares valued at 41,000 JPY at the

start of January, and finishing the month on a

less satisfactory 38,200 JPY. Comparisons to

the Nikkei 225 stock index (the price-weighted

average of Japans top 225 performing

companies) present a predictable story, where

the index has followed in a similar pattern to the

Japanese bank’s performance, with it beginning

the month at 19,000 JPY and now falling to

around 17,500 JPY. The figure below describes

the infliction the bank’s performance is having

on Japans economy, with the last third of the

graph representing the month of January, which

witnessed a correlated plummet for the two.

The bank’s announcement of contractionary

policy had also spread its impact beyond the

Tokyo Stock Exchange to international

markets. This simply furthers what has been a

difficult January for the global financial sector,

with Wall Street’s S&P 500 index having fallen

7.4% over the past month.

Daniel Land

Figure: BoJ vs Nikkei 225 Index

NEFS Market Wrap-Up

18

Oil and Gas

Before the Christmas break, the oil situation

was bad – not dire. Now, one month on you’d

struggle to find anyone optimistic. Prices have

plummeted; ongoing is, to put it bluntly, a glut.

What’s more is that the effects are being felt;

producers’ equities have fallen further at the

start of this year.

So disastrous is the current nature of oil prices

that the governor of Alaska is in favour of

introducing what will be the first state income

tax in 35 years. This is designed to compensate

for the losses in oil-related tax revenue, which,

in Texas, has amassed to approximately 50%

in both oil and gas. Last year over 17,000 oil

and gas workers were laid off in the US – this is

a significant amount especially when we

consider that the Texan working population is

held up largely by the oil and gas industries. On

top of the job losses, 42 North American

companies have filed for bankruptcy protection,

stressing the acknowledgement of volatility in

the industry. An analyst for Oppenheimer & Co

even went so far as to say that more than half

of independent drilling companies in the US

could go bankrupt before prices bounce back.

Often forgotten too, are the companies that

issue credit cards to regular gas consumers,

which, incidentally, take a 3% transaction fee.

Because of this, the $120 billion less spent at

the pump has translated into a $3 billion fall in

these companies’ revenue. Furthermore, along

with bankruptcy and revenue losses, the risk of

oil companies defaulting on drilling loans has

sky-rocketed, particularly problematic for banks

such as Bank of America Merryl Lynch and

Wells Fargo who have $27 and $17 billion in oil

and energy loans respectively.

Ultimately, however, we have to remember the

words of James Hamilton, economics professor

at the University of California, who reminded us

that the worst affected locations in the US will

be the same as those in the 1980s oil glut: those

who export the most. Consequently, then, the

overall effect on the US, a net importer, will be

positive. These words also, however, translate,

onto a global scale and so we can say that the

effect for a net exporter like Russia and OPEC

will be negative, very negative.

Tom Dooner

Week Ending 31st January 2016

19

Retail

Retail equities have not come off unscathed by

recent bearish investor sentiments. The FTSE

350 retail index has fallen by 6.54% since the

7th of December, the date at which NEFS

released its last market wrap up. Coming up to

Christmas, retailers witnessed a relative fall in

sales from previous years which is alarming for

a sector that traditionally expects to achieve

14% (according to the Office for National

Statistics) of its sales during the month of

December.

A relative trading slump occurred before

Christmas this year with the share price of blue-

chip retailers including Next plunging as a

result. Next’s sales were down by 0.5% in the

60 days before Christmas, well below city

forecasts, causing its share price to tumble by

5% after its festive results were announced on

January the 5th. Warm weather has been cited

as an explanation for poor fourth quarter results

and Next even produced the rather convincing

graph below to explain.

The years busiest day for internet shopping

occurred on Black Friday in November as

retailers offered a multitude of discounts to

battle for sales. Consumers are obviously

becoming increasingly savvy when it comes to

seeking out these deals as more people are

going online to take advantage of Black Friday

and the Boxing Day sales instead of regular

shopping in the 2 weeks before Christmas. For

example, John Lewis reported a 10.7% rise in

online sales on the first day of its discounts:

Christmas day. Although Next shunned the

Black Friday sales and still performed well on

the day, its lack of stock and relatively

weakening online presence is being reflected in

its share price which has fallen by 13.6% since

the 2nd of December.

Overall, Christmas has been relatively

downbeat for retailers, especially those who

failed to invest heavily in online trade. Online

giants including Amazon and Ebay have

certainly soaked much trade away from high-

street brands as they focus on sales instead of

profits. However, this has had severe

consequences as even they took huge share

price hits, both falling by 12% following poor

earnings reports.

Sam Hillman

NEFS Market Wrap-Up

20

Technology

In general, the technology heavy, NASDAQ

index has fallen 8% in the last month, mainly

due to the strengthening dollar, interest rate

hikes and the Chinese stock market crash. In

the past week the news has been dominated by

firms releasing their Q4 results, with many of

the market giants making headlines. For

example, Apple [NASDAQ: AAPL] has had to

recall 12 years’ worth of plugs which have

caused safety concerns due to overheating.

Amazon [NASDAQ: AMZN] was one of the

week’s top losers due to an unpredicted small

increase in sales. The online shopping firm

reporting a 21.8% rise in fourth quarter sales,

pointing mainly to the holiday shopping season

and increased used of its cloud computing

system. However, this increase was 5.7 times

less than the sales figures predicted by city

analysts. This shortfall sent Amazon’s share

price tumbling 13%, as shown on the graph

below, as investors felt the market had

overvalued the company. This event continued

Amazon’s trend of missing analyst forecast.

Five out of the last eight predictions have been

missed, which has baffled many shareholder as

the company has invested in increasing its

workforce by 50%, as well as buying new

machinery. The firm also announced earlier in

the week that it will be pumping more cash into

“Amazon Web Services”. This is likely to reduce

its cash flow further, while the return on this

investment is unknown, therefore, I would warn

against investing in Amazon.

As I briefly mentioned earlier, the Christmas

period has brought about a large increase in

sales of cloud computing services. Consumers

of these services are not just households but

also large corporations, such as high street

banks, who can save vast amount of

investment on infrastructure by “renting” the

memory storage service. Microsoft [NASDAQ:

MSFT] has particularly benefited from this

increase in sales, with revenue for its cloud

services division rising 5% to $6.3bn in the last

quarter. However, company profits for the final

three months of 2015 fell 15% to $5bn. Many

point to the fall in PC sales, which could be due

to the strengthening US dollar making

purchases for foreign customers more

expensive. Unlike Amazon, however, these Q4

results where much better than expectations,

thus the share price rose 5.5% during Fridays

trading.

Sam Ewing

(A graph of the Amazon share price in the last week. Source: Yahoo! Finance)

Week Ending 31st January 2016

21

Pharmaceuticals

With the advent of the New Year, we have seen

the FTSE 350 Index - Pharmaceutical &

Biotechnology fall by 4.46% in the last month

and the NASDAQ Biotechnology Index fall by

16% also in the last month. This is due to the

‘Irrational’ sell-offs in the Pharmaceuticals

sector in the recent weeks. 2015 had been a

good year for Pharmaceuticals & Biotechnology

stocks as they outperformed the S&P 500 yet

again by a healthy margin.

GlaxoSmithKline and Qualcomm are in

currently in negotiation to set up a joint venture

potentially worth up to $1bn to develop medical

technology. This is one of the latest examples

of mergers between the healthcare and

technology industry, and we may very well see

more of this type of convergence happening.

After months of unhappiness and resentment

against the high drug prices, the

Pharmaceuticals & Biotechnology sector met

up in San Francisco at the annual JPMorgan

Healthcare Conference to hopefully start off the

New Year on a positive note.

The sentiment is that the recent Pharmaceutical

sell off would pose a threat to the IPO market.

Shire PLC has started off the year by

announcing its long awaited $32bn takeover of

US-based Baxalta, but investors have shown

signs of loss of confidence in mega deals as the

proposed deal pushed down the shares in both

companies subsequently. Another large-cap

biotech company, Celgene has also trimmed its

profit forecast and is predicting that the

revenues this year would be below analyst

expectations.

Industry executives are on the defence as they

argue that investors are not seeing the bigger

picture as biopharma companies are

discovering more drugs than they have in

years, such as cancer immunotherapies, a

breakthrough towards countering tumours

which have been untreatable till date.

In other news, the NHS has recently approved

a £5,700-a-month skin cancer drug called

Opdivo as it is marketed by its Manufacturer

Bristol-Myers Squibb. Opdivo is the second of

an important new class of cancer drugs to be

recommended by the National Institute of

Health and Care Excellence in the past four

months. This has triggered a 3.12% rise in the

price of Bristol-Myers Squibb Co, and is likely to

continue this trend and to outperform the

market.

It is rare to see one single industry group remain

the market leader in performance for more than

year or two but the Pharmaceutical &

Biotechnology stocks have done just that since

2011 until last year in 2015 when it started to

show signs of reversion. 2016 will be a much

more challenging year for this sector, and we

would have to closely observe the different

headwinds of the economy to make a better

assessment of the year’s forecast.

Samuel Tan

NASDAQ Biotechnology Index (NBI) Credits: Yahoo Finance

NEFS Market Wrap-Up

22

COMMODITIES

Energy

Over the past weeks, there have been major

changes in energy markets. Weakening

economic indicators in China caused a fairly

major stock market sell off, which caused the

demand for energy to diminish markedly.

Notably, Brent crude hit its lowest price in 12

years, trading briefly at $27 a barrel last week.

Since then, the prices of Brent crude and West

Texas Intermediate have made sharp rises.

This was in part due to minor rises in global

stocks. However, the bounce back can mainly

be attributed to the announcement that the

Russian energy minister will hold talks with

OPEC with regard to a potential oil supply cut.

The initial reaction was for Brent crude oil

futures to shoot up by around 7%. Currently it is

thought that a 5% cut in production is what is on

the table, although it is still highly improbable

that any action will actually be taken from these

talks. Talks could be unfruitful given that Saudi

Arabia, the largest producer in OPEC,

maintains the view that Russia would be unable

to cut production. The significance of these

talks has been further downplayed by Rosneft

(Russia’s largest state-controlled oil producer).

A spokesperson from the group claimed that

nothing had changed that would increase the

likelihood of oil production cut.

In the light of these recent developments

surrounding the oil market the World Bank has

slashed its estimates of the average oil price

during 2016. The previous forecast, from just 3

months ago, is down from $52 per barrel to $37

– an almost 25% drop from the average 2015

price. It cited the main factor in the decision was

the unexpectedly aggressive slowdown in the

Chinese economy, which has been shown to

have substantial effects on commodity prices in

general. The bank also stated that the recent oil

drop in the early part of 2016 has had little to do

with fundamentals, and was therefore part of an

irrational market sell off. Furthermore they

predict a steady price rise throughout 2016.

William Norcliffe-Brown

Brent Crude 4 Hour Candlestick (Source:

Oanda)

Week Ending 31st January 2016

23

Precious Metals

Gold entered 2016 with a significant

appreciation over the last 12 weeks from

around 1066.60 USD/oz to around 1114.30

USD/oz. A number of factors which played the

key role in determining the price in the first week

of January, 2016, as illustrated in the first figure

below. One of the key drivers identified was

lower oil prices combined with strengthened US

dollar. The metal is regaining a stronger

position since a sharp fall in October, 2015,

when the Fed Statement had a negative effect

on investments.

According to Thomson Reuters GFMS, as long

as the prices stabilise or, preferably, recover

further, Gold should expect a greater investor

interest in Asian markets. Furthermore, GFMS

forecasts a steady gradual increase in the

metal’s price in the second half of 2016 by up to

5%. This prediction is mainly being brought on

by the shrinking supply from the mining industry

and, again, reinforced by the increasing

demand from Asia.

On the other hand, there are concerns of

equities markets falling, weakening Gold’s

position in the market. There also are worries

that a similar trend to the one in 2008 could

arise. A significant fall in the metal’s position

resulted in the early 2008 as a combined

outcome of a sharp decline in energy prices, a

shift in higher real interest rates and partly due

to the credit crisis.

This year Silver seemed to be slowly regaining

its position in the market up to 26th January,

2016, while still lagging behind Gold. Whilst

industrial demand is slowing, increasing

interest from investors could force the price up

and change the current depreciation. The

amount of Silver sold increased by 61%

between 2009 and 2015. As prices remain

steadily decreasing (as shown in the second

figure), a lower level production is to be

expected due to the declining profitability of the

metal. In turn, a lower supply may shift prices

back up to a new stable equilibrium to meet the

demand. However, this week, the price slowly

dropped between 26th and 28th January from

14.564 to 14.255 USD/t oz.

Platinum supply was lower in 2015. However,

the demand followed a similar trend. According

to Johnson Matthey, although both indicators

are moving in the same direction, it is still

surprising to observe a lack of response with

respect to the price level. 2016 projects an

expansion of the metal’s supply because of the

increasing scale of “recycling”, while demand is

also expected to rise. Overall, P. Duncan, JM

General Manager, expects a net deficit to result

in the coming months.

Goda Paulauskaite

Silver prices (2012-2016)

NEFS Market Wrap-Up

24

Agriculturals

During the preceding Christmas holiday period,

Agricultural Commodities exhibited a number of

fluctuations in a number of different markets,

driven in no small part by concerns over

Chinese demand and weakness in emerging

markets.

Wheat, for example, as measured by the

Chicago board of trade index, fell over 2% over

Russian plans to eliminate a proposed tax on

wheat exports. The tax was originally intended

to mitigate rising food prices within Russia

through incentivising domestic producers in

turn to supply a domestic market, increasing

supply and lowering price within Russia. Had

the tax have been implemented, global supply

would be lowered, increasing prices and

allowing wheat to continue its quintuple session

rise. In contrast, however, the tax has now been

deemed unlikely to be implemented, with First

Deputy Agriculture Minister Evgenii Gromyko

stating that his ministry were proposing either

lowering, or more drastically, completely

eliminating an export tax on wheat. In the

simple but accurate words of US Commodities

Analyst Jason Roose, “if they reduce the tax,

that simply means more wheat in the world”. In

other words, increased supply, which will in turn

lower global wheat prices, as exhibited by the

aforementioned price correction on the Chicago

exchange.

Elsewhere in the expansive field of agricultural

commodities, we have seen other fluctuations

in price, due to a plethora of factors, including,

but not limited to, technical factors. For

example, expectations of unusually high South

American soybean crops have caused a bullish

market reaction from traders, with market rallies

expected to be limited as a result. "When we dip

into some support areas, we'll see that buying

from time to time, but I don't really look for this

buying interest to be maintained or sustained

unless weather in South America is very dry in

the long term," said Brian Hoops, analyst at

Midwest Market Solutions.

Whilst there were other movements in similar

markets, such as corn futures in particular,

wheat and soybeans exhibited the most notable

changes in the preceding period. Agricultural

commodities remains an interesting sector to

cover, with inevitable macro-economic

fluctuations driven by Chinese economic

concerns undoubtedly affecting prices across a

range of commodities.

Jack Blake

Week Ending 31st January 2016

25

CURRENCIES

Major Currencies

On Wednesday, the 28th January 2016, Janet

Yellen declared that the Fed probably won’t

increase the interest rate in March, which is not

surprising considering the low inflation rate.

Many economists already expected anyway

that the next rise of the interest rates will follow

not earlier than June. With the lifting of the

interest rate to approximately 0.25% in

December, the Fed finally ended the era of

cheap money in the United States. Yellen now

wants to follow a policy of slow but steady return

to 2% on the medium-term and between 3 and

4% on the long-term. However, the expected

inflation rate stays unchanged at a low level,

too. On the other hand the labour market in the

US is improving which was pivotal for the last

uprating for the times being. To be able to

further raise the interest rate higher inflation

would be necessary as a strong Dollar actually

hurts the US-industry.

The inflation rate in the Eurozone on the other

hand raised from 0.2% in December to 0.4% in

January which is its highest level since October

2014. However, as M3 money supply

decreased to 4.7% in December 2015, from 5%

in November and M1 money supply decreased

from 11.1% to 10.7% during the same period,

many experts doubt that the expansive

monetary policy of the ECB is actually working.

Additionally, the perpetually low oil prices

continue to force the inflation rate down, as well.

Furthermore, president of the ECB, Mario

Draghi pledged unexpectedly to review the

ECB stimulus programme in March this year.

After a relatively stable performance of the Euro

on the exchange market last week, Draghi’s

statement led to higher volatility at the end of

this week. After it showed a positive trend at the

beginning of the week – the EUR/USD

appreciated on Thursday to 1.091, but

devalued again to 1,083 during Friday’s trading.

However, zero interest policy in Europe

remains unchanged favourable which is why

the Euro will predictably depreciate again

against the dollar throughout 2016 if the Fed

follows its “return-to-normal” strategy. As there

is a large gap between the target inflation of

nearly under 2% and the actual inflation rate,

the ECB surely will follow policies to approach

this goal. Therefore, the weaker Euro will exert

upward pressure on inflation in 2016.

Accordingly, predictions by the ECB assume

the inflation rate will rise to 0.7% in 2016.

Alexander Baxmann

NEFS Market Wrap-Up

26

The Research Division was formed in early 2011 and is a part of the Nottingham Economics and Finance Society (NEFS, formerly known as NFS and UNIS). It consists of teams of analysts closely monitoring particular markets and providing insights into their developments, digested in our NEFS Weekly Market Wrap-Up. The goal of the division is both the development of the analysts’ writing skills and market knowledge, as well as providing NEFS members with quality analysis, keeping them up to date with the most important financial news. We would appreciate any feedback you may have as we strive to grow the quality and usefulness of weekly market wrap-ups.

For any queries, please contact Josh Martin at [email protected]. Sincerely Yours, Josh Martin, Director of the Nottingham Economics & Finance Society Research Division

This Publication has been prepared solely for informational purposes, and is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, product,

service or investment. The opinions expressed in this Publication do not constitute investment advice and independent advice should be sought where appropriate.

Whilst reasonable effort has been made to ensure the accuracy of the information contained in this Publication, this cannot be guaranteed and neither NEFS nor any

other related entity shall have any liability to any person or entity which relies on the information contained in this Publication, including incidental or consequential

damages arising from errors or omissions. Any such reliance is solely at the user’s risk.

As featured on:

Sponsors: Platinum: Gold:

About the Research Division The Research Division was formed in early 2011 and is a part of the Nottingham Economics and Finance Society (NEFS, formerly known as NFS and UNIS). It consists of teams of analysts closely monitoring particular markets and providing insights into their developments, digested in our NEFS Weekly Market Wrap-Up. The goal of the division is both the development of the analysts’ writing skills and market knowledge, as well as providing NEFS members with quality analysis, keeping them up to date with the most important financial news. We would appreciate any feedback you may have as we strive to grow the quality and usefulness of weekly market wrap-ups. For any queries, please contact Jack Millar at [email protected] Sincerely Yours, Jack Millar, Director of the Nottingham Economics & Finance Society Research Division